private equity co-investment considerations and structures

TRANSCRIPT

Private Equity Co-Investment Considerations and Structures

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

TUESDAY, JANUARY 5, 2021

Presenting a live 90-minute webinar with interactive Q&A

Arash Farhadieh, Partner, Willkie Farr & Gallagher, New York

Laura Friedrich, Partner, Willkie Farr & Gallagher, New York

John M. Knapke, Partner, Willkie Farr & Gallagher, New York

Mark Proctor, Partner, Willkie Farr & Gallagher, New York

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-877-447-0294 and enter your Conference ID and PIN when prompted.

Otherwise, please send us a chat or e-mail [email protected] immediately

so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the ‘Full Screen’ symbol located on the bottom

right of the slides. To exit full screen, press the Esc button.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 2.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the link to the PDF of the slides for today’s program, which is located

to the right of the slides, just above the Q&A box.

• The PDF will open a separate tab/window. Print the slides by clicking on the

printer icon.

FOR LIVE EVENT ONLY

Copyright © 2020 by Willkie Farr & Gallagher LLP. All Rights Reserved. These materials may not be reproduced or disseminate d in any form without the express permission of Willkie Farr & Gallagher LLP.

Private Equity Co-Investment

Considerations and StructuresLaura Friedrich | Mark Proctor | Arash Farhadieh | John Knapke

January 5, 2021

Arash FarhadiehPartner

New York

Laura FriedrichPartner

New York

Mark ProctorPartner

New York

2

John KnapkePartner

New York

Speakers

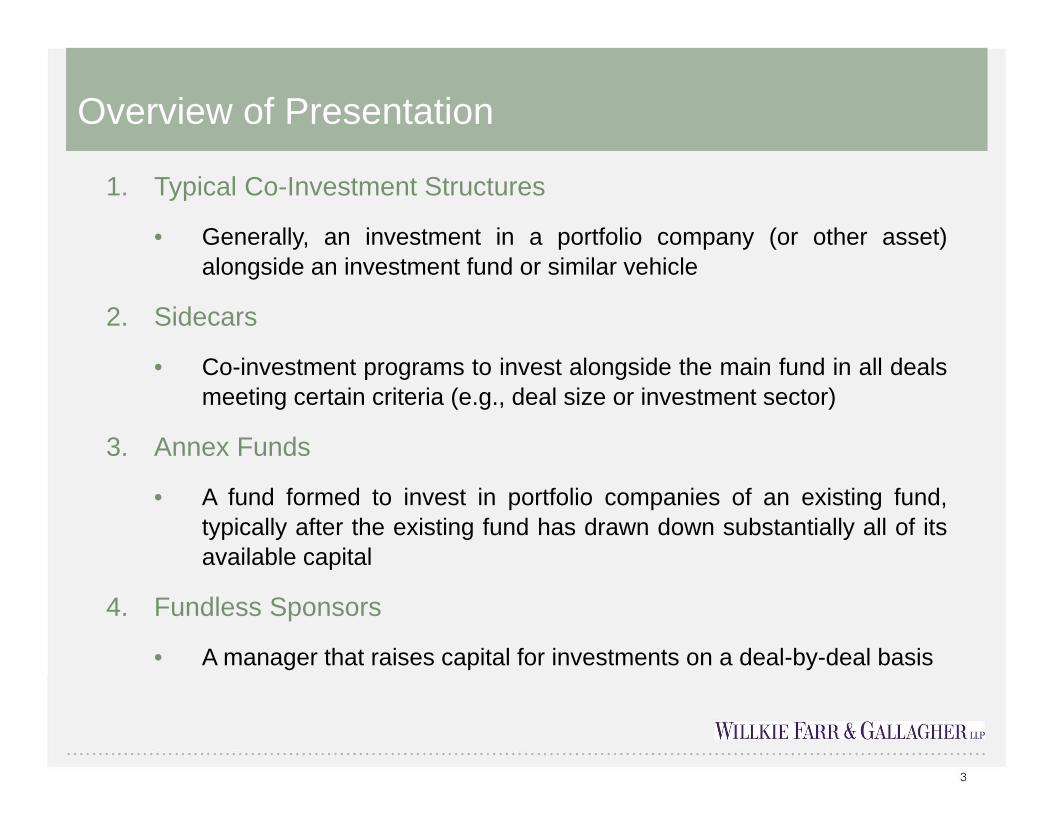

1. Typical Co-Investment Structures

• Generally, an investment in a portfolio company (or other asset)

alongside an investment fund or similar vehicle

2. Sidecars

• Co-investment programs to invest alongside the main fund in all deals

meeting certain criteria (e.g., deal size or investment sector)

3. Annex Funds

• A fund formed to invest in portfolio companies of an existing fund,

typically after the existing fund has drawn down substantially all of its

available capital

4. Fundless Sponsors

• A manager that raises capital for investments on a deal-by-deal basis

Overview of Presentation

3

• Sponsor Perspective

o A co-investment can serve to fill a capital need – to address concentration

limits, for a larger-sized deal or to improve diversification of a fund’s portfolio

o Offering co-investments can enhance fundraising for a commingled fund

• Investor Perspective

o Co-investment opportunities offer the ability to gain additional access to desired

investments

o Co-investing alongside a sponsor provides a path to a direct-investment

program

o Co-investment fees are typically lower than fees for a commingled fund

Overview – Why Offer Co-Investments?

5

Commingled

Fund

Co-Investment

Vehicle

Portfolio

Companies

A, B, C …

Portfolio

Company

D

LP

LP

LP

Direct Co-Investors

LPsGP GP LPs

Overview – Typical Co-Investment Structure

6

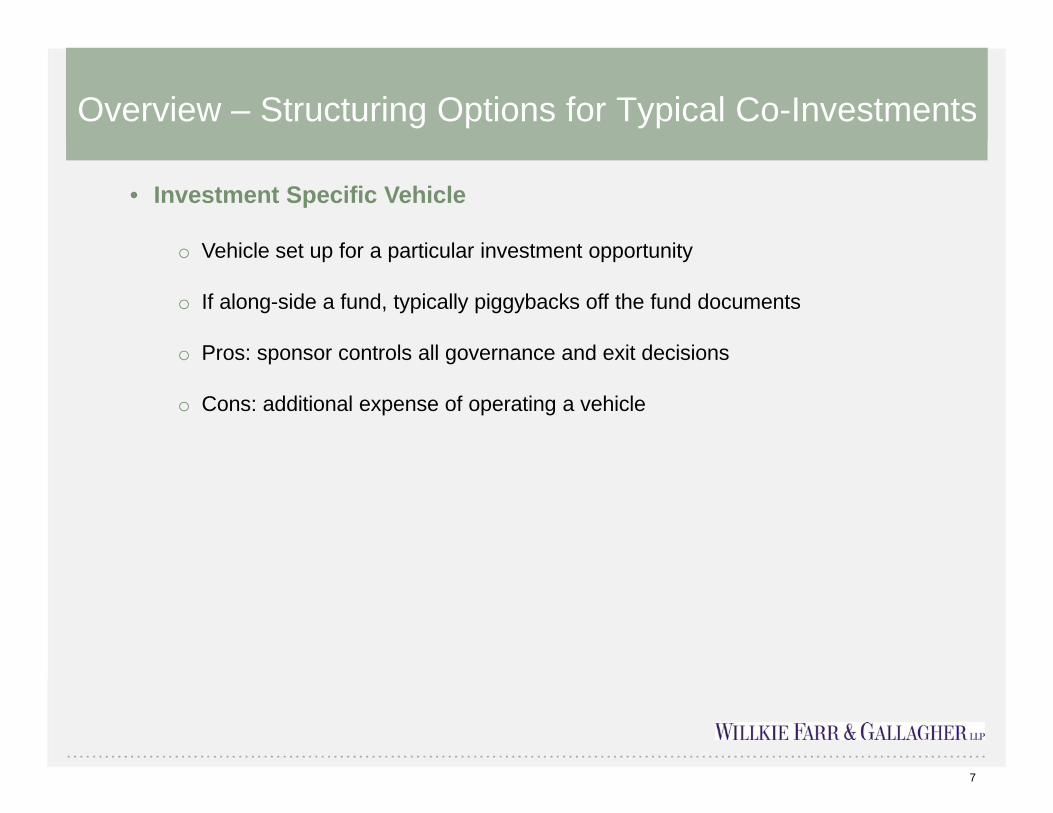

• Investment Specific Vehicle

o Vehicle set up for a particular investment opportunity

o If along-side a fund, typically piggybacks off the fund documents

o Pros: sponsor controls all governance and exit decisions

o Cons: additional expense of operating a vehicle

Overview – Structuring Options for Typical Co-Investments

7

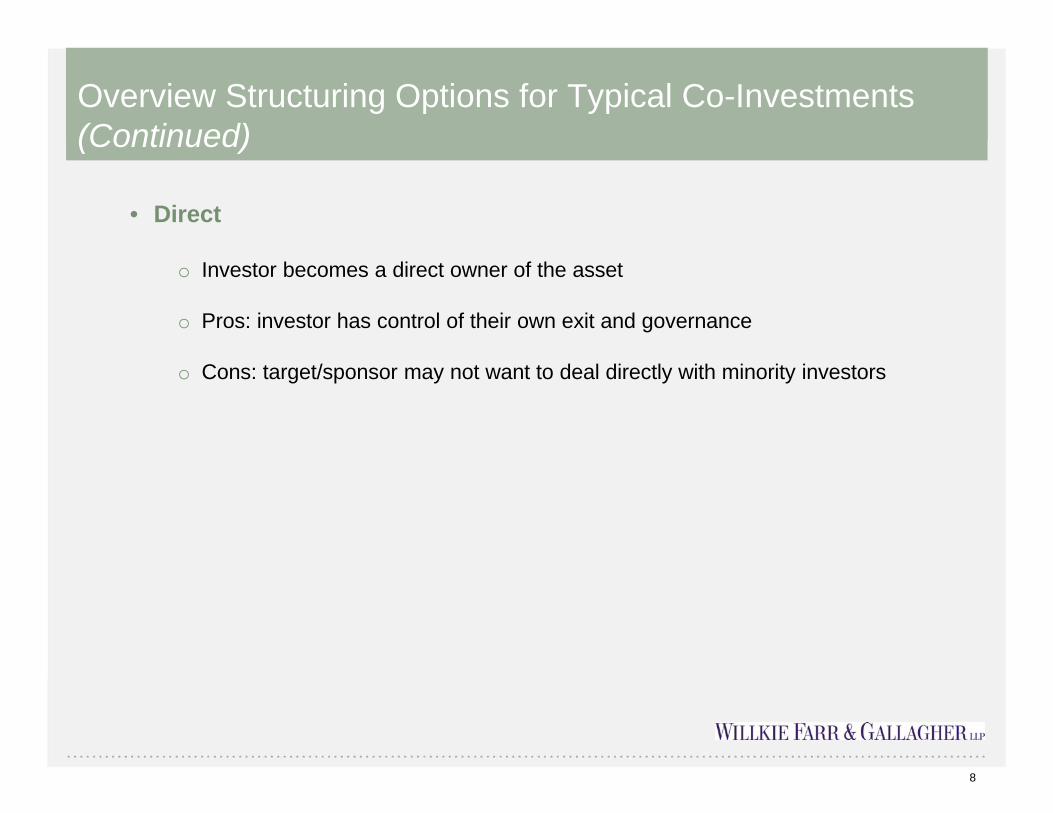

• Direct

o Investor becomes a direct owner of the asset

o Pros: investor has control of their own exit and governance

o Cons: target/sponsor may not want to deal directly with minority investors

Overview Structuring Options for Typical Co-Investments

(Continued)

8

• Additional Structures

o Within the existing fund (never actually seen it in practice, but have seen

plumbing for it in Fund LPAs)

o SMA/Fund of One

Overview Structuring Options for Typical Co-Investments

(Continued)

9

• Existing LPs vs. Strategic Co-investors

• Pro rata vs. priorityo Managing side letter obligations

• Timing and commitment processo Offering materials (PPM vs. marketing deck with risk/conflict disclosure)

o Equity Commitment Letter

o LPA (often marked against commingled fund)

o Subscription agreement vs. bringdown letter

o Can take as long as a full fundraise and be just as expensive

Offering Typical Co-Investments

10

• Management Fees/Carryo Market is all over the place (depends on the circumstances of the deal)

o Some are fee-free (especially if linked to a commingled fund; achieves a

blended fee rate)

o Sometimes just reimbursement of expenses and a back-end carry

o Sometimes just an up-front transaction fee and no management fee

o Clawbacks are less common

• Expenseso In the commitment or outside?

o Can be paid through recycling/current income

o Can be paid at the back-end out of distributions

o More often capped/budgeted as compared to commingled funds

• Broken Deal Expenseso Who pays?

o Significant disclosure issues for a linked commingled fund

Co-Investment Terms

11

• Follow-On Investmentso Better to have it committed (much more complicated in terms of dilution, share

classes, etc. if it is discretionary)

o Can reserve part of an initial commitment for follow-ons

o Preemptive rights

• Governanceo Removal, termination (usually at higher percentages or not permitted at all;

often linked to a commingled fund)

o LPAC - approve principal trades (who is on it? Often shared with a commingled

fund)

o Key Person rights are less common

o Veto Rights

• Side Letters

• Exitso Drags, tags

o What if an investor wants a longer hold?

Co-Investment Terms (Continued)

12

• Allocation of co-investments

o Adequate disclosure

o Fiduciary duties

o Complying with operating agreements/side letters

• Do you need an audit? Custody rule considerations

• Do you legally need a PPM? FINRA considerations; for CaymanIslands, private funds may all need PPMs now

• Co-investment sponsor is still an investment adviser; disclosure onForm ADV

Regulatory Considerations

13

• Sponsor Perspective

o Sidecars (sometimes referred to as overage or overflow funds), are programmatic co-investment vehicles

organized by a sponsor to invest alongside the sponsor’s main fund in each opportunity meeting certain specified

criteria (e.g., deals larger than a certain size or deals in specific sectors)

o These structures provide the sponsor with flexibility to pursue and consummate deals that might otherwise be too

large for the main fund (e.g., due to investment concentration restrictions in the main fund documents, or which

would cause the main fund to be over-exposed to a particular investment/sector) without having to resort to

leverage or syndication of investments to third parties

o In contrast to co-investment structures formed on an investment-by-investment basis as the need arises,

Sidecars provide the sponsor with a ready pool of capital that is available for deployment without the need for ad

hoc fundraising as and when specific opportunities arise, reducing the amount of time that might otherwise be

required to secure co-investment capital and providing greater certainty that capital will be available to

consummate a deal

o Investors in a Sidecar will not typically have the enhanced information or governance rights that are often

requested in the deal-by-deal co-investment context, and the sponsor can retain a greater deal of control over

the Sidecar’s investments than it would in the context of a deal-specific co-investment

o Sidecars allow a sponsor to charge fees and carry, albeit typically at reduced rates relative to the main fund

o The governing documents and commercial terms of Sidecars will typically be based on those of the main fund,

making them relatively easy to administer

Overview – Why Consider Sidecars?

15

• Investor Perspective

o Investing in Sidecars allows investors to gain additional exposure to a sponsor’s deals which they may not be

able to achieve by way of an investment in the sponsor’s main fund (e.g., where the main fund is oversubscribed)

o When investing in a Sidecar, an investor only has to diligence one set of documents, and does so upfront,

reducing the amount of time and effort that an investor must spend evaluating co-investment opportunities

o In addition, investments in a Sidecar often require less ongoing monitoring from an investor than traditional deal-

by-deal co-investments

o Because investments in Sidecars are typically subject to reduced fees and carry, by investing in a Sidecar an

investor can reduce the effective rate of the fees and carry they pay to a particular sponsor, thus improving their

overall net returns from that sponsor

o By that same token, investors in a Sidecar will typically have fewer information and governance rights than they

would in the context of a deal-specific co-investment

o The deployment of capital committed to a Sidecar depends on the opportunities sourced by the sponsor,

resulting in the risk that a Sidecar may not ultimately invest the capital committed by investors, leaving investors

paying organizational and ongoing expenses for a vehicle that makes fewer investments than anticipated

o Investments in Sidecars will typically be more concentrated than an investment in the main fund, and there are

conflicts of interest that may arise in connection with the investment activities of a Sidecar

Overview – Why Consider Sidecars?

16

• Fees and carry – Typically charged at a reduced rate relative to the main fund; fees may be based on invested

capital

• Allocation of investments – The main fund will have first priority

o In some arrangements, the main fund will take 100% of the opportunity until the sponsor determines that the

main fund has received an appropriate amount, with the Sidecar receiving the remainder; in other

arrangements, the main fund and Sidecar documents may prescribe a particular allocation methodology (e.g.,

with the main fund receiving priority up to a certain threshold, with any remaining amounts shared between

the main fund and the Sidecar until the main fund reaches its maximum concentration limit)

o Many Sidecar arrangements will provide considerable discretion to the GP to vary from the stated allocation

methodology (and, in some situations, bypass the overage fund and offer excess allocation opportunities to

third party co-investors) in appropriate circumstances

• Investments and dispositions – Typically made pari passu with the main fund in the same type and combination of

securities, at substantially the same time and on substantially the same terms as the main fund invests and disposes

of investments (subject to legal, regulatory and tax considerations)

• Investment period and term – Typically tied to the investment period and term of the main fund

• GP Removal and fund termination – Typically will occur automatically upon the removal of the main fund’s GP or

termination of the main fund

• Consent matters – Typically rely on the LPAC of the main fund to clear conflicts, though will often provide the

flexibility to form a separate LPAC for the Sidecar to address any conflicts on which the interests of the main fund and

the Sidecar diverge

Common Sidecar Terms

17

• Conflicts are inherent in any co-investment arrangement, including Sidecars, and

the conflicts may be more acute in situations where some of the Sidecar investors

are not also investors in the main fund

o In particular, conflicts are likely to arise in the allocation between the main fund and the

Sidecar of investment opportunities, common expenses, fees received from portfolio

companies and the sponsor’s time and attention

• Conflicts can be mitigated by including prescriptive language in the governing

documents of each of the main fund and the Sidecar providing how conflicts will be

resolved

o The less prescriptive the language in the documents (i.e., the more discretion granted to

the sponsor), the greater the potential for conflicts that are not clearly addressed

o In situations where conflicts arise that are not addressed in the fund documents, sponsors

may need to seek investor or LPAC consent to the sponsor’s proposed resolution of those

conflicts

• Conflicts should be clearly disclosed to investors in each of the main fund and the

Sidecar in their respective offering documents

Sidecars – Addressing Conflicts

18

• An Annex Fund is a fund formed to invest in portfolio companies of an

existing fund, typically after the existing fund has drawn down or reserved

for investments and expenses substantially all of its available capital and it

does not expect any recyclable proceeds in the near future

• Historically Annex Funds have been raised to support an existing fund’s

portfolio companies that may be experiencing difficulties typically due to

macroeconomic, or sector, developments

o For example, during the global financial crises, and more recently the energy

sector dislocation, a number of Annex Funds were raised

• More recently, a variation of the traditional Annex Fund has become more

prevalent, specifically to support the portfolio companies of growth equity

funds where the existing funds are performing well and the nature of the

underlying companies is such that additional growth capital is needed

(either to help the portfolio companies develop or to fund strategic

acquisitions) in order to fully realize the potential for the portfolio

What is an Annex Fund?

20

The term Annex Fund is sometimes used interchangeably with a Top-Up

Fund or a Build-Up Fund – while in some circumstances those terms are

appropriate in other circumstances the latter refer to co-investment/overage

funds discussed earlier

Depending on the specific needs of an existing fund’s portfolio companies,

their maturity and return profile, aside from an Annex Fund, GPs may

consider alternatives to Annex Funds, including the following:

• GP-led secondaries and continuation funds:o GPs looking for a long-term liquidity solution can sponsor a new fund, known

as a “Continuation Fund,” that would acquire and continue to hold interests in

one or more pre-identified portfolio companies held by the existing fund

o The success of a Continuation Fund will depend on the nature of the

underlying portfolio companies, their economic prospects and needs and

maturity of the overall portfolio – in many circumstances, a Continuation Fund

is a not a feasible option

Alternatives to Annex Funds

21

• Preferred equity lineso GPs can offer additional interests in the existing fund, which may either be

offered as the same class of interests held by existing investors in the fund

(i.e., “pari passu interests”) or as preferred securities, which pay a fixed

amount to new investors in priority to the fund’s existing waterfall

o An offering of pari passu interests requires the GP to address a number of

issues and conflicts of interest such as the valuation of the underlying portfolio

in order to establish the subscription price for the offered interests and dilution

of interests of the existing investors

Because of these issues, it is preferable in many instances for the fund to

issue preferred interests

o Given the complexity and financial impact both on existing LPs and the GPs’

potential carry, GPs need to carefully weigh the benefits and costs associated

with this alternative

Alternatives to Annex Funds (Continued)

22

• NAV or Asset-backed facilitieso A NAV facility is a credit facility that is non-recourse to the Fund and secured

by pledging the Fund’s interests in all or some of its portfolio companies, and

the proceeds from the NAV facility will be used to provide additional capital to

its portfolio companies

This type of a facility works exceptionally well where the underlying

portfolio companies are performing and producing cash flows

o The Fund’s governing agreements should be carefully reviewed to ensure that

entering into such NAV facility is permitted and is consistent with its terms,

relating to, among other things, recycling, borrowings, and follow-on

investment limitations

Separately, the governing documents of each portfolio company must be

reviewed to ensure that the Fund is permitted to implement the pledge

• Given the complexity involved in organizing an Annex Fund, GPs will often weigh

alternative options and will make a determination based on the performance and

needs of the portfolio companies and feedback from LPs

Alternatives to Annex Funds (Continued)

23

Existing Fund

Portfolio

Existing Fund’sLPsLPs New

LPs

Add‐on Investments in debt or equity

Annex Fund

Typical Annex Fund Structure

24

• Key considerations for GPs include:

o Conflicts of Interest

GP’s entitlement to management fee and carried interest in the Annex

Fund

GP’s commitment to the Annex Fund

Purchase price determination in respect of Annex Fund’s investment in the

existing fund’s portfolio companies

Annex Fund interest offered to current investors in the existing fund pro

rata based on their relative commitments vs. offering to any new third

party investors

Allocation of the investment opportunities between the Annex Fund and

the existing fund (where recyclable capital becomes available)

Annex Funds: Key Considerations for Private Equity GPs

25

• Key considerations for GPs include:

o Terms of the Governing Agreement of the existing fund and Regulatory

Matters

The governing agreement of the existing fund should be reviewed to

assess the restrictions and required consents and/or amendments

To ensure compliance with the requirements of the Advisers Act (as well

as from an investor relations perspective) GPs should proactively engage

their existing LPs and LPACs, and put in place robust disclosures and

mechanics to appropriately address LP/LPAC concerns

o Economic Terms of the Annex Fund offering

GP’s economics attributable to an Annex Fund will depend in part on the

reasons for its formation, e.g., where the Annex Fund has been formed

because of underperformance of the existing portfolio, LPs may require no

fee or carry or a tiered fee or carry

Annex Funds: Key Considerations for Private Equity GPs (Continued)

26

• Key considerations for existing fund LPs include:

o Whether third party investors will be able to participate in the Annex Fund or if it

will only be offered to the existing fund’s LPs

o Will the Annex Fund participate in all follow-on investment opportunities or a

select identified group of the portfolio companies? If all portfolio companies,

how will investment opportunities be allocated if the existing fund has available

capital (e.g., due to recycling)?

o Purchase price mechanic in respect of Annex Fund’s investment in the existing

fund’s portfolio companies – e.g., will the GP obtain independent valuation or

fairness opinions? Is there a distinction between primary and secondary

investments?

o GP’s entitlement to management fee and carried interest in the Annex Fund – if

the existing fund is not performing, LPs may require that the carry be

aggregated across the funds or impose a tiered waterfall

o GP’s commitment to the Annex Fund

Annex Funds: Key Considerations for existing fund LPs

27

• Annex Fund Formation:

o Full suite of typical fundraising documents should be prepared, with particular

focus on ensuring that the offering documents include full disclosure of conflicts

of interest, in particular if third party investors will participate in the Annex Fund

o Detailed disclosure of the performance of the existing fund’s portfolio

companies should be included in the offering documents as well as any

material expected developments in respect of the portfolio

o LPs/LPAC of the existing funds should be consulted in a transparent manner,

including in respect of potential changes in the existing fund’s portfolio, for

example, if a portfolio company receives a meaningful offer or LOI

Annex Fund Fundraising

28

• In circumstances where the Annex Fund is being formed to provide

follow-on capital to distressed assets (e.g., during a financial crisis),

the LPs will likely be more proactive and will expect steeper discounts

in fees and carry

• For a distressed portfolio, LPs will also be more likely to identify the

specific group of investments they want the Annex Fund to participate

in and may demand fairness opinions

Investor Reactions to Annex Funds

29

• A fundless sponsor is a manager that raises capital for

investments on a deal-by-deal basis

• There is no blind pool – the manager must shop each

individual deal to limited partners

What is a Fundless Sponsor?

31

• Useful for teams who are looking to raise capital without a

track record, or who have had prior track record issues

Why Adopt a Fundless Sponsor Model?

32

Pros: • Can raise capital relatively quickly and inexpensively (single-asset fund can be

raised in 4-8 weeks, as opposed to 2 years)

• Investments not cross-collateraized – GP earns carry on each successful deal

at the time of realization (or full LP payout), without having to worry about

clawbacks

• GP does not need to spend as much time/resources on fund management

aspect

• Few allocation issues

Cons:• Need to raise capital and execute deals at the same time – this requires

twice the energy

• Targets / sellers prefer a counterparty with capital at the ready – may lose

out in competitive processes without capital lined up

• Manager usually pays all broken deal expenses

• No committed capital means smaller fee base

What are the Pros and Cons of the Fundless Sponsor Model?

33

• 1-2% management fee

• 10-20% carried interest, sometimes with escalation provision

• Term of 5, 7 or 10 years (10 is considered long)

• No investment period – all capital contributed at closing

• Expenses and management fees are often outside of commitment

o Operating expenses may be subject to a cap

GP may seek to exclude indemnification expenses from this cap

o Expenses may be paid by portfolio company directly

o Management fee may be paid out of cash flow or capital contributions

• Each investment vehicle has follow-on rights

• LP giveback – GP will seek to recall 100% of distributions

• Often no LPAC because investors tend to be individuals and family offices

Market Terms for Fundless Sponsor Model

34

• Conflicts of interest tend to be simpler in fundless sponsor deals, because

each partnership tends to have its own discreet investment

• Unlike co-investment vehicles, do not have fund-related allocation issues, and

do not have issues around which fund gets an allocation of an investment

• Fundless sponsors often want to preserve the optionality to roll their

investments into a fund, or merge multiple investments together into a single

vehicle

o Merger requires consent of LPs in both vehicles

Often build consent provisions into both vehicles’ organizational

documents

o Roll-up requires consent of LPs in vehicle and consent of fund

Build consent provisions into vehicle’s organizational documents

Fund consent obtained in fund organizational documents or by

LPAC

Conflicts of Interest – Fundless Sponsor Deals

35

Investment Adviser Registration• Fundless sponsors need to consider investment adviser registration thresholds

o NY: Exempt reporting adviser registration at $25mm; full registration at

$150mm

o If first vehicle has $150mm or more in assets, registration is required

immediately

o Fundless sponsors often try to keep first vehicle below $150mm – allows them

to delay registration for longer period of time

Fundless Sponsors - Regulatory Considerations

36

Broker-Dealer Issues• Finder’s Fees

o Broker dealer issues often arise in the context of fundless sponsor deals, where relying on a network of

finders, who are not registered as broker dealers

o Paul Anka No Action Letter (1991) – allows for payment of cash finder’s fee under very limited

circumstances

o Outside of bounds of Paul Anka letter, very difficult to compensate finders

o Some investors will set up their own aggregator vehicles to invest in a fundless sponsor vehicle and

charge second level of management fee

• Fees Paid by Portfolio Companies

o Transaction Fees: GP should not take transaction-based compensation from portfolio company unless GP

is a registered broker dealer or there is a full management fee offset – Blackstreet No Action Letter (2016)

GP may be entitled to reasonable compensation for work in connection with diligence/pursuit of

transaction

o Consulting Fees / Monitoring Fees: portfolio companies may pay GP a consulting or monitoring fee on an

ongoing basis, so long as such fee is fully disclosed to limited partners

Any accelerated monitoring fee payments (paid upon early exit of investment) must be fully

disclosed

Fundless Sponsors - Regulatory Considerations

37