private and public equity investing: how do they...

TRANSCRIPT

Private and Public Equity Investing: How do they Diverge?

Michael Miele,

Goldman Sachs Private Equity Group

May 16th 2007

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities. For Caesarea Center Conference use only, not for further distribution to the public.

2

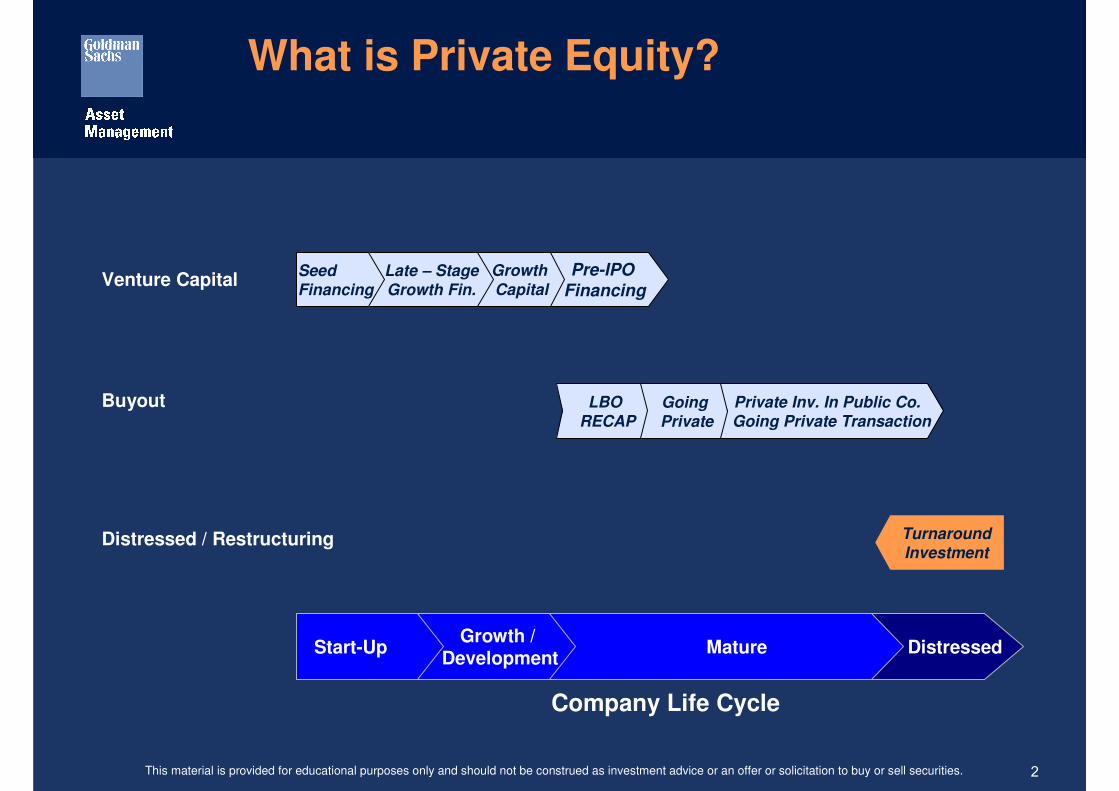

Private Inv. In Public Co.Going Private Transaction

Going Private

What is Private Equity?

Company Life Cycle

DistressedMatureGrowth /

DevelopmentStart-Up

TurnaroundInvestment

Distressed / Restructuring

Buyout LBO RECAP

Pre-IPO

FinancingGrowth Capital

Late – StageGrowth Fin.

Venture CapitalSeedFinancing

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

3

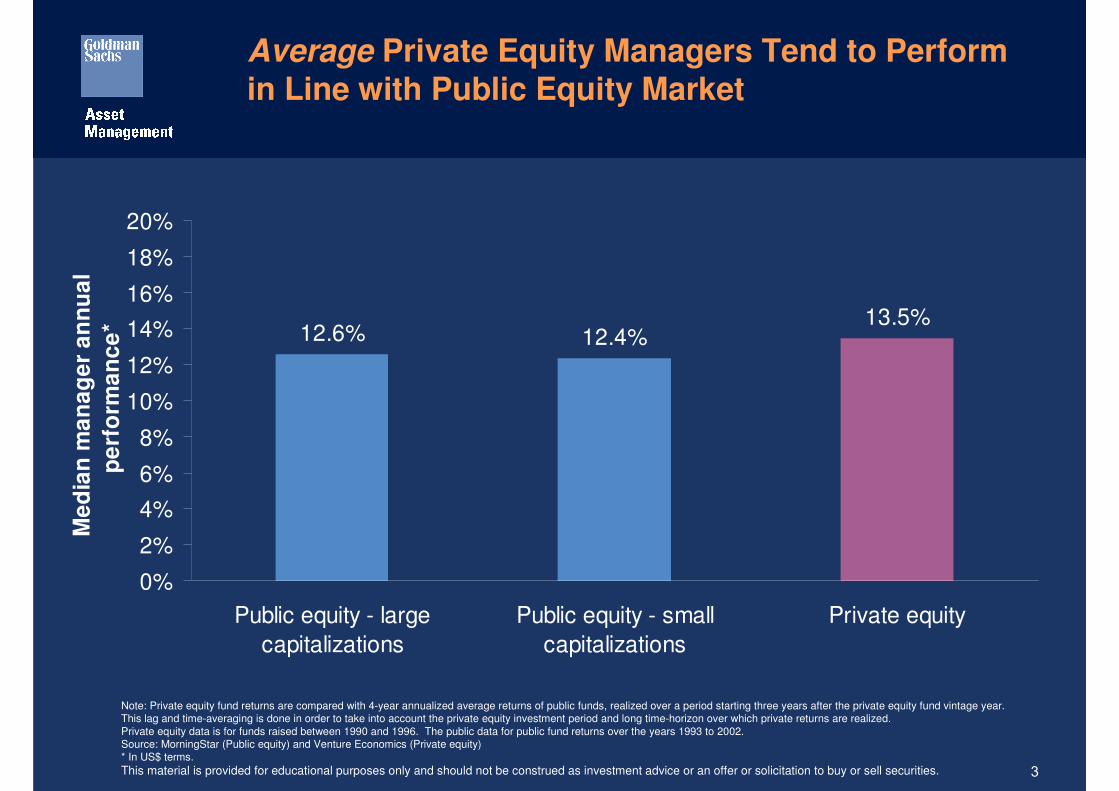

Average Private Equity Managers Tend to Perform in Line with Public Equity Market

Note: Private equity fund returns are compared with 4-year annualized average returns of public funds, realized over a period starting three years after the private equity fund vintage year. This lag and time-averaging is done in order to take into account the private equity investment period and long time-horizon over which private returns are realized. Private equity data is for funds raised between 1990 and 1996. The public data for public fund returns over the years 1993 to 2002. Source: MorningStar (Public equity) and Venture Economics (Private equity)* In US$ terms.

12.6% 12.4%13.5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Public equity - large

capitalizations

Public equity - small

capitalizations

Private equity

Me

dia

n m

an

ag

er

an

nu

al

pe

rfo

rma

nc

e*

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

4

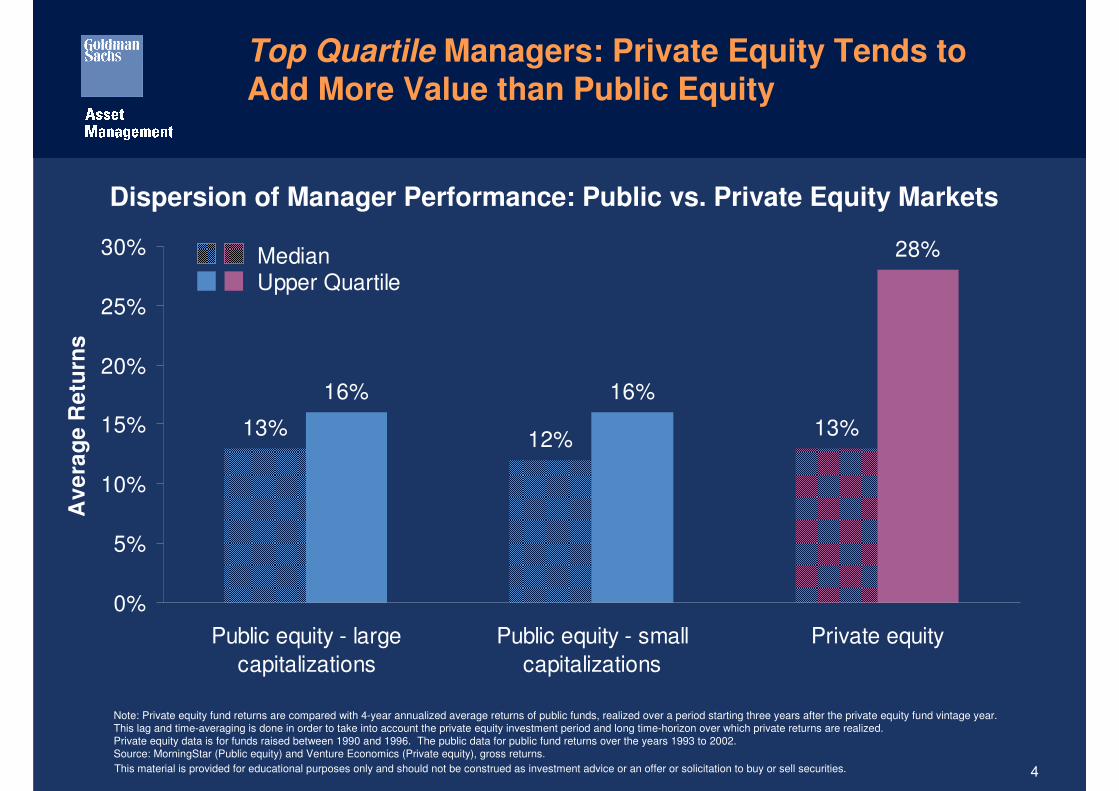

Top Quartile Managers: Private Equity Tends to Add More Value than Public Equity

13%12%

13%

16% 16%

28%

0%

5%

10%

15%

20%

25%

30%

Public equity - large

capitalizations

Public equity - small

capitalizations

Private equity

Av

era

ge

Re

turn

s

Upper QuartileMedian

Dispersion of Manager Performance: Public vs. Private Equity Markets

Note: Private equity fund returns are compared with 4-year annualized average returns of public funds, realized over a period starting three years after the private equity fund vintage year. This lag and time-averaging is done in order to take into account the private equity investment period and long time-horizon over which private returns are realized. Private equity data is for funds raised between 1990 and 1996. The public data for public fund returns over the years 1993 to 2002. Source: MorningStar (Public equity) and Venture Economics (Private equity), gross returns.

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

5

Manager Selection is Critical

The distribution of returns from private equity suggests that:

• Returns are asymmetrically distributed

• Manager selection is rewarded, not asset allocation

• Investing in a private equity index is neither possible, nor desirable

Source: Goldman Sachs Private Equity Group.Past performance is not indicative of future returns, which may vary. This illustration does not represent the performance of any fund or product managed by GSAM or GS & Co.For illustrative purposes only.

Average Return

Equals Index

Public Equity Markets

Average Return

Target Return

Estimated 10 - 20% of

Private Equity

Managers

Private Equity Markets

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

6

Chance

Skill

Company selection

Ability to influence strategy

Financial engineering

Informational advantages

Ability to drive operational improvement

Sourcing

Levers of Value Creation

Private equity managers who take advantage of these sources of returns have potential to offer superior long-term investment performance

relative to public markets.

Private MarketsSources of Value Creation Public Markets

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

7

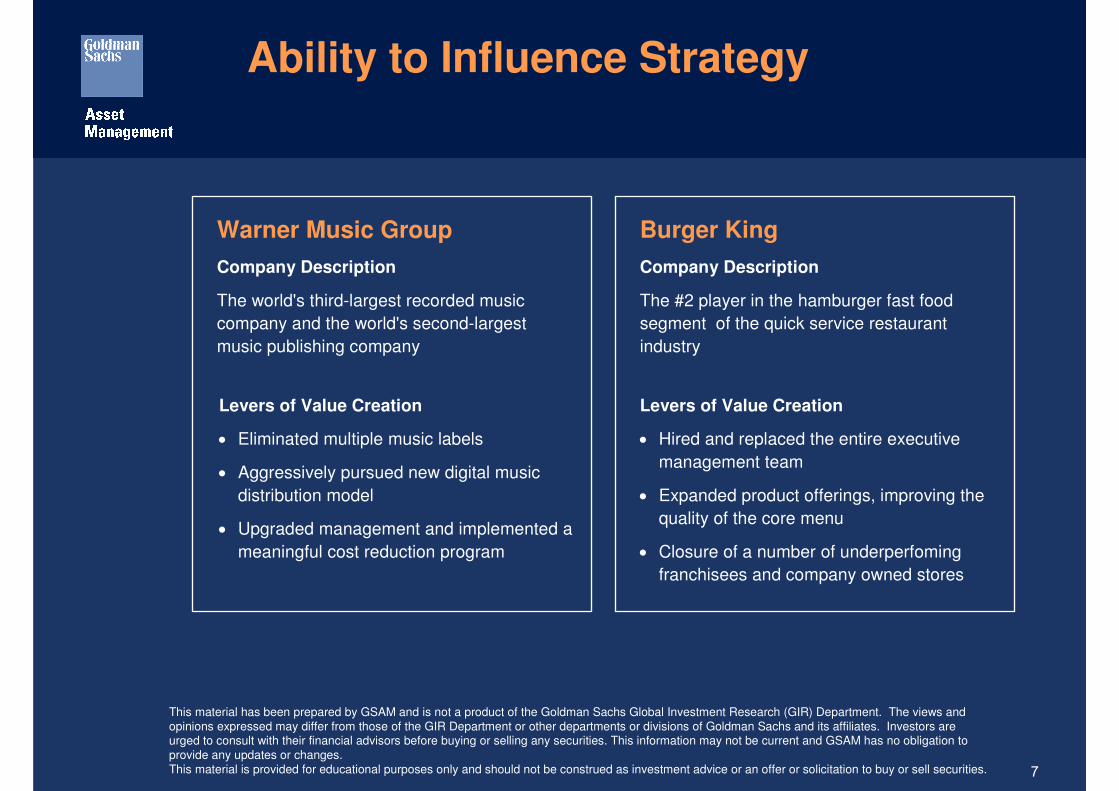

Ability to Influence Strategy

Warner Music Group

Company Description

The world's third-largest recorded music

company and the world's second-largest

music publishing company

Levers of Value Creation

• Hired and replaced the entire executive

management team

• Expanded product offerings, improving the

quality of the core menu

• Closure of a number of underperfoming

franchisees and company owned stores

Levers of Value Creation

• Eliminated multiple music labels

• Aggressively pursued new digital music

distribution model

• Upgraded management and implemented a

meaningful cost reduction program

Burger King

Company Description

The #2 player in the hamburger fast food

segment of the quick service restaurant

industry

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

This material has been prepared by GSAM and is not a product of the Goldman Sachs Global Investment Research (GIR) Department. The views and opinions expressed may differ from those of the GIR Department or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and GSAM has no obligation to provide any updates or changes.

8

Financial Engineering

Texas Genco

Company Description

One of the largest wholesale electric power

generating companies in the U.S.

Seagate Technology

Company Description

Worldwide leader in the design, manufacturing

and marketing of hard disc drives

Levers of Value Creation

• Forward sale of power for multiple years

enabled attractive financing and exit

Levers of Value Creation

• Acquisition of company together with

Veritas in a complex share swap

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

This material has been prepared by GSAM and is not a product of the Goldman Sachs Global Investment Research (GIR) Department. The views and opinions expressed may differ from those of the GIR Department or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and GSAM has no obligation to provide any updates or changes.

9

Informational Advantages

Bare Escentuals

Company Description

Market leader in the fast growing mineral

based cosmetics and skin care category

Levers of Value Creation

• Opportunity not available to public market

investors

• Huron was created in the aftermath of the

Enron/Arthur Andersen scandal

• Grew organically and through acquisition

Huron Consulting

Company Description

Huron provides consulting services to leading

corporate, law firm, and public institution clients

Levers of Value Creation

• Private high growth company unavailable

to public market investors

• Expanded available distribution points by

opening new retail stores, growing

existing wholesale accounts, adding new

wholesale accounts, and growing in

international markets

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

This material has been prepared by GSAM and is not a product of the Goldman Sachs Global Investment Research (GIR) Department. The views and opinions expressed may differ from those of the GIR Department or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and GSAM has no obligation to provide any updates or changes.

10

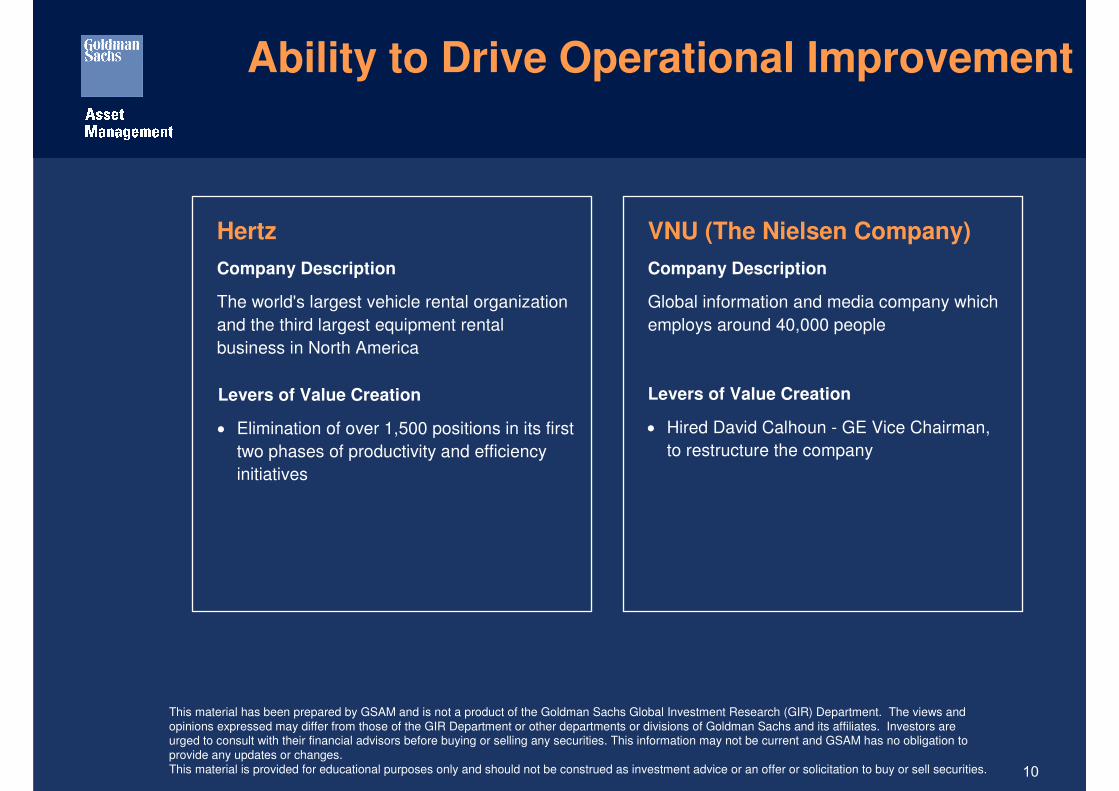

Ability to Drive Operational Improvement

Hertz

Company Description

The world's largest vehicle rental organization

and the third largest equipment rental

business in North America

VNU (The Nielsen Company)

Company Description

Global information and media company which

employs around 40,000 people

Levers of Value Creation

• Elimination of over 1,500 positions in its first

two phases of productivity and efficiency

initiatives

Levers of Value Creation

• Hired David Calhoun - GE Vice Chairman,

to restructure the company

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

This material has been prepared by GSAM and is not a product of the Goldman Sachs Global Investment Research (GIR) Department. The views and opinions expressed may differ from those of the GIR Department or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and GSAM has no obligation to provide any updates or changes.

11

Private Equity Investing Challenges

• Illiquidity

• Difficulty of Measuring and Benchmarking Performance

• Achieving a Target Allocation

• Portfolio Rebalancing

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

12

Private Equity – The Future?

SunGard has 53 research-and-development projects under way, many

of them long-term, compared with about 10 before the takeover.

Cristóbal I. Conde, CEO, SunGard

With private-equity owners, their expectations tend to be even higher than

Wall Street's. David Brandon, CEO, Domino’s Pizza

High debt can lead to a scaled-down executive suite. So top executives

tackle duties typically left to others in a larger corporate setting….You're

going to get involved in things you could never have done in a major

corporation. David Beer, CEO, Bakery Chef

Source: “The Private-Equity CEO: Facing Tough Stakeholders”, The Wall Street Journal, Erin White and Gregory ZuckermanThis material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

13

Disclosures

This material is provided at your request for informational purposes only. It is not an offer or solicitation to buy or sell any securities.

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell

securities.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by GSAM to buy, sell, or hold any

security. Views and opinions are current as of the date of this presentation and may be subject to change, they should not be construed as

investment advice.

Furthermore no action has been or will be taken in Israel that would permit a public offering of the interests or a distribution of this presentation to

the public in Israel. GSAMI will obtain warranties from each offeree that it is purchasing an interest for investment purposes only and not for

purposes of resale.

No part of this material may be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an

employee, officer, director, or authorized agent of the recipient, without GSAM’s prior written consent.

Past performance is not indicative of future results, which may vary. The value of investments and the income derived from investments can go

down as well as up. Future returns are not guaranteed, and a loss of principal may occur.

The information in this document is for informational purposes only, and it highlights certain investment products that the Private Equity Group

offers. It does not constitute an offer to sell, or a solicitation of an offer to buy, any products referenced herein. Any such offering will be made only

in accordance with the terms and conditions set forth in the Private Placement Memorandum or Offering Memorandum for the Fund.

Alternative Investments Funds (including private investment funds and hedge funds) are subject to less regulation than other types of pooled

investment vehicles, may make speculative investments, may be illiquid and can involve significant use of leverage, making them substantially

riskier than other investments, including any products which may be shown as a comparison herein. Alternative Investment Funds may incur high

fees and expenses that would offset trading profits. Alternative Investment Funds are not required to provide periodic pricing or valuation

information to investors. Alternative Investment Funds may involve complex tax structures and may involve delays in distributing important tax

information to investors. Alternative Investments by their nature, involve a substantial degree of risk, including the risk of total loss of an investor's

capital, and volatility in the performance of the Fund. Investment in an Alternative Investment Fund is suitable only for sophisticated investors for

whom an investment in such fund does not constitute a complete investment program and who fully understand and are willing to assume the

risks involved in an Alternative Investment Fund.

Prior to investing, investors are strongly urged (i) to review carefully the Offering Memorandum (including the risk considerations described

therein), the Subscription Agreement and all related documents for the Alternative Investment Fund, (ii) to ask such additional questions of the

Investment Manager, General Partner or Managing Member as they deem appropriate, and (iii) to discuss any prospective investment in the Fund

with their legal and tax advisers, particularly with regard to applicable securities, tax or exchange control regulations.

Copyright © 2007, Goldman, Sachs & Co. All rights reserved. Ref# 07/1388