pricing target nols in mergers and acquisitions from the participating firms' perspective

TRANSCRIPT

Advances in Accounting, incorporating Advances in International Accounting xxx (2014) xxx–xxx

ADIAC-00235; No of Pages 11

Contents lists available at ScienceDirect

Advances in Accounting, incorporating Advances inInternational Accounting

j ourna l homepage: www.e lsev ie r .com/ locate /ad iac

Pricing target NOLs in mergers and acquisitions from the participatingfirms' perspective

Wei-Chih Chiang a,⁎, William Stammerjohan b,1, Ted D. Englebrecht b,2

a School of Business Administration, University of Houston — Victoria, Sugar Land, TX 77479, United Statesb School of Accounting and Information Systems, College of Business, Louisiana Tech University, Ruston, LA 71272, United States

⁎ Corresponding author. Tel.: +1 281 275 8880; fax: +E-mail addresses: [email protected] (W.-C. Chiang),

(W. Stammerjohan), [email protected] (T.D. Englebrec1 Tel.: +1 318 257 3828.2 Tel.: +1 318 257 3552.3 See Code Sections 39(a), 53, 172(b)(1), 904(c), and

sections cited in this paper refer to the Internal ReveHereinafter, code sections will be noted as sections.

http://dx.doi.org/10.1016/j.adiac.2014.04.0030882-6110/© 2014 Elsevier Ltd. All rights reserved.

Please cite this article as: Chiang, W.-C., et al.in Accounting, incorporating Advances in Inter

a b s t r a c t

a r t i c l e i n f oAvailable online xxxx

Keywords:Target NOLsM&ATax Reform Act of 1986Section 382

While prior research has extensively examined the market response to target net operating loss carryforwards(NOLs) in mergers and acquisitions (M&A) announcements, the question of whether target NOLs are priced bythe participating firms during the price negotiation process has not been explicitly addressed. Answers to thisquestion could provide direct measures to assist firms in pricing target NOLs in M&As. Our results show thatthe participating firms price target NOLs based on how long it will take the acquirer to use the acquired NOL inboth nontaxable and taxable acquisitions under the Tax ReformAct of 1986. Also, we find a significant differencein themarket pricing and the participant pricing of target short-lived NOLs before, and continuing well after, theannouncement date. Our findings suggest that the importance of the differences between the market and theparticipating firms perspectives should be considered when conducting future research in this area.

© 2014 Elsevier Ltd. All rights reserved.

1. Introduction

In general, the tax benefits gained from mergers and acquisitions(M&A) activities are accrued at both corporate and shareholderlevels (Auerbach & Reishus, 1988a). Use of target net operatinglosses (NOLs) and other tax carryforwards to reduce tax liabilitiesmight be the most visible tax benefit to an acquirer (Haw, Pastena,& Lilien, 1987). Tax law allows acquiring firms to use these tax carry-forwards against their future earnings so that the future tax savingsmake target carryforwards valuable.3 Auerbach and Reishus(1988b) observe three large tax saving acquisitions, which tookadvantage of target tax carryforwards worth hundreds of millionsof dollars in the late 1970s and early 1980s. Although Auerbach andReishus (1988b) find that tax carryforwards may provide tax-savings in M&A activities, their study provides no evidence that theutilization of tax credits and tax loss carryforwards play an impor-tant role in motivating M&A activities. However, Congress hasbeen concerned with tax benefits taken by merging firms andhas attempted to limit tax incentives from business combinations.

1 281 275 [email protected]).

1212(a). Unless specified, codenue Code of 1986 (TRA 86).

, Pricing target NOLs in mergenational Accounting (2014), h

Specifically, several provisions are included in the Internal RevenueCode to restrict the use of NOLs and other tax carryforwards.4 Forexample, Section 382 limits the amount of NOLs that can be utilizedeach year by the successor corporation.

Despite congressional constraints, empirical research generallyshows that target NOLs are priced by the market. Hayn (1989)finds the amount of NOL carryforwards and unused tax credits dueto expiration is the most prominent tax attribute in nontaxable ac-quisitions. Haw et al. (1987) provide evidence that troubled firmswith tax loss carryforwards receive higher acquisition premiumsthan troubled firms without tax loss carryforwards. Moore andPruitt (1987) note that NOLs are priced by the market. However,they also remark that the probability of expiration under theSection 382 revision in the Tax Reform Act of 1976 (TRA 76) reducesthe present value of NOLs. Plummer and Robinson (1990) examinethe relationship between target tax carryforwards and excess stockreturns when a pending acquisition is announced, but they find nosignificant relationship.

The common factor in the studies discussed above is that they arebased on the pricing of target NOLs “by the market,” which is gener-ally measured by cumulative abnormal returns around an event date.On the other hand, this study takes a different approach, whichinvestigates the pricing of target NOLs by the participating firms(i.e., the acquirer and the target) during the price negotiation

4 See, for example, Sections 172(b)(1)(E), 269, 381, 382, 383, and 384. See Scholes et al.(2009, 488, footnote 17) for a summary of the impacts of Sections 381, 382, 383, and 384.

rs and acquisitions from the participating firms' perspective, Advancesttp://dx.doi.org/10.1016/j.adiac.2014.04.003

Taxable Acquisition Nontaxable Acquisition

(Category 1) (Category 2) (Category 3) (Category 4) (Category 5)

Structure of Acquisition

Asset Acquisition†

Stock Acquisition with a §338

Election

Stock Acquisition without a

§338 Election

Asset Acquisition

Stock Acquisition

Whether target NOLs

can be used by the acquirer.

No. However, target NOLs

can be used to offset the gain

associated with the step-

up.

No. However, target NOLs

can be used to offset the gain

associated with the step-

up.

Yes. Yes. Yes.

Examples of Using Target NOLs: 1. Step-up transactions (Categories 1 & 2): Category 1 scenario is used as an example.

Assume the tax basis of target assets is $100 and the target has $250 in NOLs. Acquirer pays $300 cash to acquire target assets. Target will have a capital gain of $200. Target could use its NOLs to offset the entire capital gain but the remaining $50 in NOLs will be lost. Acquirer’s tax basis in the acquired assets is $300.

2. NOLs carryover transactions (Categories 3, 4, & 5): Category 3 scenario is used as an example. Assume the tax basis of target assets is $100 and the target has $250 in NOLs. Target

shareholders have a tax basis of $80 in target stock. Acquirer pays $300 cash to acquire all of target stock. Target shareholders have a capital gain of $220. Target NOLs, $250, are carried over to acquirer, but the use of target NOLs is subject to Section 382 limitation. The tax basis of target assets, $100, is also carried over to acquirer.

†Following by a liquidation of the target.

Fig. 1. Usability of target NOLs by acquirers.

2 W.-C. Chiang et al. / Advances in Accounting, incorporating Advances in International Accounting xxx (2014) xxx–xxx

process. Although it is ignored by prior research, understanding howthe participating firms price target NOLs is important for several rea-sons. First, while prior research has found that investors include thevalue of target NOLs in the price of a target's stock, it is not necessarythat the participating firms will follow the same pattern in pricingtarget NOLs. For instance, information asymmetry may driveparticipating firms to price target NOLs differently from the market(Bayless & Diltz, 1991; Myers & Majluf, 1984). Hayn (1989, 141) no-tices that the coefficient of the independent variable EXPIRE (i.e., theportion of target NOLs expiring within two years) is negative andsignificant in taxable acquisitions. In a more recent acquisitionprice based study, Henning, Shaw, and Stock (2000) examine theeffect of target taxes on acquisition price and conclude that acquirerspay little for target NOLs in taxable acquisitions.5 In terms of meth-odology, Hayn (1989) and Henning et al. (2000) represent themarket's and the participating firms' perspectives, respectively. Thedifferent findings between Hayn (1989) and Henning et al. (2000)indicate that the market and the participating firms could have dif-ferent viewpoints and, hence, a further investigation on the pricingof target NOLs by the participating firms is warranted. Second, thesemi-strong form of efficient market hypothesis provides that capitalmarkets incorporate all publicly available information into stockprices in a quick and efficient manner (Fama, 1970; Malkiel, 2005).Following this hypothesis, the market should adjust its pricing oftarget NOLs after the announcement date. Consequently, thepricing of target NOLs by the market and by the participatingfirms should be similar after the completion of the efficient marketadjustment. In this situation, testing the pricing of target NOLs by themarket or by the participating firms should make little difference.

5 Since Section 382 limitation is not a focal issue in Henning et al. (2000), they do notfurther separate target NOLs into the short-lived and long-lived NOLs.

Please cite this article as: Chiang, W.-C., et al., Pricing target NOLs in mergein Accounting, incorporating Advances in International Accounting (2014), h

However, when themarket adjustment has not been completed or in-vestors' cognitive processing biases exist (Barberis, Shleifer, &Vishny, 1998; Daniel, Hirshleifer, & Subrahmanyam, 1998), a directtest on the pricing of target NOLs by participating firms can providedifferent insights. Third, Hayn (1989) shows that when the depen-dent variable is the target's cumulative abnormal returns duringthe period around the announcement date, the independent variableEXPIRE has a significant coefficient of 0.43 in the nontaxable transac-tions. For practical purposes, how to incorporate Hayn's finding inthe price negotiation process can be a difficult task to the participat-ing firms since Hayn measures the target's cumulative abnormalreturns rather than the acquisition price of the target. Therefore, a di-rect inquiry on whether target NOLs are priced by participating firmscould provide more practical information for participating firms innegotiating the price of target NOLs. Specifically, if the associationbetween the acquisition price and target NOLs is examined, the coef-ficient of target NOLs can be used to estimate the value of target NOLsincluded in the acquisition price. Last, the pricing of target NOLs bythe market basically presents investors' responses to the acquisitionannouncement, while pricing of target NOLs by participating firmsusually achieves consensus during the price negotiation process,which may be established several months before the announce-ment date. According to the semi-strong form of efficient markethypothesis, the pricing of target NOLs by the market should bequickly adjusted toward the pricing of target NOLs by participatingfirms after the announcement date. Prior research (e.g., Hayn,1989; Moore & Pruitt, 1987) suggests that the value of targetNOLs is included in the stock price before the acquisition is an-nounced. Naturally, as the participating firms (but not the market)have more information prior to the acquisition announcement, thevalue of target NOLs priced by the participating firms during thenegotiation process may differ from the value of target NOLsincluded by the market before the announcement date.

rs and acquisitions from the participating firms' perspective, Advancesttp://dx.doi.org/10.1016/j.adiac.2014.04.003

8 In a taxable asset acquisition following a complete liquidation of the target, the targetcorporation is subject to capital gain tax on the sale of the assets, and then, the targetshareholders are subject to tax on the liquidation of their stock. However, the target cor-

3W.-C. Chiang et al. / Advances in Accounting, incorporating Advances in International Accounting xxx (2014) xxx–xxx

Furthermore, several studies (e.g., Haw et al., 1987; Hayn, 1989;Moore & Pruitt, 1987; Plummer & Robinson, 1990) are conductedwith samples under the pre-TRA 86 tax law. Prior to TRA 86, capitalgains associated with the step-up of the tax basis of target's assetswere nontaxable. However, TRA 86 made capital gains associatedwith asset sales taxable and this change had dramatic consequenceson this type of acquisition, making this type of taxable acquisitionvery rare under TRA 86 (Scholes, Wolfson, Erickson, Maydew, &Shevlin, 2009). Moreover, TRA 86 revised the Section 382 limitationto make the use of target NOLs stricter than before. Therefore,revisiting the pricing of target's NOLs under TRA 86 could provideupdated information on these issues.

This paper contributes to the extant literature by employingparticipating firms' perspectives when investigating whetheracquirers pay for target NOLs in both taxable and nontaxable acqui-sitions. Although tax savings may not be the main motivation ofM&A, the potential tax benefits and burdens are considered in theprice negotiation process (Ginsburg & Levin, 2006). Since the acqui-sition price is usually settled during the negotiation process beforethe announcement date, we are also able to examine whether thereare differences in the pricing of target NOLs by the market and theparticipating firms before and after the announcement date. Ourresults show:

(1) The participants assign value to target NOLs that can be usedby the acquirer to reduce taxes in the near term (short-livedNOLs) in both taxable and nontaxable acquisitions underTRA 86.

(2) There are differences in the market and participant pricing oftarget short-lived NOLs before the announcement date andthese differences extend well past the announcement date.

This paper proceeds as follows. Section 2 develops the hypothe-ses and Section 3 describes the research methods. Section 4summarizes the sample statistics and Section 5 discusses the re-sults. Section 6 provides the discussions and concludes this study.

2. Hypothesis development

Among target deferred tax attributes, net operating loss carryfor-wards (NOLs) possess the possibility of reducing future tax liabilitiesfor acquirers. As outlined in Scholes et al. (2009, Table 13.1, 413),there are five basic categories of freestanding C corporation acquisi-tions: (1) taxable asset acquisition, (2) taxable stock acquisitionwitha Section 338 election, (3) taxable stock acquisition without aSection 338 election, (4) nontaxable asset acquisition, and (5) non-taxable stock acquisition.6 The transferability of the target's tax attri-butes and therein the potential usability of target NOLs by acquirersin each category of acquisitions are summarized in Fig. 1. Twonumeric examples are also provided in Fig. 1 to illustrate the use oftarget NOLs in M&As.

The target's tax attributes survive in three cases: taxable stock acqui-sitionwithout a Section 338 election (i.e., Category 3 acquisition in Fig. 1),nontaxable asset acquisition (i.e., Category 4 acquisition in Fig. 1), andnontaxable stock acquisition (i.e., Category 5 acquisition in Fig. 1). 7 Al-though a target's deferred tax attributes could be eliminated in a taxableasset acquisition (i.e., Category 1 acquisition in Fig. 1), Scholes et al. (2009,

6 The terms taxable and nontaxable relate to the immediate tax consequences to thetarget and/or target shareholders. Taxable acquisitions involve primarily cash consider-ation and result in immediate tax consequences at the target level. Nontaxable acquisi-tions involve primarily stock consideration and result in deferred tax consequences atthe target level (Scholes et al., 2009, 407–413).

7 Exceptions occur for type B, divisive type D, and type E of Section 368(a) nontaxableacquisitions. After a type B acquisition, acquirers can still use target NOLs in a consolidatedtax return even though the target NOLs are not directly transferred in these acquisitions.As discussed later in footnote 17, there are no divisive type D transactions in our originalsample and we eliminate the three type E targets from our final sample.

Please cite this article as: Chiang, W.-C., et al., Pricing target NOLs in mergein Accounting, incorporating Advances in International Accounting (2014), h

410) note that this type of acquisition rarely occurs under TRA 86 due tohigh tax costs.8 In a taxable stock acquisition with a Section 338 election(i.e., Category 2 acquisition in Fig. 1), target NOLs can be used by thetarget corporation to offset its corporate-level gain associated with thestep-up in assets, but any unused target NOLs are lost and cannot becarried over to the acquirer. This type of acquisition is only viable whenthe target has enough NOLs to offset much of the capital gains tax associ-ated with the step-up in basis.9 Given that prior research (e.g., Ayers,Lefanowicz, & Robinson, 2003; Henning et al., 2000) indicates thatacquisitions with Section 338 elections comprise only 2% or less of alltaxable acquisitions, we assume that these cases are rare in our sampleand do not distinguish between those taking the election and those nottaking the election.10

In addition to showing the importance of target short-lived NOLs innon-taxable acquisitions, Hayn (1989, 141) suggests that the value oftarget short-lived NOLs is included in the stock price prior to the acqui-sition announcement, but the market lowers its pricing when a taxableacquisition is announced. That is, the value of target short-lived NOLs isnegatively priced by the market when a taxable acquisition is an-nounced. However, Henning et al. (2000) do not discover the negativerelationship but find that acquirers pay little for target NOLs in taxableacquisitions. The different findings between Hayn (1989) and Henninget al. (2000) may arise from several sources. First, the finding of Hayn(1989) is based on target short-lived NOLs since the Section 382 limita-tion is considered in her study. Henning et al. (2000) focus on the entiretarget NOLs in step-up transactions because the Section 382 limitationdoes not apply to this type of acquisition. Second, Hayn (1989) andHenning et al. (2000) represent the market's and the participatingfirms' perspectives, respectively. Hayn (1989) employs an event studyto measure the market's response (i.e., cumulative abnormal returns)to the acquisition announcement, but Henning et al. (2000) relate ac-quisition price to target tax attributes. The market and the participatingfirmsmay price target NOLs differently. Third, different types of taxabletransactions included in their samples are not proportional. Hayn's sam-ple is from the period before the enactment of TRA 86. Step-up transac-tions (e.g., Categories 1 and 2 acquisitions in Fig. 1) were not unusualbefore TRA 86 was enacted.11 Although Henning et al. (2000) use thesample under TRA 86, their study focuses on taxable transactions suchthat most of their samples are involved with step-up transactions.That is, the majority of Hayn's taxable acquisition subsample may con-sist of stock acquisitions without a Section 338 election (i.e., Category3 acquisition in Fig. 1), but the sample of Henning et al. (2000)may con-tain more step-up acquisitions (e.g., Categories 1 and 2 in Fig. 1). Asshown in Fig. 1, the usability of target NOLs by acquirers in these typesof taxable transactions is different so that the pricing of target NOLscould differ.

As previously noted, taxable asset acquisitions (i.e., Category 1acquisition in Fig. 1) are rare after the enactment of TRA 86 and taxablestock acquisitions with a Section 338 election (i.e., Category 2 acquisi-tion in Fig. 1) consist of less than 2% of taxable acquisitions (Ayerset al., 2003; Henning et al., 2000). As a result, stock acquisitionswithouta Section 338 election (i.e., Category 3 acquisition in Fig. 1) could be the

poration can offset the capital gains with its NOLs and the acquirer obtains a step-up inthe tax basis of the acquired target assets.

9 In theHenninget al. (2000) sample, 147of 154 transactionswith Section 338 electionsinvolve target NOLs which could be used to offset 86.4% of target's gain on the sale.10 We conduct a set of tests to address the sensitivity of our results to this assumption.We re-run our models after deleting those taxable acquisitions with the largest targetNOLs, 1%, 2%, 5%, and 10% under the assumption that the targets with the largest NOLswould be the ones most likely acquired with a Section 338 election. These untabulated re-sults produce no significant differences in our primary NOL coefficients.11 Step-up transactions consist of 17% of the largest pre-TRA 86 acquisitions (Scholeset al., 2009, 410, footnote 12).

rs and acquisitions from the participating firms' perspective, Advancesttp://dx.doi.org/10.1016/j.adiac.2014.04.003

4 W.-C. Chiang et al. / Advances in Accounting, incorporating Advances in International Accounting xxx (2014) xxx–xxx

major type of taxable transactions after TRA 86 was enacted. Conse-quently, Categories 3, 4, and 5 in Fig. 1 should be the most commontypes of acquisitions under TRA 86. Since target NOLs could be used byacquirers in these types of acquisitions, we expect target NOLs to bepriced by participants in both taxable and non-taxable acquisitionsunder TRA 86. We state our expectations in hypothesis H1:

H1. Target NOLs are priced by the participating firms in both taxableand nontaxable acquisitions.

Even though target NOLs may provide future tax savings to theacquirer, the acquirer's use of target NOLs may be restricted bySection 382. Specifically, Section 382 limits the annual use of acquiredNOLs to an amount equal to the long-term tax-exempt market ratemultiplied by the market value of the target's equity at the time of theownership change.12 Moore and Pruitt (1987) demonstrate that theSection 382 revision in TRA 76 reduces the present value of targetNOLs because the revision increases the probability of the expirationof these deferred tax assets before they can be used to reduce futuretaxes. Because current Section 382 is more restrictive under TRA 86than the former Section 382 under TRA 76, the present value of targetNOLs subject to the current Section 382 in our study could be evenmore severely discounted.13 Morris (2004, 195) argues that when theSection 382 limitation applies, the value of target NOLs should besignificantly discounted or even eliminated by acquirers. It is also clearto the market that tax savings provided by target NOLs in the first fewyears are more valuable than tax savings that can only be used later(Hayn, 1989). That is, both the market and acquiring firms considerthe Section 382 limitation and discount the value of target NOLs.

While target NOLs may be priced based on tax savings, NOLs alsoprovide signals regarding the potential failure of the target's businessoperation (Amir & Sougiannis, 1999; Amir, Kirschenheiter, & Willard,1997). Large NOLs may result from reoccurring and accumulatedoperating losses that signal potential failure of the target under currentmanagement. Naturally, this could reduce the price at which the targetcan be acquired. Given that the combination of Section 382 limitationsand the fact that larger NOLs may also signal potential failure of the tar-get under current management, we expect that the value assigned totarget NOLs usable only in the long term (long-lived NOLs) will beless than the value assigned to target NOLs usable in the near term(short-lived NOLs). Given the differences in value, and given the highlikelihood of transferability of tax attributes in both our taxable andnontaxable transactions, we state our expectations in H2 and H3:

H2. Target NOLs usable in the near term are priced by the participatingfirms in both taxable and nontaxable acquisitions.

H3. Target NOLs only usable in the long term are priced at a lower ratethan NOLs usable in the near term in both taxable and nontaxableacquisitions.

The question of whether target NOLs are included in the stock pricebefore the acquisition announcement has been investigated in priorresearch. Some studies find that the value of NOLs is included in thestock price. For example, in their event study, Moore and Pruitt (1987)conclude that NOLs are priced by the market but that this value isreduced by the increased probability of expiration under the revisionsin Section 382 included in TRA 76. Moreover, Haw et al. (1987) showthat troubled firms with tax loss carryforwards gained a 33.7% acquisi-tion premium while the acquisition premium for those without taxloss carryforwards was only 19.6%. An interpretation, of this excess

12 As an example, target T is acquired by acquirer A for $1000. T has $250 inNOLs and thelong-term tax-exempt rate is 5%. Acquirer A can only apply $50 of the acquired NOLs toeach year's tax return, i.e., recovery of the full tax benefit of the acquired NOLs will takeat least five annual tax returns.13 See Scholes et al. (2009, 488, footnote 18) for an explanation of the differences be-tween TRA 76 and TRA 86 on this issue.

Please cite this article as: Chiang, W.-C., et al., Pricing target NOLs in mergein Accounting, incorporating Advances in International Accounting (2014), h

premium, could be that tax loss carryforwards provide future taxsavings. However, it may also be interpreted in line with the conceptthat target NOLs may be negatively priced prior to the acquisitionannouncement. If the acquisition is anticipated, the premium assignedin the M&A price may represent a move from a pre-acquisitiondepressed price to fair value. Nevertheless, Hayn (1989) argues that be-cause of the difficulty of anticipating the tax status of an acquisition, thepotential benefits of tax attributes are not fully included in the partici-pating firms' stock prices prior to the acquisition announcement.

The above studies imply that although themarket includes the valueof target NOLs in the stock price before the acquisition announcement,the value of target NOLs might not be fully incorporated. Specifically,it seems that the value of target NOLs is understated by the market(Haw et al., 1987; Hayn, 1989). Moreover, management is usually as-sumed to know more about the firm's value than potential investors(Myers &Majluf, 1984). Likewise, an acquiring firmusually receives im-portant private information on the target after signing a letter of intent(Bruner, 2004). That is, the participating firms should knowmore aboutthe target's value than the market (Laamanen, 2007). Accordingly, weexpect that the market will underprice target NOLs as compared tothe participants prior to the announcement. However, under the semi-strong form of efficient market hypothesis (Fama, 1970), once the ac-quisition is announced and more information is released, the marketprice will reflect all available information (Malkiel, 2005). As a result,we expect that the difference between market and participant pricingof target NOLs should be eliminated after the announcement date. Westate our expectations in H4 and H5:

H4. The market will price target NOLs at a lower rate than the partici-pating firms prior to the announcement date.

H5. The difference in the pre-acquisition announcement pricing oftarget NOLs by the market and participating firms will diminish afterthe announcement date.

3. Research methods

3.1. Model development

Although event studies have been commonly used in prior researchto investigate themarket's pricing of NOLs (e.g., Haw et al., 1987; Hayn,1989; Moore & Pruitt, 1987; Plummer & Robinson, 1990), the currentstudy applies a price level approach to examining the price of targetNOLs assigned by participating firms. This approach is more consistentwith Henning et al. (2000).

Based on Ayers et al. (2003), we develop our models for hypoth-esis tests. Ayers et al. (2003, 2787) relate PREM, the difference be-tween the acquisition price (AP) and the target's pre-mergermarket value (MV), to a set of independent and control variables.Wemodify this model to relate AP toMV and a similar set of indepen-dent and control variables.14 There are two reasons that we employAP as our primary dependent variable as opposed to PREM. First,employing AP allows us to provide an operational measure of theprice of target NOLs in the M&A setting.15 Second, employing APallows us to directly compare the pre-announcement market pricingof target NOLs and participant pricing of target NOLs.

Regarding MV, we incorporate the Feltham and Ohlson (1995)model modified by Amir and Sougiannis (1999), which separates thecomponents of deferred taxes from other net assets. That is, we modelthemarket value of equity (MV) on the targets' components of deferred

14 In the Ayers et al. (2003) model, it is defined that PREM equals APminusMV. We sim-ply rewrite the equation to show that AP equalsMV plus PREM. Later, following Amir andSougiannis (1999) and Ayers et al. (2003), we decompose MV and PREM to develop ourmodels (2) and (3).15 The estimated target NOL coefficients in our models provide future M&A participantswith an average measure of target NOL pricing.

rs and acquisitions from the participating firms' perspective, Advancesttp://dx.doi.org/10.1016/j.adiac.2014.04.003

5W.-C. Chiang et al. / Advances in Accounting, incorporating Advances in International Accounting xxx (2014) xxx–xxx

taxes (DTC), adjusted net book value (ABV), and current abnormalearnings (CAE).

MV ¼ α0 þα1kDTCk þα2ABV þα3CAE þω ð1Þ

Market value of equity (MV) is defined as the market value of thetarget's equity prior to the acquisition announcement. Prior researchhas shown that information regarding the relationship between thepricing and book values of deferred taxes is lost when the numbersare aggregated (e.g., Amir & Sougiannis, 1999; Amir et al., 1997). Sinceour primary interest is the pricing of the NOL component, we decom-pose net deferred taxes into six components: (1) deferred tax assetsfrom the NOL carryforwards (NOL), (2) deferred tax assets from otherloss carryforwards (OLC), (3) deferred tax assets from tax creditcarryforwards (TCC), (4) all other deferred tax assets (AODTA), (5) thedeferred tax asset valuation allowance (VA), and (6) deferred tax liabil-ities (DTL). Adjusted book value (ABV) is the target's net book valueminus net deferred taxes. Current abnormal earning (CAE) is currentearnings in the year before the announcement year minus expectedearnings for that year. Expected earnings are defined as net operatingassets at the beginning of the year times the cost of capital. Proxies forthe cost of capital are obtained from Ibbotson (2008).

As for AP we adopt the control variables identified by Ayers et al.(2003), including the taxability of the acquisition (NTAX), the bidder'spre-announcement ownership in the target (BOWN),management hos-tility (HOST), competing bids (CB), tender offers (TEN), target leverage(LEV), target return on market value of equity (ROE), and the target'snet book value tomarket value of equity ratio (BKMV). Additionally, be-cause of the importance of research and development expenses in M&Apricing as documented by Laamanen (2007) and Hsu, Kim, and Song(2009), we include the target's research and development expenses(XRD) as an additional control variable. Laamanen (2007) argues thatan acquirer pursuing the acquisition of a technology-based companyhas a more positive perception of the target's R&D investments thanthe market and is willing to pay a higher premium for target R&D-related assets. Also, we include indicator variables for the target firm'sindustry and year of acquisition.16 Accordingly, our modifications onthese models lead to the following model17:

AP ¼ β0 þ ρ1NOLþ ρ2OLC þ ρ3TCC þ ρ4AODTAþ ρ5VAþ ρ6DTLþ β2ABV þ β3CAE þ β4NTAX þ β5BOWNþ β6HOST þ β7CBþ β8TEN þ β9LEV þ β10ROEþ β11BKMV þ β12XRDþ Σβ13iSICi þ Σβ14 jYEARj þ η:

ð2Þ

Acquisition price (AP) is the value paid for each share of the target'sequity as reported in the Securities Data Corporation's M&A database(the SDC database). NOL, OLC, TCC, AODTA, VA, and DTL are as reportedin the last annual report prior to the announcement date and are deflat-ed by the number of target common shares outstanding in that same re-port. ABV and CAE are defined in model (1). Taxability of the acquisition(NTAX) is an indicator variable set to one for nontaxable acquisitions.Owned before (BOWN) is the percentage of the target's common stockowned by the acquirer prior to the announcement date. Hostility(HOST) is set to one if the target's management opposed the acquisition.Competing bids (CB) is set to one if a competing bidder existed. Tenderoffer (TEN) is set to one if the acquisition was initiated with a tender

16 Since the one-digit SIC zero contains only two observations, these two firms are com-bined with the SIC one group for controlling the industry effect.When these two observa-tions are deleted, the results remain unchanged.17 Erickson andWang (2000, 76, Model 6) use the Feltham and Ohlson (1995) model toestimate the fairmarket value of the target,which is subtracted from the actual acquisitionprice to compute the acquisition premium in their Model 7. Erickson and Wang (2000)treat acquisition premium as the dependent variable in Model 7. However, if we decom-pose the acquisition premium in theirModel 7 into acquisition priceminus the fairmarketvalue of the target and, then,move the fairmarket value of the target to the right hand sideof the equation, their Model 7 would look very similar to ourmodels, except that Ericksonand Wang (2000) and our study use different control variables.

Please cite this article as: Chiang, W.-C., et al., Pricing target NOLs in mergein Accounting, incorporating Advances in International Accounting (2014), h

offer. Target leverage (LEV) is the target's ratio of long-termdebt tomar-ket value four weeks prior to the announcement date. Return on themarket value of equity (ROE) is the ratio of the target's net income be-fore extraordinary items reported in the last annual report divided bythe target's market value four weeks prior to the announcement date.Book tomarket ratio (BKMV) is the ratio of target's net book value of eq-uity in the last annual report prior to the announcement date divided bythe target's market value four weeks prior to the announcement date.Research and development expense (XRD) is the target's average re-search and development expense in the last two annual reports priorto the announcement date. All the monetary variables, AP, NOL, OLC,TCC, AODTA, VA, DTL, ABV, CAE, and XRD are deflated by the number oftarget common shares outstanding in the last annual report prior tothe announcement date. SICi are indicator variables set to one whenthe target is a member of one-digit SIC code i, and YEARj are indicatorvariables set to one if the acquisition occurred in year j. The indicatorvariables, NTAX, HOST, CB, TEN, SICi and YEARj are set to zero when theconditions are absent.

Section 382 restricts the annual usage of acquired target NOLs to thelong-term tax-exempt rate times themarket value of the target. For thispurpose, the long-term tax-exempt rate is defined as the highest adjust-ed federal long-term rate for the previous three-month period. Specifi-cally, where the amount of target NOLs is greater than the long-termtax-exempt rate times the market value of the target, Section 382 limi-tations render someportion of the acquiredNOLs as unusable in thefirstyear.18 Similar to Hayn (1989), we further separate the acquired NOLsinto short-lived NOLs (NOLS) and long-lived NOLs (NOLL). NOLS repre-sents the amount of acquired NOLs that can be used within the firstyear, and NOLL represents the amount of acquired NOLs that cannotbe used within this period.

AP ¼ β0 þ φ1NOLSþ φ2NOLLþ ρ2OLCþ ρ3TCC þ ρ4AODTAþ ρ5VAþ ρ6DTLþ β2ABV þ β3CAEþ β4NTAX þ β5BOWNþ β6HOST þ β7CBþ β8TEN þ β9LEV þ β10ROEþ β11BKMV þ β12XRDþ Σβ13iSICi þ Σβ14 jYEARj þ δ

ð3Þ

NOLS andNOLL are calculated from information in the last annual re-port prior to the announcement date, themarket value of the target eq-uity, and the long-term tax-exempt rate. NOLS and NOLL are deflated bythe number of target common shares outstanding in the last annual re-port prior to the announcement date. The other variables in model (3)are the same as described above.

Next, to examine any difference in the pricing of target NOLs by theM&A participants and the market in the period surrounding the an-nouncement date, we estimate a system of two seemingly unrelated re-gressions that are comprised of model (3) described above and model(4) described below.Model (4) employsmarket value (MV), themarketvalue of the target's equity deflated by the number of target commonshares outstanding in the last annual report prior to the announcementdate as the dependent variable. Model (4) also employs the same disag-gregation of deferred taxes and the same controls for industry and yearas model (3).19

MV ¼ α0 þ φ1NOLSþ φ2NOLLþ ρ2OLCþ ρ3TCC þ ρ4AODTAþ ρ5VAþ ρ6DTLþ α2ABV þ α3CAEþ Σα4iSICi þ Σα5 jYEARj þω

ð4Þ

All the variables in model (4) are as described above.

18 Furthermore, if the market value of target NOLs is greater than two times long-termtax-exempt rate times the total value paid for the target, some portion of the target NOLswill be unusable within the first two years. As the ratio of acquired NOLs to the total valueof the acquisition increases, the time delay between the acquisition and the acquirer's abil-ity to use the target NOLs for tax savings becomes longer.19 The STEST statement in the SAS procedure PROC SYSLIN allows us to test the hypoth-eses relating to parameters in different equations.

rs and acquisitions from the participating firms' perspective, Advancesttp://dx.doi.org/10.1016/j.adiac.2014.04.003

Table 1Sample.

Panel A: sample selection process

Selection step Number of firms deleted Number of firms

Research insights inactive firms delisted from the NYSE/ASE during 1997–2006 2506Financial institutes or electric utilities; not wholly owned by acquirer after acquisition; not in the SDC database 1677Missing financial or transactional data 136Type E reorganizations 3Negative book value 30Full sample 660

Panel B: sample by SIC and year

SIC code Industry Obs. Year Obs.

1–999 Agriculture, forestry, and fishing 2 1997 861000–1999 Metal and mining 77 1998 1132000–2999 Food, textile, and chemicals 125 1999 1093000–3999 Rubber, metal, and machines 204 2000 1204000–4999 Transportation 43 2001 485000–5999 Wholesale and retail trade 93 2002 267000–7999 Hotel and other services 84 2003 258000–8999 Health and engineering services 32 2004 36

2005 502006 47

6 W.-C. Chiang et al. / Advances in Accounting, incorporating Advances in International Accounting xxx (2014) xxx–xxx

3.2. Variables

The continuous dollar variables in the models are deflated by thenumber of target common shares outstanding in the last annual reportprior to the announcement date to reduce heteroscedasticity (Amiret al., 1997). The acquisition price (AP) represents the total value ofconsideration paid to target shareholders and is based on VALIMP (theimplied value of a transaction) as reported in the SDC database. Thetarget's market value (MV) is based on the daily closing price as report-ed on the Center for Research in Security Prices (CRSP) database. Datafor the deferred tax variables, DT, NOL, OLC, TCC, AODTA, VA, and DTL,are collected from the target's last annual report prior to the announce-ment date.20 FISCAL in the SDC database is used to identify the date ofthe last fiscal year-end prior to the announcement date. Similar toAmir et al. (1997), all of the deferred tax values are recorded as positivenumbers so that the corresponding coefficients clearly indicate the rela-tionship between the acquisition price and the deferred tax attributes.The deferred tax components, NOL, OLC, TCC, AODTA, VA, and DTL, areavailable from the targets' 10-Ks in the Edgar online database as foot-note disclosures are required by SFAS No. 109.

NOLS and NOLL are apportioned from the NOL under the require-ments of Section 382. NOLS is the lesser of the total acquired targetNOLs or the market value of the target's equity multiplied by the long-term tax exempt rate. The long-term tax-exempt rate is defined as the

20 Prior research has identified limitations of using Compustat based financial data to es-timate actual U.S. tax liability (Lisowsky, 2009) and to classify whether or not a companywould report a loss carry-forward on their U.S. federal tax return (Mills, Newberry, &Novack, 2003). Specifically, Lisowsky (2009) finds the following hierarchy where tax re-lated financial disclosures are helpful in estimating total tax on the tax return: first profit-able firmswithoutNOLs, profitable firmswith NOLs, unprofitable firmswithout NOLs, andfinally unprofitable firms with NOLs. We separate our sample into profitable firms withNOLs and unprofitable firms with NOLs subsamples. The results (untabulated) show thatNOLS is positively significant in ourmodels (3) and (4) in both subsamples. It implies that,our findings remain unchanged regardless of the hierarchical information of target NOLs.Moreover, Mills et al. (2003) document that Compustat's misclassification of U.S. tax re-turn NOLs tends to arise from: the existence of foreign NOLs, acquired NOLs, and fromCompustat's coding errors. We avoid Compustat coding errors by taking our data directlyfrom the target's tax footnotes. However, given that our NOL information comes from thetargets financial statements, it is comprised of aggregate numbers that may contain ac-quired and/or foreign NOLs. It should be noted that if these non-U.S. and/or acquired NOLsare either non-transferable or not subject to the limitations of I.R.C. Section 382, the resultwould work against our reported findings, i.e., the result is that the true findings could bestronger than what we report. While the potential existence of non-U.S. and/or acquiredNOLs should not inflate our results, we do note that our lack of confidential tax return datamay pose a limitation to our study.

Please cite this article as: Chiang, W.-C., et al., Pricing target NOLs in mergein Accounting, incorporating Advances in International Accounting (2014), h

highest adjusted federal long-term rate for the previous three-monthperiod. NOLS represents the maximum amount that can be used fortax savings by the acquirer in the first year following the acquisition,and NOLL represents the remaining amount that is only available inthe second year and beyond.

The target financial variables, ABV, CAE, LEV, ROE, BKMV, andXRD, arecontained in the last annual report before the announcement date andobtained from Research Insights. ABV is calculated as the net bookvalue of target shareholders' equity minus net deferred taxes. Currentabnormal earnings (CAE) is calculated following Amir et al. (1997).Current earnings are calculated as income before extraordinary itemsplus tax-adjusted interest expense minus tax-adjusted other nonoper-ating income. All tax-adjusted items are calculated by using the originalamounts multiplied by one minus the maximum federal corporateincome tax rate effective in the year prior to the announcementyear.21 Current abnormal earnings (CAE) are then computed as currentearnings minus expected normal earnings. Expected normal earningsequal net operating assets at the beginning of the year before the an-nouncement year times the cost of capital. Consistent with prior re-search (e.g., Amir & Sougiannis, 1999; Givoly & Hayn, 1991; Landry,1998), we obtain proxies for the cost of capital from the IbbotsonYearbook.

The taxability of the acquisition (NTAX) is an indicator variablewhich is coded based on the Commerce Clearing House (“CCH”) CapitalChanges Reporter. The CCH Capital Changes Reporter contains asummary of the target's U.S. federal income tax ramifications for eachacquisition. The tax status of each acquisition is determined by a reviewof the corresponding summary.22 NTAX is coded one when the acquisi-tion is nontaxable and zero otherwise. BOWN, HOST, CB, and TEN areobtained from the SDC database based on PCTACQ (percentage of sharesacquired), ATTC (attitude code of the transaction), CHA (challenging bidflag), and TEND (tender offer flag). Given that PCTACQ is the percentageof a target's shares acquired in the acquisition, BOWN equals 100 minusPCTACQ. When ATTC shows “Hostile,” HOST equals one; and zero

21 The maximum federal corporate income tax rate between 1997 and 2006 was a con-stant 35%.22 An example of the CCH summary that was coded taxable is: “Chaparral Steel Co. 12-31-1997. Merged into Texas Industries, Inc. by merger of its wholly-owned subsidiary.Compare cash received with basis of shares surrendered to compute capital gain or loss.Company's opinion. Per share Chaparral Steel Co. common ($0.10 par): $15.50 cash.” An-other example of the CCH summary that was coded nontaxable is: “Caliber System, Inc.01-27-1998. Merged into FDX Corp. by merger of its wholly-owned subsidiary. Nontax-able. Counsel's opinion.”

rs and acquisitions from the participating firms' perspective, Advancesttp://dx.doi.org/10.1016/j.adiac.2014.04.003

Table 2Summary statistics of variables.

Panel A: financial variables

Variable Minim. Maxim. Mean Median Std. Err. 1st Qrt 3rd Qrt

AP 0.29 165.00 33.22 28.35 25.69 13.61 45.23MV 0.36 150.00 22.59 18.70 17.86 9.12 30.90ABV −1.85 76.17 10.89 8.77 9.08 4.73 14.48CAE −47.58 8.48 −1.36 −0.82 3.39 −2.06 0.12NOL 0 22.02 0.48 0.04 1.29 0 0.45NOLS 0 1.42 0.13 0.03 0.20 0 0.19NOLL 0 21.15 0.36 0 1.22 0 0.12OLC 0 2.89 0.04 0 0.22 0 0TCC 0 3.59 0.12 0 0.35 0 0.07AODTA 0 11.45 1.17 0.63 1.68 0.25 1.30VA 0 19.90 0.46 0.01 1.59 0 0.28DTL 0 33.16 1.66 0.73 2.68 0.24 1.80LEV 0 19.82 0.53 0.25 1.13 0.06 0.58ROE −36.16 14.75 0.88 0.87 2.44 0.04 1.74BKMV 0.02 13.42 0.69 0.52 0.81 0.30 0.83XRD 0 6.87 0.32 0 0.77 0 0.30BOWN 0 0.94 0.07 0 0.21 0 0

Panel B: indicator variables

Number of firms where the indicator variable is

Variable 0 1NTAX 411 249HOST 645 15CB 616 44TEN 447 213

Notes:

1. Sample consists of 660 firms listed on New York or American Stock Exchanges and acquired during 1997–2006.2. AP: acquisition price;MV:market value of target's equity 4 weeks prior to the announcement date; ABV: adjusted book value of target; CAE: current abnormal earnings; NOL: deferred

tax asset fromNOL; NOLS: deferred tax asset from short-lived NOL; NOLL: deferred tax asset from long-livedNOL; OLC: deferred tax asset from other loss carryforwards; TCC: deferredtax asset from tax credit carryforwards; AODTA: all other deferred tax assets; VA: valuation allowance; DTL: deferred tax liabilities; LEV: target's leverage; ROE: return onmarket valueof equity; BKMV: ratio of target's book value of equity to market value of equity; XRD: target's R&D expenses; BOWN: the percentage of target's common stock owned by the acquirerprior to the announcement date.

3. NTAX: one, nontaxable acquisition; zero otherwise. HOST: one, hostile acquisition; zero, otherwise. CB: one, multiple bidders; zero, otherwise. TEN: one, tender offer; zero, otherwise.

7W.-C. Chiang et al. / Advances in Accounting, incorporating Advances in International Accounting xxx (2014) xxx–xxx

otherwise. If CHA indicates multiple bidders, CB equals one; zero other-wise. TEN equals one when a tender offer exists; zero otherwise.

4. Sample selection and summary statistics

4.1. Sample selection

The following steps were used to select our sample firms. First, weidentify inactive firms in Research Insights whichwere delisted from ei-ther the New York or American Stock Exchanges during 1997–2006.Second, the targets are required to be listed in the SDC database, andafter the acquisition, the targets are all wholly owned by the acquirers.Also, following Amir et al. (1997), we exclude firms classified aseither financial institutions (one-digit SIC code 6) or electric utilities(two-digit SIC code 49). Third, the firm's last annual financial state-ment prior to acquisitionmust be available online from the Edgar on-line database. Fourth, acquisitions involved with divisive type D andtype E reorganizations are excluded.23 Last, firms with negative netbook value are removed.

This process generates afinal sample consisting of 660firms. Table 1,Panel A presents the sample selection process, and Table 1 Panel Bshows the final sample by SIC code and Year. The most common one-digit SIC code is three (i.e., rubber, metal, and machine industries),

23 We examined our original sample for divisive typeD reorganizations via two variablesin the SDC database, SPIN and SPLIT. None of our acquisitions were identified as divisivetype D transactions. Type E reorganizations are identified via the RECAP variable in theSDC database. Three acquisitions were identified as type E reorganizations and removedfromourfinal sample:AlliedDigital TechnologiesCo., Uniflex Inc., andBig FlowerHoldingsInc.

Please cite this article as: Chiang, W.-C., et al., Pricing target NOLs in mergein Accounting, incorporating Advances in International Accounting (2014), h

containing 209 firms, while only two firms have the one-digit SICcode of zero (i.e., agriculture, forestry, and fishing industries). Theyear 2000 has the largest number of observations.

4.2. Summary statistics

Table 2, Panel A, shows the summary statistics for the financial var-iables that are stated in dollars per share. Themean target net operatingloss carryforward (NOL) is $0.48 per share. On average, the short-livedNOLs consist of 27% of the target's NOLs. However, this result is due totargets with very large NOLs. While 55.3% of the targets have someNOLs, less than half of these have NOLs that cannot be used by theiracquirers within the first year. Table 2, Panel B, presents the frequenciesof the indicator variables, NTAX, HOST, CB, and TEN. Almost 38% of theacquisitions are nontaxable, and only 2% of the acquisitions involvemanagement hostility.

5. Empirical results

Table 3 presents the regression results for model (2), which isapplied to the full sample, nontaxable subsample, and taxablesubsample. The findings show that the coefficient on NOL is insig-nificant in all three estimations, indicating that aggregated targetNOLs are not priced by the participating firms in either nontax-able or taxable acquisitions. Consistent with the findings ofHenning et al. (2000), hypothesis H1 is not supported.

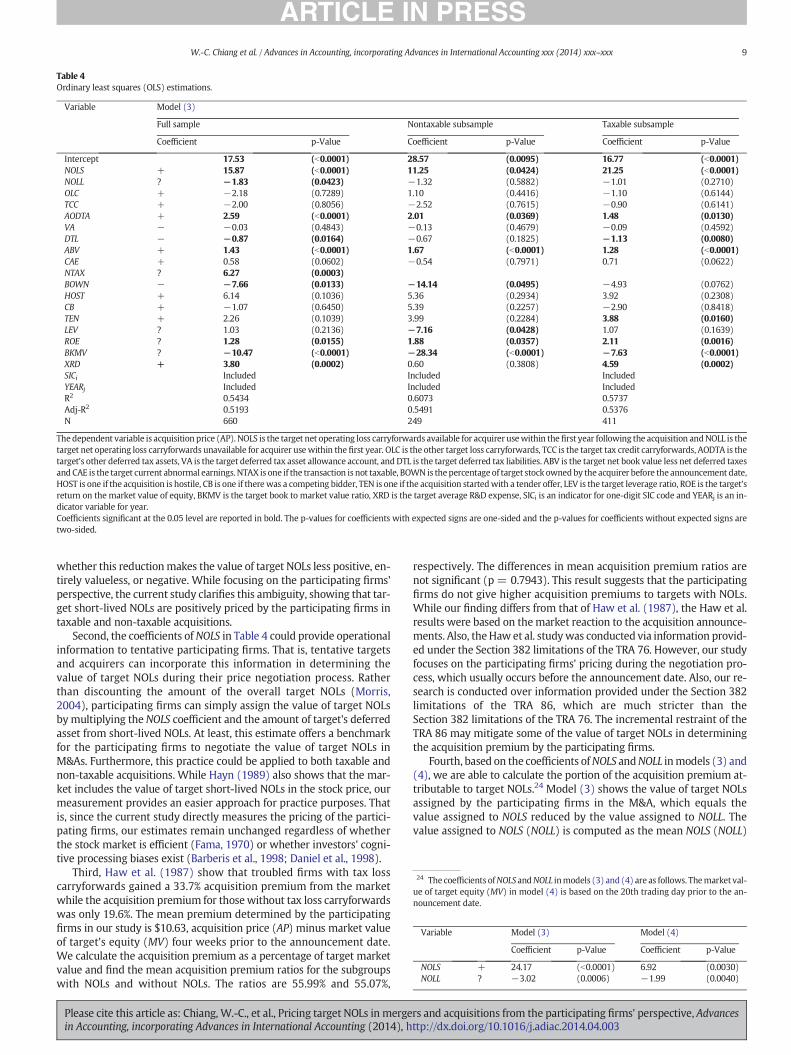

However, we find a different result when NOL is divided into short-lived NOLs (NOLS) and long-lived NOLs (NOLL) in model (3). In Table 4,hypothesis H2 is fully supported with significant NOLS coefficients forthe full, nontaxable, and taxable samples (p ≤ 0.0001, 0.0095, 0.0001,

rs and acquisitions from the participating firms' perspective, Advancesttp://dx.doi.org/10.1016/j.adiac.2014.04.003

Table 3Ordinary least squares (OLS) estimations.

Variable Model (2)

Full sample Nontaxable subsample Taxable subsample

Coefficient p-Value Coefficient p-Value Coefficient p-Value

Intercept 19.48 (b0.0001) 31.89 (0.0035) 19.32 (b0.0001)NOL + −0.50 (0.7215) 0.60 (0.3918) 0.34 (0.3496)OLC + −2.16 (0.2753) 1.61 (0.4150) −1.35 (0.6364)TCC + −2.36 (0.8424) −2.56 (0.7642) −1.15 (0.6427)AODTA + 2.65 (b0.0001) 2.01 (0.0377) 1.73 (0.0053)VA − −0.20 (0.3989) −0.37 (0.4117) −0.63 (0.2286)DTL − −0.79 (0.0283) −0.66 (0.1860) −0.93 (0.0251)ABV + 1.47 (b0.0001) 1.69 (b0.0001) 1.34 (b0.0001)CAE + 0.58 (0.0621) −0.63 (0.8323) 0.76 (0.0528)NTAX ? 6.75 (0.0001)BOWN − −8.12 (0.0102) −13.17 (0.0626) −6.43 (0.0329)HOST + 5.26 (0.1428) 5.23 (0.2988) 3.86 (0.4782)CB + −0.37 (0.5458) 5.69 (0.2143) −1.61 (0.7088)TEN + 2.49 (0.0846) 3.77 (0.2418) 3.74 (0.0214)LEV ? 0.93 (0.2699) −8.18 (0.0196) 0.97 (0.2158)ROE ? 1.27 (0.0174) 2.00 (0.0259) 1.87 (0.0056)BKMV ? −11.26 (b0.0001) −29.40 (b0.0001) −8.42 (b0.0001)XRD + 4.38 (b0.0001) 0.83 (0.3367) 5.81 (b0.0001)SICi Included Included IncludedYEARj Included Included IncludedR2 0.5308 0.6018 0.5552Adj-R2 0.5068 0.5449 0.5188N 660 249 411

Coefficients significant at the 0.05 level are reported in bold. The p-values for coefficients with expected signs are one-sided and the p-values for coefficients without expected signs aretwo-sided.The dependent variable is acquisition price (AP). NOL is the target net operating loss carryforwards. OLC is the other target loss carryforwards, TCC is the target tax credit carryforwards,AODTA is the target's other deferred tax assets, VA is the target deferred tax asset allowance account, and DTL is the target deferred tax liabilities. ABV is the target net book value less netdeferred taxes and CAE is the target current abnormal earnings. NTAX is one if the transaction is not taxable, BOWN is the percentage of target stock owned by the acquirer before theannouncement date, HOST is one if the acquisition is hostile, CB is one if there was a competing bidder, TEN is one if the acquisition started with a tender offer, LEV is the target leverageratio, ROE is the target's return on the market value of equity, BKMV is the target book to market value ratio, XRD, is the target average R&D expense, SICi is an indicator for one-digit SICcode and YEARj is an indicator variable for year.

8 W.-C. Chiang et al. / Advances in Accounting, incorporating Advances in International Accounting xxx (2014) xxx–xxx

respectively). Similar to Hayn (1989), we find that the participants as-sign significant value to those target NOLs that can be used in the nearterm, but do not assign significant value to those acquired NOLs thatcan only be used over a longer period. The negative sign on NOLL isconsistent with the idea that excess net operating loss carryforwardsindicate past problems that are reflected in reduced acquisition prices.

We report the results of the differences in the NOLS and NOLL coeffi-cients along with a sensitivity test regarding the time definitions ofshort-lived vs. long-lived NOLs in Table 5. We re-estimate model (3)after altering the definition of NOLS so that short-lived NOLs are definedas the amounts that could be used in the first one, two, three, four, orfive-years under Section 382 limitations. In each case, long-lived NOLs(NOLL) are defined as the total target operating loss carryforwards(NOL) minus the short-lived NOLs (NOLS). These results supporthypothesis H3 with a significant difference in NOLS and NOLL pricingunder the one-year and two-year definitions of NOLS. Furthermore,thesefindings showa consistent pattern ofmore positive pricing of targetoperating loss carryforwards that can be used in the near term.

We estimate a system of seemingly unrelated regressions usingmodels (3) and (4) for each of the 51 trading days surrounding the an-nouncement date to test hypotheses H4 and H5. The estimation periodstarts 20 trading days before the announcement date and continuesuntil 30 trading days following the announcement date. Acquisitionprice per share (AP) is the dependent variable for model (3) and thetarget's market value per share (MV) is the dependent variable formodel (4). Similar to the results reported in Table 4, short-lived NOLs(NOLS) are defined as acquired NOLs that could be used in the firstyear and long-lived NOLs (NOLL) are defined as acquired NOLs that can-not be used in the first year. We summarize the results of these estima-tions in Fig. 2.

The NOLS findings fully support hypothesis H4. The market and par-ticipant pricing of acquired NOLS are significantly different over each of

Please cite this article as: Chiang, W.-C., et al., Pricing target NOLs in mergein Accounting, incorporating Advances in International Accounting (2014), h

the 20 trading days prior to the announcement (all p ≤ 0.008). TheNOLS findings also support, at least partially, the idea behind hypothesisH5. The market and participant pricing of acquired NOLS remain signifi-cantly different over each trading day through the 23rd trading day fol-lowing the announcement (all p ≤ 0.036). Afterwards, the differencesare not significant. However, the NOLL findings show that the participat-ing firms and the market price target NOLL similarly before and after theannouncement date. As a result, the NOLL findings do not support eitherhypothesis H4 or H5.

6. Discussion and conclusions

Our results offer several insights into the pricing of target NOLs bythe participating firms in M&As under the current tax law (TRA 86).First, our results show that aggregated target NOLs are not priced bythe participating firms in taxable acquisitions. This finding is consistentwith Henning et al.'s (2000) findingwhich concludes that acquirers paylittle for target NOLs in taxable acquisitions. It should be noted that thesample of Henning et al. (2000) primarily consists of step-up acquisi-tions (e.g., Categories 1 and 2 in Fig. 1)where target NOLs cannot be car-ried over to and used by the acquirer. However, the majority of taxableacquisitions examined in the current study are not step-up acquisitions(i.e., Category 3 acquisition in Fig. 1) and target NOLs can be transferredto and used by the acquirer, in general. Despite the essential differenceof transferability of target NOLs in the samples, both Henning et al.(2000) and the current study show that the participating firms do notassign value to target NOLs. Nevertheless, after we decompose targetNOLs into short-lived and long-lived NOLs, we find that the participat-ing firms assign positive value to target short-lived NOLs. Moreover,Hayn (1989, 141) notes that the market partially includes the value oftarget short-lived NOLs in the stock price, but the value is reducedwhen a taxable acquisition is announced. However, it is not clear

rs and acquisitions from the participating firms' perspective, Advancesttp://dx.doi.org/10.1016/j.adiac.2014.04.003

24 The coefficients ofNOLS andNOLL inmodels (3) and (4) are as follows. Themarket val-ue of target equity (MV) in model (4) is based on the 20th trading day prior to the an-nouncement date.

Variable Model (3) Model (4)

Coefficient p-Value Coefficient p-Value

NOLS + 24.17 (b0.0001) 6.92 (0.0030)NOLL ? −3.02 (0.0006) −1.99 (0.0040)

Table 4Ordinary least squares (OLS) estimations.

Variable Model (3)

Full sample Nontaxable subsample Taxable subsample

Coefficient p-Value Coefficient p-Value Coefficient p-Value

Intercept 17.53 (b0.0001) 28.57 (0.0095) 16.77 (b0.0001)NOLS + 15.87 (b0.0001) 11.25 (0.0424) 21.25 (b0.0001)NOLL ? −1.83 (0.0423) −1.32 (0.5882) −1.01 (0.2710)OLC + −2.18 (0.7289) 1.10 (0.4416) −1.10 (0.6144)TCC + −2.00 (0.8056) −2.52 (0.7615) −0.90 (0.6141)AODTA + 2.59 (b0.0001) 2.01 (0.0369) 1.48 (0.0130)VA − −0.03 (0.4843) −0.13 (0.4679) −0.09 (0.4592)DTL − −0.87 (0.0164) −0.67 (0.1825) −1.13 (0.0080)ABV + 1.43 (b0.0001) 1.67 (b0.0001) 1.28 (b0.0001)CAE + 0.58 (0.0602) −0.54 (0.7971) 0.71 (0.0622)NTAX ? 6.27 (0.0003)BOWN − −7.66 (0.0133) −14.14 (0.0495) −4.93 (0.0762)HOST + 6.14 (0.1036) 5.36 (0.2934) 3.92 (0.2308)CB + −1.07 (0.6450) 5.39 (0.2257) −2.90 (0.8418)TEN + 2.26 (0.1039) 3.99 (0.2284) 3.88 (0.0160)LEV ? 1.03 (0.2136) −7.16 (0.0428) 1.07 (0.1639)ROE ? 1.28 (0.0155) 1.88 (0.0357) 2.11 (0.0016)BKMV ? −10.47 (b0.0001) −28.34 (b0.0001) −7.63 (b0.0001)XRD + 3.80 (0.0002) 0.60 (0.3808) 4.59 (0.0002)SICi Included Included IncludedYEARj Included Included IncludedR2 0.5434 0.6073 0.5737Adj-R2 0.5193 0.5491 0.5376N 660 249 411

The dependent variable is acquisition price (AP). NOLS is the target net operating loss carryforwards available for acquirer usewithin thefirst year following the acquisition andNOLL is thetarget net operating loss carryforwards unavailable for acquirer usewithin the first year. OLC is the other target loss carryforwards, TCC is the target tax credit carryforwards, AODTA is thetarget's other deferred tax assets, VA is the target deferred tax asset allowance account, and DTL is the target deferred tax liabilities. ABV is the target net book value less net deferred taxesand CAE is the target current abnormal earnings. NTAX is one if the transaction is not taxable, BOWN is thepercentage of target stock ownedby the acquirer before the announcement date,HOST is one if the acquisition is hostile, CB is one if therewas a competing bidder, TEN is one if the acquisition startedwith a tender offer, LEV is the target leverage ratio, ROE is the target'sreturn on the market value of equity, BKMV is the target book to market value ratio, XRD is the target average R&D expense, SICi is an indicator for one-digit SIC code and YEARj is an in-dicator variable for year.Coefficients significant at the 0.05 level are reported in bold. The p-values for coefficients with expected signs are one-sided and the p-values for coefficients without expected signs aretwo-sided.

9W.-C. Chiang et al. / Advances in Accounting, incorporating Advances in International Accounting xxx (2014) xxx–xxx

whether this reductionmakes the value of target NOLs less positive, en-tirely valueless, or negative. While focusing on the participating firms'perspective, the current study clarifies this ambiguity, showing that tar-get short-lived NOLs are positively priced by the participating firms intaxable and non-taxable acquisitions.

Second, the coefficients of NOLS in Table 4 could provide operationalinformation to tentative participating firms. That is, tentative targetsand acquirers can incorporate this information in determining thevalue of target NOLs during their price negotiation process. Ratherthan discounting the amount of the overall target NOLs (Morris,2004), participating firms can simply assign the value of target NOLsbymultiplying the NOLS coefficient and the amount of target's deferredasset from short-lived NOLs. At least, this estimate offers a benchmarkfor the participating firms to negotiate the value of target NOLs inM&As. Furthermore, this practice could be applied to both taxable andnon-taxable acquisitions. While Hayn (1989) also shows that the mar-ket includes the value of target short-lived NOLs in the stock price, ourmeasurement provides an easier approach for practice purposes. Thatis, since the current study directly measures the pricing of the partici-pating firms, our estimates remain unchanged regardless of whetherthe stock market is efficient (Fama, 1970) or whether investors' cogni-tive processing biases exist (Barberis et al., 1998; Daniel et al., 1998).

Third, Haw et al. (1987) show that troubled firms with tax losscarryforwards gained a 33.7% acquisition premium from the marketwhile the acquisition premium for thosewithout tax loss carryforwardswas only 19.6%. The mean premium determined by the participatingfirms in our study is $10.63, acquisition price (AP) minus market valueof target's equity (MV) four weeks prior to the announcement date.We calculate the acquisition premium as a percentage of target marketvalue and find the mean acquisition premium ratios for the subgroupswith NOLs and without NOLs. The ratios are 55.99% and 55.07%,

Please cite this article as: Chiang, W.-C., et al., Pricing target NOLs in mergein Accounting, incorporating Advances in International Accounting (2014), h

respectively. The differences in mean acquisition premium ratios arenot significant (p = 0.7943). This result suggests that the participatingfirms do not give higher acquisition premiums to targets with NOLs.While our finding differs from that of Haw et al. (1987), the Haw et al.results were based on themarket reaction to the acquisition announce-ments. Also, theHaw et al. studywas conducted via information provid-ed under the Section 382 limitations of the TRA 76. However, our studyfocuses on the participating firms' pricing during the negotiation pro-cess, which usually occurs before the announcement date. Also, our re-search is conducted over information provided under the Section 382limitations of the TRA 86, which are much stricter than theSection 382 limitations of the TRA 76. The incremental restraint of theTRA 86 may mitigate some of the value of target NOLs in determiningthe acquisition premium by the participating firms.

Fourth, based on the coefficients ofNOLS andNOLL inmodels (3) and(4), we are able to calculate the portion of the acquisition premium at-tributable to target NOLs.24 Model (3) shows the value of target NOLsassigned by the participating firms in the M&A, which equals thevalue assigned to NOLS reduced by the value assigned to NOLL. Thevalue assigned to NOLS (NOLL) is computed as the mean NOLS (NOLL)

rs and acquisitions from the participating firms' perspective, Advancesttp://dx.doi.org/10.1016/j.adiac.2014.04.003

Table 5Sensitivity tests for short-lived NOL.

Variable Short-lived NOL as the multiples of annual section 382 limitation

1-Year amount 2-Year amount 3-Year amount 4-Year amount 5-Year amount

NOLSExpected sign + + + + +Coefficient 15.87 5.88 2.62 0.86 −0.23p-Value (b0.0001) (0.0114) (0.1122) (0.3219) (0.5537)

NOLLExpected sign ? ? ? ? ?Coefficient −1.83 −1.60 −1.31 −0.98 −0.62p-Value (0.0423) (0.0916) (0.1886) (0.3436) (0.5633)

Difference of NOLS and NOLL coefficientsExpected sign + + + + +NOLS-NOLL 17.71 7.48 3.93 1.84 0.40p-Value (b0.0001) (0.0045) (0.0577) (0.2058) (0.4262)

Coefficients significant at the 0.05 level are reported in bold. The NOLS p-values are one-sided and the NOLL p-values are two-sided.NOLS is the target net operating loss carryforwards available for acquirer use within the first years following the acquisition and NOLS is the target net operating loss carryforwards un-available for acquirer usewithin the first years following the acquisition. First years are alternatively defined as 1, 2, 3, 4, and 5 years following the acquisition. The other variables reportedin Table 3 are included in these estimations but suppressed in the presentation of the results.

10 W.-C. Chiang et al. / Advances in Accounting, incorporating Advances in International Accounting xxx (2014) xxx–xxx

times the coefficient of NOLS (NOLL). Therefore, the values assignedto NOLS and NOLL equal $3.14 (=$0.13 × 24.17) and $1.09 (=$0.36× 3.02) per share, respectively. Themean value of target NOLs assignedby the participating firms is $2.05 per share. Moreover, the mean valueof target NOLs assigned by the market in model (4) could be calculatedin a similarmanner and result in $0.18 per share. As a result, the meanpremium attributable to target NOLs is $1.87 (=$2.05–$0.18)per share. Although target NOLs comprise only 4.63% of targetnet book value ($0.49/$10.59), they account for 17.59% of the acquisi-tion premium ($1.87/$10.63) as determined by the participating firms.

Last, our findings indicate that the target long-lived NOLs (NOLL) arepriced similarly by the participating firms and the market before andafter the announcement date. However, the differences in the market

Notes:

1. Figure 2 displays the differences in the market pricing (MNOLs (NOLS) and long-lived NOLs (NOLL) on a daily bdate (MV-20) and continuing until 30 trading days follow(NOLS:MVt-AP) represents the difference between the mpricing of the same NOLS. The dashed line (NOLL:MVt-pricing of NOLL on day t and the particpant pricing of th

2. The differences in the market and participant pricing of level for the entire period up until 24 trading days (MV+days with significant differences in the market and partic

Fig. 2. Differences in market value pricing (MV) and participant pricing (AP) of target NOLs surusing models (3) and (4).

Please cite this article as: Chiang, W.-C., et al., Pricing target NOLs in mergein Accounting, incorporating Advances in International Accounting (2014), h

and the participant pricing of target short-lived NOLs (NOLS) exist be-fore the announcement date and extend well past the announcementdate. These findings suggest that additional information is gradually(rather than immediately) incorporated by the market after the an-nouncement date. It implies that, when an event study is employed toassess the market pricing of target NOLs around the announcementdate, the selected window period should be long enough to cover theentire market adjustment period. Otherwise, the cumulative abnormalreturns would not account for the complete effect of the information.For example, the window period in Hayn (1989, 150) starts 40 daysbefore the announcement date and ends on 10 days following theannouncement. Since our findings show that it may take the market24 days to incorporate the acquisition information, the cumulative

V) and participant pricing (AP) for both short-lived asis starting 20 tradings days before the announcement ing the announcement date (MV+30). The solid line

arket pricing of NOLS on day t and the particpant AP) represents the difference between the market e same NOLL.

the short-lived NOLs (NOLS) are significant at the 0.05 24) following the announcement date. There are no ipant pricing of the long-lived NOLs (NOLL).

rounding the announcement date as estimated in a set of seemingly unrelated regressions

rs and acquisitions from the participating firms' perspective, Advancesttp://dx.doi.org/10.1016/j.adiac.2014.04.003

11W.-C. Chiang et al. / Advances in Accounting, incorporating Advances in International Accounting xxx (2014) xxx–xxx

abnormal returns calculated in Hayn (1989) may not include the entiremarket adjustment to the information. As a result, the market pricingfound in Hayn (1989) may underrepresent the participating firmspricing.

Our study is subject to the normal limitations of archival research.We cannot saywith certainty that ourfindingswould hold over a differ-ent sample, over a different time period, or over changes in tax law. Wedo not have access to proprietary tax return information, so our NOLfindings are related to the sum of domestic, acquired, and foreignNOLs commonly reported as a single number in the tax footnotes, as op-posed to being related to NOLs listed on the targets' U.S. federal taxreturns. While this may be viewed as a limitation to the current study,it should be noted, as discussed above in footnote 18, that this factorshould not inflate our results.

Even with these limitations, the current study provides contri-butions to the extant literature by adding the participating firmsperspective on the pricing of target NOLs in M&As. Prior researchprimarily focuses on the market perspectives and consequently,the participating firms perspective has not been explicitly ad-dressed. However, our findings suggest that the market and theparticipating firms perspectives may not always match; thereby in-dicating the importance of considering this difference whenconducting future research in this area.

References

Amir, E., Kirschenheiter, M., & Willard, K. (1997). The valuation of deferred taxes.Contemporary Accounting Research, 14, 597–622.

Amir, E., & Sougiannis, T. (1999). Analysts' interpretation and investors' valuation of taxcarryforwards. Contemporary Accounting Research, 16, 1–33.

Auerbach, A. J., & Reishus, D. (1988a). The impact of taxation onmergers and acquisitions.In A. J. Auerbach (Ed.),Mergers and acquisitions (pp. 69–85). Chicago, IL: The Univer-sity of Chicago Press.

Auerbach, A. J., & Reishus, D. (1988b). Taxes and the merger decision. In J. C. Coffee, L.Lowenstein, & S. Rose-Ackerman (Eds.), Knights, raiders and targets: The impact ofthe hostile takeover (pp. 300–313). New York, NY: Oxford University Press.

Ayers, B. C., Lefanowicz, C. E., & Robinson, J. R. (2003). Shareholder taxes in acquisitionpremiums: The effect of capital gains taxation. Journal of Finance, 58, 2783–2801.

Barberis, N., Shleifer, A., & Vishny, R. (1998). A model of investor sentiment. Journal ofFinancial Economics, 49(3), 307–343.

Bayless, M. E., & Diltz, J.D. (1991). The relevance of asymmetric information to financingdecisions. Journal of Business Finance & Accounting, 18, 331–344.

Bruner, R. F. (2004). Applied mergers & acquisitions. Hoboken, NJ: John Wiley & Sons.

Please cite this article as: Chiang, W.-C., et al., Pricing target NOLs in mergein Accounting, incorporating Advances in International Accounting (2014), h

Daniel, K., Hirshleifer, D., & Subrahmanyam, A. (1998). Investor psychology and securitymarket under- and overreactions. Journal of Finance, 53, 1839–1886.

Erickson, M., &Wang, S. -W. (2000). The effect of transaction structure on price: Evidencefrom subsidiary sales. Journal of Accounting and Economics, 30, 59–97.

Fama, E. (1970). Efficient capital markets: A review of theory and empirical work. Journalof Finance, 25, 383–417.

Feltham, G. A., & Ohlson, J. A. (1995). Valuation and clean surplus accounting for operatingand financial activities. Contemporary Accounting Research, 11, 689–731.

Ginsburg, M.D., & Levin, J. S. (2006). Mergers, acquisitions, and buyouts: A transactionalanalysis of the governing tax, legal, and accounting considerations. New York, NY:Aspen Publishers.

Givoly, D., & Hayn, C. (1991). The aggregate and distributional effect of the Tax Reform Actof 1986 on firm valuation. Journal of Business, 64, 363–392.

Haw, I. -M., Pastena, V., & Lilien, S. (1987). The association between market-based mergerpremiums and firm's financial position prior to merger. Journal of Accounting, Auditing& Finance, 2, 24–42.

Hayn, C. (1989). Tax attributes as determinants of shareholder gains in corporate acquisi-tions. Journal of Financial Economics, 23, 121–153.

Henning, S. L., Shaw, W. H., & Stock, T. (2000). The effect of taxes on acquisition price andtransaction structure. The Journal of the American Taxation Association, 22, 1–17.

Hsu, K. H. Y., Kim, Y. S., & Song, K. R. (2009). The relation among targets' R&D activities,acquirers' returns, and in-process R&D in the US. Journal of Business Finance &Accounting, 36, 1180–1200.

Ibbotson (2008). Stocks, bonds, bills, and inflation 2008 yearbook (Valuation ed.). Chicago,IL: Ibbotson Associates.

Laamanen, T. (2007). On the role of acquisition premium in acquisition research. StrategicManagement Journal, 28, 1359–1369.

Landry, S. (1998). Evidence on the value-relevance of deferred tax assets and deferred taxliabilities. (Ph. D. Diss.). : University of Florida.

Lisowsky, P. (2009). Inferring U.S. tax liability from financial statement information. TheJournal of the American Taxation Association, 31, 29–63.

Malkiel, B. G. (2005). Reflections on the efficient market hypothesis: 30 years later. TheFinancial Review, 40, 1–9.

Mills, L. F., Newberry, K. J., & Novack, G. F. (2003). How well do Compustat NOL dataidentify firms with U.S. tax return loss carryovers? The Journal of the AmericanTaxation Association, 25, 1–17.

Moore, N. H., & Pruitt, S. W. (1987). The market pricing of net operating loss carryforwards:Implications of the tax motivations of mergers. The Journal of Financial Research, 10,153–160.

Morris, J. E. (2004). Accounting for M&A, equity, and credit analysts. New York, NY:McGraw-Hill.

Myers, S.C., & Majluf, N. S. (1984). Corporate financing and investment decisions whenfirms have information that investors do not have. Journal of Financial Economics,13, 187–221.

Plummer, E., & Robinson, J. R. (1990). Capital market evidence of windfalls from theacquisition of tax carryovers. National Tax Journal, 43, 481–489.

Scholes, M. S., Wolfson, M.A., Erickson, M., Maydew, E. L., & Shevlin, T. (2009). Taxes andbusiness strategy: A planning approach (4th ed.). Upper Saddle River, NJ: Pearson/Prentice Hall.

rs and acquisitions from the participating firms' perspective, Advancesttp://dx.doi.org/10.1016/j.adiac.2014.04.003