pricewaterhousecoopers india pvt ltd moneytree tm … · pricewaterhousecoopers india pvt ltd....

TRANSCRIPT

Technology Institute

This special reportprovides summary results of Q3 ’13, Q2 ’14, and Q3 ’14.

PricewaterhouseCoopers India Pvt Ltd

MoneyTreeTM India ReportQ3 2014Data provided by Venture Intelligence

www.pwc.com/globalmoneytreewww.pwc.in

PwC MoneyTreeTM India Report – Q3 ’14 2

1. Overview 3

2. Analysis of private equity investments

Total equity investments in PE-backed companies

Investments by industry

Investments by stage of development

Investments by region

Top 20 PE deals

4

4

5

7

8

9

3. Analysis of PE exits

Total PE exits

Exits by industry

Exits by type

Top five PE exits

10

10

11

12

13

4. Active PE firms 14

5. Sector focus: IT & ITeS sector

Total PE investments

Investments by stage of development

Investments by region

Investments by subsector

PE exits in the sector

15

15

17

18

19

20

6. Definitions

Contacts

21

22

Table of contents

PwC MoneyTreeTM India Report – Q3 ’14 3

1. Overview

Focussed on the future

Q3 ’14 saw 103 PE deals, valued at 3.01 billion USD. This represents a 4% increase over the PE deal value in Q2 ’14 and a 97% increase over the deal value in Q3 ’13.

It may be too simplistic to attribute the heightened activity to the ever-improving macro-economic environment, but the latter did play its part. Inflation was at 6.46% in September 2014, as compared to 9.84% during the same period last year and the cooling off in crude prices meant that fiscal deficit was broadly in control. More importantly, investors see a government keen on making investments into the country easier, and one that is focussed on enabling infrastructure for that purpose. This is great news for private equity investors looking to exit investments of four-plus-years vintage. Overall, FDI inflows over the last four months alone have exceeded 10.75 billion USD, and strengthening these inflows over the next few quarters could provide a further boost to the overall macro-economy.

The public markets have not looked back from the beginning of the year, and together with heightened strategic investor interest, provided composite exit opportunities to PE funds. In terms of fresh investments, PE investors have been selective and continue to take longer to consummate deals than ever before, the exception being the e-commerce sector. It stood out with deals worth 1,175 million USD during Q3 ’14, propelling an increasing number of investors to be convinced of its potential in India.

The IT & ITeS and healthcare sectors showed significant PE deal activity, followed by energy, education and engineering & construction. With the launch of the government’s Make in India programme and the proposed labour reforms, the manufacturing sector is also expected to gain investor interest. Thus PE investors are expected to turn their focus on manufacturing and infrastructure over a period of time.

Sanjeev Krishan Private Equity Industry Leader PwC India

PwC MoneyTreeTM India Report – Q3 ’14 4

2. Analysis of private equity investments

Total equity investments in PE-backed companies

Private equity investments in India have recorded an uninterrupted five-quarter upswing with 3.01 billion USD in the third quarter of the year across 103 deals, a moderate increase of 4% in value and a 3% drop in volume. In Q2 ’14, 2.91 billion USD was invested in 106 deals.

But the good news is that investments have doubled as compared to the same quarter last year, despite a 9% reduction in the volume. Q3 of the previous year saw 1.53 billion USD invested in 113 deals.

The Information technology and IT-enabled services (IT & ITeS) sector has made a comeback as the top sector, attracting 1.64 billion USD in 56 deals, more than half the total investments for the quarter. It is more than a two-fold jump as compared to the previous quarter and two and half times higher than the same period last year.

The healthcare & life sciences sector has emerged second in terms of investment value with investments worth 292 million USD in 11 deals, a 45% decline as compared to the previous quarter.

With regard to investments by stage of development, the growth stage has received the highest value of investments worth 1.84 billion USD across 34 deals.

0

1,000

2,000

3,000

4,000

5,000

6,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Quarter

Number of deals

Data provided by Venture Intelligence.

Q119

Q223

Q321

Q438

Q144

Q242

Q346

Q462

Q1100

Q287

Q3106

Q499

Q1118

Q295

Q3139

Q4178

Q1165

Q2108

Q3136

Q487

Q173

Q248

Q369

Q4102

Q195

Q284

Q3122

Q4104

Q1121

Q2131

Q3145

Q4125

Q1132

Q2120

Q3131

Q4108

Q1107

Q2124

Q3113

Q498

Q1133

Q2106

Q3103

Q4

576

357

845

2,038

1,776

2,768

1,9632,081

2,6552,587

807711

1,010

2,370

2,044

1,582

3,829

1,197

1,371

727

5,401

4,378

3,815

2,097

1,652

2,049

2,710

1,952

2,7042,211

3,864

1,229923

147242

464

1,528

1,177

4,834

2,1902,398

2,9113,013

Value of deals (in US$ Mn)

Total equity investments

Bangalore has emerged as the leader in terms of PE investments (both by value and volume of deals) in this quarter with an investment of 1.8 billion USD from 29 deals.

PwC MoneyTreeTM India Report – Q3 ’14 5

Investments by industry Q3 ’13, Q2 ’14 and Q3 ’14

The IT & ITeS sector attracted 1.64 billion USD in 56 deals which is more than half of the total investments. In Q2 ’14, total investment in the IT & ITeS sector was 746 million USD in 47 deals, while in Q3 ’13, it was 618 million USD from 41 deals.

In the healthcare and life sciences sector the total investment value was 292 million USD in 11 deals, a 45% decline as compared to the previous quarter. In Q2 ’14, the total deal value was 526 million USD across 12 deals, while in Q3 ’13, it was 196 million USD in 16 deals.

The energy and engineering and construction sectors have received 284 million USD (nine deals) and 181 million USD (two deals), respectively, ending the draught in these sectors during the last quarter. The energy sector received just 56 million USD in the last quarter, while engineering and construction got none.

The education sector has performed remarkably well, with the highest investment in recent times, 176 million USD in just four deals, a multifold jump from the previous quarters, followed by the manufacturing sector with 147 million USD.

“The decline in investment value in Q3 ’14 over the previous quarter is due to a fewer number of deals of ticket size over 100 million USD in this quarter as compared to the previous one. However, on a year-over-year basis, the investment value in healthcare and life sciences is up by almost 50%, with the average deal ticket size going up from 12.25 million to 26.54 million USD, thereby showing the continued uptrend in sector appetite to absorb larger sized deals.”

Dr Rana MehtaExecutive Director, Healthcare, PwC India

“Financial investors in the power and utilities space are now focussed almost entirely on clean technology where policy and regulatory frameworks have been remarkably positive and stable over the years. The central government’s focus on energy security and renewable energy is now finding support at the state level, with several announcing new policies and procurement.”

Kameswara RaoPower & Mining Leader, PwC India

“Renewed market sentiments following the formation of the new Government along with significantly improved overall business confidence resulted in strong results this quarter. In the technology sector, e-commerce businesses continued to attract investor interest driven by strong growth prospects. The e-commerce market continues to be a primarily minority stake market, with the majority of deal flow driven by growth-stage deals. Newer online e-commerce business segments such as classifieds, real estate, grocery and healthcare, have started to exhibit significant growth opportunities. Looking ahead, companies in m-commerce and digital technologies (SMAC) are expected to be in favour.”

Sandeep Ladda Technology Industry Leader, PwC India

PwC MoneyTreeTM India Report – Q3 ’14 6

After an excellent performance in the last quarter, the banking and financial sector dropped by 85% to 147 million USD from 958 million USD in the last quarter.

Investments by industries

Energy

Healthcare & life sciences

Textiles & garments

Information technology (IT)& IT-enabled services (ITeS)

Manufacturing

Others

Engineering& construction

Shipping & logistics

Banking, financial services& insurance

1,5001,000 2,0005000

$5

$0

$51$25

$10

$147$62

$57

$176$9

$51

$0$5$18

$0$77

$0

$181

$147

$232

$486$45

$144

$38

$0

$958$91

$292$526

$196

$284$56

$79

$1,640$746

$618

Travel & transport

Education

Fast moving consumergoods (FMCG)

Value of deals (in US$ Mn)

Q3 2013

Q2 2014

Q3 2014

Data provided by Venture Intelligence.

Note: ‘Others’ include other services, travel and transport, media and entertainment, hotels and resorts, education, fast-moving consumer goods, sports and fitness, agri-business, food and beverages, and retail.

PwC MoneyTreeTM India Report – Q3 ’14 7

Investments by stage of development Q3 ’13, Q2 ’14 and Q3 ’14

In Q3 ’14, most PE investors preferred the growth route as this stage received investments worth 1.8 billion USD in 34 deals. Late-stage investments were valued at 857 million USD in 15 deals during this quarter.

Investments by stage of development

0 500 1,000 1,500 2,000

Other

Pre-IPO

Early

PIPE

Growth

Late

Buyout

100

16

124

138

23

88

699151

1,833897

412

8571,158

266

8517

588Value of deals (in USD Mn)

Q3 2013

Q2 2014

Q3 2014

Data provided by Venture Intelligence.

Note: Definitions for the stage of development categories can be found in the ‘definitions’ section of this report.

Growth stage in the above graph includes both growth and growth-PE stages.

PwC MoneyTreeTM India Report – Q3 ’14 8

Investments by region Q3 ’13, Q2 ’14 and Q3 ’14

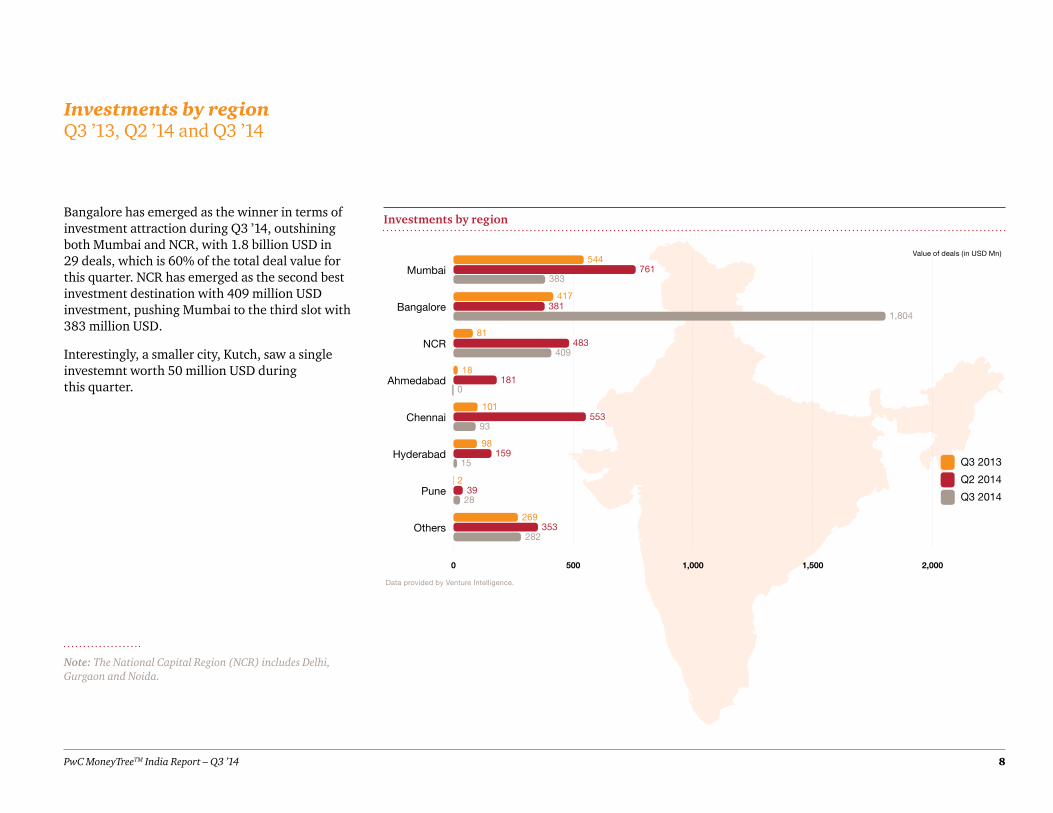

Bangalore has emerged as the winner in terms of investment attraction during Q3 ’14, outshining both Mumbai and NCR, with 1.8 billion USD in 29 deals, which is 60% of the total deal value for this quarter. NCR has emerged as the second best investment destination with 409 million USD investment, pushing Mumbai to the third slot with 383 million USD.

Interestingly, a smaller city, Kutch, saw a single investemnt worth 50 million USD during this quarter.

Investments by region

Note: The National Capital Region (NCR) includes Delhi, Gurgaon and Noida.

0 500 1,000 1,500 2,000

Others

Pune

Hyderabad

Chennai

Ahmedabad

NCR

Bangalore

Mumbai

Value of deals (in USD Mn)

93

159

553

0

2

269

101

28

282

39

353

98

15

18118

409483

81

1,804381

417

383761

544

Q3 2013

Q2 2014

Q3 2014

Data provided by Venture Intelligence.

PwC MoneyTreeTM India Report – Q3 ’14 9

Top 20 PE deals Q3 ’14

The top 20 deals comprised 78% of the total deal value in Q3 ’14. The top four deals constituted 48% of the total deal value. About 84% of the deals in this quarter are below the value of 50 million USD.

Top 20 PE deals in Q3 2014

Company Industry InvestorsDeal amount (in USD Mn)

Flipkart IT & ITeS Morgan Stanley, GIC, Tiger Global, Accel India, Iconiq Capital, DST Global, Others 1,000

GMR Holdings Eng & construction KKR 164

Manipal Global Education Services Education PremjiInvest 150

Narayana Hrudayalaya Healthcare & life sciences CDC Group 150

Bilt Paper Manufacturing IFC 100

Sterlite Power Grid Ventures Energy StanChart PE 83

Cholamandalam Investment and Finance Company BFSI Apax Partners 83

ReNew Wind Power Energy ADB, GEF 70

Hike IT & ITeS Tiger Global, Others 65

Syngene International Healthcare & life sciences India Value Fund 64

Quikr IT & ITeSWarburg Pincus, Norwest, Tiger Global, Matrix Partners India, Nokia Growth Partners, Omidyar Network, Kinnevik, Others

60

Snapdeal.com IT & ITeS Ratan Tata 50

Continuum Wind Energy Energy IFC 50

Spykar Lifestyle Textiles & garments Metmin Investments 50

Olacabs IT & ITeS Sequoia Capital India, Tiger Global, Matrix Partners India, Steadview 42

Delhivery Shipping & logistics Nexus Ventures, Multiples PE, Others 35

ACME Solar Energy Energy IFC 34

Freecharge.in IT & ITeS Sequoia Capital India, Ru-Net Holdings, Others 33

BigBasket IT & ITeS Helion Ventures, Ascent Capital, Zodius Capital, Lionrock Capital 33

Century Real Estate- SPV Hotels & resorts Blackstone 33Data provided by Venture Intelligence.

PwC MoneyTreeTM India Report – Q3 ’14 10

3. Analysis of PE exits

Total PE exits

The exit activity in the third quarter of 2014 has dropped by 18%, with a total value of 1.11 billion USD in 31 deals, as compared to the the previous quarter which saw 1.35 billion USD worth investment in 56 deals. During the same period last year, the total exit value was just 534 million USD in 25 deals.

With a single deal worth 234 million USD, the telecom sector dominated the exit space in this quarter followed by the manufacturing sector (229 mllion USD in two deals).

As a result of a surging stock market, almost 72% of the total exits happened through public market deals, valued at 801 million USD.

Total private equity exits

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Quarter

Number of deals

12 6 8

Q1 Q2 Q3 Q412

Q116

Q213

Q322

Q425

Q114

Q217

Q320

Q427

Q134

Q239

Q339

Q435

Q130

Q216

Q315

Q411

Q119

Q245

Q334

Q432

Q147

Q232

Q346

Q455

Q133

Q227

Q333

Q427

Q145

Q235

Q332

Q438

Q137

Q242

Q325

Q433 24 56 31

Q1 Q2 Q3 Q4

1,029

172

1,008

644

559

827854

612

834

202

592

279

599

1,212

927

235

787

68

449

1,905

683

1,323

280

936

416 385

886

3,063

1,131

1,320

1,5061,615

116

257

238

167534

1,941

1,133

1,294

416

1,107

1,349

Value of deals (in US$ Mn)

Data provided by Venture Intelligence.

PwC MoneyTreeTM India Report – Q3 ’14 11

Exits by industry Q3 ’13, Q2 ’14 and Q3 ’14

The telecom sector led the exits this quarter in terms of value, with a single deal worth 234 million USD. This sector didn’t witness any exits in the previous quarter or even in the same period last year. The manufacturing sector saw a drop of 40% in value, to 229 million USD in two deals, as compared to the previous quarter (381 million USD in five deals). In Q3 ’13, the sector saw five deals worth 77 million USD.

The BFSI and energy sectors have witnessed exit deals worth 188 million USD (five deals) and 142 million USD (two deals), respectively, whereas healthcare dropped to 40 million USD, an 88% fall as compared to the previous quarter.

Exits by industry

Note: Others include engineering and construction, shipping and logistics, textiles and garments, energy, other services, retail, food and beverages and hotels and resorts.

38

92

255

170

188

418

142

100

275

65

1230

515

0

229381

77

40323

17

0 100 200 300 400 500

Others

Banking, financial services& insurance

Information technology& IT-enabled services

Energy

Textiles & garments

Manufacturing

Healthcare & life sciences

Q3 2013

Q2 2014

Q3 2014

Value of deals (in US$ Mn)

Data provided by Venture Intelligence.

PwC MoneyTreeTM India Report – Q3 ’14 12

Exits by type Q3 ’13, Q2 ’14 and Q3 ’14

Public market sales have continued to be the preferred mode of exit with more than 72% of the total exit value coming from public deals (801 million USD in 20 deals). Strategic sales saw value worth 144 million USD in seven deals, followed by secondary sales (90 million USD in two deals).

This quarter witnessed one IPO worth 37 million USD.

Exits by type

Note: N/A indicates this information has not been publicly disclosed.

Note: Definitions of the types of exit can be found in the ‘definitions’ section of this report.

3511

144

176

170142

3700

90373

121

801795

95

0 200 400 600 800 1,000

Buyback

Strategic sale

IPO

Secondary sale

Public market sale

Q3 2013

Q2 2014

Q3 2014

Value of deals (in US$ Mn)

Data provided by Venture Intelligence.

PwC MoneyTreeTM India Report – Q3 ’14 13

Top five PE exits Q3 ’14

The top five exits comprised 65% of the total exit value in Q3 ’14.

Top 5 PE exits in Q3 2014

Company Industry InvestorsDeal amount (USD Mn)

Idea Cellular Telecom Providence 234

Mahindra & Mahindra Manufacturing Goldman Sachs 227

Petronet LNG Energy ADB 117

Repco Home Finance BFSI Carlyle 79

IndusInd Bank BFSI General Atlantic 66 Data provided by Venture Intelligence.

PwC MoneyTreeTM India Report – Q3 ’14 14

4. Active PE firms

Based on the volume of deals, Sequoia Capital has emerged as the most active investor for Q3 ’14.

The most active PE investors in the third quarter of 2014 include the following:

Most active PE investors in Q3 ’14

Investors No of deals

Sequoia Capital India 7

Nexus Ventures 6

Matrix Partners India 6

Helion Ventures 5

Kalaari Capital 5

Tiger Global 5

IFC 4

SAIF 4

Qualcomm Ventures 4

Omidyar Network 3

Faering Capital 3

Blume Ventures 3

IDG Ventures India 3

India Quotient 3

Inventus Capital Partners 3 Data provided by Venture Intelligence.

Investors No of deals

Accel India 3

ADB 2

Infuse Ventures 2

Saama Capital 2

Mayfield 2

Parampara Capital 2

Bessemer 2

Ratan Tata 2

Norwest 2

Zodius Capital 2

IvyCap Ventures 2

Steadview 2

Apax Partners 2

JAFCO Asia 2

WestBridge 2

* Number of deals includes both single and co-investments by PE firms. In cases where two or more firms have invested in a single deal, it is accounted as one deal for each of the firms.

PwC MoneyTreeTM India Report – Q3 ’14 15

5. Sector focus IT & ITeS sector

Total PE investments

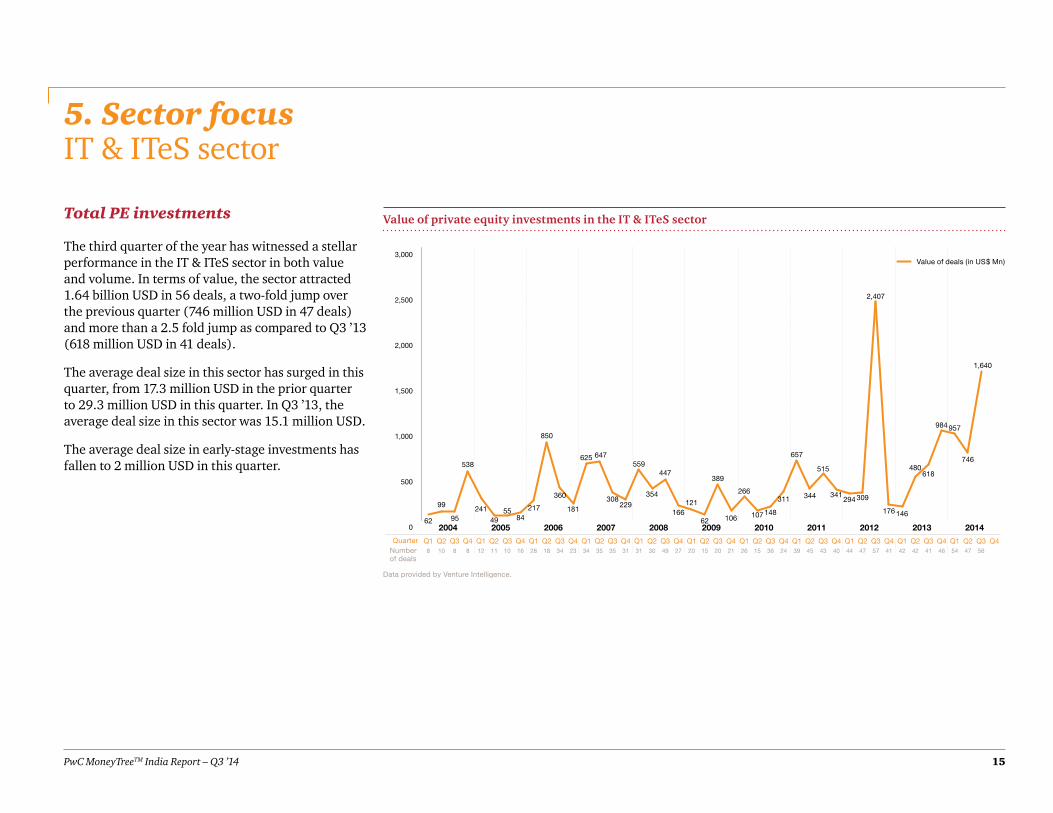

The third quarter of the year has witnessed a stellar performance in the IT & ITeS sector in both value and volume. In terms of value, the sector attracted 1.64 billion USD in 56 deals, a two-fold jump over the previous quarter (746 million USD in 47 deals) and more than a 2.5 fold jump as compared to Q3 ’13 (618 million USD in 41 deals).

The average deal size in this sector has surged in this quarter, from 17.3 million USD in the prior quarter to 29.3 million USD in this quarter. In Q3 ’13, the average deal size in this sector was 15.1 million USD.

The average deal size in early-stage investments has fallen to 2 million USD in this quarter.

Value of private equity investments in the IT & ITeS sector

0

500

1,000

1,500

2,000

2,500

3,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Quarter

Number of deals

Data provided by Venture Intelligence.

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

241

49 84

850

360

625

181

647559

447

62

121

389

148107106

657

16621755

229308

354 266 341 309

515

311 344 294

2,407

176

538

95

99

62

618480

146

984 957

1,640

746

Value of deals (in US$ Mn)

318 10 8 8 12 11 10 16 28 18 34 23 34 35 35 31 30 49 27 20 15 20 21 26 15 36 24 39 45 43 40 44 47 57 41 42 42 41 46 54 47 56

PwC MoneyTreeTM India Report – Q3 ’14 16

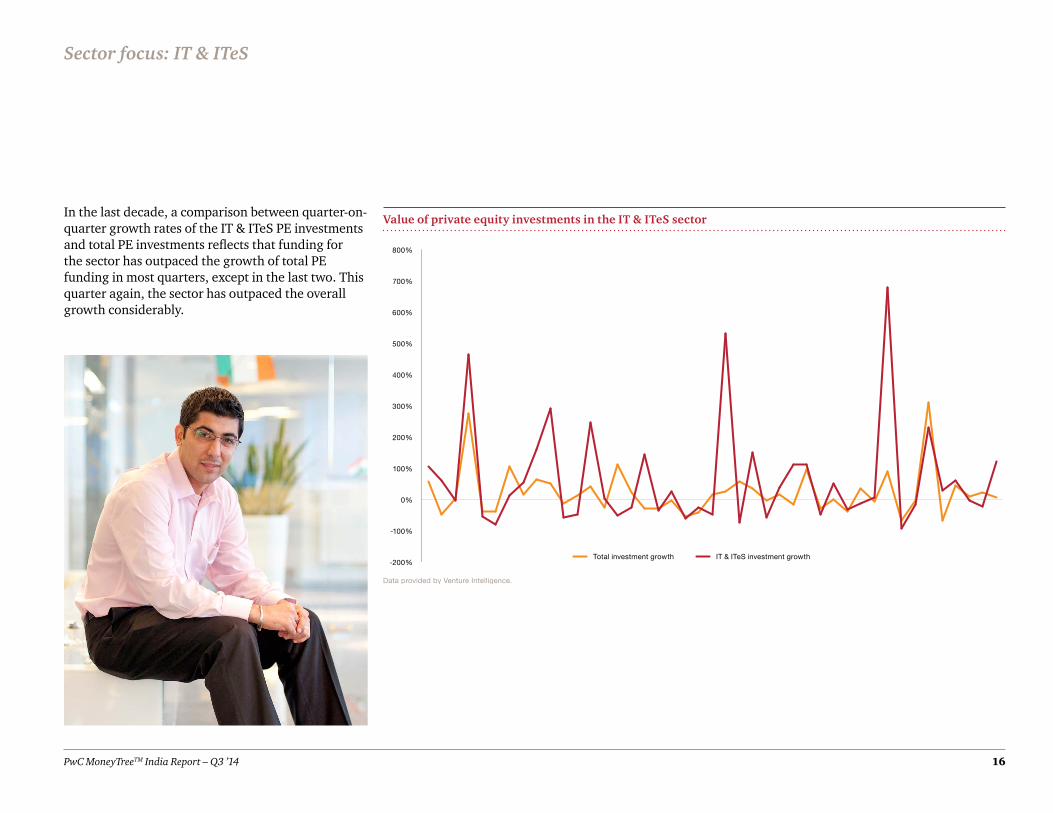

In the last decade, a comparison between quarter-on-quarter growth rates of the IT & ITeS PE investments and total PE investments reflects that funding for the sector has outpaced the growth of total PE funding in most quarters, except in the last two. This quarter again, the sector has outpaced the overall growth considerably.

Value of private equity investments in the IT & ITeS sector

Sector focus: IT & ITeS

-200%

-100%

0%

100%

200%

300%

400%

500%

600%

700%

800%

Total investment growth IT & ITeS investment growth

Data provided by Venture Intelligence.

PwC MoneyTreeTM India Report – Q3 ’14 17

Investments by stage of development Q3 ’13, Q2 ’14 and Q3 ’14

Investments in the growth stage have outpaced all other modes in this quarter, seeing 92% of the total value. Growth investments in this quarter stood at 1.51 billion USD, a three-fold increase from the previous quarter and a six-fold growth over Q3 ’13.

There was neither a buy-out, nor a pipe deal in the technology sector in this quarter. Only three late-stage investments were valued at 70 million USD.

IT & ITeS investments by stage of development

Sector focus: IT & ITeS

0 500 1,000 1,500 2,000

Pre-IPO

Early

PIPE

Growth

Late

Buyout

000

102

0

64

43

190

1,506506

245

70117

15

03

315

Q3 2013

Q2 2014

Q3 2014

Value of deals (in US$ Mn)

Data provided by Venture Intelligence.

PwC MoneyTreeTM India Report – Q3 ’14 18

Investments by region Q3 ’13, Q2 ’14 and Q3 ’14

Bangalore has continued its run as the best IT investment destination in this quarter, attracting 72% of the total investments in the sector during this quarter. The city has attracted 1.18 billion USD in 17 deals, followed by Mumbai (211 million USD in 15 deals) and NCR (144 million USD in nine deals).

IT & ITeS investments by region

Sector focus: IT & ITeS

5

35

17

10

0

4

16

0

63

0

13

2

28

3214

144224

6

1,179321

235

211104

341

0 200 400 600 800 1,000 1,200 1,400

Others

Kochi

Pune

Hyderabad

Chennai

NCR

Bangalore

Mumbai

Q3 2013

Q2 2014

Q3 2014

Value of deals (in US$ Mn)

Data provided by Venture Intelligence.

PwC MoneyTreeTM India Report – Q3 ’14 19

Investments by subsector Q3 ’13, Q2 ’14 and Q3 ’14

The online services subsector has received almost 85% of total deal value, with 1.39 billion USD in 28 deals, followed by mobile services (138 million USD in nine deals) and enterprise software (79 million USD in 13 deals).

None of the other subsectors received considerable investments in this quarter.

IT & ITeS investments by subsector

Sector focus: IT & ITeS

79

29

48

4

0

1

12

7

25

0

0

6

138

300

33333

228

3

1,385579

262

0 200 400 600 800 1,000 1,200 1,400 1,600

Others

Networkingtechnology

Mobileservices

Enterprisesoftware

IT products

IT services

ITeS—BPO

Onlineservices

Q3 2013

Q2 2014

Q3 2014

Value of deals (in US$ Mn)

Data provided by Venture Intelligence.

PwC MoneyTreeTM India Report – Q3 ’14 20

PE exits in the sector Q3 ’13, Q2 ’14 and Q3 ’14

The exit activity in the IT & ITeS sector was meagre this quarter, with the sector seeing only five exits valued at just 38 million USD, an 85% drop from the previous quarter and a 86% drop from the same period last year. In Q2 ’14, there were 13 exits worth 255 million USD, while Q2 ’13 saw exits worth 275 million USD in nine deals.

All the exits in this sector were through strategic sale in this quarter.

Total private equity exists in the IT & ITeS sector

Sector focus: IT & ITeS

0

500

1,000

1,500

2,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Quarter

Number of deals

6 4 3

Q1 Q2 Q3 Q410

Q15

Q25

Q38

Q49

Q16

Q24

Q311

Q412

Q18

Q220

Q38

Q47

Q15

Q25

Q33

Q43

Q16

Q25

Q310

Q48

Q111

Q25

Q33

Q411

Q17

Q27

Q34

Q46

Q111

Q27

Q36

Q48

Q16

Q211

Q39

Q46 7 13 5

Q1 Q2 Q3 Q4

26

29 57

377

13076

103

244

19

1125

37

161

113153

55

323

12

315

671

55

289

67

348

79 87169

1,717

577

129

1,053

250

7222176

93275

540

230

408

158 38

255

Value of deals (in US$ Mn)

Data provided by Venture Intelligence.

PwC MoneyTreeTM India Report – Q3 ’14 21

6. Definitions

Stages of development

Early stage: This refers to the first or second round of institutional investments in companies that adhere to the following:

• Less than five years old

• Not part of a larger business group

• Investment is less than 20 million USD

Growth stage: This refers to investments of less than 20 million USD. Also, investments meeting the following criteria are considered in the growth stage:

• Third or fourth round funding of institutional investments

• First or second round of institutional investments for companies that are more than five years old and less than 10 years old or spin-outs from larger businesses

Growth stage-PE: This includes the following:

• First or second round of investments worth 20 million USD or more

• Third or fourth round funding for companies that are more than five years old and less than 10 years old or subsidiaries or spin-outs of larger businesses

• Fifth or sixth rounds of institutional investments

Types of PE exits

Buyback: This includes the purchase of the PE or VC investors’ equity stakes by either the investee company or its founders or promoters.

Strategic sale: This includes the sale of the PE or VC investors’ equity stakes (or the entire investee company itself) to a third-party company (which is typically a larger company in the same sector).

Secondary sale: Any purchase of the PE or VC investors’ equity stakes by another PE or VC investors constitutes secondary sale.

Public market sale: This includes the sale of the PE or VC investors’ equity stakes in a listed company through the public market.

Initial public offering (IPO): This includes the sale of PE or VC investors’ equity stake in an unlisted company through its first public offering of stock.

Late stage: This comprises the following:

• Investment in companies that are a decade old

• Seventh or later rounds of institutional investments

PIPEs: The following constitute as PIPEs:

• PE investments in publicly listed companies via preferential allotments or private placements

• Acquisition of shares by PE firms via the secondary market

Buyout: This is an acquisition of controlling stake via purchase of stakes of existing shareholders.

Buyout–large: This includes buyout deals of 100 million USD or more in value.

Other: This includes PE investments in special purpose vehicle (SPV) or project-level investments.

PwC MoneyTreeTM India Report – Q3 ’14 22

www.pwc.com/globalmoneytreewww.pwc.in

Contacts

Sandeep Ladda Leader, Technology [email protected]

Sanjeev Krishan Leader, Private Equity [email protected]

This report was researched and written by the following:

Pradyumna Sahu Director, Technology [email protected]

Sibi Sathyan Knowledge Manager, Private Equity [email protected]

For more information

If you would like to discuss how these findings might impact your business or your future strategy, please reach out to any of our technology industry leaders listed below.

Raman Chitkara Global Technology Leader 1 408 817 3746 [email protected]

Rod Dring – Australia Werner Ballhaus – Germany Yury Pukha – Russia 61 2 8266 7865 49 211 981 5848 7 495 223 5177 [email protected] [email protected] [email protected]

Estela Vieira – Brazil Sandeep Ladda – India Greg Unsworth – Singapore 55 1 3674 3802 91 22 6689 1444 65 6236 3738 [email protected] [email protected] [email protected]

Christopher Dulny – Canada Masahiro Ozaki – Japan Philip Shepherd – UAE 416 869 2355 81 3 5326 9090 97 1 43043501 [email protected] [email protected] [email protected]

Jianbin Gao – China Hoonsoo Yoon – Korea Jass Sarai – UK 86 21 2323 3362 82 2 709 0201 44 0 1895 52 2206 [email protected] [email protected] [email protected]

Pierre Marty – France Ilja Linnemeijer – The Netherlands Tom Archer – US 33 1 5657 58 15 31 88 792 4956 1 408 817 3836 [email protected] [email protected] [email protected]

About PwC’s Technology Institute

The Technology Institute is PwC’s global research network that studies the business of technology and the technology of business with the purpose of creating thought leadership that offers both fact-based analysis and experienced-based perspectives. Technology Institute insights and viewpoints originate from active collaboration between our professionals across the globe and their first-hand experiences working in and with the technology industry.

About PwC

PwC firms help organisations and individuals create the value they are looking for. We are a network of firms in 157 countries with more than 195,000 people who are committed to delivering quality in assurance, tax and advisory services. Find out more and tell us what matters by visiting us at www.pwc.com.

www.pwc.com

PricewaterhouseCoopers and Venture Intelligence have taken responsible steps to ensure that the information contained in the MoneyTreeTM report has been obtained from reliable sources. However, neither of the parties can warrant the ultimate validity of the data obtained. Results are updated periodically. Therefore, all data is subject to change at any time. Before making any decision or taking any action, you should consult a competent professional adviser.

© 2014 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see http://www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. MW-15-0805PwC MoneyTreeTM India Report – Q3 ’14