presents taxation of first and third party snts with vincent j. russo, j.d., ll.m. cela, cap...

TRANSCRIPT

Presents

Taxation of First and Third Party SNTs

With

Vincent J. Russo, J.D., LL.M. CELA, CAPSponsored by:

Tuesday, March 25, 2014

What We Will Cover

• Understanding • Special Needs Trusts• Trust Taxation and the Grantor

Trust Rules

• Taxation of • First Party SNTs• Third Party SNTs• Tax Issues

• Tax Traps and Tips

2Vincent J. Russo & Associates, P.C. ©2014

3

Special Needs Planning: Trusts

• Exempt Trusts Under OBRA 1993• First Party Special Needs Trusts• D4a or Payback trust

• Pooled Trusts• Asset and/or Income

• Third Party Special Needs Trusts • Supplemental Needs

Vincent J. Russo & Associates, P.C. ©2014

4

First Party Special Needs Trust

• Vehicle to Manage Assets and Income for a Person with Special Needs

• Income and Assets Available for the Benefit of the Person with Special Needs

• Maximizes and Maintain Government Benefits• SSI and Medicaid

• Pay Back to State for Medicaid on Termination of Trust

Vincent J. Russo & Associates, P.C. ©2014

5

Third Party Supplemental Needs Trust

• Vehicle to Manage Assets and Income for a Person with Special Needs

• Income and Assets Available for the Benefit of the Person with Special Needs

• Maximize and Maintain Government Benefits• SSI and Medicaid• No Pay Back to State for Medicaid

Vincent J. Russo & Associates, P.C. ©2014

6

Special Needs Trust:Tax Issues

• Income Tax Rates• Trust versus Individual

• Qualifying for Grantor Trust Status• As to Income and Principal

• Step Up in Basis

• Filing of Tax Returns• Trust and Personal Tax Returns• Who reports the Trust Income

Vincent J. Russo & Associates, P.C. ©2014

7

2014 Tax Bracket

Tax Rate Single Married-Joint Estate or Trust10% up to $9,075 up to $18,150 N/A

15% $9,076 - $18,151 up to $2,500

36,900 73,800

25% $36,901 - $73,801 - $2,501 -

89,350 148,850 5,800

28% $89,351 - $148,851 - $5,801-

186,350 226,850 8,900

33% $186,351 - $226,851 - $8,901 -

405,100 405,000 12,150

35% 405,101 - 406,750 405,101 – 457,60039.6% over $406,750 over $457,600 over $12,150

Vincent J. Russo & Associates, P.C. ©2014

8

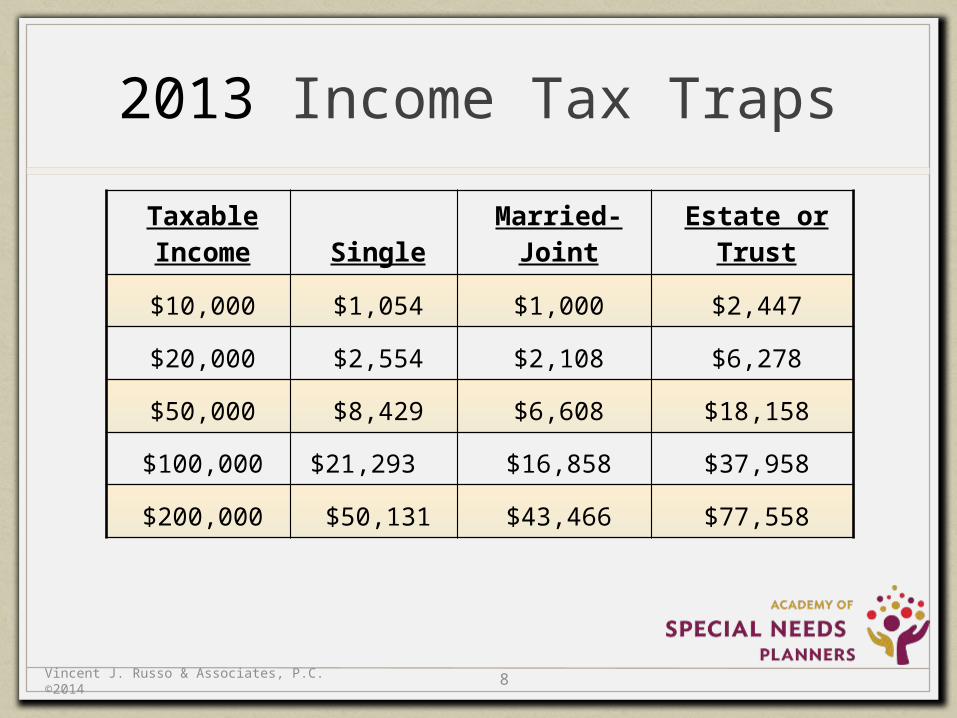

2013 Income Tax Traps

TaxableIncome Single Married- Joint Estate or Trust

$10,000 $1,054 $1,000 $2,447

$20,000 $2,554 $2,108 $6,278

$50,000 $8,429 $6,608 $18,158

$100,000 $21,293 $16,858 $37,958

$200,000 $50,131 $43,466 $77,558

Vincent J. Russo & Associates, P.C. ©2014

9

Income Taxes: Trust Income

• Must be Reported on the Trust Income Tax Return (unless an exception is met)

• If Exception is met, • All income may be reported on the grantor’s personal

income tax return• All or part of the income may be reported on the

beneficiary’s personal income tax return• All or part of the income may be reported on the trust

income tax return

Vincent J. Russo & Associates, P.C. ©2014

10

Income Taxes: Examples of Grantor Trusts

• All • First Party Special Needs Trust• Revocable Third Party Special Needs Trusts

• Optional • Third Party Irrevocable Special Needs Trust

Vincent J. Russo & Associates, P.C. ©2014

11

Income Taxes: Grantor Trust(Taints)

• Reversionary Interest in the Trust (IRC §673)

• Grantor may Exchange Property of Equivalent Value in Non-Fiduciary Capacity (IRC §675)

• Use Trust Income to Pay Premiums of Insurance on Life of Grantor or Grantor’s Spouse (IRC §677)

Vincent J. Russo & Associates, P.C. ©2014

12

Income Taxes: Grantor Trust(Taints)

• Power to Revoke (IRC §676)• Do not use the Power to Revoke if a First Party Special

Needs Trust (where the beneficiary is accessing or seeking to qualify for Supplemental Security Income and/or Medicaid)

• Income Payable by Grantor or Non-Adverse Party (trustee) to the grantor (IRC §677)• Without the consent of an Adverse Party (Trustee) • any person who has a substantial beneficial interest in the

trust which would be adversely affected (IRC §672)

Vincent J. Russo & Associates, P.C. ©2014

13

Obtaining Grantor Trust Status Over Principal

• Important when Dealing with Appreciated Assets• Will allow the Grantor to Maintain IRC § 121 exemption

on sale of primary residence• Ensures that individual capital gains tax rates apply when

trust assets are sold• For example, Sale of Stock and Bonds

Vincent J. Russo & Associates, P.C. ©2014

14

Obtaining Grantor Trust Status Over Principal

• Grantor Trust Powers that give Grantor Trust Status with Respect to Principal • Power to substitute assets of equivalent value or power to

add charitable beneficiaries

• Powers within the Internal Revenue Code which cause Estate Tax Inclusion • § 2036(a)(2) – testamentary power of appointment to

change beneficiaries

Vincent J. Russo & Associates, P.C. ©2014

15

Income Taxes: Non-Grantor Trusts

• All• Testamentary Trusts• Qualified Disability Trust

• Optional• Third Party Irrevocable Special Needs Trusts

Vincent J. Russo & Associates, P.C. ©2014

16

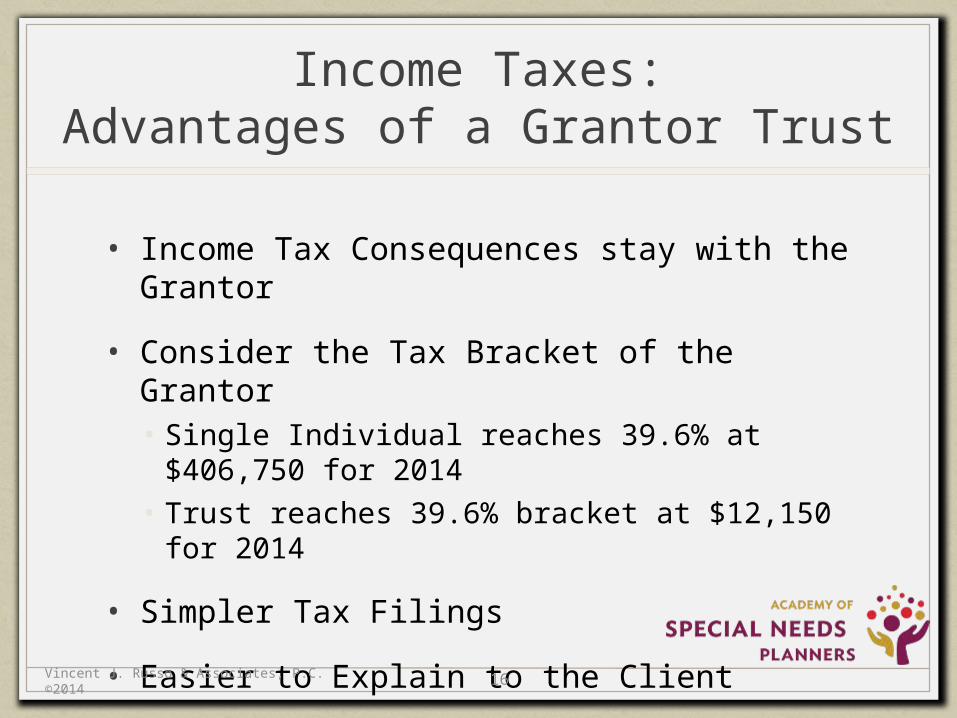

Income Taxes:Advantages of a Grantor Trust

• Income Tax Consequences stay with the Grantor

• Consider the Tax Bracket of the Grantor• Single Individual reaches 39.6% at $406,750 for 2014• Trust reaches 39.6% bracket at $12,150 for 2014

• Simpler Tax Filings

• Easier to Explain to the Client

Vincent J. Russo & Associates, P.C. ©2014

17

Income Taxes: Advantages of a Non-Grantor Trust

• Grantor does not have to come up with funds to pay tax on “phantom income”

• Spread out the income tax consequences

• Beneficiary who receives the income pays the income tax in beneficiary’s tax bracket

• Higher exemption amount as a “Qualified Disability Trust”

Vincent J. Russo & Associates, P.C. ©2014

18

Income Taxes: Disadvantages of a Non-Grantor Trust

• If not Careful, Higher Overall Taxes

• Beneficiary does not Understand that they need to come up with Income Tax Payments

• More Complicated• Trustee needs to pay attention to calendar year-end

distributions

Vincent J. Russo & Associates, P.C. ©2014

19

Income Taxes: What The Grantor Needs To Know

• Tax Impact on the Trust, the Grantor and Beneficiaries

• Filing of Income Tax Returns• Trust• Grantor• Beneficiary

• Impact on Gift and Estate Taxes

Vincent J. Russo & Associates, P.C. ©2014

20

Income Taxes: What the Trustee Needs To Know

• Fiduciary Record Keeping

• Year End Income Tax Planning• Sixty Five Day Rule

• Filing of Tax Returns• Due April 15th (for Tax Years ended 12/31)• Five-Month Extension Available• Extension of time to file (not to pay)

Vincent J. Russo & Associates, P.C. ©2014

21

Federal Uniform Gift and Estate Tax System for 2014

• $5,340,000 Federal Exemption which can be used either during Lifetime and/or at Death• If during lifetime, offsets taxable gifts• If at death, offsets estate tax on taxable estate (including

prior taxable gifts)• Note : taxable gifts are gifts in excess of the annual

exclusion amount which has varied in years past (currently $14,000 in 2013-2014)

Vincent J. Russo & Associates, P.C. ©2014

22

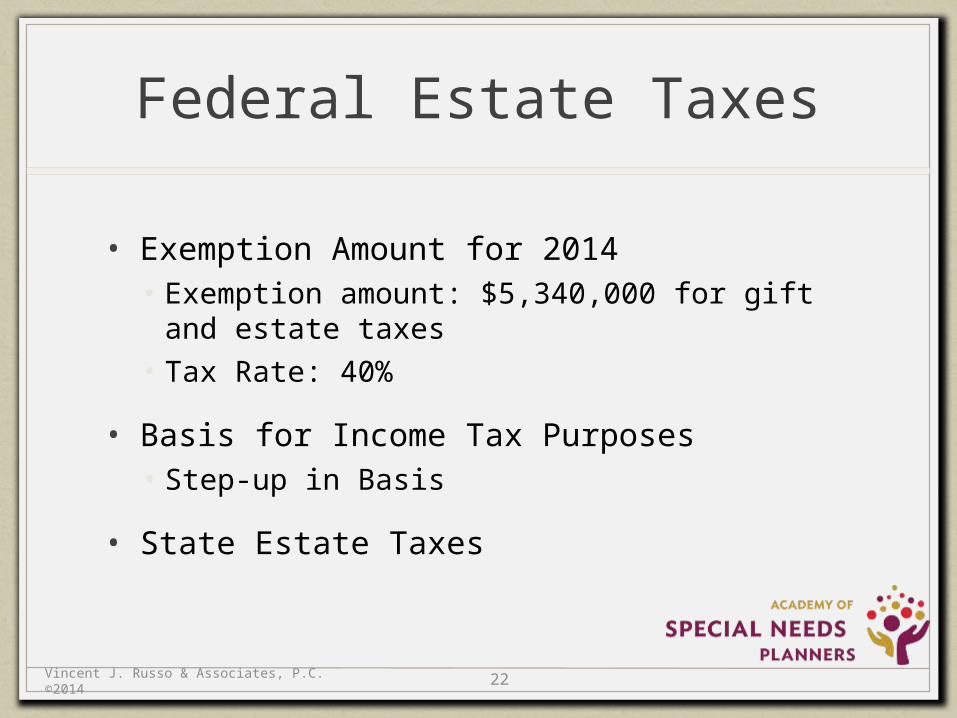

Federal Estate Taxes

• Exemption Amount for 2014• Exemption amount: $5,340,000 for gift and estate taxes• Tax Rate: 40%

• Basis for Income Tax Purposes • Step-up in Basis

• State Estate Taxes

Vincent J. Russo & Associates, P.C. ©2014

23

Trusts in a Special Needs Practice

• First Party Special Needs Trust

• Pooled Trusts

• Third Party Special Needs Trust

Vincent J. Russo & Associates, P.C. ©2014

24

First Party Special Needs Trusts: Taxation

• Gift Taxation on Funding• Incomplete

• Income Taxation on Income Generated• Grantor Trust

• Estate Taxation on Demise of Beneficiary• Included in the Estate

Vincent J. Russo & Associates, P.C. ©2014

25

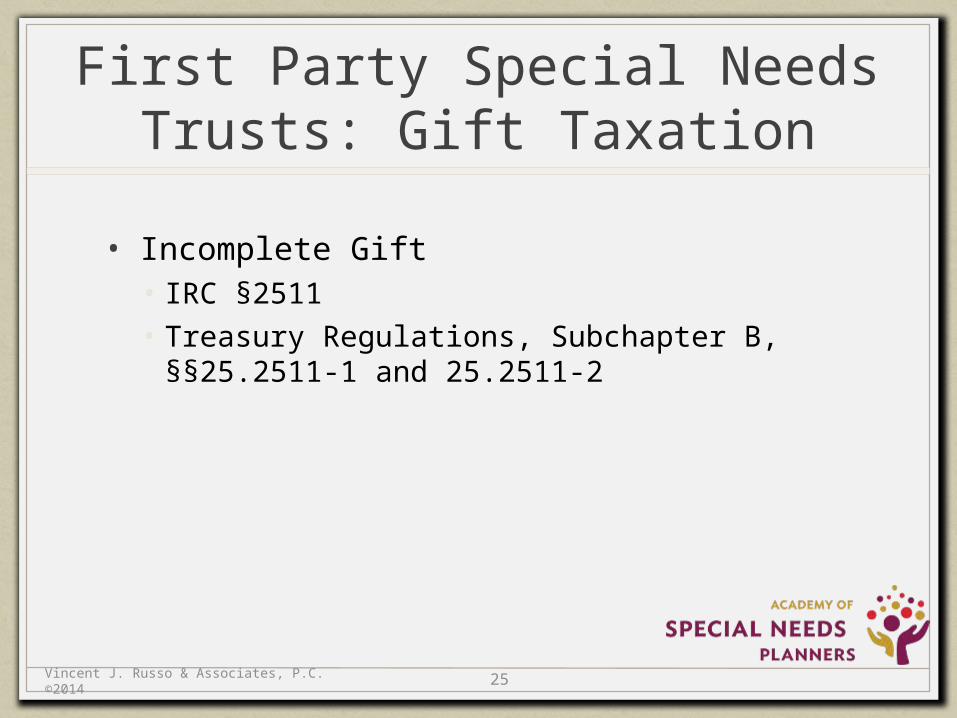

First Party Special Needs Trusts: Gift Taxation

• Incomplete Gift • IRC §2511• Treasury Regulations, Subchapter B, §§25.2511-1 and

25.2511-2

Vincent J. Russo & Associates, P.C. ©2014

26

First Party Special Needs Trusts: Income Taxation

• Who is the Grantor? • The Beneficiary• Revenue Ruling 83-25

• Kiddie Tax Issue

• Who Pays the Income Tax? • Grantor if Grantor Trust • IRC §§ 671- 677• IRC §673 – Reversionary Interest

Vincent J. Russo & Associates, P.C. ©2014

27

First Party Special Needs Trusts: Estate Taxation

• Included in the Estate of the Grantor/Beneficiary• IRC §2036(a)(1) • TAM 9506004• Code §§2036 and 2038

Vincent J. Russo & Associates, P.C. ©2014

28

First Party Special Needs Trusts: Estate Taxation

• Consider: Valuation of Future Periodic Payments on Structured Settlements

• Three Methods of Valuation• Commercial Annuity• § 7520 Rate• Willing Seller and Willing Buyer will pay for the future

periodic payments

Vincent J. Russo & Associates, P.C. ©2014

29

SNTs - Gift and Estate Taxes: PLR 9437034

• Decedent Created an Irrevocable Trust

• Funded with Structured Settlement Proceeds with a Guaranteed Payment

• Special Needs Trust Created to be the Recipient of the Settlement Proceeds

• SNT Provisions• For sole benefit of Decedent• Testamentary Special Power of Appointment

Vincent J. Russo & Associates, P.C. ©2014

30

SNTs - Gift and Estate Taxes: PLR 9437034

• Included in Estate for Estate Tax Purposes• IRC §2038(a)(1) • Decedent has the right at death to alter disposition of

trust assets• Decedent has the right at death to alter disposition of trust

assets

• Incomplete Gift • IRC Reg. §25.2511-2• Donor retained special power to change the enjoyment of

the trust assets

Vincent J. Russo & Associates, P.C. ©2014

31

Income Tax Traps (Issue Awareness)

• Income Tax Brackets

• Kiddie Tax

• Estimated Tax Payments

• State Income Tax Return Requirements

Vincent J. Russo & Associates, P.C. ©2014

32

Pooled Trusts under OBRA

• Established by a Not for Profit

• Sub-Account for the Sole Benefit of a Person who is Disabled

• Pay Back to the State unless the Remaining Funds are held by the Trust or for the Benefit of the Charity • 42 U.S.C. § 1396p (d)(4)(c)

Vincent J. Russo & Associates, P.C. ©2014

33

Pooled Trusts: Income Taxes

• No Definitive Authority• Income Taxes• Treas. Reg. §1.642(c)-5• Review the Master Pooled Trust and Joinder Agreement• Income on Sub-Account reported as a:• Grantor or Complex Trust

• Gift Taxes• Incomplete gift on funding of the sub-account

• Estate Taxes• Included in the Estate of the participant

Vincent J. Russo & Associates, P.C. ©2014

34

Inter Vivos Third Party Supplemental Needs Trusts

• Gift Taxation• Complete or Incomplete• Revocable or Irrevocable Trusts

• Income Taxation to Settlor, Trust, Beneficiary• Grantor Trust or Complex Trust

• Estate Taxation• Included or Not Included in the Estate

Vincent J. Russo & Associates, P.C. ©2014

35

Inter Vivos Third Party Supplemental Needs Trusts

• Grantor Trust for Income Tax purposes• Power to Remove Trustee• Discharge Obligation of Support• Retention of Certain Administrative Powers

Vincent J. Russo & Associates, P.C. ©2014

36

Inter Vivos Third Party Supplemental Needs Trusts

• Income Taxation as a Complex Trust• Retained Income Trust• Distributed Income – Beneficiary• Qualified Disability

• Trust Issues• Distributable Net Income• End of Year Distributions

Vincent J. Russo & Associates, P.C. ©2014

37

Inter Vivos Third Party Supplemental Needs Trust

• Tax Consequences• Does the grantor have a taxable estate?• When will the Trust be funded?• Non – Taxable Estate• Grantor Trust for Income Tax Purposes• Incomplete Gift• Included in Estate for Estate Tax Purposes

• Taxable Estate• Income / Gift / Estate Tax Consequences

Vincent J. Russo & Associates, P.C. ©2014

38

Third Party Supplemental Needs Trusts: Taxes

• Gift• Complete versus Incomplete• Control by drafting trust provisions

• Income• Grantor Trust• Non-Grantor Trust• Simple Trust or Complex Trust• Conversion from Grantor Trust

Vincent J. Russo & Associates, P.C. ©2014

39

Third Party Supplemental Needs Trusts: Estate Taxes

• Included in Estate of Grantor• Strings Attached• Maintain Control or Beneficial Enjoyment• Reversion

• Excluded from Estate of Grantor• No Strings Attached • No Control or Beneficial Enjoyment Retained

Vincent J. Russo & Associates, P.C. ©2014

40

Testamentary Third Party Supplemental Needs Trusts

• Gift Taxation• Not subject to Gift Tax laws

• Income Taxation to Settlor, Trust, Beneficiary• Complex Trust

• Estate Taxation• Included in the Estate

Vincent J. Russo & Associates, P.C. ©2014

41

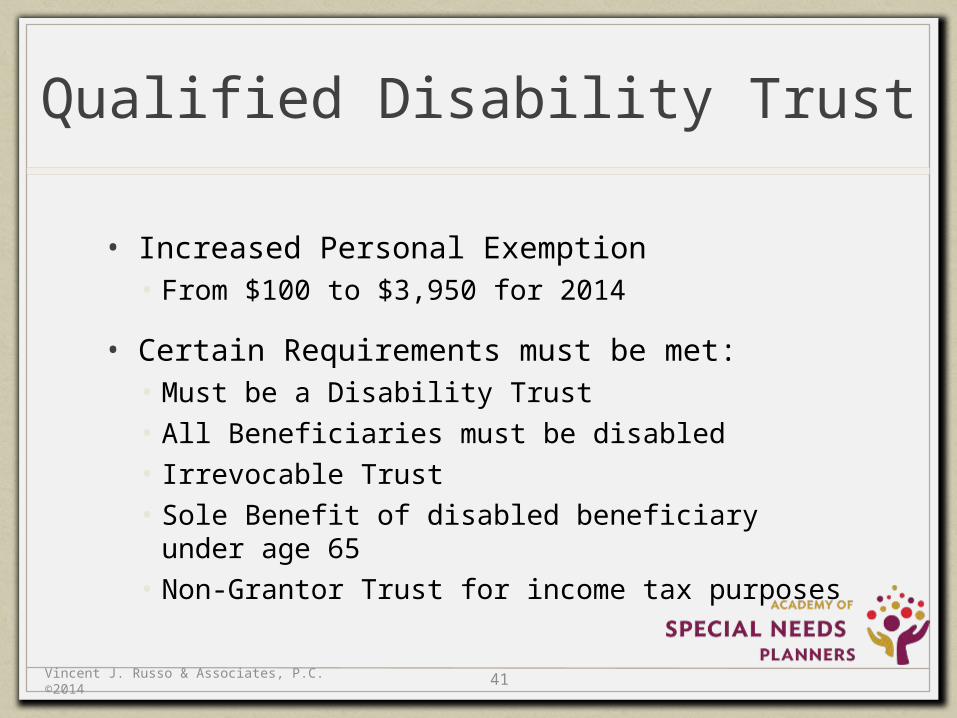

Qualified Disability Trust

• Increased Personal Exemption• From $100 to $3,950 for 2014

• Certain Requirements must be met:• Must be a Disability Trust• All Beneficiaries must be disabled• Irrevocable Trust• Sole Benefit of disabled beneficiary under age 65• Non-Grantor Trust for income tax purposes

Vincent J. Russo & Associates, P.C. ©2014

42

IRAs, SNTs and Medicaid

• IRAs• Available versus Not Available• Permanent Pay Status• Required Minimum Distributions• Annuities

• SNTs• Trust Assets not available as to Medicaid

Vincent J. Russo & Associates, P.C. ©2014

43

IRAs: Trust as Designated Beneficiary

• IRC Reg. §1.401(a)(9)-4, A-5)

• #1 - Trust must be valid under state law

• #2 - Trust must be irrevocable or will, by its terms, become irrevocable upon death of the participant

• # 3- The beneficiaries must be “identifiable ... from the trust instrument”

• #4 - Certain documentation must be provided to “the plan administrator” by 10/31 of the year following the year of participant’s death

• #5 - All trust beneficiaries must be individuals

Vincent J. Russo & Associates, P.C. ©2014

44

Third Party Designation of SNT as IRA Beneficiary

• Bob’s child, Krista, is 35 years old and has CP

• Options• Bob creates a Living Third Party SNT for Krista• Bob creates a Revocable Trust with SNT for Krista • Bob creates a Will with SNT for Krista

• Bob designates SNT as his IRA beneficiary

Vincent J. Russo & Associates, P.C. ©2014

45

IRAs and SNTs: PLR 200620025 Facts

• Taxpayer A, age 69 died

• Four sons surviving; Child B is disabled

• Sons are named beneficiaries of the inherited IRA event

Vincent J. Russo & Associates, P.C. ©2014

46

IRAs and SNTs: PLR 200620025 Strategy

• Separate Sub-IRAs Established for Each Child

• Make the Annual RMDs

• Court Authorized Establishment of First Party SNT with a Pay Back Provision and the Transfer of Child B’s Share of the IRA to the SNT

Vincent J. Russo & Associates, P.C. ©2014

47

IRAs and SNTs: PLR 200620025 Ruling

• SNT is a Grantor Trust

• Transfer of B’s Share of the IRA to SNT is not a Taxable Event

• Trustee may Calculate the Annual RMDs Based on Life Expectancy of Taxpayer B

Vincent J. Russo & Associates, P.C. ©2014

48

IRAs and SNTs: PLR 201116005

• Beneficiary’s Father Died Owning two IRAs Benefitting Beneficiary and his Siblings.

• Beneficiary is Disabled and Medicaid Eligible.

• Beneficiary Proposed to Transfer his Share of the Inherited IRAs to a First Party Special Needs Trust in Order to Protect his Medicaid Benefits.

Vincent J. Russo & Associates, P.C. ©2014

49

IRAs and SNTs: PLR 201116005

• IRS held that as a General Rule, if a Beneficiary Transfers an Inherited IRA, there is an Immediate Taxable Event

• However, in this case the Beneficiary’s Transfer of the IRA to the SNT would not be a Taxable Event

• The Transfer was not a Gift as it was made to a Grantor Trust. So essentially, the Beneficiary Transferred the IRA to Himself.

Vincent J. Russo & Associates, P.C. ©2014

50

IRAs and SNTs: PLR 201117042

• IRA Owner Established an IRA.

• IRA Owner then Contracted Muscular Dystrophy and was deemed Disabled

• A Court Authorized the Creation of a SNT for IRA Owner

• The Court Ordered that Amount Equal to Balance in the IRA be Transferred to the SNT

Vincent J. Russo & Associates, P.C. ©2014

51

IRAs and SNTs: PLR 201117042

• When the IRA Owner tried to Comply with the Court order, the IRA Provider Refused because an IRA cannot be set up in the Name of a Trust. The IRA provider Distributed the funds to a Non-IRA account and issued a 1099 as a Taxable Event.

• IRS Allowed the IRA Owner to Roll the Funds over to a New IRA.

Vincent J. Russo & Associates, P.C. ©2014

52

Irrevocable Life Insurance Trust with Supplemental Needs

• Crummey Powers• Draft withdrawal provision so that the beneficiary with

special needs does not have a withdrawal power• Provide for the Donor to control who has a withdrawal

power• Provide for other beneficiaries with a withdrawal power

Vincent J. Russo & Associates, P.C. ©2014

53

Credit Shelter and Marital Trusts with Supplemental Needs

• Credit Shelter Trust• Supplemental needs provisions as income and principal

• Marital Trust• Supplemental needs provisions as to principal but not

income if qualifying the trust for the marital deduction

Vincent J. Russo & Associates, P.C. ©2014

54

Drafting: Supplemental Needs Trust Provisions

• Drafting Supplemental Needs Provisions as a Contingency Plan• In connection with minor trusts, descendant trusts,

generation skipping trusts• Can have trigger provisions as to Medicaid except for a

beneficiary–spouse and if the Trust is inter-vivos

Vincent J. Russo & Associates, P.C. ©2014

55

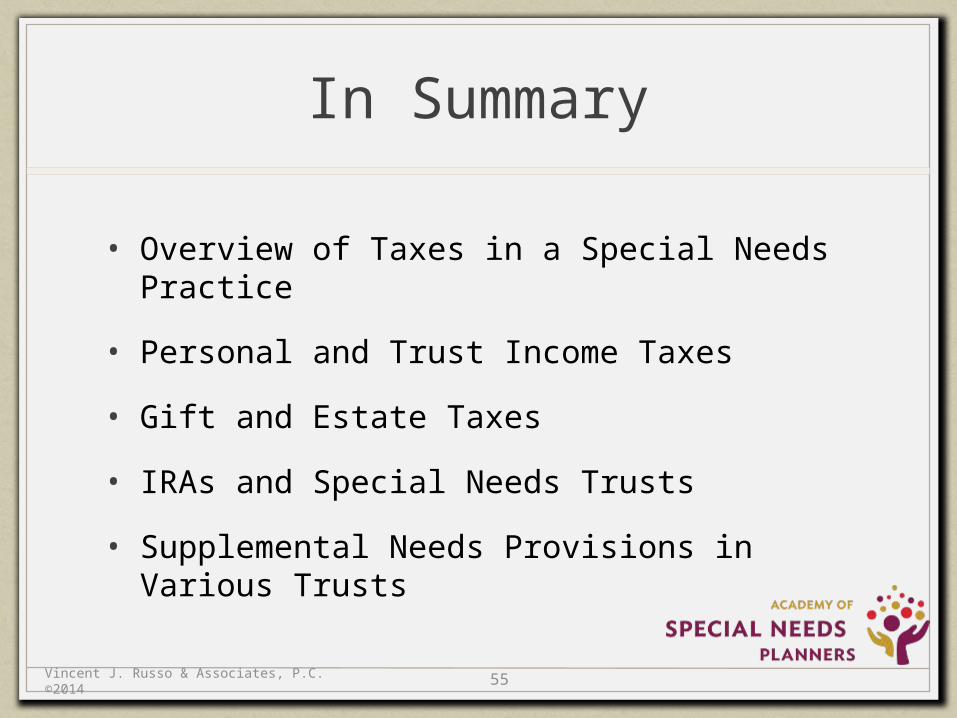

In Summary

• Overview of Taxes in a Special Needs Practice

• Personal and Trust Income Taxes

• Gift and Estate Taxes

• IRAs and Special Needs Trusts

• Supplemental Needs Provisions in Various Trusts

Vincent J. Russo & Associates, P.C. ©2014