presented by group 2 group 2 pension core course 2011...

TRANSCRIPT

G P j t NIGERIAG P j t NIGERIAGroup Project: NIGERIA Group Project: NIGERIA

Presented ByPresented By

Group 2 Group 2

Pension Core Course 2011Pension Core Course 2011The World BankThe World Bank

Outline

1. Introduction of the Group p

2. Nigeria’s Demographic & Economic Characteristics

3. Pension System

4. Reform Needs & Challenges

5. Enabling Conditions

6 Reform Objectives6. Reform Objectives

7. Reform Options

8. Assessment of Technical Feasibility of Reform Options

9. Reform Proposal and Justification

10. Fitting Reform with Broader Social Protection & Growth Objectives

11. Proposed Coalition & Consensus Building Strategy

12. Communication/Public Information Strategy

13 Summary13. Summary

Location of Nigeriag

Introduction of the Group

Membership

NAME COUNTRY1 J. O. OMUYA NIGERIA2 AKIN FANIMOKUN NIGERIA3 DEMOLA SOGUNLE NIGERIA4 KUNLE HUSSAIN NIGERIA5 GORDON BULINDA KENYA5 GORDON BULINDA KENYA6 ATONTE DIETE-SPIFF NIGERIA7 DICKSON GAMA TANZANIA8 NOBBY SIMUTENOA ZAMBIA9 OLUSEGUN WRIGHT NIGERIA10 MARIANO BOSCH IDBA11 LEILY MENDOZA EL SALVADOR

4

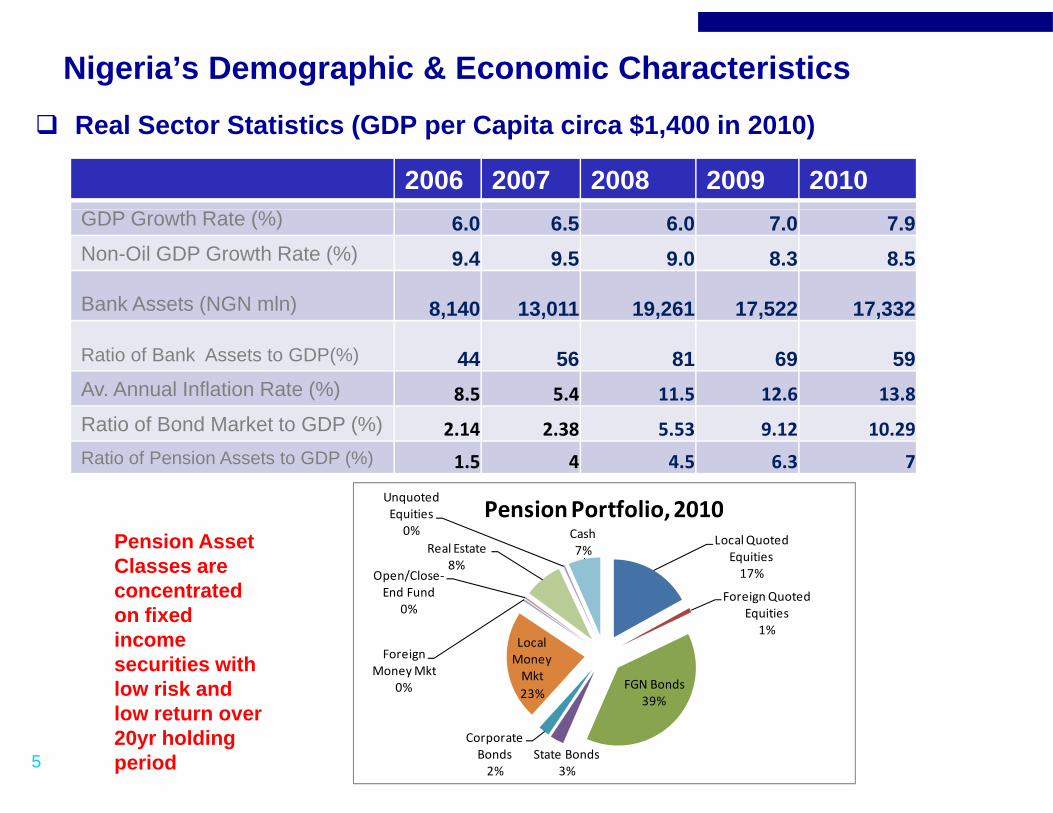

Nigeria’s Demographic & Economic Characteristics Real Sector Statistics (GDP per Capita circa $1,400 in 2010)

2006 2007 2008 2009 2010GDP Growth Rate (%) 6.0 6.5 6.0 7.0 7.9Non-Oil GDP Growth Rate (%) 9.4 9.5 9.0 8.3 8.5

Bank Assets (NGN mln) 8 140 13 011 19 261 17 522 17 332Bank Assets (NGN mln) 8,140 13,011 19,261 17,522 17,332

Ratio of Bank Assets to GDP(%) 44 56 81 69 59Av. Annual Inflation Rate (%) 8.5 5.4 11.5 12.6 13.8

Ratio of Bond Market to GDP (%) 2.14 2.38 5.53 9.12 10.29Ratio of Pension Assets to GDP (%) 1.5 4 4.5 6.3 7

Unquoted PensionPortfolio 2010

Local Quoted Equities17%

Foreign Quoted

Open/Close‐End Fund

Real Estate8%

Equities0% Cash

7%

Pension Portfolio, 2010Pension Asset Classes are concentrated

Equities1%

FGN Bonds39%

Local Money Mkt23%

Foreign Money Mkt

0%

0%on fixed income securities with low risk and

5

39%

State Bonds3%

Corporate Bonds2%

low return over 20yr holding period

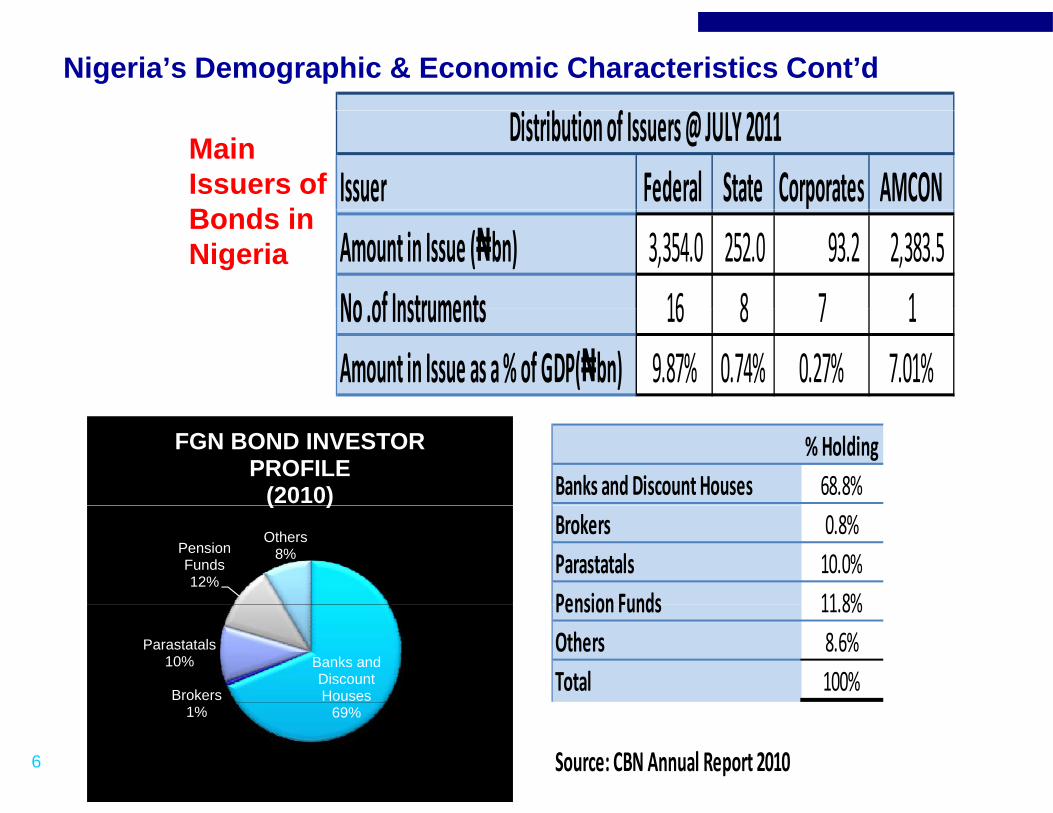

Nigeria’s Demographic & Economic Characteristics Cont’d

b fIssuer Federal State Corporates AMCON

Distribution of Issuers @ JULY 2011Main Issuers of B d i

Amount in Issue (₦bn) 3,354.0 252.0 93.2 2,383.5 No of Instruments 16 8 7 1

Bonds in Nigeria

No .of Instruments 16 8 7 1Amount in Issue as a % of GDP(₦bn) 9.87% 0.74% 0.27% 7.01%

FGN BOND INVESTOR PROFILE

(2010)

% HoldingBanks and Discount Houses 68.8%

Pension Funds12%

Others8%

( )Brokers 0.8%Parastatals 10.0%Pension Funds 11 8%

Banks and Discount HousesBrokers

Parastatals10%

Pension Funds 11.8%Others 8.6%Total 100%

6

69%1%

Source: CBN Annual Report 2010

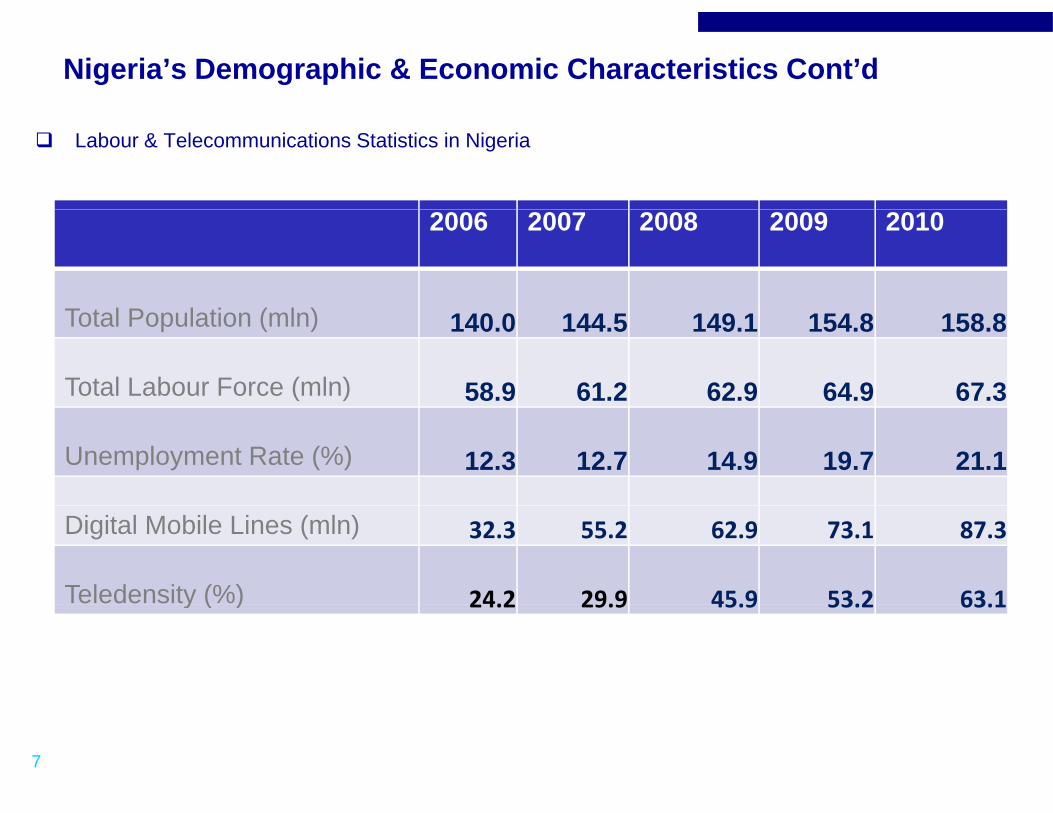

Nigeria’s Demographic & Economic Characteristics Cont’d

Labour & Telecommunications Statistics in Nigeria

2006 2007 2008 2009 2010

T l P l i ( l )Total Population (mln) 140.0 144.5 149.1 154.8 158.8

Total Labour Force (mln) 58.9 61.2 62.9 64.9 67.3

Unemployment Rate (%) 12.3 12.7 14.9 19.7 21.1

Digital Mobile Lines (mln) 32.3 55.2 62.9 73.1 87.3

Teledensity (%) 24.2 29.9 45.9 53.2 63.1y ( ) 24.2 29.9 45.9 53.2 63.1

7

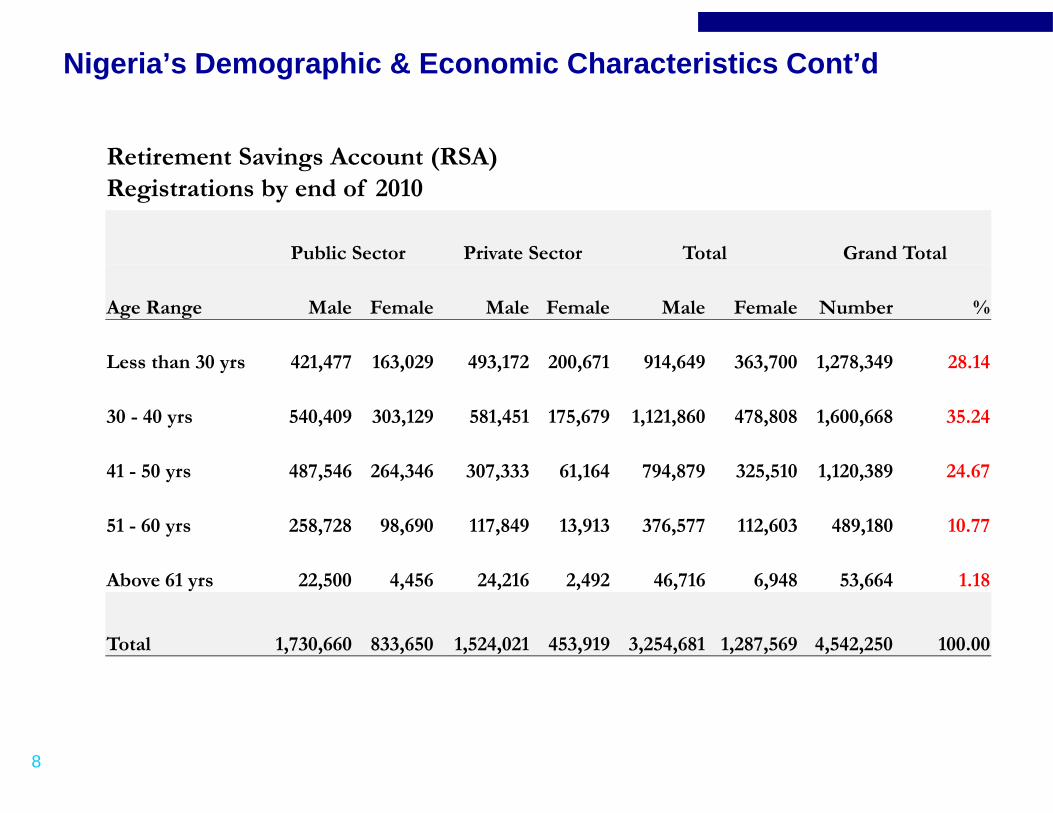

Nigeria’s Demographic & Economic Characteristics Cont’d

Retirement Savings Account (RSA)Registrations by end of 2010

Public Sector Private Sector Total Grand Total

Age Range Male Female Male Female Male Female Number %Age Range Male Female Male Female Male Female Number %

Less than 30 yrs 421,477 163,029 493,172 200,671 914,649 363,700 1,278,349 28.14

30 - 40 yrs 540,409 303,129 581,451 175,679 1,121,860 478,808 1,600,668 35.24

41 - 50 yrs 487,546 264,346 307,333 61,164 794,879 325,510 1,120,389 24.67

51 - 60 yrs 258,728 98,690 117,849 13,913 376,577 112,603 489,180 10.77

Above 61 yrs 22,500 4,456 24,216 2,492 46,716 6,948 53,664 1.18

Total 1,730,660 833,650 1,524,021 453,919 3,254,681 1,287,569 4,542,250 100.00

8

Nigeria’s Demographic & Economic Characteristics Cont’dC /T l P l i C /L b F

Coverage Statistics

6.00%

7.00%

8.00%

Coverage/Total Population Coverage/Labour Force

3.00%

4.00%

5.00%

0.00%

1.00%

2.00%

2006 2007 2008 2009 2010

7

8

65YR/Total Population 65YR/Pop Aged 15‐64

4

5

6

7

rcen

tage

0

1

2

3Per

9

02010 2015 2020 2025 2030 2035 2040 2045 2050

Year

Description of Existing Pension System

Regulatory Framework- First Law in 1961 (Provident Fund)- NSITF

C t L P i R f A t

Qualifying Conditions- Retirement age is 60 yrs or 35 yrs in

service whichever is lower butcontributor is eligible from 50 yrs- Current Law: Pension Reform Act

2004 Type of Programme/Scheme

- Defined ContributionA unified system of individual account

g y- Guaranteed minimum pension paid to

members who have contributed for atleast 20 yrs

Pension BenefitsA t i b d t t l t ib ti- A unified system of individual account

system that replaced former socialinsurance system

- Applicable to new entrantsto workforce in Jan 2005 (private

sector) and J l 2004 (p blic sector)

- Amount is based on total contributionand accrued rights (under DB) plusreturn on investment

- Pensioner receives a lump sum ifamount in the individual account issector) and July 2004 (public sector)

- Workers on old system expected toswitch unless within 3 yrs ofretirement

Coverage

- Sufficient to purchase an annuity- or sufficient to fund programmed

withdrawal of at least 50% ofannual salary at retirementC t ib t h ti d b f Coverage

- All federal public sector employees(including military?)

- All private sector employees workingin firms with 5 workers or more

- Contributor who retired beforeage 50 may receive 25% of totalcontribution as a lump sum

Survivor Benefits- Benefit is 100% of balance in

Source of Funds- Contributor: 7.5% of gross salary

(2.5% for military personnel)- Employer: 7.5% of gross salary

(12 5% for military personnel)

Benefit is 100% of balance indeceased’s individual account plussum from employer-sponsored lifeinsurance policy

- Survivor may purchase an annuity orgo into a programmed withdrawal

10

(12.5% for military personnel)- Employers finance life insurance

policy for their employees,guaranteeing 3X employee’s annualsalary

go into a programmed withdrawalbased on life expectancy

Description of Existing Pension System Cont’d P i R f A t 2004• Pension Reform Act 2004The Pension Reform Act (PRA) 2004 provides for the establishment of aContributory Pension Scheme with the following objectives: Ensure seamless funding of the retirement scheme by assisting Ensure seamless funding of the retirement scheme by assisting

improvident individuals save in order to cater to their livelihood duringold age

Ensure that private and public sector employee receives histi t b fit d h d d tretirement benefits as and when due and to

Establish a uniform set of rules, regulations and standards for theadministration and payments of retirement benefits.

The PRA 2004 also established the National Pension Commission(PENCOM). Its duties include: Regulate, supervise and ensure the effective administration of

pension matters in Nigeria, Approval, licensing and supervision of all pension fund administrators Establishment of standards, rules and issuance of guidelines for the

management and investment of pension funds under this Actmanagement and investment of pension funds under this Act.

11

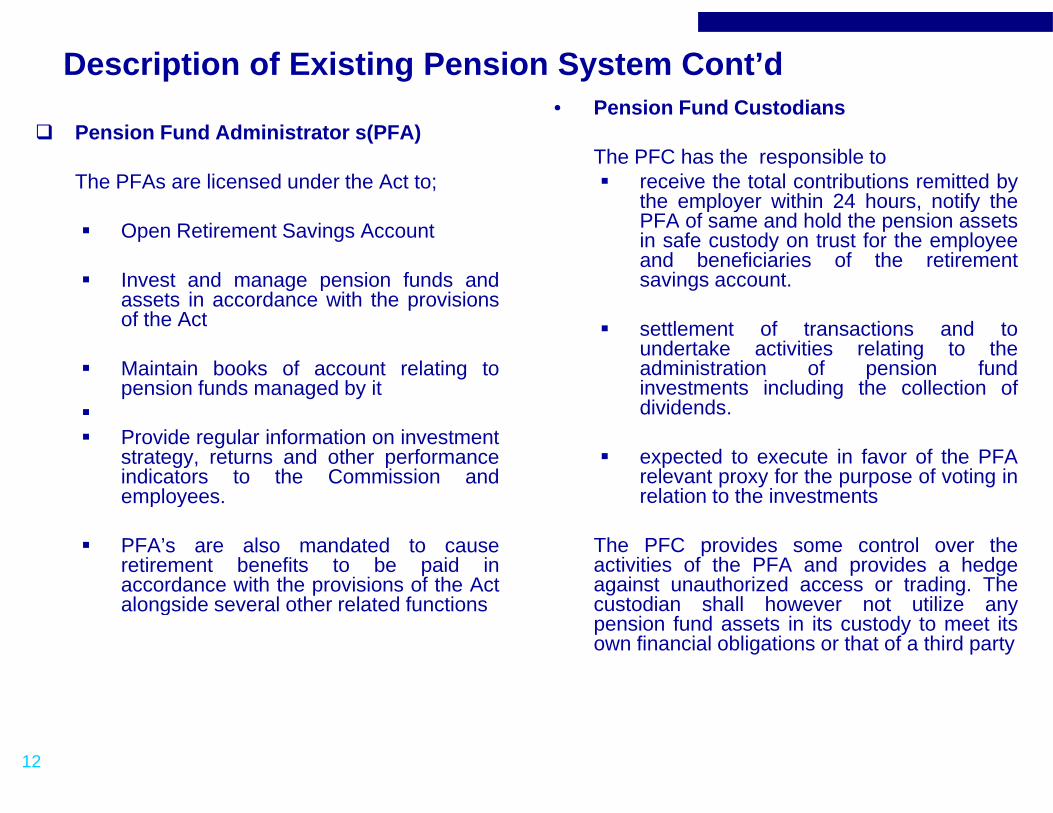

Description of Existing Pension System Cont’d • Pension Fund Custodians

Pension Fund Administrator s(PFA)

The PFAs are licensed under the Act to;

Pension Fund Custodians

The PFC has the responsible to receive the total contributions remitted by

the employer within 24 hours, notify the Open Retirement Savings Account

Invest and manage pension funds andassets in accordance with the provisions

p y , yPFA of same and hold the pension assetsin safe custody on trust for the employeeand beneficiaries of the retirementsavings account.

pof the Act

Maintain books of account relating topension funds managed by it

settlement of transactions and toundertake activities relating to theadministration of pension fundinvestments including the collection ofdividends

Provide regular information on investmentstrategy, returns and other performanceindicators to the Commission andemployees.

dividends.

expected to execute in favor of the PFArelevant proxy for the purpose of voting inrelation to the investmentsp y

PFA’s are also mandated to causeretirement benefits to be paid inaccordance with the provisions of the Actalongside several other related functions

The PFC provides some control over theactivities of the PFA and provides a hedgeagainst unauthorized access or trading. Thecustodian shall however not utilize anyalongside several other related functions custodian shall however not utilize anypension fund assets in its custody to meet itsown financial obligations or that of a third party

12

Structure of DC

Life InsuranceCompanies

Maintain Life Insurance

PenComEnforcement

policy for each employee Employer

License Operators

Transfer contributions to

d f PFA Employees

A i PFCPFC

(h ld th t )

PFA/CPFA(Manages the Money;

order of PFA Employees

Appoints PFC(holds the assets) ( g s y;administers Pensions)

13

Contribution Fund Flow

EMPLOYEREMPLOYEE7 5% (2 5%) 7 5% (12 5%)7.5% (2.5%) 7.5% (12.5%)

Total ContributionTotal Contribution

Based on 15 % Employee Income Transferred by Employer to order

f PFA

Reports to E l

PFA Reports to PFA PFC

of PFA

Employee

14

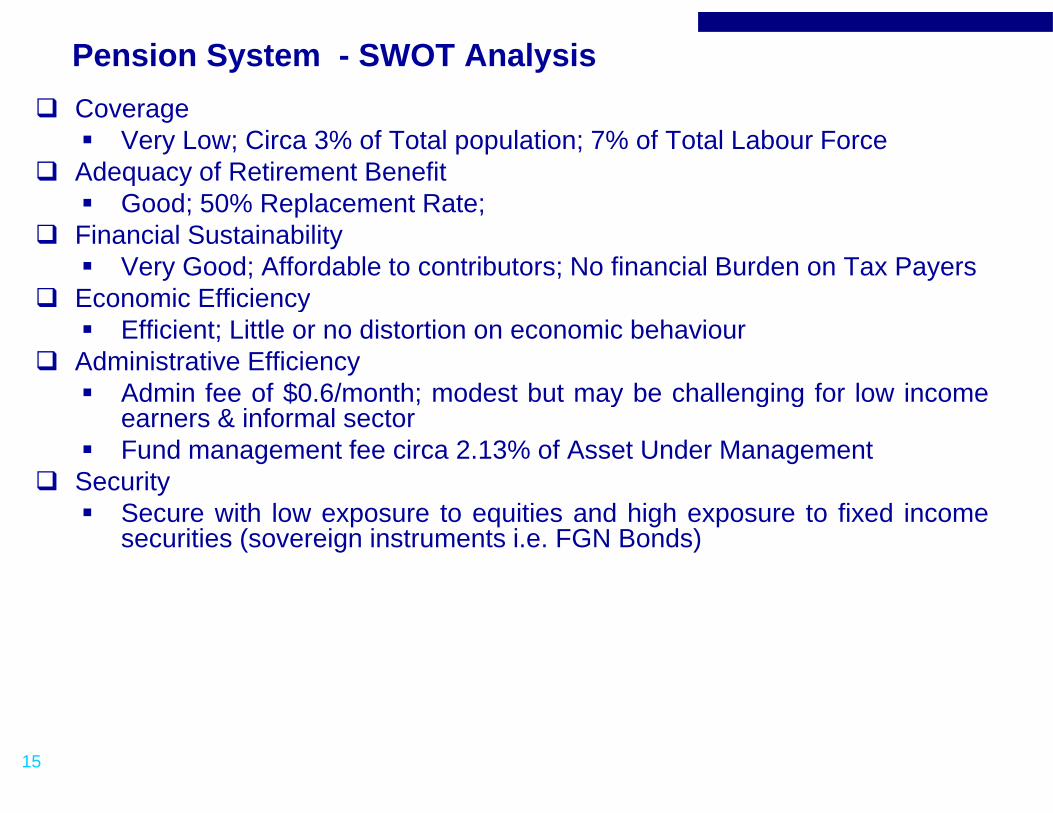

Pension System - SWOT Analysis Coverage Coverage Very Low; Circa 3% of Total population; 7% of Total Labour Force

Adequacy of Retirement Benefit Good; 50% Replacement Rate;Good; 50% Replacement Rate;

Financial Sustainability Very Good; Affordable to contributors; No financial Burden on Tax Payers

Economic Efficiencyy Efficient; Little or no distortion on economic behaviour

Administrative Efficiency Admin fee of $0.6/month; modest but may be challenging for low incomey g g

earners & informal sector Fund management fee circa 2.13% of Asset Under Management

SecurityS ith l t iti d hi h t fi d i Secure with low exposure to equities and high exposure to fixed incomesecurities (sovereign instruments i.e. FGN Bonds)

15

Reform Needs & Challenges 2ND PILLAR REFORM 2ND PILLAR REFORM

Extending the coverage of pension scheme

Improving pension investment management

Improving pension data and account administration

16

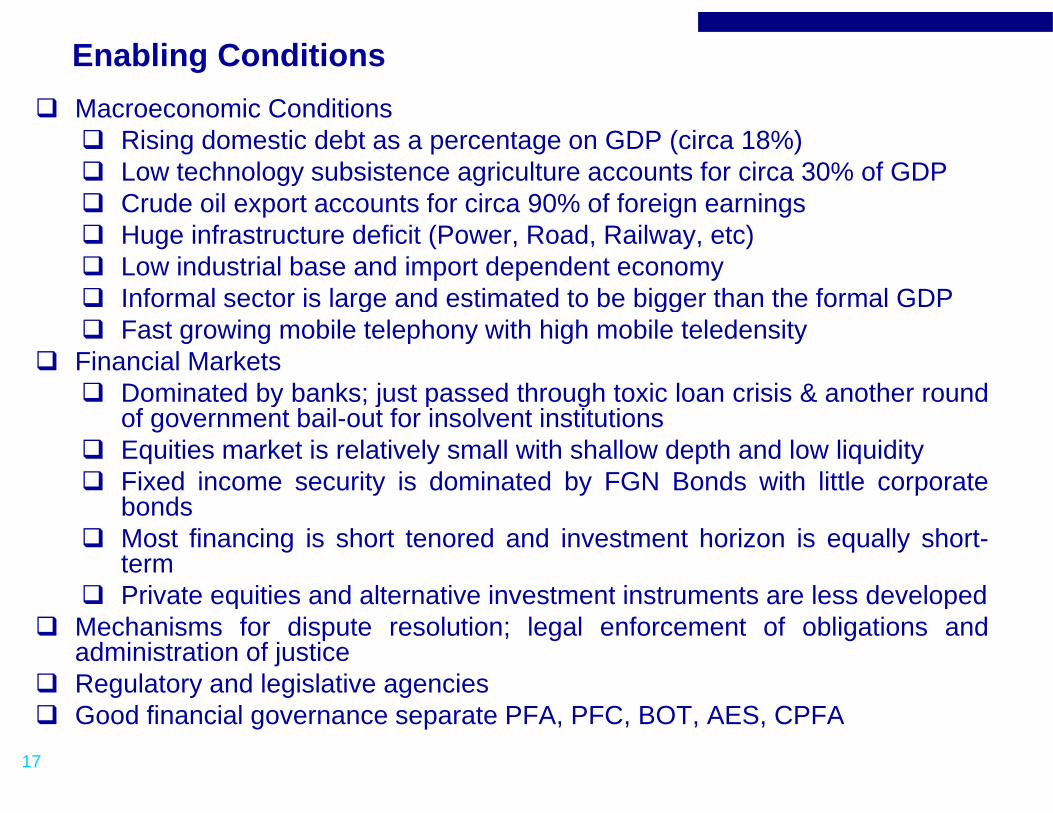

Enabling Conditions Macroeconomic Conditions Macroeconomic Conditions Rising domestic debt as a percentage on GDP (circa 18%) Low technology subsistence agriculture accounts for circa 30% of GDP Crude oil export accounts for circa 90% of foreign earnings Crude oil export accounts for circa 90% of foreign earnings Huge infrastructure deficit (Power, Road, Railway, etc) Low industrial base and import dependent economy Informal sector is large and estimated to be bigger than the formal GDPg gg Fast growing mobile telephony with high mobile teledensity

Financial Markets Dominated by banks; just passed through toxic loan crisis & another roundy j p g

of government bail-out for insolvent institutions Equities market is relatively small with shallow depth and low liquidity Fixed income security is dominated by FGN Bonds with little corporate

bondsbonds Most financing is short tenored and investment horizon is equally short-

term Private equities and alternative investment instruments are less developedate equ t es a d a te at e est e t st u e ts a e ess de e oped

Mechanisms for dispute resolution; legal enforcement of obligations andadministration of justice

Regulatory and legislative agencies

17

Good financial governance separate PFA, PFC, BOT, AES, CPFA

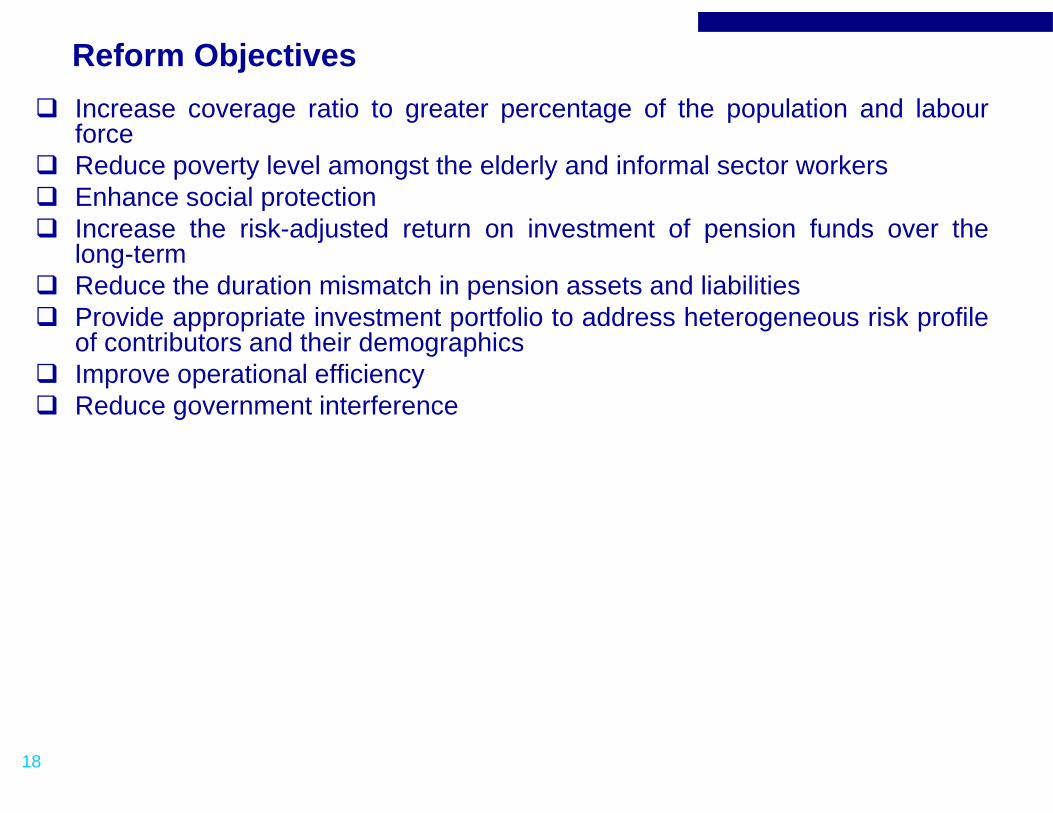

Reform Objectives Increase coverage ratio to greater percentage of the population and labour Increase coverage ratio to greater percentage of the population and labour

force Reduce poverty level amongst the elderly and informal sector workers Enhance social protectionp Increase the risk-adjusted return on investment of pension funds over the

long-term Reduce the duration mismatch in pension assets and liabilities P id i t i t t tf li t dd h t i k fil Provide appropriate investment portfolio to address heterogeneous risk profile

of contributors and their demographics Improve operational efficiency Reduce government interference Reduce government interference

18

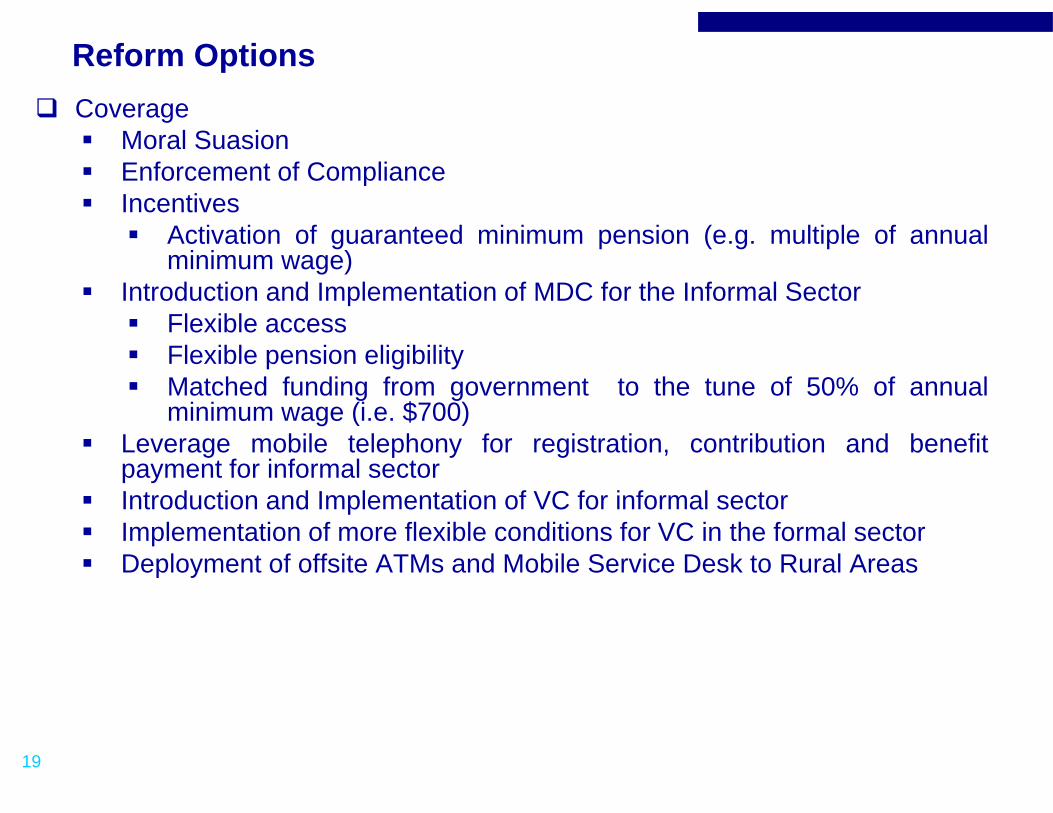

Reform Options Coverage Coverage Moral Suasion Enforcement of Compliance IncentivesIncentives Activation of guaranteed minimum pension (e.g. multiple of annual

minimum wage) Introduction and Implementation of MDC for the Informal Sector Flexible access Flexible pension eligibility Matched funding from government to the tune of 50% of annual

i i (i $700)minimum wage (i.e. $700) Leverage mobile telephony for registration, contribution and benefit

payment for informal sector Introduction and Implementation of VC for informal sectorIntroduction and Implementation of VC for informal sector Implementation of more flexible conditions for VC in the formal sector Deployment of offsite ATMs and Mobile Service Desk to Rural Areas

19

Reform Options

Investment Management Increase and Diversification of Asset Classes

Weighted Average Return on Increase and Diversification of Asset Classes

Re-setting of Investment Limits on existing Asset Classes Life Cycle Investment Management

Aggressive

Investment = 11.6% in 2010; Only a quarter of pension gg

Balanced Conservative

Umbrella Fund or Fund of Funds

passets have TTM greater than 10 yrs

Investment Guidelines to Allow Direct Equity Investment in Long TermInfrastructure Projects under a Private Public Partnership (PPP)

Extension of Investment Horizon to Match Liability Structure

Pension Data and Administration Deployment of Robust Secure and Scalable ICT Deployment of Robust, Secure and Scalable ICT Data Clean-up Opening of Transfer Window On line Registration of Contributors

20

On-line Registration of Contributors

Technical Feasibility of Reform Options Cost of MDC To Government Cost of MDC To Government

Matching ½ of Annual Minimum Wage = N108,000 ($700)

Cost of new 5,000,000 Contributors every YR = N540 bln ($3.4 bln)

Coverage Ratio can Double to 14% in YR 1 at a cost of circa 1.6% ofgGDP

70 00%

Projected Coverage RatioCoverage/Total Population Coverage/Labour Force

30.00%

40.00%

50.00%

60.00%

70.00%

Percen

tage

Social and Political Support

0.00%

10.00%

20.00%P

Social and Political Support Other Reform Options will Cost Government Little or Nothing Operators and Fund Managers Bearing ICT and Other Reform Costs

will be Compensated through increased number of Contributors and

21

will be Compensated through increased number of Contributors andAUM

Reform Proposal & JustificationProposal Old Law/Regulation New Law/Regulation Justificationp g g

Increased Coverage Ratio Minimum Pension

N/A

-Activation of Minimu-m Guaranteed Pension

- MDC for Informal Sector

VC for Informal Sector

-Poverty Reduction

-Social Protection Enhancement

-Low Implementation Cost

N/A

5-YR lock-up period for VC for tax exemption

-VC for Informal Sector

-Flexible VC for Formal Sector

- ATM & Mobile Service Desk in Rural Areas

-Provision of Economies of Scale to Operators

tax exemption

N/A

Rural Areas

Pension Investment Management Eligible Asset Class

I t t Li it

-Additional Asset Classes

R tti f I t t Li it

-Adequacy of Pension Benefits in Future

Investment Limits

N/A

N/A

-Re-setting of Investment Limits

-Introduction of Multi-Funds & Life Cycle Default Option

-Introduction of Umbrella Fund or Fund of Funds

-Diversification of Risk

-Development of Infrastructure

-Reduction of Unemployment

N/A

Fund of Funds

-Direct Infrastructure Project Investment under PPP

-Improvement of GDP

-Zero cost to Government

Pension Data & Administration ICT Infrastructure

National Database

T f Wi d

-Deployment of Robust, Secure and Scalable ICT

-Completion of Data Clean-up Project

A ti ti f T f Wi d

- Increased Access to Informal Sector & Low Income Earners

-Reduction of Adm Cost

22

Transfer Window

Registration of Contributors

-Activation of Transfer Window

-Online Registration of Contributors

Reform Proposal Fit with Broader Social Protection & Growth ObjectivesGrowth Objectives

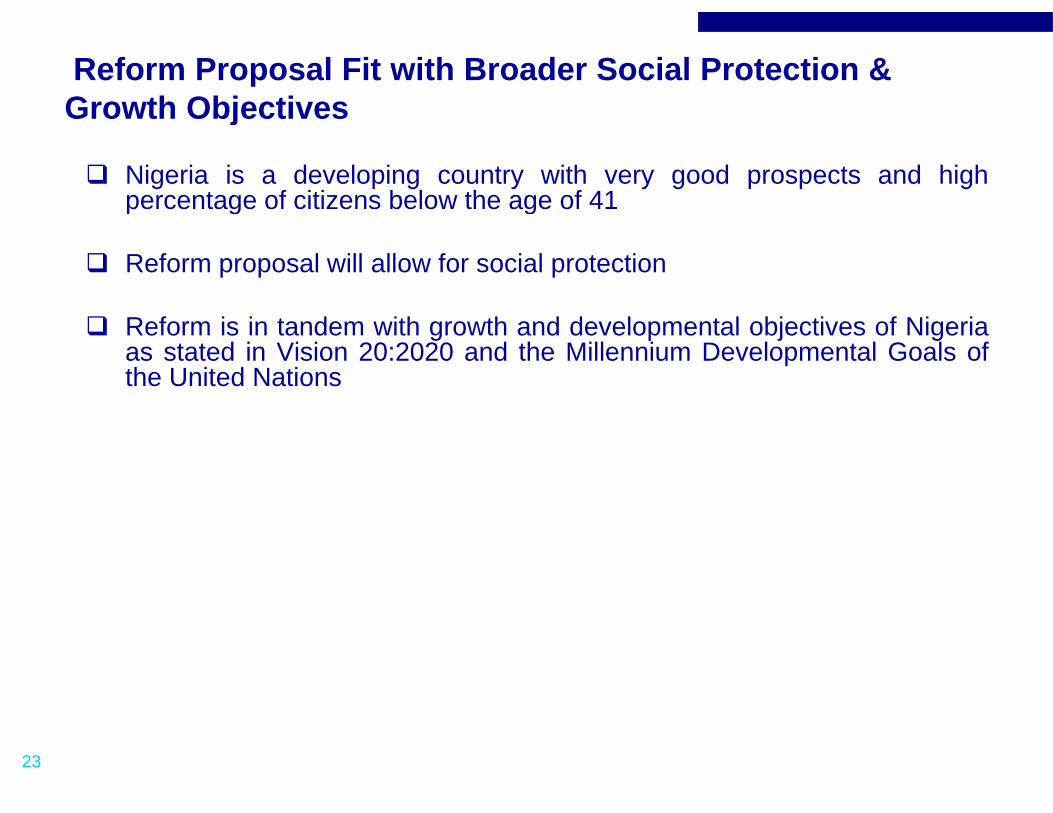

Nigeria is a developing country with very good prospects and highpercentage of citizens below the age of 41p g g

Reform proposal will allow for social protection

Reform is in tandem with growth and developmental objectives of Nigeriaas stated in Vision 20:2020 and the Millennium Developmental Goals ofthe United Nations

23

Proposed Coalition/Consensus Building Strategy

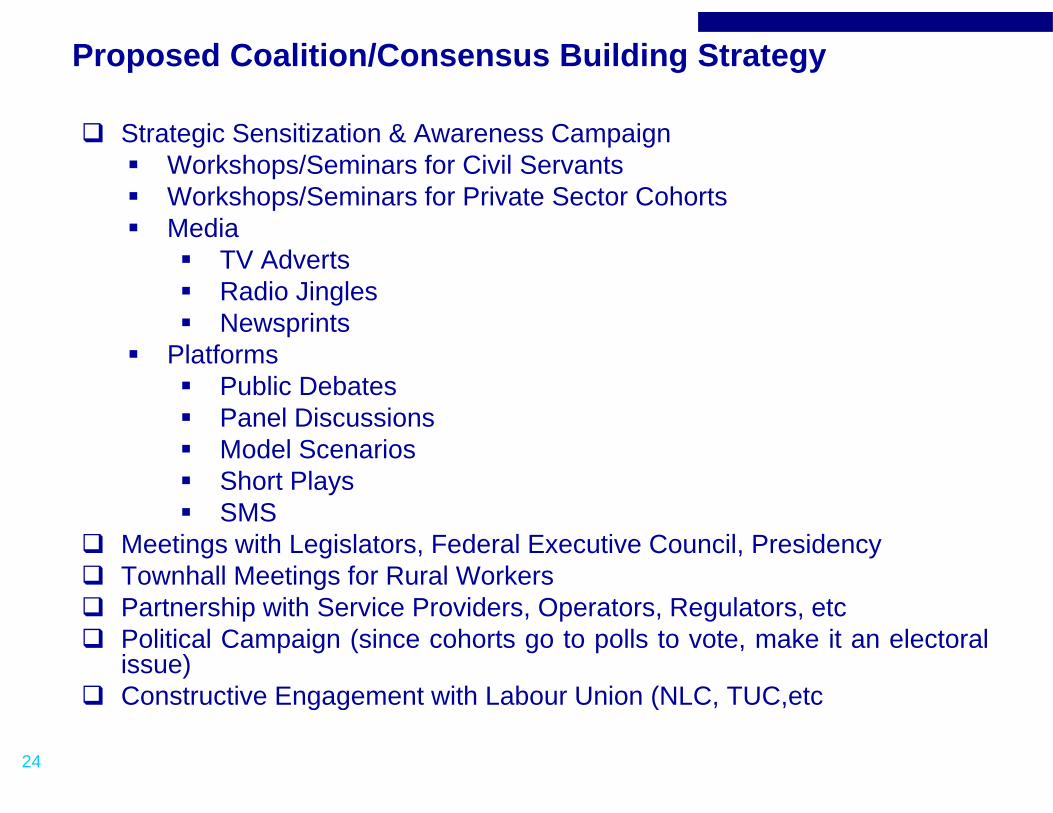

Strategic Sensitization & Awareness Campaign Workshops/Seminars for Civil Servants Workshops/Seminars for Private Sector Cohortsp Media

TV Adverts Radio Jingles Newsprints

Platforms Public Debates Panel Discussions Model Scenarios Short Plays

SMS SMS Meetings with Legislators, Federal Executive Council, Presidency Townhall Meetings for Rural Workers Partnership with Service Providers Operators Regulators etc Partnership with Service Providers, Operators, Regulators, etc Political Campaign (since cohorts go to polls to vote, make it an electoral

issue) Constructive Engagement with Labour Union (NLC, TUC,etc

24

Constructive Engagement with Labour Union (NLC, TUC,etc

Communication/Public Information Strategy Sustained/Continuous awareness creation through media and regular Sustained/Continuous awareness creation through media and regular

jingles Regular engagements of all stakeholders including Trade Unions Artisans Cooperative Societies Farmers Market Women Housewives Casual Labourers Legislators, Civil Servants, Operators, Executives, etc

Continuous publicity of the positives to underscore workability of proposals E PRO E t f St t D i d E ti Engage PRO Expert for Strategy, Design and Execution Information Centre for Q & A

25

Summary

Increase coverage ratio and extend social protection to the most Increase coverage ratio and extend social protection to the mostvulnerable segment of the population using a combination ofincentives and reform options which are relatively cheap

Create pension investment management strategy and guidelineswhich will reduce the duration mismatches between pension assetsand liabilities, ensure adequate pension benefits in future andsimultaneously deepen the financial system and improve economicy p y pgrowth

Deploy ICT to increase efficiency of pension administration andleverage economies of scale to reduce administrative cost whileleverage economies of scale to reduce administrative cost whileensuring financial inclusion.

Engage engage and engage all the stakeholders and obtain political Engage, engage and engage all the stakeholders and obtain politicalsupport and buy-in

26

THANK YOUTHANK YOU

27