presented by carol jordan nmls# 98985 and renee duval nmls#97967 certified mortgage professionals nh...

TRANSCRIPT

Presented byCarol Jordan NMLS# 98985 and Renee Duval NMLS#97967

Certified Mortgage ProfessionalsNH Mortgage Bankers Association designation

Licensed by the New Hampshire Banking DepartmentNMLS ID# 2561

MA Lender License #MC2561

Selling Distressed Properties

Approved by the New Hampshire Real Estate Commission

E1569 – 3 hours continuing education

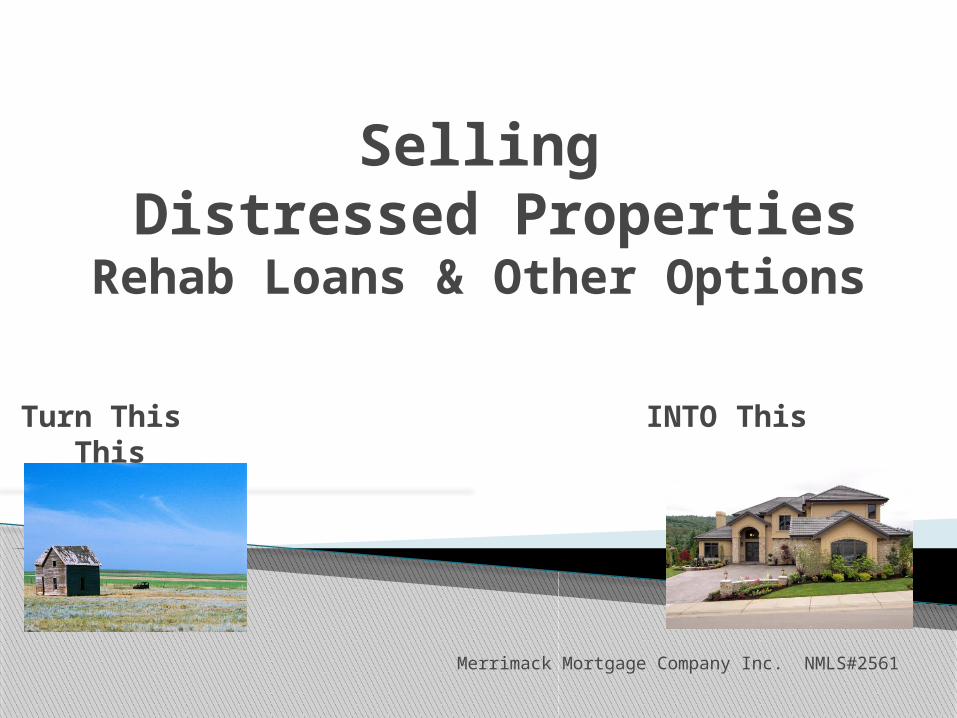

Selling Distressed Properties

Rehab Loans & Other Options

Turn This INTO This This

Merrimack Mortgage Company Inc. NMLS#2561

Selling Distressed PropertiesApproved by the NH Real Estate Commission Course #E1569

Merrimack Mortgage Company Inc. NMLS#2561

The views expressed in this presentation are those of the presenters, Renee Duval and Carol Jordan and do not reflect those of our employer, colleagues or its clients.

The information provided by us is for

informational purposes only and is not intended as legal or tax advice.

Disclaimer

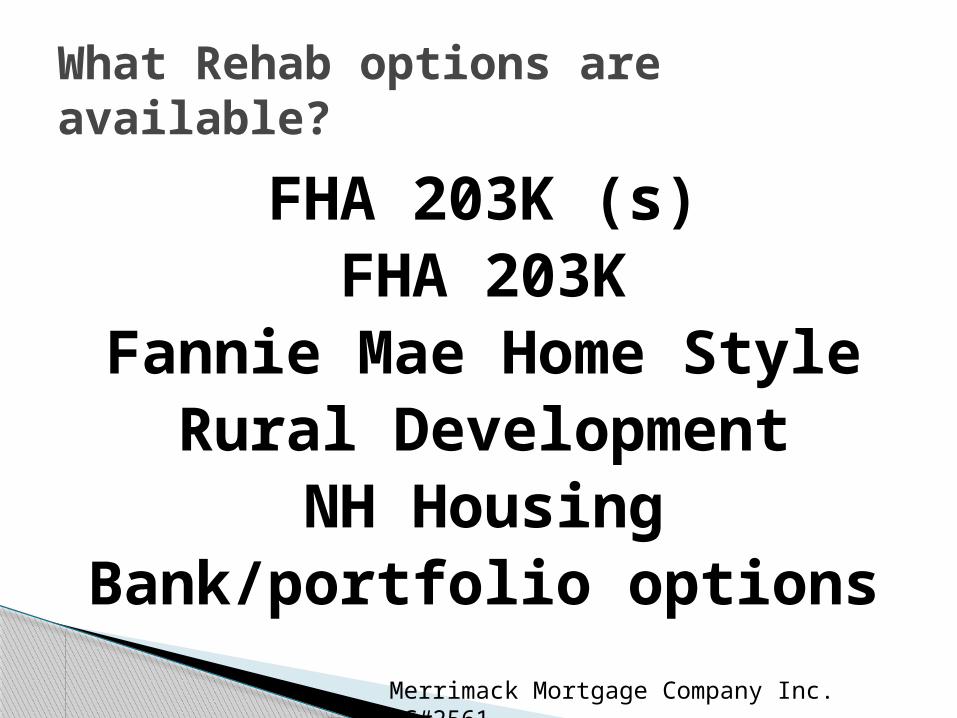

FHA 203K (s)FHA 203K

Fannie Mae Home StyleRural Development

NH HousingBank/portfolio options

What Rehab options are available?

Merrimack Mortgage Company Inc. NMLS#2561

203K is an FHA rehab loan

203Ks is the streamline version of the FHA 203K

FHA 203K and 203Ks

Merrimack Mortgage Company Inc. NMLS#2561

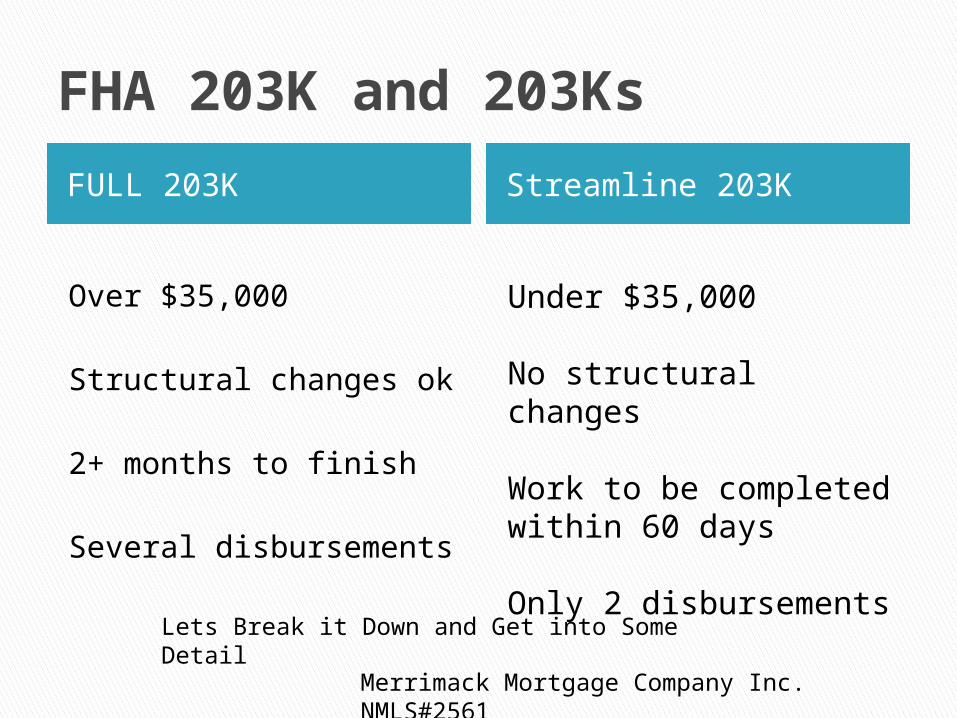

FHA 203K and 203Ks

FULL 203K Streamline 203K

Over $35,000

Structural changes ok

2+ months to finish

Several disbursements

Under $35,000

No structural changes

Work to be completed within 60 days

Only 2 disbursements

Lets Break it Down and Get into Some Detail

Merrimack Mortgage Company Inc. NMLS#2561

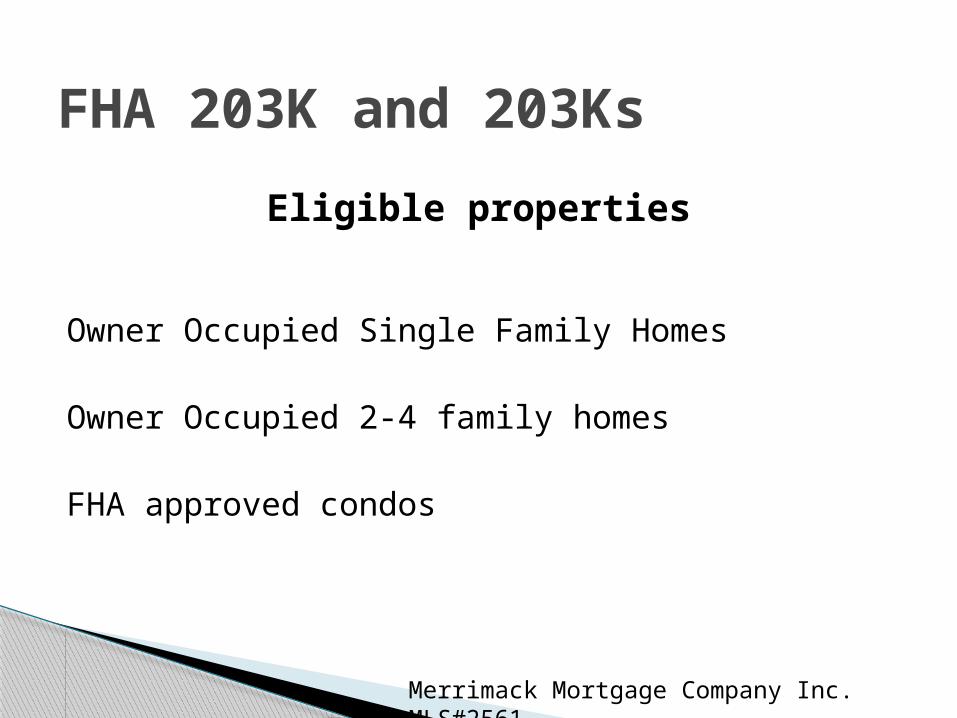

Eligible properties

Owner Occupied Single Family Homes

Owner Occupied 2-4 family homes

FHA approved condos

FHA 203K and 203Ks

Merrimack Mortgage Company Inc. MLS#2561

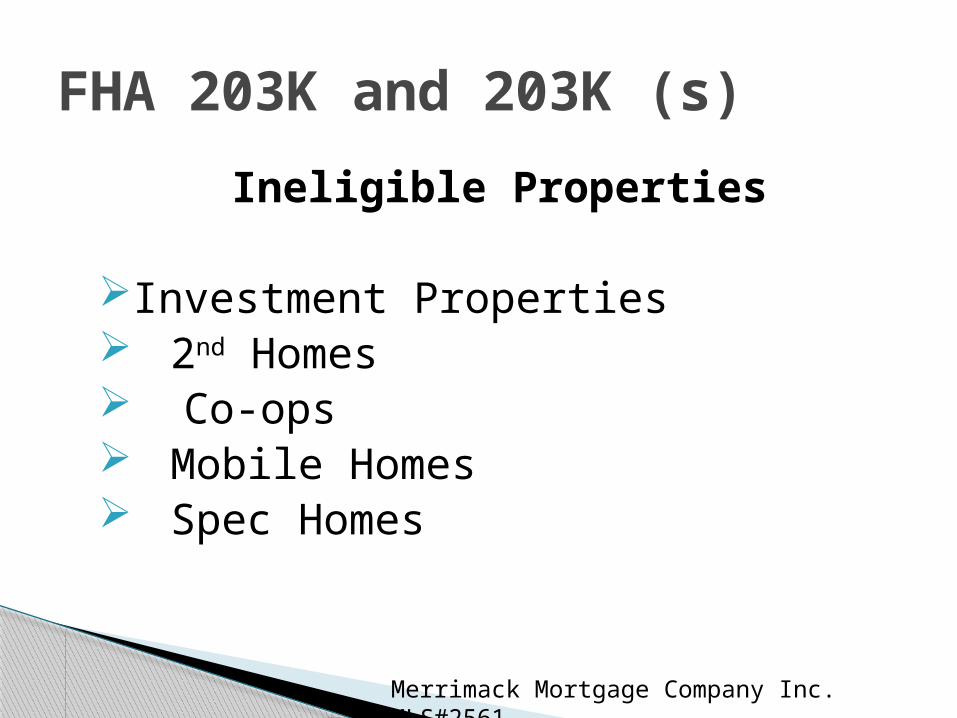

Ineligible Properties

Investment Properties 2nd Homes Co-ops Mobile Homes Spec Homes

FHA 203K and 203K (s)

Merrimack Mortgage Company Inc. NMLS#2561

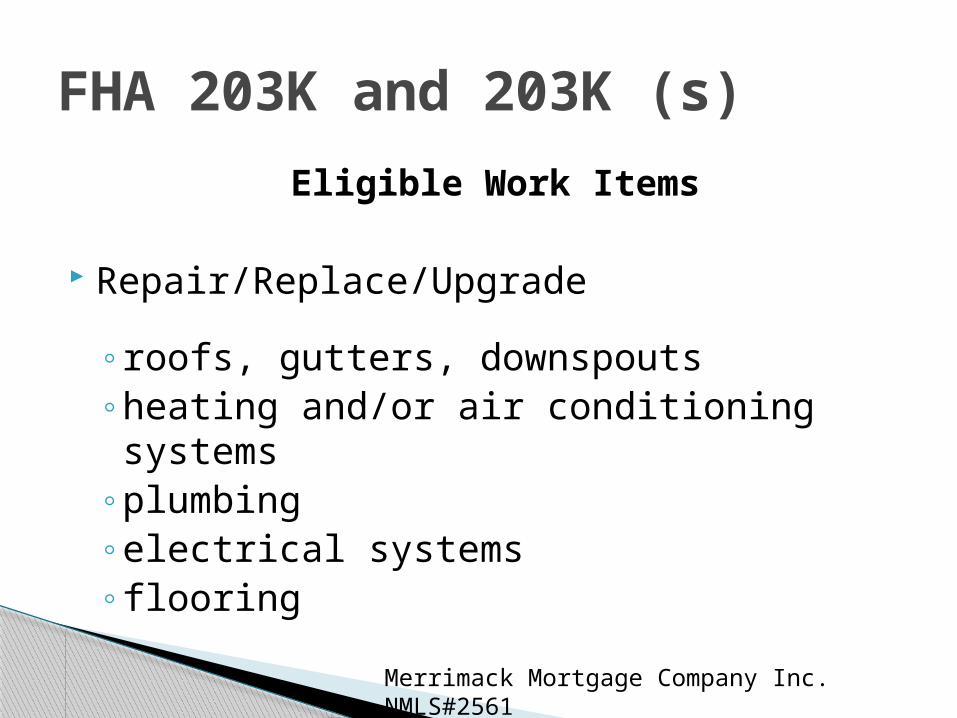

Eligible Work Items

Repair/Replace/Upgrade

◦roofs, gutters, downspouts◦heating and/or air conditioning systems◦plumbing ◦electrical systems◦flooring

FHA 203K and 203K (s)

Merrimack Mortgage Company Inc. NMLS#2561

Eligible Work Items

Repair/Replace/Upgrade

◦septic systems

◦wells

◦decks & porches

FHA 203K and 203K (s)

Merrimack Mortgage Company Inc. NMLS#2561

Eligible Work Items

Minor remodeling with no structural changes

kitchens

bathrooms

basements

Merrimack Mortgage Company Inc. NMLS#2561

FHA 203K and 203K (s)

Eligible Work Items

Weatherization

◦windows

◦doors

◦ insulation

◦roof & attic ventilation

◦siding

FHA 203K and 203K (s)

Merrimack Mortgage Company Inc. NMLS#2561

Eligible Work Items Purchase and installation of appliances

◦ ranges/oven

◦ refrigerators

◦ washers/dryers

◦ dishwashers

◦ built in microwaves

Merrimack Mortgage Company Inc. NMLS#2561

FHA 203K and 203K (s)

Eligible Work Items

lead based paint stabilization or abatement

accessibility improvements for persons with disabilities

FHA 203K and 203K (s)

Merrimack Mortgage Company Inc. NMLS#2561

Eligible Work Items

Painting◦ Interior ◦ Exterior

Basement waterproofing

FHA 203K and 203K (s)

Merrimack Mortgage Company Inc. NMLS#2561

These items are eligible for full 203k only..

Major rehabilitation or remodeling

Relocation of load bearing walls

Repair of structural damage

Merrimack Mortgage Company Inc. NMLS#2561

FHA 203K (full version)

These items are eligible for full 203k only..

Repairs/rehab requiring architecturaldrawings or exhibits

Landscaping or other site amenities

Merrimack Mortgage Company Inc. NMLS#2561

FHA 203K (full version)

These items are eligible for full 203k

Any repair or improvement requiring a work schedule longer than 2 months

Rehabilitation activities that require more than 2 payments per specialized contractor

Required appraisal repairs that are not eligible repairs under the streamline 203K

FHA 203K (full version)

Merrimack Mortgage Company Inc. NMLS#2561

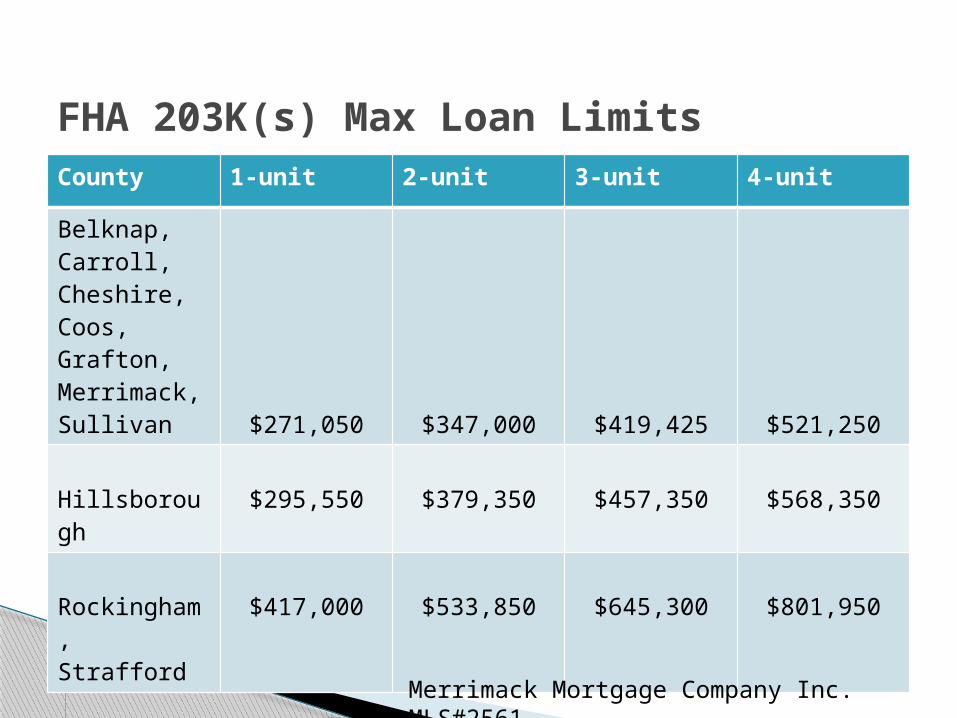

County 1-unit 2-unit 3-unit 4-unit

Belknap, Carroll, Cheshire, Coos, Grafton, Merrimack, Sullivan $271,050 $347,000 $419,425 $521,250

Hillsborough $295,550 $379,350 $457,350 $568,350

Rockingham,Strafford

$417,000 $533,850 $645,300 $801,950

FHA 203K(s) Max Loan Limits

Merrimack Mortgage Company Inc. MLS#2561

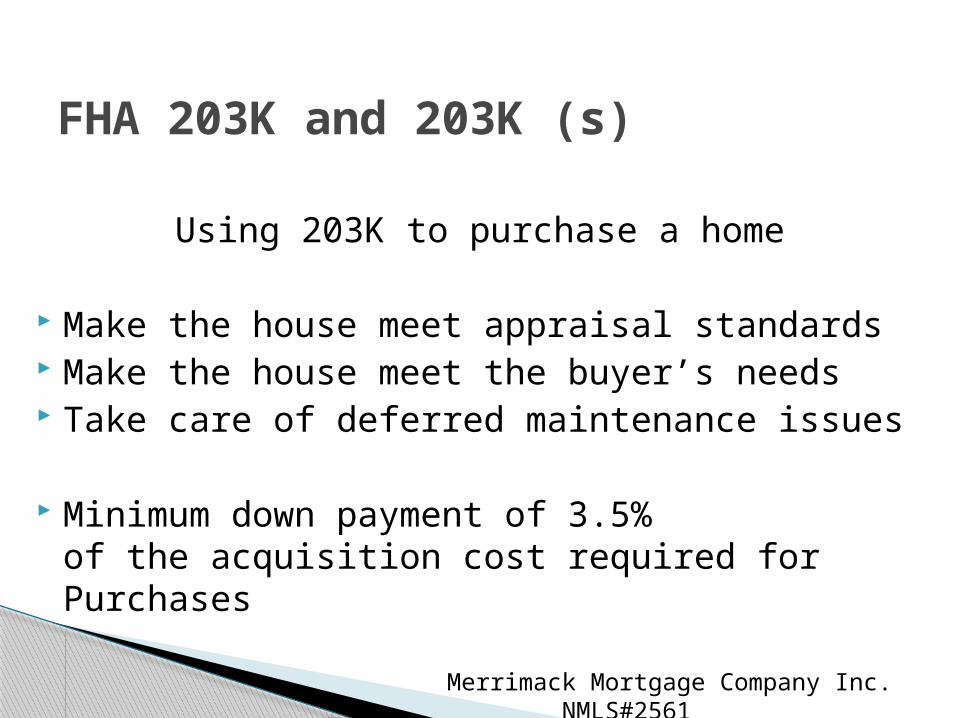

Using 203K to purchase a home

Make the house meet appraisal standards Make the house meet the buyer’s needs Take care of deferred maintenance issues

Minimum down payment of 3.5% of the acquisition cost required for Purchases

FHA 203K and 203K (s)

Merrimack Mortgage Company Inc. NMLS#2561

Using 203K to purchase a home

Down Payment & Loan Amount based on acquisition cost

Sales price = $245,000 Rehab = $ 35,000 Acquisition Cost = $ 280,000 3.5% down = -$ 9,800 Loan $270,200

FHA 203K and 203K (s)

Merrimack Mortgage Company Inc. NMLS#2561

Example Calculation of Down Payment

Sales price = $245,000+Rehab $ 35,000= Acquisition Cost $280,000

$280,000 X 3.5% = $9,800 minimum down

$280,000 - $9,800 = $270,200 max loan

FHA Max loan limits per county apply

FHA 203K and 203Ks

Merrimack Mortgage Company Inc. MLS#2561

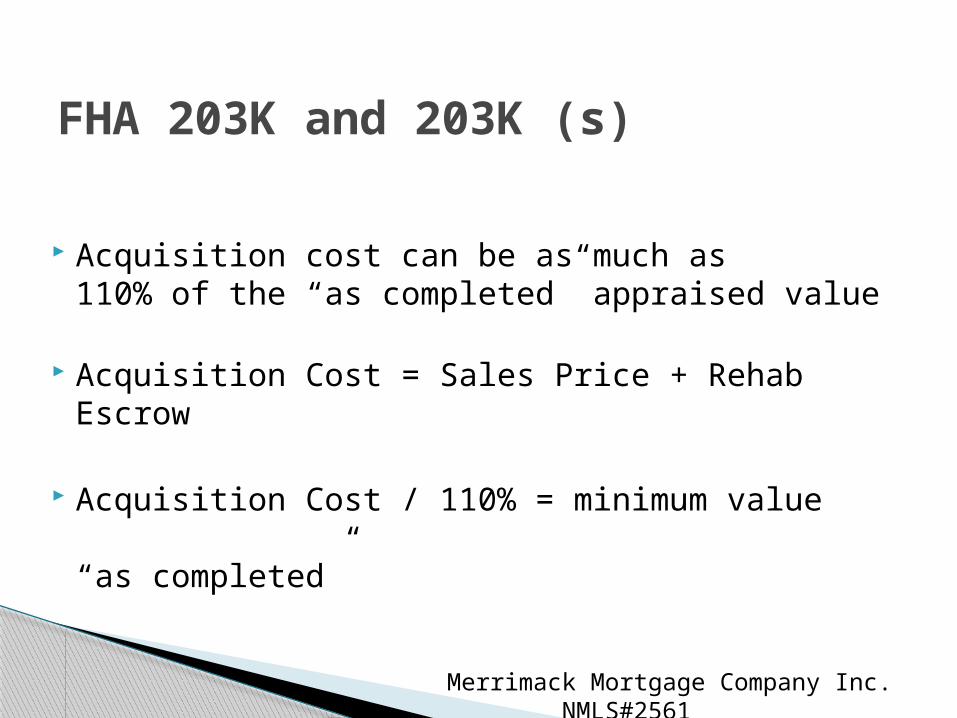

Acquisition cost can be as much as110% of the “as completed” appraised value

Acquisition Cost = Sales Price + Rehab Escrow

Acquisition Cost / 110% = minimum value “as completed”

FHA 203K and 203K (s)

Merrimack Mortgage Company Inc. NMLS#2561

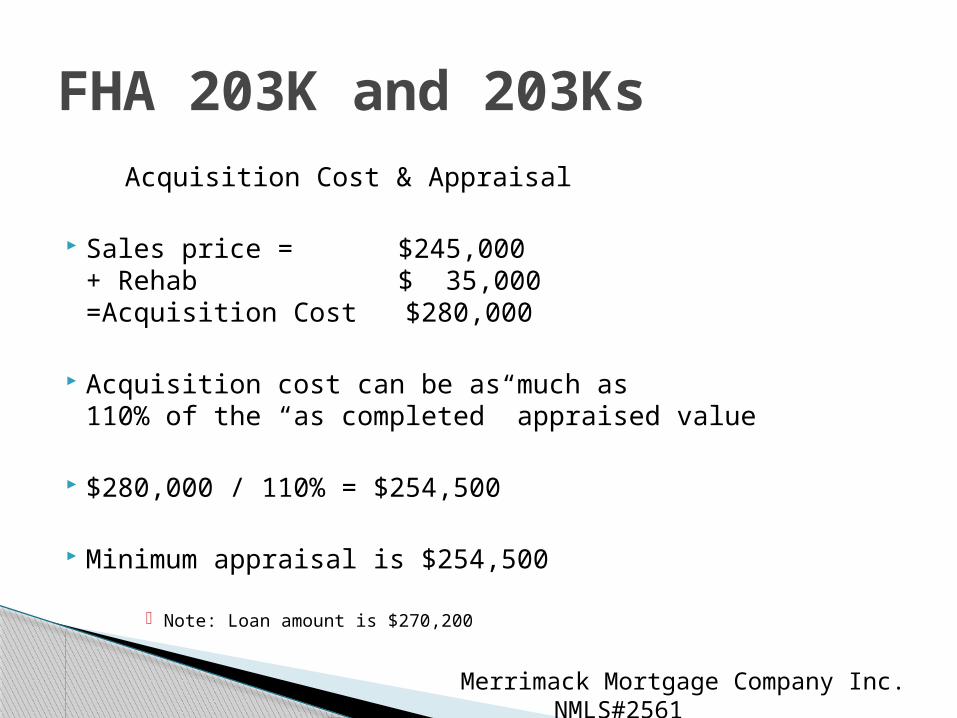

Acquisition Cost & Appraisal

Sales price = $245,000+ Rehab $ 35,000=Acquisition Cost $280,000

Acquisition cost can be as much as110% of the “as completed” appraised value

$280,000 / 110% = $254,500

Minimum appraisal is $254,500

Note: Loan amount is $270,200

FHA 203K and 203Ks

Merrimack Mortgage Company Inc. NMLS#2561

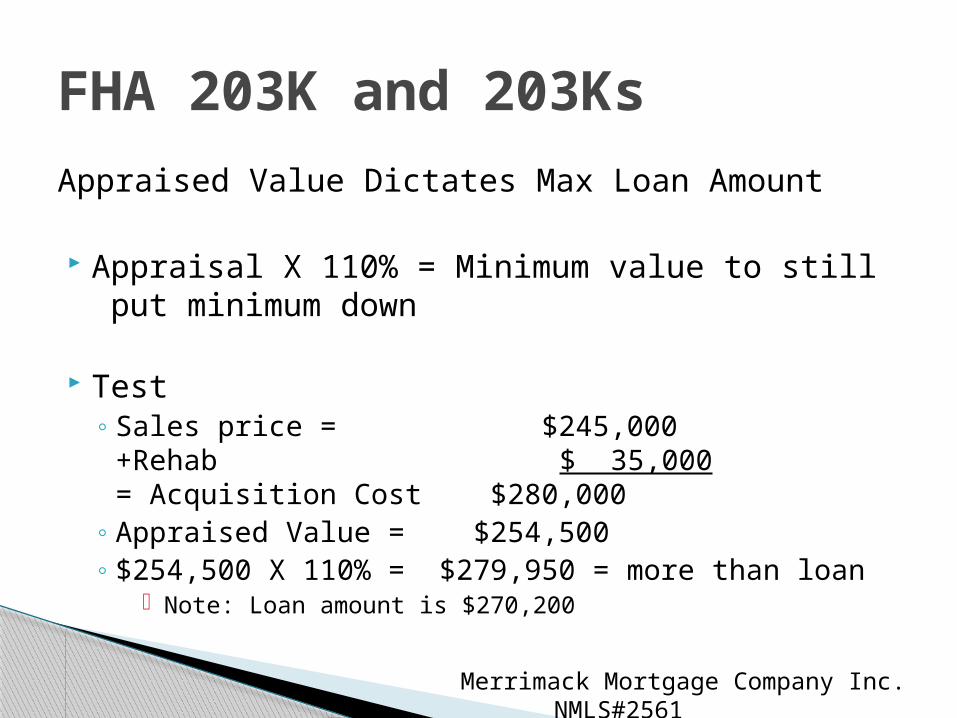

Appraised Value Dictates Max Loan Amount

Appraisal X 110% = Minimum value to still put minimum down

Test◦ Sales price = $245,000

+Rehab $ 35,000= Acquisition Cost $280,000

◦ Appraised Value = $254,500◦ $254,500 X 110% = $279,950 = more than loan

Note: Loan amount is $270,200

FHA 203K and 203Ks

Merrimack Mortgage Company Inc. NMLS#2561

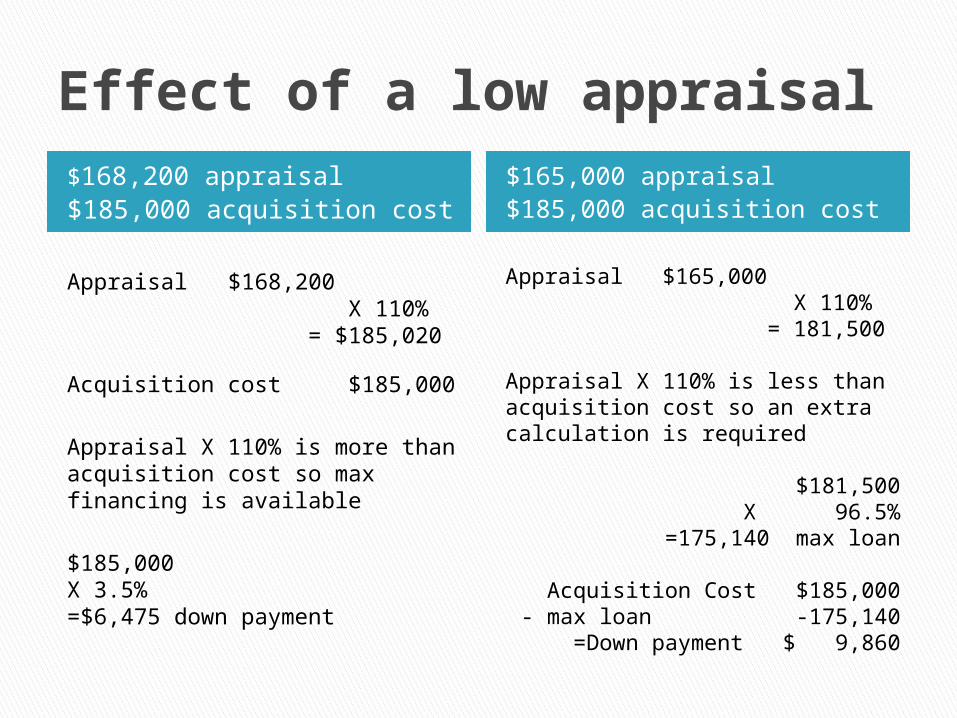

Effect of a low appraisal $168,200 appraisal$185,000 acquisition cost

$165,000 appraisal$185,000 acquisition cost

Appraisal $168,200 X 110% = $185,020

Acquisition cost $185,000

Appraisal X 110% is more than acquisition cost so max financing is available

$185,000X 3.5%=$6,475 down payment

Appraisal $165,000 X 110% = 181,500

Appraisal X 110% is less thanacquisition cost so an extra calculation is required

$181,500X 96.5%

=175,140 max loan

Acquisition Cost $185,000- max loan -175,140

=Down payment $ 9,860

Available for Refinances too!

Buy “as is” and start rehab processafter closing at new owner’s convenience

Existing owners can do home improvements Maximum Loan to Value is 96.5% of

“as completed” value for Refinances

FHA 203K and 203K (s)

Merrimack Mortgage Company Inc. NMLS#2561

Appliances

Identify appliances by model Estimates from stores should include installation in the price

A labor estimate from the installing contractor is necessary when the price does not include installation

FHA 203K and 203K (s)

Merrimack Mortgage Company Inc. NMLS#2561

All contractors must provide licenses where required by state or local municipalities and/or the licenses of specialty sub-contractors like plumbers or electricians

For properties built before 1978, contractors must be lead paint certified.

Contractors cannot be related to the borrower

Merrimack Mortgage Company Inc. NMLS#2561

FHA 203K and 203K (s)

Contractor credentials, work experience, licensing information, previous work preformed, client and vendor references must be evaluated.

All contractors must provide a W9

All Contractors to sign the 203K agreement

FHA 203K and 203K (s)

Merrimack Mortgage Company Inc. NMLS#2561

203K contractor agreement

203K contractor agreement

Work not covered by this agreement will not be required unless it is required by reasonable inference as being necessary to produce the intended result.

No additional repairs will be required unless they come up as a result of work in process.

203K contractor agreement

By executing this Agreement, the contractor represents that he/she has visited the site and understands local conditions, including state and local building regulations and conditions under which the work is to be performed.

203K contractor agreement

Owner: Unless otherwise provided for in the Agreement, the owner will secure and pay for necessary easements, exceptions from zoning requirements, or other actions which must precede the approval of a permit for this project. If owner fails to do so then the contract is void.

203K contractor agreement

If the contractor fails to correct defective work or persistently fails to carry out the work in accordance with the agreement or general provisions, the owner may order the contractor in writing to stop such work, or apart of the work, until the cause for the order has been eliminated.

203K contractor agreement

The contractor will supervise and direct the work and the work of all subcontractors.

He/she will use the best skill and attention and will be solely responsible for all construction methods and materials and for coordinating all portions of the work.

The contractor must correct promptly any work of his/her own or his/her subcontractors found to be defective or not complying with the terms of the contract

203K contractor agreement

The contractor will not employ any subcontractor to whom the owner may have

a reasonable objection

The owner will not require the contractor to employ any subcontractor to whom the contractor has a reasonable objection.

203K contractor agreement

All contractors and subcontractors will be afforded reasonable opportunity for the storage of materials and equipment by the owner and by each other.

Any costs arising by defective or ill-timed work will be borne by the responsible party.

203K contractor agreement

The contractor will maintain order and discipline among employees and will not assign anyone unfit for the task.

The contractor is responsible for, and indemnifies the Owner against, acts and omissions of employees, subcontractors and their employees, or others performing the work under this Agreement with the contractor.

203K contractor agreement

Unless otherwise specified in the Agreement, the contractor will provide for and/or pay for all labor, materials, equipment, tools, machinery, transportation, and other goods, facilities, and services necessary for the proper execution and completion of the work.

203K contractor agreement

The contractor warrants to the owner that all materials and equipment incorporated are new and that all work will be of good quality and free of defects or faults.

203K contractor agreement

The contractor will pay all sales, use and other taxes related to the work and will secure and pay for building permits and/or other permits, fees, inspections and licenses necessary for the completion of the work unless otherwise specified in the Agreement.

203K contractor agreement

The contractor will comply with all rules, regulations, laws, ordinances and orders of any public authority or HUD inspector bearing on the performance of the work.

The contractor will provide shop drawings, samples, product data or other information provided for in this Agreement, where necessary.

203K contractor agreement

Work by Owner or Other Contractors

The owner reserves the right to perform work related to the project, but which is not a part of this Agreement

The owner reserves the right to award separate contracts in connection with other portions of the project not detailed in this Agreement.

203K contractor agreement

Claims or disputes relating to the Agreement or General Provisions will be resolved by the Construction Industry Arbitration Rules of the American Arbitration Association (AAA) unless both parties mutually agree to other methods.

The notice of the demand for arbitration must be filed in writing with the other party to this Agreement and with the AAA and must be made in a reasonable time after the dispute has arisen.

The award rendered by the arbitrator(s) will be considered final and judgment may be entered upon it in accordance with applicable law in any court having jurisdiction thereof.

203K contractor agreement

The contractor will keep the owner’s residence free from waste or rubbish resulting from the work.

All waste, rubbish, tools, construction materials, and machinery will be removed promptly after completion of the work by the contractor.

203K contractor agreement

With respect to the scheduled completion of the work, time is of the essence.

If the contractor is delayed at anytime in the progress of the work by change orders, fire, labor disputes, acts of God or other causes beyond the contractor’s control, the completion schedule for the work or affected parts of the work may be extended by the same amount of time caused by the delay.

203K contractor agreement

With respect to the scheduled completion of the work, time is of the essence.

The contractor must begin work no later than 30 days after loan closing and will not cease work for more than 30 consecutive days.

203K contractor agreement

Payments may be withheld because of

◦ (1) defective work not remedied

◦ (2) failure of contractor to make proper payments to subcontractors, workers, or suppliers

◦ (3) persistent failure to carry out work in acceptance with this Agreement o with these general conditions

◦ (4) legal claims

203K contractor agreement

Final payment will be due after submission of receipts or other evidence of payment covering all subcontractors or suppliers who could file a lien.

If liens are found, final payment will be due after complete release of any and all liens arising out of the contract.

The contractor agrees to indemnify the Owner against such liens and will refund all monies including costs and reasonable attorney’s fees paid by the owner in discharging the liens.

203K contractor agreement

The contractor is responsible for initiating, maintaining, and supervising all necessary or required safety programs.

The contractor must comply with all applicable laws, regulations, ordinances, orders or laws of federal, state, county or local governments.

The contractor will indemnify the owner for all property loss or damage to the owner caused by his/her employees or his/her direct or subcontractors.

203K contractor agreement

The contractor will purchase and maintain such insurance necessary to protect from claims under workers compensation and from any damage to the owner(s) property from the conduct of this contract.

203K contractor agreement

The owner may order changes, additions or modifications (using form HUD-92577) without invalidating the contract.

Such changes must be in writing and signed by the owner and accepted by the lender.

Not all change order requests may be accepted by the lender, therefore, the contractor proceeds at his/her own risk if work is completed without an accepted change order.

203K contractor agreement

The contractor will provide a one-year warranty on all labor and materials used in the rehabilitation of the property.

This warranty must extend one year from the date of completion of the contract.

This warranty must extend for longer than one year if prescribed by law or otherwise specified by other terms of this contract.

203K contractor agreement

If the owner fails to make a payment under the terms of this Agreement, through no fault of the contractor, the contractor may, upon ten working days written notice to the owner, and if not satisfied, terminate this Agreement.

The owner will be responsible for paying the contractor for all work completed.

If the contractor fails or neglects to carry out the terms of the contract, the owner, after ten working days written notice to the contractor, may terminate this Agreement.

203K contractor agreement

Disbursement of Funds

All Rehab funds (not disbursed at closing)are placed in Escrow

Any unused funds when project is completed must be applied to reduce the balance of the mortgage or the borrower may elect to pay for any additional elective improvements or repairs to the property.

FHA 203K and 203K(s)

Merrimack Mortgage Company Inc. NMLS#2561

All rehab work must be performed by a qualified and experienced contractor, chosen by the borrower and completed in a workmanlike manner

Borrowers may not use relatives as their contractors

FHA 203K and 203K(s)

Merrimack Mortgage Company Inc. NMLS#2561

Maximum rehab amount is $35,000 for streamline This amount includes a contingency reserve and certain fees that are financeable.

(roughly $31,500 for actual work to be performed)

Merrimack Mortgage Company Inc. NMLS#2561

Program Specific RequirementsStreamline FHA 203K(s)

No more than 2 payments per specialized contractor

◦ 1st for material costs (not to exceed 50% of costs)◦ 2nd payment upon completion◦ All required permits due at 1st disbursement

No consultant, plan reviewer or specification or repairs/work write-up required on streamline

Program Specific RequirementsStreamline FHA 203K (s)

Merrimack Mortgage Company Inc. NMLS#2561

Self- Help is strongly discouraged unless applicant’s ability to completely perform the work in a timely and workman like manner is self-evident and easily documented.

Lender /Investor specific pre-approval required for self-help

Most lenders will not allow self-help

Contractors not to be related to borrowers

Program Specific RequirementsFull FHA 203K

Merrimack Mortgage Company Inc. NMLS#2561

Fee Consultant Required

Borrower must use an FHA Fee Consultant

Fee Consultant inspects the home and reviews the contractor’s proposal

Fee consultant uses the Work write up form See Exhibit B

Fee consultant analyzes the feasibility of the project and can also require additional items so the property will meet FHA standards

Merrimack Mortgage Company Inc. NMLS#2561

Program Specific Requirements Full FHA 203K

Fee Consultant Required

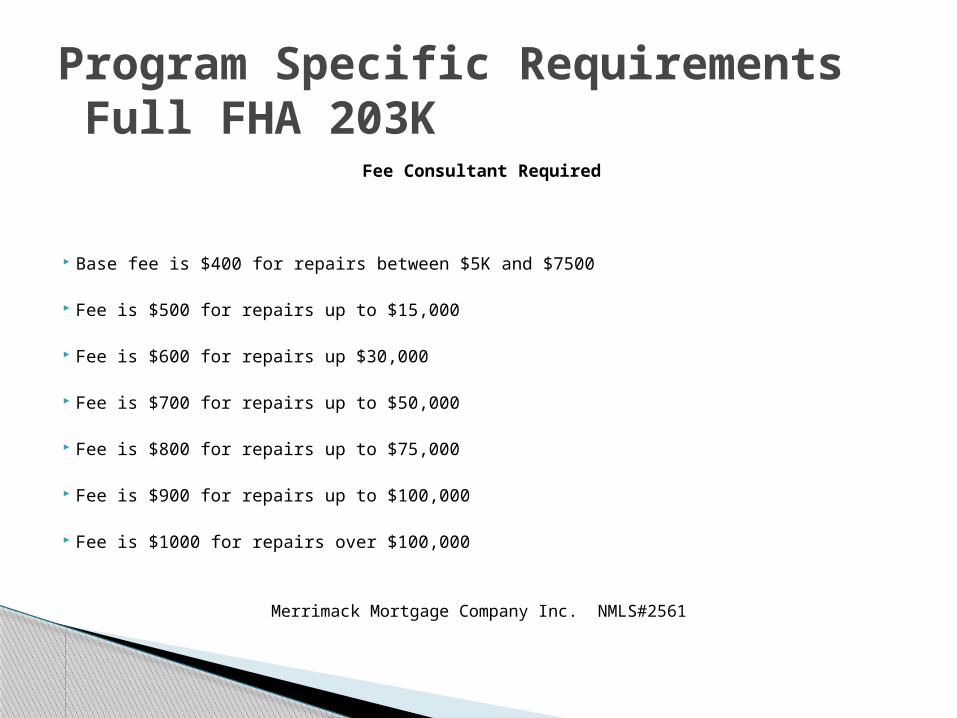

Base fee is $400 for repairs between $5K and $7500

Fee is $500 for repairs up to $15,000

Fee is $600 for repairs up $30,000

Fee is $700 for repairs up to $50,000

Fee is $800 for repairs up to $75,000

Fee is $900 for repairs up to $100,000

Fee is $1000 for repairs over $100,000

Merrimack Mortgage Company Inc. NMLS#2561

Program Specific Requirements Full FHA 203K

What can the listing agent do when the house needs repairs/renovations?

What can the buyer agent do when the house needs repairs/renovations?

FHA 203K or 203Ks Discussion

Merrimack Mortgage Company Inc. NMLS#2561

FHA 203K or 203Ks Questions?

Merrimack Mortgage Company Inc. NMLS#2561

Lets talk about RD now…

Also known as USDA Farmer’s Home Rural Development

Merrimack Mortgage Company Inc. NMLS#2561

Rural Development

For RD eligible buyers and properties only

Income Limits Apply

Geographical Limitations Apply

Single Family and Condo only

Owner Occupied only

Rural Development

Merrimack Mortgage Company Inc. NMLS#2561

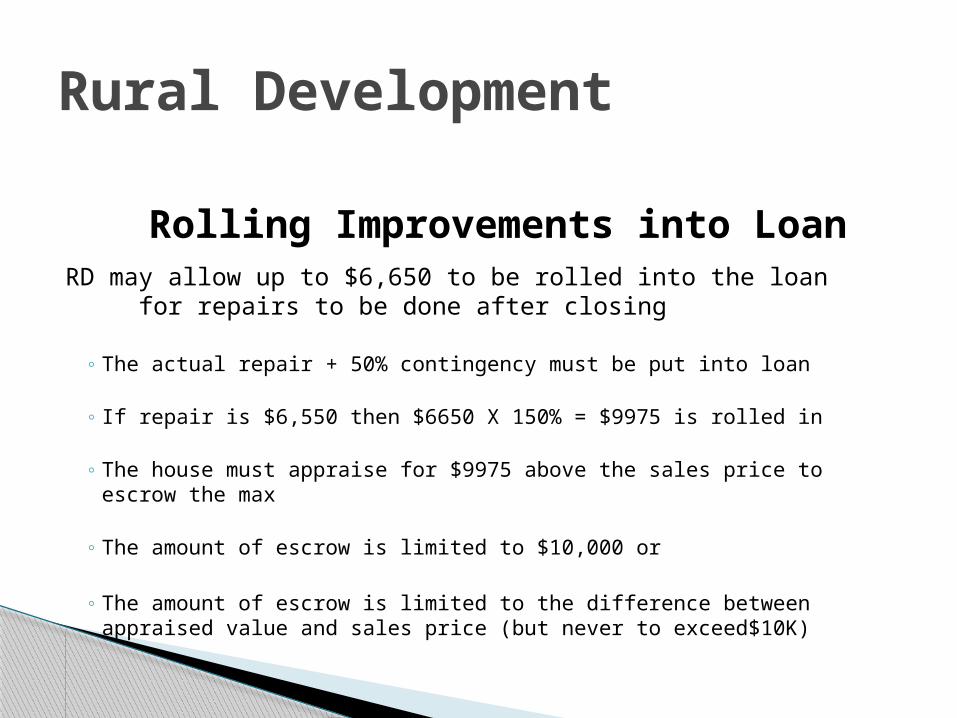

Rolling Improvements into LoanRD may allow up to $6,650 to be rolled into the loan for repairs to be done after closing

◦ The actual repair + 50% contingency must be put into loan

◦ If repair is $6,550 then $6650 X 150% = $9975 is rolled in

◦ The house must appraise for $9975 above the sales price to escrow the max

◦ The amount of escrow is limited to $10,000 or

◦ The amount of escrow is limited to the difference between appraised value and sales price (but never to exceed$10K)

Rural Development

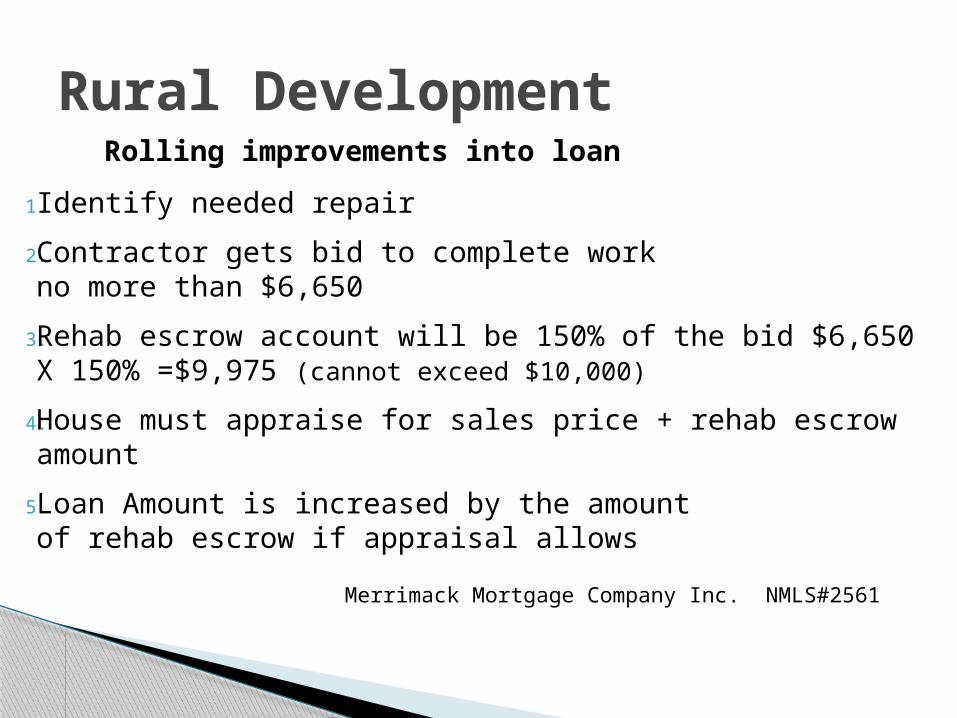

Rolling improvements into loan

1. Identify needed repair

2. Contractor gets bid to complete work no more than $6,650

3. Rehab escrow account will be 150% of the bid $6,650 X 150% =$9,975 (cannot exceed $10,000)

4. House must appraise for sales price + rehab escrow amount

5. Loan Amount is increased by the amountof rehab escrow if appraisal allows

Merrimack Mortgage Company Inc. NMLS#2561

Rural Development

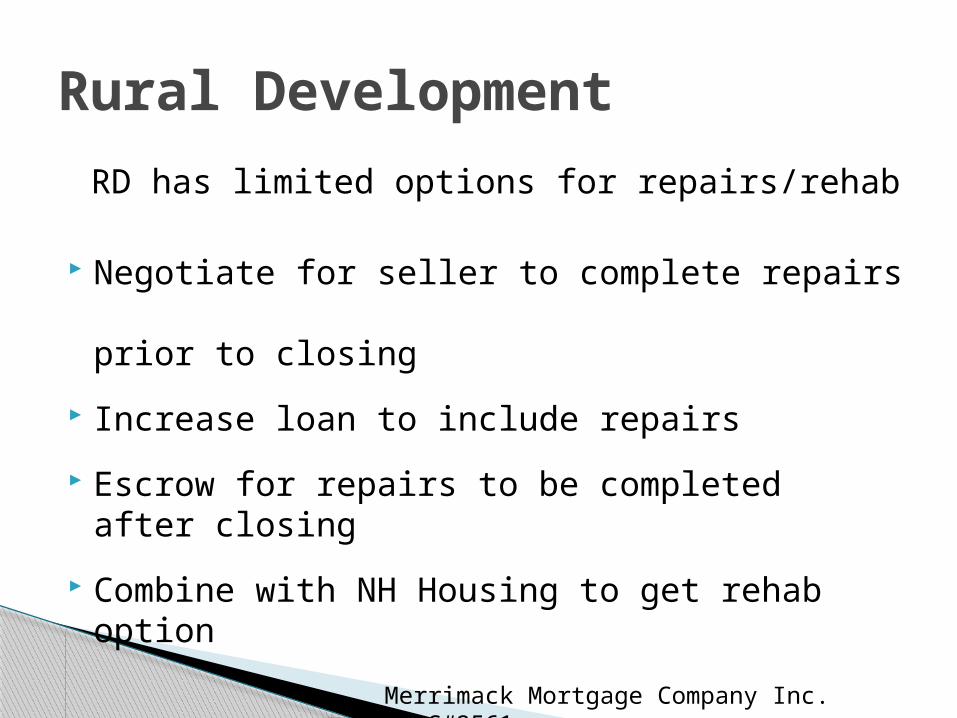

RD has limited options for repairs/rehab

Negotiate for seller to complete repairs prior to closing

Increase loan to include repairs

Escrow for repairs to be completed after closing

Combine with NH Housing to get rehab option

Rural Development

Merrimack Mortgage Company Inc. NMLS#2561

Escrowing for improvements

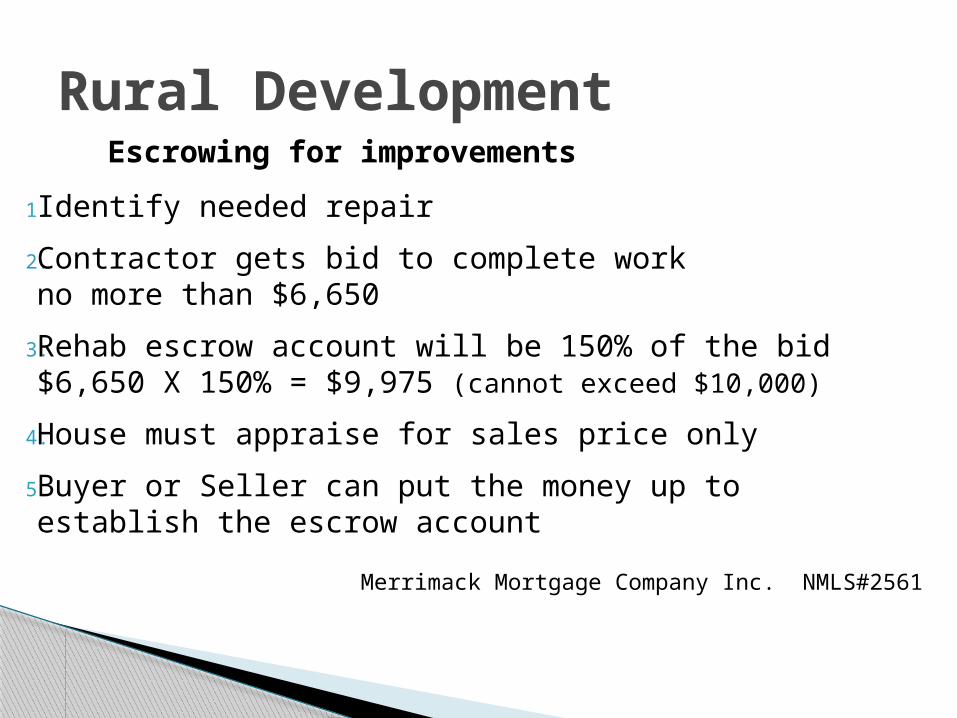

1. Identify needed repair

2. Contractor gets bid to complete work no more than $6,650

3. Rehab escrow account will be 150% of the bid $6,650 X 150% = $9,975 (cannot exceed $10,000)

4. House must appraise for sales price only

5. Buyer or Seller can put the money up to establish the escrow account

Merrimack Mortgage Company Inc. NMLS#2561

Rural Development

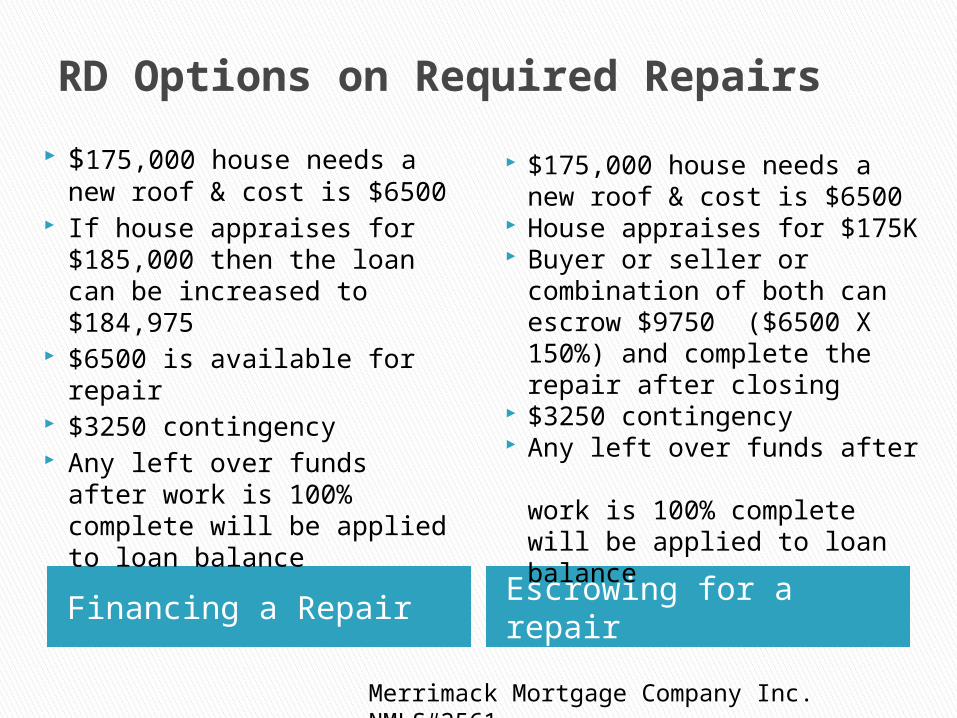

RD Options on Required Repairs

Financing a Repair Escrowing for a repair

$175,000 house needs a new roof & cost is $6500

If house appraises for $185,000 then the loan can be increased to $184,975

$6500 is available for repair

$3250 contingency Any left over funds after

work is 100% complete will be applied to loan balance

$175,000 house needs a new roof & cost is $6500

House appraises for $175K Buyer or seller or

combination of both can escrow $9750 ($6500 X 150%) and complete the repair after closing

$3250 contingency Any left over funds after

work is 100% complete will be applied to loan balance

Merrimack Mortgage Company Inc. NMLS#2561

Repairs completed before closing

Repairs completed after closing◦Repairs rolled into loan◦Buyer or seller escrows

Combine with NH Housing

Questions on RD?

New Hampshire Housing Finance Authority

Not limited to 1st time buyers

Income Limits Apply

Flex Programs offer rehab options

NH Housing

New Hampshire Housing Finance Authority

Basic FHA 203Ks guidelines apply

Contractor requirements same as 203Ks

Rehab options exist combining with either FHA or RD

NH Housing

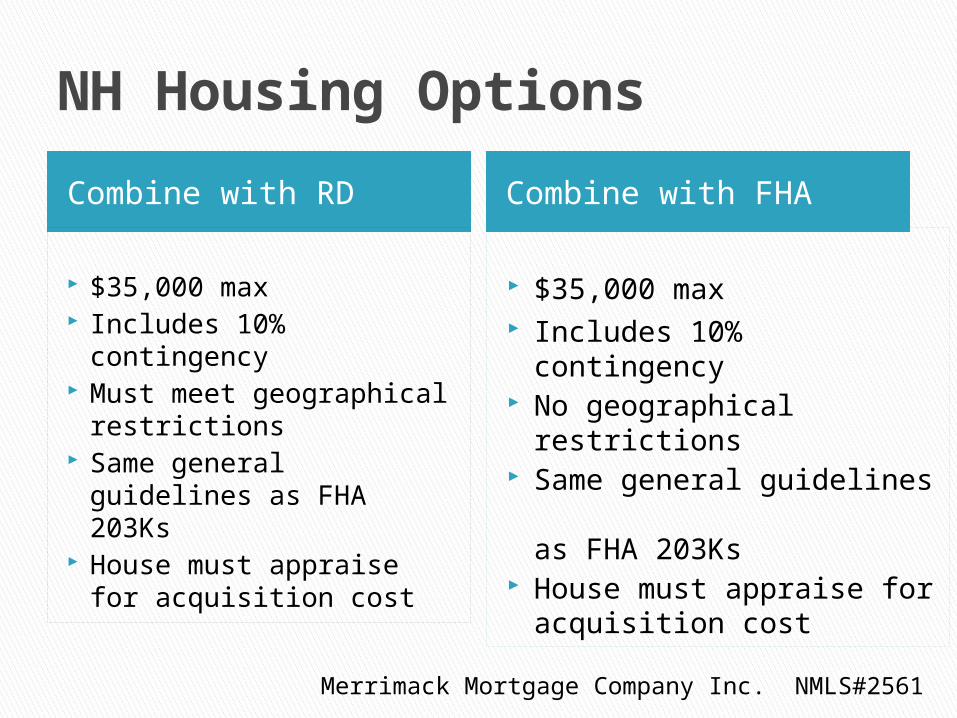

NH Housing Options

Combine with RD Combine with FHA

$35,000 max Includes 10%

contingency Must meet geographical

restrictions Same general

guidelines as FHA 203Ks House must appraise for

acquisition cost

$35,000 max Includes 10% contingency No geographical

restrictions Same general guidelines

as FHA 203Ks House must appraise for

acquisition cost

Merrimack Mortgage Company Inc. NMLS#2561

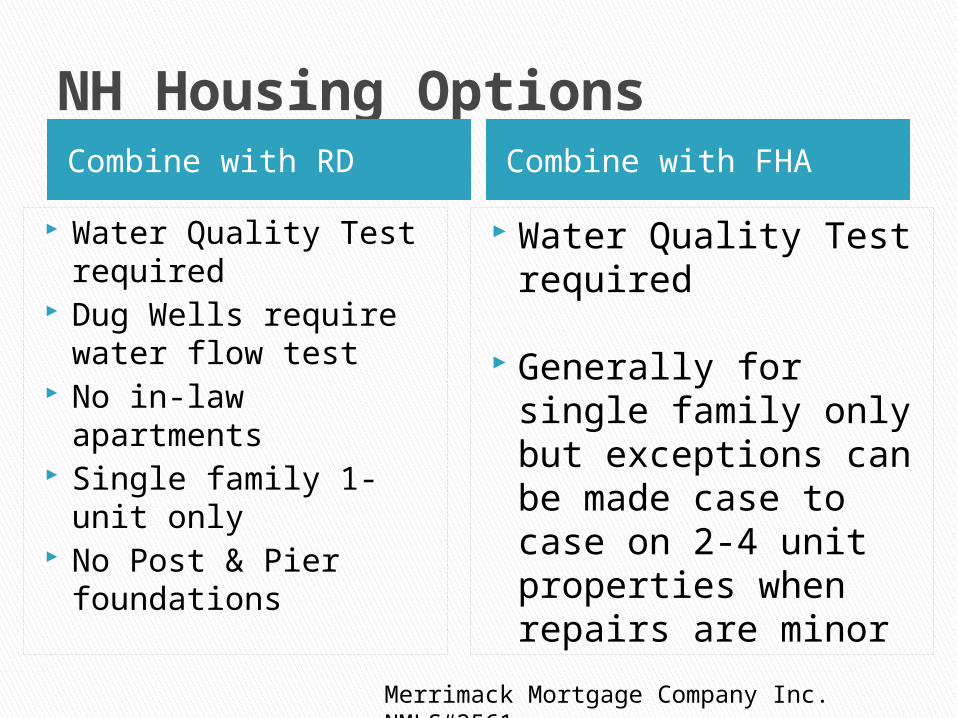

NH Housing Options Combine with RD Combine with FHA

Water Quality Test required

Dug Wells require water flow test

No in-law apartments Single family 1-unit

only No Post & Pier

foundations

Water Quality Test required

Generally for single family only but exceptions can be made case to case on 2-4 unit properties when repairs are minor

Merrimack Mortgage Company Inc. NMLS#2561

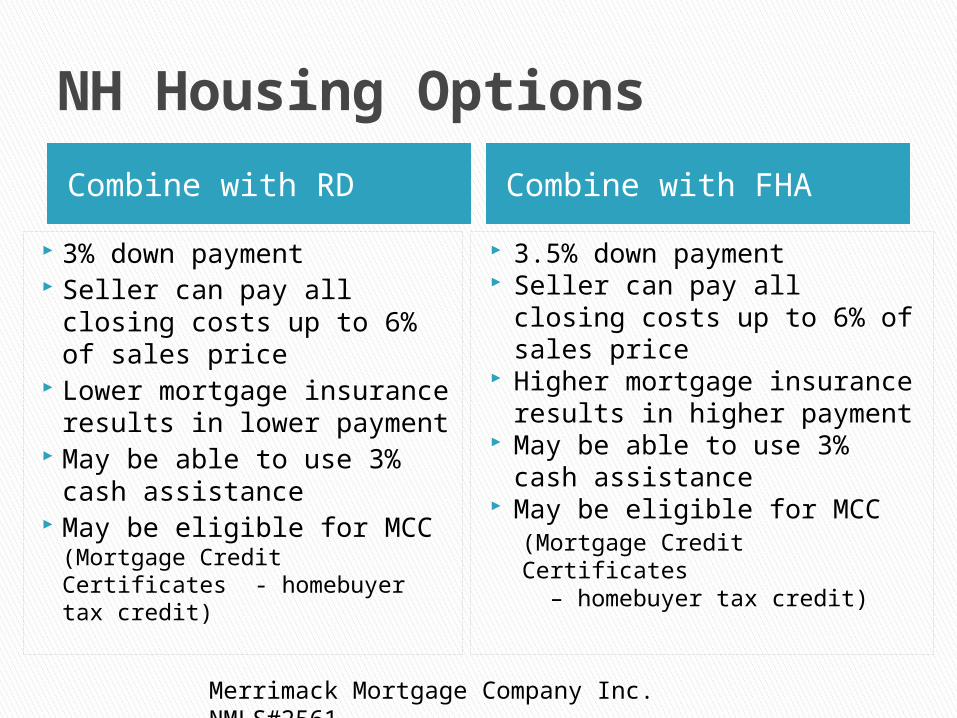

NH Housing Options

Combine with RD Combine with FHA

3% down payment Seller can pay all closing

costs up to 6% of sales price

Lower mortgage insurance results in lower payment

May be able to use 3% cash assistance

May be eligible for MCC(Mortgage Credit Certificates - homebuyer tax credit)

3.5% down payment Seller can pay all closing

costs up to 6% of sales price

Higher mortgage insuranceresults in higher payment

May be able to use 3% cash assistance

May be eligible for MCC(Mortgage Credit Certificates – homebuyer tax credit)

Merrimack Mortgage Company Inc. NMLS#2561

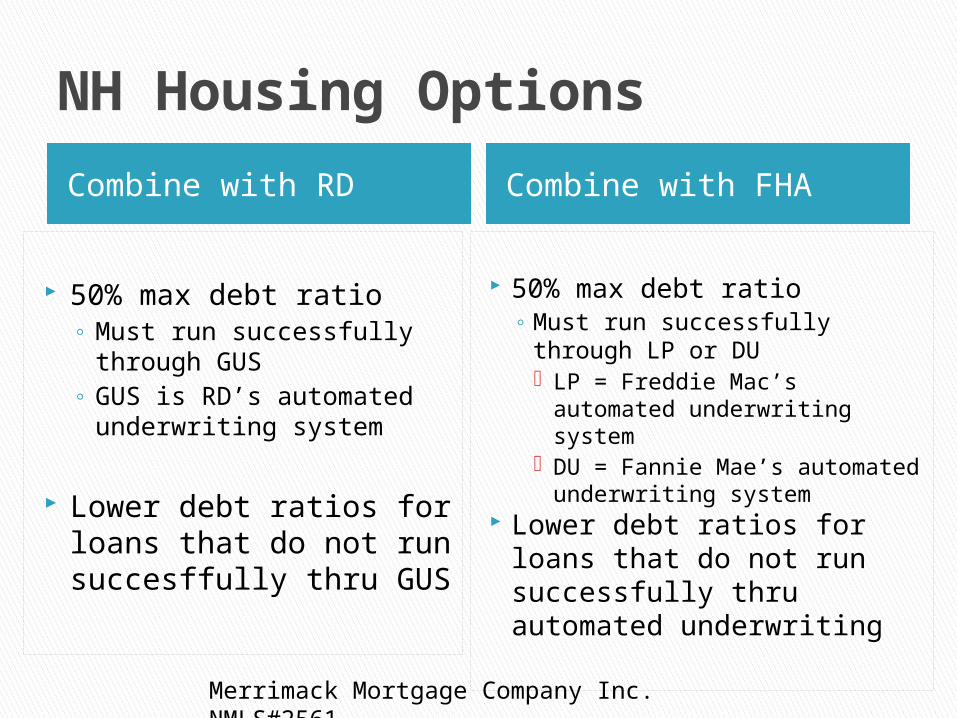

NH Housing Options

Combine with RD Combine with FHA

50% max debt ratio ◦ Must run successfully

through GUS◦ GUS is RD’s automated

underwriting system

Lower debt ratios for loans that do not run succesffully thru GUS

50% max debt ratio◦ Must run successfully through

LP or DU LP = Freddie Mac’s automated

underwriting system DU = Fannie Mae’s automated

underwriting system Lower debt ratios for loans

that do not run successfully thru automated underwriting

Merrimack Mortgage Company Inc. NMLS#2561

NH Housing Options

Combine with RD Combine with FHA

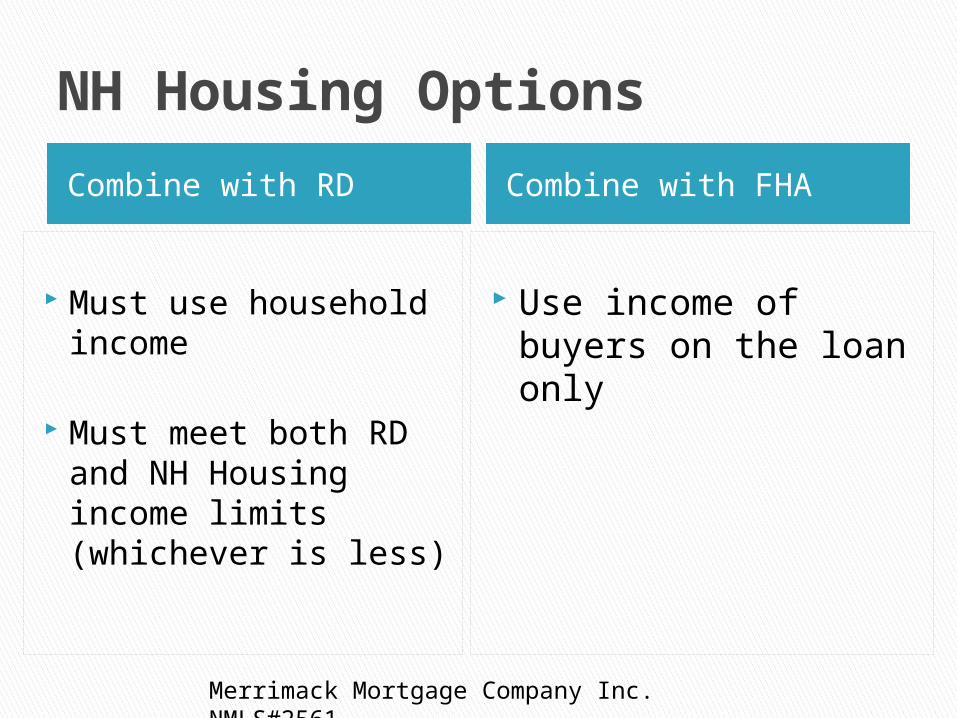

Must use household income

Must meet both RD and NH Housing income limits(whichever is less)

Use income of buyers on the loan only

Merrimack Mortgage Company Inc. NMLS#2561

Questions? Comments?

www.goNewHamphsireHousing.com

NH Housing Finance Authority

Fannie May Home Style

Fannie Mae Homepath being discontinued

Bank & Credit Union Product

Conventional Options

Merrimack Mortgage Company Inc. NMLS#2561

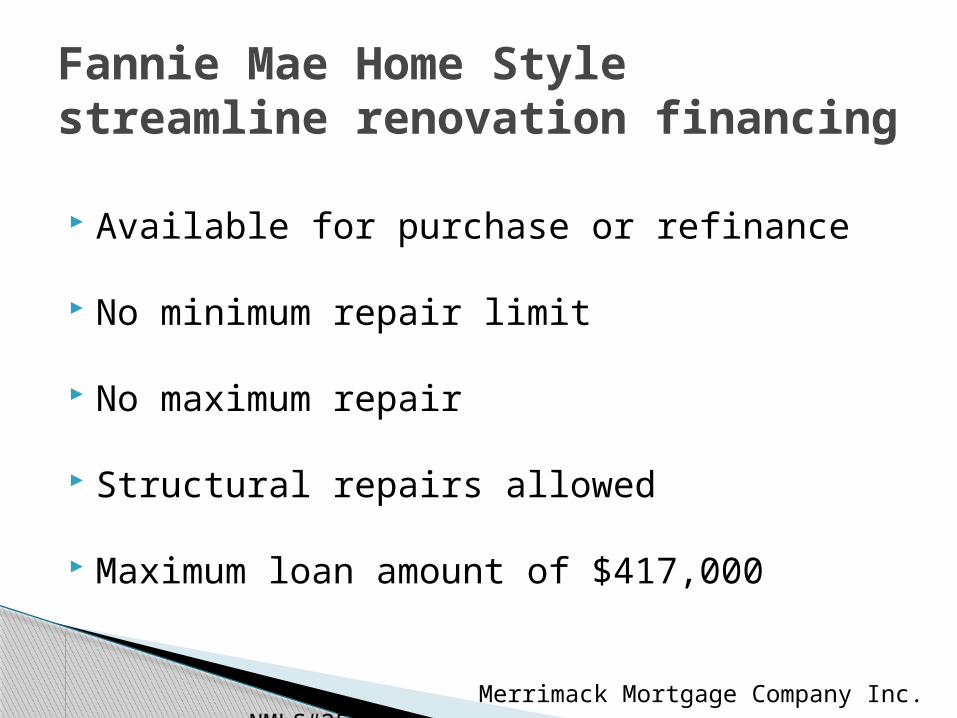

Available for purchase or refinance

No minimum repair limit

No maximum repair

Structural repairs allowed

Maximum loan amount of $417,000

Fannie Mae Home Stylestreamline renovation financing

Merrimack Mortgage Company Inc. NMLS#2561

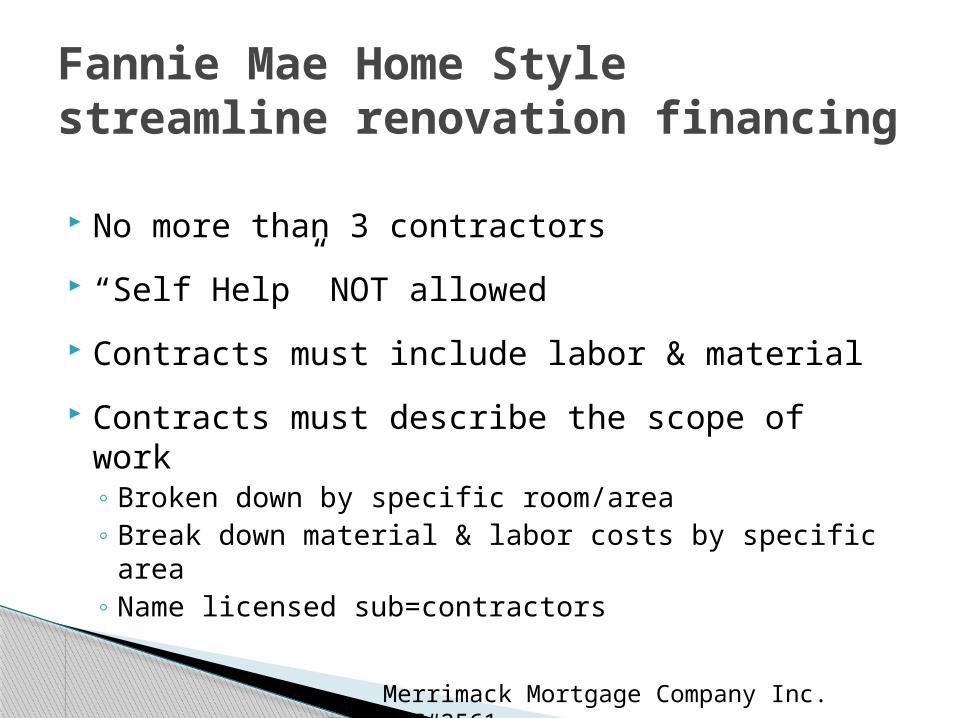

No more than 3 contractors

“Self Help” NOT allowed

Contracts must include labor & material

Contracts must describe the scope of work◦ Broken down by specific room/area◦ Break down material & labor costs by specific

area◦ Name licensed sub=contractors

Fannie Mae Home Stylestreamline renovation financing

Merrimack Mortgage Company Inc. NMLS#2561

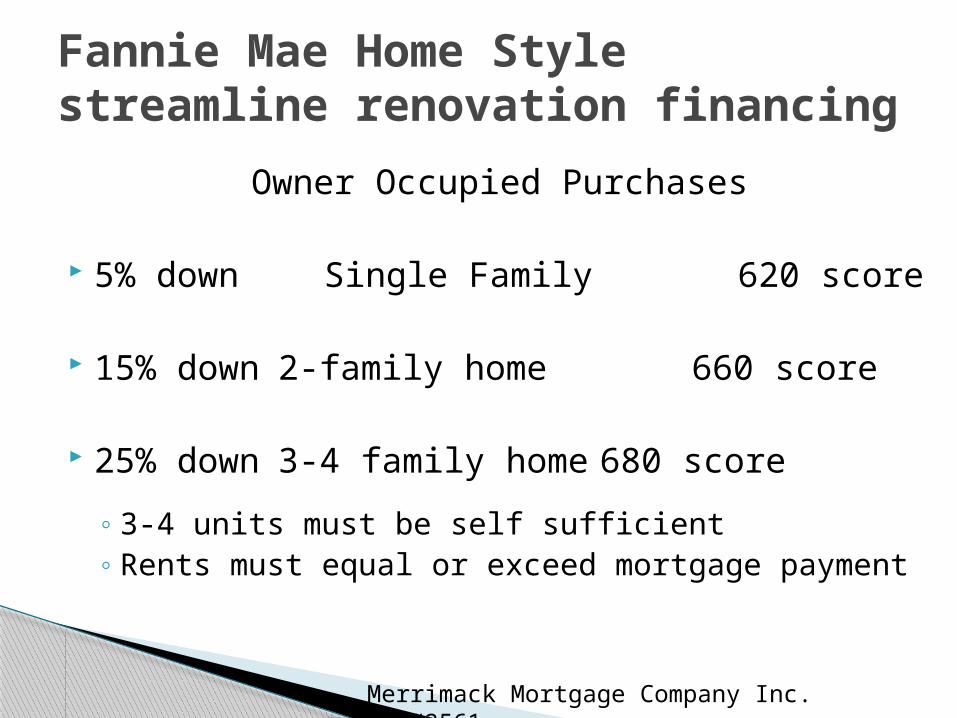

Owner Occupied Purchases

5% down Single Family 620 score

15% down2-family home 660 score

25% down3-4 family home 680 score

◦ 3-4 units must be self sufficient◦ Rents must equal or exceed mortgage payment

Fannie Mae Home Stylestreamline renovation financing

Merrimack Mortgage Company Inc. NMLS#2561

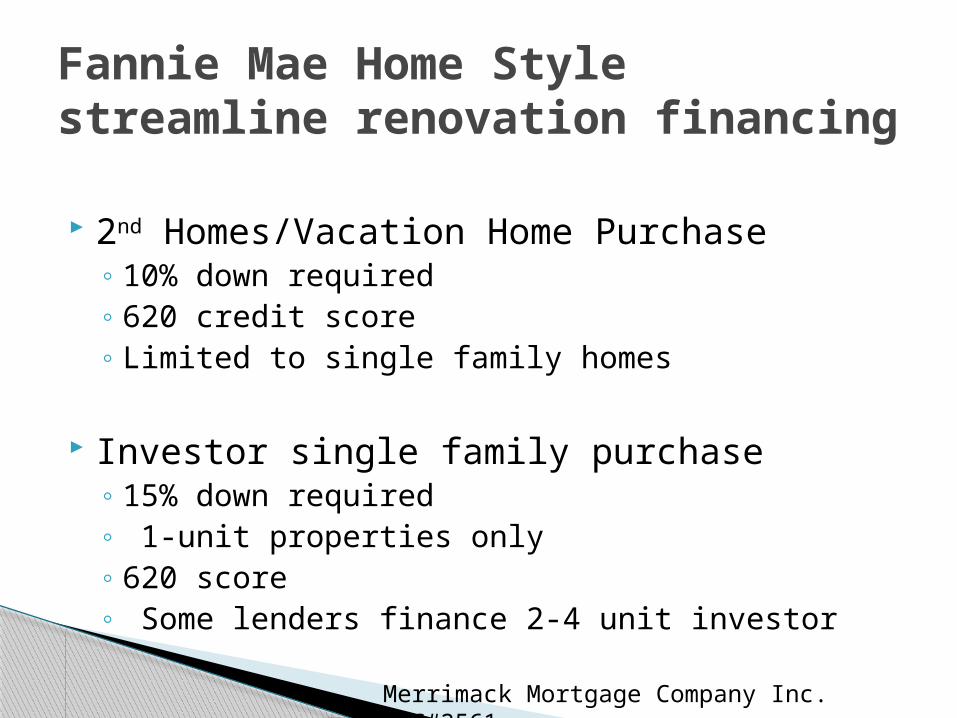

2nd Homes/Vacation Home Purchase◦ 10% down required◦ 620 credit score ◦ Limited to single family homes

Investor single family purchase◦ 15% down required◦ 1-unit properties only◦ 620 score◦ Some lenders finance 2-4 unit investor

Fannie Mae Home Stylestreamline renovation financing

Merrimack Mortgage Company Inc. NMLS#2561

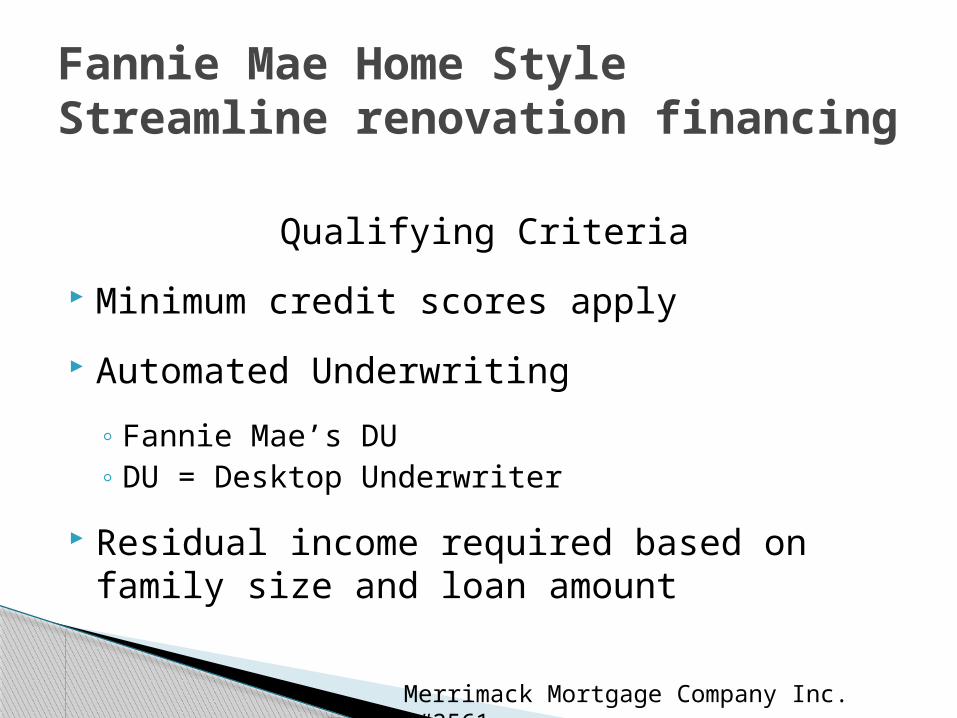

Qualifying Criteria

Minimum credit scores apply

Automated Underwriting

◦ Fannie Mae’s DU◦ DU = Desktop Underwriter

Residual income required based on family size and loan amount

Fannie Mae Home StyleStreamline renovation financing

Merrimack Mortgage Company Inc. NMLS#2561

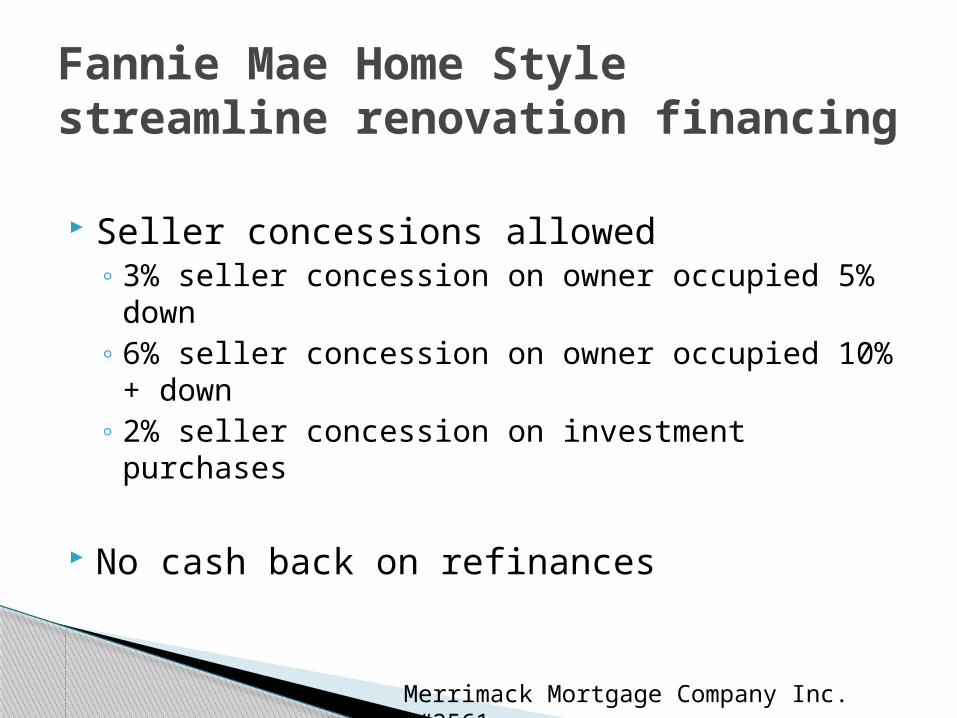

Seller concessions allowed ◦ 3% seller concession on owner occupied 5% down◦ 6% seller concession on owner occupied 10% +

down◦ 2% seller concession on investment purchases

No cash back on refinances

Fannie Mae Home Stylestreamline renovation financing

Merrimack Mortgage Company Inc. NMLS#2561

Disbursing Funds

No disbursement at closing◦ Negotiate required deposits with contractor upfront◦ Buyer must give contractor deposits

from Buyers’ own funds

2 disbursements allowed◦ Midpoint disbursement

Appraiser determines percentage of work completed Permits must be in place

◦ Final Disbursement

Fannie Mae Home Stylestreamline renovation financing

Merrimack Mortgage Company Inc. NMLS#2561

Disbursing Funds

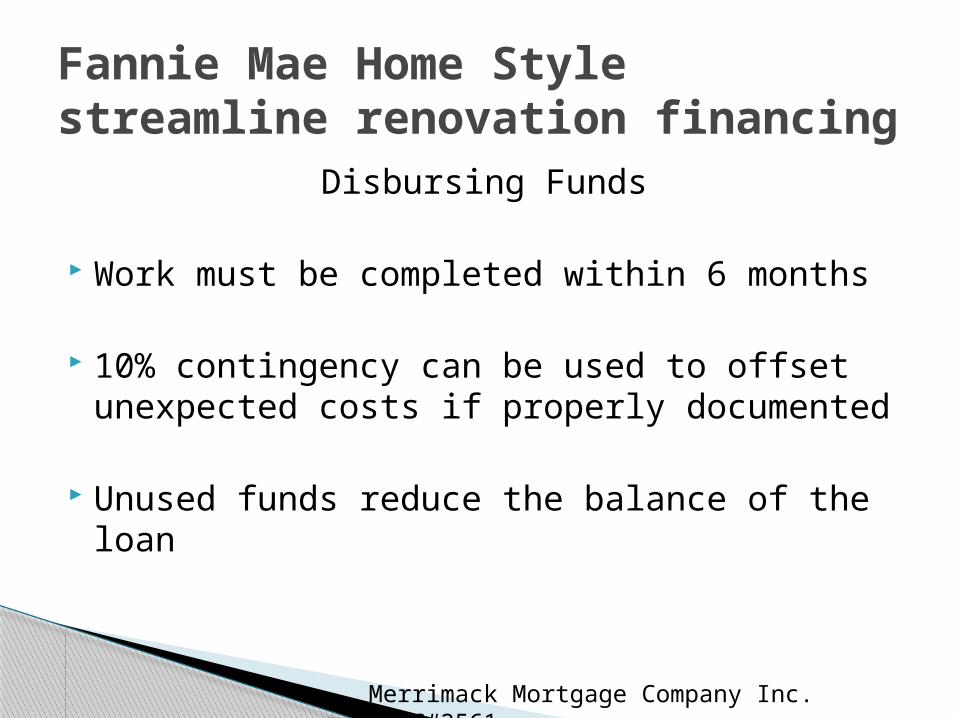

Work must be completed within 6 months

10% contingency can be used to offset unexpected costs if properly documented

Unused funds reduce the balance of the loan

Fannie Mae Home Stylestreamline renovation financing

Merrimack Mortgage Company Inc. NMLS#2561

Fannie Mae Home Stylestreamline renovation financing

Merrimack Mortgage Company Inc. NMLS#2561

Questions? Comments?

Kathi ParadisRon Thompson

603-224-6669www.communityloanfund.org

NH Community Loan Fund

What is a HUD Home?

A HUD Home is a home that had been financed by FHA and was foreclosed upon.

HUD now owns the home and is marketing it for sale

These listings are in MLS

HUD Homes

HUD Homes

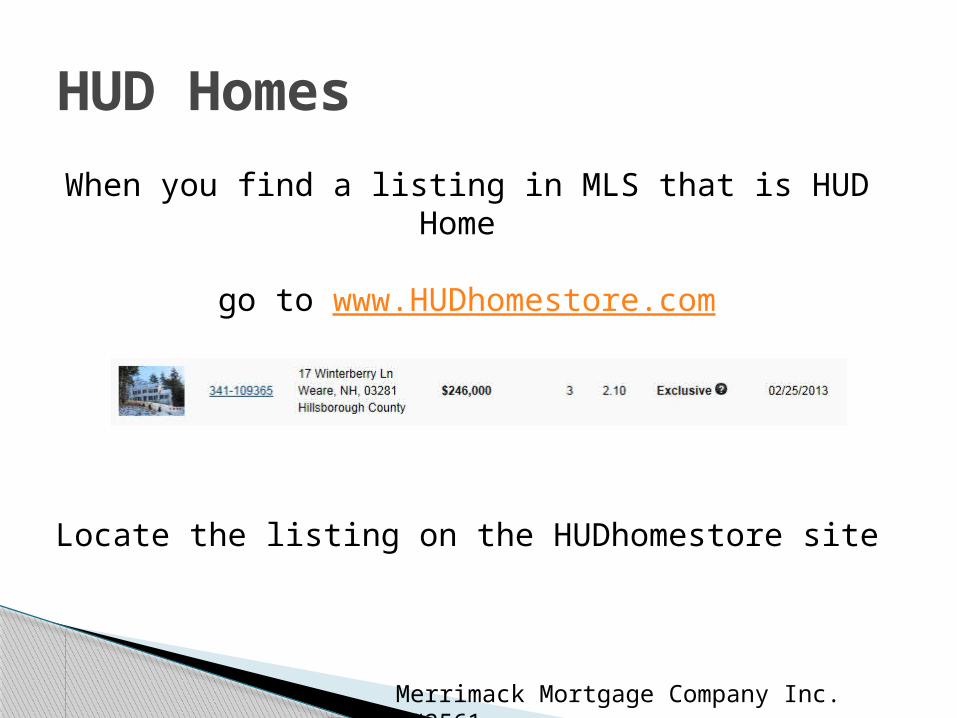

When you find a listing in MLS that is HUD Home

go to www.HUDhomestore.com

Locate the listing on the HUDhomestore site

Merrimack Mortgage Company Inc. NMLS#2561

HUD Homes

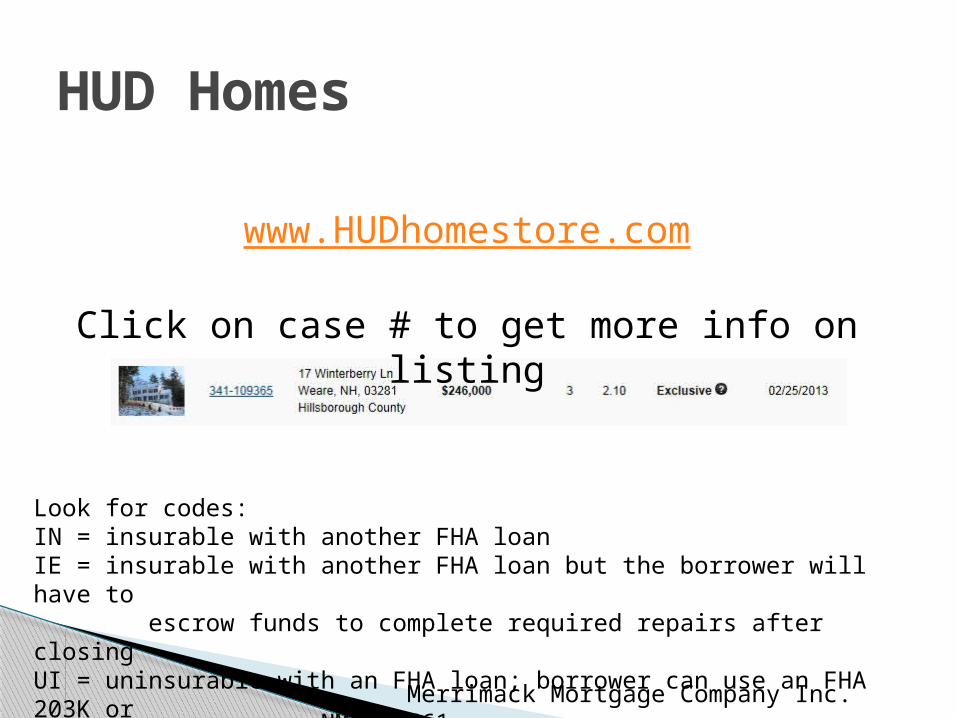

www.HUDhomestore.com

Click on case # to get more info on listing

Look for codes:IN = insurable with another FHA loanIE = insurable with another FHA loan but the borrower will have to escrow funds to complete required repairs after closingUI = uninsurable with an FHA loan; borrower can use an FHA 203K or 203Ks to obtain funds to complete needed repairs after closing.

Merrimack Mortgage Company Inc. NMLS#2561

Property Condition Report is on file atHUDhomestore.com

Click on Sales & Escrow Notes

Make sure borrower can qualify for the type of loan needed to close on HUD home

HUD Homes

Merrimack Mortgage Company Inc. NMLS#2561

www.HUDhomestore.com

Register as Bidder◦ Enter your principal broker’s NAID #◦ create a user name & password◦ provide your contact info

Submit Offers for your buyers!

HUD Homes

Merrimack Mortgage Company Inc. NMLS#2561

Appraisal is on file & can be used by lender

◦ Cannot be more than 120 days old at time of closing

◦ Appraiser must be willing to work with lender

◦ Lender can request appraisal updates/clarifications

◦ Lender can add property conditions

HUD Homes

Merrimack Mortgage Company Inc. NMLS#2561

Questions? Comments?

HUD Homes

Lender required minimum standards

All major systems must be functioning properly- Plumbing- including availability of hot water- Electrical systems- Roof & basic structure - Heating system

Any deficiencies will need to be corrected ◦ prior to closing ◦ establish escrow to repair after closing◦ use rehab loan to repair after closing

For the Listing Agent

Merrimack Mortgage Company Inc. NMLS#2561

Lender required minimum standards

no peeling exterior paint or exposed wood or obvious rot on exterior wood

Broken windows and holes in walls must be repaired

Safety issues must be addressed

Have a checklist of typical red flags

Any deficiencies will need to be corrected ◦ prior to closing ◦ establish escrow to repair after closing◦ use rehab loan to repair after closing

For the Listing Agent

Merrimack Mortgage Company Inc. NMLS#2561

Discuss completing repairs before the home inspection & appraisal

Completing repairs in advance could translate to a higher sales price or a more marketable property

If the seller has equity in the home but no cash to complete repairs then a renovation loan may allow them to upgrade deficiencies and yield a higher sales price.

For the Listing Agent

Merrimack Mortgage Company Inc. NMLS#2561

RD requires a refrigerator in the home

RD accepts dug wells that flow at 3-5 gallons per minute for a minimum of 3 hours

For the Listing Agent

Merrimack Mortgage Company Inc. NMLS#2561

If you have doubt whether the house will pass an FHA or RD inspection, talk to your lender

Consider having seller do home inspectionto identify needed repairs

Consider having a contractor look at the house to bid on required repairs

For the Listing Agent

Merrimack Mortgage Company Inc. NMLS#2561

Use checklist to identify potential problems

Be aware of typical lender required repairs

Have the buyer communicate with the lender to assure that the borrower can qualify for a rehab program

Have buyer communicate with the lender to assure they have a complete understanding of how these programs work

For the Buyers’ Agent

Merrimack Mortgage Company Inc. NMLS#2561

P&S Considerations◦ Allow extra time for Financing Contingency◦ Allow extra time for Closing◦ Negotiate for repairs to be completed by the Seller.◦ Negotiate Seller Contributions

Access to the property◦ contractors need to get into the house◦ will Seller allow unescorted access by contractors◦ Are you able to meet all contractors at the property

For The Buyers’ Agent

Merrimack Mortgage Company Inc. NMLS#2561

Have your clients work with their lender to determine the best products and time frame their individual situation.

When you need a REHAB loan

Pick up the Phone and Call(603) 225-LOAN (5626)

For the Buyers’ Agent

Merrimack Mortgage Company Inc NMLS 2561

109

Licensed by the New Hampshire Banking Department MA Lender License #MC 2561 The information in this presentation is Accurate as of

the date of publishing. Information, terms and conditions are subject to change without notice.

Always Check with Financial Advisors for Tax information.

This is not an extension of credit or a commitment to lend. Subject to Underwriting approval

Merrimack Mortgage Company Inc. NMLS#2561

9/18/2013

Merrimack Mortgage Company

Gonewhampshirehousing.com

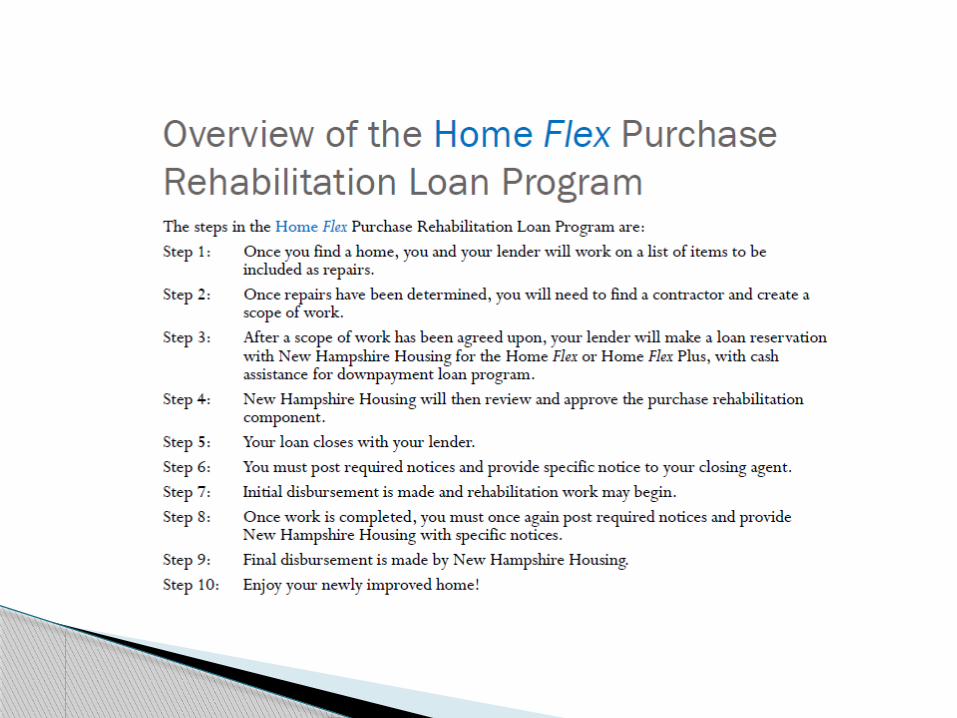

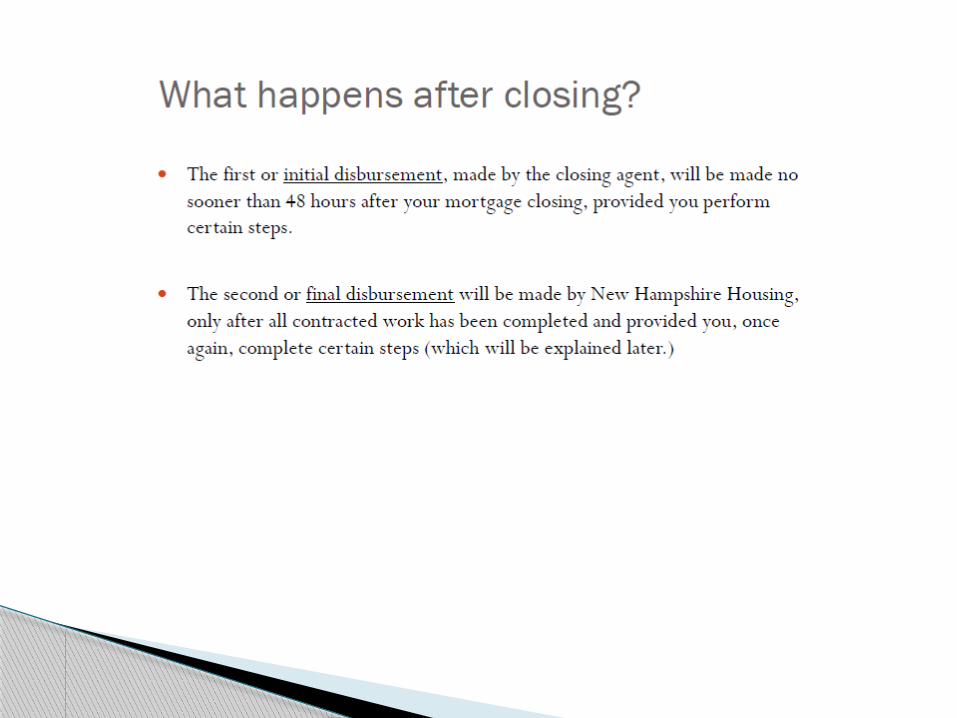

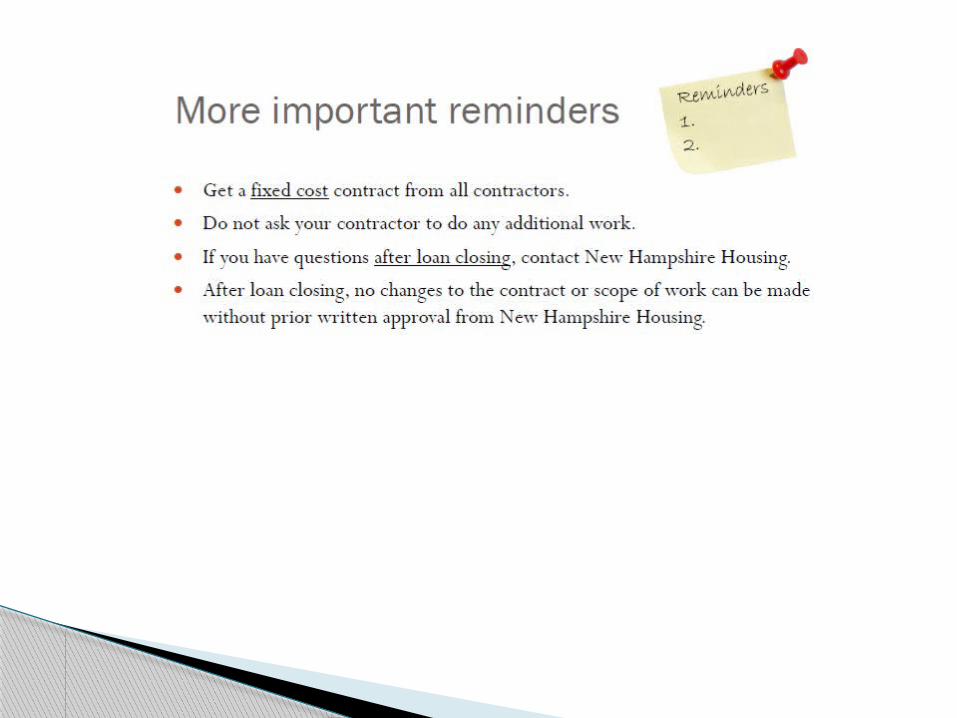

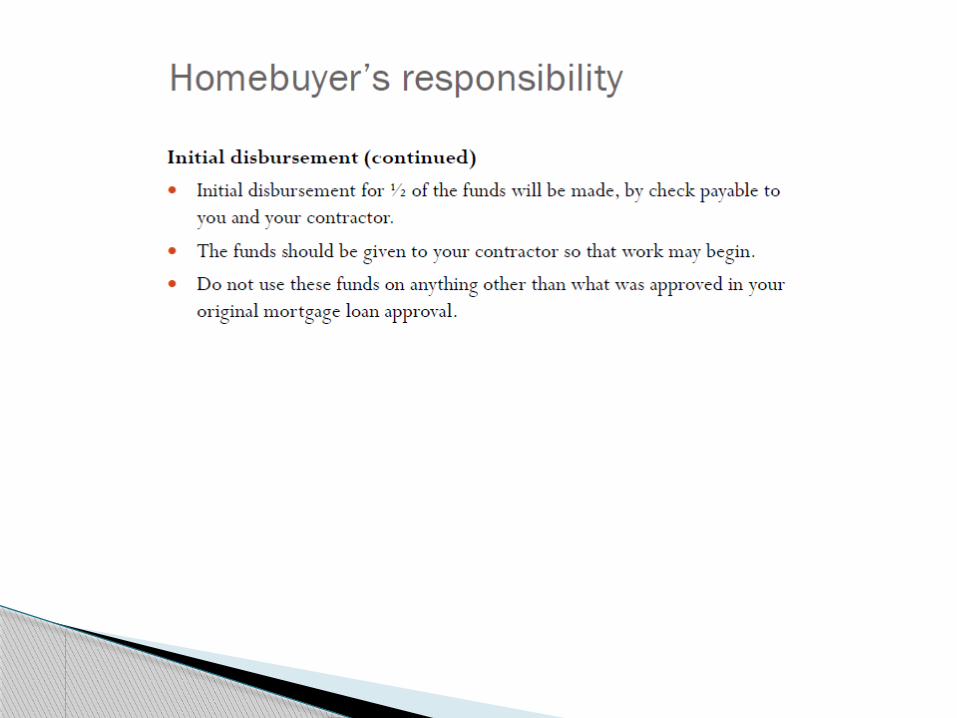

The following slides are taken directly from a course required by NH Housing when buyers use NH Housing rehab programs …