presented by:- amit luthra managing partner luthra & luthra , chartered accountants

DESCRIPTION

Foreign Entities – Setting up of office in India. Presented by:- Amit Luthra Managing Partner Luthra & Luthra , Chartered Accountants. 23 rd July 2011. India: The rest of the story. - PowerPoint PPT PresentationTRANSCRIPT

Presented by:- Presented by:- Amit LuthraAmit Luthra

Managing PartnerManaging PartnerLuthra & Luthra, Chartered Luthra & Luthra, Chartered

AccountantsAccountants

Foreign Entities – Setting up of office in India

23rd July 2011

India: The rest of the storyIndia: The rest of the story UNCTAD survey projected India as the second most important FDI UNCTAD survey projected India as the second most important FDI

destination (after China) during 2010-2012. destination (after China) during 2010-2012. Sectors attracting higher inflows servicesSectors attracting higher inflows services telecommunication, telecommunication, construction activities and construction activities and computer software and hardware. computer software and hardware.

Leading sources of FDILeading sources of FDI Mauritius,Mauritius, Singapore, Singapore, US and US and UK. UK. This presentation is about understanding the way Foreign This presentation is about understanding the way Foreign

Companies can set up their offices in India so as to mine the Companies can set up their offices in India so as to mine the existent business potential.existent business potential.

Luthra & Luthra, Chartered Accountants

FDI in India

Luthra & Luthra, Chartered Accountants

Regulatory Provisions:

FEMA,1999/RBI Regulations Section 6(6) of Foreign Exchange Management

Act,1999 read with Notification No.22/2000 dated May3, 2000 as amended from time to time

Master Circular No. 03/2011-12 dated 01 July,2011

Companies Act,1956 Section 591-602 of the Companies Act,1956

related to Companies Incorporated outside India

Luthra & Luthra, Chartered Accountants

Regulatory Aspects-Detailed Regulatory Aspects-Detailed AnalysisAnalysis

1. As Foreign Company/entity 1. As Foreign Company/entity a. Liaison Office (L.O.)a. Liaison Office (L.O.) Body incorporated outside India are allowed to set up a L.O.Body incorporated outside India are allowed to set up a L.O. Mere communication channel between Head office and Mere communication channel between Head office and

parties in Indiaparties in India Commercial/ income generating activities are strictly not Commercial/ income generating activities are strictly not

permittedpermitted Expenses to be met by foreign parent company.Expenses to be met by foreign parent company. Required to be registered with the Registrar of Companies Required to be registered with the Registrar of Companies

(ROC).(ROC). An extension of parent company in India, is also known as An extension of parent company in India, is also known as

Representative Office. Representative Office. Required to get its annual accounts audited and submit Required to get its annual accounts audited and submit

annual activity report to the RBI .annual activity report to the RBI .Luthra & Luthra, Chartered

Accountants

Scope of Activities:-Scope of Activities:-

PermissiblePromoting export from and import to India

Representing the parent company/ group

companies in India

Promoting technical/ financial

collaborations between foreign parent and

Indian companies

Acting as a communication channel

between the parent company and Indian

companies

Prohibited

Cannotundertake any activity of trading,

commercial or industrial nature

enter into business contracts in its own

name

render any consultancy or any other

service with or without any consideration

charge any commission/ fee or earn any

income for services rendered

have any signing or commitment powers

borrow, lend money or acquire, transfer or

dispose off any movable property without

prior permission of the RBI

acquire immovable property in India

Luthra & Luthra, Chartered Accountants

b. Branch Officeb. Branch Office Body incorporated outside India and engaged in manufacturing or trading Body incorporated outside India and engaged in manufacturing or trading

activities are allowed to set up with specific approval of RBI. activities are allowed to set up with specific approval of RBI.

It is an extension/permanent establishment of the parent company in India.It is an extension/permanent establishment of the parent company in India.

Required to be registered with the (ROC).Required to be registered with the (ROC).

Foreign companies have general permission to establish branch/unit in SEZ Foreign companies have general permission to establish branch/unit in SEZ

(Special Economic Zones) to undertake manufacturing or service activities, (Special Economic Zones) to undertake manufacturing or service activities,

subject to certain rules.subject to certain rules.

Foreign Banks do not require FEMA approval, they have obtained necessary Foreign Banks do not require FEMA approval, they have obtained necessary

RBI approval under the Banking Regulation Act, 1949.RBI approval under the Banking Regulation Act, 1949.

Profits earned by branches can be freely remitted, subject to payment of Profits earned by branches can be freely remitted, subject to payment of

applicable taxes.applicable taxes.

Funding is possible from parent company and from Indian operations.Funding is possible from parent company and from Indian operations.

Required to submit annual activity report to the RBI.Required to submit annual activity report to the RBI.

Branch Office on Stand Alone Basis in SEZ:-Branch Office on Stand Alone Basis in SEZ:- Such Branch Offices are restricted to Special Economic Zone (SEZ) alone Such Branch Offices are restricted to Special Economic Zone (SEZ) alone

and no business activity/ transaction is allowed outside the SEZs in India, and no business activity/ transaction is allowed outside the SEZs in India, which include branches/subsidiaries of its parent office in Indiawhich include branches/subsidiaries of its parent office in India

Luthra & Luthra, Chartered Accountants

Scope of Activities:-Scope of Activities:-

Permitted Representing the parent company in India

and acting as buying/ selling agents in

India

Export/ import of goods

Rendering professional or consultancy

services

Carrying out research work in areas in

which the parent company is engaged

Promoting technical or financial

collaborations between Indian companies

and parent or overseas group company

Rendering services in Information

Technology and development of software

in India

Rendering technical support to the

products supplied by the parent/ group

companies, foreign airline/shipping

company

Prohibited

Not allowed to carry out any manufacturing or retail

trading activity of any nature

undertake domestic trading (i.e. domestic

procurement and sale of goods)

Entities from Pakistan, Bangladesh, Sri Lanka,

Afghanistan, Iran and China are not allowed

to acquire immoveable property in India

even for a Branch Office. These entities

are allowed to take such property on lease

for a period not exceeding 5 years

Luthra & Luthra, Chartered Accountants

c. Project Office (PO):-c. Project Office (PO):-

A foreign entity may open PO to execute a contract awarded by the A foreign entity may open PO to execute a contract awarded by the

Indian Government or any Indian Company.Indian Government or any Indian Company. RBI has granted general permission RBI has granted general permission to foreign Companies for setting to foreign Companies for setting

up POup PO Project office is treated as an extension/permanent establishment of Project office is treated as an extension/permanent establishment of

parent company.parent company. Required to be registered with the Registrar of Companies.Required to be registered with the Registrar of Companies. Profits earned can be freely remitted from India (Subject to payment Profits earned can be freely remitted from India (Subject to payment

of taxes).of taxes). Funding is possible from project operations and receipts from parent Funding is possible from project operations and receipts from parent

company. Can also be company. Can also be funded by Multilateral financial funded by Multilateral financial

agency/Cleared by an appropriate authority like DRDO,IRDA etc agency/Cleared by an appropriate authority like DRDO,IRDA etc Required to submit annual activity report to the Reserve Bank of Required to submit annual activity report to the Reserve Bank of

India by 30India by 30thth April of every year April of every year

Luthra & Luthra, Chartered Accountants

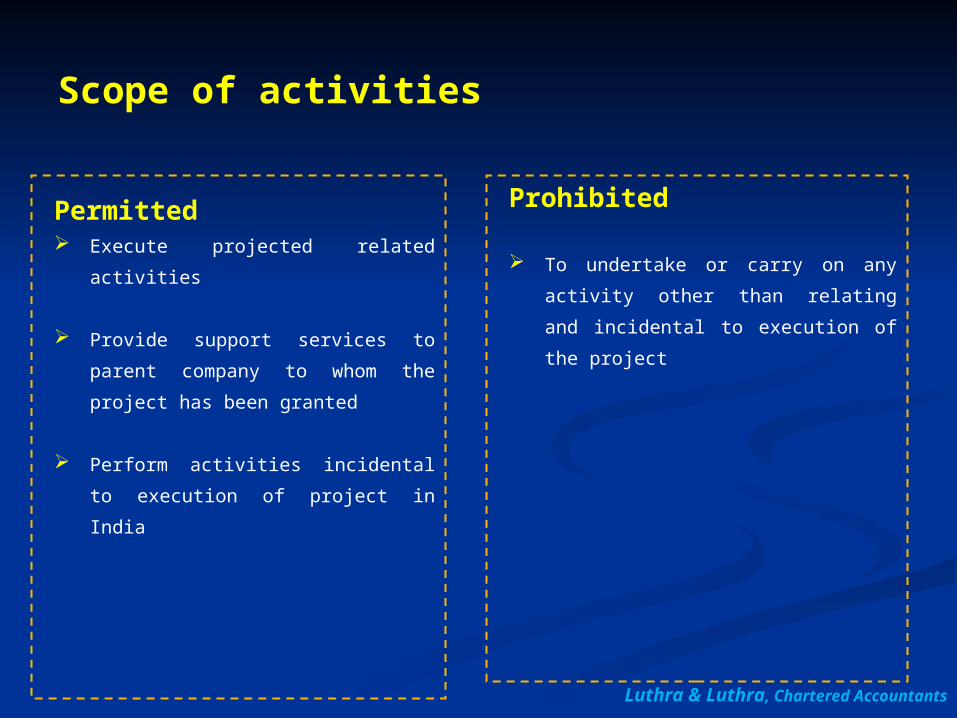

Scope of activities

Permitted Execute projected related activities

Provide support services to parent

company to whom the project has

been granted

Perform activities incidental to

execution of project in India

Prohibited

To undertake or carry on any activity

other than relating and incidental to

execution of the project

Luthra & Luthra, Chartered Accountants

2. Indian Incorporated Entities2. Indian Incorporated Entities i) Joint Venture , ii) Wholly owned subsidiaries iii) Acquiring i) Joint Venture , ii) Wholly owned subsidiaries iii) Acquiring an existingan existing company and iv) LLP company and iv) LLP

Joint VentureJoint Venture Foreign entities can set up JV with Indian party where FDI is permitted Foreign entities can set up JV with Indian party where FDI is permitted

under FDI Policy under FDI Policy Unlike LO/BO/PO,JV has more flexibility with regard to the nature of Unlike LO/BO/PO,JV has more flexibility with regard to the nature of

operations and both can leverage their area of expertise.operations and both can leverage their area of expertise.

Wholly owned subsidiariesWholly owned subsidiaries Foreign companies can set up WOS in sectors where FDI is permittedForeign companies can set up WOS in sectors where FDI is permitted Unlike LO/BO/PO/JV, WOS has significantly higher flexibility with regard to Unlike LO/BO/PO/JV, WOS has significantly higher flexibility with regard to

nature of operations. (Subject to Sectoral limits, if any, under FDI Policy)nature of operations. (Subject to Sectoral limits, if any, under FDI Policy)

Acquiring an existing CompanyAcquiring an existing Company Acquiring an existing Indian company (wholly or partly)- a popular way of Acquiring an existing Indian company (wholly or partly)- a popular way of

entering into India. entering into India. Legal, financial and technical due diligence suggested to avoid any Legal, financial and technical due diligence suggested to avoid any

unforeseen liability to either party is of critical importance. unforeseen liability to either party is of critical importance.

Luthra & Luthra, Chartered Accountants

Limited Liability PartnershipLimited Liability Partnership

A recently introduced legal entity.A recently introduced legal entity. Partners have limited liability. Partners have limited liability. It is expected that LLPs may soon become a popular It is expected that LLPs may soon become a popular

vehicle for FDI. vehicle for FDI. Other ordinary partnerships have unlimited liability - Other ordinary partnerships have unlimited liability -

therefore not considered as a vehicle for foreign therefore not considered as a vehicle for foreign investment. investment.

Investment in LLPs,- prior approval of the Investment in LLPs,- prior approval of the RBI/GovernmentRBI/Government

Luthra & Luthra, Chartered Accountants

Foreign Charitable organization’s –Office Foreign Charitable organization’s –Office in Indiain India

A foreign non-profit organization setting up an office in India A foreign non-profit organization setting up an office in India needs:- needs:-

i) to be registered as a trust/society/company (Section 25), i) to be registered as a trust/society/company (Section 25),

ii) permission from the Reserve Bank of India and also ii) permission from the Reserve Bank of India and also

iii) a No Objection Certificate from the Ministry of External Affairs. iii) a No Objection Certificate from the Ministry of External Affairs.

Example:-Example:-A place of work in a restricted area (like a tribal or a border area A place of work in a restricted area (like a tribal or a border area requires a special permit– usually issues either by the Ministry of requires a special permit– usually issues either by the Ministry of Home Affairs or by the relevant local authority (i.e., district Home Affairs or by the relevant local authority (i.e., district magistrate). magistrate).

Luthra & Luthra, Chartered Accountants

Operational AspectsImportant compliances- FEMA

Opening of LO/BO

File application in form FNC 1 for RBI Permission

Application will be considered under two routes Automatic route where 100% FDI is allowed In consultation with MOF where 100% is not allowed

Additional Criteria considered by RBI:

Track record:

For Branch Office — a profit making track record during the immediately preceding five financial years in the home country.

For Liaison Office — a profit making foreign Company track record during the immediately preceding three financial years in the home country.

Luthra & Luthra, Chartered Accountants

Net worthFor Branch Office — not less than USD 100,000For Liaison Office — not less than USD 50,000(Net Worth = Paid up Capital+ Free Reserve – Intangible Assets )

Documents to be filed:English version of the Certificate of Incorporation and Memorandum & Articles of Association attested by Indian Embassy / Notary Public in the Country of Registration. Latest Audited Balance Sheet of the applicant entity.

LO of Insurance/ Banking Companies Insurance Companies- Approval of IRDA Banking Companies- Approval of Department of Banking

Operations and Development (DBOD), Reserve Bank of India.

Operational AspectsImportant compliances- FEMA

Luthra & Luthra, Chartered Accountants

Branch Office in Special Economic Zones (SEZs)

General permission to foreign companies for establishing branch SEZ to undertake manufacturing and service activities, subject to:-

their functioning in 100 % FDI sectors;

Complying with Companies Act,1956 (Section 592 to 602);

Function on a stand-alone basis. RBI Notification No.FEMA/102/2003-RB dated 03-10-2003 and circular No.58 dated 16-01-2004 as amended from time to time.

Branches of Foreign Banks

Foreign banks do not require separate approval under FEMA, for opening branch office in India. However, approval from RBI is required under Banking Regulation Act, 1949.

Luthra & Luthra, Chartered Accountants

Operational AspectsImportant compliances- FEMA

Project office

RBI has granted general permission to establish Project Offices, provided foreign Companies have secured a contract from an Indian company to execute a project in India, and

the project is funded directly by inward remittance from abroad; or

is funded by a International Financing Agency; or the project has been cleared by an appropriate authority; or Entity in India awarding the contract has been granted Term

Loan by a Public Financial Institution or a bank.

However, if the all the above criteria are not met, the foreign entity has to approach the RBI, Central Office, for approval.

Luthra & Luthra, Chartered Accountants

Operational AspectsImportant compliances- FEMA

Validity

LO/BO- Initial approval for 3 years and further extended by Authorised Dealer Bank and RBI respectively

PO- Till the period of project

Validity extension exceptions

No extension to the LO’s of following entities: NBFC Construction and development sectors (excluding

infrastructure development companies)

Upon expiry of the validity period, these entities have to either close down or be converted into a JV /WOS by forming a Company, in conformity with the extant FDI policy

Luthra & Luthra, Chartered Accountants

Operational AspectsImportant compliances- FEMA

Operational AspectsImportant compliances- FEMA

Remittance of profit-BO

Can repatriate profit (net of taxes), on production of the following documents to AD : Audited B/S and P&L account for the relevant year Chartered Accountant’s certificate certifying

manner of arriving at the remittable profit entire remittable profit has been earned from

permitted activities

(Profit should not include any profit on revaluation of the assets of the branch)

Luthra & Luthra, Chartered Accountants

CLOSURE OF LO/BO

Authorised Dealer Bank Category - I bank with the following documents:

Copy of the RBI permission/ approval from the sectoral regulator's such as IRDA,SEBI etc

Auditor’s certificate- i) indicating the manner of remittable amount has been arrived at/statement

of assets and liabilities, indicating the manner of disposal of assets; ii) confirming that all liabilities (gratuity and other benefits to employees,

etc.), have been met/ provided for; and iii)confirming that no income accruing from sources outside India (including

proceeds of exports) has remained un-repatriated to India. No-objection / Tax Clearance Certificate. Confirmation from the applicant/parent company that no legal proceedings

in any Court in India are pending and there is no legal impediment to the remittance.

Report from the ROC regarding compliance with the provisions of the Companies Act.

Any other document/s, specified by the Reserve Bank while granting approval.

Luthra & Luthra, Chartered Accountants

Operational AspectsImportant compliances- FEMA

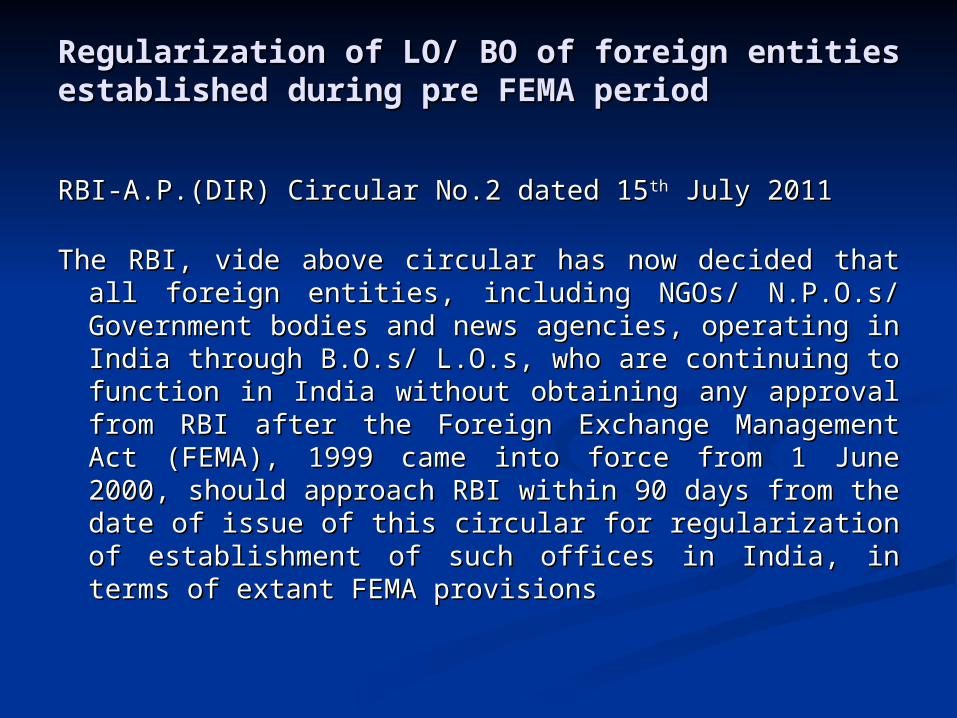

Regularization of LO/ BO of foreign entities Regularization of LO/ BO of foreign entities established during pre FEMA periodestablished during pre FEMA period

RBI-A.P.(DIR) Circular No.2 dated 15RBI-A.P.(DIR) Circular No.2 dated 15thth July 2011 July 2011

The RBI, vide above circular has now decided that all The RBI, vide above circular has now decided that all foreign entities, including NGOs/ N.P.O.s/ foreign entities, including NGOs/ N.P.O.s/ Government bodies and news agencies, operating in Government bodies and news agencies, operating in India through B.O.s/ L.O.s, who are continuing to India through B.O.s/ L.O.s, who are continuing to function in India without obtaining any approval from function in India without obtaining any approval from RBI after the Foreign Exchange Management Act RBI after the Foreign Exchange Management Act (FEMA), 1999 came into force from 1 June 2000, (FEMA), 1999 came into force from 1 June 2000, should approach RBI within 90 days from the date of should approach RBI within 90 days from the date of issue of this circular for regularization of issue of this circular for regularization of establishment of such offices in India, in terms of establishment of such offices in India, in terms of extant FEMA provisionsextant FEMA provisions

Operational AspectsImportant Compliance- The Companies Act,1956Section 592- Section 592- Foreign Companies within 30 days of the establishment shall file e-form 44

for registration with-

A certified copy of the charter/MOA of the Company. Address of principal office List of directors/secretary Name of the Indian authorize representative Full address of the office in India

Section 593-Foreign company shall file e-Form-49 : In case an alteration is made in MOA of a foreign company/Registered

office/directors or secretary of a foreign company, on or before the 31st January, of the year following the year in which the alteration was made.

In case of alteration is made in name or address of the authorised person/principle place of business, within one month from the date on which the alteration was made.

Luthra & Luthra, Chartered Accountants

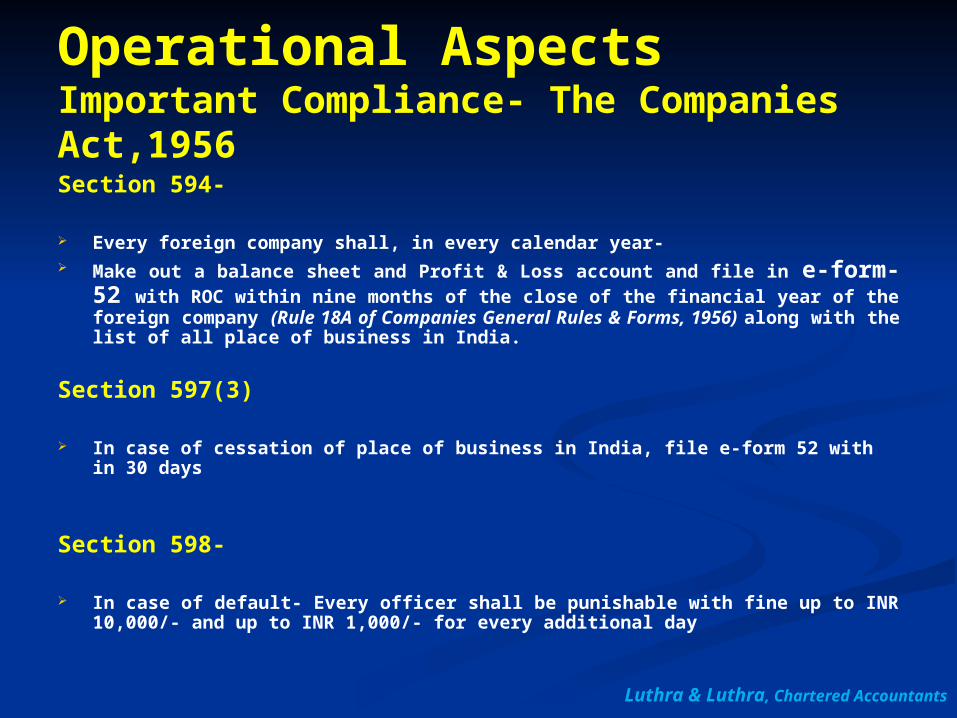

Section 594-

Every foreign company shall, in every calendar year- Make out a balance sheet and Profit & Loss account and file in e-form-52

with ROC within nine months of the close of the financial year of the foreign company (Rule 18A of Companies General Rules & Forms, 1956) along with the list of all place of business in India.

Section 597(3)

In case of cessation of place of business in India, file e-form 52 with in 30 days

Section 598-

In case of default- Every officer shall be punishable with fine up to INR 10,000/- and up to INR 1,000/- for every additional day

Operational AspectsImportant Compliance- The Companies Act,1956

Luthra & Luthra, Chartered Accountants

Tax Implications & Transfer Tax Implications & Transfer Pricing RulesPricing Rules

A. Direct TaxesA. Direct Taxes

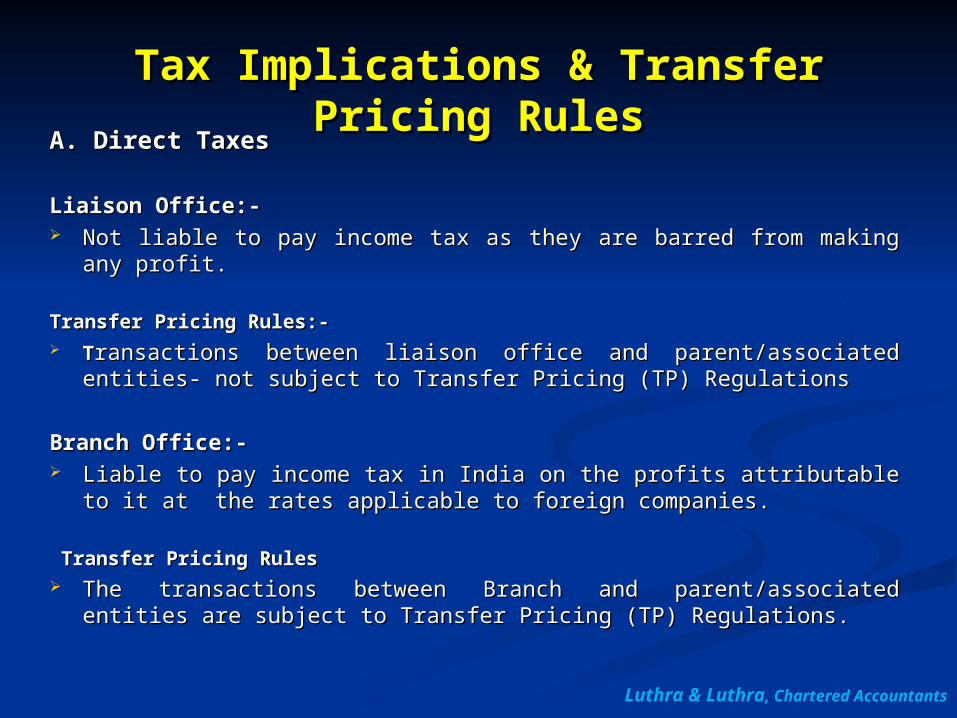

Liaison Office:-Liaison Office:- Not liable to pay income tax as they are barred from making any Not liable to pay income tax as they are barred from making any

profit.profit.

Transfer Pricing Rules:- Transfer Pricing Rules:- TTransactions between liaison office and parent/associated entities- ransactions between liaison office and parent/associated entities-

not subject to Transfer Pricing (TP) Regulationsnot subject to Transfer Pricing (TP) Regulations

Branch Office:- Branch Office:- Liable to pay income tax in India on the profits attributable to it at Liable to pay income tax in India on the profits attributable to it at

the rates applicable to foreign companies. the rates applicable to foreign companies.

Transfer Pricing RulesTransfer Pricing Rules The transactions between Branch and parent/associated entities are The transactions between Branch and parent/associated entities are

subject to Transfer Pricing (TP) Regulations.subject to Transfer Pricing (TP) Regulations.Luthra & Luthra, Chartered

Accountants

Tax Implications & Transfer Tax Implications & Transfer Pricing RulesPricing Rules

Project Office:-Project Office:- Liable to pay income tax in India on its profits at the rates Liable to pay income tax in India on its profits at the rates

applicable to foreign companies. applicable to foreign companies.

Transfer Pricing RulesTransfer Pricing Rules Transactions between project office and associated entities are Transactions between project office and associated entities are

subject to Transfer Pricing (TP) Regulations.subject to Transfer Pricing (TP) Regulations.

JV/WOS:-JV/WOS:- Liable to pay income tax in India on its profits at the specified rates Liable to pay income tax in India on its profits at the specified rates

Transfer Pricing RulesTransfer Pricing Rules The transactions between Indian Subsidiary/JV and The transactions between Indian Subsidiary/JV and

parent/associated entities are subject to Transfer Pricing (TP) parent/associated entities are subject to Transfer Pricing (TP) Regulations.Regulations.

B. Indirect Taxes:-B. Indirect Taxes:- All the above entities except L.O are subject All the above entities except L.O are subject to applicable indirect taxes. to applicable indirect taxes. Luthra & Luthra, Chartered

Accountants

What kind of office to Open:- What kind of office to Open:- SuggestionSuggestionLiaison officeLiaison office

Suggested for a foreign company that does not have existing business in India but wishes to Suggested for a foreign company that does not have existing business in India but wishes to understand and explore the Indian market.understand and explore the Indian market.

For collection of market information, interaction with Indian customers and providing For collection of market information, interaction with Indian customers and providing information about parent company and its products to prospective Indian customers.information about parent company and its products to prospective Indian customers.

To promote technical and financial collaborations between parent/group companies and To promote technical and financial collaborations between parent/group companies and Indian companies where services are to be provided from off-shore. Indian companies where services are to be provided from off-shore.

Branch officeBranch office

Where the foreign entity has understood the Indian market and wishes to provide services Where the foreign entity has understood the Indian market and wishes to provide services from India on a regular basis.from India on a regular basis.

It can undertake most of the activities, as mentioned above and enjoys greater operational It can undertake most of the activities, as mentioned above and enjoys greater operational freedom in comparison to Liaison and Project offices.freedom in comparison to Liaison and Project offices.

Project officeProject office When a foreign entity has been awarded a contract in India.When a foreign entity has been awarded a contract in India.

Entity incorporated in India e.g. JV, LLP, wholly or partly owned companyEntity incorporated in India e.g. JV, LLP, wholly or partly owned company Wide range of business activities envisaged; Wide range of business activities envisaged; Having long term perspective of mining Business potential in IndiaHaving long term perspective of mining Business potential in India

Luthra & Luthra, Chartered Accountants

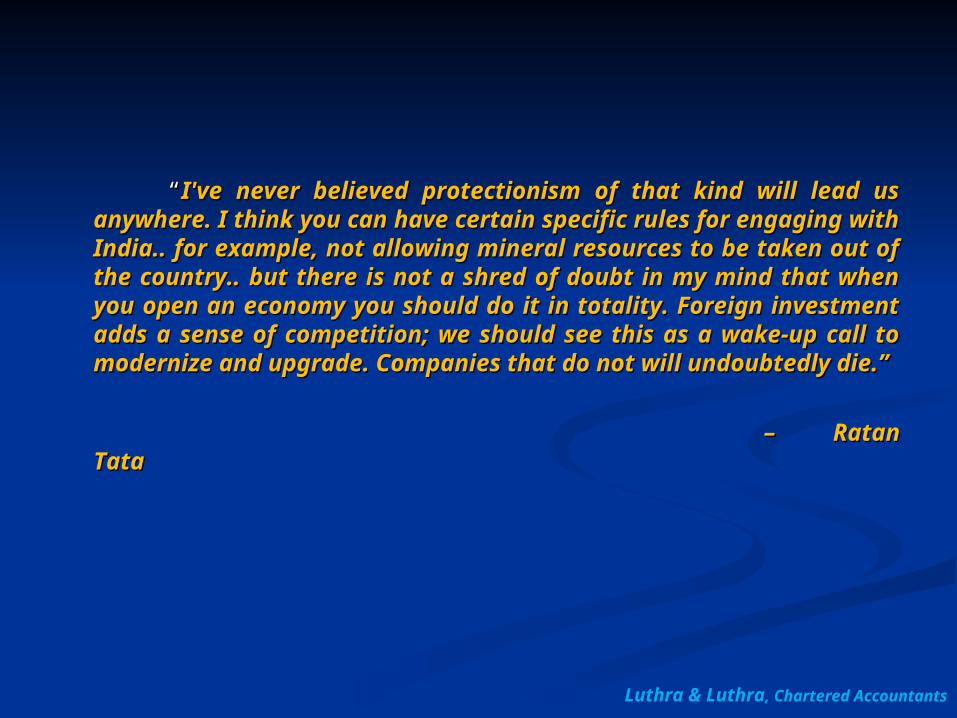

“ “I've never believed protectionism of that kind will lead us I've never believed protectionism of that kind will lead us anywhere. I think you can have certain specific rules for anywhere. I think you can have certain specific rules for engaging with India.. for example, not allowing mineral engaging with India.. for example, not allowing mineral resources to be taken out of the country.. but there is not resources to be taken out of the country.. but there is not a shred of doubt in my mind that when you open an a shred of doubt in my mind that when you open an economy you should do it in totality. Foreign investment economy you should do it in totality. Foreign investment adds a sense of competition; we should see this as a wake-adds a sense of competition; we should see this as a wake-up call to modernize and upgrade. Companies that do not up call to modernize and upgrade. Companies that do not will undoubtedly die.” will undoubtedly die.”

– – Ratan Ratan TataTata

Luthra & Luthra, Chartered Accountants

COMPARATIVE ANALYSISCOMPARATIVE ANALYSISOperational requirementsOperational requirements

Key Parameters

Liaison Office

Project Office

Branch Office

Joint Venture Wholly Owned

Subsidiary

LLP

Procedure for set up

• Approval of RBI

• Registration with ROC

• Intimation to RBI

• Registration with ROC

• Approval of RBI

• Registration with ROC

•Registration with ROC

•No Government approval where 100 % FDI permitted under automatic route

• Registration with ROC

• No Government approval up to sectoral limit permitted under automatic route of FDI policy

• Registration with Registrar of LLP

• Government approval only for LLP’s operating under Service /activities where 100% FDI is allowed

Set up time

3 to 4 weeks

3 to 4 weeks 3 to 4 weeks

5 to 6 weeks, generally due finalization of JV agreement

2 to 3 weeks

2 to 3 weeks

Luthra & Luthra, Chartered Accountants

COMPARATIVE ANALYSISOperational requirements

Key Paramet

ers

Liaison Office

Project Office

Branch Office

Joint Venture Wholly Owned Subsidiary

LLP

Flexibility of operations

Very restrictive

Commercial income generating activities are not permitted

Set up only for execution of a particular project

As compared to LO, wider scope of activities can be undertaken

Cannot undertake manufacturing and retail trading however , it can render professional/ consultancy services

Post set up, expanding scope of operations may involve regulatory approvals

Expanding scope of operations is subject to internal approvals and procedural filings and does not require approval from regulatory authorities such as RBI/FIPB etc

Foreign companies can set up JV with Indian Party in permitted sectors (subject to sectoral limits, if any, under the FDI policy)

Significantly higher flexibility in nature of operations

Expanding scope of operations is subject to internal approvals and procedural filings and does not require approval from regulatory authorities such as RBI/FIPB etc

Foreign companies can set up WOS in permitted sectors (subject to sectoral limits, if any, under the FDI policy)

High flexibility in nature of operations due to less reporting to Registrar of LLP, audit etc

Luthra & Luthra, Chartered Accountants

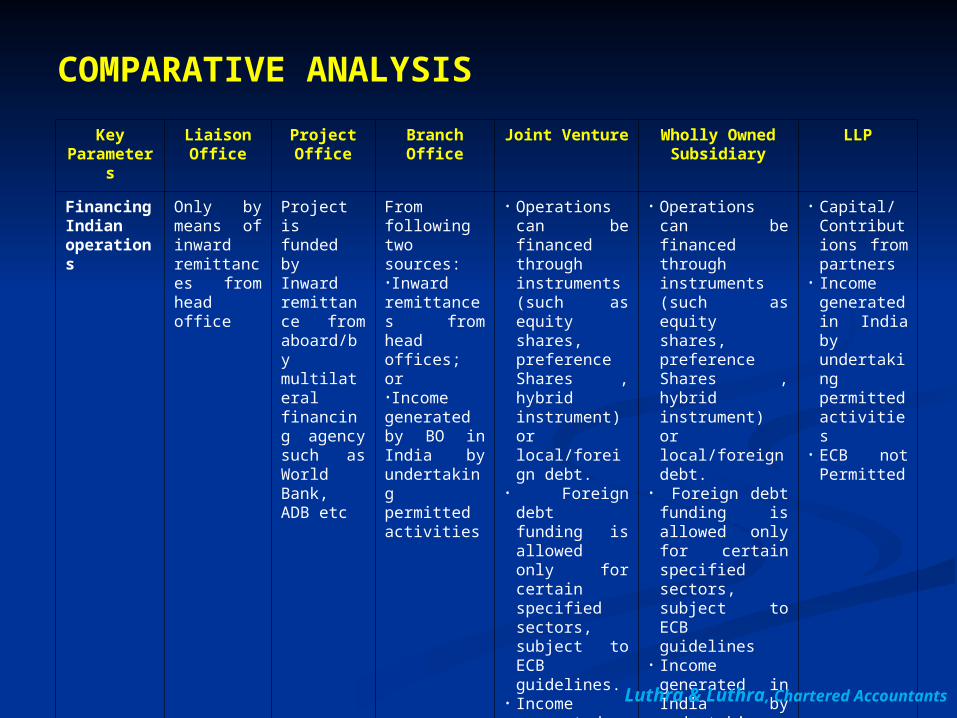

COMPARATIVE ANALYSIS

Key Paramete

rs

Liaison Office

Project Office

Branch Office

Joint Venture Wholly Owned Subsidiary

LLP

Financing Indian operations

Only by means of inward remittances from head office

Project is funded by Inward remittance from aboard/by multilateral financing agency such as World Bank, ADB etc

From following two sources:•Inward remittances from head offices; or•Income generated by BO in India by undertaking permitted activities

• Operations can be financed through instruments (such as equity shares, preference Shares , hybrid instrument) or local/foreign debt.

• Foreign debt funding is allowed only for certain specified sectors, subject to ECB guidelines.

• Income generated in India by undertaking permitted activities

• Operations can be financed through instruments (such as equity shares, preference Shares , hybrid instrument) or local/foreign debt.

• Foreign debt funding is allowed only for certain specified sectors, subject to ECB guidelines

• Income generated in India by undertaking permitted activities

• Capital/Contributions from partners

• Income generated in India by undertaking permitted activities

• ECB not Permitted

Luthra & Luthra, Chartered Accountants

COMPARATIVE ANALYSIS

Key Paramet

ers

Liaison Office

Project Office

Branch Office

Joint Venture

Wholly Owned

Subsidiary

LLP

Validity

Transfer of Asset

Permission for 3 years, this may be extended from time to time by an AD Category I bank.

Can transfer movable asset with specific approval of RBI

For the time period of specified project.

With specific approval of RBI

Permission for 3 years, this may be extended from by RBI not by AD

With specific approval of RBI

Perpetual Succession

No such restriction

Perpetual Succession

No such restriction

Perpetual Succession

With specific approval of RBI

Luthra & Luthra, Chartered Accountants

COMPARATIVE ANALYSIS

Key Paramet

ers

Liaison Office Project Office

Branch Office

Joint Venture

Wholly Owned Subsidiary

LLP

Reporting

• File Annual Activity Certificate from a CA, as at 31st March with-in 30 days to the AD Bank.

• Need to file Balance Sheet as at 31st March and global accounts (as at last financial year) with ROC

• Intimate ROC, If there are any changes in charter, directorship or Authorised signatory

• Need to file Balance Sheet as at 31st March and global accounts (as at last financial year) with ROC

• Intimate ROC, If there are any changes in charter, directorship or Authorised signatory

• File Annual Activity Certificate from CA , as at 31st March with in 30 days to the AD Bank.

• Need to file Balance Sheet as 31st March and global accounts (as at last financial year) with ROC

• Intimate ROC, If there are any changes in charter, directorship or Authorised signatory

• Intimate RBI on receipt of funds with in 30 days.

• File Form FC-GPR Part A with in 30 days of allotment of equity/CCP/CCD

• Statement of Asset and liabilities as at 31st March by 15th July of each year

• Every other reporting as applicable to an Indian Company as per applicable Acts.

• Intimate RBI on receipt of funds with in 30 days.

• File Form FC-GPR Part A with in 30 days of allotment of equity/CCP/CCD

• Statement of Asset and liabilities as at 31st March by 15th July of each year

• Every other reporting as applicable to an Indian Company as per applicable Acts.

As per government directions

Luthra & Luthra, Chartered Accountants

COMPARATIVE ANALYSIS

Key Key ParametersParameters Liaison OfficeLiaison Office Branch Office/ Project OfficeBranch Office/ Project Office

Indian Incorporated Entities(J.V., Indian Incorporated Entities(J.V., WOSWOS

LLP etc)LLP etc)

Income Tax Income Tax

a) Statusa) Status

• Foreign companyForeign company • Foreign companyForeign company • Indian company Indian company

b) Tax on b) Tax on IncomeIncome

• Liaison offices are not liable to pay income tax in India as they are prohibited to make any profit under the rules

• -Transfer Pricing Rules:

• Transactions between liaison office and parent/associated entities are not subject to Transfer Pricing (TP) Regulations

• Branch and Project office is liable to pay income tax in India on the profits attributable to it at the rates applicable to foreign companies

• Transfer Pricing Rules• The transactions between

Branch and parent/associated entities are subject to Transfer Pricing (TP) Regulations.

• Subject to tax Subject to tax As per applicable rules & regulationsAs per applicable rules & regulations

• Transfer Pricing Rules• The transactions between Indian

Subsidiary/JV and parent/associated entities are subject to Transfer Pricing (TP) Regulations.

c) Tax on c) Tax on remittancremittance of e of profits profits

• Not applicable – since no Not applicable – since no profits are earnedprofits are earned

• Intermittent repatriations of Intermittent repatriations of profits is allowed subject to profits is allowed subject to BO/PO having discharged its tax BO/PO having discharged its tax obligation as aboveobligation as above

• No additional taxes to be paid No additional taxes to be paid on repatriationon repatriation

• Profits can be remitted by way of Profits can be remitted by way of dividend dividend

• Dividend distribution is subject to tax Dividend distribution is subject to tax @ 16.60875% on the amount of @ 16.60875% on the amount of dividend to be discharged by the dividend to be discharged by the company over & above aforesaid taxcompany over & above aforesaid tax

d) Tax on d) Tax on capital capital repatriatirepatriationon

• Upon closure, surplus cash Upon closure, surplus cash if any to be repatriated if any to be repatriated without any tax obligationwithout any tax obligation

• Upon closure, surplus cash if any Upon closure, surplus cash if any to be repatriated subject to to be repatriated subject to BO/PO having discharged its tax BO/PO having discharged its tax obligation in Indiaobligation in India

• Repatriation of share capital Repatriation of share capital permitted. Taxable as capital gains in permitted. Taxable as capital gains in case of buy-backcase of buy-back

Tax requirements

Luthra & Luthra, Chartered Accountants

Legal/ Regulatory requirements

COMPARATIVE ANALYSIS

Key Parameter

s

Liaison Office

Project office

Branch Office

Joint Venture

Wholly Owned

Subsidiary

LLP

Service tax Compliance

Not required - LO cannot render taxable services

May be required to obtain registration depending upon nature of operations or kind of services

May be required to obtain registration depending upon nature of operations or kind of services

May be required to obtain registration depending upon nature of operations

May be required to obtain registration depending upon nature of operations

May be required to obtain registration depending upon nature of operations

Closure of business – Exit

5 to 6 months (subject to tenure and level of operations)

5 to 6 months (subject to tenure and level of operations)

5 to 6 months (subject to tenure and level of operations)

18 to 24 months (subject to tenure and level of operations)

18 to 24 months (subject to tenure and level of operations)

5 to 6 months (subject to tenure and level of operations)

Luthra & Luthra, Chartered Accountants

““There is nothing so dangerous as the There is nothing so dangerous as the pursuit of a rational investment policy pursuit of a rational investment policy in an irrational world”in an irrational world”

- John Maynard - John Maynard KeynesKeynes

Luthra & Luthra, Chartered Accountants

Luthra & Luthra, Chartered Accountants

Queries, if any, are welcome

Luthra & Luthra, Chartered Accountants