presentation - venture capital financing, major deal elements

TRANSCRIPT

Major Deal Elements Venture Capital Term Sheets Analysis

Daniel J. PiedraJ.D., expected ‘16University of San Diego School of Law

Major Deal Elements

1. A Preferred Return

2. Protection of Valuation and Position re: Future Money

3. Management of the Investment

4. Exit Strategies

Preferred Return❖ Perception of the VC Investor:

❖ When the Investor writes the check, he has done almost everything he promised

❖ The entrepreneur has done nothing yet

❖ Result: The VC wants its money to be paid back before the Entrepreneur gets his/her return.

❖ Instrument: CONVERTIBLE PREFERRED STOCK

Preferred Return❖ Dividends:

❖ Paid to Preferred First

❖ Cumulative or Accruing

❖ Liquidation Preference ❖ “Straight” Liquidation Preference: The Preferred receives its original

investment amount plus accrued dividends (if any) before Common receives anything.

❖ Participating (“Double Dip”) Preferred: The Preferred first gets its liquidation preference and then shares any remaining proceeds with Common. Increasingly subject to a cap of 3X or 4X (including preference).

Preferred Return: Liquidation Events

❖ Liquidation, dissolution, sale of assets

❖ Money comes into corporation

❖ Money paid out to stockholders to redeem stock

❖ “Deemed liquidation”— merger or other positive event

❖ Consideration may be stock or cash

❖ Consideration may go directly to stockholders

Protection of Valuation:Conversion and Anti-dilution

❖ Anti-dilution Adjustment increases the number of shares received on conversion of Preferred

❖ What Triggers Anti-dilution Adjustment?

❖ Issuance or “deemed issuance” of Common at less than preferred issuance price

❖ “Deemed issuance”— adjust upon issuance of derivative security; if common never issued, readjust later

❖ Options, warrants

❖ Convertible securities

Protection of Valuation:Conversion and Anti-dilution

❖ Conversion Events: When Does Preferred Convert Into Common?

❖ Voluntary

❖ Forced: often some % of Preferred can force conversion of all

❖ Automatic--upon “Qualified IPO”

❖ Minimum total offering; minimum share price (usually 3 to 5 times initial purchase price)

❖ Conversion Ratio--initially 1:1

❖ Adjustments--stock splits, etc; price anti-dilution

❖ Exceptions--option pool, conversion of preferred, outstanding warrants, other existing conditions, other special exceptions

Valuation❖ Conversion Ratio:

❖ Original Purchase Price (OPP)/ Conversion Price (CP)

❖ Initially OPP = CP, so Conversion Ratio = 1:1

❖ “Full ratchet”: CP reset to equal price at which diluting security is sold

❖ “Weighted average”: CP new = CP old x R

❖ Where R = (N + M/CP old)/(N+S)

❖ N = old shares outstanding (fully diluted)

❖ S = new shares to be issued

❖ M = new money ($)

Protection of Position: Preemptive Rights

❖ Permits Investors to participate pro rata in future financings, to preserve their percentage ownership

❖ Subject to exclusions:

❖ Option pool issuances

❖ Strategic alliances & licenses

❖ “Pay to Play”

Preemptive Rights, cont'd

❖ Granted by Founders/Other Investors

❖ First Refusal: Gives Investors the right to acquire shares offered by the grantor, pro rata

❖ May be partial or “all or nothing”

❖ Tag Along (Co-Sale): Gives Investors the right to sell shares pro rata if a Founder sells shares to others

❖ Helps lock in Founders

Management of the Investment❖ Board Seat(s)

❖ Importance of the “Independent Director(s)”

❖ Business Approvals ❖ Capital Expenditures, etc.

❖ Approval of Annual Budget and Operating Plans

❖ Information Rights ❖ Reports, financial statements — NDA advised

Other Management Considerations

❖ Option Pools

❖ Traditionally 12% to 18% at Round One

❖ Two Year Pool

❖ Vesting of Founders/Key Management Stock

❖ Non-Competition and Invention Agreements

Exit Strategies• IPOs and Registration Rights

• Sale/Acquisition

• Redemption of Stock

• Registration Rights

Registration Rights

❖ Shares cannot be freely sold without filing a Registration Statement with the SEC

❖ Only the Company can file

❖ So the Investors negotiate for certain Registration Rights to insure a contractual ability to exit into the public markets

Registration Rights, cont’d❖ Enables Investors to sell shares publicly by means

of a registered offering❖ Sales prior to end of 1-year holding period❖ Avoid compliance with volume limitations of

Rule 144❖ Registration paid for by the Company❖ Are Founders included?

Demand Registration Rights

❖ Exercisable after the IPO or within 3-7 years of investment

❖ Can be exercised 1 to 3 times;

❖ Can be exercised by holders of 20-50% of the registrable shares, with value of [$$$]

Piggyback Registration Rights❖ Investors “piggyback” on another registration

❖ Can they participate in other shareholders’ demand rights?

❖ Subject to underwriter “cutback”

❖ S-3 Registrations generally unlimited

❖ Acorn

❖ Beach

Redemption

❖ The Company’s repurchase of Preferred Stock at the demand of the Investors

❖ When Used: When the Company hasn’t gone public

❖ Because Founders Don’t Want To

❖ Because Business Doesn’t Develop Into an IPO Type

Redemption, cont’d❖When Does Redemption Kick In?

❖Typically after Five (5) years❖Often phased over Three (3) years

❖Trigger❖Automatic❖Upon vote of Preferred

❖Price❖Initial Purchase Price paid plus accrued dividends❖Sometimes additional return

❖Different classes of preferred — later classes won’t let earlier investors out first

Macon, Inc. Venture Capital Term Sheets Analysis

Daniel J. PiedraJ.D., expected ‘16University of San Diego School of Law

Differences & Similarities

Acorn Ventures

Beach Fund

Acorn Ventures

Capitalization Table: Acorn, with Escrow

Capitalization Table: Acorn, No-Escrow

Beach Fund

Capitalization Table: Beach

Similarities ❖ Investment Amount: $5 million

❖ Series A Convertible Preferred Stock

❖ Conversion Rate

❖ Registration Rights

❖ Information Rights

❖ No Termination Rights

❖ Closing Conditions: Acorn — “Securities Purchase Agreement”; Beach — “Conditions Precedent to Financing”

❖ No “No-shop” Provision

Differences

❖ Valuation ❖ Acorn: Pre-Calculated

❖ $7.53 million, with 3 million “performance shares”

❖ Performance Shares: “Shares held in escrow; non-issuable if Macon doesn’t reach performance milestone

❖ Beach: Standard, with employee option pool

Dividends (Differences)❖ Acorn:

❖ Non-cumulative — $0.08 (standard) on a Series A Preferred Outstanding, when and as declared by the Board of Directors

❖ Other dividends: Participates with Common Stock on an as-converted basis

❖ Most beneficial to company❖ Beach

❖ Cumulative — most beneficial to investors; bad for company❖ 10% (above standard) per year commencing on one year

anniversary of issuance of Series A Preferred❖ Ends when dividend accrual reaches 25% of Series A Purchase Price❖ Can also cease with consent of Board of Directors

Liquidation (Differences)❖ Acorn

❖ 3x multiple — A return of three times the initial pay issuance price

❖ Lower than standard 5x

❖ Beach ❖ 1 1/4 multiple — A return of 1.25 the initial purchase

price plus all declared but unpaid dividends

❖ Pro rata distribution

Automatic Conversion (Differences)❖ Acorn

❖ Majority of Preferred can consent to conversion

❖ No assurance that VC can control or at least veto and /or change number of holders

❖ Valuation: $25 million offering at $5 million/share

❖ Beach ❖ Valuation: $25 million offering at $20/share

❖ Consent of Preferred not required

❖ Automatic conversion at IPO

Liquidation Differences, cont’d

Acorn: ❖ Better option

❖ Investor payment is approx. $5,330,000 at a $0.08 dividend

❖ Preferred is capped at three times initial investment amount

❖ Lower than standard (5x)

❖ Better for a merger and IPO because Investors are capped at 3x their initial investment

Liquidation Differences, cont’d

Beach: ❖ Larger initial payback to the investors of roughly

$7,500,000 at a $0.25 unpaid dividend

❖ Allows for pro rata distribution of remaining proceeds to all shareholders

❖ No multiplier on distribution of remaining assets

❖ Excludes reference to subsequent financings

Anti-Dilution (Differences)❖ Acorn

❖ Broad-based weighted average❖ Carve out: No adjustment for issuance up to 3 million Common to

employees, directors, etc., pursuant to board-approved equity incentive plans❖ Helps to retain talent and incentivize employees

❖ Beach ❖ Weighted average❖ Share issuance of less than 50% of Series A Purchase Prices slips to

full ratchet ❖ Conditional: Only if Series A holder invests its pro rata share

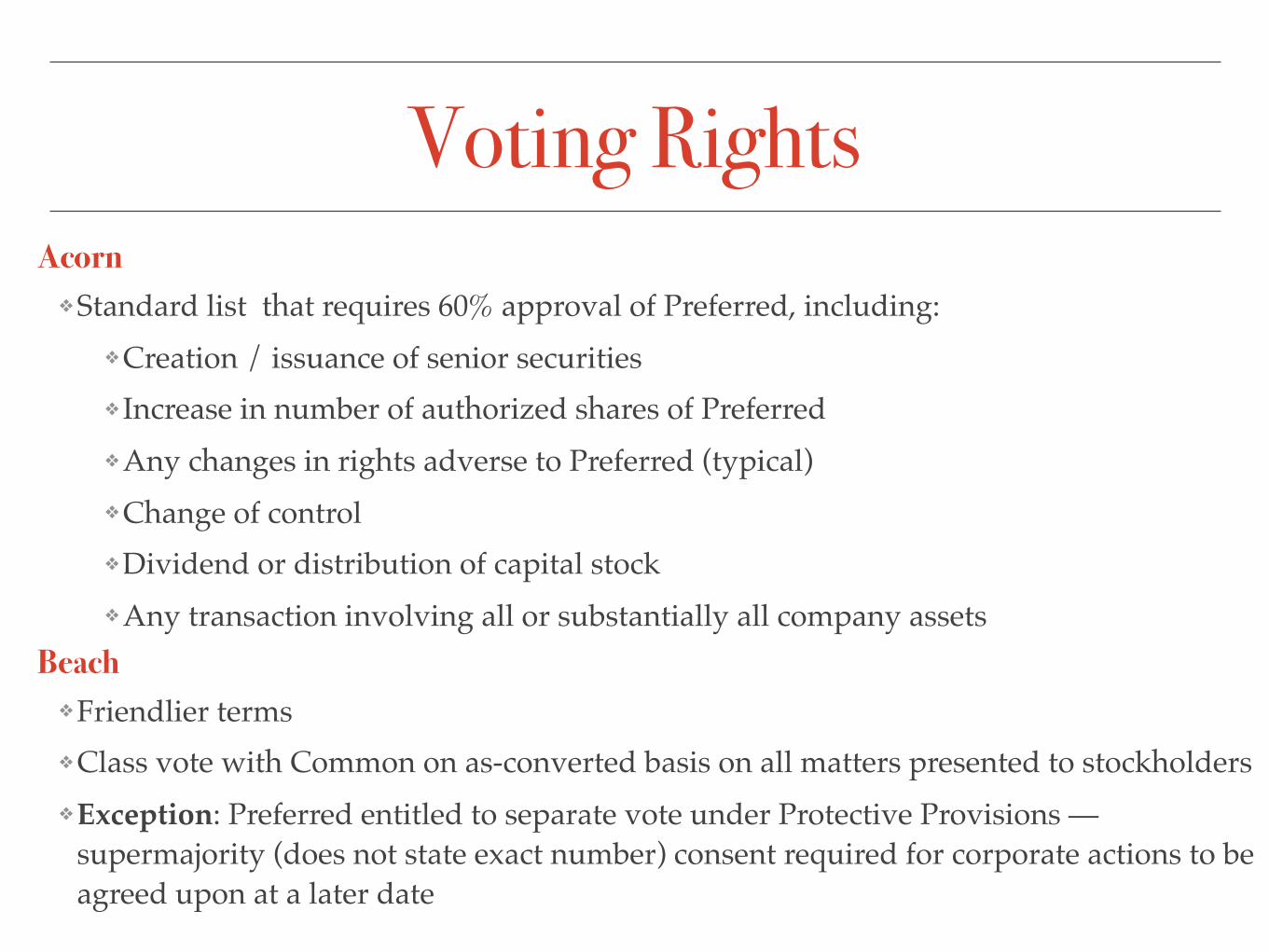

Voting RightsAcorn

❖Standard list that requires 60% approval of Preferred, including:❖Creation / issuance of senior securities❖ Increase in number of authorized shares of Preferred❖Any changes in rights adverse to Preferred (typical)❖Change of control❖Dividend or distribution of capital stock❖Any transaction involving all or substantially all company assets

Beach ❖Friendlier terms❖Class vote with Common on as-converted basis on all matters presented to stockholders❖Exception: Preferred entitled to separate vote under Protective Provisions —

supermajority (does not state exact number) consent required for corporate actions to be agreed upon at a later date

Rights of First Refusal & Co-Sale❖ Acorn

❖Right of First Refusal❖Preferred has

❖ (1) pro rata right based on equity ownership to participate in subsequent equity financings; and

❖ (2) right to consider purchase of any potential sale of Common stock

❖Right of Co-Sale: Except through an IPO sale, Preferred have right to participate in Common transferring of shares

❖ Beach ❖Neither Right of First Refusal nor Co-Sale Rights

Anti-Dilution (Differences)

Beach ❖Down round after Series A financing❖No waiver ❖Reset of anti-dilution protection by existing investors required

Board Representation❖ Acorn

❖Favorable to investors❖ If Performance Shares released, then investors have option to replace the

outside director with a investor-chosen director❖Harmful to control

❖ Beach ❖More favorable to Founders❖Arrangements include:

❖One member elected by the Founder;❖Two Series A Investor-elected representatives;❖One outsider company nominated; and ❖One outsider company nominated and acceptable to all

#2: The No Frills Term Sheet

On-its-Face Selection of One Term

Sheet

Selection: Beach Fund❖ Acorn has three investors;

potential conflicts❖ Dividend term concerning but

negotiation — Board’s consent authority mitigating factor

❖ Simple Board structure❖ Acorn’s Registration Rights

potential to be expensive❖ Better liquidation preference

(except for merger)

#3: Term Alterations During Negotiations

1.Valuation

2.Liquidation Preference

1. Caps

3.Anti-Dilution Provisions

4.Dividends

5.Voting Rights

6.Redemption Rights

7.Founders Vesting Rights

8.Board Composition

9.Miscellaneous

Valuation

❖ Risk of "counting chickens before the eggs have hatched”

❖ Goal: Increase value placed on company to minimize cost of VC investment

❖ Develop financial projections for time of likely VC exit

Liquidation Preference

❖ Goal: Cap on Participating Preferred

❖ Non-Participating Preferred

❖ Cannot participate as common shareholders

❖ Aim for non-participating preferred shares, but odds are slim

❖ IPO inapplicable

Dilution❖ Focus on definition of “Outstanding Securities”

❖ Investors want full ratchet

❖ Conversion price of preferred is adjusted downward for a dilutive issuance on a dollar-for-dollar basis

❖ Least favorable to company

❖ Always try to get a “floor” on ratchet

❖ Company wants broad-based provision

❖ Calculating dilution based upon a “weighted average” more beneficial to the company

❖ Easily negotiable

Dividends❖ “When as declared by Board” – a non-cumulative dividend

❖ If Board does not declare then there is no dividend

❖ Standard for an early stage company

❖ Typical not to get a dividend every year – VC more interested in getting a bigger return at end, rather than a bit back every year

❖ For later-stage companies, it is more common to see cumulative dividend, generally paid out

❖ These companies have more money and investors may want to start seeing return

Voting Rights❖ Focus on limiting to events that directly impact preferred

rights or investments

❖ holder of Preferred will have the

❖ 1:1 votes / share ideal

❖ Avoid provisions that give investors too much management control

❖ Acorn: Substantial control requirements

❖ Beach: Certain corporate actions requires “supermajority” vote by Series A Preferred

❖ Indicated flexibility

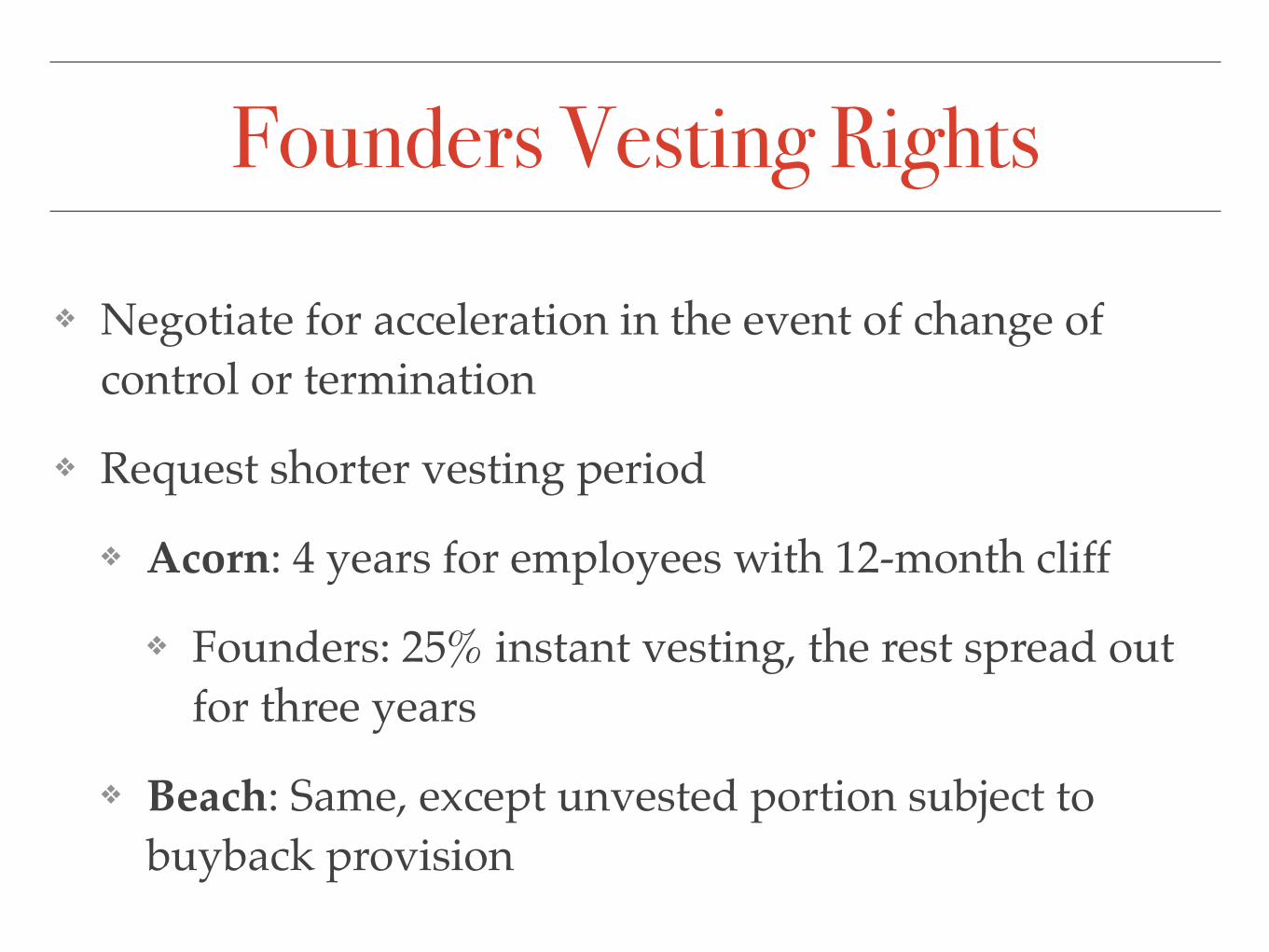

Founders Vesting Rights

❖ Negotiate for acceleration in the event of change of control or termination

❖ Request shorter vesting period

❖ Acorn: 4 years for employees with 12-month cliff

❖ Founders: 25% instant vesting, the rest spread out for three years

❖ Beach: Same, except unvested portion subject to buyback provision

Board Composition❖ Heavily negotiated❖ All about control❖ Critical for exits❖ Common for VCs to want at least one seat on the board (and perhaps

more depending on the amount invested)❖ Focus on the final seat

❖ Will preferred and common vote together as a single class or separately?

❖ Additional control granted if Company fails to meet benchmarks?❖ Negotiations will focus on amount invested and level of control sought or

required

Rights of First Refusal & Co-Sale Acorn ❖ Right of First Refusal too broad — includes all Series

A Preferred❖ Recommended: Preferred may exercise such right

only at a price equal to the lower of: ❖ (i) the price offered by the proposed third party

purchaser; and ❖ (ii) the price most recently set by the Board of

Directors as the fair market value of the Common.

Miscellaneous

❖ Information Rights ❖ Seek appropriate restrictions such as a non-disclosure

agreement

❖ Protective Provisions ❖ Ensure that VCs do not have too much control

❖ Drag Along Rights ❖ Focus on appropriate thresholds

#4: Slow Growth or Fast Growth

Benefits & Drawbacks for

Company

• Instant growth mean results in higher valuation from subsequent investors

• If passion for company is high, then slow growth best option — but VC

investors wary

• Hobson’s Choice

• Key Determinant of Valuation: Risk

• Low valuation at start up

• Limit involvement with too many investors so as not to set unreachable

milestones

• Value of company grows and risks decrease as milestones are reached

• Result: Cost of company shares increase

• Ultimate Question: What is goal of company?

• Large Business

• Small Business

#5: Realization: IPO v. Merger

Benefits & Drawbacks for

Company

Acorn: •Automatic Conversion: Upon IPO, preferred shares are converted to

common, whereas the VC loses liquidation preference•Beneficial to Company

•Vesting Provision•One-year accelerated vesting following change of control transaction•Favorable to Founder

Beach: •Automatic conversion: For IPO, subject to share price limitation and

aggregate proceeds offering•70% preferred holders, acting as single voting class, can elect to not treat a

consolidation or merger as a dissolution or winding up•Favorable to preferred, because liquidation preference survives merger or

consolidation•Vesting Provision

•Restricts Founders’ access to shares with 48-month vesting period; early exit poses challenge

#6: Other Considerations

Important Factors Outside

of the Term Sheet

•Reputation

•Good chemistry with leaders

•Experience

•Track record

•Length of operation

•Successful investments

•Post-exit relationships with previous partners

•Successful management and operational structure

Personalities, Management & Track Record

VC Involvement: Normally involves a representation on boardOther factors:

Active •Value-added services (i.e., marketing, market knowledge, recruitment, etc.)

•An active partnership

Passive / Major Decisions •Involvement in major decisions

•Appointed board member as watchdog

•Information rights (periodic statements of financial and other information.

•Get-in and get-out

Viability Fund must have committed financiers who are “going for the gold”

Flexibility: • Founders should seek out flexible in adjusting to

unpredictable events and changes in Company• Many VCs have rigid rules

Geographic Proximity