presentation to universita’roma3 low cost-modello differenziato di business 13 th of december 2010...

TRANSCRIPT

1

Presentation to Universita’Roma3

Low Cost-Modello differenziato di Business

13th of December 2010

1

2

easyJet Business Model easyJet’s business model is centred on being:

low cost, financially strong and highly efficient

Building Europe’s number one air transport network – by establishing a dense point-to-point network serving Europe’s largest unique catchments through convenient airports

Providing a strong customer proposition and

strong visible brand

Dynamic fares…if you book early, you pay less

Optional extras – pay only for what you need

Distribution - over 98% initial sales on-line

Operate a highly utilised fleet

3

Europe’s best performing airline-Highlights 2010

easyJet’s advantaged network and improved consumer demand has driven strong revenue performance

Total revenue per seat up 5.1% reported, +3.3% at constant currency

Seats flown grew by 6.0%, with a 15.9% increase in mainland Europe

Market share has grown from 6.5% to 7.6% over the last year

Underlying profit per seat grew by £2.53 to £3.36

Fuel costs reduced by £2.19 per seat as higher priced hedges rolled off

Mix improvement offset the increased costs of disruption

Return on equity grew 3.1ppt to 8.6%

Continued strong cash generation, net cash flow from operations improved by £229m to £363m

3* Excludes interest income* Excludes interest income

4

easyJet has strengthened

4

5

Cost per seat - key drivers

5

6

Delivering cost savings

Additional £65m of cost reduction identified

Original target p.a. by F’11

Increased target p.a. by F’12

Ownership - exit expensive aircraft from fleet £40m £30m

Maintenance - in-sourcing, SRT deal & further contract renegotiation, efficiency projects

£8m £35m

Overheads - leverage scale £6m £10m

Airports & Handling – handing & volume deals, check-in process improvement, some self handling & low cost terminals

£9m £60m

Crew – productivity & flexibility initiatives, Boeing exit (no requirement to ring fence crew), new rostering systems

£30m £35m

Fuel – GPU usage, flight planning, fuel reporting and pilot technique

£30m £20m

Total £125m £190m

Delivers a net benefit to the bottom line of £1 per seat by end F’12

7

Efficient fleet management

771 includes 4 aircraft held for sale (4 x A320) which will exit the fleet by 30.09.10

8

easyJet’s Growth First flight operated on the 10th

November 1995 between Luton and Glasgow

Average year on year growth of 15% 2006 -2008

Passenger Growth

20 bases across Europe inc. Rome (FCO) established in 2009

Further mid-term growth 7.5% per annum - over 5 year

48.8 M passengers transported in 2010 (+7,9%)

9

easyJet’s phenomenal growth in Europe

easyJet has seen continued growth since start of operations in 1995

easyJet is No3 in Italy, No2 in France and Spain and No1 in the UK

easyJet has seen continued growth since start of operations in 1995

easyJet is No3 in Italy, No2 in France and Spain and No1 in the UK

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

Year

Passen

gers

easyJet France

easyJet

easyJet France 5,500,000 6,600,000 8,000,000 10,000,000 11,000,000 12,000,000

easyJet 33,000,000 38,000,000 44,000,000 45,000,000 48,000,000 53,000,000

2006 2007 2008 2009 2010 2011

10

Network- What we are interested in

Slots in primary, congested Airports, to attract good yields

Airfields is not our Business

Good catchment areas, with natural, healthy mix of outgoing and incoming passengers

Airports with different services for different Airlines models

Airports available to share investments principles

Airports which come up with ideas to promote, and not kill, high load factor

Less spreadsheets, more facts

Point to point- W patterns are operational and cost burdening

11

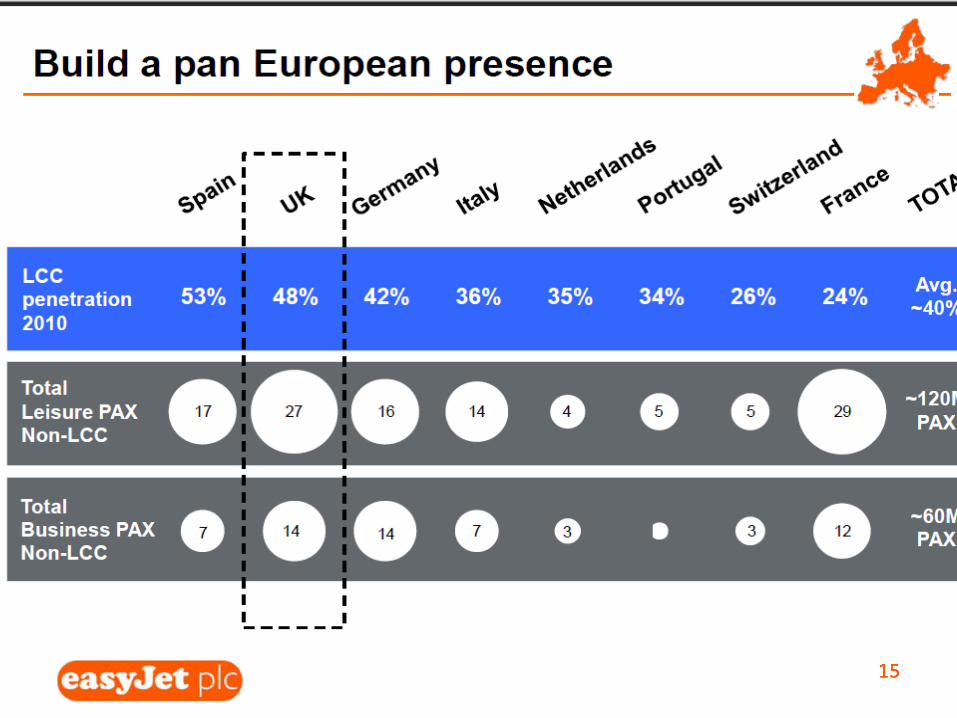

Network – Connecting Convenient Airports

UK’s largest airline

Europe’s 4th largest airline

Accessible Network:

Over 300m inhabitants within one hours drive on an easyJet airport

Increasing diversity

Pan European Network – 53% of passengers originate from outside the UK

Third of flying does not touch the UK

Vital Network Statistics:

29 countries

20 bases

123 airports

More than 500 routes

196 aircraft

48.8 million passengers

12

Breadth and depth of network Leading presence on Europe’s

top 100 routes

Strong, defendable positions

London Gatwick No.1

Milan Malpensa No.1

Geneva No.1

Paris No.2

Berlin Schönefeld No.1

13

Efficient fleet management

1313

141414

151515

16

easyJet growth in Fiumicino

Start of Operations in November 08

Start of based operations in November 09

Steady, Constant growth year on year

99000

1058000

1921000

0

500000

1000000

1500000

2000000

2500000

2008 2009 2010

YEAR OF OPERATIONS

PA

SS

EN

GE

RS

NU

MB

ER

17

easyJet in Ciampino

Decrease of traffic in favour of FCO started in 2009

Process continues based on slots and infrastructures availability

1034000

884000

682000

0

200000

400000

600000

800000

1000000

1200000

2008 2009 2010

YEAR OF OPERATIONS

PA

SS

EN

GE

RS

NU

MB

ER

18

Differential pricing for LCC’s = Growth

Airports across Europe moving to ‘pay for use’ & ‘differential pricing’ – rewarding efficient use of Airports

Establishing a differential pricing structure should be easier and does not need to represent a downgraded quality of services

Low cost does not mean no seats and no shops

More efficient infrastructure usage allows for differential pricing (as per EU regs) e.g.:

Parking positions accessible by foot (walk in-walk out everywhere); no buses, no airbridges

Per usage charges; not per departing passenger

Airports across Europe moving to ‘pay for use’ & ‘differential pricing’ – rewarding efficient use of Airports

Establishing a differential pricing structure should be easier and does not need to represent a downgraded quality of services

Low cost does not mean no seats and no shops

More efficient infrastructure usage allows for differential pricing (as per EU regs) e.g.:

Parking positions accessible by foot (walk in-walk out everywhere); no buses, no airbridges

Per usage charges; not per departing passenger

19

The Key Economic Driver- “The passenger”

Growth incentives to be encouraged at all airports, especially where infrastructure changes are not possible, to reward growth in overall traffic volumes

A charging structure that favours efficient airlines; with lesser passenger weighted charges, delivers demonstrable and measurable benefits:

Higher load factors and therefore more passengers driving commercial revenues for airport

Lower environmental impact of air travel for passengers, through efficient use of aircraft

20

…..we need each other to get the job done!

easyJet

Airports

21

Thank you!