presentation to the health market inquiry · bonitas open scheme market share 53,8% 13,4% ......

TRANSCRIPT

PRESENTATION TO THE

HEALTH MARKET

INQUIRY

19 May 2016

BONITAS | HMI1

Agenda

• Presenters

• Dr A Ramasia (Principal Officer)

• Mr R Cowlin (Trustee)

• Mr G van Emmenis ( Chief Operations Officer)

• Historical Overview and Scheme Profile

• Risk Management and Non-Healthcare Costs

• Market Forces

BONITAS | HMI2

HISTORICAL OVERVIEW

AND SCHEME PROFILEDr A Ramasia

BONITAS | PRESENTATION TITLE3

Historical Overview

• Founded in 1982 primarily as a scheme for the black civil servants,

within the Medscheme stable

• 34 years old

• Second largest open medical scheme in South Africa

• Manages 650 000 lives

• R3.3 bn in reserves

• Solvency of 26%

• Largest general practitioner network in South Africa

(6200 contracted GPs)

• Specialist network of 2600 practitioners

• Membership within Municipalities (SALGA), Eskom, Other large

corporate entities

BONITAS | HMI4

BONITAS | HMI5

Bonitas open scheme market share

53,8%

13,4%

4,6% 4,6% 3,9% 3,3% 3,0% 2,4% 2,4%

8,6%

Discovery Bonitas Momentum Medihelp Bestmed Medshield Fedhealth Sizwe Liberty Otherschemes

2013 2014

Source: CMS Annual Reports

BONITAS | HMI6

BONITAS GOVERNANCE STRUCTURES

Board of Trustees

11 positions

1 vacancy

Audit and Risk

3 Independent members

2 Board members

Working and Strategic Committee

5 Board members

2 Executives

Investment

1 Independent members

2 Board members

Remco

2 Independent members

3 Board members

Appeals

3 Independent members

7

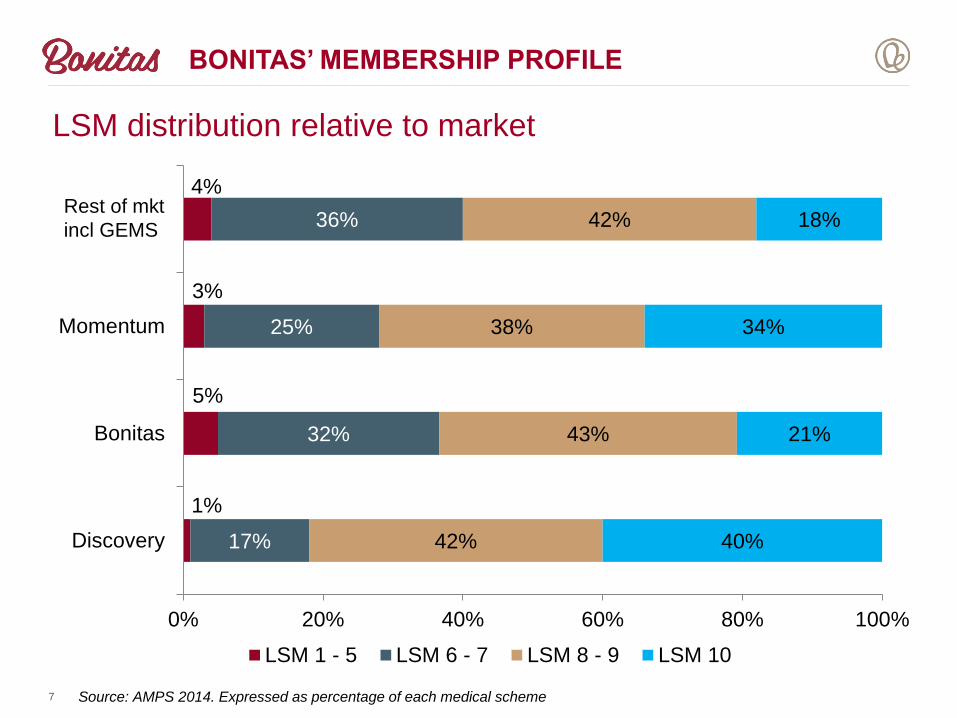

LSM distribution relative to market

Source: AMPS 2014. Expressed as percentage of each medical scheme

1%

5%

3%

4%

17%

32%

25%

36%

42%

43%

38%

42%

40%

21%

34%

18%

0% 20% 40% 60% 80% 100%

Discovery

Bonitas

Momentum

Market

LSM 1 - 5 LSM 6 - 7 LSM 8 - 9 LSM 10

BONITAS’ MEMBERSHIP PROFILE

Rest of mkt

incl GEMS

BONITAS | HMI8

BONITAS’ MEMBERSHIP PROFILE

67%

22%

7%

4%

Black

White

Coloured

Indian

39%

54%

4%

3%

Black

White

Coloured

Indian

39%

45%

6%

10%

Black

White

Coloured

Indian

Discovery

Bonitas Fedhealth

Momentum

44%

44%

5%

7%

Black

White

Coloured

Indian

Source: AMPS 2014

BONITAS | HMI9

PMB cost graphs

5 145

5 885

6 597

7 830

2011 2012 2013 2014

PMB cost - R per beneficiary per year

14%

12%

19%

52%

THE IMPACT OF PMBS

BONITAS | HMI10

Bonitas PMB claims as a proportion of total risk claims

38,7% 39,9%43,3% 45,9% 48,1% 49,4%

52,9% 53,9%

8,4% 8,9%

10,2%9,4%

9,3% 9,5%9,7% 10,5%

52,9% 51,2%46,5% 44,6% 42,6% 41,0%

37,3% 35,6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014 2015

Risk Amt PMB IH Risk Amt PMB OOH Risk Amt Non PMB

THE IMPACT OF PMBS

Managed care moving from rules based to member-centric

initiatives with providers playing a key role

BONITAS | HMI11

MHC EVOLVING

Empowerment

Activation tailored

to needs

Improved

outcomes

Positive

experience

Transactional

Defined Benefit

Contained Cost

! VALUE-BASED

Managed care moving from rules based to member-centric

initiatives with providers playing a key role

MHC EVOLVING

High

risk

individuals

Emerging risk

individuals

Diseased individuals

Individuals with risk factors or acute episodes

Healthy individuals

Stratified scheme

population

Stratified Disease Management (DM)

High risk beneficiary

programme (DM) +

lifestyle interventions

Emerging Risk

(DM) + lifestyle

interventions

Other (DM)

Cases +

interventions

Strategic

purchasing

Coordination

of care

Individual wellness

Benefit utilisation risk

management/exception

management

Fraud, waste & abuse

management

BI, analysis and

monitoring

2015 Savings

Total Estimated (net) Reduction in Claims R158.30 pmpm

Total Estimated (net) Reduction in Claims R559.1 million

Reduction as a % of 2015 Risk Claims 6.3%

Reduction as a % of 2015 Risk Contributions 5.3%

BONITAS | HMI13

VALUE OF MANAGED CARE

Based on directly measurable savings only and does not take in to account behaviour change as a

result of managed care interventions (“halo” effect) and direct savings which cannot currently be

quantified.

RISK MANAGEMENT AND

NON-HEALTHCARE

COSTSGerhard van Emmenis

BONITAS | PRESENTATION TITLE14

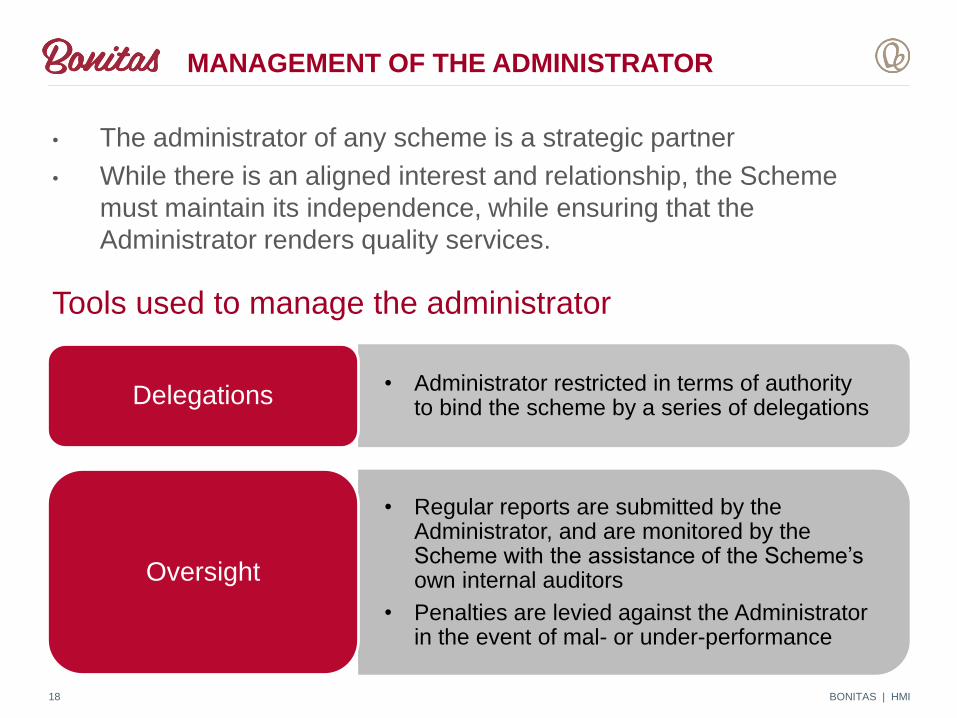

Independent relationship between Scheme and Administrator -

Managing the risk• As seen from the Historical overview, the Scheme commenced

operating as such within the Medscheme stable.

• Due to the change in the legislative environment, the Scheme had to

be re-structured and exist in its current form

• The Scheme separated completely from Medscheme, which it retains

as a strategic service provider.

• The Scheme is the dominant partner in the relationship

• Branding of the Scheme and Medscheme remains completely separate

– there is a concerted effort to ensure that both the corporate identities

and the branding of the Scheme remains distinct from that of its

administrator.

• Also, the Scheme ensures its independence by ensuring that the

following elements remains fully within its control

BONITAS | HMI15

CORPORATE GOVERNANCE PRINCIPLES

• Tariffs negotiations with Service Providers are done by the Fund

• With managed care agreements, the Schemes MHO only facilitates the negotiation process

• Final decisions and contracts concluded solely by the Scheme

Tariffs Negotiations

• Procurement is done by the Scheme strictly in line with its own procurement process

• Independently managed internally by the Scheme

Procurement

BONITAS | HMI16

• Opening and closing of bank accounts are only done on instruction of the Board of Trustees

• Control is maintained over these bank accounts as is required in terms of section 26(1)(c) of the Medical Schemes Act

• The Scheme’s investments are independently maintained by the Scheme’s duly appointed investment advisors

Banking & Investments

BONITAS | HMI17

CORPORATE GOVERNANCE PRINCIPLES

Tools used to manage the administrator

BONITAS | HMI18

• Administrator restricted in terms of authority to bind the scheme by a series of delegations

Delegations

• Regular reports are submitted by the Administrator, and are monitored by the Scheme with the assistance of the Scheme’s own internal auditors

• Penalties are levied against the Administrator in the event of mal- or under-performance

Oversight

MANAGEMENT OF THE ADMINISTRATOR

• The administrator of any scheme is a strategic partner

• While there is an aligned interest and relationship, the Scheme

must maintain its independence, while ensuring that the

Administrator renders quality services.

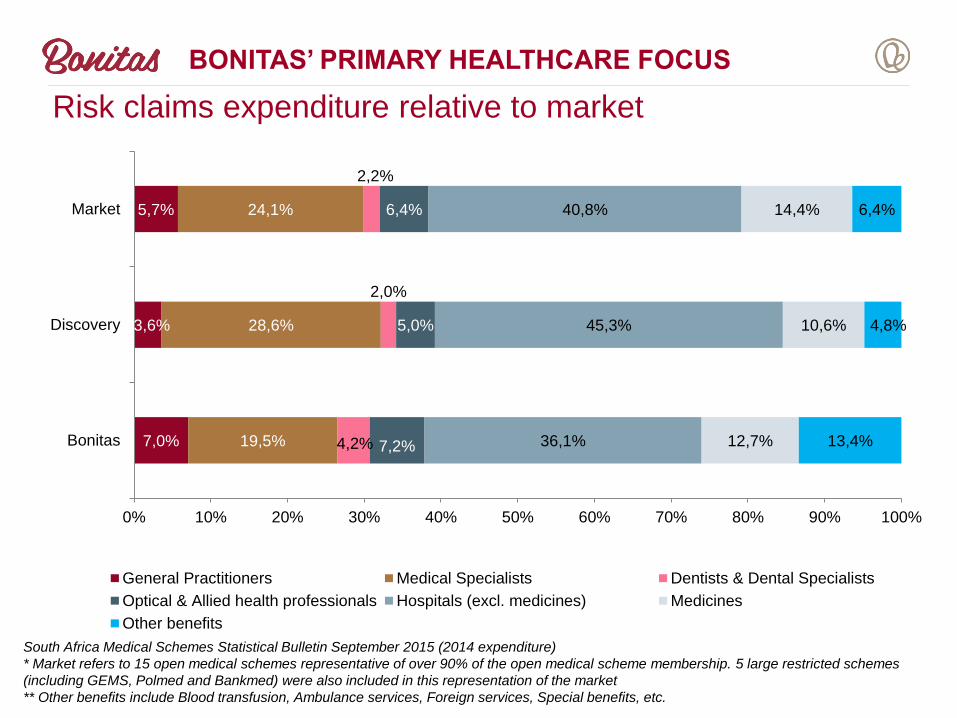

Risk claims expenditure relative to market

South Africa Medical Schemes Statistical Bulletin September 2015 (2014 expenditure)

* Market refers to 15 open medical schemes representative of over 90% of the open medical scheme membership. 5 large restricted schemes

(including GEMS, Polmed and Bankmed) were also included in this representation of the market

** Other benefits include Blood transfusion, Ambulance services, Foreign services, Special benefits, etc.

7,0%

3,6%

5,7%

19,5%

28,6%

24,1%

4,2%

2,0%

2,2%

7,2%

5,0%

6,4%

36,1%

45,3%

40,8%

12,7%

10,6%

14,4%

13,4%

4,8%

6,4%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Bonitas

Discovery

Market

General Practitioners Medical Specialists Dentists & Dental Specialists

Optical & Allied health professionals Hospitals (excl. medicines) Medicines

Other benefits

BONITAS’ PRIMARY HEALTHCARE FOCUS

Risk+Savings claims expenditure relative to market

South Africa Medical Schemes Statistical Bulletin September 2015 (2014 expenditure)

* Market refers to 15 open medical schemes representative of over 90% of the open medical scheme membership. 5 large restricted schemes

(including GEMS, Polmed and Bankmed) were also included in this representation of the market

** Other benefits include Blood transfusion, Ambulance services, Foreign services, Special benefits, etc.

7,5%

5,8%

6,8%

21,6%

27,8%

25,1%

4,1%

4,8%

3,4%

7,4%

8,3%

8,0%

35,5%

34,6%

36,1%

15,5%

16,7%

17,9%

8,3%

2,1%

2,8%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Bonitas

Discovery

*Market

General Practitioner Specialists, Pathology & Radiology Dentists & Dental Specialists

Optical & Allied Health Professionals Hospital Medicines

** Other benefits

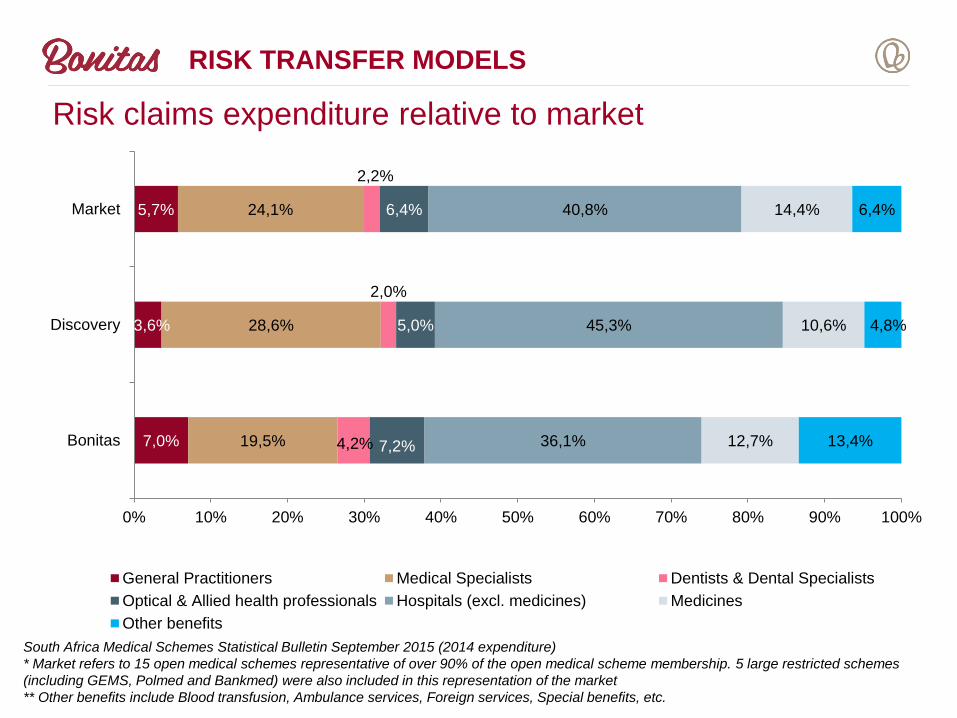

RISK TRANSFER MODELS

Risk claims expenditure relative to market

South Africa Medical Schemes Statistical Bulletin September 2015 (2014 expenditure)

* Market refers to 15 open medical schemes representative of over 90% of the open medical scheme membership. 5 large restricted schemes

(including GEMS, Polmed and Bankmed) were also included in this representation of the market

** Other benefits include Blood transfusion, Ambulance services, Foreign services, Special benefits, etc.

7,0%

3,6%

5,7%

19,5%

28,6%

24,1%

4,2%

2,0%

2,2%

7,2%

5,0%

6,4%

36,1%

45,3%

40,8%

12,7%

10,6%

14,4%

13,4%

4,8%

6,4%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Bonitas

Discovery

Market

General Practitioners Medical Specialists Dentists & Dental Specialists

Optical & Allied health professionals Hospitals (excl. medicines) Medicines

Other benefits

RISK TRANSFER MODELS

Risk Transfer Arrangements: Costs maintained at or near CPI

since inception in 2004

BONITAS | HMI22

Claims and Capitation Fees

0

50

100

150

200

250

300

350

400

450

500

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ind

ex

Dental: DENIS Optical: PPN/Iso Leso

Total In-hospital Claims CPI

RISK TRANSFER MODELS

BONITAS | HMI23

RISK TRANSFER MODELS - DENTAL

Dental costs contained in risk transfer arrangement

BONITAS | HMI24

Administration Costs pmpm

Year 2008 2009 2010 2011 2012 2013 2014

Discovery Health Medical Scheme 223 238 232 233 236 245 254

Bonitas Medical Fund 150 173 183 193 214 223 230

Momentum Health 182 187 183 169 170 173 184

Medihelp 212 204 209 216 234 266 311

Bestmed Medical Scheme 236 263 244 269 274 240 233

Medshield Medical Scheme 208 162 130 131 151 174 204

Fedhealth Medical Scheme 210 217 213 248 261 271 288

Liberty Medical Scheme 201 227 272 315 316

Sizwe Medical Fund 203 214 214 246 264 272 314

Keyhealth 201 222 240 245 251 254 283

MHC Costs pmpm

Year 2008 2009 2010 2011 2012 2013 2014

Discovery Health Medical Scheme 49 53 67 70 74 79 83

Bonitas Medical Fund 56 61 67 74 71 81 80

Momentum Health 48 50 51 49 46 45 47

Medihelp 37 40 40 46 54 56 63

Bestmed Medical Scheme 45 53 55 56 50 53 48

Medshield Medical Scheme 47 46 40 43 47 51 57

Fedhealth Medical Scheme 40 45 49 58 56 70 74

Liberty Medical Scheme 55 60 64 77 75

Sizwe Medical Fund 50 45 48 53 58 70 75

Keyhealth 43 51 52 56 62 65 70

Source: CMS Annual Reports

COMPARISON OF ADMIN AND MHC FEES

Comparison of Admin Fees: % of Contributions

BONITAS | HMI25

2008 2009 2010 2011 2012 2013 2014

Discovery Health Medical Scheme 13,7% 13,4% 12,4% 11,7% 11,2% 10,6% 10,2%

Bonitas Medical Fund 8,9% 9,4% 8,8% 8,8% 9,3% 8,7% 8,2%

Momentum Health 11,8% 10,8% 9,9% 9,6% 9,2% 9,2% 9,4%

Medihelp 8,5% 8,4% 8,0% 7,8% 8,7% 9,5% 10,4%

Bestmed Medical Scheme 14,0% 14,5% 9,9% 10,3% 10,2% 8,5% 7,8%

Medshield Medical Scheme 13,0% 9,6% 6,8% 6,1% 6,3% 6,9% 7,7%

Fedhealth Medical Scheme 11,6% 10,8% 9,2% 9,7% 9,8% 9,6% 9,9%

Liberty Medical Scheme 10,8% 10,5% 11,4% 12,1% 11,4%

Sizwe Medical Fund 10,7% 10,3% 9,4% 9,3% 9,0% 8,5% 9,0%

Keyhealth 8,5% 8,4% 8,3% 7,5% 7,0% 6,8% 7,2%

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

14,0%

16,0%

Discovery Health Medical Scheme

Bonitas Medical Fund

Momentum Health

Medihelp

Bestmed Medical Scheme

Medshield Medical Scheme

Fedhealth Medical Scheme

Liberty Medical Scheme

Sizwe Medical Fund

Keyhealth

Source: CMS Annual Reports

COMPARISON OF ADMIN FEES

2008 2009 2010 2011 2012 2013 2014

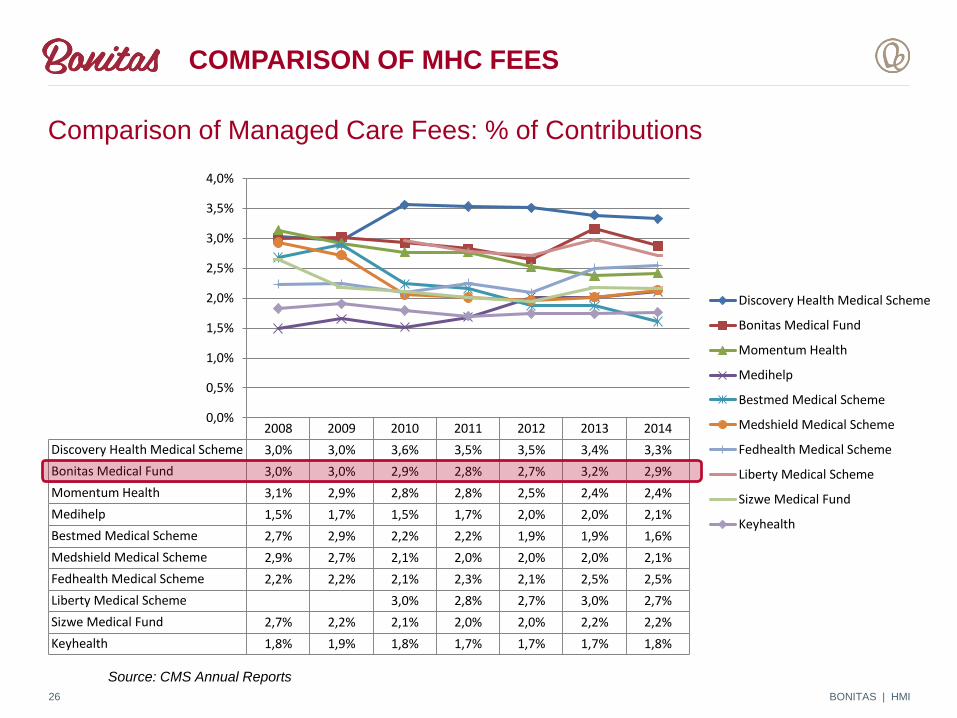

Discovery Health Medical Scheme 3,0% 3,0% 3,6% 3,5% 3,5% 3,4% 3,3%

Bonitas Medical Fund 3,0% 3,0% 2,9% 2,8% 2,7% 3,2% 2,9%

Momentum Health 3,1% 2,9% 2,8% 2,8% 2,5% 2,4% 2,4%

Medihelp 1,5% 1,7% 1,5% 1,7% 2,0% 2,0% 2,1%

Bestmed Medical Scheme 2,7% 2,9% 2,2% 2,2% 1,9% 1,9% 1,6%

Medshield Medical Scheme 2,9% 2,7% 2,1% 2,0% 2,0% 2,0% 2,1%

Fedhealth Medical Scheme 2,2% 2,2% 2,1% 2,3% 2,1% 2,5% 2,5%

Liberty Medical Scheme 3,0% 2,8% 2,7% 3,0% 2,7%

Sizwe Medical Fund 2,7% 2,2% 2,1% 2,0% 2,0% 2,2% 2,2%

Keyhealth 1,8% 1,9% 1,8% 1,7% 1,7% 1,7% 1,8%

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

Discovery Health Medical Scheme

Bonitas Medical Fund

Momentum Health

Medihelp

Bestmed Medical Scheme

Medshield Medical Scheme

Fedhealth Medical Scheme

Liberty Medical Scheme

Sizwe Medical Fund

Keyhealth

Comparison of Managed Care Fees: % of Contributions

BONITAS | HMI26

Source: CMS Annual Reports

COMPARISON OF MHC FEES

Tax Matters

• Tax contributions treated less favourably

• Largest impact in change in tax dispensation felt by higher LSM

groups which traditionally can afford medical aid

• Many buying down

• Unintended consequence may be to add to the burden of public

health care

• Misconception that self administered schemes save 14% VAT on

administration fee – saving is much less as VAT would be paid on

the components necessary for self administration

BONITAS | HMI27

BONITAS | HMI28

FRAUD, WASTE AND ABUSE

Fraud, Waste &

Abuse

Over-

Servicing

Billing

agents

Member

participation

Tariff

manipulation

False

claimsSyndicated

Opportunistic

Member

apathy

Provider

behaviour

(PMB’s)

BONITAS | HMI29

FRAUD, WASTE AND ABUSE

R1.4bn claims

assessed for HCPs

only

2.05m claim

events; 4.5m lines

Identified R72m FWA

= 5% of claims

5-month analysis (medical professionals only)

BONITAS | HMI30

Operational

improvements to

systemic

weaknesses and

policy gaps

Focused

member &

provider

education

Change

provider

billing

behavior

ZERO Tolerance

Policy

Industry

Consortium

Predictive

Analytics

Preventative

rather than

reactive

FRAUD, WASTE AND ABUSE

MARKET FORCESRodney Cowlin

BONITAS | PRESENTATION TITLE31

BONITAS | HMI32

No of new members brought on by brokers

66 272

43 921

61 162

51 794

29 745

43 618

38 335

34 608 34 675 34 547

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

No Broker Broker

Note: The Prosano amalgamation impact has been removed in the 2013 figure

BROKERS

BONITAS | HMI33

No of new members by type of broker26 8

21

19 8

86 31 8

04

27 4

69

13 7

97

24 6

59

22 5

99

28 8

10

20 5

25

20 9

37

12 021

4 756

4 55010 540

7 625

18 116

8 247

10 108

7 242 6 172

40 6

05

26 5

59

32 4

61

24 1

87

15 8

10

18 9

42

15 7

35

16 2

05

14 1

50

13 5

62

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Corporate Broker Direct Medical Scheme Broker

Note: The Prosano amalgamation impact has been removed in the 2013 figure

BROKERS

BONITAS | HMI34

NEW VS LEFT MEMBERS

79 447

51 190

68 815

62 196

37 837

52 177

37 762

44 344

39 422 40 473

47 794

43 575 44 17241 560

49 024

44 75642 289

21 897

35 880

42 227

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

New Left

Note: The Prosano amalgamation impact has been removed in the 2013 figure

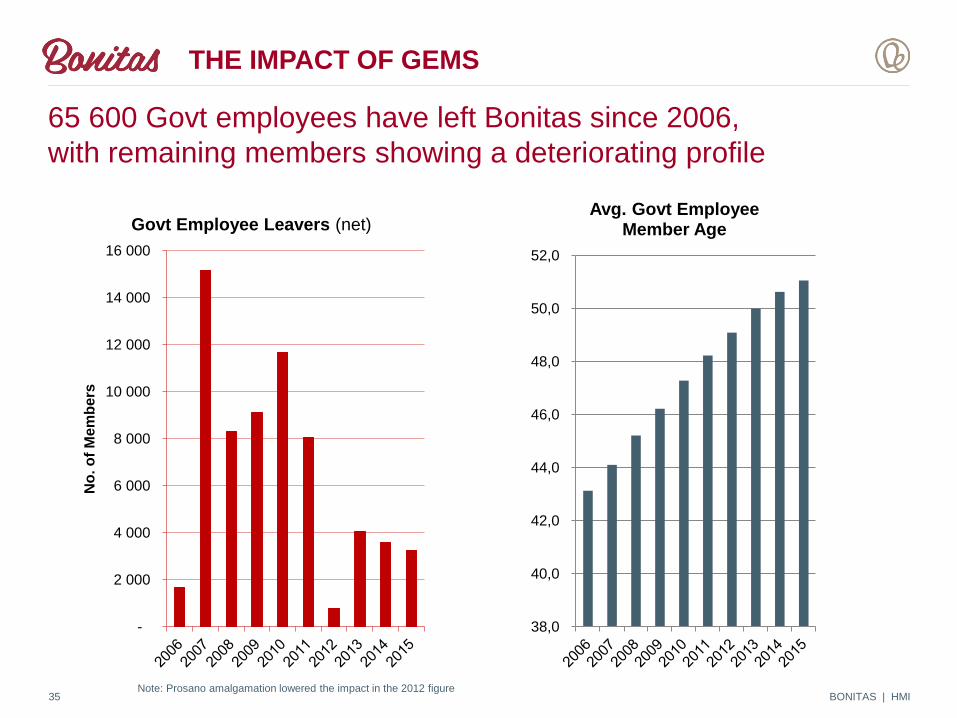

65 600 Govt employees have left Bonitas since 2006,

with remaining members showing a deteriorating profile

BONITAS | HMI35

-

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

No

. o

f M

em

bers

Govt Employee Leavers (net)

38,0

40,0

42,0

44,0

46,0

48,0

50,0

52,0

Avg. Govt Employee Member Age

Note: Prosano amalgamation lowered the impact in the 2012 figure

THE IMPACT OF GEMS

Summary

• Governance structures

• The impact of PMBs

• The impact of GEMS

• Brokers

• Risk share models

• Value based services

• Fraud, waste and abuse

BONITAS | HMI36

THANK YOU

BONITAS | HMI37