presentation title here - c.ymcdn.com · colorado charter school policy & facility summit |...

TRANSCRIPT

0Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Economic & Real Estate Update

Presented to The Colorado Leagueof Charter Schools

Bryan FryTJ JohnsonTim Callahan

February 25, 2016

1Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Global Effect

Economic Outlook 2016Market Factors

Source: C&W Research, Kiplinger, IMF

• Election Year 2016• GDP growth over all of 2016 will be 2.5%, up slightly from 2.4% in 2015.• Global growth, currently estimated at 3.1 percent in 2015, is projected at 3.4

percent in 2016 and 3.6 percent in 2017. The pickup in global activity is projected to be more gradual than in the October 2015 World Economic Outlook (WEO), especially in emerging market and developing economies.

• Risks to the global outlook remain tilted to the downside and relate to ongoing adjustments in the global economy: a generalized slowdown in emerging market economies, China’s rebalancing, lower commodity prices, and the gradual exit from extraordinarily accommodative monetary conditions in the United States. If these key challenges are not successfully managed, global growth could be derailed.

• By the end of 2016, the 10-year Treasury bond rate should be 2.6%, versus 1.9% now, with the 30-year mortgage rate at 4.3%, from 3.8%.

2

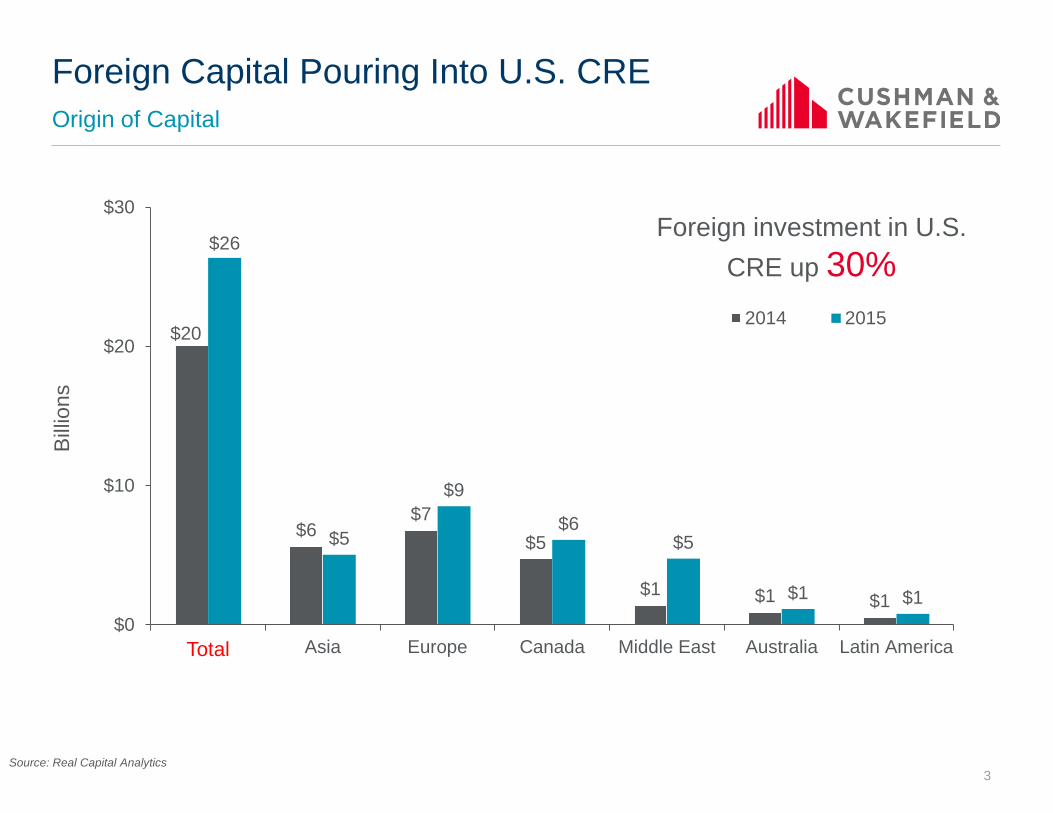

Foreign Capital Pouring Into U.S. CREOrigin of Capital

$20

$6$7

$5

$1 $1 $1

$26

$5

$9

$6$5

$1 $1$0

$10

$20

$30

Total Asia Europe Canada Middle East Australia Latin America

2014 2015

Bill

ions

Foreign investment in U.S. CRE up 30%

Total

Source: Real Capital Analytics3

17%

14%

8%

10%

7% 7%6%

5%4% 4% 4% 3% 3% 2% 2% 2% 2% 1%

0% 0%

-1%-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Investors Are Drawn to the U.S. FundamentalsOffice Rent Growth: U.S. Markets vs. Other Cities Around the World

Source: CW Research, Costar 4

5Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Local Economic Drivers

6

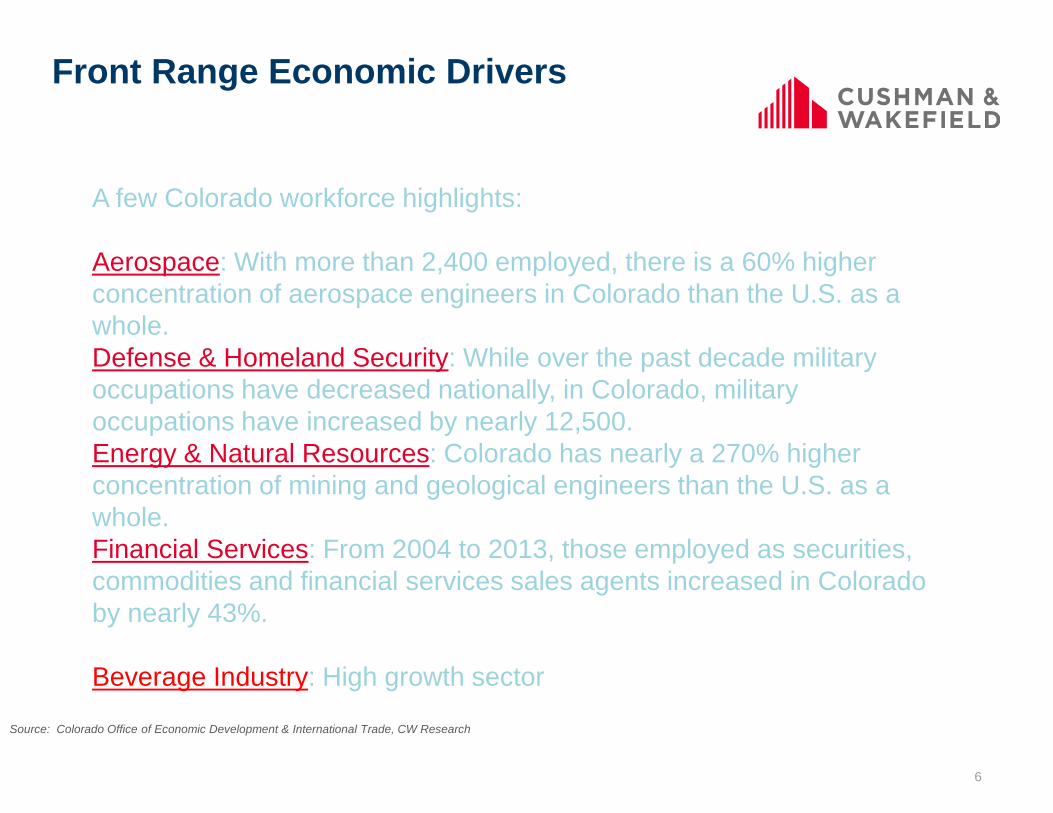

Front Range Economic Drivers

Source: Colorado Office of Economic Development & International Trade, CW Research

A few Colorado workforce highlights:

Aerospace: With more than 2,400 employed, there is a 60% higher concentration of aerospace engineers in Colorado than the U.S. as a whole.Defense & Homeland Security: While over the past decade military occupations have decreased nationally, in Colorado, military occupations have increased by nearly 12,500.Energy & Natural Resources: Colorado has nearly a 270% higher concentration of mining and geological engineers than the U.S. as a whole.Financial Services: From 2004 to 2013, those employed as securities, commodities and financial services sales agents increased in Colorado by nearly 43%.

Beverage Industry: High growth sector

7

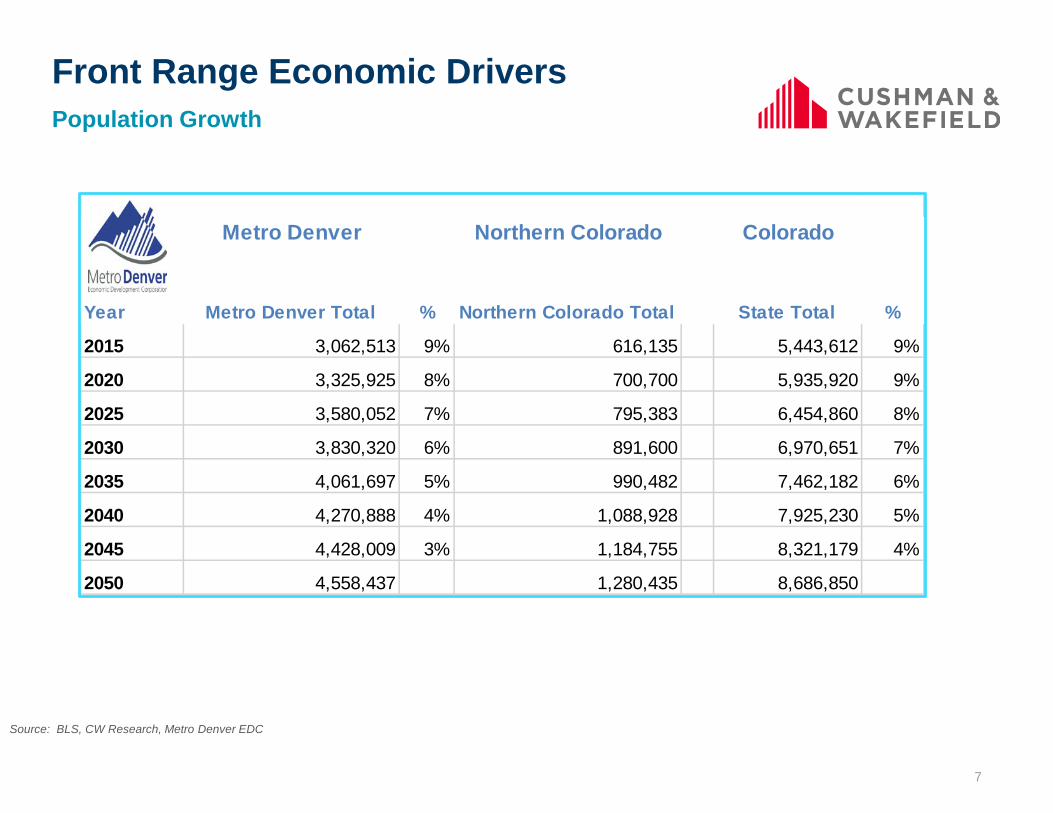

Front Range Economic DriversPopulation Growth

Source: BLS, CW Research, Metro Denver EDC

Colorado

Year Metro Denver Total % Northern Colorado Total State Total %

2015 3,062,513 9% 616,135 5,443,612 9%

2020 3,325,925 8% 700,700 5,935,920 9%

2025 3,580,052 7% 795,383 6,454,860 8%

2030 3,830,320 6% 891,600 6,970,651 7%

2035 4,061,697 5% 990,482 7,462,182 6%

2040 4,270,888 4% 1,088,928 7,925,230 5%

2045 4,428,009 3% 1,184,755 8,321,179 4%

2050 4,558,437 1,280,435 8,686,850

Metro Denver Northern Colorado

8

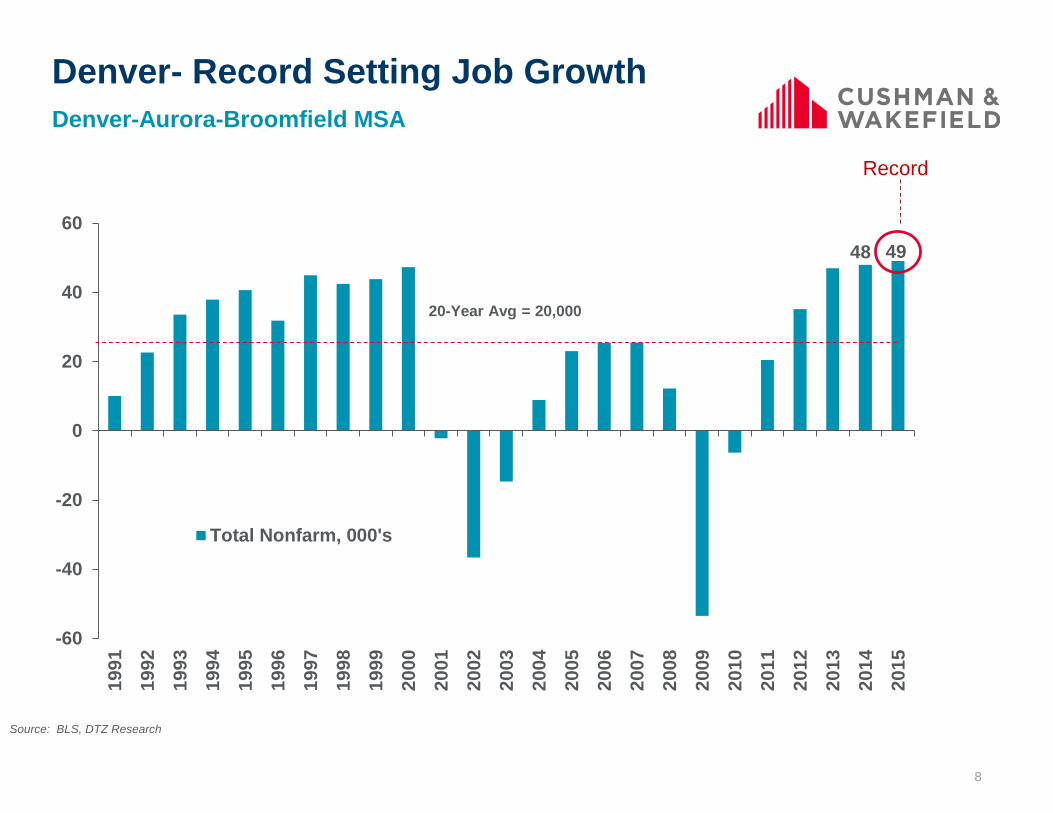

Denver- Record Setting Job GrowthDenver-Aurora-Broomfield MSA

Source: BLS, DTZ Research

48 49

-60

-40

-20

0

20

40

60

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Total Nonfarm, 000's

20-Year Avg = 20,000

Record

9

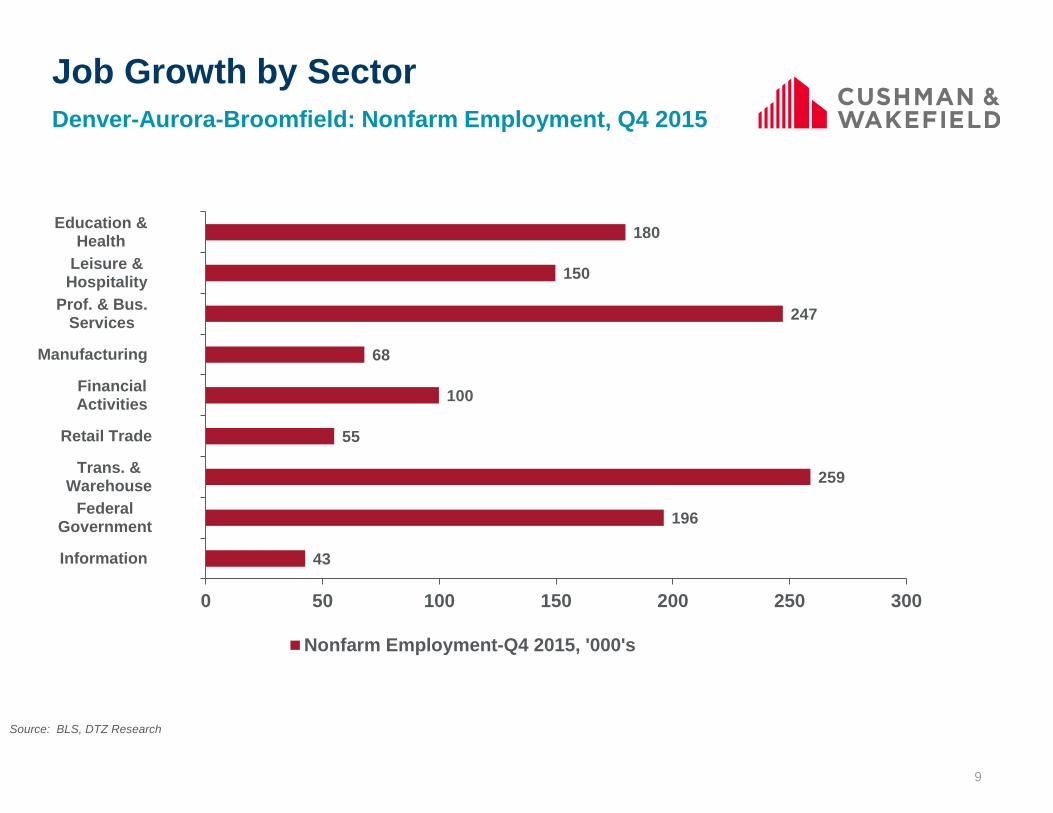

Job Growth by SectorDenver-Aurora-Broomfield: Nonfarm Employment, Q4 2015

43

196

259

55

100

68

247

150

180

0 50 100 150 200 250 300

Information

FederalGovernment

Trans. &Warehouse

Retail Trade

FinancialActivities

Manufacturing

Prof. & Bus.Services

Leisure &Hospitality

Education &Health

Nonfarm Employment-Q4 2015, '000's

Source: BLS, DTZ Research

10

Denver – Recent Employment Trends

1320

1330

1340

1350

1360

1370

1380

1390

1400

1410

Jul 2

014

Aug

201

4Se

p 20

14O

ct 2

014

Nov

201

4D

ec 2

014

Jan

2015

Feb

2015

Mar

201

5A

pr 2

015

May

201

5Ju

n 20

15Ju

l 201

5A

ug 2

015

Sep

2015

Oct

201

5N

ov 2

015

Dec

201

5

Total Nonfarm Employment, 000's

2022242628303234363840424446485052

Y/Y Job Growth, 000's

No Let Up in Denver Continued Growth in 2015

Oil prices began to fall here

36,825 pace in 2015

Source: BLS, DTZ Research

11

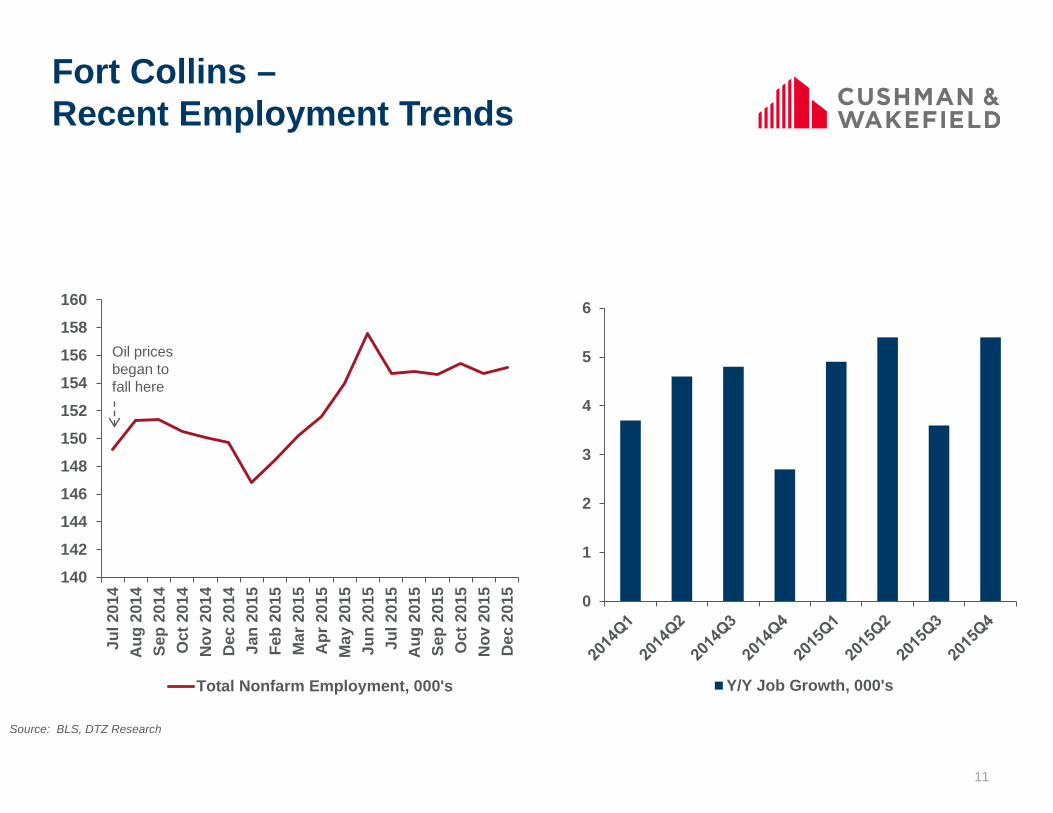

Fort Collins –Recent Employment Trends

140142144146148150152154156158160

Jul 2

014

Aug

201

4Se

p 20

14O

ct 2

014

Nov

201

4D

ec 2

014

Jan

2015

Feb

2015

Mar

201

5A

pr 2

015

May

201

5Ju

n 20

15Ju

l 201

5A

ug 2

015

Sep

2015

Oct

201

5N

ov 2

015

Dec

201

5

Total Nonfarm Employment, 000's

0

1

2

3

4

5

6

Y/Y Job Growth, 000's

Oil prices began to fall here

Source: BLS, DTZ Research

12

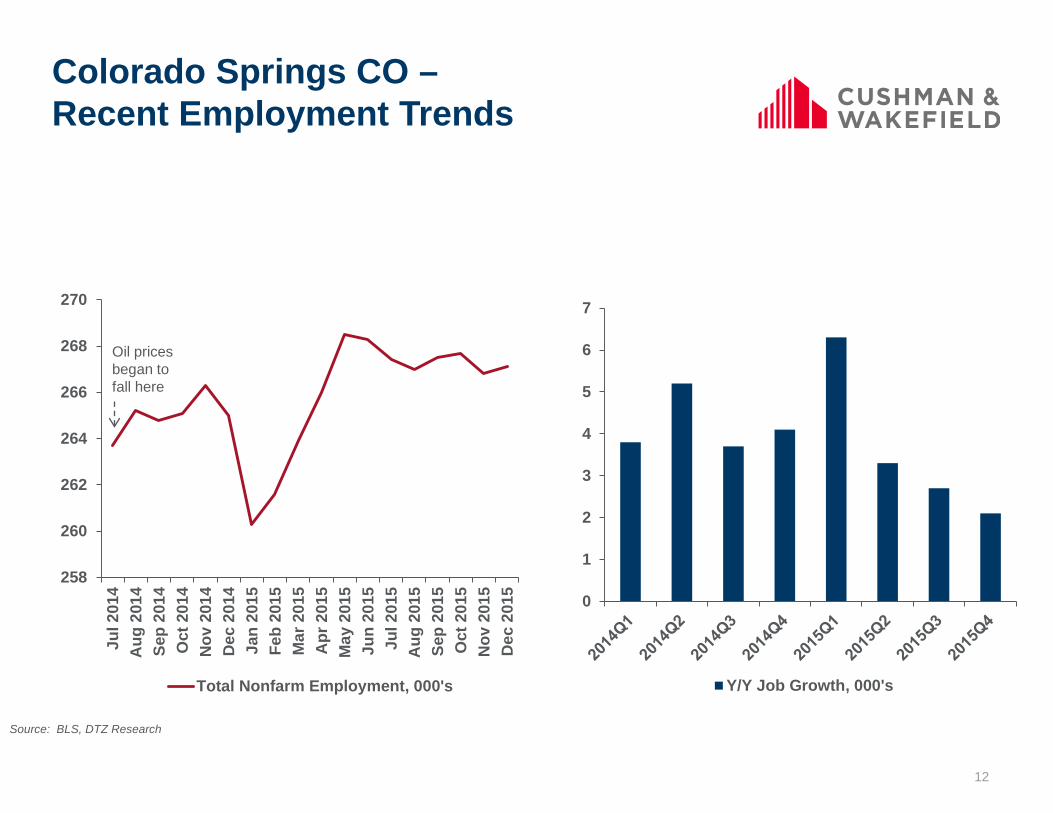

Colorado Springs CO –Recent Employment Trends

258

260

262

264

266

268

270

Jul 2

014

Aug

201

4Se

p 20

14O

ct 2

014

Nov

201

4D

ec 2

014

Jan

2015

Feb

2015

Mar

201

5A

pr 2

015

May

201

5Ju

n 20

15Ju

l 201

5A

ug 2

015

Sep

2015

Oct

201

5N

ov 2

015

Dec

201

5

Total Nonfarm Employment, 000's

0

1

2

3

4

5

6

7

Y/Y Job Growth, 000's

Oil prices began to fall here

Source: BLS, DTZ Research

13Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Denver’s Stunning Growth TrajectoryTotal Nonfarm Employment

855,000

1.39M

2.11M

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

1990 2000 2015 2020 2025 2030

Nearly the size of San Francisco Today (2.2 M)

Source: BLS

14Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Economy & EducationKey Concepts

Employment growth- more households, students in some locations.

Technology & Education integration- incubators

Metro Denver development corridors are light rail centric

How does education fit in the live, work, play development model

Will Millennials remain in urban density after children

How does the limited supply of properties and higher real estate prices impact Charter

School growth opportunities

Gentrification impacting housing prices and shifting enrollment

Source: BLS

15Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Demographics

16Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

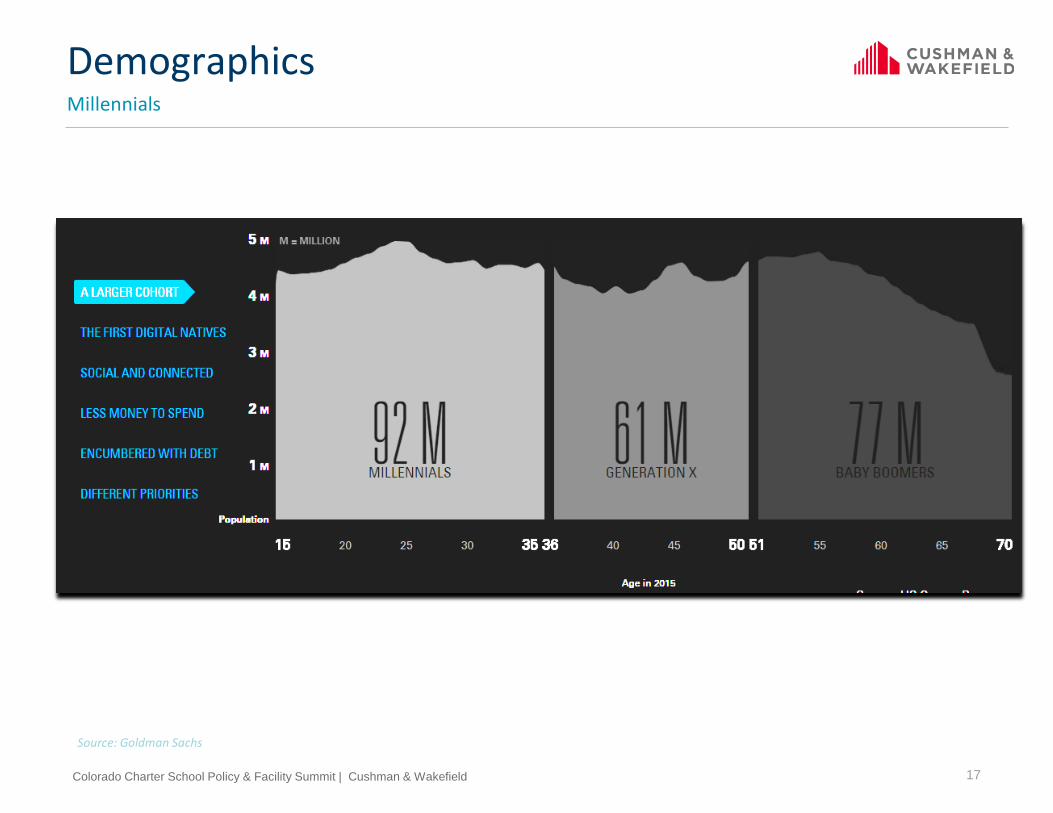

DemographicsMillennials

33% of all adults by 2020

75% of work force by 2025

$1T in US consumer spending

Colorado developers and employers are

adopting the workplace strategy to meet

their needs

Source: Brookings Institute

17Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

DemographicsMillennials

Source: Goldman Sachs

18Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

DemographicsMillennials

Source: Goldman Sachs

19Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

DemographicsMillennials

Source: Goldman Sachs

20Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

DemographicsMillennials

Source: Goldman Sachs

21Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

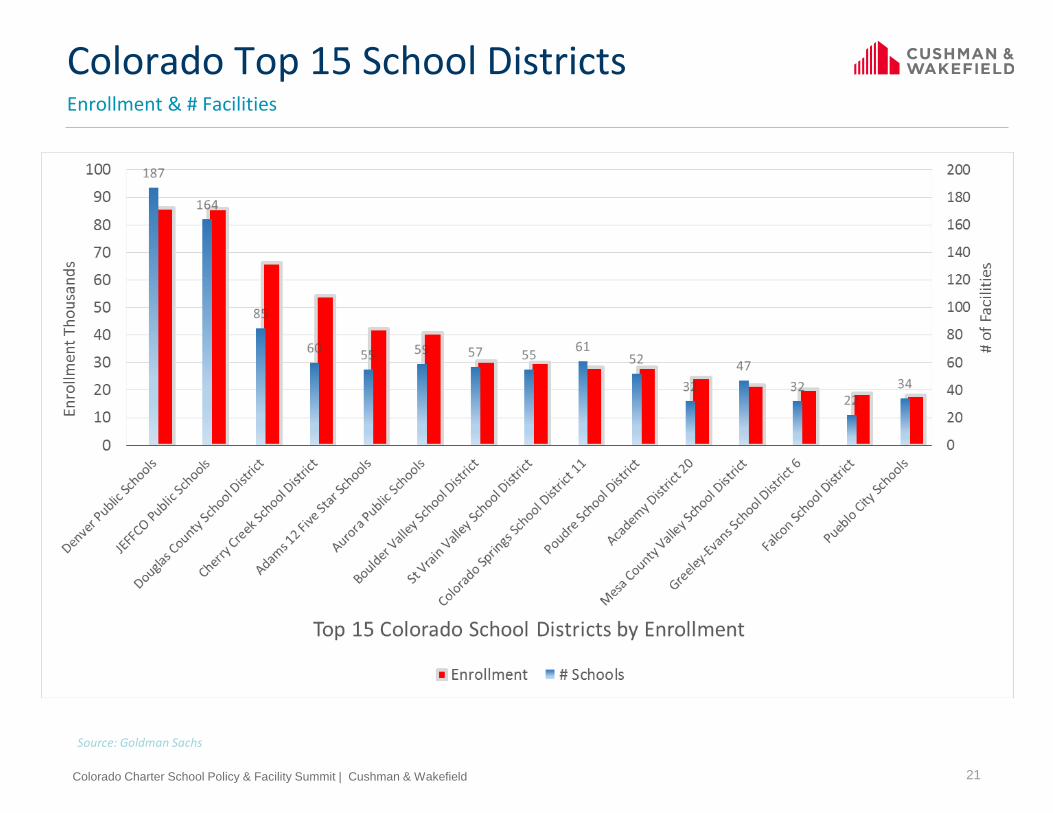

Colorado Top 15 School DistrictsEnrollment & # Facilities

Source: Goldman Sachs

22Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

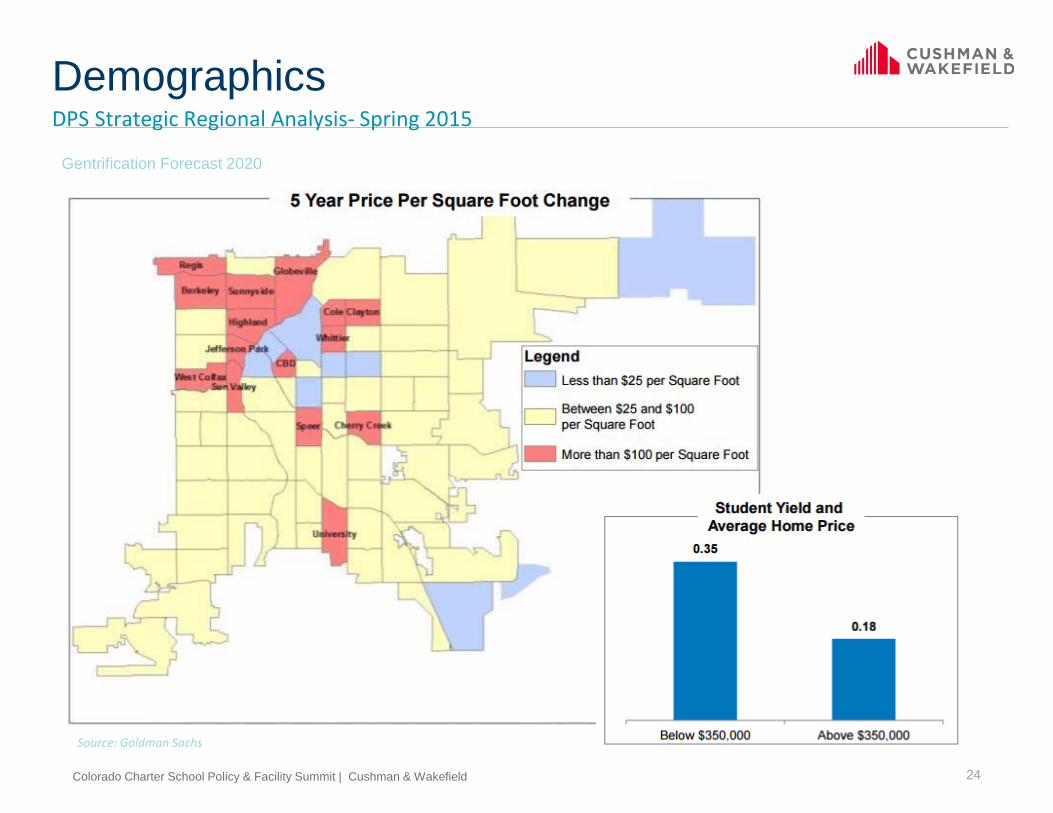

DemographicsDPS Strategic Regional Analysis- Spring 2015

Source: Goldman Sachs

Demographic/Capacity gap: compares the number of DPS students today (and forecast in 5 years) to the number of seats available in the region.

23Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

DemographicsDPS Strategic Regional Analysis- Spring 2015

Source: Goldman Sachs

24Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

DemographicsDPS Strategic Regional Analysis- Spring 2015

Source: Goldman Sachs

Gentrification Forecast 2020

25Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Real Estate Overview

26Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

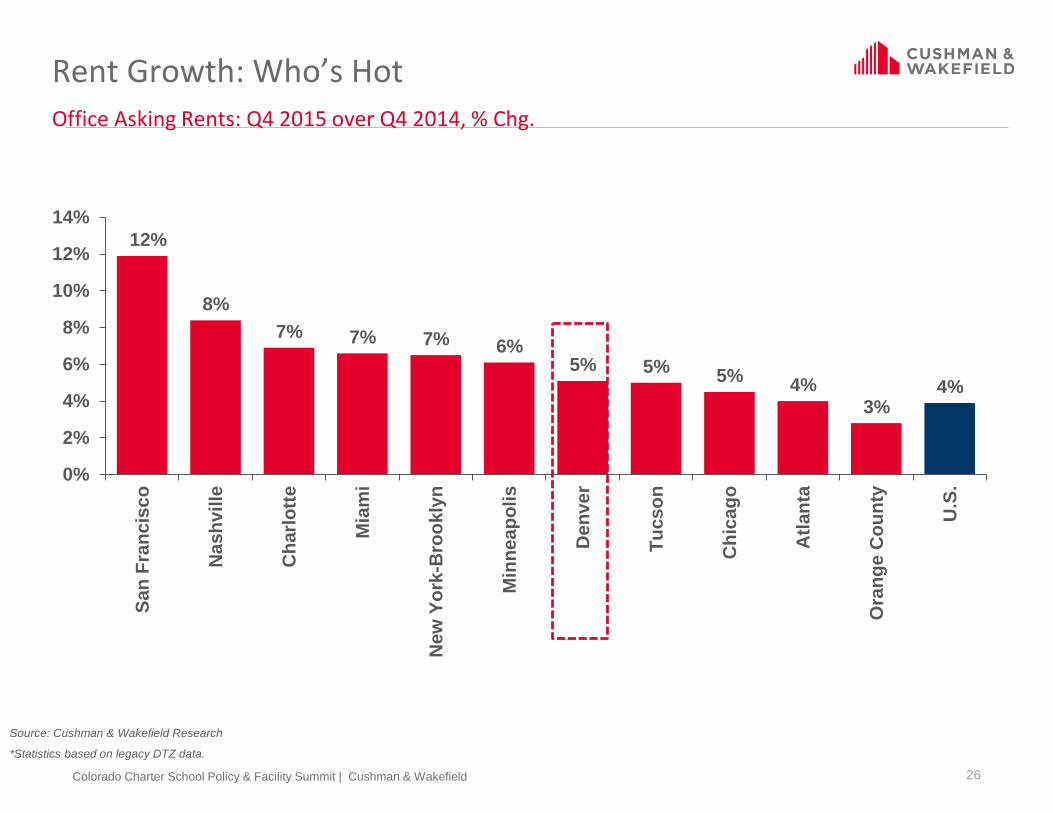

Rent Growth: Who’s HotOffice Asking Rents: Q4 2015 over Q4 2014, % Chg.

Source: Cushman & Wakefield Research

12%

8%7% 7% 7% 6%

5% 5% 5% 4%3%

4%

0%

2%

4%

6%

8%

10%

12%

14%

San

Fran

cisc

o

Nas

hvill

e

Cha

rlotte

Mia

mi

New

Yor

k-B

rook

lyn

Min

neap

olis

Den

ver

Tucs

on

Chi

cago

Atla

nta

Ora

nge

Cou

nty

U.S

.

*Statistics based on legacy DTZ data.

27Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

DemographicsFort Collins

158,600 population

Median Age: 29.5

Median HH Income: $53,780

Diversified Employment Base- Technology, Healthcare, Financial Services, Energy,

Education

Attracting Millennials for jobs and lifestyle

Source: BLS

28Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Ft Collins – Commercial Development UpdateHarmony Technology Park

Being developed by MAVDevelopment

• 105 acre site• Planned for Office, Flex, and Retail spaces

• HTP One• Proposed 70,700 SF office building

• 5042 Technology Place• Existing 50,000 SF flex building, only 9,600 SF currently

available for lease.

• Retail center• 36,000 Sf of retail space expected to deliver late 2015.

29Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

DemographicsMetro Denver

3,000,000 Population

Median Age: 36.6

Median HH Income: $56,514

Diversified Employment Base- Technology, Healthcare, Financial Services, Energy

Attracting Millennials for jobs and lifestyle

Source: BLS

30Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Joint Venture between Continuum Partners and CIM Group• $419 million project

• $47.9 million in tax-increment financing from Denver

• 26 acre site• University of Colorado Health Sciences vacated in 2008

• Proposing 900-1,100 apartment units, for-sale housing, 250,000 SF of retail 125,000 SF of office and a 140-room hotel.

• Will demolish all existing structures except for the historic nurses dormitory, five-story bridge and parking structure• Dormitory will be converted to apartments and the bridge

will become the Hotel.

• 1st phase scheduled to open late Summer 2017• 600 apartment units and ground floor retail.

Denver- Commercial Development Update9th & Colorado Blvd. Redevelopment

31Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Denver- Commercial Development UpdateUnion Station

OFFICE• Six Buildings built since 2009 (Five completed

since 2014)

• 697,938 square feet

• Two Buildings under construction

• 148,808 square feet

• One Building planned

• 418,790 square feet

RETAIL

• 149,440 square feet of newly constructed retail since 2012.

• King Soopers, Twelve new restaurants in and around Union Station

• 70,238 square feet under construction

• Whole Foods

• As of now, aware of another 19,429 square feet that is planned.

RESIDENTIAL• Four Buildings built since 2013

• 1,098 units

• Two Buildings under construction

• 740 units

• One Building planned

• 618 units

HOSPITALITY

• Crawford Hotel (opened July 2014)

• 112 Rooms

• Kimpton Hotel (expected to deliver April 2016)

• 200 Rooms

• Hotel Indigo (expected to deliver October 2016)

• 203 Rooms

• Hilton Garden Inn (proposed)

• 200 Rooms

32Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

DemographicsColorado Springs

600,000 population

Median Age 35.2

Median HH Income $55,650

Government –DoD driven employment base

93% High School Graduation Rate- National Average 86%

Source: BLS

33Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Colorado Springs Development

Collection of Four Venues that are expected to attract 1,000,000 new visitors each year, create 300 construction jobs, thousands of new retail jobs and $10 million in additional tax revenues.

UNITED STATES OLYMPIC MUSEUM | City for Champions | January 2018 | SW Downtown Urban Renewal Area

COLORADO SPORTS & EVENTS CENTER | City for Champions | TBD | SW Downtown Urban Renewal Area

SPORTS MEDICINE & PERFORMANCE CENTER | City for Champions | Spring 2017 | N Nevada UCCS Campus

• Museum providing highly interactive “Olympic Experience”, highlighting values, historic moments, outstanding athletes and teams, and collective memories of the Olympic & Paralympic games.

• State-of-the-art theater, gift shop, café, and broadcast studio.

• Outdoor multi-use stadium accommodating soccer, rugby, and lacrosse. • Indoor venue with flexible hard-court configuration. • Pre-Olympic and amateur sporting events (Olympic Time Trials, Qualifiers, Playoffs and World Championship events).

• Will be a nationally renowned destination for elite athlete clinical, testing, and counseling services and related university research and education.

• Will include a handicapped-accessible track and field facility.

CATALYST CAMPUS | O’Neil/Braxton | Summer 2016 | Pikes Peak & Colorado

• Collaborative work and education environment geared toward bolstering local technology, engineering and manufacturing industries.• Private sector companies (primarily DoD in nature) collaborating with public sector entities to spur workforce development, education and

startups to create long-lasting jobs in the community.

34Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Class B Office Market AnalyticsFort Collins-Loveland-Greeley

35Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

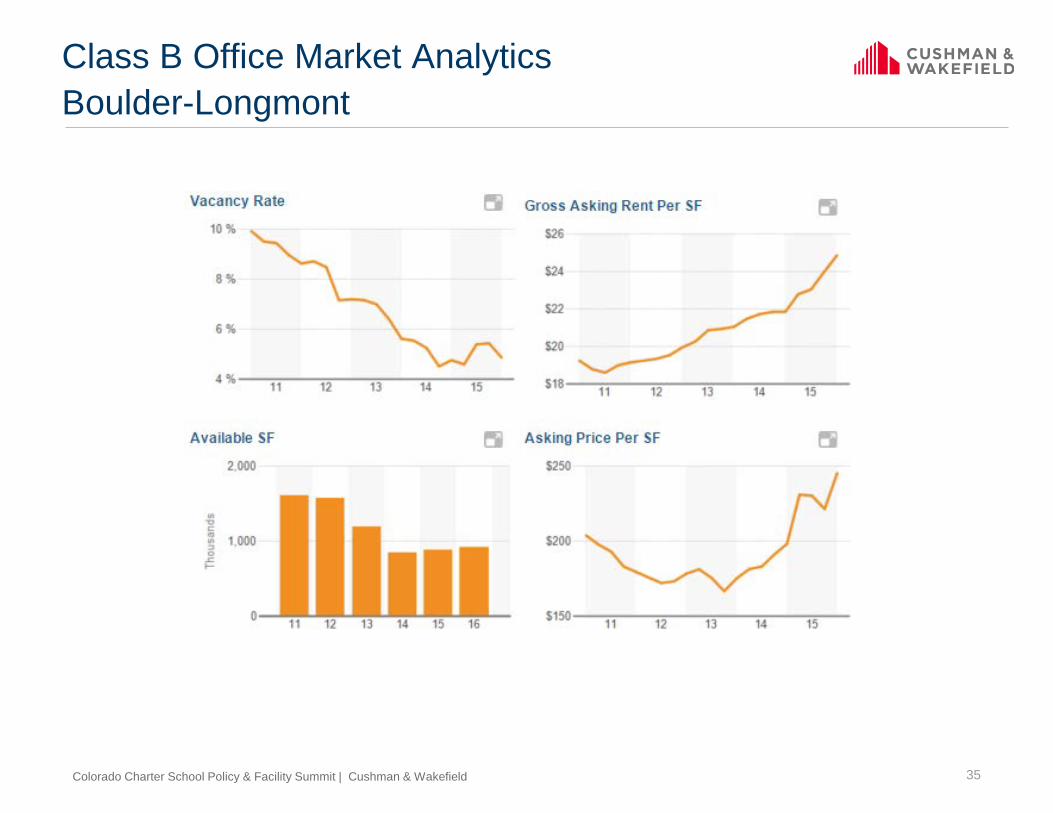

Class B Office Market AnalyticsBoulder-Longmont

36Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Class B Office Market AnalyticsNorth Metro Denver

37Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Class B Office Market AnalyticsDowntown

38Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Class B Office Market AnalyticsSouth Metro Denver

39Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Class B Office Market AnalyticsColorado Springs

40Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Class B Office Market AnalyticsPueblo

41Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Residential GrowthMetro Denver

42Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

1

2

34

5

6

7

8

9

10

RESIDENTIAL GROWTH AREAS

1. NW Metro

2. Arvada

3. Parker/ Douglas County

4. Castle Rock

5. SW Metro

6. DIA Corridor

7. SE Aurora

8. East Aurora

9. NE Metro

10. Denver

43Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

NORTHWEST METRO

• Avg. Price Pt. for New Home:$548,803

• # of New Units: 356

• Avg. Price Point for Existing Homes: $453,956

**

*ANTHEM

COAL CREEK VILLAGES

FLATIRON MEADOWS

44Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

** *

ARVADA

• Avg. Price Pt. for New Home: $509,355

• # of New Units: 477

• Avg. Price Pt. for Existing Homes: $343,664

**

*CANDELAS

LEYDEN ROCK

WHISPER CREEK

45Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

*** *

PARKER / DOUGLAS COUNTY

• Avg. Price Pt. for New Home: $467,232

• # of New Units: 593

• Avg. Price Pt. for Existing Homes: $378,462

SIERRA RIDGE

RIDGEGATE

MERIDIAN VILLAGE

46Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

*

**

*

CASTLE ROCK

• Avg. Price Pt. for New Home: $459,291

• # of New Units: 595

• Avg. Price Pt. for Existing Homes: $411,824

MEADOWS

TERRAIN

CRYSTAL VALLEY RANCH

47Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

*

**

SOUTHWEST METRO

• Avg. Price Pt. for New Home: $579,428

• # of New Units: 180

• Avg. Price Pt. for Existing Homes: $325,257

SOLTERRA

LYONS RIDGE

48Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

* *

*

DIA CORRIDOR

• Avg. Price Pt. for New Home: $330,783

• # of New Units: 43

• Avg. Price Pt. for Existing Homes: $270,402

GREEN VALLEY RANCH

DENVER CONNECTION

HIGHPOINTE

49Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

*

*

*

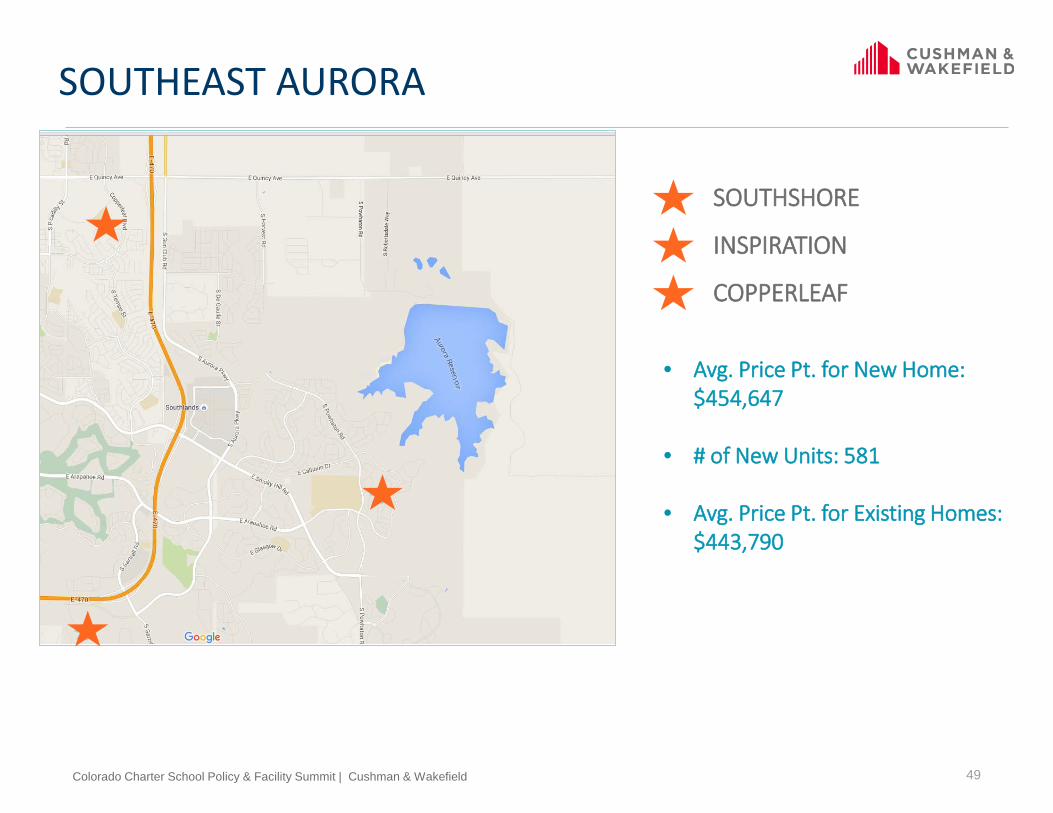

SOUTHEAST AURORA

• Avg. Price Pt. for New Home: $454,647

• # of New Units: 581

• Avg. Price Pt. for Existing Homes: $443,790

SOUTHSHORE

INSPIRATION

COPPERLEAF

50Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

** *

*

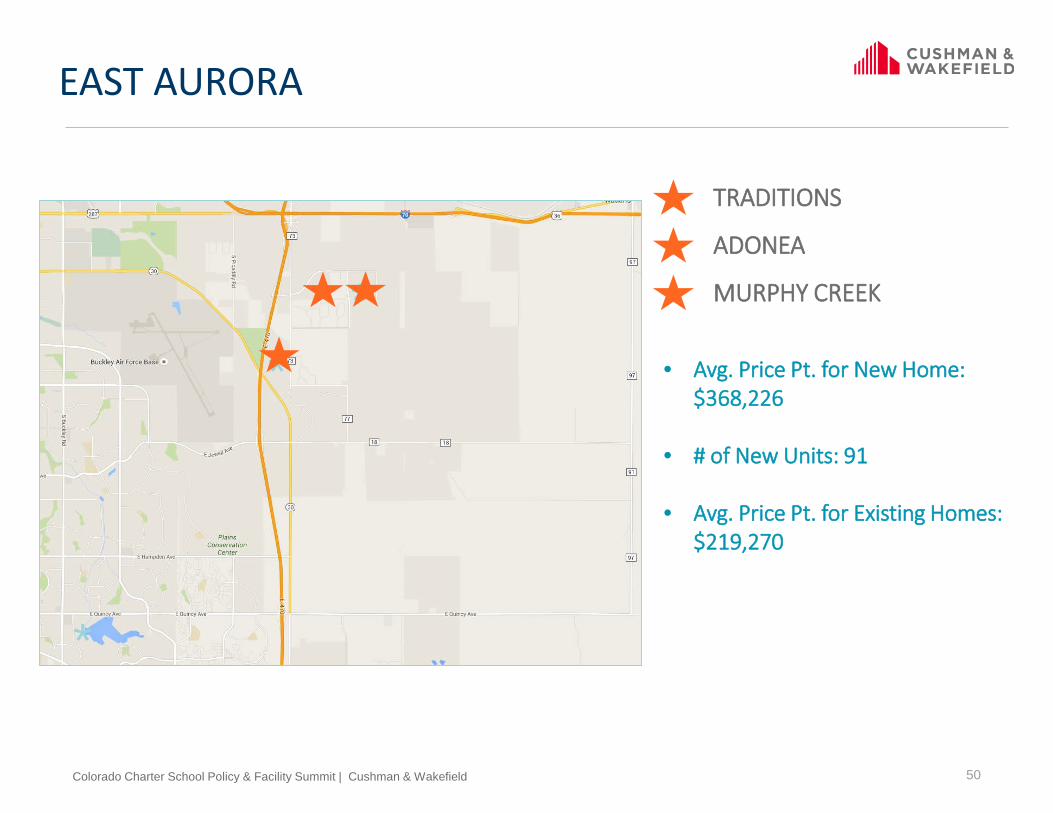

EAST AURORA

• Avg. Price Pt. for New Home: $368,226

• # of New Units: 91

• Avg. Price Pt. for Existing Homes: $219,270

TRADITIONS

ADONEA

MURPHY CREEK

51Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

**

**

*

NORTHEAST AURORA

• Avg. Price Pt. for New Home: $339,393

• # of New Units: 134

• Avg. Price Pt. for Existing Homes: $285,532

REUNION

BRANTNER

BUFFALO RUN

52Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

*

DENVER

• Avg. Price Pt. for New Home: $552,100

• # of New Units: 318

• Avg. Price Pt. for Existing Homes: $479,056

STAPLETON

BOULEVARD ONE

SLOAN’S LAKE

53Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Demographic Trends

Who is moving here?

Why are they

moving?

What does the

future hold?

54Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

Residential Trends

Branding Within

Communities

Density

Home Prices

55Colorado Charter School Policy & Facility Summit | Cushman & Wakefield

cushmanwakefield.com

BRYAN FRY

+1 303 312 4221

TJ JOHNSON

+1 303 312 4222

© 2015

Cushman & Wakefield makes no guarantee, warranty, or representation about information contained herein which is subject to errors, and omissions, and change without notice. It is your responsibility to independently confirm its accuracyand completeness.The information contained herein shall not be used with the consent of Cushman & Wakefield

TIM CALLAHAN

+1 303 312 4216