presentation on intra-state availability based tariff (abt)sldcguj.com/compdoc/ea meeting.pdf ·...

TRANSCRIPT

Presentation on

Intra-State Availability Based Tariff (ABT)

6th Energy Accounting Meeting

Date : 8th September’2008

Presentation By State Load Dispatch CentreGujarat Energy Transmission Corporation Ltd.

INTRA-STATE ABT IN INDIA

• Successful implementation of ABT at Inter-State level

continue since more than six years

Gujarat was first State to issue regulation of Intra-State ABT ( issued on 11th August’2006)

Benefit of Intra State ABT recognized in NEP and accordingly all State has initiated process for implementation.

Delhi has successfully implemented Intra-State ABT from 1st September’2007. Methodology is similar to Gujarat.

SLDC/STU is Nodal agency for implementation of Intra State ABT. Mock exercise of scheduling and accounting

and continued for more than 22 months.

Amount of more than 20,000 crore successfully settled

under Inter-State ABT mechanism by the end of year

2007.

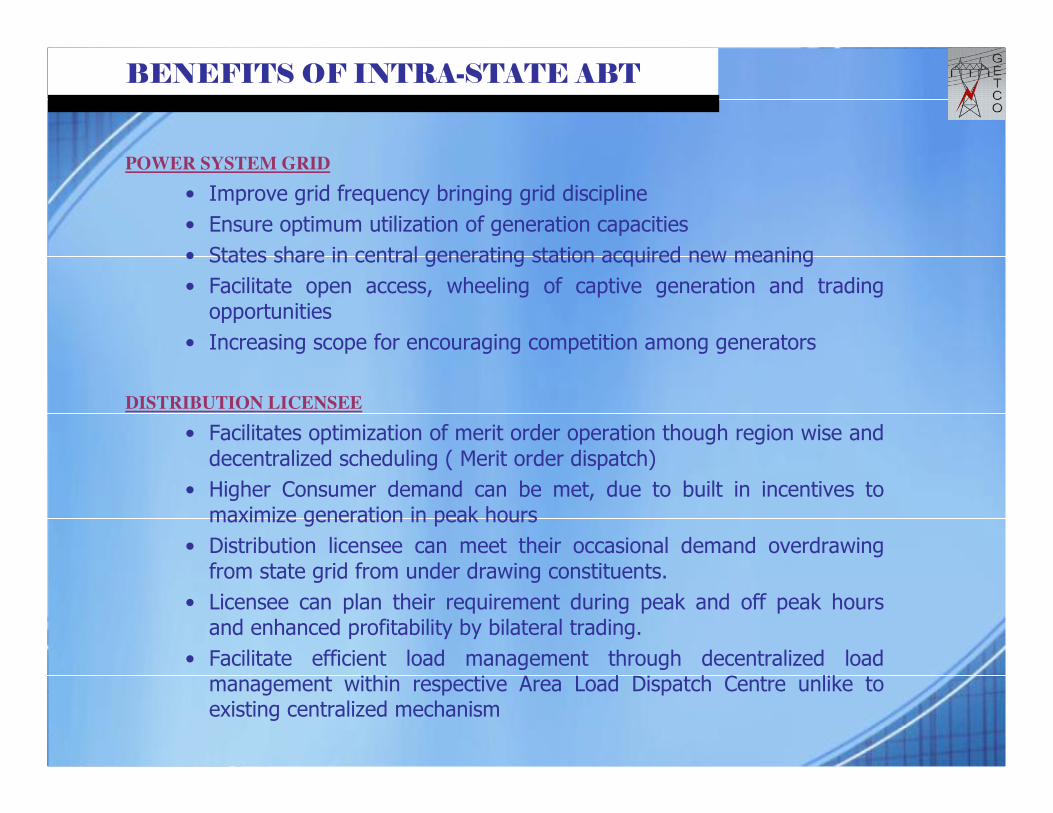

POWER SYSTEM GRID

• Improve grid frequency bringing grid discipline

• Ensure optimum utilization of generation capacities

• States share in central generating station acquired new meaning

• Facilitate open access, wheeling of captive generation and trading opportunities

• Increasing scope for encouraging competition among generators

DISTRIBUTION LICENSEE

• Facilitates optimization of merit order operation though region wise and decentralized scheduling ( Merit order dispatch)

• Higher Consumer demand can be met, due to built in incentives tomaximize generation in peak hours

• Distribution licensee can meet their occasional demand overdrawing from state grid from under drawing constituents.

• Licensee can plan their requirement during peak and off peak hours and enhanced profitability by bilateral trading.

• Facilitate efficient load management through decentralized load management within respective Area Load Dispatch Centre unlike toexisting centralized mechanism

BENEFITS OF INTRA-STATE ABT

BENEFITS TO GENERATOR

• Generation during peak hours encouraged through effective frequency linked incentives and discourages during off peak hours.

• Hydro electric generation is being harnessed more optimally

• Provide flexibility in scheduling by day ahead and same day availability declaration and making revision to accommodate variation in production

• Provide proper recovery of fixed and variable charges as it is based on scheduling under ABT mechanism

• Generators can pay back for extra generation through weekly settlement of UI charges unlike to existing monthly billing system

END USER OR OA USERS

• Facilitate open access to end users provide scope for trading orpurchasing power from third party

• Accommodate wheeling by captive generating plant and provide flexibility to declare by captive generator and revised requisition by OA users

• Ensure quality and reliability of power supply to end users.

• Reduction in cost of power as distribution licensee can reduce their purchase cost by optimization of merit order dispatch

BENEFITS OF INTRA-STATE ABT

– Responsible for implementation of Intra State ABT as a “Nodal Agency” coordinating various activities

– Responsible for scheduling of all Intra State generators and coordinating with RLDC for scheduling of central generating station from State

– Checking that there is no gaming in its availability declaration,

– Revision of availability declaration and injection schedule for dispatching by State generators

– Metering and energy accounting for measurement of energy exchanges through State grid

– Issuance of UI accounts as per commercial mechanism to all intra State UI members and settlement of UI & REC payment for exchange through regional grid

– Collections/disbursement of UI payments within intra state entities and settlement with regional pool account

– Responsible for reporting to Hon’ble commission regarding observance of grid code, mock trial of ABT and relevant grid performance.

ROLE OF SLDC/STU

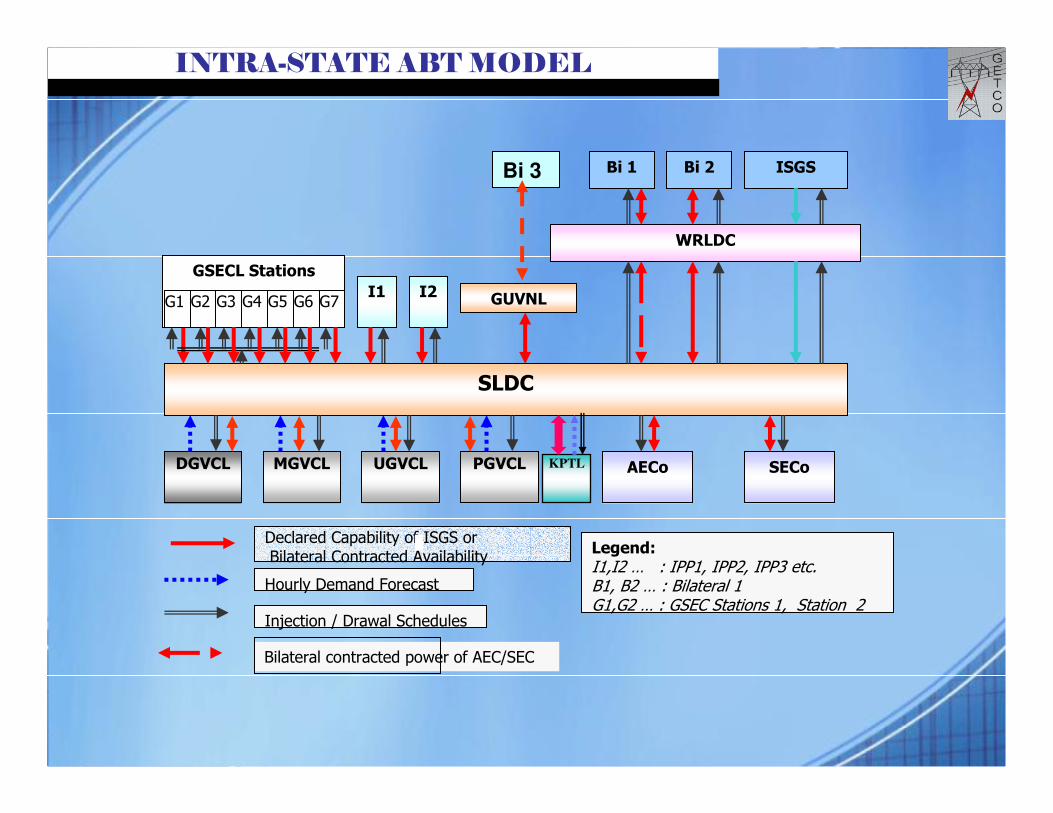

GSECL Stations

I1 I2

DGVCL MGVCL UGVCL PGVCL

SLDC

AECo SECo

Declared Capability of ISGS orBilateral Contracted Availability

Hourly Demand Forecast

Legend:I1,I2 … : IPP1, IPP2, IPP3 etc.B1, B2 … : Bilateral 1G1,G2 … : GSEC Stations 1, Station 2

Injection / Drawal Schedules

G1 G2 G3 G4 G5 G6 G7

Bilateral contracted power of AEC/SEC

ISGS

WRLDC

Bi 2Bi 1

GUVNL

Bi 3

KPTL

INTRA-STATE ABT MODEL

GSECL StationsI1 I2

DGVCL MGVCL UGVCL PGVCL

SLDC

AECo SECo

Declared Capability of SGS/ISGS orBilateral Contracted Availability

Requisition to SLDC

Legend:I1,I2 … : IPP1, IPP2, IPP3 etc.B1, B2 … : Bilateral 1G1,G2 … : GSEC Stations 1, Station 2

Injection / Drawal Schedules

G1G2G3G4G5G6G7

Bilateral contracted power of distribution licensee

ISGS

WRLDC

Bi 2Bi 1

GUVNL

Bi

3

KPTL

INTRA-STATE ABT MODEL

SLDC

SUGEN MUNDRA

SEZ

Bilateral contracted power to distribution licensee

WRLDC

Bil 1 Bil 2 ISGSMSEB/

MPPTCLBil

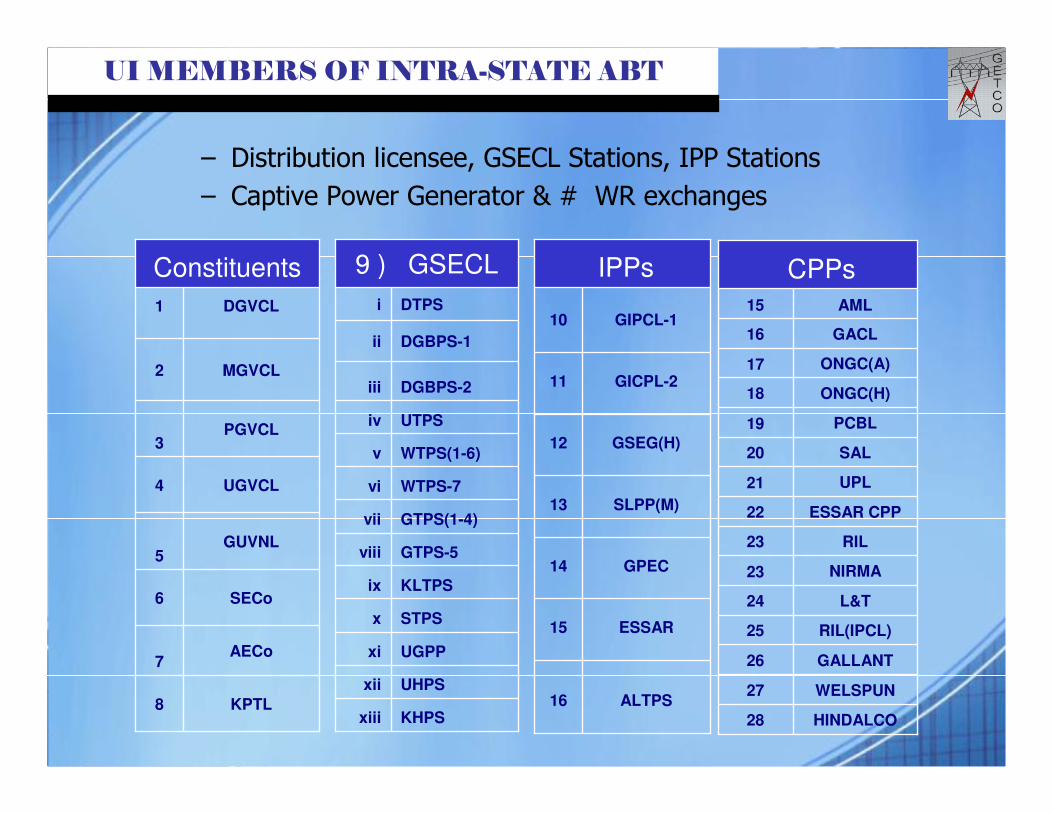

UI MEMBERS OF INTRA-STATE ABT

– Distribution licensee, GSECL Stations, IPP Stations

– Captive Power Generator & # WR exchanges

Constituents

KPTL8

AECo7

SECo6

GUVNL5

UGVCL4

PGVCL3

MGVCL2

DGVCL1

KHPSxiii

UHPSxii

UGPPxi

STPSx

KLTPSix

GTPS-5viii

GTPS(1-4)vii

WTPS-7vi

WTPS(1-6)v

UTPSiv

DGBPS-2iii

DGBPS-1ii

DTPSi

9 ) GSECL

ALTPS 16

ESSAR15

GPEC14

SLPP(M)13

GSEG(H)12

GICPL-211

GIPCL-110

IPPs

HINDALCO28

WELSPUN27

GALLANT 26

RIL(IPCL)25

L&T24

NIRMA23

RIL23

ESSAR CPP22

UPL21

SAL20

PCBL19

ONGC(H)18

ONGC(A)17

GACL16

AML15

CPPs

ALLOCATION OF CAPACITY

– Bilateral Power Purchase agreement signed by distribution licensee with GUVNL and State generating Stations. Accordingly, State generating capacity allocated to distributionlicensee from each station.

– Power from central sector generating station purchased by GUVNL and same has been allocated to distribution licensee.

– Power purchase from CPP by GUVNL is allocated to distribution licensee.

– Power purchase from wind farm by GUVNL is allocated to distribution licensee.

– Bilateral purchase/sale by GUVNL through trading is indicated to respective distribution licensee on day to day basis.

– Captive/private generator wheeling power to more than one users ( GIPCL-1) has submitted allocation for each users.

– Allocation of WEG is derived weekly by GEDA based on energy injection by WEG & wheeling to respective distribution licensee area.

– Allocation is prepared based on consumption pattern. It will changed whenever new capacity addition/modification takes

place and allocation of central generating stations revised.

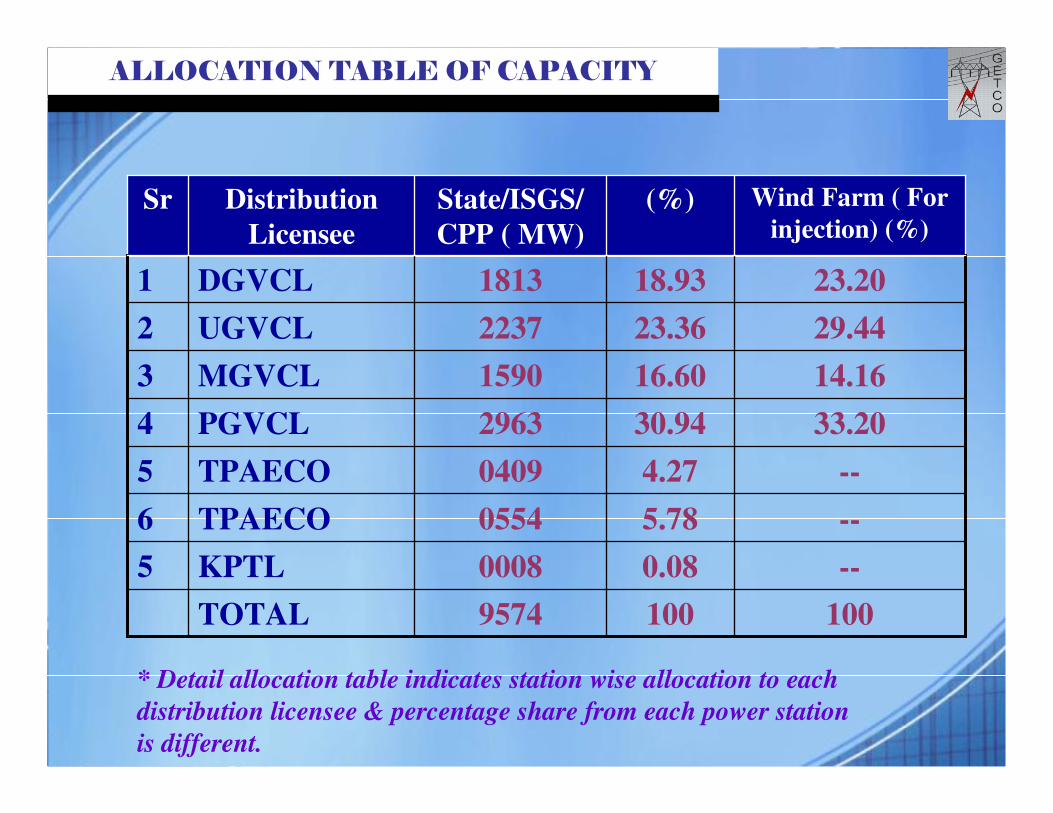

ALLOCATION TABLE OF CAPACITY

--0.080008KPTL5

1001009574TOTAL

5.78

4.27

30.94

16.60

23.36

18.93

(%)

--0409TPAECO5

--0554TPAECO6

2963

1590

2237

1813

State/ISGS/

CPP ( MW)

33.20PGVCL 4

14.16MGVCL3

29.44UGVCL2

23.20DGVCL1

Wind Farm ( For

injection) (%)Distribution

Licensee

Sr

* Detail allocation table indicates station wise allocation to each

distribution licensee & percentage share from each power station

is different.

STEPS TAKEN BY SLDC/STU

– Meter Installation to interface points completed

– Round the clock scheduling activities organized

– Data polling to SLDC on weekly basis

– Energy Accounting on weekly basis organized

– Weekly UI & REC mock bill organized

– Monthly Accounting organized

– Energy Accounting Committee formulated

– Communication for scheduling through website established

– Energy Accounting Meeting conducted

– Report submitted to Hon’ble Commission

– Compliance of directives issued by Hon’ble commission

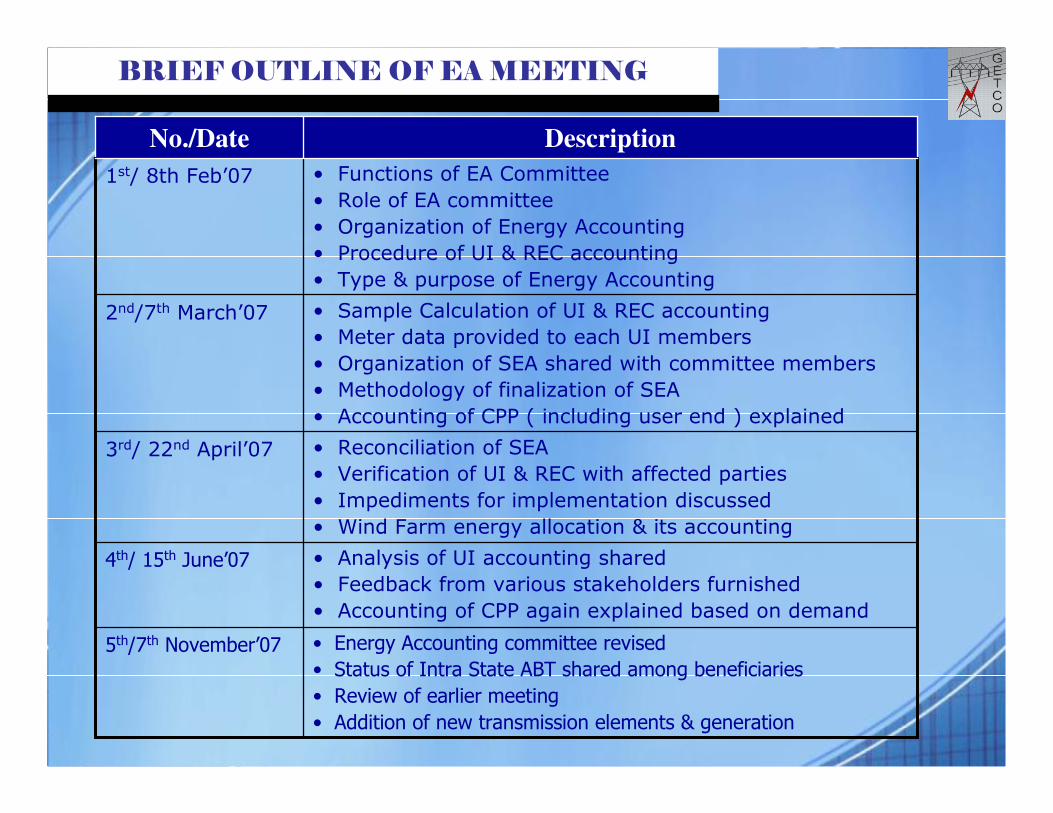

BRIEF OUTLINE OF EA MEETING

• Energy Accounting committee revised

• Status of Intra State ABT shared among beneficiaries

• Review of earlier meeting

• Addition of new transmission elements & generation

5th/7th November’07

• Analysis of UI accounting shared

• Feedback from various stakeholders furnished

• Accounting of CPP again explained based on demand

4th/ 15th June’07

• Reconciliation of SEA

• Verification of UI & REC with affected parties

• Impediments for implementation discussed

• Wind Farm energy allocation & its accounting

3rd/ 22nd April’07

• Sample Calculation of UI & REC accounting

• Meter data provided to each UI members

• Organization of SEA shared with committee members

• Methodology of finalization of SEA

• Accounting of CPP ( including user end ) explained

2nd/7th March’07

• Functions of EA Committee

• Role of EA committee

• Organization of Energy Accounting

• Procedure of UI & REC accounting

• Type & purpose of Energy Accounting

1st/ 8th Feb’07

DescriptionNo./Date

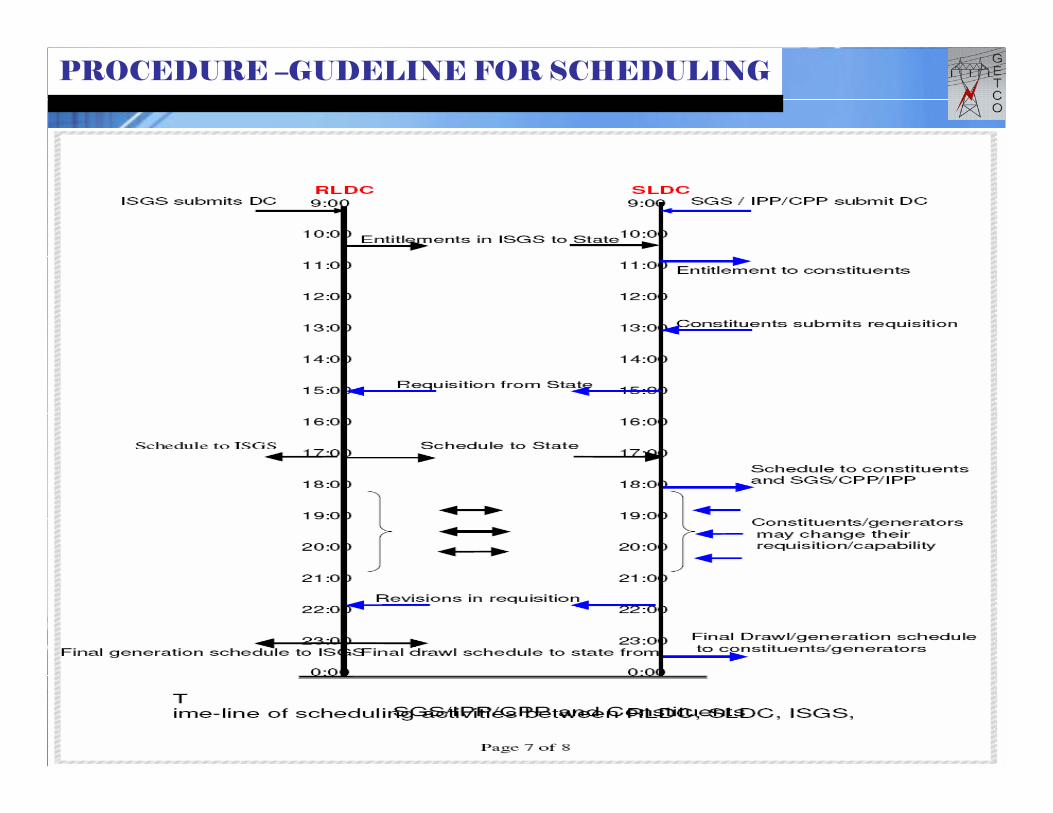

PROCEDURE –FOR SCHEDULING

– Methodology for scheduling and calculating availability is finalized as per provision 26 of regulation issued by GERC and provision 11 of Intra State ABT order.

– Based on allocation, experience of mock exercise and inter state ABT , guidelines for scheduling discussed time to time through various meeting.

– Scheduling process is adopted by SLDC as per state grid code issued by Hon’ble commission.

– IEGS provides that operation of all entities within State would be coordinated by concerned SLDC's , who in turn would coordinate to RLDCs. Accordingly, SLDC will determine by consolidating requirement of distribution licensee from ISGS.

PROCEDURE –GUIDELINE FOR SCHEDULING

1) While submitting availability declaration by generator, they should ensure feasible production in order to avoid from gaming and larger deviation from schedule.

2) While submitting requisition by distribution licensee, distribution licensee has to ensure minimum technical requirement of generator in order to ensure continuity of generating stations.

3) Distribution licensee shall have to plan their requisition to the extent of their entitlement received from respective generating stations and optimization of resources. While requisition, optimization of merit order is to take care of by respective distribution licensee.

4) Generator has to submit their technical minimum level ( with andwithout combined cycle for gas based station ), technical level for oil support for thermal plant as per existing agreement or with consent of respective beneficiaries.

5) Requisition from Nuclear Power Station and hydro power station is concerned, entire availability is to be utilized by distribution licensee at all the times.

PROCEDURE –GUDELINE FOR SCHEDULING

5) Scheduling of hydro power station will be mutually decided by SLDC and

respective hydro power station considering system and irrigationrequirement. There is exception that hydro power resource may beexploited by SLDC as per requirement of grid and schedule prepared by SLDC shall be bounded to respective beneficiaries.

6) Excessive revision by generator and distribution licensee may beavoided by precise forecasting.

7) While submitting requisition for central sector stations ,changes of less than two (2) percent of the previous schedule shall be avoided. [IEGC CLAUSE 6.5(17)]

8) Subsidiaries of GUVNL shall submit their deficit/surplus to GUVNL for bilateral trading. Accordingly, bilateral power is to be indicated by GUVNL to respective distribution licensee.

9) Scheduling of Captive generator wheeling to more than one OA users has to submit allocation for each OA users.

10) It is generally accepted that availability declaration submitted by captive generator as per requirement of OA users ( few CPPs are also indicating same) so that separate requisition from respective OA users is not required. Otherwise, OA users has to submit their requirement through respective distribution licensees.

PROCEDURE –GUDELINE FOR SCHEDULING

PROCEDURE –COMPUTATION OF UI FOR GENERATOR

& DISCOM

UI COMPUTATION OF GENERATOR

Sample Calculation of UI for gas based generating station (GSEG(H))

explained to All participants for understanding various aspects in separate

calculation sheet. Calculation covers computation of UI in each 96 blocks

of one day, corrected Schedule and injection schedule.

Link to Calculation sheet

UI COMPUTATION OF DISCOM

Sample Calculation of UI for distribution licensee explained /discussed to

All participants for understanding various aspects explained to all

participants for understanding various aspects in separate calculation sheet.

Calculation covers computation of UI in each 96 blocks of one day,

corrected Schedule and drawal schedule.

Link to Calculation sheet

PROCEDURE –COMPUTATION OF UI FOR GENERATOR

& DISCOM

UI COMPUTATION OF GSEG(H)

Sample Calculation of UI for gas based generating station (GSEG(H))

explained to All participants for understanding various aspects in separate

calculation sheet. Calculation covers computation of UI in each 96 blocks

of one day, corrected Schedule and injection schedule.

Link to Calculation sheet

UI COMPUTATION OF DISCOM

Sample Calculation of UI for distribution licensee explained /discussed to

all participants for understanding various aspects explained to all

participants for understanding various aspects in separate calculation sheet.

Calculation covers computation of UI in each 96 blocks of one day,

corrected Schedule and drawal schedule.

Link to Calculation sheet

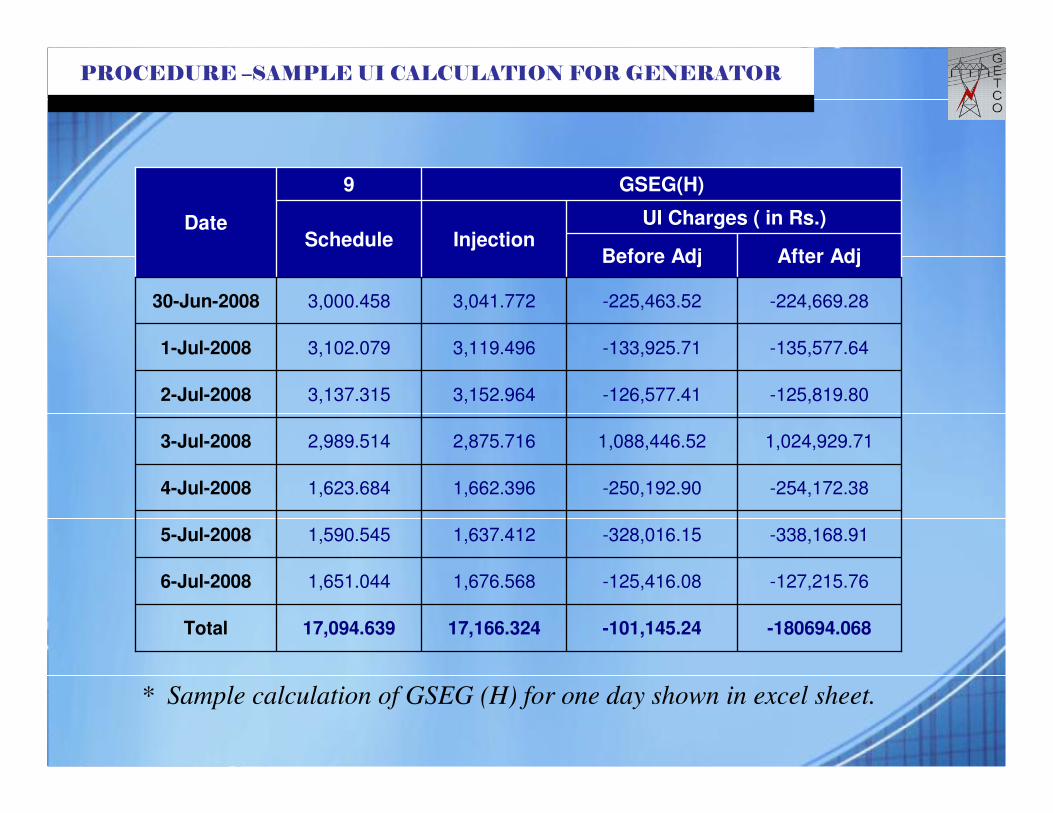

PROCEDURE –SAMPLE UI CALCULATION FOR GENERATOR

-180694.068-101,145.2417,166.32417,094.639Total

-127,215.76-125,416.081,676.5681,651.0446-Jul-2008

-338,168.91-328,016.151,637.4121,590.5455-Jul-2008

-254,172.38-250,192.901,662.3961,623.6844-Jul-2008

1,024,929.711,088,446.522,875.7162,989.5143-Jul-2008

-125,819.80-126,577.413,152.9643,137.3152-Jul-2008

-135,577.64-133,925.713,119.4963,102.0791-Jul-2008

-224,669.28-225,463.523,041.7723,000.45830-Jun-2008

After AdjBefore Adj

UI Charges ( in Rs.)InjectionSchedule

GSEG(H)9

Date

* Sample calculation of GSEG (H) for one day shown in excel sheet.

PROCEDURE –SAMPLE UI CALCULATION FOR GENERATOR

* Sample calculation of MGVCL for one day shown in excel sheet.

-18198712.47-17631889.81116180.284118828.326

-1183058.95-1134887.7814990.49215236.177

6189060.306355554.7815695.22114811.593

16668.55246141.4314869.56714792.853

-9077821.84-8767910.0916166.44417442.337

-11963668.47-12132971.7015906.54917552.270

-2230211.83-2222708.2118562.76418898.157

50319.7724891.7519989.24620094.938

After AdjBefore Adj

UI Charges ( in Rs.)DrawalSchedule

MGVCL2

• According to regulation 15 (i), SLDC has been mandated to maintain pool account reproduced as below :

“State pool accounts for (i) payments regarding unscheduled -interchanges (UI Account) and (ii) reactive energy exchanges (Reactive Energy Account), shall be prepared by the SLDC on a weekly basis and these shall be issued to all constituents by Wednesday of the Week following the next Week for the seven-day period ending on the previous Sunday mid-night.

PROCEDURE –ENERGY ACCOUNTING

• Accounting Methodology comprises preparation of UI Account Bill, Reactive Account Bill and State Energy Account.

1)SLDC will prepare a datum schedule for generator and distribution licensee within three days which will be used for commercial accounting purpose.

2) Computation of net MWH injection of each generating station will be calculated furnishing meter reading on everyweek

3)Computation of net energy drawl of each beneficiary (distribution licensee/open access consumers) will be carried out by furnishing meter reading from each interface points.

4) Generator ( including CPP) having zero schedule i.e. there isno exchange of power with grid, such generator is to consider as consumer of respective distribution licensee during this period. Hence energy drawl by such generator shall be considered as drawal from respective distribution licensee. Net energy drawal/injection between distribution licensee and generator will be changed identifying such blocks.

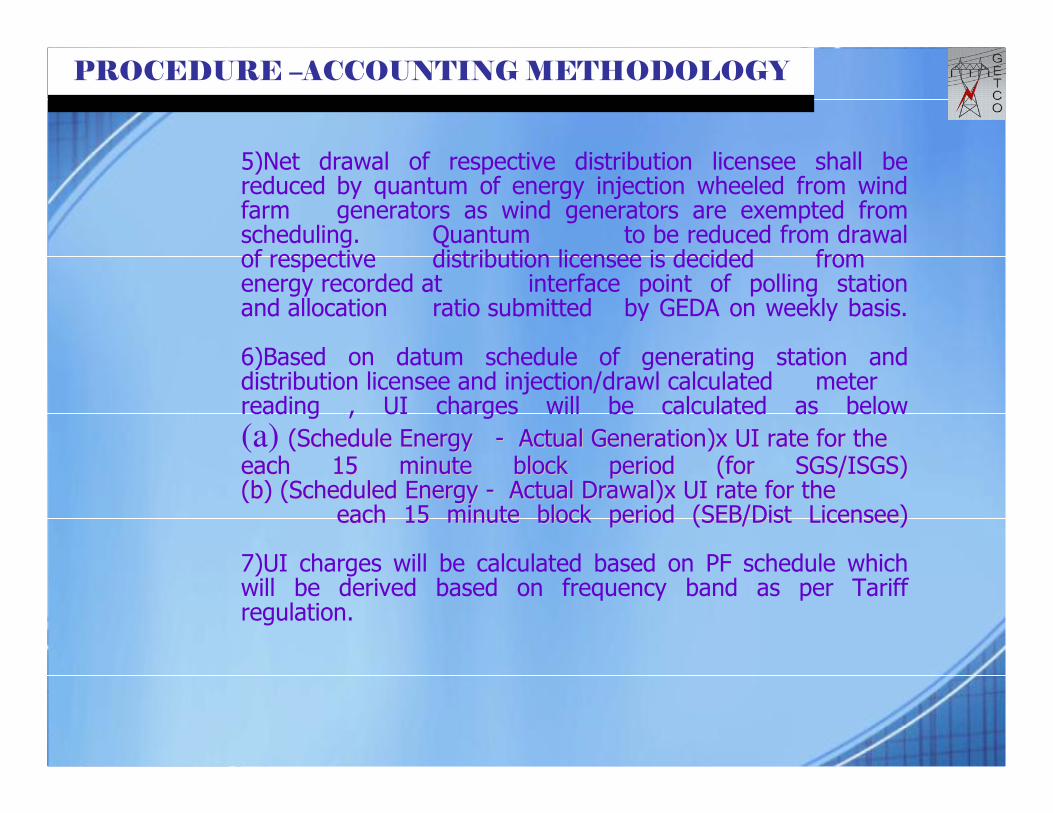

PROCEDURE –ACCOUNTING METHODOLOGY

5)Net drawal of respective distribution licensee shall be reduced by quantum of energy injection wheeled from wind farm generators as wind generators are exempted from scheduling. Quantum to be reduced from drawal of respective distribution licensee is decided from energy recorded at interface point of polling station and allocation ratio submitted by GEDA on weekly basis.

6)Based on datum schedule of generating station and distribution licensee and injection/drawl calculated meter reading , UI charges will be calculated as below

(a) (Schedule Energy (Schedule Energy -- Actual Generation)x UI rate for the Actual Generation)x UI rate for the each 15 minute block period (for SGS/ISGS)each 15 minute block period (for SGS/ISGS)(b) (Scheduled Energy (b) (Scheduled Energy -- Actual Drawal)x UI rate for the Actual Drawal)x UI rate for the

each 15 minute block period (SEB/Dist Licensee)each 15 minute block period (SEB/Dist Licensee)

7)UI charges will be calculated based on PF schedule which will be derived based on frequency band as per Tariff regulation.

PROCEDURE –ACCOUNTING METHODOLOGY

8) After deriving UI charges of intra state generator/distribution licensee, we import data from WRPC for energy exchanged among inter state periphery. The UI charges payable by Gujarat, will be accommodated within Intra State Account against WR.

9) Accommodating actual UI charges of WR, Zero balancing methodology is applied for nullifying UI charges differences between payables and receivables. Provision 16 (l) of Intra State ABT order provides same reproduced as below :

“16(l) If total payment receivables in the UI pool account is more or less than UI payable ,then UI payables/receivables will be suitably adjusted to make payable and receivables amounts equal.”

SLDC has adopted averaging methods as adopted at Inter State level for zero balancing of pool account.

10) Weekly Statement comprises schedule which is actually been used for UI computation ( i.e. Post-facto schedule after applying frequency correction) and actual drawl.

PROCEDURE –ACCOUNTING METHODOLOGY

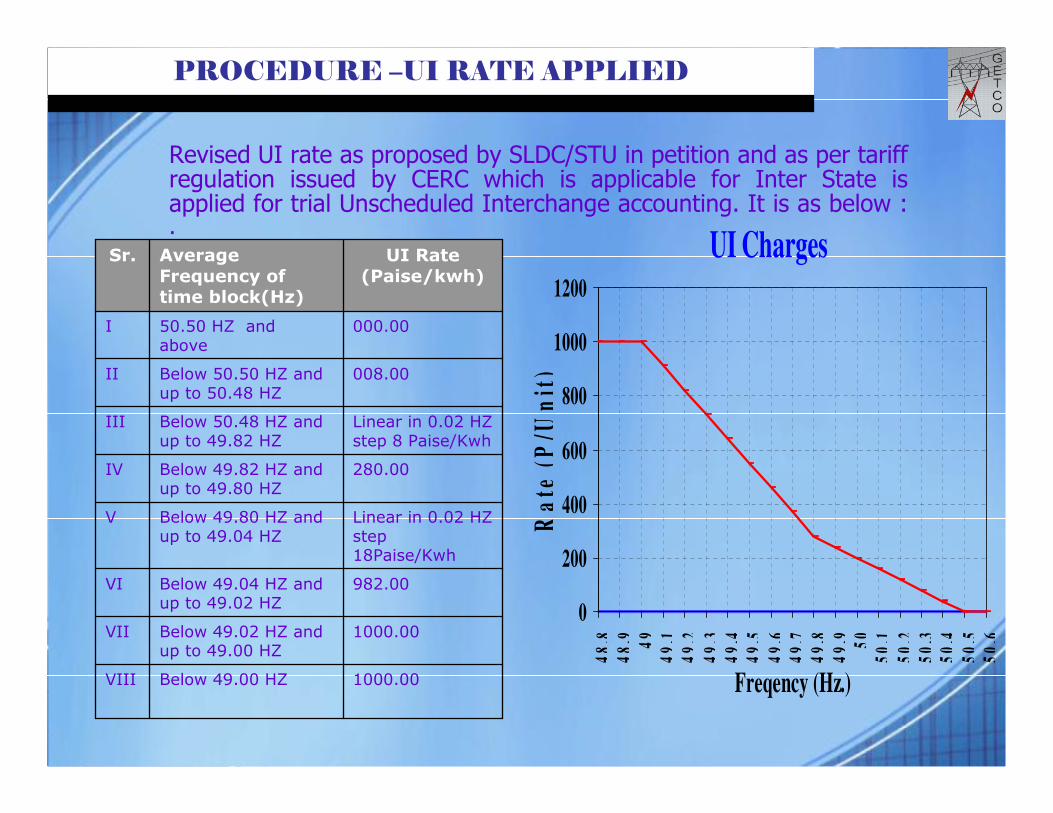

Revised UI rate as proposed by SLDC/STU in petition and as per tariff regulation issued by CERC which is applicable for Inter State isapplied for trial Unscheduled Interchange accounting. It is as below : .

PROCEDURE –UI RATE APPLIED

1000.00Below 49.00 HZ VIII

1000.00Below 49.02 HZ and up to 49.00 HZ

VII

982.00Below 49.04 HZ and up to 49.02 HZ

VI

Linear in 0.02 HZ step 18Paise/Kwh

Below 49.80 HZ and up to 49.04 HZ

V

280.00Below 49.82 HZ and up to 49.80 HZ

IV

Linear in 0.02 HZ step 8 Paise/Kwh

Below 50.48 HZ and up to 49.82 HZ

III

008.00Below 50.50 HZ and up to 50.48 HZ

II

000.0050.50 HZ and above

I

UI Rate

(Paise/kwh)

Average

Frequency of time block(Hz)

Sr. UI Charges

0

200

400

600

800

1000

1200

48

. 84

8.9 49

49

.14

9.2

49

.34

9.4

49

.54

9.6

49

.74

9.8

49

.9 50

50

.15

0.2

50

.35

0.4

50

.55

0.6

Freqency (Hz.)

Ra

te (

P/U

nit

)

PROCEDURE –ZERO BALANCING MECHANISM AT REGIONAL LEVEL

-6199.56314-5633.919566199.833116688.67745TOTAL

-47.80352-47.80352ER

637.00774637.00774SR

-2057.81725-2057.81725NR

-16.13323-14.40273BHAHVDC

-2.76137-2.48441VIN HVDC

778.43583860.12714JINDAL

-52.09671-39.49384SIPAT

-107.51918-95.22783GGPP

24.3101433.99185KGPP

-56.54482-49.68665VSTPS-3

-87.45112-76.31346VSTPS-2

-105.83845-88.81875VSTPS-1

-216.22177-192.44432KSTPS

1670.462341816.52732DNH

584.52101632.10962DD

195.66496222.73445GOA

-490.31796-329.25687MSEDCL

-2223.54207-2028.94375CSEB

-735.51569-611.22618MPPTCL

2309.431092486.17933GUVNL

Adj-RecRecAdj-PayPay

for week 30/6 to 6/7

UI Account of WRLDC

Simple Case study

Of regional pool

Account for week

23/6 to 29/6/08 ;

To explain

Zero-balancing

Methodology

Followed at

Inter State level

Methodology

• UI amount is drawn for all UI members on actual basis.

• UI pool account shall be separated for each receivable and payable members, so that total receivable and payable can be sum up separately.

• Difference in UI receivables and Payables exist because UI for generator drawn at ex-bus periphery and UI for distribution licensee drawn at respective periphery of distribution licensee based on estimation of losses. Since estimated losses applied on uniform basis

which is practically not uniform in network.

• According to regulation of GERC ( provision 16(l)), UI pool account shall be adjusted to zero balance by nullifying difference. SLDC is mandated to devise suitable methodology for same.

• At regional level, difference of UI receivable and payable is adjusted by averaging method i.e. payable and receivable are adjusted to average value ( 50:50 percentage). However, inter regional account remain unadjusted and difference due to this is shared among other beneficiaries.

PROCEDURE –ZERO BALANCING MECHANISM

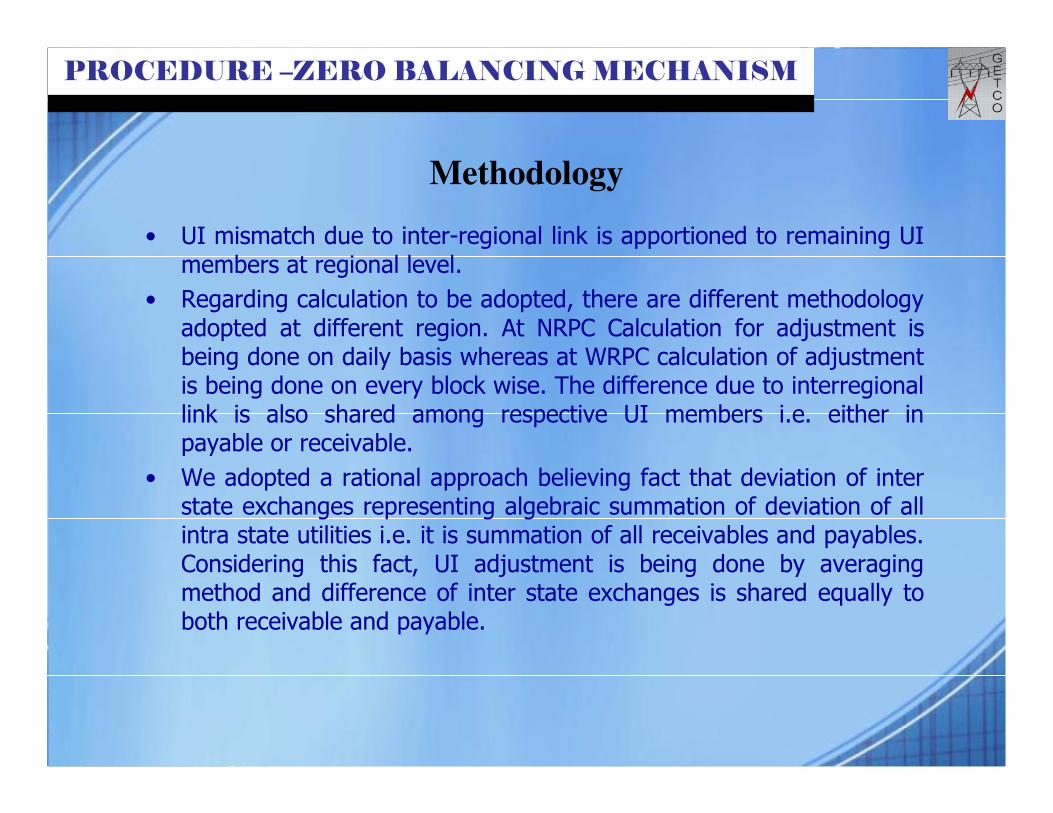

Methodology

• UI mismatch due to inter-regional link is apportioned to remaining UI members at regional level.

• Regarding calculation to be adopted, there are different methodology adopted at different region. At NRPC Calculation for adjustment is being done on daily basis whereas at WRPC calculation of adjustment is being done on every block wise. The difference due to interregional link is also shared among respective UI members i.e. either in payable or receivable.

• We adopted a rational approach believing fact that deviation of inter state exchanges representing algebraic summation of deviation of all intra state utilities i.e. it is summation of all receivables and payables. Considering this fact, UI adjustment is being done by averaging method and difference of inter state exchanges is shared equally to both receivable and payable.

PROCEDURE –ZERO BALANCING MECHANISM

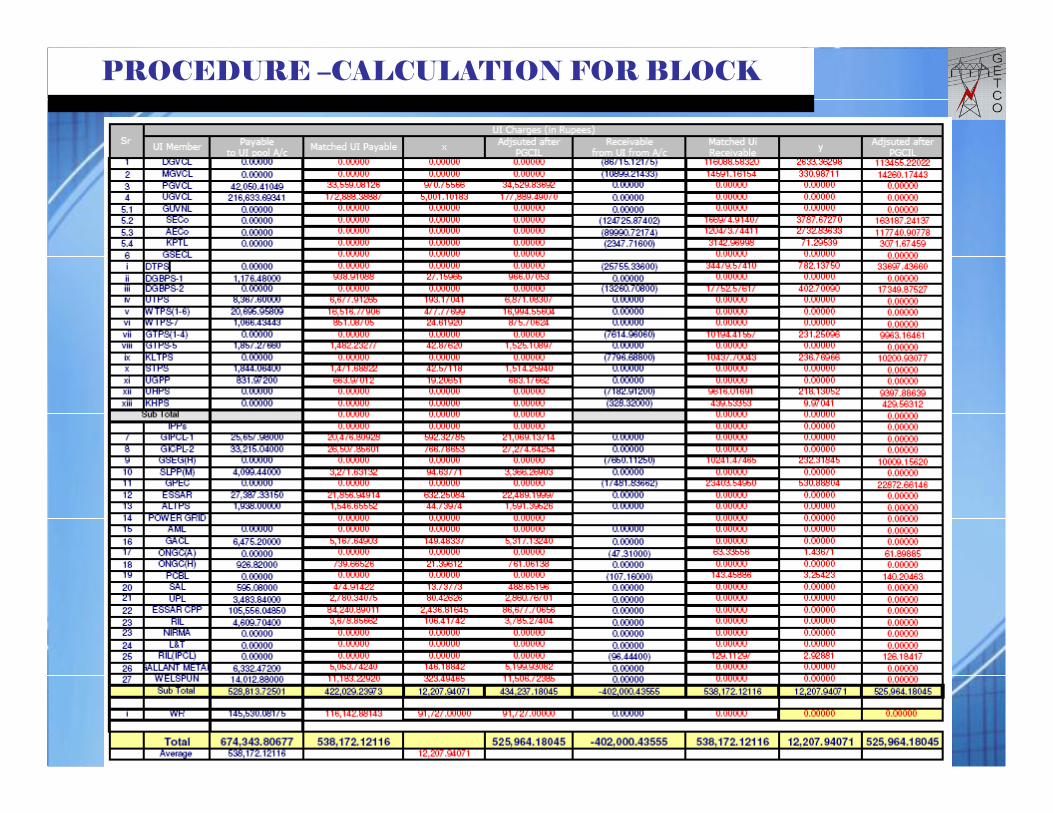

PROCEDURE –CALCULATION FOR BLOCK

Methodology

• UI pool account is computed on actual basis. Mis -match between UI receivables and payables derived is (674343.80676612-402000.43555482=272343.3712113). This difference is to be shared by as 50:50 among UI members of receivable and payable.

• UI matching is to be calculated by averaging method i.e. total of payable and receivable is adjusted to average value of both receivable and payable i.e.(674343.80676612+402000.43555482=538172.12116047 ).

• Since Inter-State exchanges is to be matched with RLDC account, we import data from WRPC account and derive differential amount between payable and receivable which represent difference due to inter state exchanges.

• By import of WRPC data for inter state exchanges, difference amount inreceivable and payable derived i.e. (116142.881426109-91727=24415.8814261092).

• Mis match due to inter state exchanges adjusted to receivable and payable as 50:50 in proportionate to their deviation and adjusted to the tune of(538172.12116047-(24415.8814261092/2))=525964.180447415.

• Same methodology is adopted for calculation of each block and adjustment is being done for each block. Summation of all 96 block ( day ) is shown in statement of UI charges.

PROCEDURE –CACULATION FOR BLOCK

Methodology

In intra state ABT, UI pool account should be a Zero as per regulation of

Hon’ble commission, and amount receivable/payable from regional pool

account should be equated in order to nullify differential amount, averaging

method proposed by STU/SLDC in petition (931/08) accommodating

regional account.

Proposed mechanism is described as below :

1) STU/SLDC shall draw out UI charges for all UI members of Intra

State based on actual generation and drawal however with

consideration of gaming, generator under shutdown and energy

injection of wind farm.

2) Unscheduled Interchange Charges is to be adjusted for zero balancing

by adjusting receivable and payable to tune of average value of

receivables & payable at Intra State level. It nullify difference created

due to non-uniform losses i.e. difference in estimated and actual losses.

3) Amount of UI receivable and payable to the regional pool account for

common WR transaction would than be equated by apportioning

difference to each receivables and payables in order to nullify

difference exist among inter state exchanges.

PROCEDURE –PROPOSED METHOD

Methodology

State Energy Account comprises energy account of declaration schedules,

drawal/injection schedule in order to facilitate computation of fixed charges

and variable charges and apportioning to respective distribution licensee. It

provides bifurcation of schedules among distribution licensee. State Energy

Account provides calculation of following :

PROCEDURE –STATE ENERGY ACCOUNT

InformationAllocation of Power in the State 8

Accounting at CPP endDetails of CPP Accounting7

Transmission ChargesDetails of Transmission/wheeling Charges6

Incentive Charges Details of Incentives Calculation for SGS Stations5

Fixed&Variable charges for CS stationsInter State Power Exchanges from WR-NTPC

generating station/Entitlement4

Transmission Charges/ Raising bill between Seller & Buyer

Summary of Inter-State Bilateral Exchanges3

Variable ChargesSummary of Scheduled Energy (SGS Stations)2

Fixed Charges Summary of Availability/Entitlement 1

Use DescriptionSr

In accordance with oral order issued by Hon’ble commission in the matter of petition no 931/2008, commission has issued a certain directive to carry out mock exercise with realistic inputs, so that actual impact can be evaluated and at the same time, it can be ensure methodology adopted for Intra State ABT. Accordingly, SLDC/STU has made certain changes in inputs as below :

– TPL, EPOL, ESTL declaration incorporated.

– Wind farm allocation ratio incorporated which is mentioned in specific notes.

– Revised UI rates as proposed in petition is incorporated.

– Energy drawn by generator during shutdown is considered as energy drawn from respective discom. Blocks are identified and same is kept out of UI accounts. We have incorporated statement of such instances in specific notes to facilitate accounting by respective discom & generator with their contract demand.

– Generation regulation carried out by SLDC as if Discom is doing

is incorporated in accounting in Implemented schedule.

– Amount of WR matched with WRPC account.

TRIAL UI & REC ACCOUNT

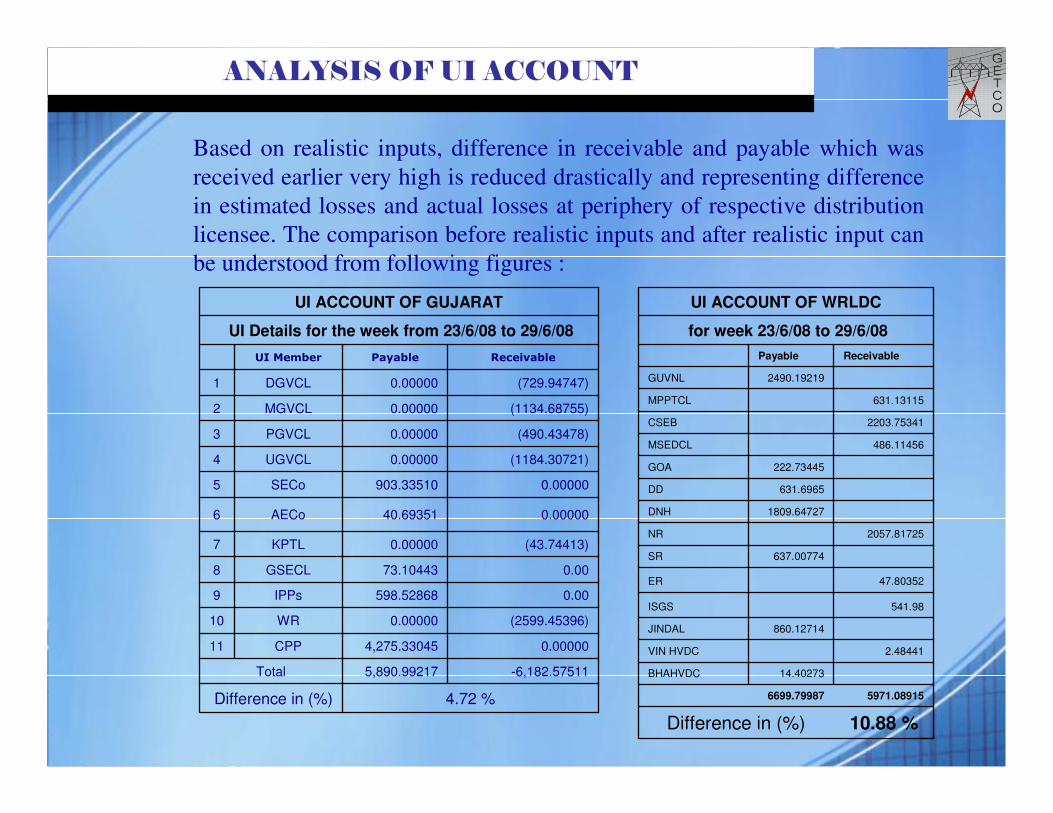

Based on realistic inputs, difference in receivable and payable which was

received earlier very high is reduced drastically and representing difference

in estimated losses and actual losses at periphery of respective distribution

licensee. The comparison before realistic inputs and after realistic input can

be understood from following figures :

ANALYSIS OF UI ACCOUNT

4.72 %Difference in (%)

-6,182.575115,890.99217Total

0.000004,275.33045CPP 11

(2599.45396)0.00000WR10

0.00 598.52868IPPs9

0.00 73.10443GSECL8

(43.74413)0.00000KPTL7

0.00000 40.69351AECo6

0.00000 903.33510SECo5

(1184.30721)0.00000UGVCL4

(490.43478)0.00000PGVCL3

(1134.68755)0.00000MGVCL2

(729.94747)0.00000DGVCL1

Receivable Payable UI Member

UI Details for the week from 23/6/08 to 29/6/08

UI ACCOUNT OF GUJARAT

10.88 %Difference in (%)

5971.089156699.79987

14.40273BHAHVDC

2.48441VIN HVDC

860.12714JINDAL

541.98ISGS

47.80352ER

637.00774SR

2057.81725NR

1809.64727DNH

631.6965DD

222.73445GOA

486.11456MSEDCL

2203.75341CSEB

631.13115MPPTCL

2490.19219GUVNL

Receivable Payable

for week 23/6/08 to 29/6/08

UI ACCOUNT OF WRLDC

IMPACT ON UI ACCOUNT AFTER REALISTIC I/P

1)Difference in receivable & payable before and after realistic input

for five weeks prepared & comparison with WRLDC account :

06.60%1.88 %46.30 %7/7/08 to 13/7/08

18.66%0.56 %45.77 %30/6/08 to 6/7/08

10.88%4.72 %24.52 %23/6/08 to 29/6/08

WRLDC Account

With Realistic Inputs

W/O Realistic Input

Difference in Receivable & Payable Wee Date

•It can be considered that with realistic inputs, difference

Between receivable and payable decreased which is respon

sible factor for impact on adjustment component. The effect

Can be seen in difference before and after adjustmenet in

Earlier account and above said accounting.

GENERATION REGULATION – SURPLUS TREATMENT

1) Generation regulation which is being handled by SLDC now as if Discom is doing, in order to avoid financial implication during mock exercise. The proposed methodology for same would be as under :

2) 1) Since entire capacity is allocated to respective distribution licensee based on demand pattern, respective distribution licensee shall plan for scheduling and submit requisition to SLDC. This would be effective from commercial operation of Intra-State ABT.

3) 2) Distribution licensee shall plan for their bilateral requirement by long term and short term forecasting and arrange purchase or sale of power directly booking corridor or through GUVNL.

4) 3) Distribution licensee shall optimize merit order operation by furnishing merit order from generating companies /GUVNL and surplus/deficit shall be accommodate within subsidiaries of GUVNL though surplus treatment. However, distribution licensee shall have to indicate their surplus/deficit whether to opt bilateral trading or to opt for UI.

5) 4) All bilateral transaction of inter state or intra state shall be done at periphery of distribution licensee i.e. buyer and seller shall be distribution licensee.

6) 5) During initial phase after Intra State ABT implementation, SLDC will provide support to carry out surplus treatment for optimization of merit order

operation till distribution licensee shall gear up.

7)

FURNISHING FEEDBACK

Distribution companies:

• Average purchase cost of PGVCL & UGVCL is low as power

generating capacity of low variable cost allocated to them. Hence

generally they do not reduced or backing down power generation

result in huge receivables of power. PGVCL & UGVCL which is

highly agriculture dominated area. Electricity demand reduced

during this period due to onset of monsoon, hence less drawal

compared to schedule result in receivables.

• DGVCL & MGVCL having power allocation of high variable cost,

are frequently facing a backing down of generation at the same

time demand is constant as it concentration of agriculture load is

less. It results in payables by MGVCL & DGVCL. However this

can be eliminated if generation regulation is handled by

respective Discom.

• SECO has less schedule result in payable. However, SECo can

reduce it by arranging more power purchase from different

stations or bilateral open access1)

FURNISHING FEEDBACK

GSECL Companies:

Most of stations are payable however margin is not significant. However it can be changed to

favorable by varying or revising declaration. Generator can declared quantum for feasible

production. However looking to deviation and in proportionate to deviation, UI is derived.

Kindly note that frequency correction is applied to gas based unit of utran, Dhuvaran. According

to procedure of UI accounting, it seems to be appropriate.

SLPP /GIPCL1/GIPCL2

SLPP & GIPCL 1 : GIPCL 1 generation reduced on 2/7/08 however schedule remain same. Also

on 3rd, generation is reduced. This can be reduced by revising declaration. SLPP generation

reduced (shutdown) however schedule remain same. They have not revised it for block of 40 to

70. Result in payable. However based on block wise deviation, amount received is representing

actual deviation of SLPP.

CPP: AML, RIL(IPCL(B), NIRAM , SAL, L&T : CPPs are not part of UI members as they don’t

have any Transaction scheduled, not third party sale nor wheeling to group of companies.

UPL & WELSPUN indicating major deviation. UPL is declaring 8 MW for wheeling but they are

drawing power during majority of block. WELSPUN is also declaring @ 24 MW whereas their

actual injection is possible half of declaration. HIDNALCO unit tripped on 30 june & 1st july

however their declaration was remain intake result in deviation. Rest of CPPs has managed

deviation in narrow band. By quoting this, we can inferred that UI of CPPs representing their

actual deviation.

Thank you