presentation innopay buckaroo partner day 15-11-2016

TRANSCRIPT

Shikko Nijland – November2016

2 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

• Innopay:innovation expertssince 2002

• OfficesinAmsterdamand Frankfurt

• 35consultants

• Payments,DigitalIdentity,e-Business

• Strategy,Co-creation,Transformation

• MemberofEBA,EPCAand ECP

• Founding memberofHollandFintech

Introduction

3 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Innopaymonitorsover50trends

4 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Today four key trendswill be highlighted2.Openbusiness

models

4.ChangingPOSinfra

3.Omnichannelauthentication

1.Regulation

5 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Trend1:Regulation2.Openbusinessmodels

4.ChangingPOSinfra

3.Omnichannelauthentication

1.Regulation

6 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

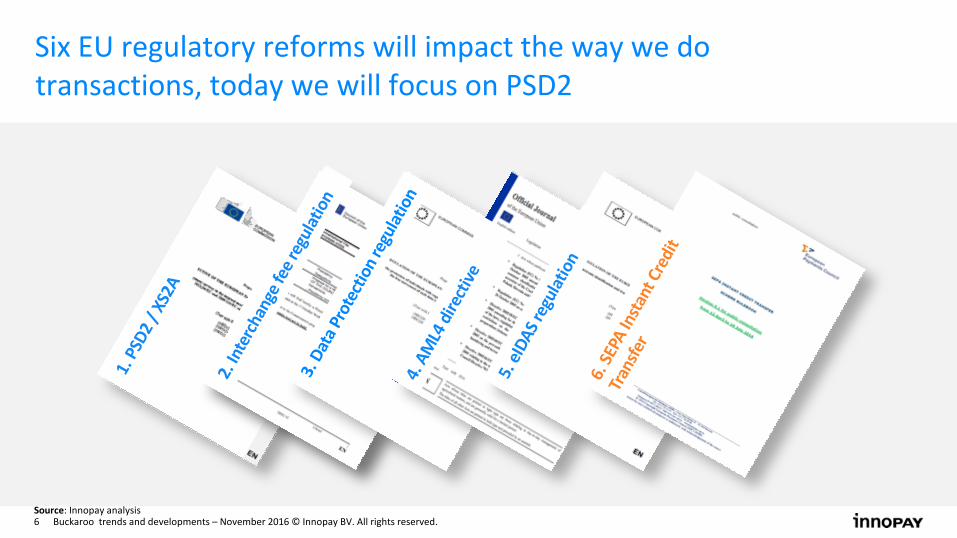

SixEUregulatoryreformswillimpactthewaywedotransactions,todaywewillfocusonPSD2

Source:Innopayanalysis

7 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Today’sfocus:marketentryoftwonewregulatedThirdPartyProviders(TPPs)underPSD2,i.e.‘PISP’and‘AISP’

XS2A

(‘API’)1

Customer

Bankdomain

PSD2XS2AERA

Bankaccount

Internetbankingandmobileapp

1Thereseems to be industry consensusthat ApplicationProgrammingInterfaces(APIs)provide for cost effective,easyand securemeansofenabling XS2A.However,EBARTSdonot mandate use ofAPIfor XS2A

PISPAISPT

PP

Source: Innopayanalysis

• BigTech• ERPvendors• Accountingsoftwarevendors• e-invoicingproviders

• NocontractualagreementsrequiredbetweenTPPandAS-PSP

• Non-discriminatorypaymentaccountaccessforlicensedTPPs(intermsoftiming,priorityandtransactioncharges)

KeyXS2A

provisions

• Incumbentbanks• Paymentinstitutions• E-moneyinstitutions• (Large)Merchants• FinTech

Potential

TPPs

Paymentaccount

SETTINGTHESCENE1

OPPORTUNITIESANDTHREATSPAYMENTSTAKEHOLDERS2

EXAMPLESUSEREXPERIENCE‘XS2A’3

8 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Accountinformationservice(AIS)valuestackisverypromisingfromaninnovationperspective

AISVALUESTACK

Applicationofdata

Insights

RawData

Adde

dvalue

Personal

Finance

Management

‘Bestoffer’

selection

Creditscoring

&loans

Purchase

offerings

(micro)

Savings&

Investments

e-Wallets&

payment

services

Source:Innopayanalysis

9 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

RTSsecurityrequirementswillinfluenceinnovationinthePSD2era

SCArequiredforALLremoteelectronicpaymenttransactions(Cards,

SCT)above10EUR,noriskbasedapproachaftertransitionalperiod

1.STRONG

CUSTOMER

AUTHENTICATION

1.EXEMPTIONS

1.COMMUNICATION

INTERFACE

1.PAN-EUREACH

SCAexemptionsareoptionalforAS-PSP,outsideremitEBAtomake

decisiononthis

Directaccess(Internetbanking)versusindirectaccess(DedicatedAPI),

atdiscretionofAS-PSP

Pan-Europeanstandardisation ofinterface,ratherthanfragmented

reach

1

2

3

4

Source:Innopayanalysis

SETTINGTHESCENE1

OPPORTUNITIESANDTHREATSPAYMENTSTAKEHOLDERS2

EXAMPLESUSEREXPERIENCE‘XS2A’3

10 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

PSD2mustbetransposedandenforcedasofJanuary2018,withearliest enforcementofsecuritystandardsinOctober2018

Min.35monthsTransitionalperiod

PSD2publishedinOJ

Dec’15

PSD2entersinto force

Jan‘16

April‘17

AdoptionRTSby Commission

Oct ‘18

RTSonstrongAuth.&secureComm.enforced

Jan‘16

StartEBAwork onRTS&Guidelines

Jan’17

Submit RTSonstrongAuth.&secure

Comm.

Transposed andenforced PSD2

byMemberStates

Jan’18

24months

18months

Source:Innopayanalysis

11 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Trend2:Opens businessmodels2.Openbusiness

models

4.ChangingPOSinfra

3.Omnichannelauthentication

1.Regulation

12 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Thefinancialindustry isexploring openingup,while other industrieshavealready embarkedtheroadtowardsopenbusinessmodels

THIRDPA

RTYINPU

TAP

Is

MAPS

UBERAPP

MESSAGING

PAYMENTPROCESSING

DELIVERYONDEMAND

RIDEREQUESTS

TRIPEXPERIENCES

UBERO

UTPU

TAPIs

Source:Innopayanalysis,Uber

13 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

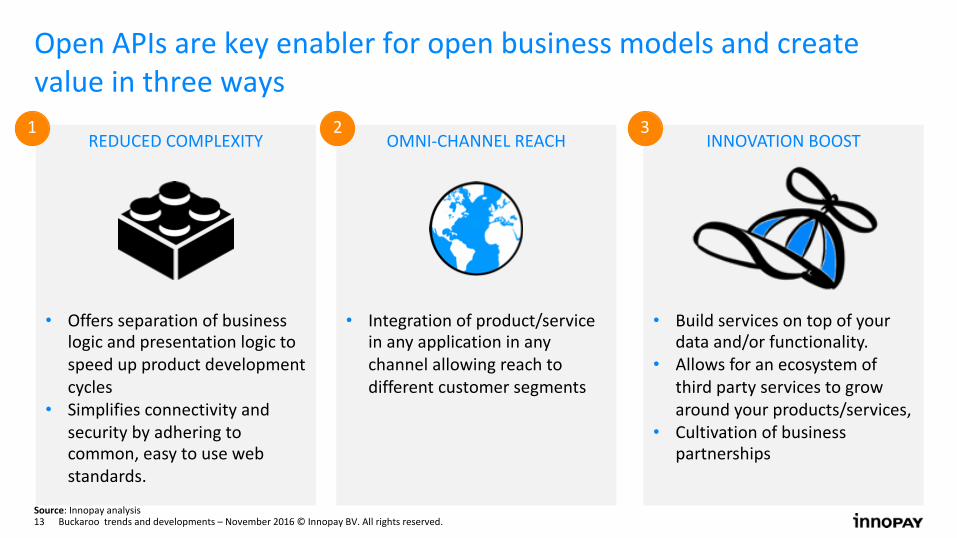

REDUCEDCOMPLEXITY

• Offersseparationofbusinesslogicandpresentationlogictospeedupproductdevelopmentcycles

• Simplifiesconnectivityandsecuritybyadheringtocommon,easytousewebstandards.

OMNI-CHANNELREACH

• Integrationofproduct/serviceinanyapplicationinanychannelallowingreachtodifferentcustomersegments

INNOVATIONBOOST

• Buildservicesontopofyourdataand/orfunctionality.

• Allowsforanecosystemofthirdpartyservicestogrowaroundyourproducts/services,

• Cultivationofbusinesspartnerships

OpenAPIsarekeyenablerforopenbusinessmodelsandcreatevalueinthreeways1 2 3

Source:Innopayanalysis

14 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

COMPANY APIUSAGE %REVENUESAPIS

AnovelapproachtodelivertheirCRMpositionandmakeiteasierforcustomerstointegratetheSalesfore CRMintotheirexistingworkflowsandcustomiseit

50%

Createamutuallybeneficialrelationshipbetweenthirdpartydeveloperstoenablemorefunctionalityandconvenienceforcustomers

Notpublicallyavailable

Extendtheirproductofferingtootherdigitalplatformssocustomerscanbenefitfromtheirlargeproductoffering

69%

APIscanbeusedtobookhotels,flightsandcars 90%

Enabledeveloperstodevelopapplications‘ontopof’platformthatenableintelligentlifestylechoices,andassessmentofnewbusinessventures

Notpublicallyavailable

ThegoaloftheplatformgoesbeyondbeinganetworkaccesspointbutaglobaldistributionplatformforitsproductsandservicesbyusingAPIstounbundletheirservices

Notpublicallyavailable

Improvingengagementandcustomerrelationshipswithclientsbyenablingdeveloperstodevelopapplications’ontopof’theplatform (e.g.socialapplicationsandgames)

Notpublicallyavailable

ManycompaniesuseAPIsforvariouscommercialpurposesandfordevelopingservicesthatfitcustomerneeds

Source:Innopayanalysis

15 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

PRICINGMODELSREVENUEMODELS

VariousrevenuemodelsareusedtopricethebenefitsthattheAPIowneroruserreceive

Source:Innopayanalysis,JohnMusser,CEOofAPIScienceandfounderofProgrammableWeb

• PayasyouGo:Fixedpricepertransaction

• Tiered:Differentpricesaccordingtovolume

• Freemium:Free,butpaidupgrade

• Unit-based:Priceperbatchoftransactions

• Revenueshare:Payshareofrevenues

• Affiliate:PaywhenAPIisused• Costperclick(CPC)• CostperAction(CPA)• Referral

• Blended:Combinationofrevenuemodels

User

pays

APIowner

pays

Indirect/

Noonepays

• WhethertheAPIownerpaysortheuserdependsonwhoderivesbusinessbenefitsfromthetransaction

• TheAPIownerhoweversetsthepriceandcandosobasedontheuser’swillingnesstopay

16 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Dependingonthetargetgroup,thelevelofopennessdiffers

PublicAPI

PartnerAPI

Internal

API

Closed

Open

• Innovationbyengagingrelevantdevelopercommunity

• Extendedmarketreach• Monetizationoptions

BENEFITSFUNCTION

APIsusedbyexternalpartnersanddeveloperstobuildinnovativeapps

• Extendeddigitalvaluechain• Partnerintegrationefficiency• Enhancedcustomerexperience• Monetizationoptions

APIsusedbybusinesspartnersand/orcustomers(e.g.corporates/merchants)

• Operationalefficiency• Costreduction• Internalcostmanagement

APIsusedbyinternaldeveloperswithinenterprise(e.g.bank)

Source:Innopayanalysis

17 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Trend3:Omnichannelauthentication2.Openbusinessmodels

4.ChangingPOSinfra

3.Omnichannel

authentication

1.Regulation

18 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

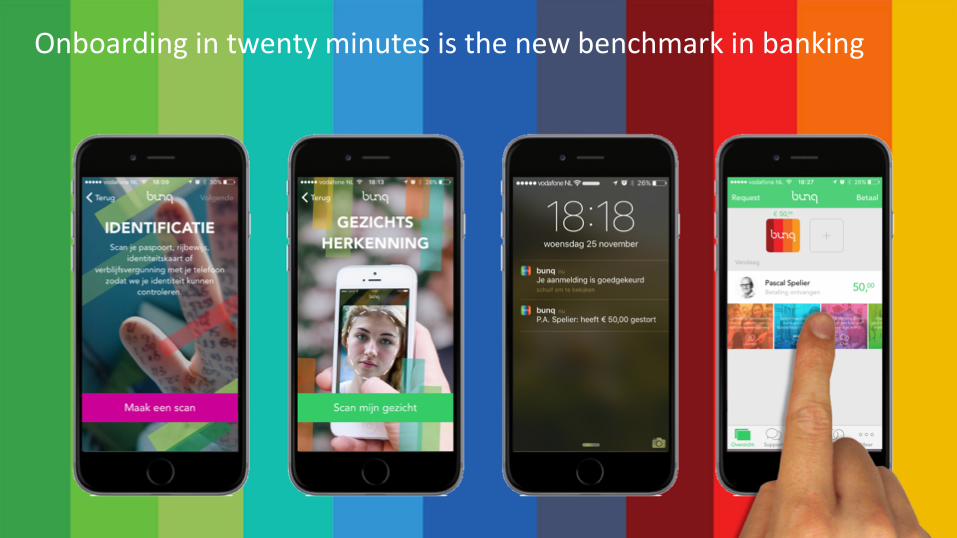

BUNQOnboarding intwentyminutesisthenewbenchmarkinbanking

19 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Recognizingcustomersisnotnew

Source:Innopayanalysis

BEHAVIOUR RELATIONSHIP

20 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Recognisingacustomerearlyinthecustomerjourneyiskeytopersonalisation

Orientation Selection Transaction Delivery Customercare

Checkout

Checkin

Orientation Selection Transaction Delivery Customercare

Hi,I’mJohnandauthorizethispayment

Hi,I’mJohn Iauthorizethispayment

Source:Innopayanalysis

21 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Butthemainchallengeistorecognisecustomers through variouschannels along their customerjourney

CUSTOMERJOURNEY

FYSICALSHOP

WEBSHOP

(MOBILE)APP

INSPIRATIONCHANNELS

CUSTOMERSERVICE

Orientation Selection Transaction Delivery Customercare

WEBSHOP

Source:Innopayanalysis,Expertgroup ‘Omnichannel CustomerIdentification - Shopping2020

22 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Connectingchannelsrequiresaccounts/identifiersthatcanbesharedacrosschannels

WEBSHOP

Source:Innopayanalysis,Expertgroup ‘Omnichannel CustomerIdentification’- Shopping2020

23 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

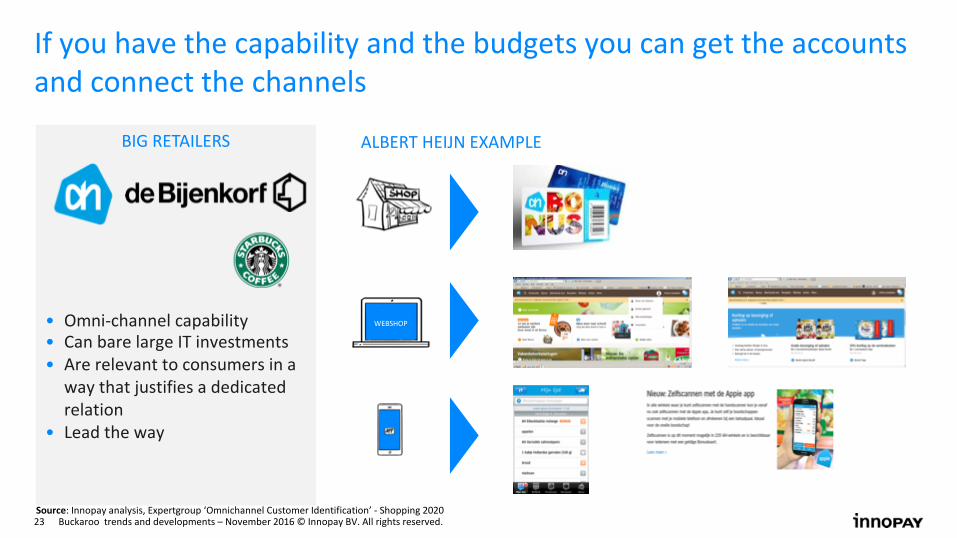

If you havethe capability and the budgetsyou can getthe accountsand connect the channels

BIGRETAILERS

• Omni-channelcapability• CanbarelargeITinvestments• Arerelevanttoconsumersinawaythatjustifiesadedicatedrelation

• Leadtheway

WEBSHOP

ALBERTHEIJNEXAMPLE

Source:Innopayanalysis,Expertgroup ‘Omnichannel CustomerIdentification’- Shopping2020

24 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

BIGRETAILERS

• Omni-channelcapability• CanbarelargeITinvestments• Arerelevanttoconsumersinawaythatjustifiesadedicatedrelation

• Leadtheway

SMERETAILERS

• Multi-channel(mostlywebandshop)

• LimitedITbudgetsand/orLimitedrelevancetoconsumers

LONGTAILRETAILERS

• Onlyone’developed’channel(maybeinfowebsite)• VirtuallynoITbudget• Mayberelevanttoconsumers

SMEretailerswillonlyhaveabusinesscasewhenreachtorelevantconsumerandITcapabilitiesareprovidedtothem

Source:Innopayanalysis,Expertgroup ‘Omnichannel CustomerIdentification’- Shopping2020

25 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

BIGRETAILERS

• Omni-channelcapability• CanbarelargeITinvestments• Arerelevanttoconsumersinawaythatjustifiesadedicatedrelation

• Leadtheway

SMERETAILERS

• Multi-channel(mostlywebandshop)

• LimitedITbudgetsand/orLimitedrelevancetoconsumers

LONGTAILRETAILERS

• Onlyone’developed’channel(maybeinfowebsite)• VirtuallynoITbudget• Mayberelevanttoconsumers

Majorityofmerchantscannotcreateenoughreachthemselvesandneedtobepartofacommunitytoeffectivelyengageconsumers

NeedforPlatform

Source:Innopayanalysis,Expertgroup ‘Omnichannel CustomerIdentification’- Shopping2020

26 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

DigitalIdentityisaprerequisiteforopenAPIs,andbanksareinaprimepositiontoleveragethiscapability

• Whetherpaymentsorsharingofcustomer’sdataexplicitconsentoftheconsumerisrequired

Explicitconsent

• Strongdigitalidentity(onboardingandauthentication)processesarekeyrequirementstoofferpaymentservices

• WithintroductionofPSD2,PISPsandAISPswillneedtocomplywithsimilarAML/KYCrequirementsasbanks

• Thisgivesbankscompetitiveadvantageinofferingthirdpartyservicesastheyalreadyhavethesemeasuresinplacefortheirownpaymentandaccountprocesses

Example:UsingaccountinformationserviceAPItocheckeligibilityforloanatconsumer’sbank

REQUIREMENTSTOPROVIDECONSUMERCONSENT EXAMPLE

Source:Innopayanalysis

27 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Trend4:Changing POSinfrastructure2.Openbusinessmodels

4.Changing

POSinfra

3.Omnichannelauthentication

1.Regulation

28 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

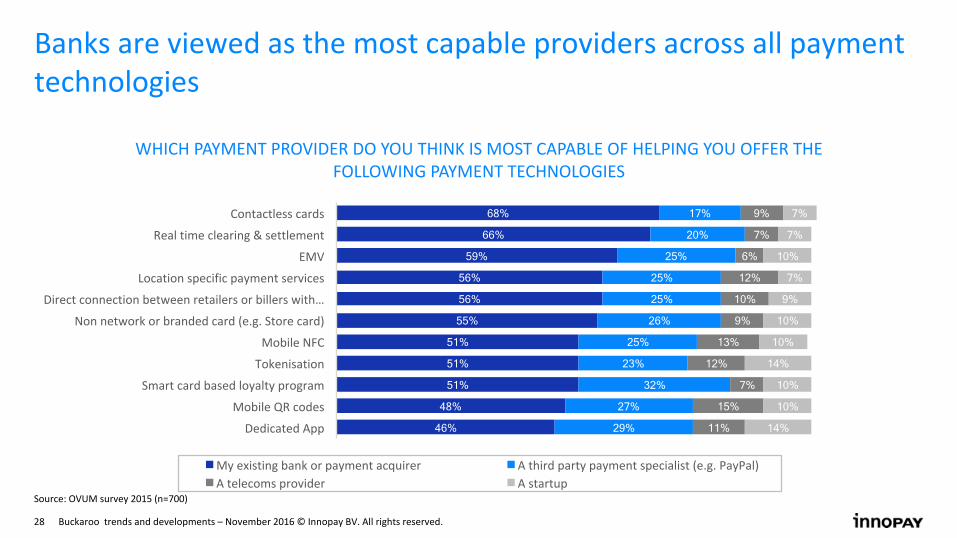

46% 48% 51% 51% 51% 55% 56% 56% 59%

66% 68%

29% 27%

32% 23% 25%

26% 25% 25%

25% 20% 17%

11% 15%

7% 12%

13% 9% 10% 12% 6%

7% 9%

14% 10% 10%

14% 10% 10% 9% 7%

10% 7% 7%

DedicatedApp

MobileQRcodes

Smartcardbasedloyaltyprogram

Tokenisation

MobileNFC

Nonnetworkorbrandedcard(e.g.Storecard)

Directconnectionbetweenretailersorbillerswith…

Locationspecificpaymentservices

EMV

Realtimeclearing&settlement

Contactlesscards

WHICHPAYMENTPROVIDERDOYOUTHINKISMOSTCAPABLEOFHELPINGYOUOFFERTHEFOLLOWINGPAYMENTTECHNOLOGIES

Myexistingbankorpaymentacquirer Athirdpartypaymentspecialist(e.g.PayPal)Atelecomsprovider Astartup

Banksareviewedasthemostcapableprovidersacrossallpaymenttechnologies

Source:OVUMsurvey2015(n=700)

29 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

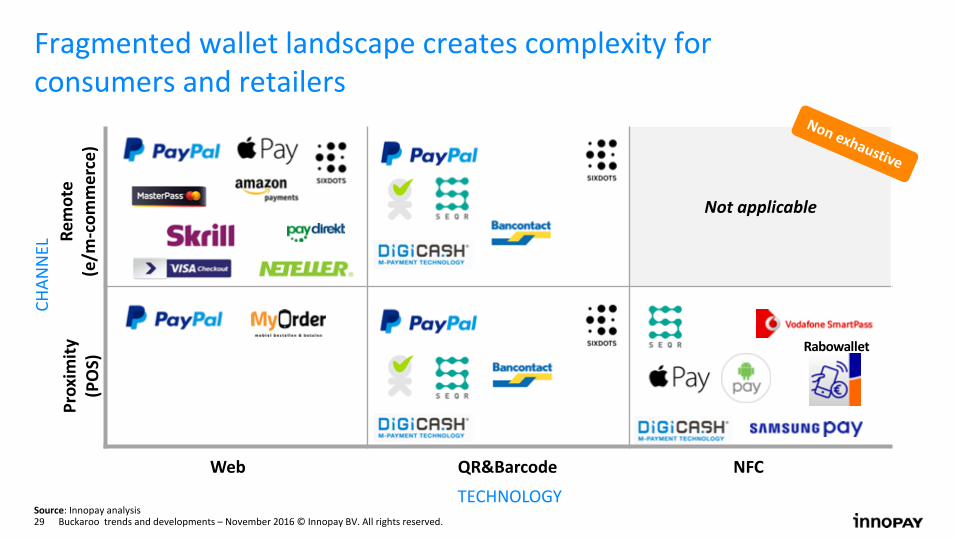

Fragmentedwalletlandscapecreatescomplexityforconsumersandretailers

TECHNOLOGY

CHAN

NEL

Web QR&Barcode NFC

Proxim

ity

(POS)

Remote

(e/m-commerce)

Rabowallet

Source:Innopayanalysis

Not applicable

30 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

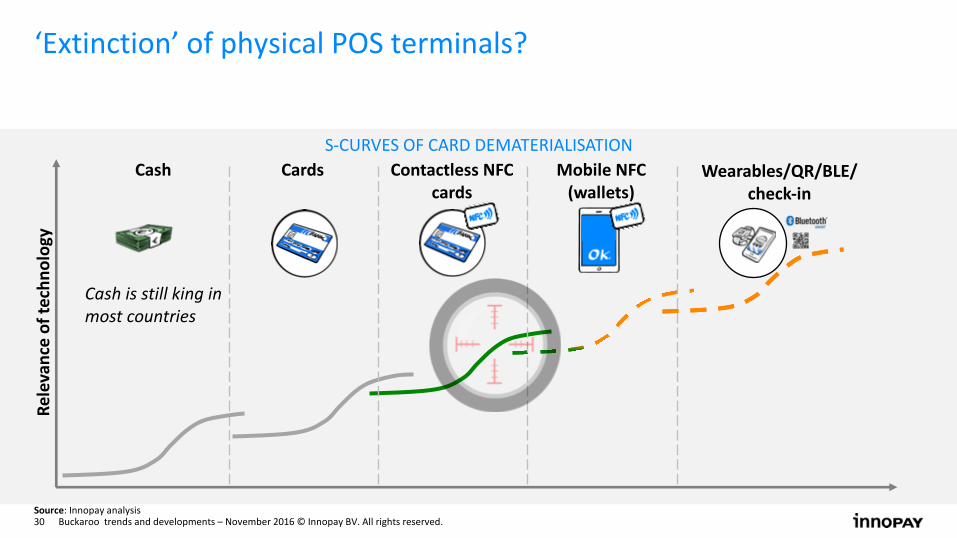

‘Extinction’ofphysicalPOSterminals?

Time

S-CURVESOFCARDDEMATERIALISATION

Relevanceoftechnology

CardsCash ContactlessNFC

cards

MobileNFC

(wallets)

Wearables/QR/BLE/

check-in

Cashisstillkinginmostcountries

Source:Innopayanalysis

31 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Devices

Customer

Journey

Orientation Selection Transaction Delivery Customercare

Context

(Crossborder)Paymentsanytime,anywhereonanydevicealsoincreasesnumberofpotentialtouchpoints

Source:Innopayanalysis

32 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.Source:Innopayanalysis

Newtypeofinfraisnecessarytofullyexploitpotentialofnewtouchpoints:Omni-touchpointConversionInfrastructure(OCI)

SHAREDINFRASTRUCTUREBENEFITS

• Customershaveonesingleexperienceandhavefulldatacontrol

• Customersgainfromautomatedrewardsandappliedgiftcards

• Organisationsbenefitfromtransparencyoftouchpointsandencounterfullaccountabilityofmarketingspend

• Organisationscanconnectdirectlyandaremoreflexibleandversatile

• Tocloseloop;presenceonconsumermobileANDintegrationinCashRegisterismandatory

Source:Innopayanalysis

Media

Brand

Retailer

33 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Wrapup

34 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Mostuselesstrendin2016…….

35 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

36 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

• Foundedin2002

• OfficesinAmsterdam(HQ)andFrankfurt

• 35+consultantsplusInternationalnetworkofassociatedexpertsviaEPCAnetwork(seealsopicture)

• Threecorepractices:Payments,DigitalIdentityandE-Business

• Strategy,co-creationandtransformation

• Memberofa.o. EBA,ECPandEPCA• FoundingmemberofHollandFintech

Moscow

Warsaw

Budapest

Milan

Rome

Malta

Frankfurt

Amsterdam

Paris

London

Copenhagen

Source:EPCA(2015)

Zurich

Riga

InnovationexpertsinPayments,DigitalIdentityandE-Business

37 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

InnovationServices

Corepractices

Strategy

Co-creation

Transformation

PAYMENTS DIGITALIDENTITY

E-BUSINESS

• Marketandproductassessment• Multi-sidedplatformdesign• Vendorandsolutionselection

• Co-creationofproductsandservices• Developingplatformsforco-creation• Buildingco-creationcapabilities

• Content-basedprojectmanagementsupport• Opportunitybasedoperatingmodelimprovement• Digitalchangeandmigrationmanagement

Ourserviceportfolioensuresclientscancountonusthroughoutthewholedigital

journey

38 Buckarootrendsanddevelopments– November2016©InnopayBV.Allrightsreserved.

Strongassetsinco-creatingvalueincomplexmulti-stakeholderfields

Bron:Innopay

2.PaymentEU1.PaymentNL

8.Accountbasedtraveling&ticketing7.Invoicing

3.(Open)Banking 4.PSD2/OpenAPI

OTA

OpenTransactionAlliance

6.InclusiveSCF5.Omni-ChannelAuthentication&

Onboarding