presentation conservative portfolio plus

DESCRIPTION

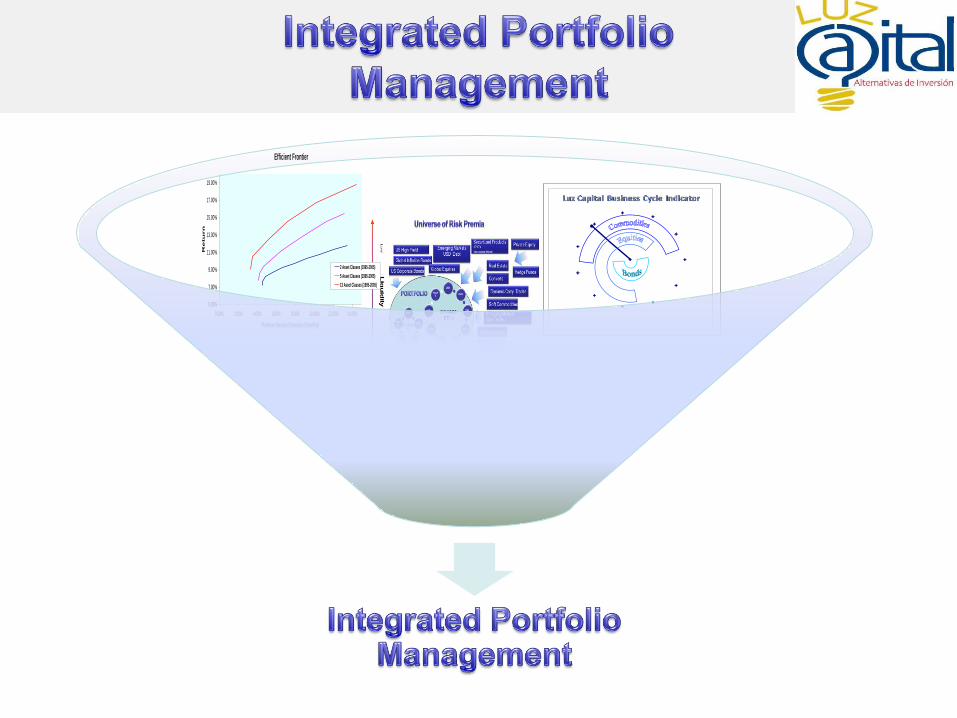

A portfolio model that uses a proprietary business cycle detection algorithm and Modern Portfolio Theory to invest in the Global MarketsTRANSCRIPT

Liquidity

Transparency

Risk

Control

Technology

Cost

Diversification

Complexity

Return

The Asset Allocation Model uses modern portfolio theory and business cycle

detection to determine the major portion of the Investment Portfolio.

The Model has been backtested from January 2003 to November 2010 with daily

valuations and monthly rebalances.

The Investment Portfolio is highly diversified by type of asset (fixed income, equity,

alternative investments and commodities), currency (G10 countries proprietary

dynamic strategy and emerging markets) and geographic region (USA, Europe, Asia,

Africa, and Latin America).

The Model invests in liquid products (ETF’s and Futures).

Credit risk is minimized by taking positions in index-replicating products.

Rotation through different asset classes is governed by a proprietary business cycle

detection model.

Model determines 100% of portfolio.

Expected returns are 400 to 500 bps above 1yr Libor.

The combined backtested and virtual portfolio net return to investors is 9.51%

annually with volatility of 7.15% since January 2003.

Annual returns were always positive even though the simulation period included, the

wars in Afghanistan and Iraq and the 2007-2008 world financial crisis.

The business environment is cyclycal and is composed of four periods : Expansion,Slowdown,

Downturn and Recovery

Cycles vary in length but they usually last 44 to 60 months from begening to end.

Technology and economic changes have modified the business cycle.

In the 70’s the US economy was dominated by industrial production, currently it is more service

oriented.

Some technical and fundamental indicators can predict the business cycle.

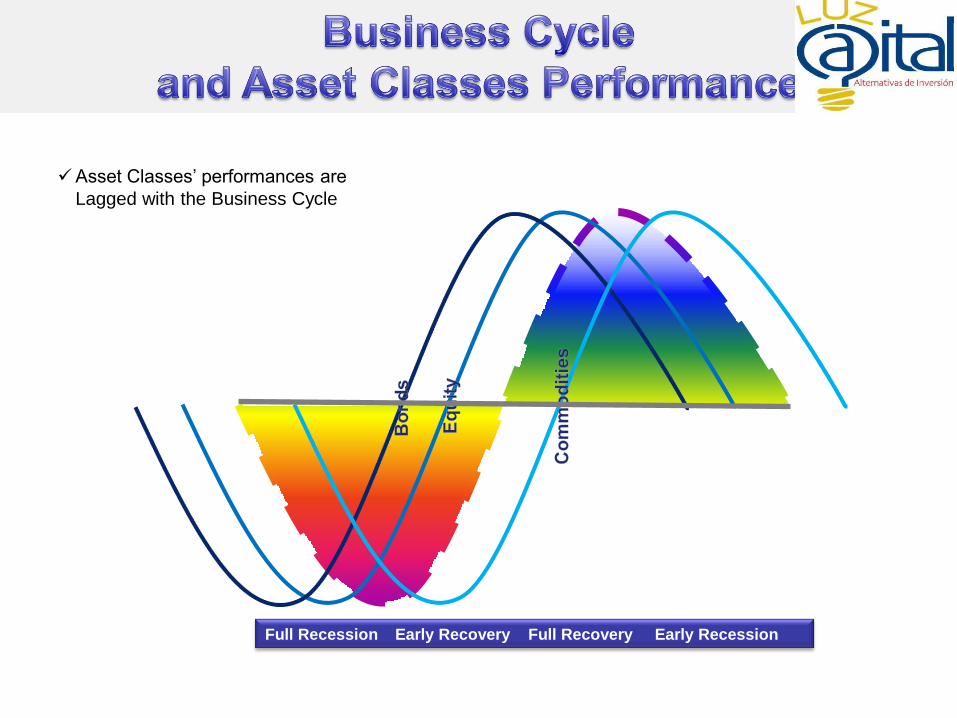

Asset Classes’ performances are

Lagged with the Business Cycle

Full Recession Early Recovery Full Recovery Early Recession

Luz Capital has developed a

proprietary business cycle

indicator

The business Cycle is partitioned

into 11 different stages.

The Indicator informs that market

data is predicting a bullish

period, only, for the Asset

Class(es) (Bonds, Equities and

Commodities) being crossed by

the radial dark blue line.

The information is used for

optimizing the asset allocation

model.

The Efficient Frontier is a financial tool that describes, for a given portfolio, the maximum

returns for different risk levels that it would had achieved in a certain period of time.

Adding more asset classes to the portfolios increases the returns and lowers the risk. Such

assets should be low correlated to the other assets in the portfolio.

We believe that the optimal asset mixed should be between 12 and 22.

Efficient Frontier

5.00%

7.00%

9.00%

11.00%

13.00%

15.00%

17.00%

19.00%

0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00%

Portfolio Standard Deviation (Volatility)

Retu

rn

2 Asset Classes (1995-2005)

5 Asset Classes (1995-2005)

13 Asset Classes (1995-2005)

Hig

h

Low

Liq

uid

ity R

isk

Transparency Risk

Lo

w

High

DBX

EMB

DBA

ERO

JYNPSP

PLW

IYR

PBHAX

Emerging MarketsCarry Trades

US Corporate Bonds

G10 Currencies

Emerging Markets

USD Debt

SHY

IGOB

SPYLQD

PBHAX

Converts

Dynamic Carry Trades

Global Inflation Bonds

Soft Commodities

Hedge FundsUS High Yield

Precious Metals

Global EquitiesReal Estate

Volatility Futures

Efficient Frontier

5.00%

7.00%

9.00%

11.00%

13.00%

15.00%

17.00%

19.00%

0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00%

Portfolio Standard Deviation (Volatility)

Re

tu

rn

2 Asset Classes (1995-2005)

5 Asset Classes (1995-2005)

13 Asset Classes (1995-2005)

U.S. Bonds

EM Sovereign

High Yield Bonds

MBS

Convertibles

U.S. Equities

Euro Equities

Japan Equities

EM Equities

Precious Metals

Oil

Agri. Commodities

U.S. Real Estate

G10 Currencies

EM Currencies

CTA

Equity Long/Short

Merger Arb

Volatility

U.S

. Not

es

U.S

. Bon

ds

EM S

over

eign

Hig

h Yie

ld B

onds

MBS

Con

verti

bles

U.S

. Equ

ities

Euro

Equities

Japa

n Equ

ities

EM E

quities

Preciou

s M

etal

s

Oil

Agri.

Com

mod

ities

U.S

. Rea

l Est

ate

G10

Cur

renc

ies

EM C

urre

ncie

s

CTA

Equity

Lon

g/Sho

rt

Mer

ger A

rb

-0.2

0.0

0.2

0.4

0.6

0.8

12/31/1994 12/23/1998 12/15/2002 12/7/2006 11/30/2010

Date

0%

20%

40%

60%

80%

100%

Allo

ca

tion

U.S..Notes

U.S..Bonds

EM.Sovereign

High.Yield.Bonds

MBS

Convertibles

U.S..Equities

Euro.Equities

Japan.Equities

EM.Equities

Precious.Metals

Oil

Agri..Commodities

U.S..Real.Estate

G10.Currencies

EM.Currencies

CTA

Equity.Long.Short

Merger.Arb

Volatility

12/31/1994 12/23/1998 12/15/2002 12/7/2006 11/30/2010

Date

0%

20%

40%

60%

80%

100%

Allo

ca

tion

U.S..Notes

U.S..Bonds

EM.Sovereign

High.Yield.Bonds

MBS

Convertibles

U.S..Equities

Euro.Equities

Japan.Equities

EM.Equities

Precious.Metals

Oil

Agri..Commodities

U.S..Real.Estate

G10.Currencies

EM.Currencies

CTA

Equity.Long.Short

Merger.Arb

Volatility

12/31/2002 1/22/2005 2/14/2007 3/8/2009 3/31/2011

Date

0%

20%

40%

60%

80%

100%

Allo

catio

n

Monthly Returns

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year

2 0 0 3 0 .3 9 % 1.77% ( 0 .6 2 ) % 1.73 % 3 .59 % 0 .16 % ( 1.2 7) % 2 .53 % 1.58 % 1.9 8 % 1.2 6 % 1.18 % 15.13 %

2 0 0 4 1.15% 1.13 % 0 .9 7% ( 5.57) % ( 1.12 ) % 1.0 5% ( 0 .2 8 ) % 1.4 2 % 1.0 2 % 1.3 2 % 0 .0 5% 1.9 4 % 2 .8 9 %

2 0 0 5 0 .9 6 % 0 .11% ( 1.3 3 ) % 0 .4 2 % 1.0 9 % 1.55% ( 0 .4 7) % 0 .71% ( 0 .17) % ( 1.12 ) % 1.8 8 % 1.6 0 % 5.3 0 %

2 0 0 6 0 .3 9 % 0 .4 9 % 0 .4 5% 1.9 6 % ( 0 .8 9 ) % ( 0 .59 ) % 1.51% 1.77% 0 .3 7% 1.8 8 % 2 .14 % 0 .2 9 % 10 .15%

2 0 0 7 0 .8 4 % ( 0 .4 6 ) % 0 .15% 1.4 7% 0 .6 5% 0 .3 1% 1.8 0 % ( 0 .0 9 ) % 3 .2 2 % 2 .8 3 % ( 0 .4 0 ) % 0 .6 5% 11.4 5%

2 0 0 8 ( 1.52 ) % 3 .11% ( 1.73 ) % ( 0 .0 3 ) % 0 .59 % ( 0 .8 1) % ( 0 .8 4 ) % 0 .2 6 % ( 3 .3 3 ) % ( 4 .4 8 ) % 6 .18 % 6 .8 5% 3 .6 8 %

2 0 0 9 ( 4 .3 4 ) % ( 1.3 4 ) % 1.8 2 % 1.4 8 % 5.6 4 % ( 0 .2 6 ) % 4 .2 3 % 1.6 7% 3 .57% ( 0 .0 5) % 3 .8 3 % 0 .4 6 % 17.58 %

2010 ( 1.3 3 ) % 1.9 3 % 3 .70 % 1.73 % ( 5.3 6 ) % ( 0 .3 7) % 2 .4 0 % 0 .13 % 4 .0 8 % 2 .2 7% ( 0 .11) % 1.6 1% 10 .8 3 %

2011 ( 0 .2 3 ) % 1.4 6 % 0 .15% # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # # 1.3 9 %

0%

5%

10%

15%

20%

25%

Histogram of Monthly Returns

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

Annual Returns

Summa ry Da ta

M o del

C o nserv

at ive

SP X

Index

7-10 Year

B o nd

Index

9.39% 5.10% 4.96%

7.05% 14.99% 7.02%

0.62 0.01 (0.01)

4.94% 8.13% 4.72%

0.89 0.01 (0.01)

69.70% 63.64% 60.61%

30.30% 36.36% 38.38%

1.69% 2.94% 1.61%

(1.35)% (3.74)% (1.43)%

6.85% 9.39% 8.15%

(5.57)% (16.94)% (5.56)%

(10.01)% (52.56)% (6.45)%

8 16 6

2 - - 12

Be nc hma rk Compa risons

SP X

Index

7-10 Year

B o nd

Index

7.21% 9.17%

Beta in Up Markets 0.29 0.30

Correlation in Up Markets 43.60% 22.35%

Alpha in Down Markets 7.25% 7.19%

Beta in Down Markets 0.26 0.37

Correlation in Down Markets 41.01% 25.31%

7.88% 7.69%

0.269 0.359

57.18% 35.68%

Beta in All Markets

Correlation in All Markets

Maximum Drawdown

Months In Maximum Drawdown

Months To Recover

Alpha in Up Markets

Alpha in All Markets

% of Positive Months

% of Negative Months

Average Loss

Best Month

Worst Month

Average Gain

Std. Deviation

Sharpe Ratio (5.0%)

Downside Deviation

Sortino Ratio (5.0%)

Compound ROR

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

$2,200

Growth of $1,000

Conservative SPX Index 7-10 year Bond

12%

8%

34%

8%

38%

Positions by World Region

EMERGING MARKETS

EUROPE

GLOBAL

JAPAN

USA

23%

9%

17%19%

23%

5%2% 2%

Portfolio By Type of Market Risk

ALTERNATIVE

COMMODITY

CURRENCY

EQUITY

FIXED INCOME

MONEY MARKET