presentation: benefits and costs of bank capital - piie · benefits and costs of bank capital...

TRANSCRIPT

Benefits and Costs of Bank Capital

Giovanni Dell’Ariccia

International Monetary Fundwith Jihad Dagher, Luc Laeven, Lev Ratnovski, and Hui Tong

http://www.imf.org/external/pubs/ft/sdn/2016/sdn1604.pdf

The views in this presentation are those of the authors and do not necessarily represent those of the IMF, its Management, or Executive Board

How much bank capital is enough?

How much bank capital would have been enough to…

absorb bank losses

prevent bank recapitalizations

…in past banking crises?

How much bank capital is enough?

1. Capital 15-23 % RWA avoids creditor losses / bank recaps in a majority of past banking crises in AE Further increases have only marginal benefits

CARs could be lower due to buffers, other regulations

2. Losses in crises in EM >> in AE as a share of bank assets, not as a share of GDP 15-23 RWA limits bank losses to 3 percent of GDP

3. Costs of transitioning >> long-term costs of higher capital Impose gradually

Encourage to raise equity rather than reduce assets

Assessing benefits of bank capital

Approach 1: NPLs in Banking Crises

0

10

20

30

40

50

60

70

80

90

Non-OECD Countries OECD Countries

NPL ratio, percent

Source: Laeven and Valencia, 2013 (IMF-ER)

NPL in OECD

0

10

20

30

40

50

60

70

Luxe

mb

ou

rg, 2

008

Swit

zerl

and

, 200

8

Swe

de

n, 2

008

Ne

the

rlan

ds,

200

8

Ge

rma

ny,

20

08

Au

stri

a, 2

008

UK

, 200

7

U.S

., 1

988

Be

lgiu

m, 2

008

Fran

ce, 2

008

U.S

., 2

007

Spai

n, 1

977

De

nm

ark

, 20

08

Spai

n, 2

008

Po

rtu

gal,

2008

Fin

lan

d, 1

991

Swe

de

n, 1

991

Slo

ven

ia, 2

00

8

No

rway

, 199

1

Hu

nga

ry, 2

008

Cze

ch R

ep

., 1

996

Ital

y, 2

008

Ire

lan

d, 2

008

Gre

ece

, 200

8

Jap

an

, 19

97

Ko

rea

, 19

97

Ice

lan

d, 2

008

NPL ratio, percent

Simulations subject to uncertainty

Loss given default (from 25% to 75%)

Conversion to RWA (ratio up to 250%)

Margin of safety (1% to 3%)

Parameters Values

(in percent)

Values

(in percent)

Values

(in percent)

1. NPL during a banking crisis 18.0 18.0 18.0

2. Loss given default 75.0 50.0 50.0

3. Loan losses (1*2) (Mean point) 13.5 9.0 9.0

4. Absorbed by prior provisionning 1.5 1.5 1.5

5. Loan losses net of provisions (3-4) 12.0 7.5 7.5

6. Margin of Safety (Residual capital) 1.0 1.0 3.0

7. Capital to assets ratio (5+6) 13.0 8.5 10.5

8. Total assets/RWA 175.0 250.0 175.0

9. Capital ratio (percent of RWA) (7*8) 22.8 21.3 18.4

Share of banking crises avoided,

based on crisis NPL data, OECD

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0 10 20 30 40 50 60

Loss given default = 50% Loss given default = 75%

Risk-Weighted Bank Capital Ratio, percent

Share of banking crises avoided

Other sources of uncertainty Security portfolios

Security losses comparable to loan losses (US data)

GFC: securities 5.2% vs loans 4.95%

“severely adverse” stress test: securities 3.6% vs loans 4.5%

Bank heterogeneity discuss later

EMs: Losses larger as share of bank assets, not as share GDP

0

10

20

30

40

50

60

70

Non-OECD Countries OECD Countries

Percent

Approach 2:

Fiscal costs of bank recaps

Figure 6. Pre-crisis Bank Capital and Fiscal Recapitalization Expenses in Banking

Crises in 2007-

0

10

20

30

40

50

60

70

Fiscal cost of bank recapitalizations, 2007-

Average bank capital ratio, 2007

Non-OECD countries

Share of risk-weighted assets, percent

OECD countries

Source: Laeven and Valencia, 2013 (IMF-ER)

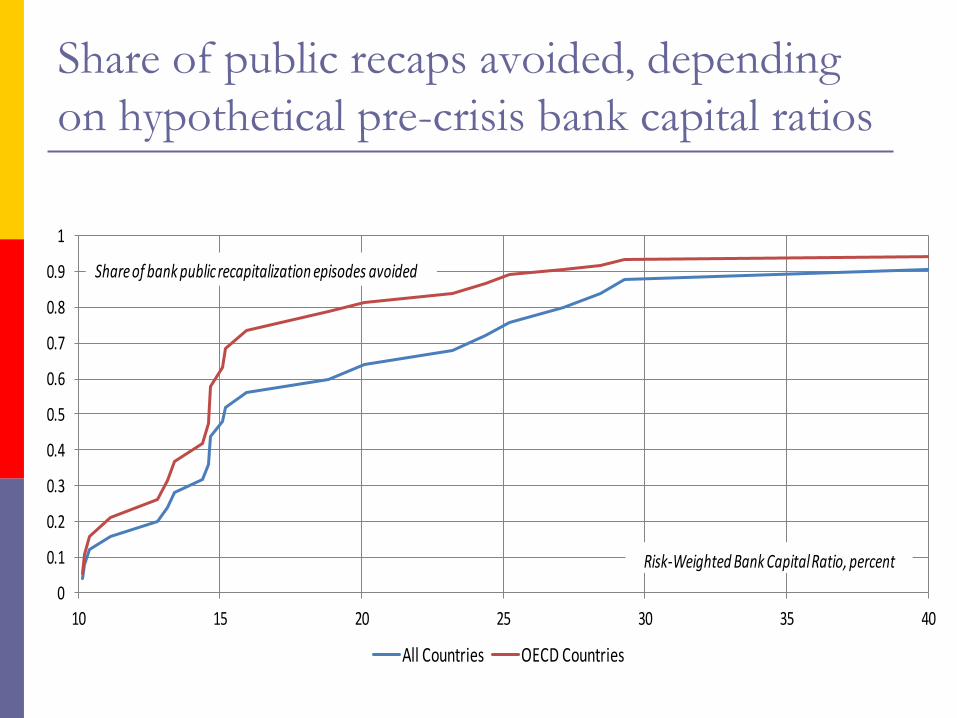

Share of public recaps avoided, depending

on hypothetical pre-crisis bank capital ratios

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

10 15 20 25 30 35 40

All Countries OECD Countries

Share of bank public recapitalization episodes avoided

Risk-Weighted Bank Capital Ratio, percent

Capital injections: Bank heterogeneity

Assessing costs of bank capital

Much uncertainty on the cost side

Estimates of steady-state costs (mostly calibrations): extremely small

Estimates of transition costs (relatively well identified, but idiosyncratic): very large

Transition costs >> Steady-state costs

Therefore

Gradually, but market may demand adjustment upfront

Good economic times

Where does this take us?

Much uncertainty on costs

Evidence from the crisis suggests minimal effect of higher capital on credit

Notes: Averages for banks - U.S. and European G-SIBs (U.S.: (Bank of America, Citigroup, JPMorgan Chase, Wells Fargo; Europe: Barclays, HSBC, Royal Bank of Scotland, BNP Paribas, Credit Agricole, Societe Generale, Deutsche Bank, and Credit Suisse). Domestic bank credit/GDP for Europe is weighted average for France, Germany, UK.

0

2

4

6

8

10

12

14

Tier 1 capital ratio Intermediation margin Domestic bank credit/ GDP (right axis)

2004 2014

0

2

4

6

8

10

12

14

Tier 1 capital ratio Intermediation margin Domestic bank credit/ GDP (right axis)

2004 2014

Europe U.S.

0

20

40

60

80

100

120

140

0

20

40

60

80

100

120

140

Summary

1. Capital 15-23 % RWA avoids creditor losses / bank recaps in a majority of past banking crises in AE

2. Costs of transitioning >> long-term costs of higher capital

3. Losses in crises in EM >> in AE as a share of bank assets, not as a share of GDP