presentasi accounting liabilities

TRANSCRIPT

ACCOUNTING

LIABILI

TIES

Prese

nted b

y ik

a ra

hmaw

ati

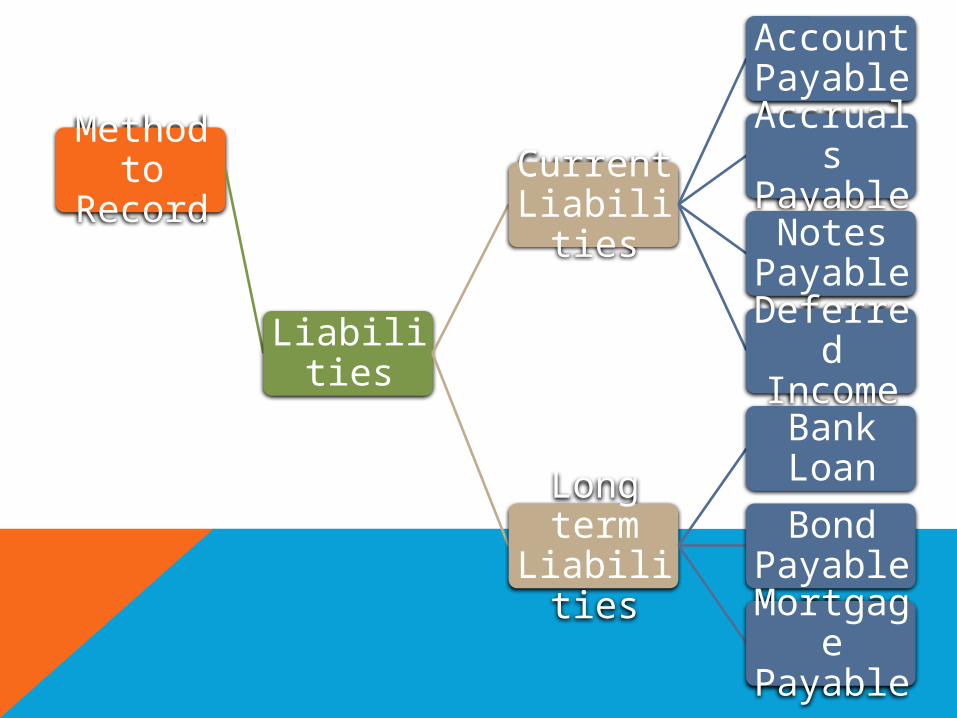

Method to

Record

Liabilities

Current Liabilitie

s

Account Payable

Accruals Payable

Notes PayableDeferre

d Income

Long term

Liabilities

Bank Loan

Bond PayableMortgag

e Payable

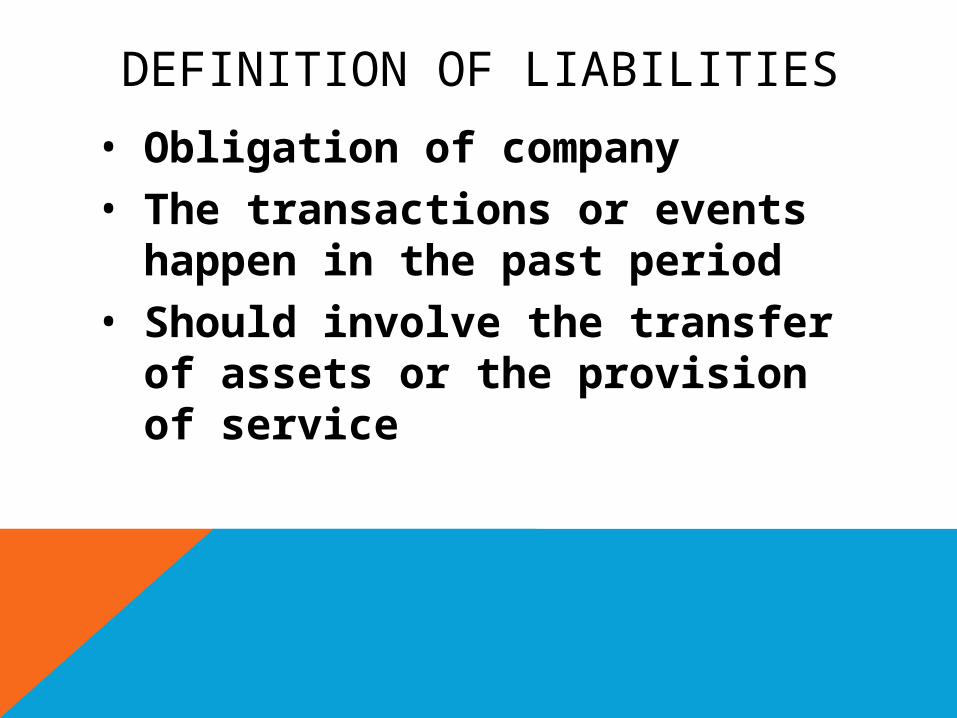

DEFINITION OF LIABILITIES

• Obligation of company• The transactions or events

happen in the past period• Should involve the transfer of

assets or the provision of service

THE RECORDING OF LIABILITIES METHOD

a) Account Payable Procedure

Card payable is the form of payable that have function to make a list from each creditor, which consist of invoice number of suppliers, the amount of payable, the amount of the payment, and the balance of the payable

b) Voucher Payable Procedure

Do not use card payable. But using vouchers archives stored in the archive alphabetically or according to their maturity dates. Archive cash out evidence serves as a record of payable.

THE MEASUREMENT OF LIABILITIES

For measurement purpose, both current and non-current liabilities can be classified into three types, namely:

• The certain amount of liabilities

• The amount of liabilities that must be estimated

• contingent liablility

CURRENT LIABILITIES

liabilities company to the third side that must be repaid within less than one year.

Account PayableAccruals PayableNotes PayableDeferred Payable

ACCOUNT PAYABLE

are liabilities that happen from the purchase of services or goods on credit

For example :

On December 25, 2013 PT Mutiara have purchase goods on credit to PT.Baja Jaya Abadi amounted to Rp 100,000,000, -.

*the above transactions were recorded by the journal as follows :

Phisik Method

Purchase Rp100.000.000,-

Account Payable Rp100.000.000,-

Perpectual Method

Merchandise Inventory Rp100.000.000,-

Account Payable Rp100.000.000,-

NB: if have PPN : can inside the amount/outside

ACCRUALS PAYABLE

The liabilities that have become expense but the company not paid yet

Example :

• Wages & Salaries payable

• Interest payable

• Tax payable

• Rent Payable

Example :

On December 31, 2013 Not yet paid the wages & salaries to employee amount Rp2.000.000

Wages & Salaries Expense Rp2.000.000,-

Wages & Salaries payable Rp2.000.000,-

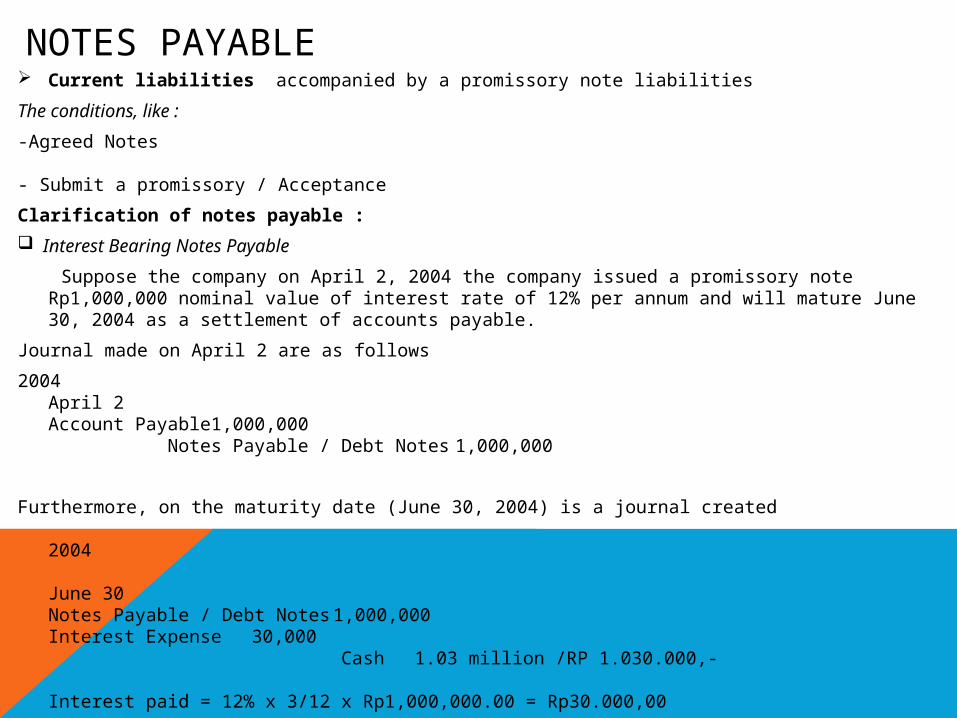

NOTES PAYABLE Current liabilities accompanied by a promissory note liabilities

The conditions, like :

-Agreed Notes

- Submit a promissory / Acceptance

Clarification of notes payable :

Interest Bearing Notes Payable

Suppose the company on April 2, 2004 the company issued a promissory note Rp1,000,000 nominal value of interest rate of 12% per annum and will mature June 30, 2004 as a settlement of accounts payable.

Journal made on April 2 are as follows

2004April 2Account Payable 1,000,000 Notes Payable / Debt Notes 1,000,000

Furthermore, on the maturity date (June 30, 2004) is a journal created

2004

June 30Notes Payable / Debt Notes 1,000,000Interest Expense 30,000 Cash 1.03 million /RP 1.030.000,-

Interest paid = 12% x 3/12 x Rp1,000,000.00 = Rp30.000,00

NOTES PAYABLE Non Interest Bearing Notes

• promissory publisher pays only nominal value, thus the nominal value is the value at maturity

EXAMPLE:

on 30 December 2003 the company did not submit bills 100,000,000.00 nominal flowering to a creditor to repay the company's debts amounted Rp90.000.000,00 him. If the deposit of promissory notes (loan notes) is the value of the debt is repaid that Rp90.000.000,00. Maturing August 30, 2004. Journal notes made at this time are:

31 December, 2003Account Payable 90,000,000Discount on Notes Payable 10,000,000 Notes Payable / Debt Notes 100,000,000

Notes 100,000,000.00 account balance and the balance of discount on notes payable Rp10,000,000.00 presented in the balance sheet as follows:

Current Liabilities:Notes Payable 100,000,000Less: Discounts on Debt Notes (10,000,000)

Acc. Payable 90,000,000

On August 30, 2004, at the time of paying bills amounting to 100,000,000.00 company makes two journals as follows:

August 30, 2004

Notes Payable 100,000,000Cash 100,000,000Interest Expense 10,000,000Discount on Notes Payable 10,000,000

DEFERRED PAYABLE• The revenue that not the right company for the year, but the advance

payment already received by the company.

• Due to the amount that was received was unearned for the period in question, then this amount is an advance payment received by the company

On August 1, 2010 accepted the rental store for a period of 2 years of 12,000,000, the end of the accounting period set December 31, 2010

• If Revenue received in advance is received in cash / cash, the above transactions were recorded by the journal as follows:

Cash 100,000,000Prepaid Rent 100.000.0000

If revenue received in Bank the journal is…

LONG TERM LIABILITIES

Liabilities company to a third side that must be repaid within more than one year. • The incidence of Long-Term

liabilitiesCurrenly the company development and to takes a number of funds

TYPE LONG TERM LIABILITIES

Bank LoanBond PayableMortgage Payable

BANK LOAN

Long term liabilities from Bank for business expansion.

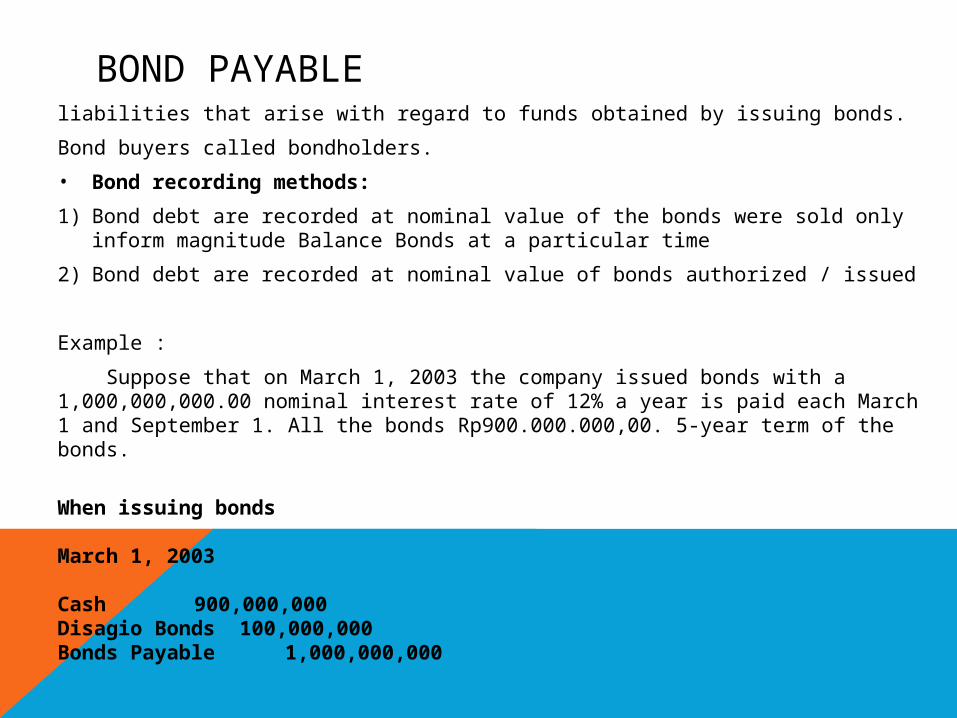

BOND PAYABLEliabilities that arise with regard to funds obtained by issuing bonds.

Bond buyers called bondholders.

• Bond recording methods:

1) Bond debt are recorded at nominal value of the bonds were sold only inform magnitude Balance Bonds at a particular time

2) Bond debt are recorded at nominal value of bonds authorized / issued

Example :

Suppose that on March 1, 2003 the company issued bonds with a 1,000,000,000.00 nominal interest rate of 12% a year is paid each March 1 and September 1. All the bonds Rp900.000.000,00. 5-year term of the bonds.

When issuing bonds

March 1, 2003

Cash 900,000,000Disagio Bonds 100,000,000Bonds Payable 1,000,000,000

BOND PAYABLE

Bonds payable are recorded at nominal value which is the value of bonds listed on the certificate. The difference between the nominal value of the cash received is recorded as a discount.

When paying interest

September 1, 2003Interest Expense 60,000,000Cash 60,000,000

Due at maturity the company must pay the amount of the maturity, the account disagio be amortized by debiting and crediting accounts Interest Expense Bonds Disagio account. Total amortization can be determined with the straight-line method or other methods. If used straight-line method, the amortization disagio for March 1 s / to 1 September was :

6/12 x (100,000,000 / 5) = Rp10,000,000.00 and journals that are created are:

September 1, 2003Interest Expense 10,000,000Disagio Bonds 10,000,000

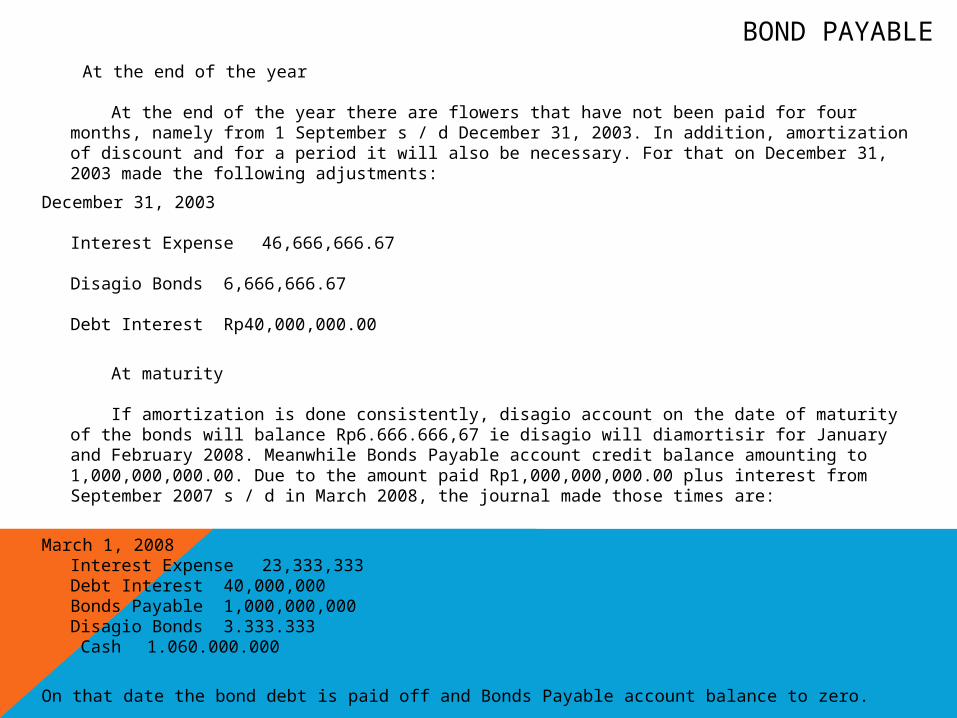

BOND PAYABLE At the end of the year

At the end of the year there are flowers that have not been paid for four months, namely from 1 September s / d December 31, 2003. In addition, amortization of discount and for a period it will also be necessary. For that on December 31, 2003 made the following adjustments:

December 31, 2003

Interest Expense 46,666,666.67

Disagio Bonds 6,666,666.67 Debt Interest Rp40,000,000.00

At maturity

If amortization is done consistently, disagio account on the date of maturity of the bonds will balance Rp6.666.666,67 ie disagio will diamortisir for January and February 2008. Meanwhile Bonds Payable account credit balance amounting to 1,000,000,000.00. Due to the amount paid Rp1,000,000,000.00 plus interest from September 2007 s / d in March 2008, the journal made those times are:

March 1, 2008Interest Expense 23,333,333Debt Interest 40,000,000Bonds Payable 1,000,000,000Disagio Bonds 3.333.333 Cash 1.060.000.000

On that date the bond debt is paid off and Bonds Payable account balance to zero.

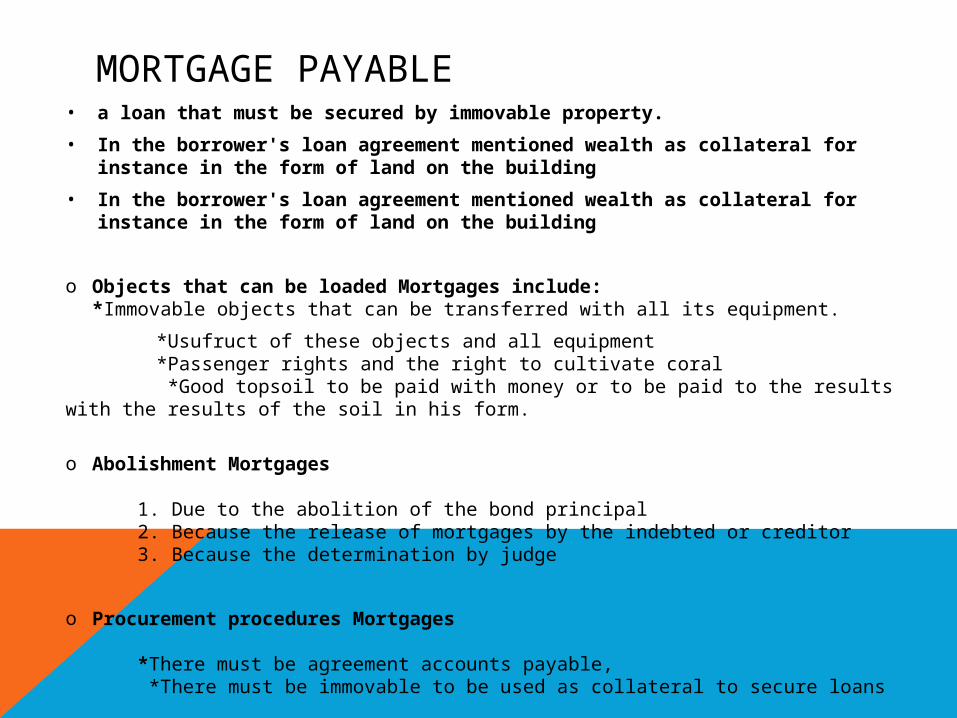

MORTGAGE PAYABLE• a loan that must be secured by immovable property.

• In the borrower's loan agreement mentioned wealth as collateral for instance in the form of land on the building

• In the borrower's loan agreement mentioned wealth as collateral for instance in the form of land on the building

o Objects that can be loaded Mortgages include:*Immovable objects that can be transferred with all its equipment.

*Usufruct of these objects and all equipment *Passenger rights and the right to cultivate coral *Good topsoil to be paid with money or to be paid to the results with the results of the soil in his form.

o Abolishment Mortgages

1. Due to the abolition of the bond principal 2. Because the release of mortgages by the indebted or creditor 3. Because the determination by judge

o Procurement procedures Mortgages

*There must be agreement accounts payable, *There must be immovable to be used as collateral to secure loans

MORTGAGE PAYABLEProblems example:

August 1 PT. X Interesting mortgage loans amounted to Rp. 20.000.000, - the administrative costs Rp. 1.000.000, - 6 months installments, interest of 15% / year repayment term of 20 months. Record:

Mortgage loan installment moment Note the adjustment at the end of the period

Answer:

Journal of Mortgage LoansCash Rp19.000.000, -By. Adm Rp. 1.000.000, -Mortgage Payable Rp20.000.000, -

Journal on August 1 for installments and interest

Interest = 15% x 6/12 x Rp.20.000.000, - = Rp. 1.500.000, - mortgage debt = Rp. 20,000,000 / USD. 20 months = Rp. 1,000,000 / month for 6 months = So the 6months x Rp. 1.000.000, - = Rp. 6.000.000, -

Mortgage debt Rp. 6.000.000, -Flowers Rp. 1.500.000, -Cash Rp. 7.500.000, -

Adjusting Journal Entry

Total cost for 6 months is Rp. 6.000.000, - then deducting the administrative costs Rp. 1.000.000, - it can be Rp. 5.000.000, - Interest = 15% x 5/12 x Rp.20.000.000, - = Rp. 1.250.000, - May 5: In August-December (end of period) there are 5 Months.

Mortgage debt Rp. 5.000.000, -Costs. Flowers Rp. 1.250.000, -Mortgage debt which immediately dibyr Rp. 5.000.000, -Flowers Utangg Rp. 1.250.000, -

THANK

YOU !!

!!!