preliminary results

DESCRIPTION

Preliminary Results. year ended 30 September 2013. Story of 2013. Introduction. Further potential. ABEC (India), Trade-Link & ECMI (Malaysia ). Supports acquisition strategy. Good growth in mid tier events. Expansion of business in Asia. 12% profit growth. Strong year. - PowerPoint PPT PresentationTRANSCRIPT

Preliminary Results...................................................................................................................

year ended 30 September 2013...................................................................................................................

Introduction .......................................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Good growth in mid tier events

Expansion of business in Asia

ITE’s first step into China

2014 sales looking good

Story of 2013

Strong year

Further potential

ABEC (India), Trade-Link & ECMI (Malaysia)

Chinacoat

7% like-for-like revenue growth

12% profit growth

Strong balance sheet Supports acquisition strategy

2

Financial Results...............................................................................................

2013

01

Financial Results 2013...................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Financial Highlights for the year to 30 September 2013

2013 2012

Audited Audited

Revenue £192.3m £172.3m

Gross profit margin 46% 45% Biennial impact

Administrative expenses £31.2m £26.6m

Headline profit before tax £59.4m £53.0m +12%

Headline diluted EPS 19.3p 16.9p

Dividend per share 7.0p 6.5p

Net trading +£12mBiennial +£4mAcquisitions +£4m

Net trading +£12mBiennial +£4mAcquisitions +£4m

+12%

+14%

+8%

4

+12% Investment in staff & infrastructure

Reduction in effective tax rate

Financial Results 2013...................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

2012 Headline

PBT

Net Biennial

Effect

Timing

£M

Portfolio growth

Acquisitions 2013 Headline

PBT

53.0

3.8

(0.9)

59.4

5.5

1.5

30

40

50

60

2012 to 2013 Headline PBT Bridge

Overheads & FX & Financing

(3.5)

5

Financial Results 2013...................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Net cash Sept 12

Cash Flow from operations

Tax

£M

Acquisitions & def considerations

Net cash Sept 13

Dividends Other

62.1

13.0

66.2 (16.4)

23.5

(2.1)

(26.1)

ABEC £14.0mTrade-Link £4.1mECMI £1.7mTurkeybuild (20%) £5.0mOther £1.3m

ABEC £14.0mTrade-Link £4.1mECMI £1.7mTurkeybuild (20%) £5.0mOther £1.3m

(11.1)

10

20

30

40

70

60

50

80 112% of Headline PBT112% of Headline PBT

2012 to 2013 Cashflow Bridge

6

Financial Results 2013...................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Sales and Yield Analysis

Metres Revenue GrossProfit Yield

000s £m £m Per m²

2012

Results from Events 798 171.2 77.5

Non annual 2012 (74) (9.3) (3.4)

Recurring Events 724 161.9 74.1 224

2013

Acquisitions 25 3.8 1.9

Timing differences (15) (3.0) (0.9)

Organic growth 12 15.5 5.9

Recurring Events 746 178.2 81.0 239

2013Non annual 2013 47 13.2 7.2

Results from Events 793 191.4 88.2

7

25 launches£4m revenue25 launches£4m revenue

Financial Results 2013...................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Currency & Hedging

Currency of Sale 2014 (F) % 2013 %

Average Translation Rate

2014YTD

2013

EUR 40 40 1.19 1.20

RUB 30 30 52 49

GBP, YTL, US$ & other 30 30

Exposure to currency fluctuation over March-April-May

€ 1.17 in 2012€ 1.17 in 2012

Forward cover on €/£ €70m @ €1.20 (2014-2016)

Exposure to sterling strength, currently £: R54Exposure to sterling strength, currently £: R54

8

1 cent = £0.3m : 1 Ruble = £0.5m

Financial Results 2013...................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Trading Update – 2014 Contracted Revenue

54% 56% 52% 56% 56%

b

20

40

60

80

%

FY 2010 FY 2011 FY 2012 FY 2013

£93m£95m£74m

52% 53%55%56%

FY 2014*

£54m

56%

10

£106m

% booked to 29th November 2013 of Event Year

£m Sales Booking – FY2014

Event Financial Year* FY 2014% of Full year revenue is based on the analyst consensus of £193m

9

Strategy.................................................

2013

02

Strategy .................................................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

‘Create sustainable growth in headline earnings per share’

By building sustainable positions of market leadership

in exhibitions in emerging markets

11

Strategy .................................................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Implementing Strategy

Strategy

Improve existing

positions

Expand to new geographies &

sectorsBuild brands

Invest in staff

12

.................................................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

ABEC (28% ownership, call on 32% in 2015)

Revenue £11.0m PBT £2.5m

Events: sqm• Acetech

Mumbai 27,000Delhi 22,000Kolkata new for 2014 Bengaluru 9,000Ahmedabad 4,000

• Real Estate8,000

• Education 9,000• Lifestyle 2,500• Other 5,000

100%Delhi

Mumbai

Bengaluru Chennai

KolkataAhmedabad

StrategyIndia

13

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Shanghai

Hong Kong

Guangzhou

Kuala Lumpur

Asia

MALAYSIA Trade-Link ITE(75% ownership)

100% Revenue £2.3m

ECMI ITE (50% ownership)MALAYSIA100% Revenue £0.9m

CHINA Sinostar ITE (50% ownership)

Revenue @£11.0m PBT £6.5m

Singapore

Yangon

Ho Chi Minh

Jakarta

Bangkok

StrategyS.E Asia

.................................................................................................................................................

100%

14

Strategy .................................................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Building & Interiors Oil & Gas Travel &

TourismFood & Drink

Transport & Logistics

Metal-working Beauty Paper Coatings

Russia

Turkey

Ukraine

Kazakhstan

Azerbaijan India

Southeast Asia

China

Expanding the Business

Pre-2012

Post-2012

Existing business

New business

Launches

15

Strategy .................................................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Maximising Opportunities

Synergy

Strengthen brand identities

Harmonise data & improve customer

intelligence

Develop ‘vertical’ expertise

Develop portfolio

management

16

ITE Beauty Events 2013

Baku

Krasnodar

Kuala Lumpur

Jakarta

Yangon

ThailandHo Chi Minh City

Kyiv

Novosibirsk

.................................................................................................................................................Strategy

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Istanbul

17

Launch for 2014

Strategy .................................................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Sustainable Growth 2003 to 2013

Hea

dlin

e di

lute

d EP

S (p

ence

)

Hea

dlin

e pr

ofit b

efor

e ta

x (£

m)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

10

20

30

40

50

60

70

0

5

10

15

20

25

30

35

£59.4m

19.3p

18

Divisional Analysis..............................................................................................................

2013

03

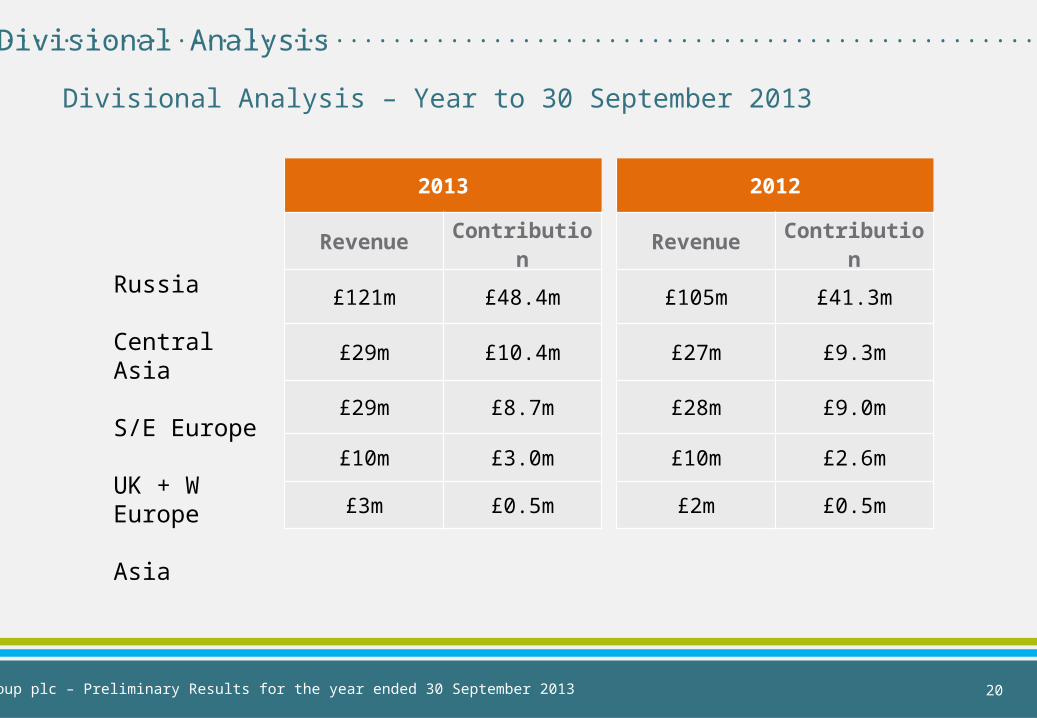

Divisional Analysis...........................................................................................................................

Divisional Analysis – Year to 30 September 2013

Russia

Central Asia

S/E Europe

UK + W Europe

Asia

2013

Revenue Contribution

£121m £48.4m

£29m £10.4m

£29m £8.7m

£10m £3.0m

£3m £0.5m

2012

Revenue Contribution

£105m £41.3m

£27m £9.3m

£28m £9.0m

£10m £2.6m

£2m £0.5m

ITE Group plc – Preliminary Results for the year ended 30 September 2013 20

Divisional Analysis...........................................................................................................................

Russia

2013 2012

m² ‘000 399 392

Revenue £121m £105m

L4L revenue growth 7%

ST. PETERSBURG

MosBuild resilienceMOSCOW

L4L revenue growth 15%

Good growth in industrial & mining portfolios

L4L revenue growth 13%

NOVOSIBIRSK

New venue expansion in 2016KRASNODAR

L4L revenue growth 27%

Volume & yield growth in new venue

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Looking forward... Regional cloning

21

Divisional Analysis...........................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Central Asia

2013 2012

m² ‘000 82 80

Revenue £29m £27m

Looking forward... Steady growth

L4L revenue growth 10%

AZERBAIJAN

Construction reboundKAZAKHSTAN

L4L revenue growth 27%

More growth in new venue

L4L revenue decline (13%)

Significant timing differencesUZBEKISTAN

22

Divisional Analysis...........................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Eastern & Southern Europe

2013 2012

m² ‘000 252 269

Revenue £29m £28m

L4L revenue growth 2%

TURKEY

Beauty and Auto well integratedUKRAINE

L4L revenue flat

Portfolio rationalisation

Acquisition of Beauty Eurasia

Looking forward... More potential bolt-ons in Turkey

23

Divisional Analysis...........................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

UK

2013 2012

m² ‘000 40 40

Revenue £10m £9m

L4L revenue growth 2%

Niche extensions trading well/mid market struggleUK

Looking forward... Extending niches overseas

Expansion overseas – The Hub (Hong Kong)

24

Divisional Analysis...........................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Asia

2013 2012

m² ‘000 18 18

Revenue £3m £2m

Looking forward... Geo-cloning & more acquisitions

INDIAABEC sales performing well

Re-focussing of ITE’s existing portfolio

Acquisition of ECMI & TradelinkSE ASIA

ECMI launch vehicle for clone events

Acquisition of ChinacoatCHINA

More acquisitions in pipeline

25

Summary ...............................................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Key messages

Good trading conditions & business momentum

Asian business to grow further

Investment in infrastructure & management

Building strength in key industry verticals

Strong balance sheet

26

Thank you.............................................................

Q & A....................................

Appendices...................................................................

2013

04

Appendices .........................................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Shareholder Structure at 27 October 2013

% No. of Shares(millions)

BlackrockSchrodersStandard LifeThreadneedle InvestmentsScottish WidowsLegal and GeneralOld MutualNBIMDirectors

ESOTOther Institutions and individuals

15.112.9 6.6 6.5 4.2 4.2 3.8 3.3 1.3

1.543.9

39.3 32.2 16.3 16.1 10.5 10.5 9.5 8.2 3.2

3.7107.8

Total Shares in issue 100 249.7

Options in the money: 0.1 0.2

Management including options in the money 1.6 3.4

Free float (Excluding Directors & ESOT) 97.2

Average daily trading volume (6 months) 0.3

30

Appendices .........................................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Key Exhibitions (in 2013 gross profit order)

Rank Event Location 2013 m² sold

2012 m² sold

1 MosBuild Moscow 68,700 66,100

2 MIOGE Moscow 24,000 22,800*

3 Turkeybuild (YAPI) Istanbul 36,200 36,100

4 World Food Moscow Moscow 24,900 24,400

5 Moscow International Travel & Tourism (MITT) Moscow 19,500 20,000

6 MODA UK (Spring & Autumn) Birmingham 35,400 36,000

* Last edition in 2011

Events by GP (2013):

45%31%

13%11%

31

Appendices .........................................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Consolidated Balance SheetSept -13

audited £‘mSept -12

audited £‘m

Non Current Assets

• Goodwill & Intangibles 122.3 131.0

• Other non-current assets 26.0 10.9

148.3 141.9

Current Assets

• Debtors due within 1 year 54.7 53.8

• Net Cash 23.5 13.0

78.2 66.8

Creditors

• Deferred Revenue & Creditors 100.9 92.4• Deferred Consideration 4.1 0.9

• Deferred Tax 11.4 14.4

• Provisions 0.8 1.2

117.2 108.9

Net Assets 109.3 99.8

£46.2m £38.6m

32

Appendices .........................................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Puts & calls £m Financial Years

Turkeybuild (20%) 4.6 2014

Summit (Turkmenistan) 1.0 2014

Scoop (Moda) (60%) 1.6 2014

ABEC (for extra 32%) TBC 2016

Tradelink 1.4 2015

ECMI TBC 2017 & 2019

£TBC

Future Consideration at Sept 2013

Deferred Consideration £m Financial Years

Jacket Required (UK) 0.3 2014

Beautex 0.2 2014

Tradelink 2.6 2014

ECMI 0.9 2014

Lentewenc 0.1 2014

4.1

33

Appendices .........................................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Venue relationships

Venue LocationTheme

ProtectionRates

AgreedPrepayments30 Sept 2013

Expocentre Moscow 2017 2015 -

Crocus Moscow 2015 2015 -

ExpoForum St Petersburg 2017 2017 -

Expocentre Novosibirsk 2021 2021 £2.2m

Expo City Yug Krasnodar 2016 2016 £0.4m

Atakent Almaty 2017 2017 £0.0m

IEC Kiev 2014 2014 £1.0m

Tuyap Istanbul 2014 2014 -

Uzexpocentre Tashkent 2019 2019 £0.2m

Expocentre Baku 2015 2015 £0.3m

TOTAL £4.1m

34

Appendices .........................................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

Russia

Central Asia & Caucasus

2013 2012

62% 61%

15% 16%

Eastern & Southern Europe

15% 16%

UK & Western Europe

6% 6%

Asia 2% 1%

Construction

Oil & Gas

2013 2012

37% 42%

13% 7%

Food 10% 10%

Travel 8% 9%

Motor 5% 5%

Fashion

IT& Medical

Other

6% 6%

5% 5%

16% 16%

Revenue by Sector and Region

35

Financial Results 2013...................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

2009 2010 2012

£M

20132011

£18M£20M

£24M

£30M

£26M

5

10

15

20

35

30

25

Overheads as % of revenue and Gross Profit

40

%

5

10

15

20

35

30

25

40

Overheads

% of Revenue

% of Gross Profit

36

Divisional Analysis...........................................................................................................................

ITE Group plc – Preliminary Results for the year ended 30 September 2013

GDP Growth in ITE’s Markets

2014 GDP growth forecast %

2015GDP growth forecast %

Russia 3.0 3.5

Kazakhstan 5.2 6.1

Azerbaijan 5.6 4.8

Uzbekistan 6.5 6.0

Ukraine 1.5 1.5

Turkey 3.5 4.3

UK 1.9 2.0

India 5.1 6.3

China 7.3 7.0

Source: IMF World Economic Outlook Database, Oct 2013

37