preliminary determination in antidumping …

TRANSCRIPT

(NON–CONFIDENTIAL)

Government of Pakistan

National Tariff Commission

REPORT

ON

PRELIMINARY DETERMINATION IN ANTIDUMPING

INVESTIGATION AGAINST DUMPED IMPORTS OF

POLYESTER STAPLE FIBRE (NOT EXCEEDING 2.0

DENIER) INTO PAKISTAN ORIGINATING IN AND/OR

EXPORTED FROM CHINESE TAIPEI, THE REPUBLIC OF

INDONESIA AND THE KINGDOM OF THAILAND

A.D.C No. 59/2021/NTC/PSF

July 30, 2021

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

1

The National Tariff Commission (the “Commission”) having regard to the Anti-

Dumping Duties Act, 2015 (the “Act”) and the Anti-Dumping Duties Rules, 2001 (the

“Rules”) relating to investigation and determination of dumping of goods into the Islamic

Republic of Pakistan (“Pakistan”), material injury to the domestic industry caused by

such imports, and imposition of antidumping duties to offset the impact of such injurious

dumping, and to ensure fair competition thereof and to the Agreement on

Implementation of Article VI of the General Agreement on Tariffs and Trade 1994 (the

“Agreement on Antidumping”).

2. The Commission is conducting this investigation, on imports of Polyester Staple

Fibre, PCT No. 5503.2010 (Not Exceeding 2.0 Denier & Excluding Colored Polyester

Staple Fiber and Regenerated Polyester Staple Fiber) (“PSF”) into Pakistan Originating

in and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of

Thailand under the Act and the Rules. The Commission has made preliminary

determination in this investigation under Section 37 of the Act. This report on

preliminary determination has been issued in accordance with the Rule 10 of the Rules.

3. In terms of Section 37 of the Act, the Commission shall make a preliminary

determination of dumping and injury, if any, not earlier than sixty days and not later than

one hundred and eighty days, after initiation of an investigation. Such preliminary

determination shall be based on the information available to the Commission at that time.

This investigation was initiated on February 06, 2021. The preliminary determination is

based on the information available to the Commission at this time.

A. PROCEDURE

4. The procedure set out below has been followed with regard to this investigation.

5. Receipt of Application:

5.1 On December 14, 2020, the Commission received a written application under

Section 20 of the Act from M/s Ibrahim Fibres Limited, and M/s ICI Pakistan Limited,

(the “Applicants”). The Applicants have alleged that PSF originating in and/or exported

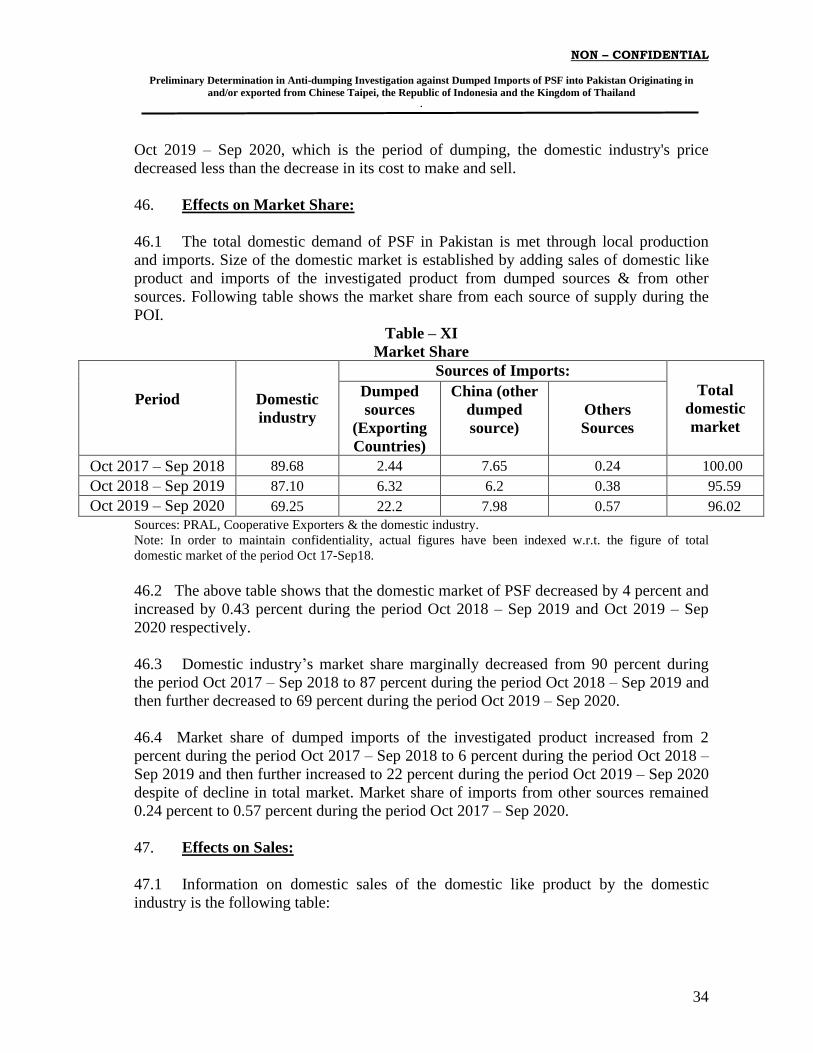

from Chinese Taipei, the Republic of Indonesia, the Republic of Korea and the Kingdom

of Thailand is being dumped into Pakistan, which has caused and is causing material

injury to the domestic industry producing PSF.

5.2 The Commission informed the Diplomatic Missions of Chinese Taipei, the

Republic of Indonesia, the Republic of Korea and the Kingdom of Thailand through note

verbal(s) dated December 18, 2020 of the receipt of application in accordance with the

requirements of Section 21 of the Act.

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

2

6. Evaluation and Examination of the Application:

6.1 The examination of the application showed that it met the requirements of Section

20 of the Act as it contained sufficient evidence of dumping of PSF into Pakistan from

Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand and material

injury to the domestic industry caused therefrom. Requirements of Rule 3 of the Rules,

which relate to the submission of information prescribed therein were also found to have

been met.

6.2 The Commission found that volume of alleged dumped imports of investigated

product from the Republic of Korea account for less than three percent of total imports of

a like product i.e. 2.03 percent, therefore anti-dumping investigation will not be initiated

against the Republic of Korea.

7. The Domestic Industry:

7.1 Section 2(d) of the Act defines domestic industry as:

“domestic industry” means the domestic producers as a whole of a domestic like

product or those of them whose collective output of that product constitutes a major

proportion of the total domestic production of that product, except that when any such

domestic producers are related to the exporters or importers, or are themselves

importers of the allegedly dumped investigated product in such a case “domestic

industry” shall mean the rest of the domestic producers”. Explanation.- For the purposes

of this clause, producers shall be deemed to be related to exporters or importers only if;

(i) one of them directly or indirectly controls the other;

(ii) both of them are directly or indirectly controlled by the same third person;

or

(iii) together they directly or indirectly control a third person;

Provided that there are grounds for believing or suspecting that the effect of the

relationship is such as to cause the producer concerned to behave differently from non-

related producers and for that purpose one shall be deemed to control another when the

former is legally or operationally in a position to exercise restraint or direction over the

latter”.

7.2 The domestic PSF manufacturing industry comprises of three Units i.e. M/s. ICI

Pakistan Limited, M/s Ibrahim Fibers Limited and M/s Rupali Polyester Limited having

installed production capacity of 537,347 MT per annum on three shifts basis. The

Applicants constitute 95 percent of the domestic production and their installed production

capacity is 512,600 MT per annum on three shifts basis.

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

3

7.3 The importers have objected the initiation of the investigation on the grounds that

one of the Applicant namely M/s ICI Pakistan Limited did not qualify as domestic

industry in view of the exceptions contained in the definition of the term ‘domestic

industry’ in Section 2(d) of the Act. They have referred to provision of Section 2(d) of

the Act and Article 4 of the Agreement on Anti-dumping in order to explain the

requirements of control for exclusion from the definition of domestic industry. Section

2(d) reads as follows;

“Producers shall be deemed to be related to exporter or importer only if:

(a) One of them is directly or indirectly controls the other;

(b) Both of them are directly or indirectly controlled by a third person; or

(c) Together they directly or indirectly control a third person,

Provided that there are grounds for believing or suspecting that the effect of the

relationship is such as to cause the producer concerned to behave differently from

non-related producers. For the purpose of this paragraph, one shall be deemed to

control another when the former is legally or operationally in a position to exercise

restraint or direction over the later.”

7.4 In this regard it is held that the exclusion of any producer from domestic industry

is dependent upon the expected behavior of the firm concerned. In case it is suspected

that the firm would jeopardize the interest of other domestic producers by way of its

interests in imports, only then such firm would be excluded from the domestic industry. It

is also important to note that the expected behavior of the firm concerned is in relation to

anti-dumping application and not the marketing behavior of the firm. In this regard the

practice and standards being followed by other traditional users of anti-dumping law and

the history of the WTO negotiations has been considered by the Commission. In this

regard a famous lawyer in the field of antidumping with the name of Van Beal & Bellis

in his book titled “Antidumping and other Trade Protection Laws of the EC” has clarified

this issue of imports by related companies with reference to the EC (European

Commission) practice. As per page 202 of the book, “A community producer is held to

be an importer regardless of whether it imports directly or through related trading

companies. However, when assessing its conduct, indirect imports are relevant only as

long as the related importer supplies the community producer or acts in coordination with

it”. A reference is also made to EU antidumping investigation of “Quarto Plates” in

which the Commission found that none of the producers had themselves imported the

products. All imports were carried out by a trading company belonging to the same

corporate group as one complaining producer. However, this company was found to act

independently. Based on the structure of the group, each company would maintain its

own financial accounts, submit separate annual reports and have no profit or loss transfer

agreement with the holding company. Furthermore, the two companies filed separate

income tax returns, has its own board of directors and conduct business relations with

other companies at arm’s length. The EC therefore, concluded that the imports could not

affect the status of the producers concerned.

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

4

7.5 In this regard a reference to “A Handbook of Anti-Dumping Investigations” by

Judith Czako, john Human and Jorge Miranda would not be out of place. The handbook

lists following factors for deciding upon the exclusion of producer/related producer from

the domestic industry:

“The basis of whether related parties should be excluded typically arises in the

context of (a) multinational enterprises with both foreign and domestic production

of goods at issue in the investigation, or (b) the entities that import the allegedly

dumped goods.”

“Among the criteria that have been considered by members in deciding whether to

exclude related parties are:

i. Whether imports of the product in question by the related producers allow them to

benefit, or serve to shield them, from the effects of dumping;

ii. Whether exclusion of related parties would unduly skew the data for the

remaining members of the industry;

iii. The level of long-term nature of the commitment shown by the producer to

domestic production, as opposed to importing activities; and

iv. The ratio of import shipments to domestic production for the related producers.

7.6 It is also to be noted that the expected behavior is dependent upon the interest of

the producer concerned. In this regard it is held that this provision may hold good when

the related parties of M/s ICI Pakistan Limited have imported the product concerned at

lower prices from the dumped sources and has sold either to ICI Pakistan Limited or in

the domestic market under the instructions of ICI Pakistan Limited. M/s Gadoon Textiles

Mills and M/s Yunus Textiles Mills imported *** MT from the Exporting Countries for

their own use. The import was not under the instruction from ICI Pakistan Limited nor

sold the imported product to ICI Pakistan Limited or in the domestic market. ICI Pakistan

Limited is an independent entity maintaining its own financial accounts, submits separate

income tax returns, has no profit and loss transfer agreement with M/s Gadoon Textiles

Mills and M/s Yunus Textiles Mills. M/s ICI Pakistan Ltd, M/s Gadoon Textiles Mills

and M/s Yunus Textiles Mills are the part of Yunus Brothers Group and have few

common Directors. Therefore, there are no grounds to exclude ICI Pakistan Limited from

the definition of the domestic industry. Above all, ICI Pakistan Limited is the major

producer and its share in domestic production during the POI was 31%. Surely it cannot

work differently than the other producers of PSF.

7.7 Based on the above referred proviso, any related producer will only be excluded

from the definition of the domestic industry when there are grounds to believe that the

relationship has caused the related producer to behave differently from non-related

producer. When it is established that related producer has not behaved differently from

non-related producer, it cannot be excluded from the definition of the domestic industry.

The proviso given in the Section is of great importance as the relevant Section only

becomes operative when the given proviso holds good.

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

5

7.8 Hence by ignoring the provisions given in a particular Section, the respective

Section itself remains inoperative in a particular situation. Therefore, while defining the

domestic industry, one cannot ignore the proviso to Section 2(d) of the Act. Had there

been no importance of such proviso, different Antidumping Authorities would not have

developed comprehensive criteria for the evaluation of whether the related producer

behaves differently from non-related producer or not.

7.9 It is therefore, held that in spite of the fact that M/s ICI Pakistan Limited is

assumed as associated producer, even then, the Commission has, determined that it

cannot be excluded from the definition of the domestic industry in the light of the above

and foregoing explanations.

8. Standing of the Application:

8.1 In terms of Section 24(1) of the Act,

“…. an application shall be considered to have been made by or on behalf of

the domestic industry only if it is supported by those domestic producers whose

collective output constitutes more than fifty percent of the total production of a

domestic like product produced by that portion of the domestic industry

expressing either support for or opposition to the application.”

Furthermore, Section 24(2) of the Act provides that:

“….. no investigation shall be initiated when domestic producers expressly

supporting an application account for less than twenty five percent of the total

production of the domestic like product produced by the domestic industry."

8.2 The Applicants are major domestic producers of PSF in Pakistan. The Applicants

produced 95 percent of total domestic production of PSF during the period from October

01, 2019 to September 30, 2020. Details of the production of PSF by the domestic

industry are as follows:

Table – I

Standing of Application

S. No Unit Name

Share in total

production

(% of total)

Status

i. M/s ICI Pakistan Limited 31% Applicant

ii. M/s Ibrahim Fibers Limited 64% Applicant

iii. M/s Rupali Polyester Limited 5% Supporting

Total 100% Source: the domestic industry.

8.3 The Applicants represent 95% of the total domestic production by the domestic

industry and supported by Rupali Polyester Ltd. which accounts for 5% of total domestic

production. The Application is supported by 100% of the producers who are expressing

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

6

their opinion on application thus the standing requirements as given in the Section 24 of

the Act are met and it is determined that the application is made by or on behalf of the

domestic industry.

8.4 It may be noted that Khalis Fibres Ltd, T & N Group and EVM were excluded

from the domestic manufacturers list as all three of these domestic manufacturers produce

regenerated Polyester Staple Fiber which does not come under the scope of the

investigated product. On the other hand, Pakistan Synthetic Ltd. from October 2016

onwards does not produce Polyester Staple Fiber and has moved it production to other

products which include PET resin, preforms, plastic and crown caps.

9. Applicants’ Views:

9.1 The Applicants, inter alia, raised the following issues in application regarding

alleged dumping of PSF and material injury to the domestic industry caused therefrom:

i. PSF imported from Chinese Taipei, the Republic of Indonesia, the

Republic of Korea and the Kingdom of Thailand into Pakistan and PSF

produced in Pakistan by the domestic industry are like products;

ii. Exporters/producers from Chinese Taipei, the Republic of Indonesia, the

Republic of Korea and the Kingdom of Thailand are exporting PSF to

Pakistan at dumped prices; and

iii. Exports of PSF by the exporters/producers from Chinese Taipei, the

Republic of Indonesia, the Republic of Korea and the Kingdom of

Thailand to Pakistan at dumped prices has caused and is causing material

injury to the domestic industry producing PSF.

9.2 The Applicants requested the Commission to address the injury, caused to the

domestic industry, by initiation of an anti-dumping investigation against dumped imports

of PSF from Chinese Taipei, the Republic of Indonesia, the Republic of Korea and the

Kingdom of Thailand and impose anti-dumping duties on these alleged dumped imports.

It has also been requested that provisional anti-dumping measures may be imposed to

prevent injury being caused during the course of investigation.

10. Exporters/Producers of PSF:

The Applicants have identified 41 exporters/ producers involved in alleged

dumping of the investigated product from Chinese Taipei, Republic of Indonesia,

Republic of Korea and Kingdom of Thailand. The Applicants have stated that there may

be other exporters/ producers of the investigated product, which are not known to them,

therefore, the Applicants have requested for imposition of antidumping duty on all

imports of the investigated product originating in and/or exported from Chinese Taipei,

the Republic of Indonesia, the Republic of Korea and Kingdom of Thailand.

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

7

11. Anti-dumping Duties In-place on Dumped Imports of PSF:

11.1 The Commission imposed following definitive anti-dumping duties on dumped

imports of PSF, importable from the People’s Republic of China (“China”), for a period

of five years effective from October 03, 2015 on the basis that the domestic industry

suffered material injury during the POI:

Table – II

Definitive Anti-Dumping Duty Rates

11.2 The Commission under Sections 58 and 59 of the Act, 2015 initiated sunset and

change circumstance review on October 02, 2020 to determine whether expiry of the

above anti-dumping duty imposed on dumped imports of PSF from China would likely to

lead to continuation or recurrence of dumping and injury, and whether change of

circumstances warrants continuation, removal or amendment of the anti-dumping duty.

11.3 The sunset and change circumstances reviews are still under process.

12. Initiation of Investigation:

12.1 The Commission, in accordance with Section 23 of the Act examined the

accuracy and adequacy of the evidence provided in application, and established that the

volume of alleged dumped imports of investigated product from the Republic of Korea

found to account for less than three percent of total imports of a like product i.e. 2.03

percent, therefore anti-dumping investigation was not initiated against the Republic of

Korea. Further, there is sufficient evidence of alleged dumping of PSF into Pakistan from

Chinese Taipei, the Republic of Indonesia, and the Kingdom of Thailand (the “Exporting

Countries”) and consequent material injury to the domestic industry. Accordingly, the

Commission issued a notice of initiation in accordance with Section 27 of the Act, which

was published in the Official Gazette1 of Pakistan and in two widely circulated national

newspapers2 (one in English language and one in Urdu Language) February 06, 2021.

Investigation concerning alleged dumped imports of PSF into Pakistan {classified under

1 The official Gazette of Pakistan (Extraordinary) dated February 06, 2021. 2 The ‘Business Recorded” and the ‘Daily Assas” of February 06, 2021. 3 PCT heading in Pakistan is equivalent to Harmonized Commodity Description and Coding System up to six-digit level.

Exporter/ Producer from China Antidumping

Duty Rates (%)

Shanghai Hengyi Polyester Fiber Co., Limited 7.88

Jiangyin Huahong Chemical Fiber Co., Limited 2.82

Jiangyin Hailun Chemical Fiber Co., Limited 8.22

Xiamen Xianglu Chemical Fiber Co. Limited 7.81

Fujian Zhengqi High-Tech Fiber Technology Co. Limited 7.72

All other exporters 11.51

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

8

PCT No3. 5503.2010} originating in and/or exported from the Exporting Countries was

thus initiated on February 06, 2021.

12.2 In pursuance of Section 27 of the Act, the Commission notified the Diplomatic

Missions of the Exporting Countries of the initiation of investigation (by sending a copy

of the notice of initiation) on February 08, 2021 with a request to forward it to all

exporters/producers involved in production, sales and export of PSF from their respective

countries. Copy of the notice of initiation was also sent on February 11, 2021 to known

exporters/producers of PSF from the Exporting Countries whose addresses were available

with the Commission with a request to be registered as an interested party in the

investigation with-in 15 days of publication of the notice. Copy of the notice of initiation

was also sent to known Pakistani importers and the Applicants on February 11, 2021.

12.3 In accordance with Section 28 of the Act, on February 11, 2021 the Commission

sent copy of full text of the written application (non-confidential version) and Exporter’s

Questionnaire to the exporters/producers of the Exporting Countries. On February 11,

2021, copy of the full text of the written application along with Exporter’s Questionnaire

was also sent to Diplomatic Missions of the Exporting Countries in Pakistan with a

request to forward it to all exporters/producers involved in production and/or sale/export

of PSF from their respective country. The Importer’s Questionnaire was also sent to the

importers of PSF on February 11, 2021.

13. Investigated Product, Domestic Like Product and Like Product:

13.1 Section 2 of the Act defines investigated product, domestic like product and like

product as follows:

i. Investigated Product:

“a product, which is subject to an antidumping investigation as described

in the notice of initiation of the investigation”.

ii. Domestic Like Product:

“means a like product that is produced by the domestic industry”.

iii. Like Product:

“a product which is alike in all respects to an investigated product or, in

the absence of such a product, another product which, although not alike

in all respects, has characteristics closely resembling those of the

investigated product”.

13.2 For the purposes of this investigation and given the definitions set out above,

investigated product, domestic like product and like product are identified as follows:

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

9

13.3 Investigated Product:

13.3.1 The investigated product is Polyester Staple Fibre (Not Exceeding 2.0 Denier &

Excluding Colored Polyester Staple Fiber and Regenerated Polyester Staple Fiber)

originating in and/or exported from the Exporting Countries to Pakistan. It is classified

under PCT No. 5503.2010. It is generally used in production of blended yarn and pure

polyester sewing thread. The blended yarn is used to produce woven and knitted fabrics.

13.3.2 Tariff structure for the financial year 2021-22 applicable on import of PSF is

given in the following table:

Table – III

Tariff Structure of Polyester Staple Fiber

Tariff Structure 2021 – 22

PCT

Code

Description CD ACD RD Concessions/

FTA Rates

5503.2010 Synthetic staple fibers, not carded,

combed or otherwise processed for

spinning

-of polyesters

--- of polyesters not exceeding 2.22

decitex

11% 2%* 0%

Fifth sch

Pt_III CD 7%,

SAFTA 5%

* exempted in 5th schedule

13.4 Domestic Like Product:

13.4.1 Under the Section 2(f) of the Act, “Domestic Like Product” means a like product

that is produced by the domestic industry.

13.4.2 The domestic like product is Polyester Staple Fibre (Not Exceeding 2.0 Denier &

Excluding Colored Polyester Staple Fiber and Regenerated Polyester Staple Fiber),

produced by the domestic industry. The domestic like product is also classified under

PCT No. 5503.2010. The domestic like product is generally used in production of

blended yarn and Pure Polyester sewing thread. The blended yarn is used to produce

woven and knitted fabrics Major uses of the domestic like product are, therefore,

identical to those of the investigated product.

13.5 Like Product:

Polyester Staple Fibre (Not Exceeding 2.0 Denier & Excluding Colored Polyester

Staple Fiber and Regenerated Polyester Staple Fiber) produced by the domestic industry

and imported from the Exporting Countries is comparable in terms of physical and

chemical characteristics, product specifications, chemical formulation, end uses and tariff

classification of the goods etc. Investigated product and domestic like product are

technically and commercially identical. Domestically produced PSF and imported PSF

are classified under the same PCT/HS Heading No. 5503.2010.

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

10

13.6 In light of the above, the Commission has determined that the investigated

product and the domestic like product are like products.

14. Period of Investigation:

14.1 In terms of Section 36 of the Act, Period of Investigation (hereinafter referred to

as “POI”) is:

i. “for the purposes of an investigation of dumping, an investigation

period shall normally cover twelve months preceding the month of

initiation of the investigation for which data is available and in no case

the investigation period shall be shorter than six months.”

ii. “for the purposes of an investigation of injury, the investigation period

shall normally cover thirty-six months:

“Provided that the Commission may at its sole discretion, select a shorter

or longer period if it deems it appropriate in view of the available

information regarding domestic industry and an investigated product”.

14.2 The Commission received the application on December 14, 2020 and initiated the

investigation on February 06, 2021. The Applicants have provided the information/data

and evidences up till September 30, 2020 in the application. Therefore, to fulfill the

requirement of Section 36 of the Act, the POI selected by the Commission for dumping

and injury are, as follows:

For determination of dumping: From October 01, 2019 to September 30, 2020

For determination of injury: From October 01, 2017 to September 30, 2020

15. Information/Data Gathering:

15.1 The Commission sent questionnaires on February 11, 2021 to the Diplomatic

Missions of the Exporting Countries in Islamabad with a request to forward it to all

exporters/ producers of the investigated product in their respective country. Exporter’s

questionnaire was also sent directly to exporters/ producers based in the Exporting

Countries whose addresses were available to the Commission on February 11, 2021 for

collection of data and information necessary for this investigation. The exporters/

producers were asked to supply information within 37 days of the dispatch of

questionnaire.

15.2 The following six exporters/ producers responded to the Commission’s request for

supplying information on the prescribed Exporter’s Questionnaire and requested for

extension in time period (beyond 37 days) for submission of information:

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

11

i. Chung Shing Textile Marketing Limited, Chinese Taipei;

ii. PT. Indorama Polychem, Indonesia;

iii. PT. Indorama Synthetics TBK, Indonesia;

iv. Indorama Polyester Industries Public Company Limited, Thailand;

v. Kangwal Polyester Co. Limited, Thailand; and

vi. Sunflag Thailand Limited, Thailand.

15.3 After taking into account the due cause shown by these exporters/ producers in

their requests, the Commission acceded to the requests and granted extension in time

period for submission of information on Exporter’s Questionnaire till April 30, 2021.

Filled-in Exporter’s Questionnaires from these exporters were received at the

Commission on April 30, 2021. Upon examination of the information received from these

exporters/ producers, certain deficiencies were found in the information supplied. These

deficiencies were communicated to the exporters/ producers and were requested to supply

the deficient information. The same was provided to the Commission.

15.4 The Commission also sent Questionnaire on May 03, 2021 to Rupali Polyester

Pvt Limited, which is other domestic producer of PSF. Rupali Polyester Pvt Ltd provided

the data/information to the Commission on May 21, 2021

15.5 On February 11, 2021, questionnaires were sent to Pakistani importers of the

investigated product known to the Commission and the importers were asked to respond

to the Commission within 37 days of the dispatch of the questionnaires. Following

importers provided the data to the Commission:

i. M/s Feroze 1888 Mills Limited;

ii. M/s Naveena Group Export Limited;

iii. M/s Master Textile Mills Limited;

iv. M/s Masood Textiles Mills Limited;

v. M/s N.M Corporation Private Limited;

vi. M/s Nishat Chunian Limited;

vii. M/s Fazal Cloth Mills Limited; and

viii. M/s Ahmed Fine Textile Mills Limited.

ix. M/s Ali Nawaz Textile (Pvt.) Limited.

15.6 No other exporters/producers from the Exporting Countries and importers

mentioned above have responded to the Commission and did not provide requisite

information within stipulated time period. Therefore, letters were issued to the non -

cooperating exporters/producers and importers on June 15, 2021 explaining that, as no

response of the questionnaire is submitted by them, therefore, Commission is constrained

to make preliminary and/or final determination in this investigation on the basis of “Best

Information Available” in terms of Section 32 of the Act.

15.7 The Commission has access to database of import statistics of Pakistan Revenue

Automation Limited (“PRAL”), the data processing arm of the Federal Board of

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

12

Revenue, Government of Pakistan. For the purpose of this preliminary determination the

Commission has used import data obtained from PRAL in addition to the information

provided by the Applicants, the exporters and the importers.

15.8 Interested parties were also invited to make their views/comments and submit

information (if any) relevant to this investigation within 45 days of initiation of

investigation. Ministry of Trade, Government of Indonesia and Khyber-Pakhtunkhwa

Textiles Mills Association has made comments /submitted information which has also

been considered while making this preliminary determination.

15.9 Thus, the Commission has sought from all available sources the relevant data and

information deemed necessary for the purposes of preliminary determination of dumping

and injury therefrom in this investigation.

16. Questionnaire(s) Response from Chinese Taipei:

Questionnaire Response by Chung Shing Textile Marketing Limited, Chinese

Taipei

16.1 The Commission sent the Exporter’s Questionnaire to Chung Shing Textile

Marketing Limited, Chinse Taipei (“Chung Shing”) on February 11, 2021. Chung Shing

in its e-mail dated April 09, 2021 applied to the Commission for extension of time period

for submission of response to questionnaire for 37 days. The Commission after

considering the reasons given in the request for extension, granted the extension for 25

days vide its letter/email dated April 09, 2021. Chung Shing vide its e-mail dated April

14, 2021 again requested the Commission for extension of time period for submission of

response to questionnaire. The Commission after considering the reasons given in the

request for extension, granted the extension for 15 days vide its letter/email dated April

19, 2021. Chung Shing response was received in the Commission on April 29, 2021.

16.2 The information submitted by Chung Shing in response to the questionnaire was

analyzed at the Commission and certain deficiencies were identified. Accordingly, those

deficiencies were communicated to Chung Shing vide the Commission’s letter dated May

31, 2021. Chung Shing was asked to provide the deficient information/data by June 07,

2021. Chung Shing responded to the deficiencies vide its e-mail dated June 15, 2021. The

information provided by Chung Shing was analyzed and again found deficient. The

Commission informed Chung Shing with the deficiencies on June 17, 2021. Chung Shing

Responded to the deficiencies on June 25, 2021. However, the same was still deficient

and the Commission vide its letter dated July 01, 2021 asked for the deficient

information. Chung Shing response in this regard was received on July 08, 2021 which is

still deficient.

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

13

17. Questionnaire(s) Response from the Republic of Indonesia:

17.1 Questionnaire Response by PT. Indorama Polychem, Indonesia

17.1.1 The Commission sent Exporter’s Questionnaire to PT. Indorama Polychem,

Indonesia (“Indorama Polychem”) on February 11, 2021. Indorama Polychem applied to

the Commission in its letter dated March 18, 2021 for extension of time period for

submission of response to questionnaire for one month. The Commission granted

extension for two weeks vide its letter dated March 29, 2021 after considering the reasons

given in the request for extension. Indorama Polychem vide its letter dated April 02, 2021

again requested the Commission for extension of time period for submission of response

to questionnaire for 2 weeks. The Commission after considering the reasons given in the

request for extension granted extension for 10 days vide its letter dated April 09, 2021.

Indorama Polychem vide its letter dated April 12, 2021 requested the Commission for

extension of time period for submission of response to questionnaire for two weeks.

The Commission after considering the reasons given in the request for extension granted

final extension for two weeks vide its letter dated April 19, 2021. Indorama Polychem

response was received in the Commission on April 30, 2021.

17.1.2 The information submitted by Indorama Polychem in response to the

questionnaire was analyzed at the Commission and certain deficiencies were identified.

Accordingly, those data deficiencies were communicated to it vide Commission’s letter

dated June 16, 2021. Indorama Polychem was asked to provide the deficient

information/data no later than 09 days, so as to enable the Commission to consider and

analyze the same for the purposes of this investigation. Indorama Polychem responded to

the deficiencies vide its letter dated June 25, 2021. However, the same was still deficient

and the Commission vide its letter dated July 08, 2021 asked for the deficient

information. Indorama Polychem response in this regard was received on July 13, 2021.

17.2 Questionnaire Response by PT. Indorama Synthetics TBK, Indonesia

17.2.1 The Commission sent Exporter’s Questionnaire to PT. Indorama Synthetics TBK,

Indonesia (“Indorama Synthetics”) on February 11, 2021. Indorama Synthetics applied to

the Commission in its letter dated March 18, 2021 for extension of time period for

submission of response to questionnaire for one month. The Commission granted

extension for two weeks vide its letter dated March 29, 2021 after considering the reasons

given in the request for extension. Indorama Synthetics vide its letter dated April 02,

2021 again requested the Commission for extension of time period for submission of

response to questionnaire for 2 weeks. The Commission after considering the reasons

given in the request for extension granted extension for 10 days vide its letter dated April

09, 2021. Indorama Synthetics vide its letter dated April 12, 2021 requested the

Commission for extension of time period for submission of response to questionnaire for

2 weeks. The Commission after considering the reasons given in the request for extension

granted final extension for 2 weeks vide its letter dated April 19, 2021. Indorama

Synthetics response was received in the Commission on April 30, 2021.

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

14

17.2.2 The information submitted by Indorama Synthetics in response to the

questionnaire was analyzed at the Commission and certain deficiencies were identified.

Accordingly, those data deficiencies were communicated to it vide Commission’s letter

dated June 16, 2021. Indorama Synthetics was asked to provide the deficient

information/data no later than 09 days, so as to enable the Commission to consider and

analyze the same for the purposes of this investigation. Indorama Synthetics responded to

the deficiencies vide its letter dated June 25, 2021. However, the same was still deficient

and the Commission vide its letter dated July 08, 2021 asked for the deficient

information. Indorama Synthetics response in this regard was received on July 13, 2021.

18. Questionnaire(s) Response from the Kingdom of Thailand:

18.1 Questionnaire Response by Indorama Polyester Industries Public Company

Limited, Thailand

18.1.1 The Commission sent Exporter’s Questionnaire to Indorama Polyester Industries

Public Company Limited, Thailand (“Indorama Polyester”) on February 11, 2021.

Indorama Polyester applied to the Commission in its letter dated March 18, 2021 for

extension of time period for submission of response to questionnaire for one month. The

Commission granted extension for two weeks vide its letter dated March 29, 2021 after

considering the reasons given in the request for extension. Indorama Polyester vide its

letter dated April 02, 2021 again requested the Commission for extension of time period

for submission of response to questionnaire for 2 weeks. The Commission after

considering the reasons given in the request for extension granted extension for 10 days

vide its letter dated April 09, 2021. Indorama Polyester vide its letter dated April 12,

2021 requested the Commission for extension of time period for submission of response

to questionnaire for 2 weeks. The Commission after considering the reasons given in the

request for extension granted final extension for 2 weeks vide its letter dated April 19,

2021. Indorama Polyester response was received in the Commission on April 30, 2021.

18.1.2 The information submitted by Indorama Polyester in response to the questionnaire

was analyzed at the Commission and certain deficiencies were identified. Accordingly,

those data deficiencies were communicated to it vide Commission’s letter dated June 16,

2021. Indorama Polyester was asked to provide the deficient information/data no later

than 09 days, so as to enable the Commission to consider and analyze the same for the

purposes of this investigation. Indorama Polyester responded to the deficiencies vide its

letter dated June 25, 2021. However, the same was still deficient and the Commission

vide its letter dated July 08, 2021 asked for the deficient information. Indorama Polyester

response in this regard was received on July 13, 2021.

18.2 Questionnaire Response by Kangwal Polyester Co. Limited, Thailand

18.2.1 The Commission sent Exporter’s Questionnaire to Kangwal Polyester Co.

Limited, Thailand (“Kangwal Polyester”) on February 11, 2021. Kangwal Polyester

applied to the Commission in its letter dated March 18, 2021 for extension of time period

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

15

for submission of response to questionnaire for one month. The Commission granted

extension for two weeks vide its letter dated March 29, 2021 after considering the reasons

given in the request for extension. Kangwal Polyester vide its letter dated April 02, 2021

again requested the Commission for extension of time period for submission of response

to questionnaire for 2 weeks. The Commission after considering the reasons given in the

request for extension granted extension for 10 days vide its letter dated April 09, 2021.

Kangwal Polyester vide its letter dated April 12, 2021 requested the Commission for

extension of time period for submission of response to questionnaire for 2 weeks. The

Commission after considering the reasons given in the request for extension granted final

extension for 2 weeks vide its letter dated April 19, 2021. Kangwal Polyester response

was received in the Commission on April 30, 2021.

18.2.2 The information submitted by Kangwal Polyester in response to the questionnaire

was analyzed at the Commission and certain deficiencies were identified. Accordingly,

those data deficiencies were communicated to it vide Commission’s letter dated June 16,

2021. Kangwal Polyester was asked to provide the deficient information/data no later

than 09 days, so as to enable the Commission to consider and analyze the same for the

purposes of this investigation. Kangwal Polyester responded to the deficiencies vide its

letter dated June 25, 2021.

18.3 Questionnaire Response by Sunflag Thailand Limited, Thailand

18.3.1 The Commission sent Exporter’s Questionnaire to Sunflag Thailand Limited,

Thailand (“Sunflag”) on February 11, 2021. Sunflag applied to the Commission in its e-

mail dated March 16, 2021 for extension of time period for submission of response to

questionnaire for 30 days. The Commission granted extension for two weeks vide its

letter dated March 29, 2021 after considering the reasons given in the request for

extension. Sunflag vide its e-mail dated April 03, 2021 again requested the Commission

for extension of time period for submission of response to questionnaire for 15 days. The

Commission after considering the reasons given in the request for extension granted

extension for 10 days vide its letter dated April 09, 2021. Sunflag response was received

in the Commission on April 15, 2021.

18.3.2 The information submitted by Sunflag in response to the questionnaire was

analyzed at the Commission and certain deficiencies were identified. Accordingly, those

data deficiencies were communicated to it vide Commission’s letter dated June 16, 2021.

Indorama Polyester was asked to provide the deficient information/data no later than 09

days, so as to enable the Commission to consider and analyze the same for the purposes

of this investigation. Sunflag responded to the deficiencies vide its letter dated July 01,

2021. However, the same was still deficient and the Commission vide its letter dated July

08, 2021 asked for the deficient information. Sunflag response in this regard was received

on July 13, 2021.

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

16

19. Verification of the Information:

19.1 In terms of Sections 32(4) and 35 of the Act and Rule 12 of the Rules, during the

course of an investigation, the Commission shall satisfy itself as to the accuracy of the

information and for this purpose verify the information supplied by the interested parties.

Accordingly, the Commission has satisfied itself as to the accuracy and adequacy of

information supplied by the interested parties to the extent possible for the purposes of

this preliminary determination.

19.2 The officers of the Commission conducted on-the-spot investigation at the

plant(s) and office(s) of the Applicants and Rupali Polyester Ltd. in the Sunset and

Change Circumstances Reviews against dumped imports of PSF from China and verified

their respective data for the period July 2017 to June 2020. Since, in this investigation,

the period of injury is from October 2017 to September 2020 and data of 33 months has

already been verified, therefore, the Commission did not conduct on-the-spot

investigation in this investigation. However, in order to verify the data for one quarter i.e.

July - September 2021, certain clarifications were sought from Applicants and Rupali

Polyester Ltd.

19.3 On-the-spot investigations at the premises of exporters/producers from the

Exporting Countries, who provided information/data in response to the questionnaire

would be conducted after this preliminary determination

20. Public File:

The Commission, in accordance with Rule 7 of the Rules, has established and

maintained a public file at its office. This file remains available to the interested parties

for review and copying from Monday to Thursday between 1100 hours to 1300 hours

throughout the investigation (except public holidays). This file contains non-confidential

versions of the application, responses to the questionnaires, submissions, notices,

correspondence, and other documents for disclosure to the interested parties.

21. Confidentiality:

21.1 In terms of Section 31 of the Act, the Commission shall keep confidential any

information submitted to it, which is by nature confidential, or determined by the

Commission to be of confidential nature for any other reason, or provided as confidential

by parties to an investigation, upon good cause shown to be kept confidential.

21.2 The Applicants have requested to keep confidential the information, which is by

nature confidential in terms of Section 31 of the Act. This information includes data

relating to sales, sale prices, cost to make and sell, inventories, production, profit/(loss),

return on investment, cash flow, growth, investment, salaries & wages, number of

employees and capacity.

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

17

21.3 On the basis of request made by the Applicants, the Commission has determined

the confidentiality in light of Section 31 of the Act and for the reasons that disclosure of

such information may be of significant competitive advantage to a competitor, or because

its disclosure would have a significant adverse effect upon the interested parties

providing such information. Therefore, the Commission kept all such information

confidential for which the Applicants made a request to keep it confidential.

21.4 However, in terms of Sub-Section (5) of Section 31, non-confidential summaries of

all confidential information, which provides reasonable understanding of the substance,

have been placed in public file.

22. Views/Comments of Interested Parties:

22.1 The Commission received views/comments from Directorate General of Foreign

Trade, Ministry of Trade, Government of Indonesia and Khyber-Pakhtunkhwa Textiles

Mills Association, which have been considered while making this preliminary

determination.

22.2 The views/comments of the interested parties and the Commission’s response are

given in annotated form at Annexure – I.

B. DETERMINATION OF DUMPING

23. Dumping:

In terms of Section 4 of the Act dumping is defined as follows:

“an investigated product shall be considered to be dumped if it is introduced

into the commerce of Pakistan at a price which is less than its normal value”.

24. Normal Value:

24.1 In terms of Section 5 of the Act “normal value” is defined as follows:

“a comparable price paid or payable, in the ordinary course of trade, for sales

of a like product when destined for consumption in an exporting country”.

24.2 Further, Section 6 of the Act states:

“(1) when there are no sales of like product in the ordinary course of trade in

domestic market of an exporting country, or when such sales do not permit a

proper comparison because of any particular market situation or low volume

of the sales in the domestic market of the exporting country, the Commission

shall establish normal value of an investigated product on the basis of either:

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

18

“a) the comparable price of the like product when exported to an

appropriate third country provided that this price is representative; or

“b) the cost of production in the exporting country plus a reasonable

amount for administrative, selling and general costs and for profits.

“(2) Sales of a like product destined for consumption in domestic market of an

exporting country or sales to an appropriate third country may be considered

to be a sufficient quantity for the determination of normal value if such sales

constitute five per cent or more of the sales of an investigated product to

Pakistan:”.

24.3 Ordinary course of trade is defined in Section 7 of the Act as follows:

“(1) The Commission may treat sales of a like product in domestic market of

an exporting country or sales to a third country at prices below per unit, fixed

and variable, cost of production plus administrative, selling and other costs as

not being in the ordinary course of trade by reason of price and may disregard

such sales in determining normal value only if the Commission determines that

such sales were made –

“(a) within an extended period of time which shall normally be a period

of one year and in no case less than a period of six months;

“(b) in substantial quantities; and

“(c) at prices which do not provide for the recovery of all costs within a

reasonable period of time.

“(2) For the purposes of sub-clause (b) of sub-section (1), sales below per unit

cost shall be deemed to be in substantial quantities if the Commission establishes

that –

“(a) a weighted average selling price of transactions under consideration

for the determination of normal value is below a weighted average

cost; or

“(b) the volume of sales below per unit cost represents twenty per cent or

more of the volume sold in transactions under consideration for the

determination of normal value.

“(3) If prices which are below per unit cost at the time of sale are above the

weighted average cost for the period of investigation, the Commission shall

consider such prices as providing for recovery of costs within a reasonable period

of time.”

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

19

25. Export Price:

The “export price” is defined in Section 10 of the Act as “a price actually paid or

payable for an investigated product when sold for export from an exporting country to

Pakistan”.

26. Dumping Determination:

26.1 As stated earlier the Applicants identified 41 exporters/producers from the

Exporting Countries involved in alleged dumping of the investigated product. The

Commission sent questionnaires to 41 exporters/producers whose complete addresses

were available with the Commission. A copy of the questionnaire was also provided to

the embassies of the Exporting Countries in Islamabad with a request to forward it to all

exporters/producers of the investigated product based in the Exporting Countries to

submit information to the Commission.

26.2 The Commission received response of the questionnaire from following

exporters/producers:

i. Chung Shing Textile Marketing Limited, Chinese Taipei;

ii. PT. Indorama Polychem, Indonesia;

iii. PT. Indorama Synthetics TBK, Indonesia;

iv. Indorama Polyester Industries Public Company Limited, Thailand;

v. Kangwal Polyester Co. Limited, Thailand; and

vi. Sunflag Thailand Limited, Thailand.

26.3 Normal value, export price and individual dumping margins for the above-

mentioned exporters/producers have been determined in accordance with Part III, IV and

V of the Act on the basis of the information provided by them.

26.4 The Commission has determined dumping margin for non-cooperating

exporters/producers from the Exporting Countries on the basis of Best Information

Available’ in terms of Section 32 of the Act and Article 6.8 and Annex II of the

Agreement on Anti-dumping.

27. Determination of Export Price for Chung Shing Textile Marketing Limited

(“Chung Shing”)

27.1 Export price for Chung Shing has been determined on the basis of the information

provided it on its export sales to Pakistan made during the POI.

27.2 According to the information, Chung Shing exported *** MT of PSF to all export

markets including Pakistan. It exported *** MT of the investigated product to Pakistan

during the POI. Chung Shing exported different types of the investigated product to

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

20

Pakistan during the POI. Export sales to Pakistan, during POI, through an un-related sales

agent i.e. Avon Commercial Corporation.

27.3 Chung Shing exported investigated product at CIF basis. To arrive at the ex-

factory level, Chung Shing has reported adjustments on account of commission, ocean

freight, insurance and custom fee. The Commission accepted these adjustments and the

export price at ex-factory level is worked out by deducting values reported for these

adjustments from the gross value of the sales transactions. Summary of calculations of

export price is placed at Annexure - II.

28. Determination of Normal Value for Chung Shing

28.1 Normal value for Chung Shing has been determined on the basis of the

information provided by it on its domestic sales made during the POI.

28.2 According to the information, Chung Shing sold different types of PSF in its

domestic market including the types, which were alike to the types of the investigated

product exported to Pakistan during the POI. Chung Shing sold *** MT in the domestic

market during POI. Chung Shing also provided monthly ex-factory price list of different

types of PSF. As the prices of raw materials of PSF fluctuated significantly during the

POI and Chung Shing did not provide monthly cost to make & sell of the investigated

product. Therefore, the Commission used monthly price lists for determination of normal

value for the purposes of this preliminary determination. For the purposes of like to like

comparison, normal value (price list) is determined only for those types which were

comparable to the types of the investigated product. If Chung Shing does not provide the

deficient information after this preliminary determination, the Commission will be

constrained to make final determination on the basis of “best information available” in

terms of Section 32 of the Act which may not be favorable to Chung Shing.

28.3 Monthly price list of Chung Shing is placed at Annexure - III.

29. Determination of Export Price for PT. Indorama Polychem, Indonesia

(“Indorama Polychem”)

29.1 Export price for Indorama Polychem has been determined on the basis of the

information provided it on its export sales to Pakistan made during the POI.

29.2 According to the information, Indorama Polychem exported *** MT of PSF to all

export markets including Pakistan. It exported *** MT of the investigated product to

Pakistan during the POI. Indorama Polychem exported different types of the investigated

product to Pakistan during the POI. Export sales to Pakistan, during POI, were directly to

unrelated customers and through un-related sales agent.

29.3 Indorama Polychem exported investigated product at CIF basis. To arrive at the

ex-factory level, Indorama Polychem has reported adjustments on account of credit cost,

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

21

commission, inland freight, ocean freight, insurance and bank charges. The Commission

accepted these adjustments and the export price at ex-factory level is worked out by

deducting values reported for these adjustments from the gross value of the sales

transactions. Summary of calculations of export price is placed at Annexure - IV.

30. Determination of Normal Value for Indorama Polychem

30.1 Normal value for Indorama Polychem has been determined on the basis of the

information provided by it on its domestic sales made during the POI.

30.2 According to the information, Indorama Polychem sold different types of PSF in

its domestic market including the types, which were alike to the types of the investigated

product exported to Pakistan during the POI. Indorama Polychem sold *** MT in the

domestic market during POI. These sales were in sufficient quantities to determine

normal value in terms of Section 6(2) of the Act, as these sales were more than 5 percent

of the export sales of the investigated product exported to Pakistan during the POI. For

the purposes of like to like comparison, normal value is determined only for those types

which were comparable to the types of the investigated product.

30.3 Analysis of the information provided by Indorama Polychem revealed that some

sales of the comparable types were not in ordinary course of trade in terms of Section

7(2) of the Act. Sales of the comparable types, which were not in ordinary course of trade

ranges from 28.82 percent to 89.91 percent of sales of a particular type of PSF. For the

purposes of determination of normal value the Commission has disregarded sales, which

were not in ordinary course of trade in accordance with Section 7 of the Act.

30.4 To arrive at the ex-factory level from delivered price, Indorama Polychem has

reported adjustment on account of credit cost, inland freight, bank charges, exchange loss

and insurance. The Commission accepted this adjustment and the normal value at ex-

factory level is worked out by deducting values reported for this adjustment from the

gross value of sales transactions. Summary of calculations of normal value is placed at

Annexure - V.

31. Determination of Export Price for PT. Indorama Synthetics TBK, Indonesia

(“Indorama Synthetics”)

31.1 Export price for Indorama Synthetics has been determined on the basis of the

information provided it on its export sales to Pakistan made during the POI.

31.2 According to the information, Indorama Synthetics exported *** MT of PSF to all

export markets including Pakistan. It exported *** MT of the investigated product to

Pakistan during the POI. Indorama Synthetics exported different types of the investigated

product to Pakistan during the POI. Export sales to Pakistan, during POI, were directly to

unrelated customers.

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

22

31.3 Indorama Synthetics exported investigated product at CIF basis. To arrive at the

ex-factory level, Indorama Synthetics has reported adjustments on account of credit cost,

inland freight, ocean freight, insurance and bank charges. The Commission accepted

these adjustments and the export price at ex-factory level is worked out by deducting

values reported for these adjustments from the gross value of the sales transactions.

Summary of calculations of export price is placed at Annexure - VI.

32. Determination of Normal Value for Indorama Synthetics

32.1 Normal value for Indorama Synthetics has been determined on the basis of the

information provided by it on its domestic sales made during the POI.

32.2 According to the information, Indorama Synthetics sold different types of PSF in

its domestic market including the types, which were alike to the types of the investigated

product exported to Pakistan during the POI. Indorama Synthetics sold *** MT in the

domestic market during POI. These sales were in sufficient quantities to determine

normal value in terms of Section 6(2) of the Act, as these sales were more than 5 percent

of the export sales of the investigated product exported to Pakistan during the POI. For

the purposes of like to like comparison, normal value is determined only for those types

which were comparable to the types of the investigated product.

32.3 Analysis of the information provided by Indorama Synthetics revealed that some

sales of the comparable types were not in ordinary course of trade in terms of Section

7(2) of the Act. Sales of the comparable types, which were not in ordinary course of trade

ranges from 22.70 percent to 100 percent of sales of a particular type of PSF. For the

purposes of determination of normal value the Commission has disregarded sales, which

were not in ordinary course of trade in accordance with Section 7 of the Act. Therefore,

normal value for those types whose 100 percent sales were not in ordinary course of trade

has been constructed on the basis of cost of production plus administrative, selling and

general costs and for profit of 5 percent of the exporter/producer in accordance with

Section 6 of the Act.

32.4 To arrive at the ex-factory level from delivered price, Indorama Synthetics has

reported adjustment on account of credit cost, inland freight, insurance, exchange loss

and bank charges. The Commission accepted these adjustments and the normal value at

ex-factory level is worked out by deducting values reported for this adjustment from the

gross value of sales transactions. Summary of calculations of normal value is placed at

Annexure - VII.

33. Determination of Export Price for Indorama Polyester Industries Public

Company Limited, Thailand (“Indorama Polyester”)

33.1 Export price for Indorama Polyester has been determined on the basis of the

information provided it on its export sales to Pakistan made during the POI.

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

23

33.2 According to the information, Indorama Polyester exported *** MT of PSF to all

export markets including Pakistan. It exported *** MT of the investigated product to

Pakistan during the POI. Indorama Polyester exported different types of the investigated

product to Pakistan during the POI. Export sales to Pakistan, during POI, were directly to

unrelated customers and through un-related sales agents.

33.3 Indorama Polyester exported investigated product at CIF basis. To arrive at the

ex-factory level, Indorama Polyester has reported adjustments on account of commission,

credit cost, inland freight, ocean freight, handling cost, duty draw back, others and bank

charges. The Commission accepted these adjustments and the export price at ex-factory

level is worked out by deducting values reported for these adjustments from the gross

value of the sales transactions. Summary of calculations of export price is placed at

Annexure - VIII.

34. Determination of Normal Value for Indorama Polyester

34.1 Normal value for Indorama Polyester has been determined on the basis of the

information provided by it on its domestic sales made during the POI.

34.2 According to the information, Indorama Polyester sold different types of PSF in

its domestic market including the types, which were alike to the types of the investigated

product exported to Pakistan during the POI. Indorama Polyester sold *** MT in the

domestic market during POI. These sales were in sufficient quantities to determine

normal value in terms of Section 6(2) of the Act, as these sales were more than 5 percent

of the export sales of the investigated product exported to Pakistan during the POI. For

the purposes of like to like comparison, normal value is determined only for those types

which were comparable to the types of the investigated product.

34.3 Analysis of the information provided by Indorama Polyester revealed that some

sales of the comparable types were not in ordinary course of trade in terms of Section

7(2) of the Act. Sales of the comparable types, which were not in ordinary course of trade

ranges from 20.37 percent to 100 percent of sales of a particular type of PSF.

34.4 For the purposes of determination of normal value the Commission has

disregarded sales, which were not in ordinary course of trade in accordance with Section

7 of the Act. Therefore, normal value for those types whose 100 percent sales were not in

ordinary course of trade has been constructed on the basis of cost of production plus

administrative, selling and general costs and for profit of 5 percent of the

exporter/producer in accordance with Section 6 of the Act.

34.5 To arrive at the ex-factory level from delivered price, Indorama Polyester has

reported adjustment on account of credit cost, commission, inland freight, insurance,

bank charges and other (cost of credit insurance). The Commission has accepted these

adjustments and the normal value at ex-factory level is worked out by deducting values

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

24

reported for these adjustments from the gross value of sales transactions. Summary of

calculations of normal value is placed at Annexure - IX.

35. Determination of Export Price for Kangwal Polyester Co. Limited, Thailand

(“Kangwal Polyester”)

35.1 Export price for Kangwal Polyester has been determined on the basis of the

information provided it on its export sales to Pakistan made during the POI.

35.2 According to the information, Kangwal Polyester exported *** MT of PSF to all

export markets including Pakistan. It exported *** MT of the investigated product to

Pakistan during the POI (in the months of Jan, Feb, Apr, May, Jun, Jul, Aug). Kangwal

Polyester exported different types of the investigated product to Pakistan during the POI.

Export sales to Pakistan, during POI, were through un-related sale agent i.e. English

Fibre and Yarn.

35.3 Kangwal Polyester exported investigated product at CIF basis. To arrive at the ex-

factory level, Kangwal Polyester has reported adjustments on account of commission,

credit cost, inland freight, ocean freight, handling cost, duty draw back, others (terminal

handling and BL Charges) and bank charges. The Commission accepted these

adjustments and the export price at ex-factory level is worked out by deducting values

reported for these adjustments from the gross value of the sales transactions. Summary of

calculations of export price is placed at Annexure - X.

36. Determination of Normal Value for Kangwal Polyester

36.1 Normal value for Kangwal Polyester has been determined on the basis of the

information provided by it on its domestic sales made during the POI.

36.2 According to the information, Kangwal Polyester sold different types of PSF in its

domestic market including the types, which were alike to the types of the investigated

product exported to Pakistan during the POI. Kangwal Polyester sold *** MT in the

domestic market during POI. These sales were in sufficient quantities to determine

normal value in terms of Section 6(2) of the Act, as these sales were more than 5 percent

of the export sales of the investigated product exported to Pakistan during the POI. For

the purposes of like to like comparison, normal value is determined only for those types

which were comparable to the types of the investigated product and for the comparable

months of export sales to Pakistan.

36.3 Analysis of the information provided by Kangwal Polyester revealed that some

sales of the comparable types were not in ordinary course of trade in terms of Section

7(2) of the Act. Sales of the comparable types, which were not in ordinary course of trade

ranges from 26.82 percent to 66.74 percent of sales of a particular type of PSF. For the

purposes of determination of normal value the Commission has disregarded sales, which

were not in ordinary course of trade in accordance with Section 7 of the Act.

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

25

36.4 To arrive at the ex-factory level from delivered price, Kangwal Polyester has

reported adjustment on account of credit cost and inland freight. The Commission has

accepted these adjustments and the normal value at ex-factory level is worked out by

deducting values reported for these adjustments from the gross value of sales

transactions. Summary of calculations of normal value is placed at Annexure - XI.

37. Determination of Export Price for Sunflag Thailand Limited, Thailand

(“Sunflag”)

37.1 Export price for Sunflag has been determined on the basis of the information

provided it on its export sales to Pakistan made during the POI.

37.2 According to the information, Sunflag exported *** MT of PSF to all export

markets including Pakistan. It exported *** MT of the investigated product to Pakistan

during the POI (in the months of Jan, Feb, May, Jun, Jul). Sunflag exported different

types of the investigated product to Pakistan during the POI. Export sales to Pakistan,

during POI, were to un-related customers.

37.3 Sunflag exported investigated product at CIF basis. To arrive at the ex-factory

level, Sunflag has reported adjustments on account of credit cost, inland freight, ocean

freight, handling cost, duty draw back, custom fee and bank charges. The Commission

accepted these adjustments and the export price at ex-factory level is worked out by

deducting values reported for these adjustments from the gross value of the sales

transactions. Summary of calculations of export price is placed at Annexure - XII.

38. Determination of Normal Value for Sunflag

38.1 Normal value for Sunflag has been determined on the basis of the information

provided by it on its domestic sales made during the POI.

38.2 According to the information, Sunflag sold different types of PSF in its domestic

market including the types, which were alike to the types of the investigated product

exported to Pakistan during the POI. Sunflag sold *** MT in the domestic market during

POI. These sales were in sufficient quantities to determine normal value in terms of

Section 6(2) of the Act, as these sales were more than 5 percent of the export sales of the

investigated product exported to Pakistan during the POI. For the purposes of like to like

comparison, normal value is determined only for those types which were comparable to

the types of the investigated product and for the comparable months of export sales to

Pakistan.

38.3 Analysis of the information provided by Sunflag revealed that all the sales of the

comparable types were not in ordinary course of trade in terms of Section 7(2) of the Act.

Therefore, normal value for those types whose 100 percent sales were not in ordinary

course of trade has been constructed on the basis of cost of production plus

NON – CONFIDENTIAL

Preliminary Determination in Anti-dumping Investigation against Dumped Imports of PSF into Pakistan Originating in

and/or exported from Chinese Taipei, the Republic of Indonesia and the Kingdom of Thailand .

26

administrative, selling and general costs and for profit of 5 percent of the

exporter/producer in accordance with Section 6 of the Act. Summary of calculations of

normal value is placed at Annexure - XIII.

39. Determination of Dumping for Non-cooperating Exporters

39.1 The Commission determined dumping for the exporters/foreign producers who

did not cooperate with the Commission and did not supply necessary information has

been determined on the basis of best information available in accordance with Section 32

of the Act. Details are given in following paragraphs.

39.2 Determination of Dumping for Non-cooperating Exporters from Chinese

Taipei

A residual dumping margin and antidumping duty rate for all other exporters from