predictions of professional economists …/67531/metadc501259/m2/1/high... · do predictions of...

TRANSCRIPT

/0 I

DO PREDICTIONS OF PROFESSIONAL BUSINESS ECONOMISTS CONFORM

TO THE RATIONAL EXPECTATIONS HYPOTHESIS?

TESTS ON A SET OF SURVEY DATA

THESIS

Presented to the Graduate Council of the

University of North Texas in Partial

Fulfillment of the Requirements

For the Degree of

MASTER OF SCIENCE

By

Russell Edward Dabbs, B.A.

Denton, Texas

August, 1989

Dabbs, Russell Edward, Do Predictions of Professional

Business Economists Conform to the Rational Expectations

Hypothesis? Tests on a Set of Survey Data. Master of

Science (Economics), August, 1989, 110 pp., 11 tables,

bibliography, 25 titles.

A set of forecast survey data is analyzed in this paper

for properties consistent with the Rational Expectations

Hypothesis. Standard statistical tests for "rational

expectations" are employed utilizing consensus forecasts

generated by an interest rate newsletter. Four selected

variables (Fed Funds rate, M1 rate of growth, rate of change

in CPI, and real GNP growth rate) are analyzed over multiple

time horizons. Results tend to reject "rational

expectations" for most variables and time horizons.

Forecasts are more likely to meet "rationality" criteria the

shorter the forecast horizon, with the notable exception of

forecasts of real GNP growth.

TABLE OF CONTENTS

LIST OF

Chapter

PageTABLES i............v................... iv

iii

1. INTRODUCTION .............. .. ........... 1

Hypotheses and Organization of the Paper

2. SURVEY OF RELATED LITERATURE ................ 8

BackgroundSurvey Data on ExpectationsEmpirical ResearchConsensus ForecastsSummary

3. METHODOLOGY ........................... 28

DataProperties of Rational ExpectationsStatistical Tests for RationalityAdaptive Expectations

4. FINDINGS . . . . . . . . . .. . . . . . . . .42

Preliminary Accuracy MeasuresUnbiasedness and Error OrthogonalityEfficiencyAdaptive ExpectationsSummary

5. SUMMARY AND CONCLUSIONS ..................... 82

APPENDIX A ..................... 85

APPENDIX B ..................... 90

APPENDIX C .......................... ...... 100

BIBLIOGRAPHY...................................109

LIST OF TABLES

Table Page

1. Preliminary Accuracy Measures .................. 43

2. OLS Unbiasedness Test Results .................. 46

3. Theil U Statistic and Decompositionof Mean Squared Error ....................... 51

4. GLS Unbiasedness Test Results .................. 54

5. OLS Efficiency Test Results .................... 59

6. GLS Efficiency Test Results ................... 66

7. Adaptive Forecast Revision ..................... 71

8. GLS Results: Adaptive Forecast Revision ....... 75

9.0 Actual Data .................................... 0 0 0 0 00 000 8 7

10. Consensus Data ................................. 88

11. Autocorrelation Functions ...................... 92

iv

CHAPTER 1

INTRODUCTION

This study tests a set of forecast survey data for

"rationality." The purpose of such a study is twofold.

First, it will provide an opportunity to analyze predictions

of professional business forecasters, the accuracy of which

is an important consideration for forecast consumers. The

determinative bases of forecast accuracy may take various

forms. Forecasts may "be evaluated relative either to an

alternative forecasting procedure (traditionally a naive

method), or to a desired statistical property... " (3,

p.301]. This study will utilize standard statistical

properties associated with rationality as the criteria for

judging the forecast accuracy of the survey data used

herein.

The second purpose behind this study is to provide

additional evidence as to whether the "rational expectations

hypothesis" is a credible assumption to apply when analyzing

the actual behavior of economic agents. That is, are

expectations, as Muth suggested, "essentially the same as

the predictions of the relevant economic theory" [4, p.316]?

Since Muth's original hypothesis is now the fundamental

tenet upon which much contemporary macroeconomic modelling

1

2

is based, it is of interest to conduct direct tests of it.

Unfortunately, the testing of the rational expectations

hypothesis (or simply "rational expectations") is highly

problematic, due to the fact that the expectations of future

economic variables and economic conditions are unobservable.

Since reliable data on expectations are relatively scarce,

rational expectations is prone to be accepted or dismissed

on the basis of indirect tests of joint hypotheses, or even

simply on grounds of faith.

The intent of this study is to examine expectations

by analyzing a recent set of survey data generated by a

monthly interest rate newsletter. In this newsletter,

entitled Blue Chip Financial Forecasts, various professional

business economists provide monthly forecasts of several

important macroeconomic variables over multiple time

horizons. Because these forecasts represent expectations of

sophisticated observers of the economy, this data set

affords an opportunity to test observable "expert"

expectations data for accuracy and conformity with the

rational expectations hypothesis.

Three points illustrate the importance of the topic.

First, a pertinent question to ask of professional

forecasters is "How accurate are your predictions?" That

is, those who regularly employ the services of "experts"

should be interested in how well these experts' predictions

fare over time. Does the information they possess enable

3

them to forecast accurately? Which variables are "easier"

to predict accurately, and which are "harder"? What happens

to accuracy as forecast horizons lengthen? These issues

ought to be of concern to consumers of "expert" forecasts

such as those supplied by the Blue Chip newsletter.

Secondly, is there an alternative explanation to

"rationality" with regard to the structure of expectations?

The most compelling feature of rational expectations is its

ability to furnish an explanation of expectations formation

explicitly in line with economic theory. Other expectations

theories (such as "extrapolative expectations" and "adaptive

expectations") have been routinely criticized as

theoretically inadequate, or "ad hoc." Rational

expectations, on the other hand, offers the chance to

appropriate a theory of expectations formation in which

agents act upon all relevant, readily available information,

not just past, selective information, as is the case with

other expectations theories. However, if Milton Friedman's

dictum is true, that the value of a theory lies in its

ability to predict, what is to become of a theoretically

compelling model of expectations, such as rational

expectations, if it fails to attract empirical support?

Further, even if one of these so-called ad hoc models is

empirically satisfying, shall it nevertheless be disregarded

on the grounds of being less theoretically compelling than

rational expectations?

4

Finally, the testing of observable data on expectations

is important in terms of the implications of rational

expectations for macroeconomic theory in general.

Expectations of economic agents are a vital component of

macroeconomic modelling. Static models which do not include

the role of expectations have long been dismissed as

unsatisfactory representations of general macroeconomic

phenomena. As a result, the search for a suitable

explanation for expectations and a workable procedure for

incorporating expectations into macro models has been of

tremendous interest.

Emphasis on the role of expectations is largely

traceable to Keynes' General Theory ;f Employment, Interest,

and Money [2]. Indeed, much work in macroeconomics since

that book's publication has been devoted to translating

Keynes' "theoretical and discursive... expectations-based

theory into an operational theory with testable hypotheses"

[1, p.14]. Non-Keynesian macroeconomic theory has also

stressed the importance of expectations. "New Classical"

economics, in particular, has fashioned macroeconomic models

around endogenously formed expectations. However, macro

models with endogenous expectations depend upon a precise

specification of how those expectations are formed,

otherwise they cannot be tested. Yet a satisfactory,

sufficiently general specification is elusive, largely due

to the difficulty of performing direct tests on expectations

5

data to confirm or reject various expectations hypotheses.

It is for these reasons--examining forecast accuracy

and expectations formation, and the wider implications of

expectations for macroeconomic theory in general--that the

present study will be of interest. By no means will the

tests to be conducted herein, or even a series of such

tests, provide conclusive evidence whether rational

expectations should be accepted or rejected as a tenable

assumption underlying actual behavior. Nevertheless, the

intent is to provide an incremental indication of the

soundness of the theory.

Hypotheses and Organization of the Paper

The general hypotheses to be analyzed in this paper are

explicitly stated as follows:

Hypothesis I. Surveyed forecasts of a set of

professional business economists conform to the Rational

Expectations Hypothesis as defined in the literature, in

accordance with the standard statistical tests for its

validity. The following properties should hold for

forecasts to be deemed "rational":

(a) Forecasts should be unbiased predictors of

realized values.

(b) Forecasts should make efficient use of readily

available, relevant information.

(c) Forecast errors should exhibit no serial

correlation.

6

Hypothesis II. Surveyed forecasts of a set of

professional business economists exhibit an alternate form

of expectations formation, . adaptive expectations.

The organization of the paper is as follows. The

second chapter contains a survey of relevant literature

pertaining to expectations formation, specifically, the

Rational Expectations Hypothesis. The third chapter

outlines the methodological procedures of the study. The

fourth chapter presents the results of the methodological

procedures. The fifth chapter contains a summary of, and

conclusions drawn from, the study.

RI-mmm - - - -I,-,-- - 11 somplim

CHAPTER BIBLIOGRAPHY

1. Carter, Michael, and Maddock, Rodney. 1984. Rationalexpectations: macroeconomics for the 1980s? HongKong: Macmillan Publishers, Ltd.

2. Keynes, John Maynard. 1937. The general theory gfemployment, interest, and money. New York:Harcourt, Brace, & World, Inc.

3. McNees, Stephen K. 1978. The rationality of economicforecasts. American Economic Review 68 (May): 301-05.

4. Muth, John F. 1961. Rational expectations and the theoryof price movements. Econometrica 29 (July): 315-35.

7

CHAPTER 2

SURVEY OF RELATED LITERATURE

Background

In The General Theory of Employment, Interest, and Money,

Keynes outlined the importance of expectations in employment

determination, liquidity preference, and, especially, with

respect to investment. It is, he stated, "natural and

reasonable that expectations of the future should play a

dominant part in the scale on which new investment is deemed

advisable" [8, p.315]. Further, Keynes attributed the

"Trade cycle" primarily to investment volatility, which

itself could be largely traced to the "precarious" nature of

expectations. As a result, some understanding of

expectations and how they are formed was crucial to the

development of a satisfactory explanation of how the economy

operates. Yet the very "precariousness" of expectations

contributed to the difficulty of incorporating this crucial

element into economic models.

In addressing the problem of expectations, Keynes first

distinguished between short term and long term expectations.

In the "short term" (that period of time in which firms make

decisions regarding "daily" output of the goods they

produce, given existing capital),, Keynes suggested that

8

9

expectations most often follow a "naive" pattern--i.e.,

normally "it is sensible for producers to base their

expectations on the assumption that the most recently

realized results will continue...1" [8, p.51]. The "state of

long term expectation," however, could not be so easily

modelled. Long term expectations, according to Keynes, were

those upon which producers based their decisions about

whether or not to enter into business, or to increase or

reduce investment in new physical capital. It was unlikely

that long term expectations followed a naive pattern (or

"conventional rule," as he termed it). Was there then an

alternative generalization that could be made for the long

term? Not really, Keynes concluded. The reason for this

was that the long term was clouded by too much uncertainty.

A sound mathematical expectation could not be generated

based upon ignorance and uncertainty [8, p.152]. Keynes was

thus skeptical of attempts to discover "the" mathematical

structure of expectations. Human knowledge and behavior was

too varied, the future too uncertain. "[H]uman decisions

regarding the future... cannot depend on strict mathematical

expectation since the basis for making such calculations

does not exist" [8, p.162]. Thus, Keynes did not seriously

attempt to find an operational explanation of expectation

formation. Behavior was simply too complicated and the

future too uncertain to allow for any significant, widely

applicable generalization as to how expectations are formed.

10

A subsequent attempt to make a more precise

generalization regarding expectations was the extrapolative

model, which is essentially an extension of the naive model

(The naive model states that the forecast of the next value

of a variable will be the same as the last realized value.)

Extrapolative expectations can be expressed as follows:

EX- = Xt.1 + A(Xt.1 - Xt-2 ) (1)

where EX is the forecasted value of X. This suggests that

expectations are formed not only on the basis of the last

realized value, but also upon the direction of change of

that value, as well as upon the value of A, the coefficient

of expectation. A negative value of A suggests that

forecasts are regressive, i.e., the forecaster expects any

trend in X to be reversed, whereas if A is positive, the

forecaster expects any trend in X to continue. The

expression is reduced to the naive model when the

coefficient of expectation equals zero [4, p.19].

Another attempt to explain how expectations are formed

is the adaptive expectations model. In essence, adaptive

expectations asserts that forecasters revise their

expectations on the basis of prior forecast errors. The

model can be expressed as

EXt = EXt. 1 + A (Xt. 1 - EXt.1) (2)

where A is the "learning coefficient," which displays the

degree to which the forecaster adjusts his forecasts to

prior forecast error. Further, it is possible that

11

additional lagged terms of forecast error may be included,

suggesting that forecast revision is based not only on the

last period's error, but also on preceding forecast errors.

The advantage of utilizing the adaptive approach to

expectations is that it relies on the appealing assumption

that forecasters learn from their mistakes. As a result, a

proxy for unobservable expectations can be generated based

upon past actual observed values. This is more satisfying

than the naive "tomorrow will be the same as today" model,

which does not allow for learning on the part of the

forecaster. The adaptive model has been widely used in

various macroeconomic models which require. some explicit

form of expectation specification (for instance, with

respect to the Permanent Income Hypothesis and models

regarding inflationary expectations [1, p.10)).

A number of disadvantages accompany adaptive

expectations. The primary criticism of the adaptive model

is that it does not allow for the ability of individuals to

make predictions based upon rational behavior, or upon all

the information available to them. Rather, forecasts are

based solely upon observations of past errors--individuals

may learn from past errors, but cannot draw upon any other

information to help render more accurate forecasts.

The Rational Expectations Hypothesis addresses the

information problem inherent in models such as adaptive

expectations by suggesting that forecasters form predictions

12

based not only on past actual values and prediction errors

of a particular variable, but also upon all readily

available, relevant information. The explicit origin of the

hypothesis is traced to John Muth's "Rational Expectations

and the Theory of Price Movements" (14]. In that article,

Muth proposed that economic agents make efficient use of

information available to them, including knowledge of the

underlying structure of the economic system, such that

expectations of particular variables are, in the aggregate,

unbiased predictors of realized values. Rationality in this

sense means that forecasters will generate subjective

predictions of future values--conditional on available

information--consistent with the objective expected outcomes

generated by the system. Forecast accuracy is thus

primarily dictated by the extent of information available.

Situations characterized by a high degree of unpredictable

uncertainty and lack of information will engender erroneous

predictions (16, p.9]. At the other extreme, perfect

information will enable forecasters to make perfect

predictions. In either case, rationality presumes that

forecasters' predictions are unbiased estimates with respect

to given information, and that the available information is

efficiently utilized.

As a result, the rational expectations approach

represents a model which is appealing in the sense that it

assumes forecasters have information available to them

13

beyond simply knowledge of past values of the variable, or

of prior prediction errors for that variable. At the same

time, the main criticism of rational expectations is also

with respect to information: the theory appears to assume

too much information. Forecasters are assumed to know the

underlying economic structure generating the actual outcome

of the variable, and react correctly, over time, to any

unpredictable change in that structure. In essence,

rational expectations is usually criticized for assuming

that economic agents know more than they actually do. (See,

for instance, Friedman [6].)

Survey Data on Expectations

Testing hypotheses as to how expectations are formed is

difficult due to the unobservability of expectations. There

do not exist wide-ranging, reliable time-series data on

expectations, and it would be prohibitively expensive to

generate such data. Even if a large-scale effort to measure

expectations were to be conducted, serious reliability

problems would emerge. One problem is that actual market

expectations are not identical with sample surveyed

expectations. For instance, Hafer and Resler [8] address

the issue of surveys of experts who are not actually engaged

in those market activities about which their forecasts

pertain. "[E]conomic theory typically calls for the use of

the 'market's' expectations. Thus, only the expectations of

those participating either directly or indirectly in the

14

market should be considered appropriate" [8, p.1050].

A related problem is that not all respondents are

equally interested or equally equipped to provide consistent

responses. For one respondent, expectations concerning the

price level one year hence may be of intense interest, and

much calculation may go into forming his expectation. For

another respondent, prices may be of only limited interest,

and his forecast may be made very casually. Yet the

predictions of both are weighted equally. These and other

problems may exist with respect to survey data.

Still, survey data provide the only means for directly

testing expectations models. Most tests regarding rational

expectations are indirect, joint tests of expectations and

the rest of the model [1, p.29]. (In such cases, failure of

the model may be blamed on some other aspect of the model,

rather than its expectations specification.) Further,

criticisms of survey data are rendered less severe the more

homogeneous the surveyed group is. Most of the empirical

tests of rationality based on survey data utilize responses

from a relatively similar set of respondents. For instance,

the most widely known set of expectations survey data is the

"Livingston" index, in which professional business

economists are surveyed twice yearly for inflationary

expectations. (The present study also utilizes a set of

survey data consisting of forecasts of business economists.)

Thus, survey data provide a useful, if problematic, method

15

of directly testing forecast rationality.

Empirical Research

A number of studies on inflationary expectations exist

using the Livingston data, a survey of business economists

conducted by Joseph Livingston for the Philadelphia Bulletin

and later for the Philadelphia Inquirer. This data,

compiled since 1946, consists of forecasts of several

economic variables for both six-month ahead and twelve-month

ahead time horizons. The predictions for the Consumer Price

Index (after converting from levels to rates of change in

the CPI) has been most frequently used in empirical studies.

The earliest such study was by Turnovsky [17]. Turnovsky

analyzed the Livingston data for extrapolative and adaptive

expectations, predictive accuracy, and, "incidentally," for

rationality.

Turnovsky gathered thirty-one observations stretching

from 1954 to 1969 to test various propositions. The first

question the author addressed was whether or not there

existed a structural break in the data over the observed

period. Since inflation appeared to be systematically

underpredicted in the 1950s but more accurately predicted in

the 1960s, Turnovsky proposed that businessmen might have

adjusted their expectational procedures over that period,

such that the entire period should not be pooled together

[17, p.1447]. A Chow test for equality between two sub-

periods (an "early" [1954-1964] period, and a "later" [1962-

'I R-Iffil I I , , , , - .-. , .", -,

16

1969] period) was performed, the results of which tended to

confirm Turnovsky's hypothesis.

Next, Turnovsky analyzed the structure of expectations

of the early and later periods for both six month ahead

("short term") and twelve month ahead ("longer term") time

horizons. The findings were that both extrapolative and

adaptive models performed much better in explaining

expectations for the later period than for the early period,

for both the short- and longer-term forecast horizons.

Further, the extrapolative model was found to be superior to

the adaptive model for both periods, especially for the

longer term horizon.

Results of rationality tests tended toward rejection of

rationality for this data set. The early period clearly

suggested that expectations were biased, for both the short-

and longer-term; the later period performed much better, in

that unbiasedness could not be rejected. However, the

efficiency property of rational expectations was violated

for all but the short term, later period model.

Overall, the study emphasized that a significant change

in the content of the expectations data occured from the

1950s to the 1960s. Specifically, Turnovsky noted that

improvement of rationality and forecast accuracy and the

change in how expectations were formed over the two periods

served as strong indications of the increased importance of

accuracy for businesses and of the increased awareness of

17

the cost of inaccurate predictions during periods

characterized by inflation (such as the mid- to late 1960s).

Pesando [15) examined the Livingston data for

rationality for the expressed purpose of discussing its

appropriateness as a proxy for market price expectations.

For instance, if the Livingston data were not found to be

rational, then models which used it to stand for market

inflationary expectations (for instance, with respect to the

impact of expectations on nominal interest rates) would

necessarily incorporate irrational market expectations. Yet

he noted that a growing literature pointed to efficiency and

rationality in the equity and capital markets. Pesando

suggested that this latter point tends to engender

skepticism of the rationality of the Livingston data, rather

than skepticism of the rationality of unobserved market

expectations.

Pesando's findings were that the Livingston data did

not on the whole adhere to the properties of rationality.

Tests of two sub-periods (1959:1-1962:2 and 1962:1-1969:2)

indicated that efficient use of past information concerning

inflation ("weak-form efficiency"), but "consistency" was

rejected--i.e., "the information utilized in generating the

[six month ahead] forecasts [was not] applied consistently

to generate the [twelve month ahead] forecasts" [15, p.854].

Further, while unbiasedness for the short term forecasts

were not rejected, it was rejected for the longer, twelve

18

month ahead forecasts. Theil's decomposition of mean square

error (MSE) into bias, regression, and disturbance

components depicted a dramatic increase in the bias

proportion from the short- to longer term forecasts.

Pesando proposed that the significant downward bias

(systematic underprediction) in the longer term forecasts

largely accounted for the difference between the rationality

results of the two forecast horizons.

Carlson (3] analyzed the Livingston data more closely

and reformulated it to derive a series adjusted for some

problems existent in the original survey. Appropriating

Pesando's methodology, Carlson found that the reformulated

series was not consistent with rationality. Nevertheless,

while Carlson's findings substantially agreed with

Pesando's, his conclusions did not. Whereas Pesando

maintained that it was unlikely that the Livingston sample

accurately reflected actual market expectations, Carlson

stated that there was no reason to reject the Livingston

data as "representative of informed opinion about the state

and direction of the economy in the near future" (3, p.50].

Evidence that rationality does not hold could not be

dismissed simply due to skepticism about the data set.

Mullineaux [13] criticized the efficiency and

consistency tests employed by Pesando and Carlson as

generating "ambiguous" results. Consequently, Mullineaux

retested Pesando's data set, as well as Carlson's

WIN -mk I-W wljA-wIw4

19

"reformulated" Livingston data, using an alternative method.

He concluded that the rationality criteria was met using the

Carlson data, whereas Pesando's data exhibited inefficiency.

(The present study will adopt Mullineaux's formulation of

the efficiency test; this will be outlined formally in

Chapter 3.)

Hafer and Resler [8] addressed the question of

homogeneity of forecasters within the Livingston survey in a

1982 article. There is no reason to presume that all

forecasters surveyed possessed identical backgrounds, or

that each had identical incentives to generate precise

predictions. Using the consensus forecast of the Livingston

data, then, would call into question the reliability of the

survey to stand for "market expectations" (8, p.1050]. As a

result, Hafer and Resler attempted to disaggregate the

Livingston data according to groups, specifically into

responses made by: (1) non-financial businesses; (2)

academic institutions; (3) commercial banks; (4) investment

banks; (5) the Federal Reserve system; and (6) unspecified.

The authors suggested, for instance, that business

economists should be more consistent with rationality than

the academicians, on the presumption that their livelihood

is much more closely linked to their forecast accuracy--

"they undoubtedly have a stronger incentive to gather and

process relevant information in the forecasting process than

do their academic counterparts" [8, p.1051].

20

Results of the rationality tests employed by Hafer and

Resler, using the Mullineaux methodology, indicate that only

one of the categories, non-financial businesses,

consistently adhered to the rationality standards. A

possible explanation offered by the authors is that

forecasters in this group are closer to the actual

production processes of goods and services, and are thus

more aware of changes in raw material prices and production

costs. This gives them an advantage in spotting

inflationary trends.

Figlewski and Wachtel [5] disaggregated the Livingston

data according to individual responses. Pooling 1,864

observations obtained from seventy-one respondents who

answered a certain number of surveys conducted between 1946

and 1975, Figlewski and Wachtel tested for unbiasedness and

efficiency using weighted least squares. Their results

indicated that forecast bias was present, and that

forecasters did not make efficient use of their most recent

forecast errors.

Brown and Maital [2] analyzed the whole range of

expectations series compiled by Livingston, including such

variables as real and nominal GNP, weekly wages,

unemployment rate, and industrial production. Over the

sample period 1961:1 to 1977:4, most forecasted variables

exhibited unbiasedness. Bias was detected for only the six-

and twelve-month ahead forecasts of weekly wages and nominal

21

nominal GNP, and the twelve-month ahead forecast of

industrial production.

Brown and Maital constructed a semi-strong form test of

efficiency, rather than the weak-form test utilized in each

of the studies discussed above. The semi-strong form

efficiency test, "which perhaps helps show what economists

do not know, regresses the current forecast error on lagged

policy and state variables whose variables were known at the

time when the forecast was made" [2, p.499]. The authors

chose three government policy variables (change in

government spending, change in M1, and change in public

debt) and six state variables (change in consumer and

wholesale prices, weekly wages, industrial production,

business investment, and unemployment rate--variables which

the respondents were themselves forecasting) upon which to

regress forecast errors. Results of the test were

unfavorable for the efficiency hypothesis. Forecasts of

only four variables (stock prices, industrial production,

business investment, and the unemployment rate) efficiently

incorporated all the relevant, available information for the

six month ahead horizon. For the twelve month ahead

horizon, only real GNP, business investment, and the

unemployment rate forecasts passed the efficiency test.

Although most rationality tests using survey data have

utilized the Livingston series on price expectations, other

variables from other surveys have been examined. Friedman

22

[7] tested interest rate expectations for rationality using

the Goldsmith-Nagan Bond and Money Market Letter. Friedman

tested six interest rates for both three- and six-month

ahead forecast horizons. Using thirty quarterly

observations compiled over the period 1969-1976, Friedman

concluded that the results on the rationality of interest

rate expectations were "mixed" to "unfavorable." Ordinary

Least Squares (OLS) estimates tended to support

unbiasedness, but also exhibited serial correlation of the

disturbances which "constitutes a prima facie contradiction

of rationality." In addition, "the evidence of serial

correlation per se invalidates the F-tests that are

generally favorable to the unbiasedness hypothesis" [7,

p.457-458]. As a result, Friedman tested the data for

unbiasedness using a "seemingly unrelated regression" (SURE)

procedure. The SURE tests indicated that the forecasts were

biased. Further, Friedman concluded that forecasts in the

Goldsmith-Nagan letter did not efficiently incorporate

readily available, relevant information.

Urich and Wachtel [18] tested expectations survey data

available on the weekly money supply announcement. Money

Market Services supplied this data, consisting of forecasts

of the change in M1 for ninety-five weeks from March, 1978

to January, 1980. Urich and Wachtel conducted rationality

tests on 20 individual respondents in the survey, on the

mean (or consensus) forecast, and on the pooled data of all

23

individuals over the entire series. The authors assert that

tests on the mean forecast introduces an aggregation bias

which distorts the test; "the survey mean may not be a

rational forecast even when all individual forecasts are

rational" [18, p.186]. In addition, a pooled cross section-

time series test may tend toward the rejection of

unbiasedness even when individual responses are rational,

due to very large sample size. As a result, the preferred

approach, according to Urich and Wachtel, are tests on

individual respondents. Standard rationality tests applied

to twenty individuals led to the rejection of unbiasedness

in about half of the cases, while all respondents met the

efficiency criterion.

Rationality tests have also been applied to specific

forecasting models as a method of determining forecast

accuracy. McNees [12] tested three notable forecast series

(those generated in the early 1970s by Chase Econometrics,

Wharton Econometrics, and Data Resources, Inc.) of the GNP

deflator, real GNP, and the unemployment rate, for multiple

(1-4 quarters ahead) forecast horizons.

Due to the presence of serial correlation, McNees

tested his data set for unbiasedness and efficiency using

both OLS and Generalized Least Squares (GLS). Results were

mixed. With GLS, rationality was not rejected (forecasts

were unbiased and efficient) in seventeen of the thirty-six

(3 forecasters times 3 variables times 4 forecast horizons)

wwvlw*"MwwwAw -4,. -6 quo

24

forecasts; rationality was rejected (due to evidence of bias

or inefficiency or both) with the remaining forecasts.

Consensus Forecasts

The data set analyzed in the present study will utilize

the consensus forecast of panelists surveyed by the interest

rate forecast newsletter Blue Chip Financial Forecasts. A

consensus forecast is simply the average of a set of

individual forecasts. Several articles (eg., Zarnowitz

[19], Makridakis and Winkler (10], McNees (11]) have

addressed forecast accuracy of consensus forecasts vis a vis

the individual forecasts of which they are composed.

Findings indicate that consensus forecasts "are more

accurate than most, sometimes virtually all, of the

individual forecasts that constitute the consensus" [11,

p.15]. The consensus forecast can be thought of as a

vehicle by which various forecasting methods of numerous

individuals are incorporated into one information set.

Hence, the consensus forecast should be more accurate

(unbiased and efficient) relative to most--if not all--of

the individual forecasts. A formal test of this proposition

(i.e.,, "Is the consensus forecast more accurate than the

individual forecasts within the Blue Chip survey?") is

beyond the scope of this paper. Nevertheless, from previous

empirical work, it is not unreasonable to suggest that the

Blue Chip consensus forecast should represent predictions of

economic variables which are more accurate than most of the

25

individual forecasts of which the consensus is composed.

Summary

Expectations of future values of economic variables is

a vital consideration both for the business sector, which

seeks accurate predictions of future economic conditions, as

well as for economic theory, which seeks an operational

explanation of expectations and how they are formed.

Various explanations of expectation formation have been

offered such as the naive model, extrapolative expectations,

and adaptive expectations. The Rational Expectations

Hypothesis suggests that, in the aggregate, individuals'

subjective expectations are consistent with the objective

probability distributions which generate the actual values

of economic variables. In other words, expectations are

unbiased and efficient predictors of realized values.

Empirical research has utilized survey data on expectations

to directly test the hypothesis, as well as evaluate

forecast accuracy based upon the statistical properties of

rationality. Such tests, on various sets of survey data,

have been generally unfavorable to the rational expectations

hypothesis.

The next chapter will discuss the data and methodology

used in the present study, which tests a recent set of

forecast survey data for accuracy and conformity to the

rational expectations hypothesis.

CHAPTER BIBLIOGRAPHY

1. Attfield, C., Demery D., and Duck, N. W. 1985. Rationalexpectations 'in macroeconomics: An introductionto theory and evidence. New York: Basil Blackwell,Inc.

2. Brown, Bryan W., and Maital, Schlomo. 1981. What doeconomists know? An empirical study of experts'expectations. Econometrica 49 (March): 491-504.

3. Carlson, John A. 1977. A study of price forecasts.Annals of Economic and Social Measurement 6: 27-56.

4. Carter, Michael, and Maddock, Rodney. 1984. Rationalexpectations: Macroeconomics for the 1980s? HongKong: Macmillan Publishers, Ltd.

5. Figlewski, Stephen, and Wachtel, Paul. 1981. Theformation of inflationary expectations. The Reviewof Economics and Statistics 58 (February): 1-10.

6. Friedman, Benjamin M. 1979. Optimal expectations and theextreme information assumptions of rationalexpectations models. Journal of MonetaryEconomics 5: 23-41.

7. Friedman, Benjamin M. 1980. Survey evidence on therationality of interest rate expectations.Journal of Monetary Economics 6: 453-65.

8. Hafer, R. W., and Resler, David H. 1982. On therationality of inflation forecasts: A new lookat the Livingston data. Southern EconomicJournal 48 (April): 1049-55.

9. Keynes, John Maynard. 1937. The general theory ofemployment, interest, and money. New York:Harcourt, Brace, & World, Inc.

10. Makridakis, Spyros, and Winkler, Robert L. 1983.Averages of forecasts: Some empirical results.Management Science 29 (September): 987-96.

11. McNees, Stephen K. 1987. Consensus forecasts: Tyranny ofthe majority? New England Economic Review (November/December): 15-21.

26

27

12. McNees, Stephen K. 1978. The rationality of economicforecasts. American Economic Review 68 (May): 301-05.

13. Mullineaux, Donald J. 1978. On testing for rationality:Another look at the Livingston price expectationsdata. Journal of Political Economy 86:329-36.

14. Muth, John F. 1961. Rational expectations and the theoryof price movements. Econometrica 29 (July): 315-35.

15. Pesando, James E. 1975. A note on the rationality of theLivingston price expectations. Journal of PoliticalEconomy 83: 849-57.

16. Sheffrin, Steven M. 1983. Rational expectations. NewYork: Cambridge University Press.

17. Turnovsky, Steven J. 1970. Some empirical evidence onthe formation of price expectations. Journal of theAmerican Statistical Association 65: 1441-54.

18. Urich, Thomas, and Wachtel, Paul. 1984. The structure ofexpectations of the weekly money supplyannouncement. Journal of Monetary Economics 13: 183-94..

19. Zarnowitz, Victor. 1984. The accuracy of individual andgroup forecasts from Business Outlook surveys.Journal of Forecasting 3: 11-26.

CHAPTER 3

METHODOLOGY

Data

The survey data on expectations for this study is

obtained from a monthly newsletter called Blue Chip

Financial Forecasts, subtitled "What Top Analysts Are Saying

About Interest Rates and Monetary Policy." The publication

is primarily devoted to forecasts of various interest rates;

over a dozen different rates are currently forecasted. In

addition, however, a handful of other variables are

forecasted on the grounds that they are "key assumptions"

underlying the interest rate forecasts (i.e., they may have

a significant determining influence on interest rates).

This study will conduct rationality tests on one of the

interest rate forecasts--the Federal Funds rate (FFR)--and

three of the "key assumption" variables: quarterly changes

in M1, in the Consumer Price Index (CPI), and in real Gross

National Product (GNP).

The forecast data is organized in the following manner.

Respondents are asked to forecast selected variables over

expanding time horizons; specifically, respondents make

monthly forecasts of quarterly data 1-5 quarters ahead. The

participants are approximately 40-45 professional business

economists employed by various companies, primarily large

28

29

commercial banks and other financial institutions. The

monthly mean of individual forecasts constitutes the Blue

Chip consensus forecast used in this study. The size and

composition of respondents in the consensus vary over the

sample period.

Ideally, the individual forecasts should be analyzed

as well. This would allow for comparisons between the

consensus forecast and the individual forecasts of which it

is composed. This is not feasible, however, because not

enough individuals are consistently identified throughout

the entire length of the data set; no meaningful conclusions

could be drawn from such an exercise. As a result, this

study will focus exclusively on the consensus forecast.

Reliance on the consensus should, nevertheless, provide

sufficient information as to how accurate this set of

professional forecasters are. Since previous studies (cited

in Chapter 2) indicate that a consensus or group mean

displays superior predictive accuracy to most of the

individuals within the group, a reasonable a priori

assumption is that the Blue Chip consensus will be more

accurate relative to most of the individual forecasts of

which it is composed. In essence, the Blue Chip consensus

may be thought of as equivalent to the more accurate of the

individual forecasters. This study will analyze the 1-4

quarter ahead consensus forecasts of the four variables

mentioned above. The relevant forecasts are those made

30

nearest the beginning of each quarter; as a result, the

forecast figures are obtained from the January 1, April 1,

July 1, and October 1 editions of the Blue Chip newsletter.

Thus, a one quarter ahead consensus forecast reported

January 1 represents the forecast for the first quarter of

that year; a two quarter ahead forecast represents the

forecast for the second quarter of that year; and so on.

Forecasts for the Fed Funds rate and Ml are obtained

beginning with the April 1, 1983 issue of the Blue Chip

newsletter. Forecasts for CPI and real GNP commenced with

the July 1, 1984 issue; hence, forecasts for these variables

are obtained from the July 1, 1984 issue onward. Actual

data is quarterly from 1983:2-1988:3 for FFR and M1, 1984:3-

1988:3 for CPI and GNP. Thus, the sample period for FFR and

M1 includes 22, 21, 20, and 19 observations, for one-, two-,

three-, and four-quarter ahead forecasts (respectively).

CPI and GNP forecasts include 17, 16, 15, and 14

observations for the 1-4 quarter ahead time horizons.

Analysis of multiple time horizons should provide some

of the most interesting results. It is reasonable to

hypothesize at the outset that accuracy should decay as

forecast horizons expand, regardless of whether the

forecasts conform to rationality or not. Thus, this study

also allows for a "test" to see if this very reasonable

presupposition holds for the variables selected from this

particular data set.

31

Properties of Rational Expectations

As a formal definition, expectations are said to be

rational if the conditional expectation of the variable in

question conforms to the mathematical expectation of the

actual value of the variable. This is to suggest that the

expectation, or forecast, of a variable X for time t, given

all the relevant information (I) readily available in time

t-1, should, on average, be correct. This may be expressed

as

E (X: It 1) = X . (1)

Should the forecaster possess "perfect foresight," the

information contained in It.. will not only be information

which is "readily available," but all possible information

concerning the variable in question--perfect information.

In this case, the actual value will always equal the

expected value. Without perfect information, some random

error should accompany expectations, i.e., the forecaster

will make efficient use of all information contained in I.,

such that any deviation of expectations from actual values

are attributable to some non-systematic, or random,

influences. This may be expressed as

Xt = E(Xt:It.1) +ct (2)

where et represents a random error term. Furthermore, the

expected value of the error term is zero. That is, if

Et = Xt - E(Xt:It-1) (3)

then

32

E(zt:It.1) = E(Xt:It-1 )

- E (Xt.1: It-,) = 0. (4)

For expectations to be "rational," all deviations of actual

X from predicted X must be captured in the error term. If

not, this indicates the presence of "systematic error" in

the forecasts--readily available information on which

predictions of X are based is not being used efficiently.

A further implication of rational expectations is that

all errors made in previous forecasts constitute readily

available information, and as such should be integrated into

the information set available to the forecaster, i.e., Ct-1

should be integrated into It... This leaves any forecast

error on Xt attributable to et alone. Thus, errors made in

time t should be orthogonal to both information available in

time t-1 and errors made in time t-1. This may be expressed

as

E(ct-It: It.1) = 0 (5)

and

E(C -Ct..) = 0 , where t>s. (6)

In essence, the focal question addressed in this study

--"Are the expectations of the surveyed forecasters

rational?"--may alternatively be posed as "Do these

forecasters make systematic (non-random) mistakes in their

predictions?" To be considered "rational," then, the Blue

Chip consensus forecasts should be consistent with the

properties outlined above.

33

Statistical Tests for Rationality

There exist several "standard" statistical tests for

the properties of rational expectations. The primary tests

are for unbiasedness, efficiency, and absence of

autocorrelation amongst the error terms.

1. Unbiasedness. From (2), it follows that a forecast

(EXt) is an unbiased estimator of the actual value (XJ) if a

regression equation is of the form

X = a + PEXt + Ct , (7)

where a=O, P=1.

That is, EXt is an unbiased predictor of X if the joint

null hypothesis (a,3) = (0,1) cannot be rejected.

2. Efficiency. From (5), it follows that forecast

errors generated in time t which are correlated with

information in time t-1 indicate an inefficient use of

readily available, relevant information. Theoretically,

such information should have been incorporated into the

forecast for time t to render a more accurate prediction.

Efficiency tests attempt to discover whether or not

information is being efficiently processed by forecasters.

Fully efficient incorporation of readily available,

relevant information suggests that the way the actual

process by which X is generated is equal to the process by

which forecasts are generated. That is, if X, behaves over

time as

Xt = ao + aiXt.1 + ... + angt.. + E (8(8)

34

then EXt should similarly evolve as

EXt = PO + 1Xt..1 + ... + PnXt.- + At (9)

such that ai=Pi, for all i. Following Mullineaux [3], we

subtract (9) from (8) to get

Xt'- EXt = 0o + - 1X. 1 + ... + Xt.. + . (10)

A "weak-form" efficiency test regresses forecast errors

of X (i.e., Xt-EXt) on lagged actual values of X. In this

instance, the forecast is weak-form efficient if H: '7 1= 72

= ... 0= 1, = 0 cannot be rejected. If H is rejected, then

efficiency is rejected. That is, "any non-zero coefficients

indicate that information was available the time the

forecasts were made which could have reduced forecast

errors, but was not properly incorporated into expectations"

[2, p.3].

This study will employ a semi-strong form efficiency

test, which includes more information on which forecast

errors of X are regressed than simply lagged values of X. A

semi-strong form test involves inclusion as independent

regressors lagged values of other variables which should

have been known to the forecaster at the time the forecast

was made. Specifically in regard to the present study, in

which four forecasted variables are analyzed, semi-strong

form efficiency tests will be constructed for each variable

using lagged values of itself and the other three as

independent regressors. For instance, forecast errors for

M1 (Mlerrort) should be unrelated to its own lagged value,

35

plus the lagged values of the Fed Funds rate, CPI, and real

GNP, i.e., for the regression equation

Mlerrort = 60 + 61Mlt.. + 62 FFRt..

+ 63 CPIt1 + 6 4GNPt.. (31)

forecasts for M1 are not semi-strong form efficient if the

joint hypothesis H.: 61 = 62 = 63 = 64 = 0 is rejected.

An important consideration remains with respect to

properly lagging the values of each independent variable.

That is, rejection of efficiency suggests that readily

available information was not incorporated into the

forecasters' information sets. Thus, it is crucial that the

independent variables be lagged far enough back so as to

ensure that such information was indeed readily available.

For example, (11) implies that a forecast made for the first

quarter of 1988 should be based upon an information set

which includes the actual values of each of the four

variables in the immediately previous quarter. However,

since a forecast published January 1, 1988 must necessarily

be made some time prior to January 1, actual values of those

variables for the previous period cannot be known to the

forecasters at the time the forecast is made, since final

figures for that period have not yet been generated. At

best, the forecaster will have access to preliminary data

indicating the approximate value of the variable for 1987:4.

However, all forecasters should have incorporated all final

realized values for 1987:3. As a result, the efficiency

36

test conducted herein will suggest that all forecasts, for

each (1-4) time horizon, should incorporate information

regarding realized values from at least two periods back,

i.e., the example characterized by (11) should be modified

to read

Mlerrort+, = So + S6M1..2 + 62FFRt-2

+ 63 CPIt-2 + 6 4GNPt-2 (12)

where s = 0,...,3 for forecast horizons 1-4, respectively.

3. Nonautocorrelation of error terms. Equation (6)

suggests that the forecast error generated in time t should

be serially uncorrelated with past forecast errors.

Autocorrelation indicates systematic errors by forecasters.

As a result, the presence of autocorrelation in the

unbiasedness regression equation (7) constitutes sufficient

evidence for rejection of rationality.

Adaptive Expectations

The Blue Chip forecast data set will also be tested to

determine the extent to which the consensus forecasts of the

four selected variables are formed adaptively. The Adaptive

Expectations Hypothesis asserts that individuals revise

their forecasts based upon their observations of past

forecasting errors. The adaptive model is in general

expressed as

EXt = EXt-1 + A (Xt-1 - EXt-1 ) (13)

where X and EX are the realized and forecasted values of the

variable, respectively. A represents the "learning

37

coefficient," i.e., indicates the degree to which the

forecaster adjusts his forecast to prior observed forecast

error. A learning coefficient of zero indicates, of course,

that past errors have no influence on forecast revision.

The greater the value of A, the greater the sensitivity of

subsequent forecasts to past forecast errors. A negative

value of A indicates that forecasts tend to exhibit

"regressivity," i.e., "survey respondents expect past errors

or actual changes to be reversed" [5, p.191].

Statistical investigation of adaptive influences is

facilitated by transforming (13) into the following

expression:

EXt - EXt.1 = AO + A1(Xt-1 - EXt-1 ) (14)

i.e., forecast revisions are regressed upon past forecast

errors. A value of A, statistically different from zero

indicates adaptive influences, the degree of which, again,

depends upon the size of A.

As with the efficiency test discussed earlier, the

issue of properly lagging past errors arises. Again, it is

vital that the information set contain realized values of

past errors. As a result, the form of the adaptive model as

expressed in (14) should be modified. Since forecasts are

made in the last month of each quarter, forecasters cannot

have access to final, actual figures for that quarter.

Consequently, they do not yet know the exact value of their

forecast error in that quarter. Strictly speaking, those

38

errors should not be included in their information sets.

The adaptive model should be altered to ensure that forecast

revision is based upon knowledge of realized forecast

errors.

However, at this point we will relax this constraint

with respect to two of the variables: the Fed Funds rate.and

Ml growth. Readily available actual data on these variables

exist throughout each quarter (weekly figures for M1, daily

figures for Fed Funds). As "sophisticated observers" of the

economy, these forecasters presumably keep abreast of such

information as it is disseminated, and thus have a

relatively accurate idea of the magnitude of their forecast

errors throughout that period. Further, we will assume

that, when forecasts are made, the most recent actual

figures on these two variables are not significantly

different from the final reported actual values for that

period. In other words, we will assume that actual data for

these variables is sufficiently available throughout the

quarter, and reasonably close to final quarterly figures

when forecasts are made, to enable forecasters to predict

future quarter values as if they knew the final, realized

values of forecast errors when they make their predictions.

For instance, a one-quarter ahead forecast for Fed

Funds published January 1, 1988 is generated sometime in

December, 1987. At that point, the forecaster does not know

the final actual value of the Fed Funds rate for 1987:4.

39

However, since the actual value of the Fed Funds rate is

published on a daily basis, the forecaster has access to a

current actual figure throughout December. It is reasonable

to suggest that this figure will not normally be

substantially different from the final actual value for

1987:4. As a result, forecast revision, with respect to M1

and Fed Funds, will be regressed on forecast errors in the

following fashion:

EXt+, - EXt- = A0 + xl(Xt-l - EXt. 1 ) (15)

where s = 0,...,3 for forecast horizons 1-4, respectively.

On the other hand, actual data regarding CPI and GNP

are not as frequently and efficiently issued as Fed Funds

and M1 figures are. Consequently, these variables will be

treated more conservatively by asserting that the last

realized forecast errors available to forecasters are those

of two periods back. For instance, multiple horizon

predictions published January 1, 1988 by Blue Chip may be

influenced by past prediction errors observed for 1987:3,

but not 1987:4. Forecasters do not have sufficient

information to assume they accurately know the final 1987:4

figure, and thus they cannot know their 1987:4 error. For

CPI and GNP, then, forecast revision will be regressed on

forecast errors according to (16):

EXt+S - EXt.. = A0 + X 1(Xt-2 - EXt-2 ) (16)

where s = O,...,3 for forecast horizons 1-4, respectively.

40

Notice that, in this instance, forecasters revise their

(t-1) predictions according to their (t-2) forecast errors,

which is not in the strictest sense consonant with the

adaptive model as expressed by (14). The modification

contained in equation (16), however, makes more intuitive

sense. Logically, forecasters should adjust their

immediately previous predictions (EXt.1), rather than their

forecasts of two periods back (EXt-2), to the most recent,

realized forecast errors (Xt-- - EXt-2) Forecasters will

always be concerned with their most recent prediction,

rather than any predictions which may have preceded it.

CHAPTER BIBLIOGRAPHY

1. Brocato, Joe, Kumar, Akhil, and Smith, Kenneth L. 1989.Individual versus group spot price forecasting inthe international petroleum market: A case study.Managerial and Decision Economics 10: 13-24.

2. Figlewski, Stephen, and Wachtel, Paul. 1981. Theformation of inflationary expectations. The Reviewof Economics and Statistics 58 (February): 1-10.

3. Mullineaux, Donald J. 1978. On testing for rationality:Another look at the Livingston price expectationsdata. Journal of Political Economy 83: 849-57.

4. Sheffrin, Steven M. 1983. Rational expectations. NewYork: Cambridge University Press.

5. Urich, Thomas, and Wachtel, Paul. 1984. The structure ofexpectations of the weekly money supplyannouncement. Journal of Monetary Economics. 13:183-94.

41

CHAPTER 4

FINDINGS

Preliminary Accuracy Measures

Examination of Table 1 provides a preliminary

indication of the forecast accuracy of the Blue Chip

consensus for the four variables analyzed in this study. In

Table 1, the Mean Error (ME), Mean Absolute Error (MAE),

Root Mean Squared Error (RMSE), and Root Mean Squared Error

divided the standard deviation of actual values (RMSE/SD)

are presented for each variable, for each of the 1-4 quarter

forecast horizons. On the basis of the first three

measures, forecasts of M1 growth appear to be the most

inaccurate. Yet this is somewhat misleading, since the

variance of M1 was substantially greater than it was for the

other variables.' It is clearly more difficult to accurately

predict a variable whose actual values "jump around" a great

deal than it is to predict one whose actual values exhibit

relatively little variability. As a result, the RMSE/SD

measure best facilitates inter-variable comparison. The Fed

Funds rate forecasts perform best over the 1-3 quarter ahead

time horizons. The RMSE/SD for real GNP growth is lowest

among the four-quarter ahead forecasts. Note that Ml growth

forecasts improve dramatically after accounting for the

variability of actual values.

42

43

TABLE 1

PRELIMINARY ACCURACY MEASURES

1 0 AHEAD 2 0 AHEAD 3 0 AHEAD 4 0 AHEAD

FED FUNDS RATE

ME -0.061 0.107 0.396 0.721MAE 0.455 0.926 1.212 1.428RMSE 0.622 1.193 1.558 1.825RMSE/SD 0.425 0.801 1.047 1.229

M1 GROWTH

ME -1.091 -1.214 -1.320 -1.611MAE 3.246 3.957 4.380 4.495RMSE 4.150 5.097 5.483 5.635RMSE/SD 0.871 1.059 1.111 1.129

RATE OF CHANGE IN CPI

ME 0.682 1.069 1.353 1.600MAE -0.965 1.281 1.487 1.643RMSE 1.657 1.934 2.195 2.502RMSE/SD 1.002 1.156 1.267 1.409

REAL GNP GROWTH

ME -0.247 -0.244 -0.407 -0.571MAE 1.659 1.506 1.327 1.229RMSE 1.906 1.774 1.551 1.468RMSE/SD 1.372 1.252 1.115 1.022

NOTE: ME=Mean Error, MAE=Mean Absolute Error,RMSE=Root Mean Squared Error,RMSE/SD=Root Mean Squared Error divided by standarddeviation of actual values.

Forecasts on the Fed Funds rate and Ml are for1983:2 to 1988:3. Forecasts on real GNP and the CPIare for 1984:3 to 1988:3.

44

The most interesting conclusion to draw from Table 1

concerns the question of what happens to accuracy as

forecast horizons lengthen. The multiple horizon

predictions of the Blue Chip consensus present an

opportunity to investigate the reasonable hypothesis that

forecast accuracy (and rationality) decays as forecast

horizons expand. Table 1 presents preliminary evidence to

show that this may not hold for all variables. For Fed

Funds, M1, and CPI forecasts, the hypothesis holds--accuracy

deteriorates as forecast horizons lengthen. This is not the

case for forecasts of real GNP growth. Forecast accuracy

actually improves as horizons lengthen for this variable, on

the basis of the MAE, RMSE, and RMSE/SD measures.

This result is in line with previous findings. While

it is true that, in general, forecast accuracy worsens as

time horizons lengthen, there are some variables (such as

both nominal and real GNP) that tend to exhibit the opposite

property. The reasoning behind this is that such variables

are often characterized by error "off-set," as opposed to

error "build-up". McNees characterizes the phenomenon in

this way:

Often, a surprise in real GNP growth in onequarter portends a surprise in the oppositedirection in the next quarter. Recall, forexample, the unexpected declines in real GNPfor in the second quarters of both 1979(energy shortage) and 1980 (credit controls).In each case, the unexpected weakness wasfollowed by unexpected strength in the sub-sequent quarter. Forecasts of the. half-yeartime span that included both quarters weremore accurate than those of either quarter

45

alone, thanks to errors of opposite signs inthe quarterly pattern [4, p.23].

Conversely, forecast errors of other variables tend to

accumulate, i.e., an unexpected change in one quarter is

often followed by an unexpected change in the next quarter

in the same direction, such that a one-quarter ahead

forecast error derived from the first unanticipated change

is less than a two-quarter ahead forecast error which is

composed of the cumulative changes of both periods.

The results arrayed in Table 1 give preliminary

indication as to how accurate the Blue Chip consensus

forecasts are for the four selected variables. The next two

sections present the results of tests outlined in Chapter 3

designed to- determine whether or not the Blue Chip forecasts

conform to the properties of rational expectations.

Unbiasedness and Error Orthogonality

The necessary conditions for rationality addressed in

Chapter 3 include unbiased forecasts, efficient use of

readily available information, and orthogonality of forecast

error terms. Discussion of test results will commence with

the Ordinary Least Squares (OLS) test for unbiasedness.

Table 2 presents the OLS unbiasedness test results.

Recall from Chapter 3, equation (7), that forecasts are

unbiased predictors of actual values if for the expression

Xt = a + PEXt + ft, (1)

(where X and EX are realized and forecasted values,

46

TABLE 2

OLS UNBIASEDNESS TEST RESULTS

ForecastHorizon aP1 Fl,..k DW R2

FED FUNDS RATE

1 Q ahead

2 Q ahead

3 Q ahead

4 Q ahead

1.243(1.889)

0.852(10.505)

2.780 0.644(2.394) (4.579)

3.850 0.489(2.657) (2.863)

4.464(2.791)

0.395(2.151)

1.793

3.325

1.717 0.839

0.776* 0.500

5.436* 0.512* 0.275

7*973* 0.372* 0.168

M1 GROWTH

1 Q ahead

2 Q ahead

3 Q ahead

4 Q ahead

. -5.373(-1.296)

1.855(3.453)

9.328 -0.117(1.193) (-0.109)

24.627(2.719)

-2.278(-1.800)

32.546 -3.413(3.241) (-2.395)

2.143

1.184

0.982* 0.374

0.620* -0.052

4.155* 0.692* 0.106

6.042* 1.023* 0.208

NOTES: Forecasts on Fed Funds rate and M1 are for 1983:2 to1988:3.T-statistics are in parentheses.DW is the Durbin-Watson statistic.2 is the adjusted R-square.The F-statistic is for the joint hypothesis(a=0,P=1) with k, n-k (k=2, n=19,...,22) degreesof freedom for forecast horizons 4, 3, 2, 1,repectively.

* Significant at the 5 percent level.+ Inconclusive at the 5 percent level.

47

TABLE 2 (Continued)

OLS UNBIASEDNESS TEST RESULTS

ForecastHorizon aP# Fk,n-k DW RK2

RATE OF CHANGE IN CPI

1 Q ahead

2 Q ahead

3 Q ahead

4 Q ahead

-0.728(-0.380)

0.113(0.042)

1.011(2.094)

0.718(1.139)

0.816 0.516(0.253) (0.723)

3.333(0.965)

-0.059(-0.081)

1.752

3.427

2.814+ 0.175

2.037 0.020

4.652* 1.940 -0.035

6.289* 1.883 -0.083

REAL GNP GROWTH

1 Q ahead

2 Q ahead

3 Q ahead

4 Q ahead

6.035(4.944)

-1.004(-2.448)

6.629 -1.169(3.768) (-1.990)

4.958 -0.573(1.682) (-0.567)

-0.347(-0.123)

1.431(1.287)

12.289* 2.170

7.101* 2.498

1.821 2.081

1.218 2.401

NOTE: Forecasts on1988:3.T-statistics

CPI and real GNP are for 1984:3 to

are in parentheses.DW is the Durbin-Watson statistic.k2 is the adjusted R-square.The F-statistic is for the joint hypothesis(a=0,P=1) with k, n-k (k=2, n=14,...,17) forforecast horizons 4, 3, 2, 1, respectively.

* Significant at the 5 percent level.+ Inconclusive at the 5 percent level.

0.238

0.165

-0.051

0.048

48

respectively), the joint null hypothesis (a,p) = (0,1)

cannot be rejected. Significant F-statistics in Table 2

warrant rejection of the joint null hypothesis, i.e.,

rejection of unbiasedness.

Unbiasedness is unambiguously rejected for the three-

and four-quarter ahead forecasts of CPI, and cannot be

rejected for the shorter one- and two-quarter ahead

forecasts. The opposite conclusions are drawn for real GNP.

As discussed above, the longer-horizon three- and four-

quarter ahead forecasts are actually more accurate than the

shorter-term one- and two-quarter ahead forecasts. The OLS

results reinforce this finding, since in this case the one-

and two-quarter ahead forecasts are biased, while the three-

and four-quarter ahead forecasts are not. CPI and real GNP

forecasts also meet the error orthogonality criterion of

rational expectations; the Durbin-Watson statistics

contained in Table 2 indicate the absence of any significant

serial correlation.

Results for the Fed Funds rate and M1 growth are less

clear. For both, the F-statistics indicate rejection of

unbiasedness for the three- and four-quarter ahead

forecasts, while the one- and two-quarter ahead forecasts

cannot be rejected. However, the Durbin-Watson statistic

indicates significant autocorrelation for both variables,

for all time horizons (with the exception of the one quarter

ahead Fed Funds forecast.) Since OLS F-statistics are not

49

reliable when autocorrelation is present, no meaningful

conclusions regarding unbiasedness can legitimately be

drawn. Yet, at the same time, the presence of serial

correlation violates a necessary condition for rationality.

Thus, we can at the very outset reject the notion that Blue

Chip consensus forecasts of these variables conform to the

rational expectations hypothesis. (Further evidence of

autocorrelation is given by the autocorrelation functions

[ACFs], which are presented in Appendix B.)

It is not desirable, however, to simply terminate the

discussion on these variables without further analysis. An

alternative to OLS which may shed more light on the nature

of forecast error is the Theil decomposition of mean squared

error (MSE). This procedure decomposes the MSE into bias,

regression, and disturbance components.

The Mean Squared Error (MSE) is given by (2):

MSE = (EX, - X,) 2 + (aE - r*ax) 2

+ (1 - r2) (UX) 2 (2)

where EX, and XA are the forecast and actual value means,

respectively, ao and ax are the forecast and actual value

standard deviations, respectively, and r is the Pearson

correlation coefficient between EX and X. Dividing (2) by

MSE yields the following:

[E(EXM - X)2 / MSE] = bias % of MSE (3)

[ (an - r*ax)2 / MSE] = regression % of MSE

[ (1 - r2) (a) 2 / MSE] = disturbance % of MSE.

50

The interpretation of the Theil decomposition is similar to

that for the OLS unbiasedness test expressed in equation

(1). That is, the bias proportion of MSE is a measure of

the tendency of forecasters to over- or underestimate actual

values; the interpretation of 0% bias in the Theil procedure

is analogous to a value of zero for the intercept in an OLS

regression of equation (1). The regression proportion of

MSE represents the extent to which forecasters over- or

underestimate changes in actual values. (For instance, with

respect to real GNP growth, we would expect that the one-

quarter ahead regression proportion of MSE should be greater

than the four-quarter ahead regression proportion. As

discussed previously, unexpected quarterly changes tend to

offset each other, over time, with real GNP. As a result,

one-quarter ahead forecast errors are often greater than

four-quarter ahead errors.) This is analogous to the

interpretation of the value of the slope coefficient ( ) in

equation (1). A large regression proportion of MSE is

similar to a value of 8 significantly different from one.

Finally, the disturbance proportion of MSE indicates the

degree to which forecast error is traceable to random

influences.

Table 3 presents the results of the Theil decomposition

of MSE (as well as another accuracy measure, the "Theil U"

statistic). We would expect that forecasts which are

consistent with the rational expectations hypothesis will

51

TABLE 3

THEIL U STATISTIC AND DECOMPOSITION OF MEAN SQUARED ERROR

1 Q AHEAD 2 0 AHEAD 3 0 AHEAD 4 0 AHEAD

FED FUNDS RATE

0.147

0.81%25.08%74. 11%

Ml GROWTH

0.526

5.68%5.16%

89.17%

RATE OF CHANGE IN CPI

0.462

16.96%5.93%

77.12%

0.550

30.53%0.98%

68. 49%

0.619

38. 02%2.12%

59. 86%

REAL GNP GROWTH

0.559

1.68%60.38%37.94%

0.511

1.89%48.41%49.71%

0.435

6.88%14.62%78.50%

NOTE: Forecasts on the Fed Funds rate are for 1983:2 to1988:3. Forecasts on CPI and real GNP are for 1984:3to 1988:3. Percentages may not sum to unity due torounding.

Theil U={MSE/ [ (1/n) ZX2] }4

Theil U

Bias %,Reg. %,Dis. %,

MSEMSEMSE

0.076

0.98%14.20%84.83%

0.194

6.44%30.90%62.65%

Theil U

0.229

14.81%33.17%52.03%

BiasReg.Dis.

%,

%,

MSEMSEMSE

0.422

6.91%10. 47%82.62%

0.565

5.80%25. 58%68.23%

0.569

8.17%33.11%58.72%

Theil U

Bias %,Reg. %,Dis. %,

MSEMSEMSE

0.285

40.90%8.74%

50.36%

Theil U

Bias %,Reg. %,Dis. %,

MSEMSEMSE

0.414

15.15%0.75%

84.10%

52

exhibit a large disturbance percentage (Dis. %, MSE), while

the bias percentage (Bias %, MSE) and regression percentage

(Reg. %, MSE) should be small.

Results of the Theil decomposition suggests a greater

justification for acceptance of rationality for Fed Funds

and M1 than do the OLS results. The one-quarter ahead Fed

Funds forecast displays a large disturbance percentage and

virtually no bias, and reinforces the OLS results in which

unbiasedness is not rejected. As time horizons increase,

the bias and regression proportions rise. Yet even the

four-quarter ahead forecast is composed largely of random

error. The results for M1 are similar; disturbance

proportions are high, though they decrease as time horizons

increase.

The CPI results show the highest degree of bias, and

the bias proportions vary directly with forecast horizons.

This is roughly consistent with the OLS results, in which

unbiasedness is rejected for the three- and four-quarter

ahead forecasts, and is not rejected for the one- and two-

quarter ahead forecasts.

The real GNP Theil results are consistent with initial

expectations. The one-quarter ahead regression percentage

is very high, indicating that forecasters experience some

difficulty in anticipating changes in real GNP; forecasters

clearly over- or underpredicted the variance of the actual

data in some systematic fashion. Yet the phenomenon of

53

offsetting errors enabled forecasters to more accurately

predict real GNP as forecast horizons increased, as is

demonstrated by the substantial reduction in the regression

proportions and increase in the disturbance proportions of

MSE as horizons lengthen. Since the OLS test statistics are

invalid in the presence of serial correlation, the data set

was re-tested using Generalized Least Squares (GLS), in the

manner of McNees [5]. An estimate of the first order

autocorrelation coefficient (p) was obtained through the

Cochrane-Orcutt procedure. The data set was then

transformed by p to, in essence, "filter out" the first

order serial correlation. This process reduced, but did not

eliminate, the autocorrelation problem, as is seen in Table

4. The Durbin-Watson statistic improved in each case, but

not enough to reject the hypothesis of autocorrelation at

the 5 percent level. Failure of GLS to substantially

eliminate the serial correlation in the residuals is a

likely indication of higher order serial correlation, or is

perhaps simply a statistical problem attributable to the

relatively small number of observations.

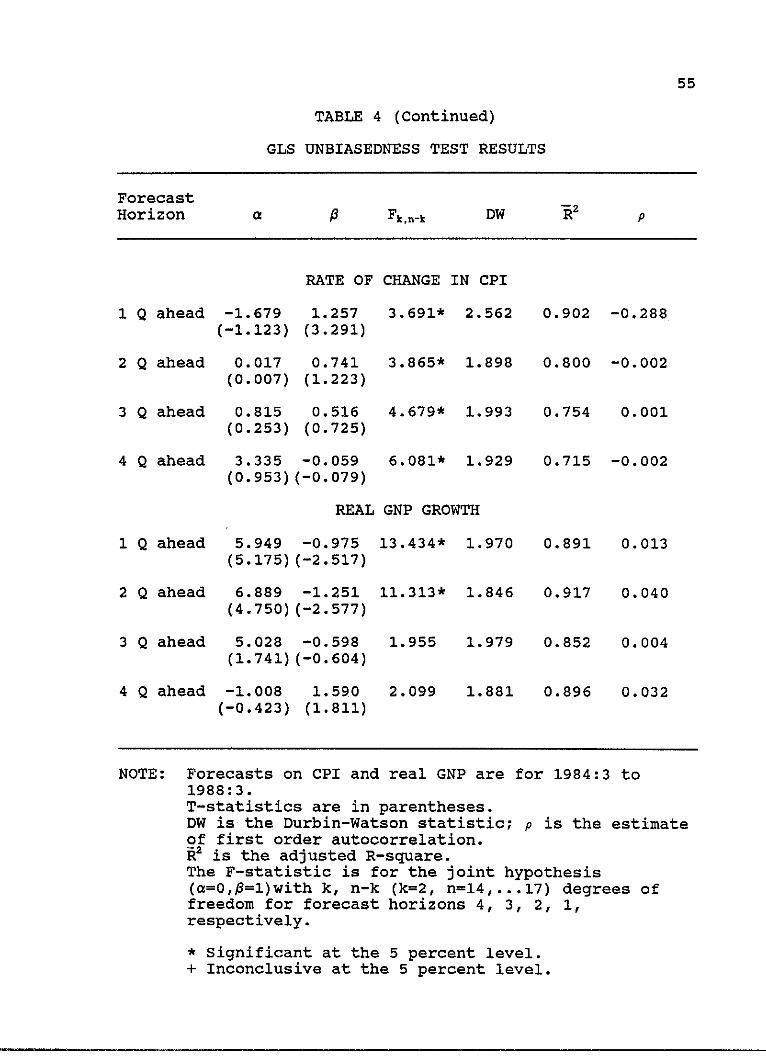

Nevertheless, using the GLS procedure as a first

approximation for correction of autocorrelation, Table 4

indicates a greater likelihood of acceptance of the

unbiasedness criterion for Ml, no significant change in