pre-ipo market, underwritting procedure, and ipo performance annual... · introduction of pre-ipo...

TRANSCRIPT

1

Pre-IPO Market, Underwritting Procedure, and IPO Performance

Hsuan-Chi Chena, Sue-Jane Chiangb*, Pei-Gi Shub

a Anderson School of Management, University of New Mexico, Albuquerque, NM 87131, USA

b Department of Business Administration, Fu-Jen Catholic University, 242 HsinChuang, Taiwan

* Corresponding author

Draft: January 15, 2018

Abstract

Using a unique data of mandatory pre-IPO market trading in Taiwan, we examine

the joint effects of pre-IPO market trading and underwriting procedures on the

short-term and long-term IPO performance. The empirical results of 476 IPOs in the

sample period 2003-2012 suggest that for the fixed price public offers, on average,

the offer price is set close to the pre-IPO market price, which is subject to insider

manipulation and significantly higher than the middle point of the price range set by

the bookbuilding offers. The higher (lower) offer price is followed by lower (higher)

initial return and poorer (better) long-run performance. The self-dealing hypothesis

relevant to issuers, investors, and underwriters can help explain the empirical

findings.

Keywords: Pre-IPO market, Bookbuilding, Fixed price offer

2

1. Introduction

The high average initial return or IPO underpricing, the percentage change from

the offer price to the first-day closing price, has been widely documented in the IPO

literature. Intuitively, the IPO underpricing anomaly could be attributed to the

underestimation of the offer price, the overestimation of the initial closing price in the

aftermarket, or both. Several theories have been proposed to shed light on relatively

low offer prices, including winner’s curse (Rock,1986), signaling theory (Allen and

Faulhaber, 1989), information asymmetry (Ritter, 1984; Ritter and Welch, 2002), and

agency problems (e.g., Ljungqvist, 2007; Ritter, 2011).1 In general, agency problems

of underwriters or the conflict of interests are important in explaining IPO

underpricing (e.g., Chang et al., 2016). As for the overestimation of the initial closing

prices in the IPO aftermarket, investor overvaluation, overoptimistm, or overreaction

may be the main factors. If the high initial returns are primarily attributed to the

relatively low offer prices, the fair initial closing prices in the aftermarket are less

likely to lead to poor post-IPO long-run performance. In contrast, if the high initial

returns are mainly attributed to the overestimation of initial closing prices, the higher

initial returns would be associated with long-run underperformance due to market

correction.

No matter which scenario would prevail, undervaluation of offer price or

overvaluation of the initial closing price, the crucial nexus that results in the

abnormal initial return relies on the malfunction of price discovery associated with

the IPO market. How to enhance price discovery for IPO shares has been explored

by academics and practitioners. The common practices of obtaining pricing-relevant

information directly from potential investors so as to enhance price discovery

include bookbuilding (e.g., Benveniste and Spindt, 1989; Spatt and Srivastava, 1991;

Sherman, 2005), auction (e.g., Biais and Faugeron-Crouzet, 2002; Derrien and

Womack, 2003), and pre-IPO trading (e.g., Derrien and Kecskes, 2007; Chang et al.,

2016).2 However, it is not clear which one would prevail when they are juxtaposed,

and whether they are substitutes or complementary in terms of price discovery.

Benveniste and Spindt (1989) and Spatt and Srivastava (1991) argue that

through the discretion in share allocation underwriters can collect true market

1 Still, there are other plausible explanations, including the ease of marketing and institutional

investors obtaining kickback from share placement and trading commission (See Loughran and Ritter,

2002). 2 The use of IPO auction is not popular around the world. For our investigated case of Taiwan, there

were 53 IPOs adopting auction prior to the introduction of compulsory pre-IPO market trading. There

were only two IPO auctions after the introduction of compulsory pre-IPO market trading during our

sample period. We do not include these two IPO firms in our sample.

- 3 -

information from sophisticated investors to set offer prices that are close to the

market prices and then reduce IPO underpricing. Sherman (2005) indicates that

bookbuilding allows underwriters to manage investor access to IPO shares,

facilitating them to reduce risk for both issuers and investors and to control spending

on information acquisition, thereby limiting either IPO underpricing or aftermarket

volatility. From the perspective of reducing information asymmetry, bookbuilding

should be preferred to fixed price offers. However, self-interested underwriters are

strongly motivated to price the offering downwards so that they can allocate

underpriced shares to their favored clients in exchange for side payments

(Ljungqvist, 2007; Loughran and Ritter, 2002; Reuter, 2006; Ritter, 2011;

Nimalendran, Ritter and Zhang, 2007; Liu and Ritter, 2010 and 2011; Goldstein,

Irvine and Puckett 2011). If this is the case, traditional bookbuilding IPOs tend to

exhibit lower offer prices and therefore higher initial returns than those associated

with other offering methods.

In addition to underwriting procedures, the existence of pre-IPO market is

supposed to facilitate price discovery for IPO shares. However, the empirical

findings are mixed. Derrien and Kecskes (2007) posit that the pre-IPO market that

provides a two-stage offering may help reduce the valuation uncertainty for IPO

firms and lead to relatively low initial returns. In contrast, Cornelli, Goldreich, and

Ljungqvist (2006) and Dorn (2009) indicate that individual investors who are likely

to be noise traders tend to trade in the pre-IPO market. The prices of IPO shares are

affected by investor sentiment that results in long-run underperformance and volatile

short-run initial returns.

If pre-IPO market trading is helpful to facilitate price discovery, the initial

returns would be significantly reduced following its introduction, and the reduction

in initial returns should be equally applicable to both fixed price offers and

bookbuilding offers. By contrast, if underwriting methods rather than the

introduction of pre-IPO market matter, then only a certain kind of underwriting

procedure has an effect on the reduction of underpricing.

Because the bookbuilding and fixed price offers are both available for

underwriting IPO shares and pre-IPO market trading is mandatory for firms seeking

IPOs in Taiwan for some periods of time, as a natural experiment, we use the IPO

sample of Taiwan for the period 2003-2012 to examine whether pre-IPO market

trading or underwriting procedures would prevail in affecting initial returns. The

empirical results for 476 IPOs show that the average initial return of IPO firms with

bookbuilding is significantly higher than that of firms adopting fixed price offers.

We further examine the long-run wealth relatives for both groups of firms and find

- 4 -

that firms adopting bookbuilding offers exhibit stronger long-run performance than

firms adopting fixed price offers. The results are consistent with the idea that the

high initial returns of bookbuilt IPOs are primarily attributed to the relatively low

offer prices rather than the overestimation of initial closing prices.

We find that in some cases the pre-IPO market prices are even higher than the

initial aftermarket prices.3 This observation motivates us to propose the self-dealing

hypothesis to explain the difference in offer prices and therefore initial returns

between fixed price offers and bookbuilding offers in the context of mandatory

pre-IPO market trading. In fixed-price offers self-dealing insiders would boost the

pre-IPO prices to benefit their wealth given that the thin-trading pre-IPO market

may faciliatet them to manipulate the pre-IPO market prices. The offer prices set

with reference to the pre-IPO market prices tend to be acceptable to uninformed

individual investors who are the major subscribers to IPO shares in fixed price offers.

By contrast, in bookbuilding offers, there are at least two motives for underwriters to

set relatively low offer prices compared to the aftermarket prices. On the one hand,

underwriters underprice IPO shares to induce truthful information revelation from

institutional investors. On the other hand, self-interested underwriters have strong

incentives to set the offer prices downwards so that they can allocate underpriced

shares to their favored clients in exchange for side payments (Loughran and Ritter,

2002; Reuter, 2006; Nimalendran, Ritter and Zhang, 2007; Liu and Ritter, 2010 and

2011; Goldstein, Irvine and Puckett 2011). Because the underwriters of

bookbuilding offers in Taiwan have larger bargaining power in setting the offer

prices, they tend to set offer prices close to the middle of prelimnary offer price

range. Moreover, institutional investors participating in the bookbuilding offers are

rational and less gullible by the pre-IPO market prices that are subject to insider

manipulation. Our empirical results support the self-dealing hypothesis by showing

that the offer prices of fixed-price offers set with reference to the pre-IPO market

prices are significantly higher than the offer prices of bookbuilding offers set close

to the middle of preliminary offer price range.

In addition, the theory of information cascade suggests that investors who

observe the investment choice made by previous investors can update their beliefs

about the value of IPO shares (Welch, 1992). The theory implies that individual

investors may update their beliefs based on pre-IPO market prices so that pre-IPO

market prices are positively related to aftermarket prices. If offer prices are adjusted

3 Prior studies also find that the pre-IPO market prices are higher than initial aftermarket prices (for

example, see Derrien and Kecskes (2007), Cornelli, Goldreich, and Ljungqvist (2006), Aussenegg,

Pichler, and Stomper (2006), and Dorn (2009).

- 5 -

upwards under the circumstance of artificially boosting pre-marker prices, the

short-run initial returns may be lower. However, stock performance may be poor if the

initial overvaluation is corrected in the long run. In contrast, if institutional investors

and underwriters of bookbuilding offers do not rely on pre-IPO market prices very

much and set the offer prices based on their own information and evaluation,

information cascade arising from pre-IPO market trades leads to short-run

overreaction at most in the aftermarket. Since the offer prices of bookbuilding offers

only partly reflect the level of pre-IPO market prices, the short-run initial returns

would be higher than those of fixed-price offers. Therefore, the long-run stock

performance of bookbuilding offers is expected to be better than that of fixed price

offers if the initial overreaction is corrected in the long run. In sum, our arguments

predict that the relatively lower (higher) offer prices are associated with higher (lower)

initial return and better (worse) long-run performance.

Both the introduction of pre-IPO market trading in 2003 and the introduction

of bookbuilding procedure in 2004 aim at enhancing price discovery for IPO firms.4

The natural setting of the Taiwan stock market with a sequential adoption of the

mandatory pre-IPO market trading and then bookbuilding offer allows us to

investigate which mechanism is effective in addressing IPO anomalies. Moreover,

when long-run performance is of interest, which one would prevail in mitigating the

alleged long-run underperformance of IPO firms? Our finding suggests that

underwriting procedure rather than pre-IPO market trading matters for both price

discovery and long-run post-IPO performance. According to the self-dealing

hypothesis, the higher the initial return is, the stronger the long-run performance.

Our findings have several policy implications. First, no matter what

underlying theories applied to explain abnormal initial returns, the most critical

point is the biased setting of offer price.5 How to reduce the information asymmetry

or agency problem between issuing firms and outsider investors and enhance price

discovery remains the most crucial issue for regulatory entities. Our findings from

the natural experiment of the IPO market in Taiwan suggest that bookbuilding rather

4 The Emerging Stock Market was initially instituted in 2002. IPO firms had the option of choosing

pre-IPO market trading at that time. Since January 1, 2003, all IPO firms had been required to have at

least 3-month pre-IPO market trading before the application of IPO. In January 2005, the duration of

mandatory pre-IPO trading was revised to 6 months. Furthermore, though bookbuilding offer was

initially allowed in 1995, it did not gain popularity because it is restricted to newly issued shares only.

At that time, old shares owned by pre-IPO shareholders are put for public subscription. Bookbuilding

offer has not been widely adopted by IPO firms until 2004 when the regulation stipulated that only

newly issued shares are eligible for public subscription. 5 Previous studies illustrate numerous possible explanations including information asymmetry (e.g.,

Ritter, 1984; Ritter and Welch, 2002), winner’s curse (e.g., Rock, 1986), signaling, timing (e.g.,

Allen and Faulhaber, 1989), overvaluation, over-optimistic, or over-reaction.

- 6 -

than pre-IPO market matters in ameliorating biased offer price and therefore

enhancing price discovery. Second, our sample allows us to compare bookbuilding

offers with fixed-price public offers given the mandatory pre-IPO market trading.

Bookbuilding is believed to be an ideal underwriting procedure in terms of price

discovery (Benveniste and Spindt, 1989; Sherman, 2000). Sherman (2005) also

illustrates the popularity of bookbuilding. It happens to the Taiwan IPO market that

bookbuilding had soon become the main stream in 2005 since its initial induction in

2004.6 In general, as compared to fixed-price public offer, bookbuilding is a better

underwriting procedure through which underwriters could collect information from

informed investors before setting the offer price.7 Our finding indicates that even

with the existence of pre-IPO market, the issues such as information asymmetry,

winner’s curse, and signaling that confronts the underwriters of fixed price offers

were not effectively tackled. Rather, the noise that exists in the pre-IPO market and

biases the setting of offer price for a fixed-price public offer remains salient in

affecting the aftermarket prices. For fixed-price public offers, setting offer prices

lower due to the concerns with information asymmetry, winner’s curse, and

signaling coupling with higher aftermarket prices arising from individual investors’

overoptimism or overreaction leads to higher initial returns (e.g. Benveniste and

Spindt, 1989; Spatt and Srivastava, 1991; Loughran, Ritter and Rydqvist, 1994). Our

finding renders little lenity to the proclaimed value of pre-IPO market trading.

Prior studies so far do not converge regarding the value of pre-IPO market

trading. Derrien and Kecskes (2007) indicate that the two-stage offering strategy

prevailing in the U.K. market is less costly than an IPO because trading reduces the

valuation uncertainty of these firms before they issue equity. They find that firms

with two-stage offering are associated with 10% to 30% lower in initial returns than

for comparable IPOs. By contrast, Goldreich and Ljungqvist (2006) and Dorn (2009)

indicate that retail buyers consistently overpay in the when-issued market relative to

the immediate aftermarket, and that was mainly due to investor sentiment. Sentiment

serves as a driver to affect when-issue prices and poor aftermarket returns. Cornelli,

Goldreich, and Ljungqvist (2006) use the midpoint of the filing price range as a

proxy of the fundamental value and the difference between fundamental value and

6 The underwriting system launched in 2004 indicates that bookbuilding IPOs need to have 50% of

issued shares put for open subscription. However, the underwriting system of having half

bookbuilding and half fixed-price offer indeed prolonged the overall underwriting schedule and

therefore was censured for inefficiency. In 2005 the underwriting system was reformed to be more

flexible that underwriters have the discretion of setting the proportion put for bookbuilding offer and

the proportion for fixed price offer which is subject to the ceiling of 20%. 7 Prior studies indicate that for tackling the problem of winner’s curse fixed-price offers need to have

higher price discount (e.g., Benveniste and Wilhelm, 1990, Spatt and Srivastava, 1991, Benveniste

and Busaba, 1997 and Biais and Faugeron-Crouzet, 2002)

- 7 -

grey market price as a proxy of investor sentiment. They find that in high sentiment

(indicating overoptimism) the grey market prices are a very good predictor of

first-day aftermarket prices, while they are not in low sentiment. Moreover, long-run

price reversal only exists in high sentiment. Our finding lends support to the limited

value of pre-IPO market trading that is unable to enhance price discovery. Rather,

the pre-IPO prices are subject to the adverse impact of individual investor sentiment

and/or manipulation.

In addition to the above studies, Chang et al. (2016) is probably the closest one

to ours. They examine 218 bookbuilding IPOs in Taiwan from the period 2005-2011

and find that the existence of the pre-IPO market facilitates price discovery in the

sense that the pre-IPO market price is predictive of the initial aftermarket price.

However, it remains a puzzling phenomenon that the average (median) initial return

of 55.3% (36.7%) seems to be inconsistent with the alleged benefit of pre-IPO

market. Nevertheless, they cite the argument put forth by Ritter (2011) that

information asymmetry comprises only a small portion of initial return. Rather, the

agency problem that is derived from underwriters’ rent-seeking behavior is the main

driver for a high average initial return. The major difference between our study and

Chang et al. (2016) is that we trace the sample back to 2003 and include both

bookbuilding and fixed-price public offers. The extension of sample period allows

us to make a comparison between the bookbuilding offers and fixed-price offers.

Therefore, we can test the self-dealing hypothesis by simultaneously including both

underwriting procedures and pre-IPO market.

The unique feature of our study is in sharp contrast with prior studies that use

bookbuilding IPOs only (e.g., Cornelli, Goldreich, and Ljungqvist, 2006; Aussenegg,

Pichler, and Stomper, 2006; Dorn, 2009). Our study potentially makes the following

incremental contributions to the IPO literature. First, we find that underwriting

procedures but not pre-IPO market trading prevails in affecting initial returns and

long-run performance. Second, we propose the self-dealing hypothesis that helps

explain the difference in setting offer prices between fixed-price public offers and

bookbuilding offers. Third, even though our finding of the positive relation between

pre-IPO market prices and aftermarket prices is consistent with the theory of

information cascade (e.g. Derrien and Kecskes, 2007; Goldreich and Ljungqvist, 2006;

Dorn, 2009; Chang et al., 2016), we are not as optimistic as prior studies that support

the efficient pre-IPO market trading. For example, Derrien and Kecskes (2007),

Goldreich and Ljungqvist (2006) and Dorn (2009) indicate that pre-IPO market prices

are a very good predictor of first-day aftermarket price. Chang et al. (2016) argue that

pre-IPO market prices are very informative about post-market prices. We find that

pre-IPO market trading is subject to insider manipulation and noisy trading (e.g.

- 8 -

Cornelli, Goldreich, and Ljungqvist, 2006; Dorn, 2009) and the positive relation

between pre-IPO market prices and aftermarket prices may be attributed to

information cascade. Finally, we connect the underwriting mechanism, initial return,

and long-run performance and find that underwriting mechanism is a major

determinant if offer prices fully (partially) reflect the levels of pre-IPO market prices,

then the initial return is relatively low (high) and long-run performance is relatively

weak (strong). Specifically, for fixed-price public offers, pre-IPO market trading

facilitates to keep both the offer price and aftermarket price relatively high, followed

by relatively lower average initial return of 8.95% and worse long-run stock

performance. In contrast, for bookbuilding offers, the offer prices are set relatively

low, which is then followed by relatively higher average initial return of 44.92% and

better long-run stock performance.

The rest of this paper proceeds as follows. Section 2 describes Taiwan’s IPO

Market. Section 3 reviews the relevant literature and develop hypotheses

accordingly. Section 4 discusses the data, variables, and empirical models. Section 5

presents the empirical results. Section 6 concludes the study.

2. IPO Market in Taiwan

As compared to IPO markets in other countries, the IPO market in Taiwan is

associated with two special attributes. First, since 2003 all IPO firms in Taiwan have

been required to have at least three-month pre-IPO market trading before listing.

Unlike other IPO markets where pre-IPO market trading is optional, the mandatory

pre-IPO market trading in Taiwan is exceptional and provides a clean IPO sample

without selection bias to examine the effectiveness of pre-IPO market trading.

Second, there are alternative underwriting procedures including bookbuilding,

fixed-price public offers, and auction to be freely chosen by issuing firms. This

feature allows us to compare the effectiveness between underwriting procedures.

2.1 Pre-IPO market

The main purpose of the pre-IPO market in Taiwan (the Emerging Stock Market,

ESM) instituted in 2002 was to enhance information transparency and visibility for

both firms preparing for getting listed following their IPOs and firms delisted from

major secondary markets. At that time, firms preparing for their IPOs had the option

to decide whether their shares are traded in the pre-IPO market before getting listed

formally. Starting January 1, 2003, all IPO firms were required to have at least

3-month pre-IPO market trading before getting listed. Since 2005, it was mandatory

for at least 6-month pre-IPO market trading before get listed on either the Taiwan

- 9 -

Stock Exchange (TWSE) or Gre-Tai Securities Market (GTSM), the two major

stock markets in Taiwan.

Compared to firms listed on TWSE and GTSM, firms that trade in the pre-IPO

market are subject to less rigorous requirements: they need to disclose financials

(audited annual/semi-annual financial statement) and important corporate events.

Moreover, they need to have written recommendations by two or more securities

firms, with one of which being the lead underwriter in the latter IPOs.

The trading in ESM is facilitated by market makers who come from the

recommending securities firms and offer bid and ask quotes during normal trading

hours through the Emerging Stock Computerized Price Negotiation and Click

System (the Click System). This is different from the order-driven system applied in

TWSE and GTSM markets. The ESM is a dealer market in which the recommending

securities firms act as market makers to assume the responsibility for continuous

trading. They quote bid and ask prices through the click system with the bid-ask

spread not exceeding 7% of the ask price. The market makers have the obligation to

trade at the quoted price when the order is smaller than 2,000 shares. For large order

that exceeds 10,000 shares, the trade is conducted through direct negotiation by

letter, telephone, or face-to-face talk. This is in sharp contrast with TWSE and

GTSM markets where all trades are through fully automated electronic trading

systems and only limit orders are accepted. Moreover, unlike the price limit applied

in TWSE and GTSM, there is no price limit in the ESM.8

Though both individual and institutional investors can trade on the ESM,

institutional investors are less likely to invest in ESM stocks because of high risks

associated with these stocks.9 Therefore, ESM trading is mainly comprised of retail

investors who tend to be noise traders. Moreover, insiders such as directors,

supervisors, and shareholders with more than 10% ownership are restricted from

selling after the firm has applied for an IPO. To sum up, several attributes associated

with the ESM in Taiwan including the quote system, no price limit, the main

composition of individual investors, and high liquidity risk give rise to price

manipulation in the ESM.10

The ESM in Taiwan is similar to U.K.’s Alternative Investment Market (AIM) in

which firms preparing for listing have the option to trade before getting listed.

8 Since June 1, 2015, the price limit has been 10% instead of 7% that had been applied in TSWE and

GESM for a long period of time. 9 Since 2011 mutual funds have been allowed to invest in the ESM. 10 The prices are easily manipulated because of low daily trading volume and no price limit.

Moreover, the high prices that are likely subject to insider manipulation are very attractive to

individual investors who tend to herd in trading stocks.

- 10 -

Nevertheless, there are several differences between the ESM in Taiwan and the AIM

in the U.K. First, pre-trading is mandatory for Taiwan’s IPO firms while optional for

U.K. IPO firms. Derrien and Kesckes (2007) find that there were only 11% of IPO

firms for the period 1995-2004 choosing the AIM for pre-market trading. Moreover,

there is no minimum duration for pre-IPO market trading for U.K. IPO firms. But

Taiwan’s IPO firms are required to be traded in the ESM for at least 6 months before

getting listed. Another similar type of pre-IPO market is found in the when-issued

markets prevailing in the European countries. Again, these pre-IPO markets are not

mandatory for European IPO firms and most of them are not unified and vary widely

from country to country (Cornelli, Goldreich and Ljungqvist, 2006). The pre-IPO

market trading in the European countries lasts only for a week or so before an IPO

firm gets listed.

In a nutshell, there are three distinctive features associated with Taiwan’s ESM

in our sampling period: (1) it is mandatory for firms seeking IPOs; (2) the duration

of pre-IPO trading is at least 3 (or 6) months; (3) the coexistence of pre-IPO market

trading and alternative underwriting procedures: bookbuilding and fixed-price public

offer. These distinctive features allow us to conduct a thorough investigation into the

impact of pre-IPO market on subsequent IPO stock performance. Specifically,

mandatory pre-IPO trading is free from the concern of selection bias. The long

duration of pre-IPO trading allows us to get a clear picture of how pre-IPO trading

affects subsequent prices in the offering and its aftermarket. The coexistence of

pre-IPO trading and alternative underwriting procedures gives us an opportunity to

examine whether pre-IPO market or underwriting procedures matter for the

enhancement of price discovery.

2.2 IPO underwriting methods

Fixed-price public offer was the only underwriting procedure in early days. To

enhance the marketability of newly issued shares, both the bookbuilding and auction

methods were inducted in 1995. Nevertheless, most bookbuilding IPOs in Taiwan

adopt hybrid bookbuilding in which half of the newly issued shared are reserved for

the tranche of fixed-price public offer.11 However, the bookbuilding method at its

first induction in Taiwan could be only applied to the issuance of primary shares. This

is in sharp contrast with the preference of issuing firms for using secondary shares in

IPOs. One reason for such a preference is that issuing primary shares in an IPO may

lead to greater regulatory scrutiny and a lengthy review process. To avoid

11 Since 2005 the underwriters of IPO firms adopting either auction or bookbuilding have had the

option of using pure auction/bookbuilding without reserving shares for the tranche of fixed-price

public offer.

- 11 -

administration procedures, issuing firms prefer selling secondary shares to investors.

For the period 1995-2003, IPO firms in Taiwan just used either pure fixed-price

public offer or hybrid auction (Chen and Wu, 2015). The use of secondary shares in

bookbuilding was allowed in 2004 so that hybrid bookbuilding was effectively

available for IPO firms since then. In 2005 the regulation was revised and stipulated

that only secondary shares are used in IPOs. From then on, bookbuilding became the

major underwriting procedure in Taiwan. In our sample period, there were pure fixed

price public offer, pure bookbuilding offer, and hybrid bookbuilding. Auction was

almost not used.

In fixed price public offers, individual investors are potential subscribers who

submit indication of buying shares up to three round lots (1,000 shares per round lot).

Institutional investors do not show any interest in participating in fixed price public

offers because of the constraint on order size. IPO lottery is used to determine share

allocation in the case of oversubscription. The offer price is negotiated and set by both

underwriters and IPO firms.

In bookbuilding offers, underwriters set a preliminary offer price range in the first

place. Investors are then invited to bid for the shares within the price range given. The

offer price is set based on the demand for and supply of the IPO shares. To avoid

ownership concentration, each investor is restricted from subscribing more than 3% of

the shares offered. Although individual investors are not excluded from bookbuilding

offers, the major participants are institutional investors.

Before 2005 the hybrid bookbuilding was performed by soliciting indication of

interests of investors at possible price levels first. The offer price was set after

bookbuilding; the same offer price was used in the tranche of fixed price public offer.

The investors in the tranche of public offer have the information of not only the

preliminary offer price range but the specific offer price when they subscribe to the

reserved shares. In 2005, to shorten the whole procedure, the hybrid bookbuilding was

carried out by synchronizing the bookbuilding and public offer tranches. That is, the

investors in the public offer tranche only know of the preliminary offer price range

but not the specific offer price.12 Figure 1 presents the detailed timeline. Moreover, to

prevent the possibility that underwriters purposely lower the offer price to benefit

bookbuilding investors, the rule in 2011 stipulated that both the lower bound of the

preliminary offer price range and the offer price could not be less than 70% of the

average of pre-IPO trading prices in the last ten days. For pure fixed price public

offers, there is no specific regulation for setting the offer price to be related to pre-IPO

12 In the fixed price public offer tranche, investors without any knowledge of the specific offer price

must deposit the dollar amount computed at the upper limit price in the preliminary offer price range.

- 12 -

trading prices.

3. Literature Review and Hypothesis Development

Pre-IPO or when-issued markets allow investors to trade for the shares of the

firms that are about to go public. However, whether a pre-IPO market facilitates price

discovery for IPO shares remains a puzzling issue. Unlike Taiwan where 3 (6)-month

pre-IPO market trading has been mandatory for firms seeking IPOs since 2003, the

U.K. gave firms an option to have their shares traded on the Alternative Stock Market

before getting listed (Derrien and Kecskés, 2007). Derrien and Kecskés (2007)

document that only 66 IPO firms chose to have an introduction on AIM before their

listing. These two-stage IPO firms have the average initial return of 11.9%, which is

significantly lower than 24.7% for the remaining 786 direct IPO firms. They argue

that the two-stage offering reduces valuation uncertainty and enhances price discovery

for the IPO firms, in turn, leads to a reduction of the initial returns.

In Europe, the pre-IPO markets are over-the-counter and vary widely from

country to country (Cornelli, Goldreich and Ljungqvist, 2006). The trading is

typically organized by independent brokers and dominated by retail investors

(Cornelli, Goldreich and Ljungqvist, 2006; Dorn, 2009). Moreover, the duration of

pre-IPO market trading typically lasts for only a week or so before the first IPO

trading day. Cornelli, Goldreich, and Ljungqvist (2006) indicate that investor

sentiment affects the price discovery function of pre-IPO market: in high-sentiment

market13 the pre-IPO prices are not only higher than offer price but also the initial

price (e.g. Dorn, 2009). Whether the high pre-IPO prices affect the offer price setting

depends on the relative bargaining power between issuing firms and associated

underwriters. The offer price tends to be set higher when issuing firms have higher

bargaining power, and that results in lower initial return. By contrast, the offer price

tend be set close to the middle point of the price range from bookbuilding procedure

when underwriters have higher bargaining power, and that results in higher initial

return. Moreover, when offer prices being set higher due to raising pre-IPO prices in

high sentiment market, the over-boosted price would be followed by long-run reversal

and therefore long-run underperformance. Dorn (2009) explores the German’s

when-issued market and find that 91 IPO firms choosing when-issued market trading

13 Cornelli, Goldreich, and Ljungqvist (2006) take the midpoint of the filing range as a proxy for the

underwriter’s ex ante prior of the fundamental value, and they define high sentiment is that pre-IPO

price is higher than midpoint of the filing range

- 13 -

before IPO are associated with the average initial return of 50%, which is lower than

the average initial return of 54% for the rest 36 IPO firms choosing direct IPO.

Since the when-issued market is mainly comprised of individual investors, high

investment sentiment would boost pre-IPO price as well as the initial price. The

overshooting in prices would be followed by long-run underperformance.

Chang et al. (2016) use 218 Taiwanese IPOs in the sample period 2005-2011 and

find that the pre-IPO market facilitates price discovery in the sense that the pre-IPO

price is predictive to the initial price. However, the average initial return of 55%

seems to be incongruent with the alleged merit associated with pre-IPO market. They

refer the argument put forth by Ritter (2011) that information asymmetry only

comprises a small portion of initial return. Rather, the agency problem manifested in

underwriters’ rent-seeking behavior is the main driver of initial return. Moreover,

Chang et al. (2016) find that both initial return and price error are significantly

positive, implying that the pre-IPO price is not only higher than offer price but also

initial price.14

We briefly summarize the similarities and differences from the above studies

regarding the pre-IPO market price, offer price and initial price. The similarities

include (S1) the pre-IPO price is higher than both the offer price and initial

aftermarket price, suggesting that overvaluation may exist in the pre-IPO market; (S2)

the initial price would gradually converge to the pre-IPO price. The differences

include (D1) the initial return would be lower (higher) when the offer price is (not) set

in accordance with the boosted pre-IPO price; (D2) whether the exitance of pre-IPO

market could facilitate price discovery for IPO shares remain a debatable issue.

In this study we propose the self-dealing hypothesis to analyze the relationship

among the pre-IPO market price, offer price, and initial aftermarket price. Moreover,

we argue that the relation among these prices in bookbuilding offers is different from

that in fixed price public offers. Those hypotheses are developed as follows.

3.1 Pre-IPO trading price and initial aftermarket price

There are three parties involved in an IPO process: the issuer, investors, and the

associated underwriter. The issuer would like to set a higher offer price for raising

more proceeds from the IPO and to have a higher initial market price that reflects the

wealth of shareholders. Based on the self-dealing motive, the issuer is likely to boost

the pre-IPO price at a higher level so that both the offer price and initial aftermarket

14 Price error is the ratio of the pre-IPO price on ESM over the closing price on the first trading day

on TWSE or GTSM. The statistics in Table 3 of Chang et al. (2016) indicate that the price errors on

one day and four days prior to IPO are significantly positive.

- 14 -

price could be higher than otherwise when the pre-IPO market price is used as a

benchmark. The boost of pre-IPO prices in Taiwan could be attainable based on three

facts. First, pre-IPO market trading is mainly comprised of individual investors who

tend to be noisy traders (Chiang, Qian, and Sherman, 2010). Second, trading in the

pre-IPO market is relatively inactive except for the first trading day.15 Third, there is

no price limit in pre-IPO trading in Taiwan’s EMS. The three facts together make the

EMS vulnerable to insider manipulation.

In addition, the theory of information cascade suggests that investors who

observe the investment choice made by previous investors can update their beliefs

about the value of IPO shares (Welch, 1992). If pre-IPO market trading prices are

boosted, these prices may become reference prices or signals to retail investors.

Therefore, pre-IPO market prices tend to be positively related to aftermarket prices

and lead to overreaction in the aftermarket. If offer prices are adjusted upwards under

the circumstance of artificially boosting pre-marker prices, the short-run initial returns

may be lower. Combining the issuer’s self-dealing motive and the theory of

information cascade, we develop the following testable hypothesis.

Hypothesis 1: The pre-IPO price is higher than both the offer price and the initial

aftermarket prices. The initial aftermarket prices would gradually

converge to the pre-IPO market price.

3.2 Pre-IPO trading price and offer price

From the perspective of an associated underwriter, setting the offer price is a

complex task. The underwriter tends to provide a preliminary offer price range based

on the issuing firm’s fundamentals. Moreover, the pre-IPO market prices give the

underwriter alternative information in setting the offer price. If underwriting fee that

is in proportion to the offering proceeds is of concern, the underwriter would prefer

setting a higher offer price. Alternatively, the underwriter may prefer setting a lower

offer price to minimize underwriting risks. Whether the offer price is set with

reference to the preliminary offer price range or the pre-IPO price depends on the

issuer’s attributes and the relative bargaining power between the underwriter and

issuer.

15 According to Chang et al. (2016), the ESM trading in the first 6 months is inactive. The average

daily dollar volume fluctuates around NT$ 4.1 million and the average daily turnover is around

0.07%, an annualized rate of about 17%. The median values are even lower.

- 15 -

Both informed and uninformed investors would prefer a lower offer price for

their best interests. However, because the pre-IPO market is associated with a

short-sales constraint and a restriction on share subscription, the pre-IPO market in

fixed price public offers is typically comprised of uninformed individual investors.

For these uninformed individual investors, pre-IPO market prices provide the major

information for them to judge whether the offer price and the initial aftermarket price

are reasonable. Therefore, the offer price could be set with reference to the boosted

pre-IPO market price. In a nutshell, for a fixed price public offer, setting the offer

price at a higher level is for the best interests of the issuing firm and underwriter, and

is also acceptable to uninformed individual investors. Because the offer price as well

as the initial aftermarket price are set higher when the pre-IPO market price is used as

a benchmark, we posit that the initial return calculated from the offer price to the

initial aftermarket price would be lower.

In a bookbuilding offer, the major participants are institutional investors. To deal

with these informed institutional investors, the lead underwriter tends to set a lower

offer price to benefit good-relation clients in exchange for side payments (Ljungqvist,

2007; Loughran and Ritter, 2002; Reuter, 2006; Ritter, 2011; Nimalendran, Ritter and

Zhang, 2007; Liu and Ritter, 2010 and 2011; Goldstein, Irvine and Puckett 2011). The

offer price is set in general with reference to the middle of offer price range while not

in tandem with pre-IPO market prices.16 Setting the offer price at a lower level would

be associated with a higher initial return.

Moreover, the relative bargaining power of underwriters also affects the setting

of offer price.17 In the IPO literature, Logue (1973) posits that relative bargaining

power between issuers and underwriters influences the magnitude of underpricing.

The underwriter’s bargaining power depends on his/her contribution to the

underwriting process and the client’s dependence on the resources contributed by the

underwriter. By contrast, the issuer’s bargaining power depends on the value of the

assets, rent generating capacity of the equity for sale, and financial independence

(Marshall, 2004). Prior studies have shed light on the measurementsof relative

bargaining power between issuers and underwriters.18

16 Cornelli, Goldreich, and Ljungqvist (2006) indicate that the midpoint of the filing price range is a

proxy of the issuer’s fundamental value assumed by the associated underwriter. 17 Many threads of literature such as international joint ventures, strategic alliances, and cooperative

agreements indicate that the relative bargaining power of the parties will have influences on the

control over decision making and allocation of equity or proceeds (Coff, 1999; Harrigan & Newman,

1990; Inkpen & Beamish, 1997; Khanna, Gulati, & Nohria, 1998; Lecraw, 1984; Yan & Gray, 1994). 18 Logue (1973) proposes a dichotomous variable based on whether the underwriter is on a list of

prestigious underwriters produced by Hayes (1971). For issuer bargaining power, he proposes that the

issue size could serve as a proxy. Carter and Manaster (1990) use the proxy of the ranking position of

an underwriter’s name within tombstone ads (Hayes, 1971).

- 16 -

In general, the underwriters of bookbuilding offers have relatively larger

bargaining power against the issuers than those of fixed price public offers do. This is

because bookbuilding offers require higher placement skills and capability to maintain

good relations with important clients than fixed price public offers do.19 This larger

bargaining power would motivate the underwriters to set lower and rational offer

prices. There are two major pieces of information for them to set offer prices: the

pre-IPO market prices and the indication of interests from bookbuilding. Because of

investment sentiment and/or insider manipulation, the pre-IPO market prices tend to

be boosted to a higher level than the indication of prices collected from

bookbuilding.20 We therefore posit that the offer price of a bookbuilding offer is set

close to the prices collected from bookbuilding, while the offer price of a fixed price

public offer is set close to the pre-IPO market prices.

Furthermore, investment sentiment would prevail in both the pre-IPO market

trading and the initial aftermarket trading. Because the offer prices of bookbuilding

offers are set with reference to bookbuilding procedure and are much lower than the

offer prices of fixed price public offers set with reference to pre-IPO market prices,

the short-run initial returns of bookbuilding offers would be higher than those of fixed

price public offers. Moreover, the initial aftermarket trading is also subject to investor

sentiment which results in initial overreaction (Cornelli, Goldreich, and Ljungqvist,

2006). This initial overreaction will be corrected in the long run. We posit that the

initial overreaction is higher for fixed price public offers than for bookbuilding offers.

Therefore, the long-run stock performance of bookbuilding offers would be better

than that of fixed price public offers if the initial overreaction is corrected in the long

run. To sum up, we develop the following testable hypotheses.

Hypothesis 2.1: The offer prices of fixed price public offers are set close to pre-IPO

market prices, which are much higher than the offer prices of

bookbuilding offers.

Hypothesis 2.2: The initial returns of fixed price public offers are lower than those of

bookbuilding offers.

19 Fagre and Wells (1982) indicate that bookbuilding underwriters can access to public equity

markets through their sales force and social and business networks. Moreover, their local knowledge

of large institutional investors allows them to precisely apprehend demand through the bookbuilding

process (Hoberg, 2007). Furthermore, the skill of using market knowledge during pricing

negotiations can be a resource that adds to bargaining power and advantage (Coff, 1999; Inkpen &

Beamish, 1997; Lecraw, 1984; Schelling, 1956). 20 Using pre-IPO market prices as a proxy of small investors’ valuation or sentiment, Cornelli,

Goldreich, and Ljungqvist (2006) find that high pre-IPO market prices are a very good predictor of

first-day aftermarket prices, while low grey market prices are not. Moreover, long-run price reversal

only follows high grey market prices.

- 17 -

Hypothesis 2.3: The long-run stock performance of fixed price public offers are worse

than that of bookbuilding offers.

4. Data, Variables, and Models

Our sample consists of 476 IPO firms in the period of 2003-2012. The data for

ESM, TWSE, and GTSM including prices, trading volume, and the number of

shares outstanding are collected from the Taiwan Economic Journal (TEJ), a data

vendor in Taiwan. Moreover, other data items such as firm age, assets, directors’

shareholdings, duration, leverage, and EPS are also collected from TEJ. IPO

characteristics such as offer prices, the number of shares issued, underwriters, and

auditing firms are collected from the IPO prospectus. All sample firms have been

subject to a regulation of ESM trading for at least 3 months since 2003 and 6 months

since 2005.

Table 1 reports the annual sample distribution and the average initial returns for

fixed price public offers and bookbuilding offers, respectively. The results show that

the number of firms choosing the fixed price public offer is significantly reduced

from 80 in 2003 to 1 in 2006. Starting from 2007, there was no IPO firm choosing

the fixed price public offer. In contrast, bookbuilding has been graduately accepted

by IPO firms as the only underwriting procedure.

We note that most bookbuilding IPOs in our sample are hybrid bookbuilding

offerings with two tranches.21 The process of bookbuilding tranche usually lasts for

four business days, and the process of fixed price offering tranche often starts one

day later than the bookbuilding tranche but ends at the same time. The

announcement of bookbuilding is accompanied with a suggested price range. The

final offer price is determined one day after the end of the bookbuilding process. We

find that the average initial return of fixed price public offers (8.9%) is much lower

than that of bookbuilding offers (44.9%).

<<Insert Table 1 Here>>

21 Among the 322 IPOs associated with bookbuilding, 313 IPOs are hybrid bookbuilding offerings

and 9 IPOs are pure bookbuilding ones.

- 18 -

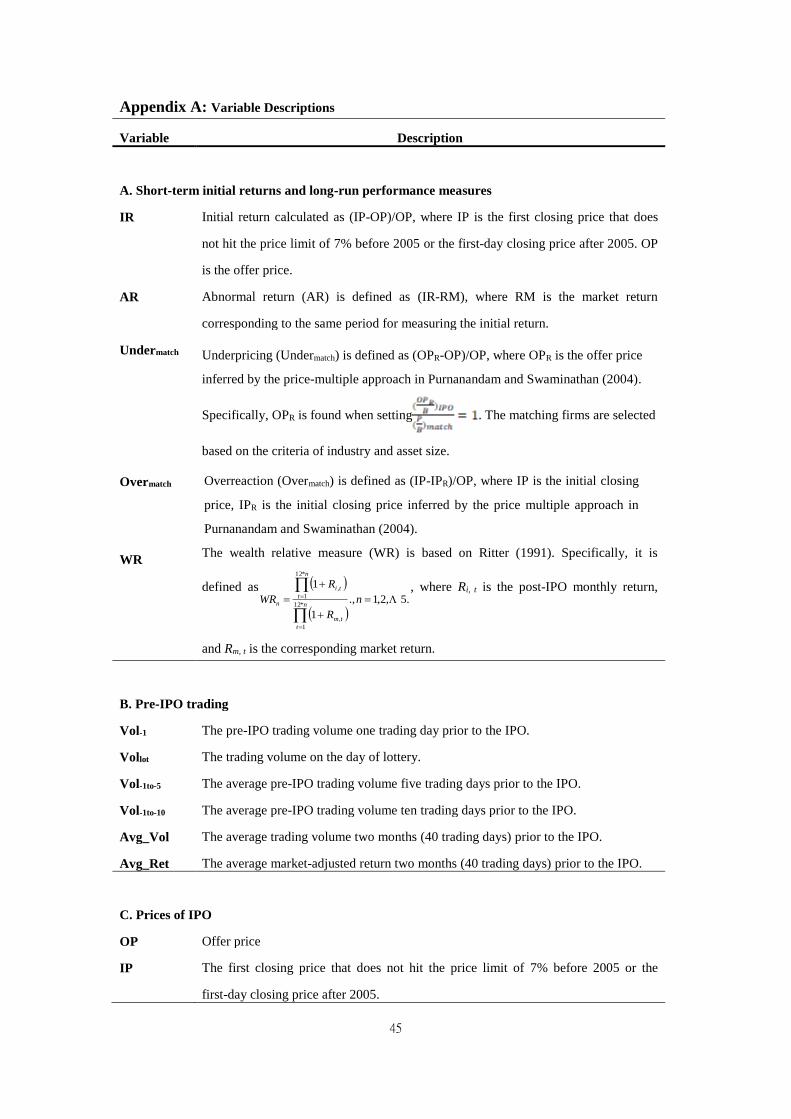

We provide the description of each variable in Appendix A. Table 2 reports the

summary statistics for variables. The initial return which is the percentage change

from the offer price to the initial closing price is 33.3% on average. The average

market-adjusted initial return is 42.0%. We also use the price-multiple approach in

Purnanandam and Swaminathan (2004) to estimate the fundamental offer price that

are derived from the price multiples of matching firms which are listing firms, close

in asset size, and in the same industry as the IPO firm. Specifically, the fundamental

offer price (OPR) is obtained from the following condition

. (1)

We then calculate the underpricing of the offer price (Undermatch) with respect to

the fundamental offer price as

. (2)

The average underpricing of offer price with respect to the fundamental offer price

is -16.9%, suggesting that the original offer price is not underpriced on average.

That is, the typical original offer price is set much higher than the estimated

fundamental offer price.

The setting of offer price at a relatively low level would result in a price

increase when shares are initially traded in the aftermarket (Aggarwal and Rivoli

(1990), Ljungqqist et al. (2006), Baker and Wurgler (2006), Dorn (2009) and Clarke

et al. (2016)). Therefore, we also calculate the overreaction of the initial price with

respect to the matching firm (Overmatch). Again, we use the price multiple approach

in Purnanandam and Swaminathan (2004) and estimate the fundamental initial price

with respect to the matching firm. The overreaction of the initial price is calculated

as

. (3)

The average overreaction of the initial price with respect to the matching firm is

50.6%. The results from the overestimation of offer price and the overreaction of the

initial price suggest that both the pre-IPO market and the post-issuance market in

Taiwan may be affected by high investor sentiment that boosts the level of offer

price as well as the initial closing price.

- 19 -

For measuring long-run stock performance, we follow Ritter (1991) and

calculate the wealth relative from 1 year through 5 years following the IPO as

.5,2,1,

1

1

*12

1

,

*12

1

,

n

R

R

WRn

t

tm

n

t

ti

n

(4)

, where Ri, t is the post-IPO monthly return, and Rm, t is the corresponding market

return. When the wealth relative is greater than 1, it suggests that the IPO firm

outperforms the market. We find that the average (median) WR1 through WR5 are

1.21 (1.04), 1.23 (0.95), 1.31 (0.94), 1.23 (0.83), and 1.19 (0.84), respectively.

For the pre-IPO market trading, we report the trading volume on the trading day

immediately prior to the IPO listing day (Vol-1), the trading volume on the day of

IPO lottery (Vollot), the average daily trading volume five days prior to the IPO

listing day (Vol-1to-5), the average daily trading volume ten days prior to the IPO

listing day (Vol-1 to -10), and the average daily trading volume two months prior to

IPO (Avg_Vol). The means in terms of thousand shares (one round lot) are 310.8,

179.1, 327.5, 1,361.9, and 146.9, respectively.

For the relevant prices of IPOs, we report the offer price (OP), the initial closing

price (IP), the fundamental offer price (OPR), the pre-IPO market price on the

trading day immediately prior to the IPO listing day (P-1), the pre-IPO market price

on the IPO lottery day (Plot), the pre-IPO market price two months prior to the IPO

listing day (AvgP), and the middle price of the price range for bookbuilding offers

(MidP). Their means are NT$46.2, NT$62.9, NT$28.6, NT$66.1, NT$65.0,

NT$63.3, and NT$50.0, respectively. The result indicates that the pre-IPO market

prices are higher when compared with the fundamental offer price estimated from

the matching firms and when compared with the middle price of the price range

from bookbuilding offers. We note that the average pre-IPO market prices such as

P-1, Plot, and AvgP are not only higher than the average offer price but also higher

than the average initial closing price, indicating that the pre-IPO market prices may

be overestimated.

We also measure the overvaluation of the pre-IPO market price on the IPO

lottery day when gauged with respect to the offer price(OVPlot-OP), the initial offer

price(OVPlot-IP), and the matching firms as the benchmark(OVPlot-match), respectively.

The average overvaluation gauged with respect to offer price, the initial offer price,

and the matching firms are 36.38% and 3.30%, 53.54%, and 43.62% respectively.

Finally, we use the offer price and the initial closing price as the benchmark to

- 20 -

measure the underpricing and overreaction of the middle price of the price range

from bookbuilding offers and find the average underpricing(UnderMidP) and

overreaction (OverMidP) are 1.24% and 43.62%.

As for the other characteristics of IPO firms, the average DGTSM of 0.75 indicates

that around three quarters of IPO firms are listed on the Gre-Tai Stock Market

because the thresholds for listing are lower for GTSM than for TWSE. Moreover,

75.8% of the IPO firms are from the electronics industry. It is consistent with the

fact that the electronics industry was the major driver for the economic development

in Taiwan over the sample period. When considering the reputation effect of auditing

firms and underwriters, we find that 81% of the IPO firms would choose to have

their financial reports audited by the big-4 auditing firms, and 85% of them would

choose reputable underwriters. The results are consistent with the prior studies on

the reputation effects of auditing firms and underwriters (see, for example, Carter

and Manaster (1990), DeAngelo (1981), and Megginson and Weiss (1991)).

Furthermore, we define the lottery odds (or the subscription success rate) as the

ratio of the number of shares offered to the public to the number of shares

subscribed by investors (Lottery). In general, a hot IPO is associated with a larger

number of subscription orders and therefore with the lower lottery odds. The average

lottery odds are 17%. The average age of the IPO firms when going public (Age) is

around 14 years. We also collect the data of duration (Duration) which is the number

of calendar days from the announcement of the IPO procedure to the initial listing

day. The average duration is 20 days. For insider ownership, we calculate the total

shareholdings owned by the directors and supervisors one year prior to the IPO

(Dir_Share). The average shareholdings owned by these insiders are 34.2%. Also,

the average debt-to-equity ratio is 35.8%, and the average earnings per share is

NT$3.74.

<<Insert Table 2 Here>>

5. Empirical Results

In Table 3 we conduct the tests in differences between the fixed price public

offers and bookbuilding offers. Panel A reports that the mean and median initial

returns (44.9% and 27.7%) and market-adjusted initial returns (49.3% and 29.0%)

for bookbuilding offers are significantly positive and larger than those of fixed price

offers. Moreover, for bookbuilding offers the mean and median underpricing gauged

with respect to their matching firms (-9.4% and -31.9%) are significantly higher than

- 21 -

those of fixed price offers. Since the underpricing is negative, the results suggest

that the offer prices are relatively overestimated, and such overvaluation is higher

for fixed price offers than for bookbuilding offers. For the overreaction of initial

aftermarket prices, we find that bookbuilding offers are associated with larger

overreaction of initial closing prices (55.0%) than fixed price offers are (41.5%).

We further examine the subsequent long-run stock performance based on the

wealth relative developed by Ritter (1991) and find that bookbuilding offers are

associated with higher wealth relative measures than fixed price offers particularly

for the first three years. The overall picture in Panel A indicates that compared to

fixed price offers, bookbuilding offers tend to set lower offer prices, which are

followed by larger price increases when IPO shares are initially traded in the

aftermarket and by higher wealth relative measures in subsequent three years. We

note that our samples for both bookbuilding and fixed price offers are selected from

the period when all IPO firms were required to be traded in the pre-IPO market

before their official listing. If pre-IPO market trading is an effective mechanism to

mitigate information asymmetry, we do not expect to find a significant difference in

the underpricing of offer price, in the overreaction of initial closing price, and in the

wealth relative measures between bookbuilding and fixed price offers. For a

robustness check, in Panel B we alternatively measure the overvaluation of the

pre-IPO market price on the IPO lottery day guaged with respect to offer price, the

initial offer price, and the matching firms. Compared to fixed price offers,

bookbuilding offers are still associated with lower offer prices and larger

overvaluation of initial closing prices.

In Panel C we examine the underwriting and firm characteristics between the

fixed price and bookbuilding offers. The IPO firms using the fixed price public offer

are more likely to be listing on the GTSM than those using the bookbuilding offer.

Since the listing requirements in terms of profitability and firm size are higher for

listing on the TWSE than for the GTSM, the result suggests that smaller and less

profitable firms are more likely to be listing on the GTSM than on the TWSE. The

firms using the bookbuilding offer are more likely to be associated with big-4

auditing firms than those choosing the fixed price offer. In contrast, the firms using

the fixed price offer tend to be associated with larger underwriters than those using

the bookbuilding offer. Moreover, we find that the odds of IPO lottery are higher for

the firms using the fixed price offer than for the bookbuilding IPO firms. Two

factors may explain the pattern. First, the firms using the fixed price offer are less

favorable to investors than the bookbuilding IPO firms. Second, since a certain

portion of the newly issued shares are distributed to the bookbulding investors for

- 22 -

the hybrid bookbuilding offers prevailing in Taiwan, the remaining portion left for

the public offer tranche would reduce the odds of IPO lottery with other conditions

being the same.

Moreover, we find the average duration for completing an IPO is shorter for the

bookbuilding offers (15.5 days) than for the fixed price offers (29.9 days). The

average offer price for bookbuilding offers (NT$49.9) is significantly higher than

that for fixed price offers (NT$38.6). Although the bookbuilding offers have a

higher average offer price than the fixed price offers, the bookbuilding offers tend to

be underpriced (with respect to their benchmark values) to a greater extent than the

fixed price offers do. The evidence can be seen in Panel B where all underpricing

measures with different benchmarks are higher for bookbuilding offers than for

fixed price offers. The average firm size in terms of total assets and earnings per

shares are both higher for bookbuilding offers than for fixed price offers.

Finally, in Panel D we report the test in differences of pre-IPO trading volume

between bookbuilding offers and fixed price offers. The results indicate that

bookbuilding offers are associated with higher trading volume than fixed price

offers are either on a specific day (the last pre-IPO trading day and the IPO lottery

day) or for a specific period of time (the last five pre-IPO trading days, the last ten

pre-IPO trading days, and the two months immediately prior to the IPO trading day).

<<Insert Table 3 Here>>

Table 4 reports the regression results. In Panel A we examine the effects of

underwriting procedure on the short-term performance measures including the initial

return, market-adjusted initial return, underpricing of offer price with respect to the

matching firm, and overreaction of initial closing price with respect to the matching

firm. The most critical variable of interest is the dummy variable of bookbuilding

offer (Dbookbuilding), which is set equal to one for bookbuilding offers, and zero

otherwise. We find that the regression coefficient is significantly positive for the

regression of initial return and for the regression of underpricing. That is, the

bookbuilding IPO firms are associated with higher initial returns and are

underpriced to a greater extent than the fixed price offering firms.

For the other control variables, we find that the firms seeking to be listing on the

GTSM tend to be underpriced. IPOs associated with higher odds of lottery tend to

have lower initial returns and smaller overreaction of initial closing price, suggesting

that these IPOs are relatively cold issues. Moreover, old, large, or long-duration

IPOs are less favored by the market and therefore are associated with lower initial

returns and lower overreaction of the initial closing price. Furthermore, we find that

- 23 -

IPO firms with higher earnings per share are associated with lower underpricing and

higher overreaction, suggesting that investors do factor the IPO firm’s fundamentals

into pricing.

In Panel B we examine the effects of the pre-IPO trading volume (Vollot) and

price-to-book ratio (Plot/B) on the short-term performance measures. We use the

pre-IPO trading volume on the IPO lottery day as the proxy of pre-IPO market

trading volume. In addition, for normalization across all IPO firms, we use the

price-to-book ratio, Plot/B, on the IPO lottery day as the proxy of pre-IPO market

valuation. This ratio can also be viewed as a measure of “overvaluation” to some

extent in the pre-IPO market trading.

The regression results show that both the pre-IPO trading volume and pre-IPO

market valuation are significantly and positively related to the initial return,

market-adjusted initial return, and overreaction of initial closing price. However,

pre-IPO market valuation is significantly and negatively related to the underpricing

of offer price with respect to its matching firm. After taking the pre-IPO trading

volume and pre-IPO market valuation into account in the regression models, we still

find that bookbuilding IPO firms tend to be underpriced more than the fixed price

offering firms.

We also use other proxies such as Vol-1, Vol-1to-5, Vol-1to-10, and Avg_Vol for

pre-IPO market trading volume and find that the results remain qualitatively similar.

We do not report these results for brevity.

Overall, we find that bookbuilding IPO firms tend to be underpriced more than

the fixed price offering firms. Both active pre-IPO trading and pre-IPO market

valuation are positively related to the overreaction of initial closing price, which

leads to significantly higher initial returns and market-adjusted initial returns.

Moreover, such pre-IPO market valuation helps reduce the underpricing of offer

price.

<<Insert Table 4 Here>>

In Table 5 we investigate the effects of underwriting procedure, pre-IPO market

underpricing, and pre-IPO market overvaluation on the long-run performance which

is measured by the post-IPO wealth relatives as used in Ritter (1991). In Panel A we

examine the impact of underwriting procedure on the long-run performance of IPO

firms. The dummy variable of bookbuilding offer (Dbookbuilding) is positively related

to WR1, WR2, and WR5, suggesting that IPO firms using bookbuilding offers exhibit

better long-run performance as compared to those using the fixed price offer. The

- 24 -

results are consistent with those of univariate analysis as reported in Panel A of

Table 3.

In Panel B of Table 5 we further include pre-IPO market overvaluations with

respect offer price (OVPlot-OP), the matched firms (OVPlot-match), and the initial

closing price (OVPlot-IP) in the regression models and examine how they are related

to the long-run performance measures. Pre-IPO market overvaluations are measured

by the difference between the pre-IPO market price on the IPO lottery day and the

offer price, the rational offer price with respect to the matching firm (OPR) and

initial closing price normalized by the offer price. The results indicate that pre-IPO

market overvaluation with respect to offer price is positive related to the first year

performance (WR1). In contrast, pre-IPO market overvaluations with respect to the

matched firm’s price and the initial closing price are negatively related to some or

all of the long-run performance measures (WR4 and WR5, WR1~WR5). That is,

relatively high pre-IPO market prices due to investor sentiment or possible insider

manipulation in the pre-IPO market are associated with poor long-run performance.

That is, if the offer price is set higher due to investor sentiment or possible insider

manipulation in the pre-IPO market that results in high pre-IPO market prices, the

boosted offer price (or lower pre-IPO market underpricing) would have a

detrimental effect on long-run performance of IPO firms. Alternatively, if the offer

price is set lower, the post-IPO market prices would rebound to higher levels,

leading to better long-run performance.

<<Insert Table 5 Here>>

In Panels A and B of Table 6, we investigate how pre-IPO market trading and

pre-IPO market valuation affect the short-term performance measures and the

long-term performance of fixed price offers, respectively. For short-term

performance in Panel A, only pre-IPO market trading is positively related to the

overreaction of initial closing price, leading to significantly higher initial returns and

market-adjusted initial returns. Pre-IPO market trading also helps reduce the

underpricing of offer price. However, pre-IPO market valuation is not significantly

related to the short-term performance measures of fixed price offers.

In Panels B of Table 6, we investigate how pre-IPO market overvaluations affect

the long-term performance of fixed price offers. The result indicates that pre-IPO

market overvaluation with respect to the matched firms’ price is negatively related

to the long-term performance measures (WR3, WR4, and WR5), and the pre-IPO

market overvaluation respect to the initial closing price is negatively related to the

- 25 -

long-term performance measures (WR1~WR5), too. In contrast, the pre-IPO market

overvaluation with respect to the offer price has no significant impact on the

long-term performance measures. That is, for fixed price offers, if the pre-IPO

market prices are relatively higher, with respect to matched firms’ price and initial

closing price, due to investment sentiment or possible insider manipulation that

would have a detrimental effect on long-run performance.

We elaborate more on these findings. First, we further extend the sample period

back to 1996 when pre-IPO market trading had not been adopted yet (unreported).

We compare the initial returns before and after the introduction of mandatory

pre-IPO market trading and find that the mean (median) initial return is 27.4%

(14.7%) before the introduction of pre-IPO market trading. The mean (median)

return significantly increases to 33.3% (18.9%) after the introduction of mandatory

pre-IPO market trading. However, the increases in initial returns are mainly

attributed to bookbuilding offers. For fixed price offers, the introduction of

mandatory pre-IPO market trading results in a significant reduction of the mean

(median) initial return from 27% (15%) before the introduction to 9% (6%) after the

introduction. On the one hand, the results from fixed price offers are generally

consistent with those in Derrien and Kecskes (2007) that pre-IPO market trading

facilitates price discovery. Therefore, pre-IPO market prices serve as good

predictors for initial after-market prices. On the other hand, the results are likely due

to noisy traders who actively participate in both the pre-IPO market and the IPO

after-market. The high investor sentiment boosts both the pre-IPO market prices and

the initial after-market prices in a similar manner. This explanation is close to those

offered in Cornelli, Goldreich, and Ljungqvist (2006) and Dorn (2009). At first

glance, pre-IPO market trading enhances price discovery because of the finding of

the reduction of average initial return. However, together with the evidence of

long-run WRs, the results suggest that the reduction of initial returns arises from the

setting of higher offer prices. If both the pre-IPO market prices and the initial

after-market prices are boosted by high investor sentiment, the long-run stock

performance tend to be poor, which is consistent with our findings.

<<Insert Table 6 Here>>

In Panels A and B of Table 7, we investigate how pre-IPO market trading and

pre-IPO market valuation affect the short-term performance measures and the

long-term performance of bookbuilding offers, respectively. For short-term

performance in Panel A, both pre-IPO market trading and pre-IPO market valuation

are positively related to the overreaction of initial closing price, leading to

significantly higher initial returns and market-adjusted initial returns. In addition,

- 26 -

pre-IPO market valuation for bookbuilding offers helps reduce the underpricing of

offer price. The results are consistent with those reported in Panel B of Table 4.

In Panels B of Table 7, we investigate how pre-IPO market overvaluations affect

the long-term performance of bookbuilding offers. The pre-IPO market

overvaluation with respect to the offer price has positively related to the long-term

performance measures (WR1 and WR3), while the pre-IPO market overvaluation

with respect to the initial closing price affect the long-term performance. The result

indicates that pre-IPO market overvaluation is only negatively related to the

third-year performance (WR3). That is, for bookbuilding offers, if the offer prices

are set relatively lower, the after-market prices would rebound to higher levels,

leading to higher initial returns and better long-run performance.

We also find that the introduction of mandatory pre-IPO market trading mainly

involves in individual noisy traders. It is possible that the involvement of noisy

traders would be more for fixed price offers than for bookbuilding offers. During the

process of a bookbuilding offer, sophisticated investors including institutional

investors are invited to indicate their willingness of buying IPO shares, and these

sophisticated investors may also involve in trading in the after-market. However,

this is not the case for fixed price offers because institutional investors do not

participate in IPO lottery due to a small number of shares (usually 1,000 shares)

which each participating investor can purchase. Therefore, high investor sentiment

prevails in both the pre-IPO and post-IPO markets due to the involvement of

individual noisy traders.

<<Insert Table 7 Here>>

The results show that for both types of offers the pre-IPO market trading volume

is positively related to initial returns, the market-adjusted initial returns, and the

overreaction of initial closing prices. This is somewhat inconsistent with Derrien and

Kecskes (2007) who argue that a pre-IPO market provides two-stage offering and

therefore reduces valuation uncertainty associated with IPO firms. If their argument

is valid in our setting, we would expect to find a negative relation between the

pre-IPO market trading volume and the initial returns. In contrast, Dorn (2009)

indicates that the retail purchases in the when-issued market can serve as a proxy of

retail sentiment. They find that IPOs aggressively bought by individual investors in

the when-issued market exhibit high first-day returns. Individual investors who

actively trade in the pre-IPO market as well as in the aftermarket result in higher

initial returns and overreaction of the initial closing price. Therefore, our findings of

- 27 -

the positive relation between the pre-IPO market trading volume and initial returns

are consistent with those in Dorn (2009).

One major feature to contrast our findings with those of prior studies is that the

pre-IPO market trading is mandatory for all IPO firms in Taiwan. Such a regulatory

requirement helps eliminate the bias of sample selection. It is surprising to find that

the compulsory pre-IPO market trading mainly attracts noisy traders. As a

consequence, such active noisy trading tends to boost the initial closing prices and

initial returns to higher levels. The most critical difference between the fixed price

offers (Panel A) and bookbuilding offers (Panel B) is the impact of pre-IPO market

trading on the underpricing. In Panel A of Table 6, we find that the coefficient on

pre-IPO market trading volume is significantly negative. But the coefficient is

insignificant for the bookbuilding offers in Panel A of Table 7. The result suggests

that the setting of offer price is positively affected by the pre-IPO market trading

volume for fixed price offers. Furthermore, it is worth noting that pre-IPO market

valuation is not significantly related to the short-term performance measures of fixed

price offers. In contrast, the valuation multiple in the pre-IPO market is negatively

related to underpricing for bookbuilding offers.

6. Conclusion

In this study we explore the joint effect of pre-IPO market trading and

underwriting procedures on short-term and long-term performance of IPO firms in

Taiwan where pre-IPO market trading is mandatory for all IPO firms. Though our

finding of the predictive power of pre-IPO market price on the initial market price

seems to echo the previous findings in Cornelli, Goldreich, and Ljungqvist (2006),

Derrien and Kecskes (2007), Dorn (2009), and Chang et al., (2016), we believe that

the predictive power is mainly due to the fact that individual investors who prevail

in both the pre-IPO market and after-market prompt the issuers’ manipulation and

information cascade that affects both pre-IPO market prices and initial after-market

prices. We further examine the role of underwriting procedure and find that