practical planning for aging and elder issues - aicpa · practical planning for aging and elder...

TRANSCRIPT

Practical Planning for Aging and

Elder Issues

Presented by:

James Shambo, Moderator

Jean-Luc Bourdon

Dirk Edwards

Personal Financial Planning Section #AICPApfp 2

Helpful Hints

Adjust your volume• Be sure your computer’s sound is turned on as well.• Click this blue button. Slide the control to the left or right to fit

your needs.

Ask your questions• Feel free to submit content related questions to the speaker by

clicking this red button. • Someone is available to assist with your technology and CPE

related questions as well.

Download your materials• Access today’s slides and learning materials by clicking this green

‘Resources’ button at any time during this presentation• If you need help accessing these materials send a message

through the Q&A application

Personal Financial Planning Section #AICPApfp 3

About the PFP Section & PFS Credential

The AICPA Personal Financial Planning (PFP) Section is the

premier provider of information, tools, advocacy and guidance for

CPAs who specialize in providing estate, tax, retirement, risk

management and/or investment planning advice to individuals,

families and business owners. (Learn more at aicpa.org/PFP.)

The Personal Financial Specialist (PFS) program allows CPAs to

gain and demonstrate competence and confidence in providing

estate, tax, retirement, risk management and/or investment

planning advice to individuals, families and business owners

through experience, education, examination, and a resulting

credential. (Learn more at aicpa.org/PFS.)

Personal Financial Planning Section #AICPApfp 4

Today’s Speakers

James Shambo, CPA/PFS (Moderator)

Lifetime Planning Concepts, Inc.

Jean-Luc Bourdon, CPA/PFS

BrightPath Wealth Planning

Dirk Edwards, CPA/PFS, JD, MBA

Edwards Consulting LLC

Personal Financial Planning Section #AICPApfp 5

Today’s Agenda

AICPA PFP survey on retirement planning

trends

Retiree health care statistics and studies

Discussing the human issues

Tax, insurance, and benefits planning

Managing documents

Retirement projection issues

Elder care resources

Elders on the move resources

PFP Section resources

Personal Financial Planning Section #AICPApfp

AICPA PFP Survey on

Retirement Planning Trends

6

Personal Financial Planning Section #AICPApfp 7

Quarterly PFP Trends Survey

Quarterly survey of CPA financial planners on

specific topics

Quantifies trends and issues to talk about

proactively with clients, media and other

professionals

The inaugural Q1 survey addressed general

retirement planning trends

• Use these statistics and trends to open conversations on these

issues with your clients, to broaden relationships with your local

media, and to communicate the value that you can provide to

your clients

• The complete executive summary and the media release can be

found at: www.aicpa.org/pfp/trendsurvey

Personal Financial Planning Section #AICPApfp 8

Dealing with diminished capacity and dementiaissues

Social Secutiy decisions

Longevity concerns

Asset withdrawal decisions

Healthcare costs

Running out of money

% of CPA's that identified this as a concern of their clients

Overall Retirement Planning Concerns for Clients

#1 Concern #2 Concern #3 Concern

79%

56%

50%

29%

20%

19%

57% said running out of money was their client’s top concern, followed

by health care costs and asset withdrawal decisions

Source: 2015 Q1 AICPA PFP Trends Survey

Personal Financial Planning Section #AICPApfp 9

Factors Causing Client Stress About Running

Out of Money

0%

10%

20%

30%

40%

50%

60%

70%

80%

Healthcarecosts

Marketfluctuations

Lifestyleexpenses

Unexpectedcosts

Being afinancialburden

Desire toleave

inheritance

Financialsupport of

children

31%27%

19%

8% 7%

27%

18%

19%

18%

8%

18%

17%

14%

20%

9%

13%

7%

% o

f C

PA's

Iden

tify

ing

Stre

ss F

acto

rs

#1 Factor #2 Factor #3 Factor

A "top 3" concern for:

76%

62%

52%

46%

24%21%

12%

Top 3: staying healthy,

investments, managing

lifestyle

Source: 2015 Q1 AICPA PFP Trends Survey

Personal Financial Planning Section #AICPApfp 10

Unexpected Events Impact Retirement Planning

18%

18%

18%

26%

29%

30%

42%

Adult child returning home

Job loss

Divorce

Diminished capacity/dimentia

Care for aging relatives

Other (most freq: income/market changes)

Healthcare concerns

% of Clients That Experience These Unexpected Events

Source: 2015 Q1 AICPA PFP Trends Survey

Personal Financial Planning Section #AICPApfp 11

Client Attitudes on Potential for Diminished

Capacity During Retirement Planning

In spite of CPA financial planners’ involvement,

• 55% had clients discussing actions but still not making a decision.

• 34% reported clients either ignoring, or reacting to it after the fact.

11%

55%

21%

13%

Taking proactive steps now to prepare

Discussing but not sure what to do

Reacting to it when and if it happens

Ignoring the issue

% of Respondents

Source: 2015 Q1 AICPA PFP Trends Survey

Personal Financial Planning Section #AICPApfp 12

Q2 Survey on elder planning issues

The 2015 2nd quarter survey addresses elder

planning issues of housing decisions, financial

abuse and fraud, and financial services needed

Plan now to use the results of this survey with your

clients, media, and other professionals

Look for results to be available shortly in the weekly

PFP News and posted at:

www.aicpa.org/pfp/trendsurvey

Personal Financial Planning Section #AICPApfp

Health Care Statistics

and Studies

13

Personal Financial Planning Section #AICPApfp 14

Annual health care costs study

Percentile Ages 65 to 79 Ages 80 to 89 Over age 90

25th percentile $1,285 $1,452 $858

Median $3,210 $3,417 $3,255

75th percentile $6,219 $6,429 $6,706

90th percentile $10,456 $11,229 $15,976

95th percentile $13,918 $15,492 $28,339

Includes out of pocket uninsured costs of health insurance including Medigap supplemental insurance, out of pocket costs for medical supplies, drugs, hospital care, doctor services, lab tests, eye, dental and nursing home care.

Source: Employee Benefits Research Institute – September 2014

Personal Financial Planning Section #AICPApfp 15

Average couple’s lifetime health care costs

in today’s dollars

Age of Retirement Lifetime estimated costs

Age 62 $271,000

Age 65 $220,000

Age 67 $200,000

Hypothetical couple with life expectancies of 82 male and 85 female

Estimated costs do not include nursing home care, over the counter medications or most dental services and applies only to retirees with traditional Medicare coverage.

Source: Fidelity Benefits Consulting 2014 Study

https://www.fidelity.com/bin-public/060_www_fidelity_com/images/2014-RHCCE-longform-graphic.jpg

Personal Financial Planning Section #AICPApfp 16

Pre-retirees expectations for lifetime health

care costs

Expected Costs Percentage of respondents

$200,000 or more 10%

$150,000 to $200,000 3%

$100,000 to $150,000 8%

$ 50,000 to $100,000 11%

Under $50,000 57%

Source: Fidelity Benefits Consulting 2014 Studyhttps://www.fidelity.com/bin-public/060_www_fidelity_com/images/2014-RHCCE-longform-graphic.jpg

Personal Financial Planning Section #AICPApfp 17

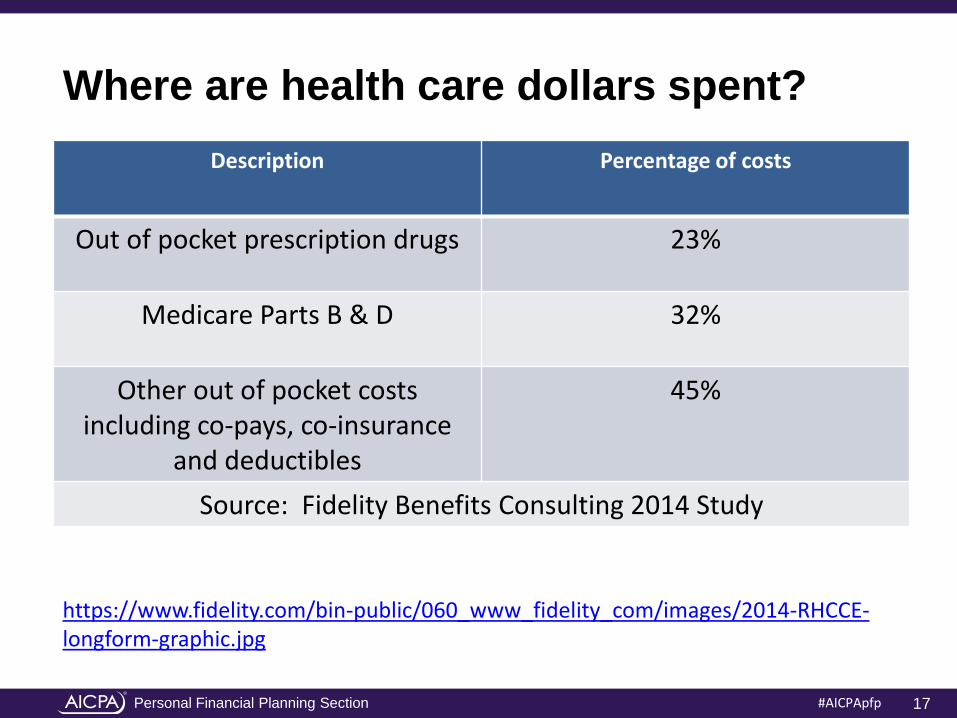

Where are health care dollars spent?

Description Percentage of costs

Out of pocket prescription drugs 23%

Medicare Parts B & D 32%

Other out of pocket costs including co-pays, co-insurance

and deductibles

45%

Source: Fidelity Benefits Consulting 2014 Study

https://www.fidelity.com/bin-public/060_www_fidelity_com/images/2014-RHCCE-longform-graphic.jpg

Personal Financial Planning Section #AICPApfp 18

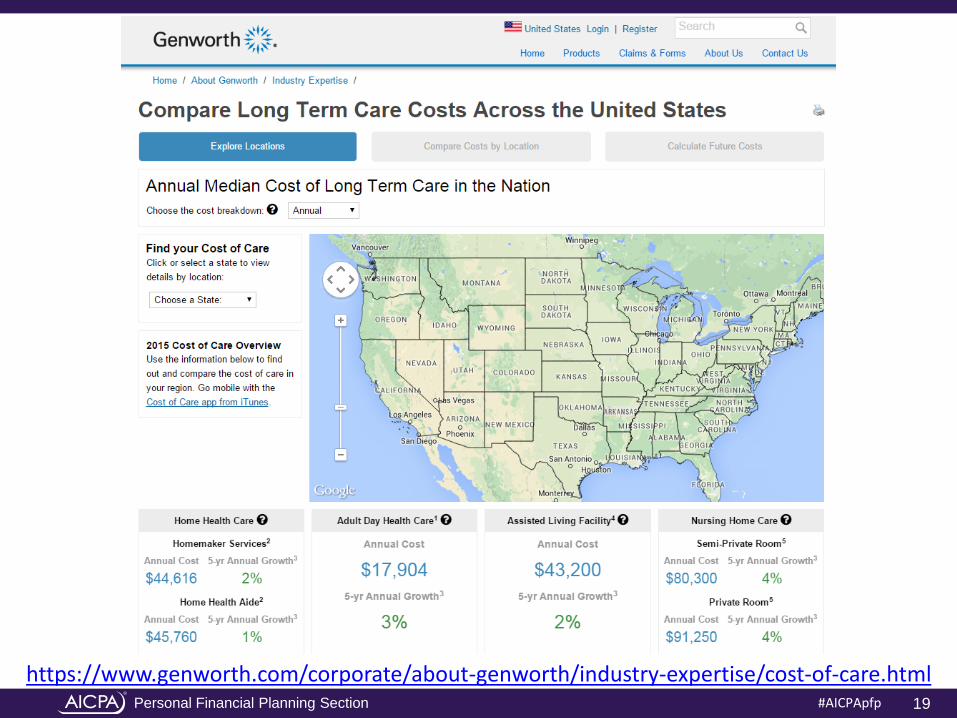

Cost of health care

Service/Facility National Median Rates

Increase over 2014

Five Year Annual Growth Rate

Homemaker services $20/Hr. 2.63% 1.61%

Home Health Aide Services $20/Hr. 1.27% 1.03%

Adult Day Health Care $69/Hr. 5.94% 2.79%

Assisted Living Facility $3,600/month 2.86% 2.48%

Nursing Home Care – SemiPrivate Room

$220/day 3.77% 3.53%

Nursing Home Care –Private Room

$250/day 4.17% 3.95%

Source: Genworth 2015 Cost of Care Survey

Personal Financial Planning Section #AICPApfp 19

https://www.genworth.com/corporate/about-genworth/industry-expertise/cost-of-care.html

Personal Financial Planning Section #AICPApfp

Discussing the Human

Issues

20

Personal Financial Planning Section #AICPApfp 21

The impact on family caregivers

Caregiver Impact Percent of caregivers

Spent more than 30 hours per week on caregiving 33%

Experienced care related distractions such as phone calls or emails while working

66%

Caregiving duties had a negative effect on their jobs 60%

Source: Genworth 2015 Cost of Care Survey

Personal Financial Planning Section #AICPApfp 22

Retirees in good health face higher lifetime

health care costs than those in poor health.

A typical healthy couple at age 65 can expect to

spend $260,000 with a 5-percent risk of exceeding

$570,000

A typical unhealthy couple can expect to spend

$220,000 with a 5-percent risk of exceeding

$465,000.

Those in good health live longer, eventually become

less healthy, and often need nursing home care.

Source: Center for Retirement Research at Boston College

Personal Financial Planning Section #AICPApfp 23

Source: Harris – AICPA survey 2012

Personal Financial Planning Section #AICPApfp 24

Blended families

Personal Financial Planning Section #AICPApfp 25

Long Term Care Demographics

Description Statistics

Americans over 65 needed LT Care in 2012 9 Million

Americans over 65 expected to need LT Care by 2020 12 Million

% of Americans in need of LT Care who receive care from family and friends

78%

Average age for admittance to nursing home 79

Percent who reach age 65 who will enter a nursing home 40%

Average length of stay - 1999 2.44 years

Percent whose stay will exceed five years 10%

Source: 40 Must Know Statistics About LT Care – Morningstar 8-9-12 article

Personal Financial Planning Section #AICPApfp

Tax, Insurance and

Benefits Planning

27

Personal Financial Planning Section #AICPApfp 28

Medicare means testing – monthly premiums

Lower MAGI limits apply in 2018 (see red $)

Single MAGI Married MAGI Part B Premium Part D Premium

$85,000 or less $170,000 or less $104.90 Your Plan’s premium

$85k to $107K $170K to $214K $146.90 Add $12.30

$107k to $160K $107K to $133.5K

$214K to $320K $214k to $267K

$209.80 Add $31.80

$160K to $214K $133.5K to $160K

$320K to $428K $267K to $320K

$272.70 Add $51.30

$214k $160K

$428K $320K

$335.70 Add $70.80

Personal Financial Planning Section #AICPApfp 29

Extending tax projections for key retirement

dates and year end planning

AICPA Tax Evaluator – Bob Keebler 10 Year

projection periods to manage tax brackets

Key retirement date planning

• 62 early SS

• 65 Medicare eligible

• 66 Full retirement age

• 70 Late SS

• 70 ½ RMDs must begin

Year end medical deduction planning key for retirees

Planning for the surviving “now single client”

Personal Financial Planning Section #AICPApfp 30

Challenge employer benefit assumptions

Always ask if clients are eligible for VA Benefits

including survivor benefits

Expect and explore additional retirement resources

for civil servants and state employees

Seek help in understanding social security spousal

benefit offsets for government employees

Seek help in understanding the windfall elimination

provisions for workers who did not have SS

withheld on at least one job (does not apply to

survivor benefits)

Personal Financial Planning Section #AICPApfp 31

I’ve run out of money – now what?

Medicaid eligibility planning

Finding a Medicaid bed

Resource: www.medicaid.gov

Personal Financial Planning Section #AICPApfp 32

Medicare basics

Part A (paid during working years)

Part B (Means tested premiums)

Part C – Medicare Advantage Plans in lieu of Parts A

and B and sometimes D

Part D – Drug Coverage

Medigap – Supplemental coverage

Personal Financial Planning Section #AICPApfp 33

Before you move

State income, estate and inheritance laws can have

a huge impact on decisions where to live at

retirement

www.leimberg.com – Numbercruncher software

provides state by state estate and inheritance

calculations

Personal Financial Planning Section #AICPApfp

Managing Documents

34

Personal Financial Planning Section #AICPApfp 35

Challenges from diminished capacity at

retirement

Ownership/beneficiary designations

Not current, difficulty in updating

• Bank Accounts

• Retirement Accounts

• Real property titling

• Problems after refinancing

Personal Financial Planning Section #AICPApfp 36

Challenges from diminished capacity at

retirement

Trusts not updated for mandatory funding formula

when combined estate under threshold

• Trust protection still appropriate?

• Increased use of disclaimers – burden on administration

Outdated provisions for children issues

• Spouses now ex-Spouses

• Substance abuse

Selection of right current Trustee/Fiduciary

• Sibling issues – leading to litigation

Personal Financial Planning Section #AICPApfp 37

Challenges from diminished capacity at

retirement

Challenge of getting qualified plan assets in trust

• Is goal of deferral still effective

• Have RMD begun, what is real period of deferral?

Guardianship appointment for yourself

• Mechanics

• Family challenges

Power of Attorney

• Not updated: aged brother-in-law, child resentment

• Financial institution non-acceptance

• Changed jurisdiction

Personal Financial Planning Section #AICPApfp 38

Physician’s Orders for

Life-Sustaining

Treatment (POLST) http://www.polst.org/educational

-resources/resource-library/

Caregiver agreements

Advisor consent to

contact pre-determined

person to notify if

advisor notices

cognitive decline

Other documents to consider

Personal Financial Planning Section #AICPApfp

Retirement Projections

39

Personal Financial Planning Section #AICPApfp 40

Chronic diseases - one wild card for retirees

The leading cause of death and disability

½ of all adults have one or more chronic diseases while 1

in four have two or more

7 of the top 10 causes of death were from chronic

diseases. Heart disease and cancer accounted for 48%

of these deaths

Arthritis is the most common cause of disability

More than 1/3 of adults and 20% of youths ages 2 to 19

are considered obese

Diabetes is the leading cause of kidney failure, lower

limb amputations and new cases of blindness

Source: Center for Disease Control 2012

Personal Financial Planning Section #AICPApfp 41

Including health care costs in retirement

projections – option 1

Use a present value amount for future health care

costs excluding long term care, dental and over the

counter medications. (Fidelity $220,000 study for 65

year old couple)

• Set this amount aside from retirement resources before running

retirement projections

• Consider creating dedicated accounts for these funds

• HSA accounts

• Additional savings dedicated to health care costs

• Long term care insurance should be used to cover the large

uncertainty not considered in this approach

Personal Financial Planning Section #AICPApfp 42

Including health care costs in retirement

projections – option 2

Considers annual cost projections for different

clients based on health.• Life expectancy tables assume ½ of population will die prior to the

estimated life expectancy

• Health clients should live longer than these tables while unhealthy

clients would be expected to have shorter life expectancies

Uses estimated annual costs based on age and

general health of client. (EBRI 9/14 Study)• Use 25 percentile of expected costs for extremely healthy clients

• Use median costs for clients without chronic diseases

• Use 75 percentile of expected costs for clients with more than one

chronic disease

• Use 90 to 95th percentile for candidates for long-term care needs.

Personal Financial Planning Section #AICPApfp 43

Addressing longevity in retirement

Prepare stress tests to living to older ages in all

retirement projections.

Make sure adequate inflation protection is included

in investments

Own long term care policies for unexpected costs

Consider using up to $125,000 of IRA to buy

Qualified Deferred Income Annuities

Consider adding low cost cash flow products such

as the Single Premium Immediate Annuity

• Reduces initial withdrawal rate on remaining portfolio

• Provides mortality insurance for those who live long lives

Personal Financial Planning Section #AICPApfp 44

Deciding on a withdrawal regime

4% rule – static withdrawal adjusted for inflation

only

RMD rules – withdrawals adjusted for age and

account balances

Safety first rules – focus on covering basic living

needs with social security and other guaranteed

payments

Dynamic rules – withdrawals adjusted for changes

in account values

• Guyton Decision Rules and Portfolio Guardrails

• Vanguards floor and ceiling rules

Personal Financial Planning Section #AICPApfp 45

Addressing other personal risks

Sensitivity to inflation:

Client’s age and life expectancy

Sources of inflation adjusted income (e.g. pension,

rental income, social security)

Fixed expenses vs. inflation sensitive expenses

Sensitivity to survivor longevity:

Expected survivor longevity (e.g. age & health gap)

Pension benefit to survivor

Single vs. MFJ tax brackets

Personal Financial Planning Section #AICPApfp 46

Best practices by creating policy statements

Retirement Savings Policy Statement

• Create a five year plan to use raises to increase savings rate to

at least 15%

Investment Policy Statement

• Establishes investment guidelines based on client specific facts

Withdrawal Policy Statement

• Establishes withdrawal rules and how a client will react when

portfolio losses arise

Personal Financial Planning Section #AICPApfp

Elder Care Resources

47

Personal Financial Planning Section #AICPApfp 48

http://www.medicare.gov/campaigns/caregiver/caregiver.html

Personal Financial Planning Section #AICPApfp 49

http://www.aarp.org/home-family/caregiving/planning-and-resources/

Personal Financial Planning Section #AICPApfp 50

http://www.eldercare.gov/Eldercare.NET/Public/Index.aspx

Personal Financial Planning Section #AICPApfp 51

https://www.livingto100.com/

Personal Financial Planning Section #AICPApfp 52

http://www.aging-parents-and-elder-care.com/Pages/Elder_Care.html

Personal Financial Planning Section #AICPApfp 53

http://www.healthgrades.com/

Personal Financial Planning Section #AICPApfp 54

http://www.medicare.gov/nursinghomecompare/

Personal Financial Planning Section #AICPApfp 55

Digital inventory resources

• http://webcache.googleusercontent.com/search?q=cache:U0lztJ

QTqxAJ:apps.americanbar.org/dch/thedl.cfm%3Ffilename%3D/

RP190000/otherlinks_files/DigitalEstateInformationForm.pdf+&c

d=3&hl=en&ct=clnk&gl=us

• http://www.theconnectivist.com/2013/12/last-digital-will-and-

testament/

• http://www.digitalpassing.com/digital-audit/

Personal Financial Planning Section #AICPApfp

Elders on the Move

Resources

56

Personal Financial Planning Section #AICPApfp 57

https://livabilityindex.aarp.org

Personal Financial Planning Section #AICPApfp 58

http://www.carf.org/Resources/RetirementLiving/

Personal Financial Planning Section #AICPApfp 59

http://blog.aicpa.org/2015/05/how-to-help-clients-understand-retirement-housing-options.html

Personal Financial Planning Section #AICPApfp

Questions?

60

Personal Financial Planning Section #AICPApfp 61

AICPA PFP Section Member Resources

Estate Tax Retirement

InvestmentInsurance & Risk

Management Practice Management

Legislative/Regulatory

Professional Responsibilities

Consumer Content

PFP Section members, inclusive of CPA/PFS credential holders, have access to resources on the latest planning strategies and trends in personal financial planning services so that they can practice competently and profitably. Visit aicpa.org/pfp/resources.

Personal Financial Planning Section #AICPApfp 62

The CPA’s Guide to Practical Retirement

Planning

Discusses the “science” of retirement planning

• As an advisor, what do I need to “know” to be competent?

• Provides practical application of various research studies

• Discusses impact of assumptions, risks, software simulation

approaches, and product selection

• Identifies components of the planning process including

advisors value, data gathering, and key decisions by age

Recognizes the “art” of retirement planning

• As an advisor, how do I “communicate” in an effective manner?

• Discusses needs of special groups: women, LGBT, divorcees

• Organized according to client decision-making periods:

• Saver, pre-retiree, and retirees in early and late years

• Addressing unique issues during each time-frame

Personal Financial Planning Section #AICPApfp 63

Upcoming PFP Section Events

Webcasts*

• Practical Planning, Thought Leadership and Best Practices for Retirement Planning Series (events are free

to everyone; no CPE offered)

Conferences

PFP/PFS members are eligible to attend 4 free events with CPE. For a listing of all

PFP webcasts, including free events, visit aicpa.org/pfp/upcomingevents.

For the full calendar of upcoming PFP Section events, visit aicpa.org/pfp/events and

click on CPE & Events.

PFP/PFS Members can access the archives (no CPE) for free at aicpa.org/pfp/library.

August 5, 1-2:45pm ET Practical Planning for Cash Flows and Withdrawal Strategies in Retirement

August 27, 1-2pm ET Planning for Spending in Retirement (consumer event)

November 4, 1-2:45pm ET Practical Planning for Social Security and Healthcare in Retirement

January 18-20, 2016 AICPA Advanced Personal Financial Planning Conference (cpa2biz.com/pfp)

July 20-22, 2015 AICPA Advanced Estate Planning Conference

November 16-17, 2015 AICPA Sophisticated Tax Planning for Your Wealthy Clients

Personal Financial Planning Section #AICPApfp 64

CPA/PFS News and Events

PFS Referral Program

• Receive 100% credit to apply toward future CPA/PFS dues by

referring a CPA to become a PFS or sit for the PFS exam

PFS Exam

• Register now for upcoming exam windows

• Discounts, sponsorships and volume pricing available

Education Opportunities

• In-depth courses in estate, retirement, tax, investments,

insurance, and PFP process

• In-person and online PFP Boot Camp

• Self-study PFS exam review course

Learn more at aicpa.org/pfp/pfs

Personal Financial Planning Section #AICPApfp 65

A CPA Financial Planner is a trusted advisor who…

Operates at the highest professional level when

delivering PFP services to clients, acting in the

clients’ best interest.

Adheres to high standards as required by the Code

of Professional Conduct and the Statement on

Standards in PFP Services through the application

of objectivity, integrity, due care and competence

required by CPAs.

Is regulated by state boards of accountancy.

Integrates advanced planning concepts, including

tax and business considerations, with the entire

financial plan.