power point presentation on franklin templeton

TRANSCRIPT

04/12/23 1

I am working with Franklin Templeton Mutual Fund since 23rd June 2008.Franklin Templeton have tie-up with various banks to deal in mutual fund.I am working for its banking channel sales category. I am dealing with BankOf India. They have allotted me three branches of Bank of India. I have to visit every branch by alternate day. I have to focused on Systematic Investment Plan(SIP). My main targeted clients are bank’s existing clients or client’s referred by them. I have to co-ordinate with the bank’s Relationship Manager. Apart from that I used to interact with all walking clients in the branch. In my meeting with my clients I tried to know what are the future goals they want to achieve and in what time duration.After assessing their risk appetite level I recommend them suitable investingplan. Sometimes it is quite tougher to convince them, as they only believes in traditional investment tool i.e. Fixed Deposit. Since it is almost one month past, I really enjoying my work with Franklin

Templeton.

PREFACE

04/12/23 2

TABLE OF CONTENTS

METHODOLOGY ……………. 3

COMPANY PROFILE ………………4

INTRODUCTION ……………..5 (i). FINANCIAL PLANNING ………… 5 (ii). TYPES OF INVESTMENT ……….. 5 (iii). STRATEGIES FOR REDUCING RISK ……… 5 (iv). ASSET ALLOCATION ………… 8

PORTFOLIO MANAGEMENT CASE STUDY ………… 9

INVESTMENT STRATEGY ……………. 12

04/12/23 3

Our investment philosophy that follows a disciplined

approach to investing with a strong focus towards process orientation is the common thread running through all our schemes.

The key guiding principle to our investment philosophy

is - maximize the risk- adjusted returns for our investors in the respective asset classes, and create wealth for them over the long-term.

We have successfully demonstrated the ability to achieve this in the past, and are confident that our process-oriented investment approach will help us sustain the same in the years to come.

METHODOLOGY

04/12/23 4

Franklin Templeton Investments is one of the largest

financial services groups in the world based at San Mateo, California USA. The group has US$580.2 billion in assets under management globally (as on June 30, 2008).

We have offices in 29 countries around the world.

Franklin Templeton has offices in 33 locations across

India and manages average AUM of Rs.24,742.06 crores for over 25 lakh investors as of June 30, 2008.

COMPANY PROFILE

04/12/23 5

(i). FINANCIAL PLANNING… Start with your financial goals… Before you choose investments, write down your

financial goals-retirement children's education and so forth. For each goal, be sure to consider:

Your risk tolerance Your time frame Next understand your investment options.

(ii). TYPES OF INVESTMENTS… While there are hundreds of mutual funds to choose

from, they mostly fall into 3 categories…

Equities (also called stocks) Fixed-income (also called bonds) Cash equivalents (a type of liquid investment such as a

money market fund)

INTRODUCTION

04/12/23 6

Successful investors use several strategies to reduce their investment risk including:

Diversification Asset allocation Rupee-cost averaging

THE POWER OF COMPOUNDING… The longer the period of your investment, the more

you accumulate, because of the power of compounding... which is why it makes sense to start investing early.

(iii). STRATEGIES FOR REDUCING RISK…

04/12/23 7

Meet Suresh and Manoj. Suresh invests Rs.5 OOO while

Manoj invests twice as much. As illustrated in the table below, even though the amount invested by Suresh is half of what Manoj puts , his investment final amount is becomes twice as much as Manoj's, simply because he started earlier - a clear instance of the benefits of compounding. This is the power of compounding.

Compounding Favours the Early Starter Suresh Manoj Investment Amount Rs.5,000 Rs.10,000 Investment Duration 20 years 10 years Final Amount Rs.81,833 Rs.40,456

(Assumed annual rate of return - 15% with dividends and capital gains reinvested.)

THE SECRET IS TO START EARLY…

04/12/23 8

The key therefore lies in starting earlier, and giving

your investments a longer time to grow The longer you have, the better compounding works…Growth of a monthly saving of Rs.1000 over a 30 year

period(Total savings: Rs.3.6 lacs)

(Assumed rate of return - 12%)

04/12/23 9

What is Asset Allocation? Asset allocation means diversifying your money among

different types of investment categories, such as stocks, bonds and cash. The goal is to help reduce risk and enhance returns.

What allocation is right for you? Asset allocation decisions involve tradeoffs among 3

important variables:

Your time frame Your risk tolerance Your personal circumstances Asset allocation plans change with time… While an asset allocation plan eliminates a lot of the

day-to-day decisions involved in investing, it doesn't mean you should just "set it and forget it."

(iv). ASSET ALLOCATION…

04/12/23 10

Here are examples of 3 model portfolios that can give you a sense of how to approach selecting your own asset mix.

Aggressive portfolio - This portfolio emphasizes

growth, suggesting 65% in stocks or equity funds, 25% in bonds of fixed-income funds and 10% in short-term money market funds or cash equivalents. Investment experts recommend this portfolio for people who have a long investment time frame.

PORTFOLIO MANAGEMENT CASE STUDY…

04/12/23 11

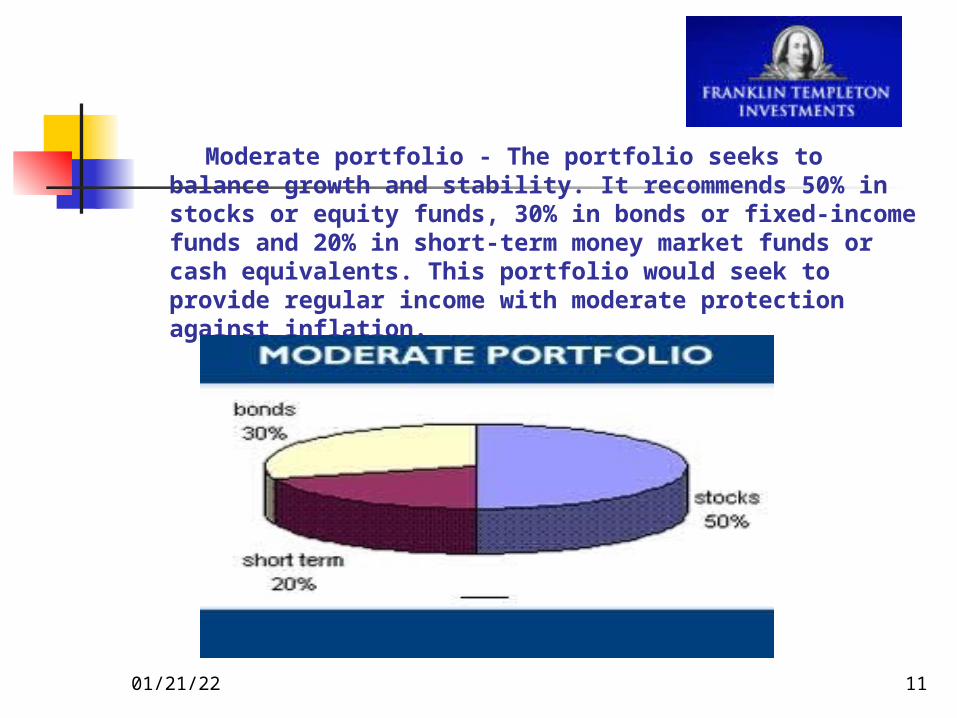

Moderate portfolio - The portfolio seeks to balance

growth and stability. It recommends 50% in stocks or equity funds, 30% in bonds or fixed-income funds and 20% in short-term money market funds or cash equivalents. This portfolio would seek to provide regular income with moderate protection against inflation.

04/12/23 12

Conservative portfolio - This portfolio suggests 25% in

stocks or equity funds, 50% in bonds or fixed-income funds, and 25% in money market funds or cash equivalents. This portfolio appeals to people who are very risk averse or who are retired.

04/12/23 13

No matter what type of savings programme you choose, it's important to review your portfolio every 6-12 months to assess your progress.

Risk and reward go hand-in-hand… When choosing investments, remember the tradeoff

between risk and return. The higher the return you seek, the more risk you'll need to accept. There's no such thing as a low risk-high return investment.

04/12/23 14

Finding the right investment has become quite a

challenge. Most of us fall prey to buying the latest top performers and accumulating a few shares of this and that without really considering our financial goals, timeframe and tolerance for risk.

What financial goals do you want to achieve? When do you hope to reach them? How much money will you need to invest to achieve

your goal? How much risk can you afford to take? Do you need to rethink your investments

periodically?

INVESTMENT STRATEGY…

04/12/23 15

The key to building wealth is to start investing early and

regularly. Regular investments, however small, can grow into a substantial amount of wealth over the long-term.

The Cost of Delaying…

Sunita, Anil and Sunil begin their careers together at the age of 25 but have different attitudes towards savings. Sunita is a conservative spender and believes in saving. Anil and Sunil believe that with good careers ahead of them it does not really matter when they start saving.

Start Early…

04/12/23 16

Sunita - Sunita gets into the habit of saving regularly from day one. She successfully saves Rs.10,000 in the first year. She continues saving Rs.10,000 per year for 35 years till her retirement. Anil - Anil gets married at the age of 27. With new

responsibilities ahead of him, he gets into the habit of saving Rs.10,000 every year and continues saving Rs.10,000 per year for 33 years till his retirement.

Sunil - Sunil is the last one to start saving. He

gets married and becomes a father at the age of 30. He, too, realises that he cannot delay his savings decision any more. He gets into the habit of saving Rs.10,000 every year and continues with this for 30 years till his retirement.

04/12/23 17

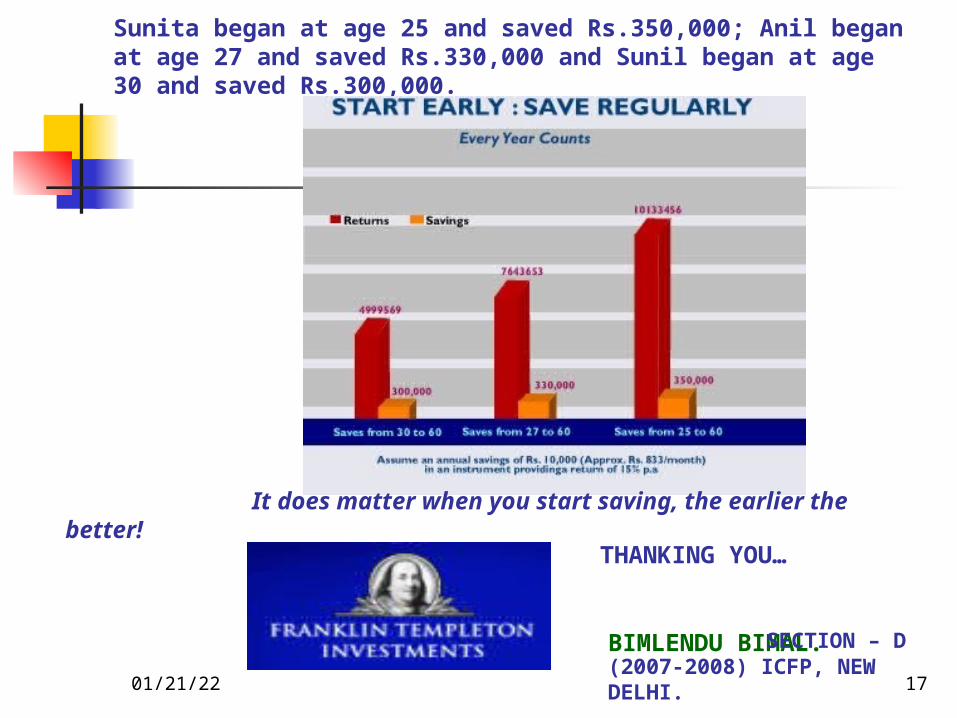

Sunita began at age 25 and saved Rs.350,000; Anil began at age 27 and saved Rs.330,000 and Sunil began at age 30 and saved Rs.300,000.

It does matter when you start saving, the earlier the better! THANKING

YOU… BIMLENDU BIMAL. SECTION – D (2007-2008) ICFP, NEW DELHI.