positive accounting theory. class announcements assignment #6 due february 20th; available on-line ...

TRANSCRIPT

POSITIVE ACCOUNTING THEORY

Class Announcements

Assignment #6 due February 20th; available on-line Research Paper Part #2 due February 13th (today) Assignment #5 available for pick up on Friday (14th)

from SCHW 396 until 2:00pm Midterm is February 17th (in-class) Business Banquet - April 2nd – 5:45-8pm, Catering -

Gabrieau's Bistro; Keynote Speaker - Annette Verschuren, Past President of Home Depot for Canada and Asia

Additional Office Hours: Friday (14th) 10:00am to 2:00pm

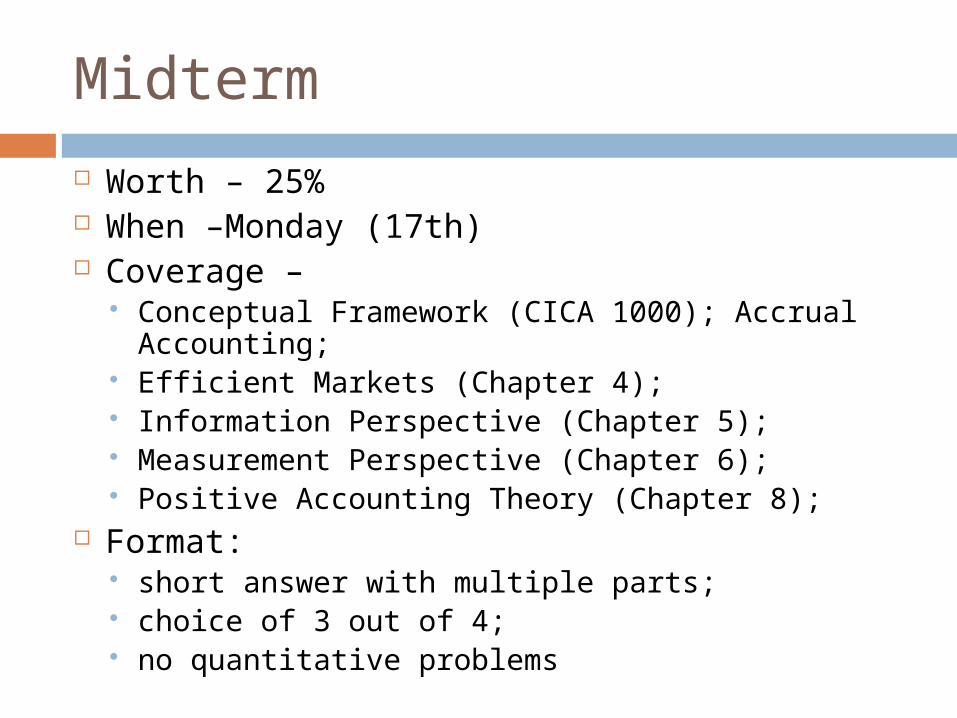

Midterm

Worth – 25% When –Monday (17th) Coverage –

Conceptual Framework (CICA 1000); Accrual Accounting;

Efficient Markets (Chapter 4); Information Perspective (Chapter 5); Measurement Perspective (Chapter 6); Positive Accounting Theory (Chapter 8);

Format: short answer with multiple parts; choice of 3 out of 4; no quantitative problems

Class Objectives

1. Viewing the firm as a series of contracts2. Contracts between agents and

principles define the relationship and expectations

3. Defining a rationale person4. Hypotheses of Positive Accounting

Theory (PAT)

Positive Accounting Theory (PAT)

The term positive refers to a theory that attempts to make good predictions of real world events

“Positive accounting theory is concerned with predicting such actions as the choice of accounting policies by firm managers and how managers will respond to proposed new accounting standards.” p. 304

Accounting policy choice is part of the overall process of corporate governance.

Positive Accounting Theory

Positive: the objective is to understand and predict managerial accounting policy choice across different firms.

Normative: the objective is to tell managers what they should or ought to do.

Positive Accounting Theory

“Firms organize themselves in the most efficient manner so as to maximize their prospects for survival” p. 304 depends on factors such as legal & institutional

environment, technology, degree of competition, etc. firm can be viewed as nexus of contracts

Firm is a nexus of contracts A firm will want to minimize the various contracting

costs associated with these contracts Many of these contracts involve accounting

information PAT argues that the firm’s accounting policies are selected to

reduce contracting costs – efficient contracting Managers require flexibility in accounting policies to allow

adoption to new or unforeseen circumstances

Positive Accounting Theory

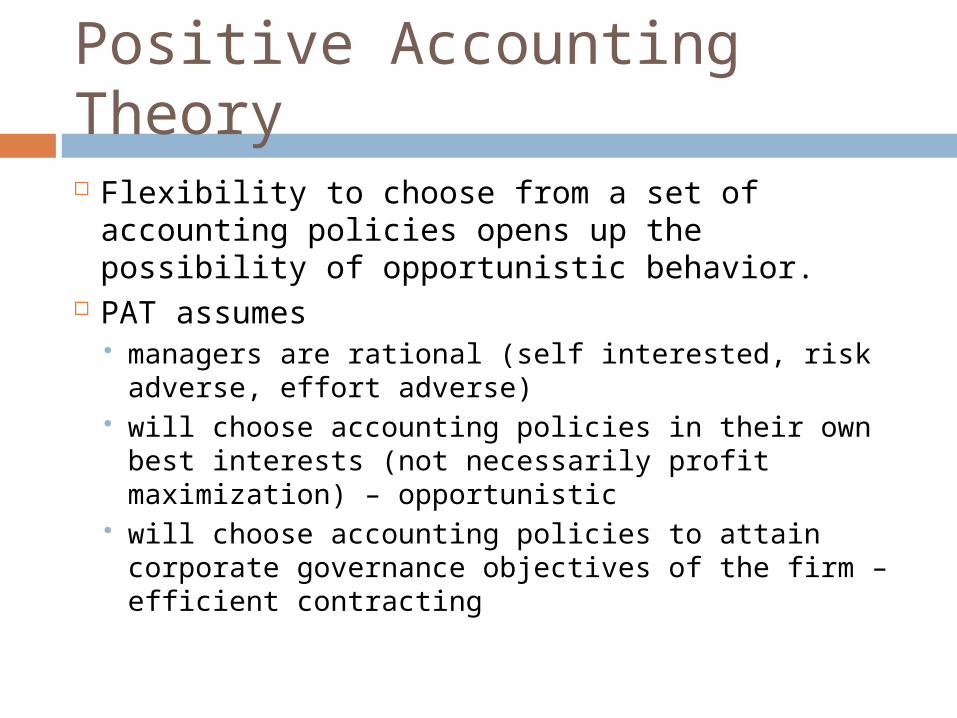

Flexibility to choose from a set of accounting policies opens up the possibility of opportunistic behavior.

PAT assumes managers are rational (self interested, risk adverse,

effort adverse) will choose accounting policies in their own best

interests (not necessarily profit maximization) – opportunistic

will choose accounting policies to attain corporate governance objectives of the firm – efficient contracting

Positive Accounting Theory: Distinguishing Versions (opportunistic vs. efficient) Difficulty in distinguishing between versions

(p. 316-318): Mian & Smith (1990)

Consolidated financial statements Christie & Zimmerman (1994)

Takeover targets Dichev & Skinner (2002)

Debt covenants Dechow (1994)

Net income more highly associated with share returns than cash flows

Guay (1999) Limit firm risk using derivatives

Evidence from empirical research of both

Positive Accounting Theory: Accounting Implications-Managing Earnings Ways to manage earnings:

Changing accounting policies Managing discretionary accruals Timing of adoption of new accounting

standards Changing real variables-R&D, advertising,

repairs & maintenance SPEs (Enron), capitalize operating expenses

(WorldCom)

Positive Accounting Theory: Accounting Policies The optimal set of accounting polices for the

firm represents a compromise: A) Tightly prescribing accounting policies

beforehand will minimize opportunistic accounting policy choices by mangers but incur cost of lack of accounting flexibility to meeting changing circumstances

B) Allowing managers to choose from a broad array of accounting polices will reduce costs of accounting inflexibility but expose the firm to the cost of opportunistic manager behavior.

Positive Accounting Theory: Hypotheses The predictions made by PAT are largely

organized around three hypothesis: (in opportunistic form)

1) Bonus plan hypothesis – select accounting policies to move earnings to current period for remuneration

2) Debt covenant hypothesis - select accounting policies to move earnings to current period to reduce possibility of technical default

3) Political cost hypothesis - select accounting policies to move earnings to future period

Positive Accounting Theory: Empirical Investigation 1) Bonus plan hypothesis – Healy

(1985), managers do choose accounting policy to maximize earnings

2) Debt covenant hypothesis – Dichev & Skinner (2002), managers choose accounting polices to maintain covenant ratios; managers work harder to avoid first covenant violation

3) Political cost hypothesis – Jones (1991), firms choose accounting policy consistent with improving their case of import protection

Overall – the three PAT hypothesis may predict manager reaction.

Class Objectives - Revisited

1. Viewing the firm as a series of contracts2. Contracts between agents and

principles define the relationship and expectations

3. Defining a rationale person4. Hypotheses of Positive Accounting

Theory (PAT)