pop and fizzle

DESCRIPTION

Pop and Fizzle. Benjamin Tal, Senior Economist. A Lost Decade. US Housing – Far From Normal. Negative Equity in US Housing Market. Credit Availability Still Looks Tight. Number of Failed Financial Institutions (US). US Labour Market: Still Long Way to Full Employment. - PowerPoint PPT PresentationTRANSCRIPT

January 2010

Pop and Fizzle

Benjamin Tal, Senior Economist

| 2

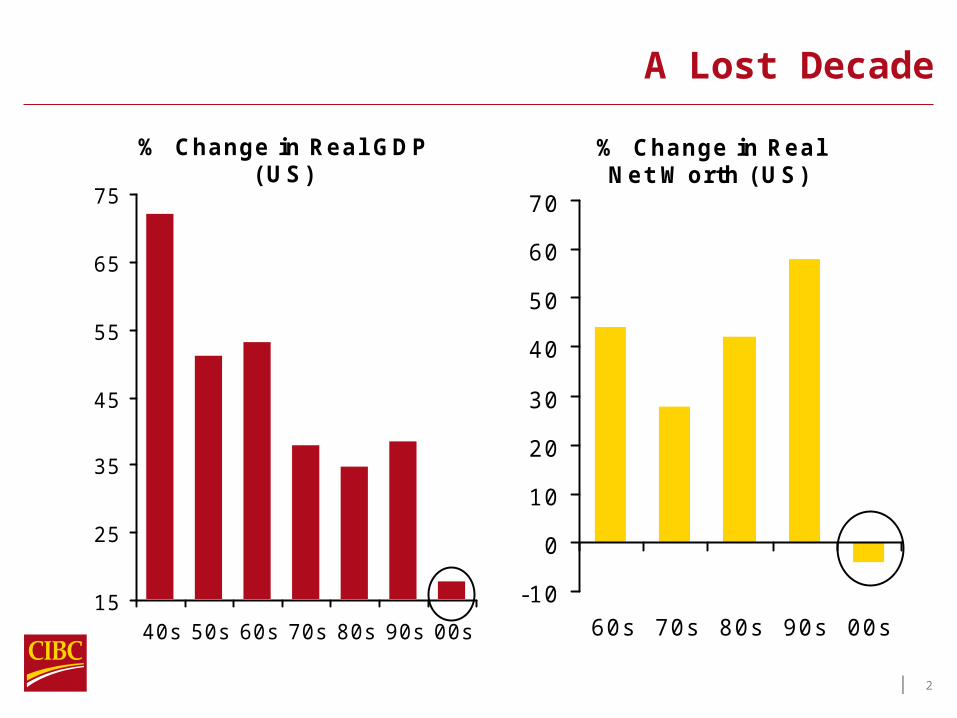

A Lost Decade

% Change in Real GDP(US)

15

25

35

45

55

65

75

40s 50s 60s 70s 80s 90s 00s

% Change in RealNet Worth (US)

-10

0

10

20

30

40

50

60

70

60s 70s 80s 90s 00s

| 3

US Housing – Far From Normal

15

35

55

75

95

115

135

155

175

99 01 03 05 07 09

Existing Home SalesNew Home Sales

I ndex1999=100

First timehome buyer

tax credit

0

2

4

6

8

10

12

14

16

18

20

99 01 03 05 07 09

Ratio - Existing home sales to new home sales

A recordhigh

| 4

Negative Equity in US Housing Market

0

2

4

6

8

10

12

14

16

18

2006 2007 2008 2009

Mn households 10 million with negative equity of more than 20%

| 5

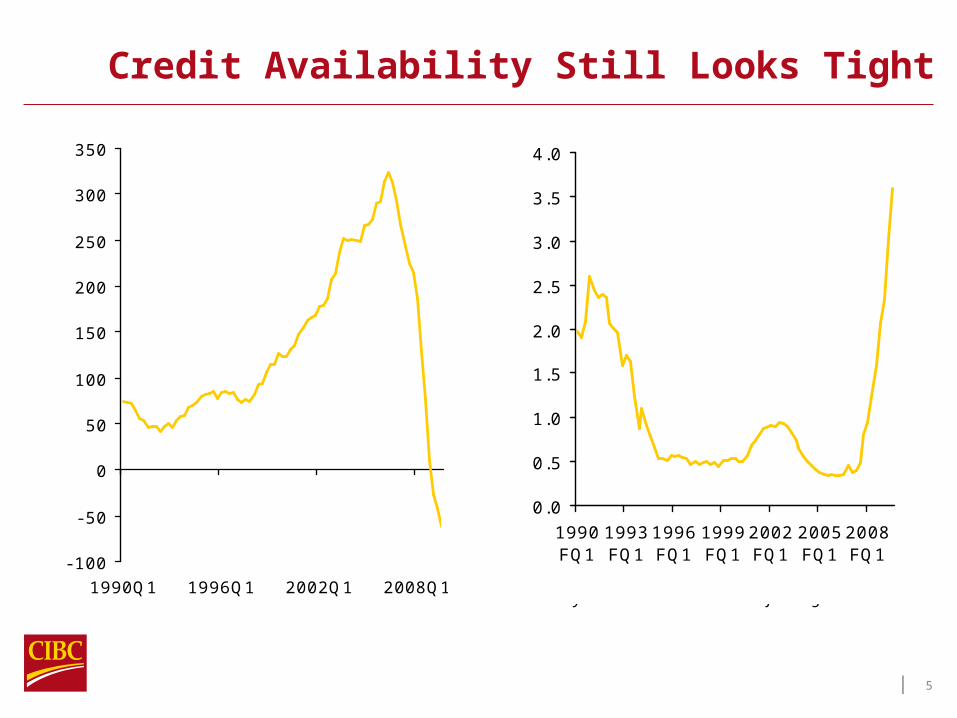

Credit Availability Still Looks Tight

- 100

- 50

0

50

100

150

200

250

300

350

1990Q1 1996Q1 2002Q1 2008Q1

Household borrowing, bn$ (4qrtr avg)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1990FQ1

1993FQ1

1996FQ1

1999FQ1

2002FQ1

2005FQ1

2008FQ1

Ratio, nonperforming loans to total loans

Money centre banks and major regionals

| 6

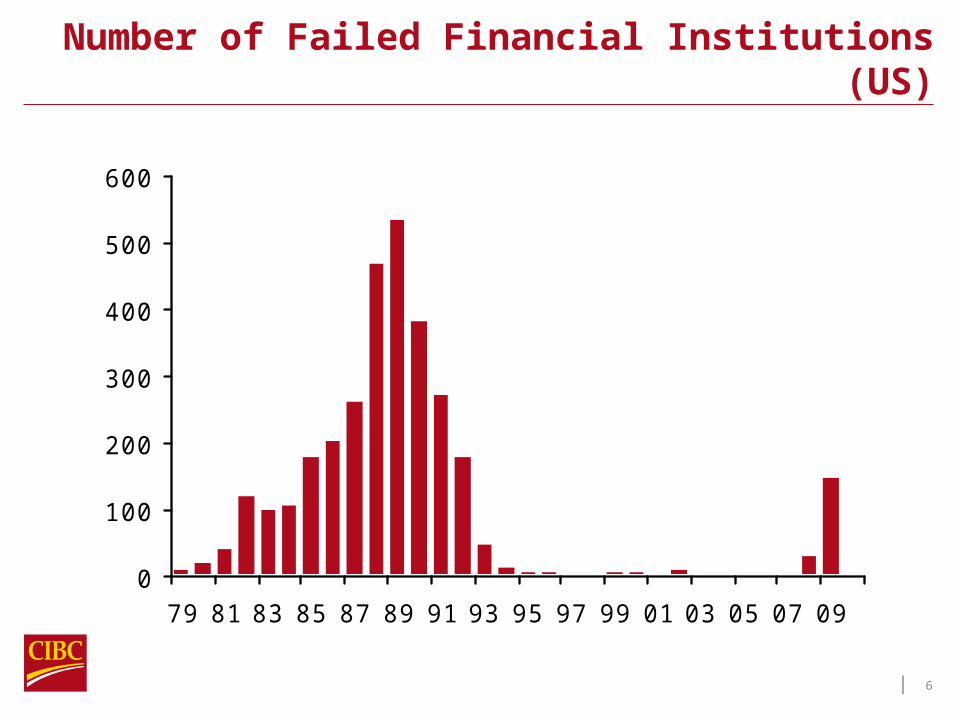

Number of Failed Financial Institutions (US)

0

100

200

300

400

500

600

79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09

Total (Units)

| 7

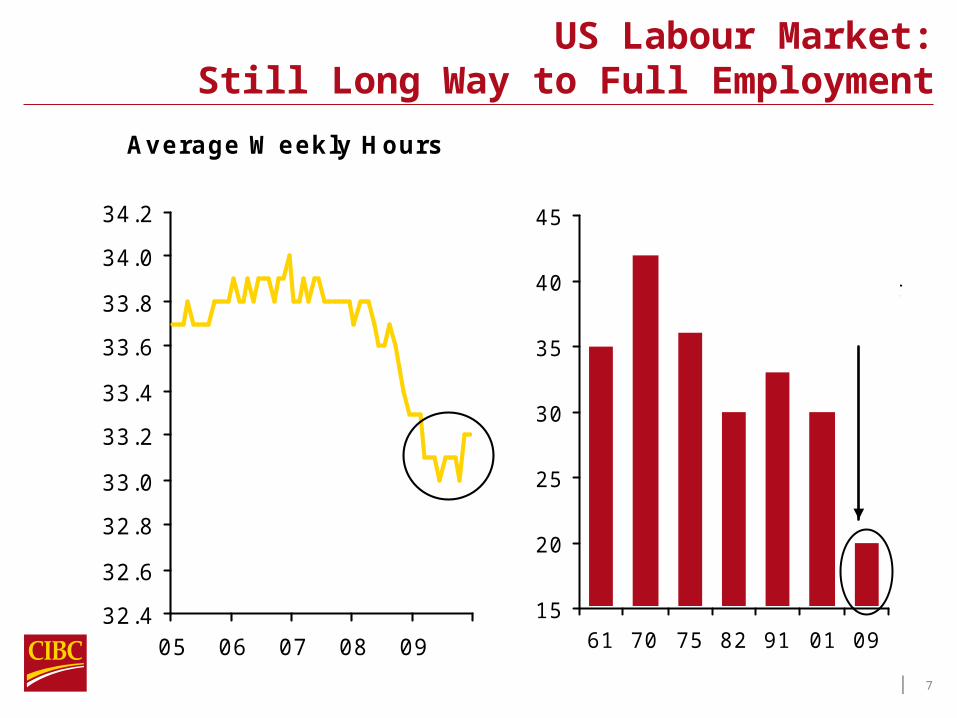

US Labour Market: Still Long Way to Full Employment

15

20

25

30

35

40

45

61 70 75 82 91 01 09

% (eve of recovery)

Probability of ExitingUnemployment in Given Month

Post-warlow

Average Weekly Hours

32.4

32.6

32.8

33.0

33.2

33.4

33.6

33.8

34.0

34.2

05 06 07 08 09

| 8

Mega Bust in US Business Spending

Business I nvestment

-25

-20

-15

-10

-5

0

5

10

15

20

25

71 77 83 89 95 01 07

y/y % chg

2009

Business I nvestment Cumulative Drop

-25

-20

-15

-10

-5

0

Q4-00 toQ2-03

Q2-08 toQ2-09

ITMeltdown

:Peak

toTrough

So farcurrent

recession

%

Source: BEA, CIBC

| 9

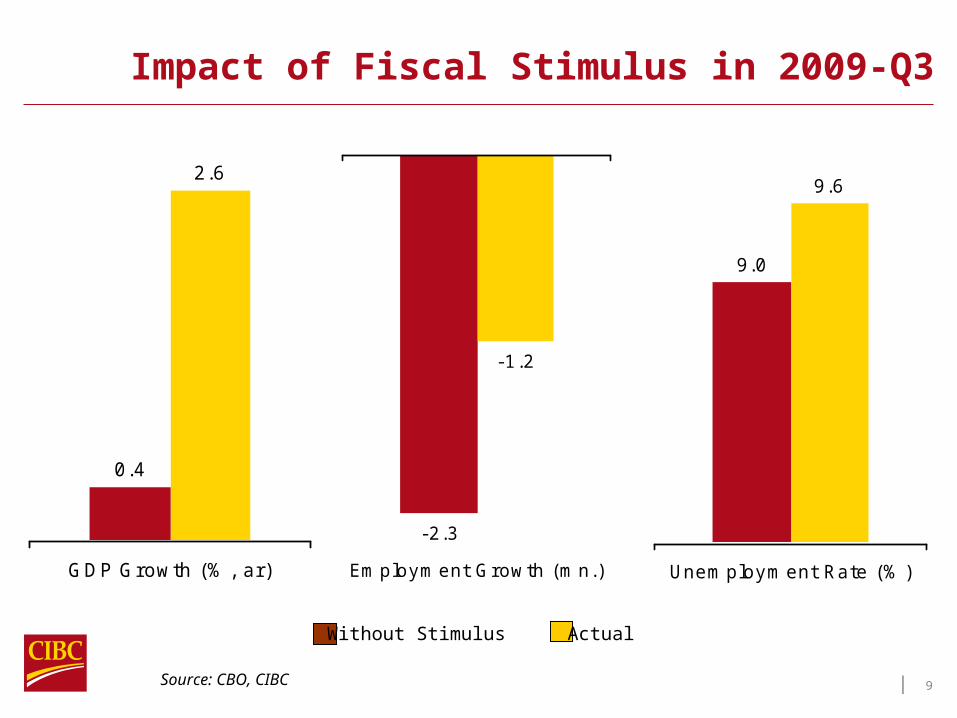

Impact of Fiscal Stimulus in 2009-Q3

Without Stimulus Actual

Source: CBO, CIBC

0.4

2.6

GDP Growth (% , ar)

-2.3

-1.2

Employment Growth (mn.)

9.0

9.6

Unemployment Rate (% )

| 10

Contribution of US Stimulus Package to US GDP Growth (%-pts)

Fiscal Stimulus

-2

-1

0

1

2

3

4

09

Q:2

09

Q:3

09

Q:4

10

Q:1

10

Q:2

10

Q:3

10

Q:4

11

Q:1

11

Q:2

11

Q:3

11

Q:4

Forecast

0

| 11

FED Financing US Budget Deficit

US Budget Deficit

-1600

-1400

-1200

-1000

-800

-600

-400

-200

0Ja

n-0

9Feb

-09

Mar-

09

Ap

r-0

9M

ay-0

9Ju

n-0

9Ju

l-0

9A

ug

-09

Sep

-09

Oct

-09

Nov-0

9D

ec-

09

$Bn

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Jan

-09

Feb

-09

Ma

r-0

9A

pr-

09

Ma

y-0

9Ju

n-0

9Ju

l-0

9A

ug

-09

Se

p-0

9O

ct-0

9N

ov

-09

De

c-0

9

Fed's holdings of US Gov't & Agcy Securities($Bn)

| 12

Massive Fiscal Stimulus Worldwide in 2009/10

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

C AN US C HN J PN AUS UK GER FRA

2009 2010

Discretionary Fiscal S timulus, % of GDP

Source: IMF

| 13

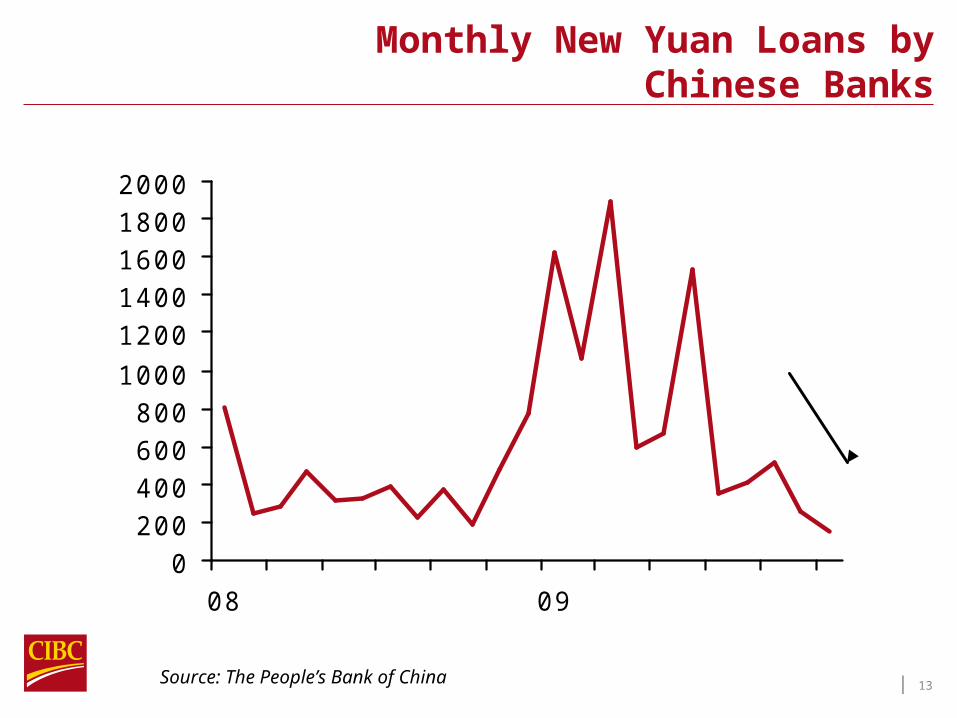

Monthly New Yuan Loans by Chinese Banks

Source: The People’s Bank of China

0200400600800

1000

12001400160018002000

08 09

bn yuan

| 14

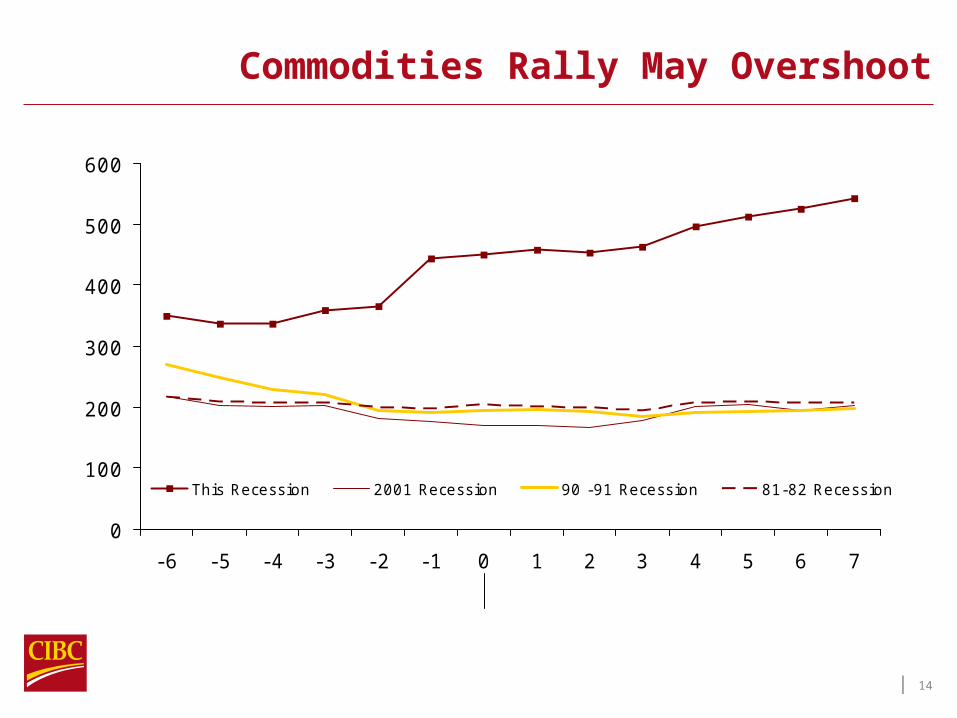

Commodities Rally May Overshoot

0

100

200

300

400

500

600

-6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7

This Recession 2001 Recession 90 -91 Recession 81-82 Recession

Months before trough in US GDP Months after trough in US GDP

S&P GSCI I ndex ( J an-70=100)

| 15

C$ Overvalued Relative to Commodities

50

60

70

80

90

100

110

08Q3 08Q4 09Q1 09Q2 09Q3 09Q4

1.00

1.05

1.10

1.15

1.20

1.25

Index (08Q3=100) reverse axis

Source: Statistics Canada, CIBC

C$/US$ (R)

BoC Commodity price index (L)

| 16

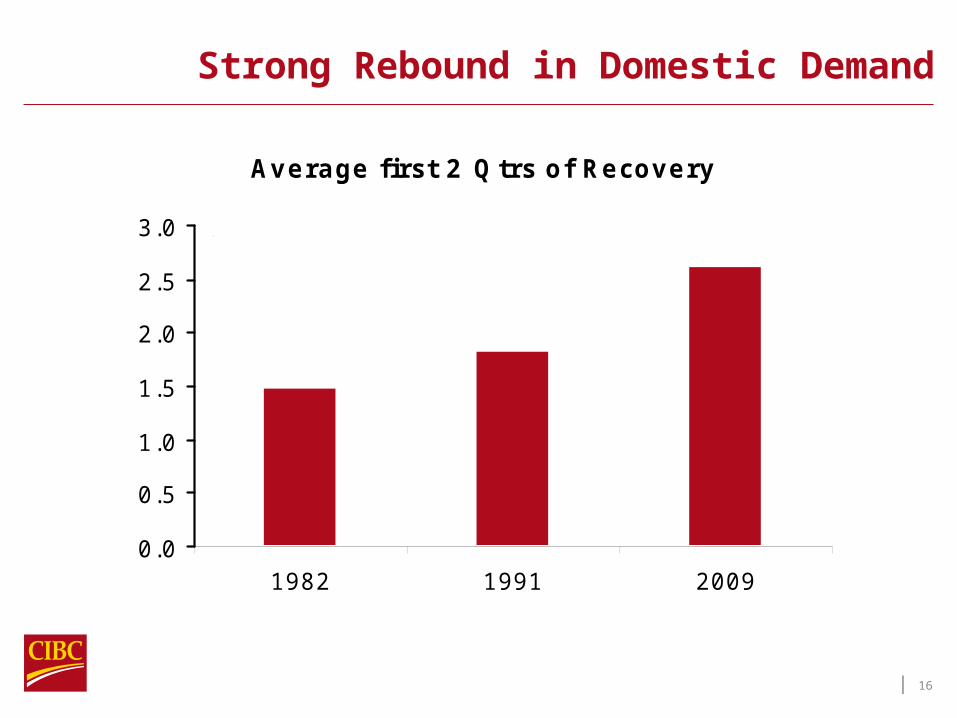

Strong Rebound in Domestic Demand

Average first 2 Qtrs of Recovery

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1982 1991 2009

% (ar)

| 17

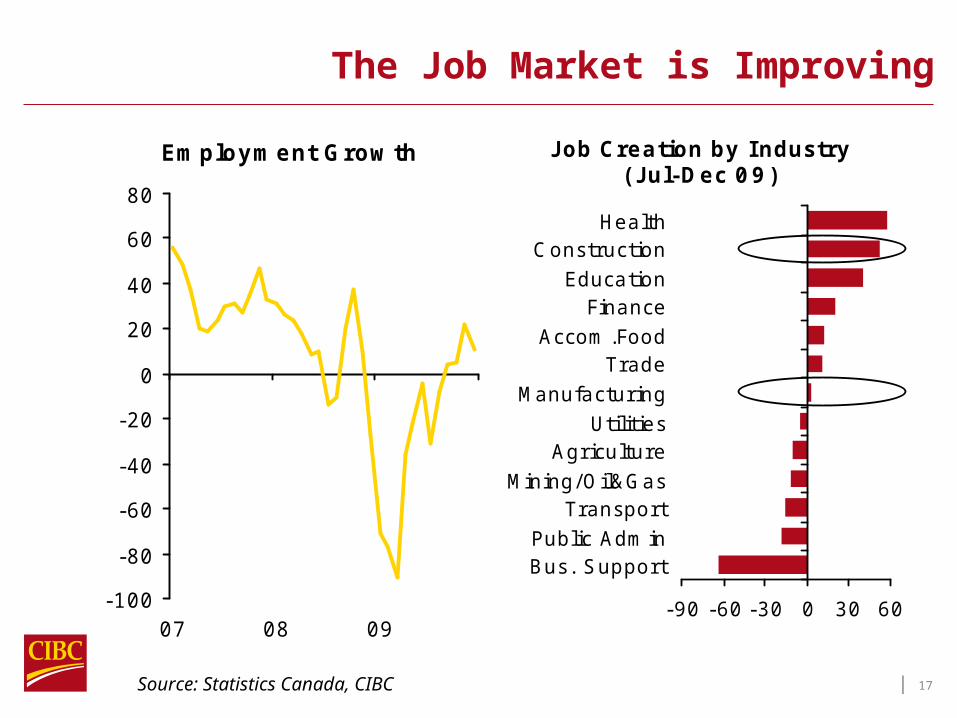

The Job Market is Improving

Employment Growth

-100

-80

-60

-40

-20

0

20

40

60

80

07 08 09

'000, m/m3-mo moving avg

J ob Creation by Industry ( J ul-Dec 09)

-90 -60 -30 0 30 60

HealthC onstruction

EducationFinance

Accom.FoodTrade

Manufacturing

UtilitiesAgriculture

Mining/Oil&GasTransport

Public AdminBus. Support

'000

Source: Statistics Canada, CIBC

| 18

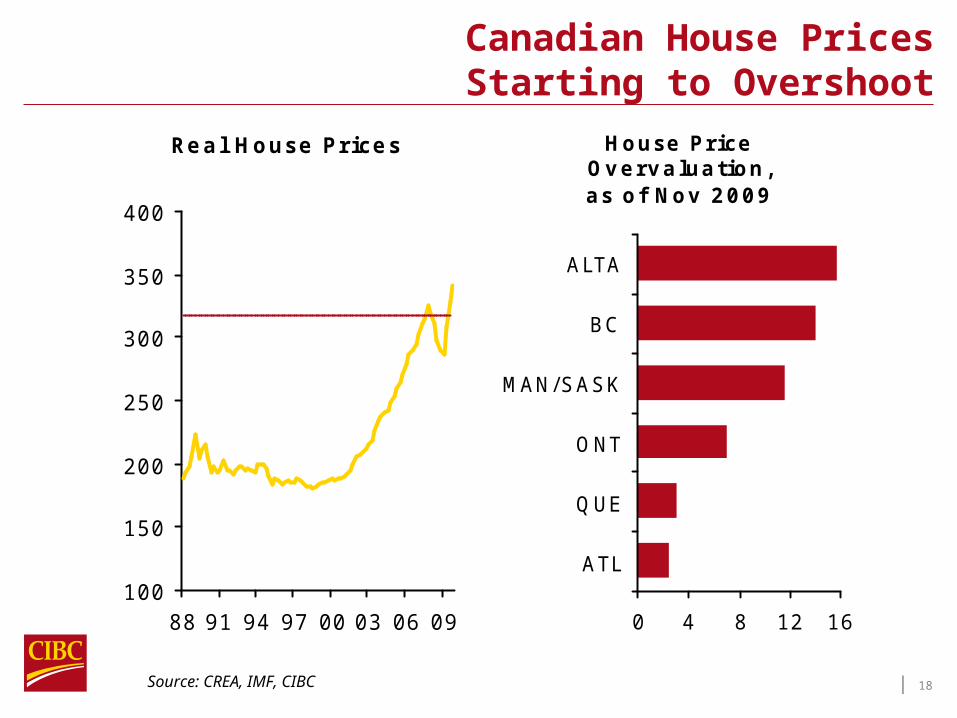

Canadian House Prices Starting to Overshoot

Source: CREA, IMF, CIBC

Real House Prices

100

150

200

250

300

350

400

88 91 94 97 00 03 06 09

$000s (2009 prices)

Fair value

House Price Overvaluation, as of Nov 2009

0 4 8 12 16

ALTA

BC

MAN/SASK

ONT

QUE

ATL %

| 19

Housing: An Important Economic Driver

Source: CREA, Statistics Canada, Bank of Canada, CIBC

House Prices lead Construction J obs

1000

1050

1100

1150

1200

1250

1300

06 07 08 09220

240

260

280

300

320

340

360

C onstruction employment (L)Avg house price (R)

$'000, 3-mo moving avg$mn

Wealth Effect on Consumption

-2

-1

0

1

2

3

4

5

06 07 08 09 10200

220

240

260

280

300

320

340

360

Housing wealth effect (L)Avg Home Price (R)

$000s

Fcst

$bn

| 20

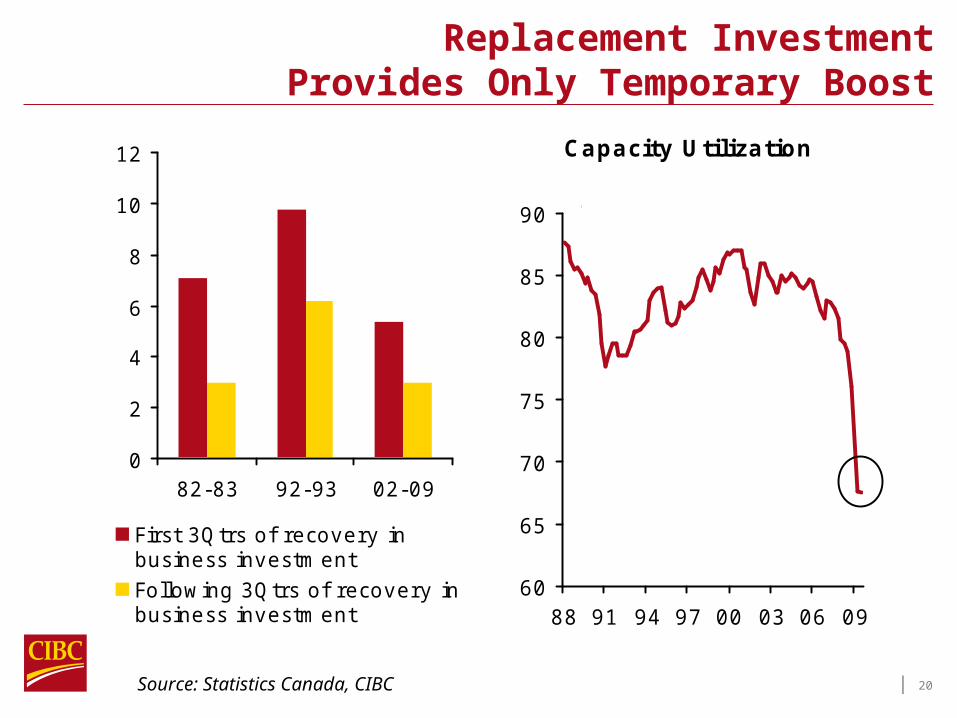

Replacement Investment Provides Only Temporary Boost

Source: Statistics Canada, CIBC

Capacity Utilization

60

65

70

75

80

85

90

88 91 94 97 00 03 06 09

%

recordlow

0

2

4

6

8

10

12

82-83 92-93 02-09

First 3Qtrs of recovery inbusiness investmentFollowing 3Qtrs of recovery inbusiness investment

| 21

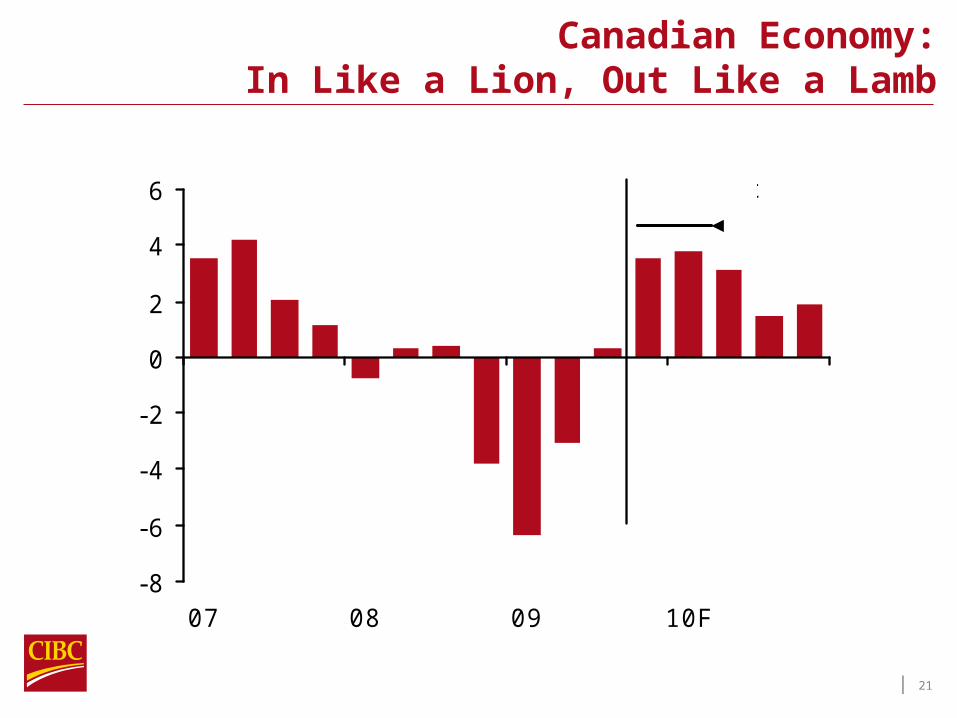

Canadian Economy:In Like a Lion, Out Like a Lamb

-8

-6

-4

-2

0

2

4

6

07 08 09 10F

q/q % chg in Real GDP, s.a.a.r. Forecast

| 22

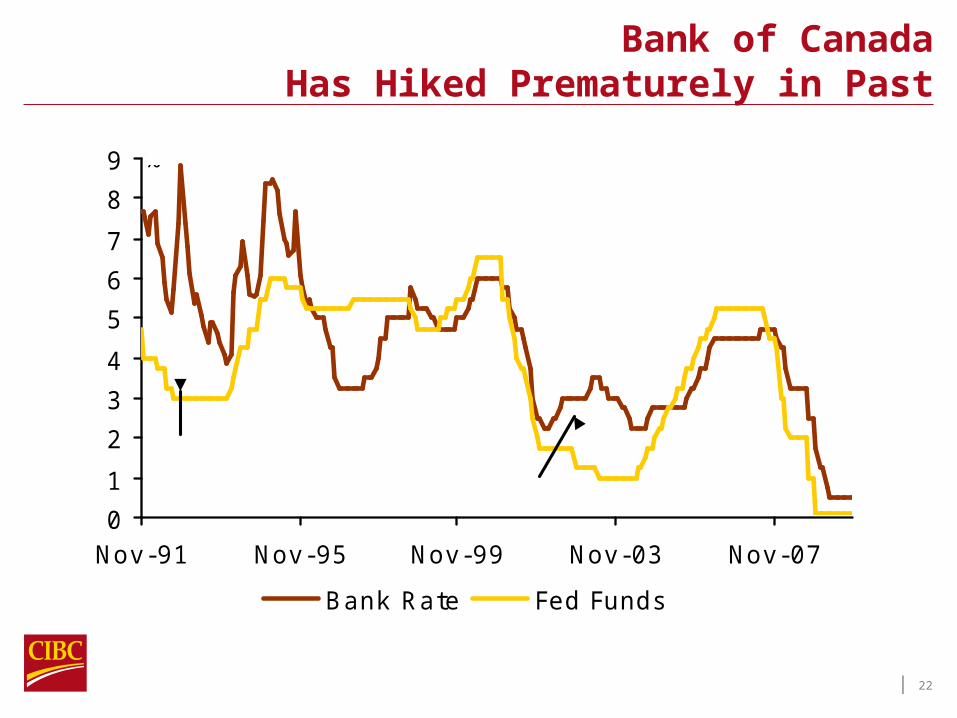

Bank of Canada Has Hiked Prematurely in Past

0

1

2

3

4

5

6

7

8

9

Nov-91 Nov-95 Nov-99 Nov-03 Nov-07

Bank Rate Fed Funds

premature tightening

premature tightening

%

| 23

Credit Continued To Expand During the Recession

Source: Statistics Canada, CIBC

Real Household Credit

-15-12

-9-6-30369

1215

75 79 83 87 91 95 99 03 07

y/y % chg

09

indicatesrecession

| 24

Average Annual Change in Consumer Bankruptcies

Source: Statistics Canada, CIBC

Since 1980

0

2

4

6

8

10

12

14

During periods of fallinginterest rates

During periods of risinginterest rates

%

| 25

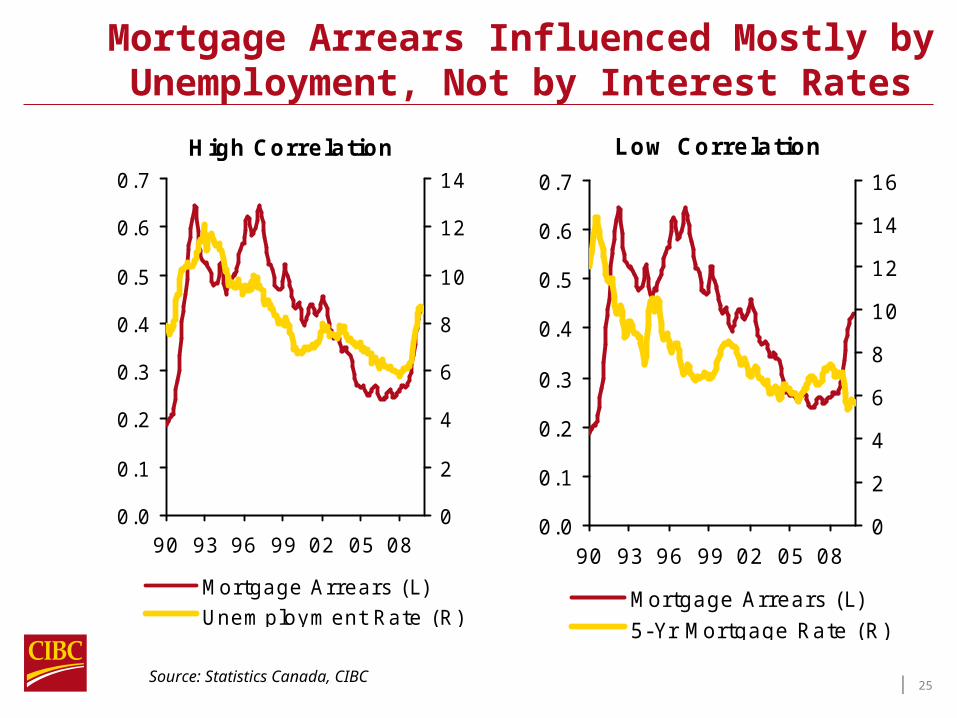

Mortgage Arrears Influenced Mostly by Unemployment, Not by Interest Rates

Source: Statistics Canada, CIBC

High Correlation

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

90 93 96 99 02 05 080

2

4

6

8

10

12

14

Mortgage Arrears (L)Unemployment Rate (R)

Low Correlation

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

90 93 96 99 02 05 080

2

4

6

8

10

12

14

16

Mortgage Arrears (L)5-Yr Mortgage Rate (R)

| 26

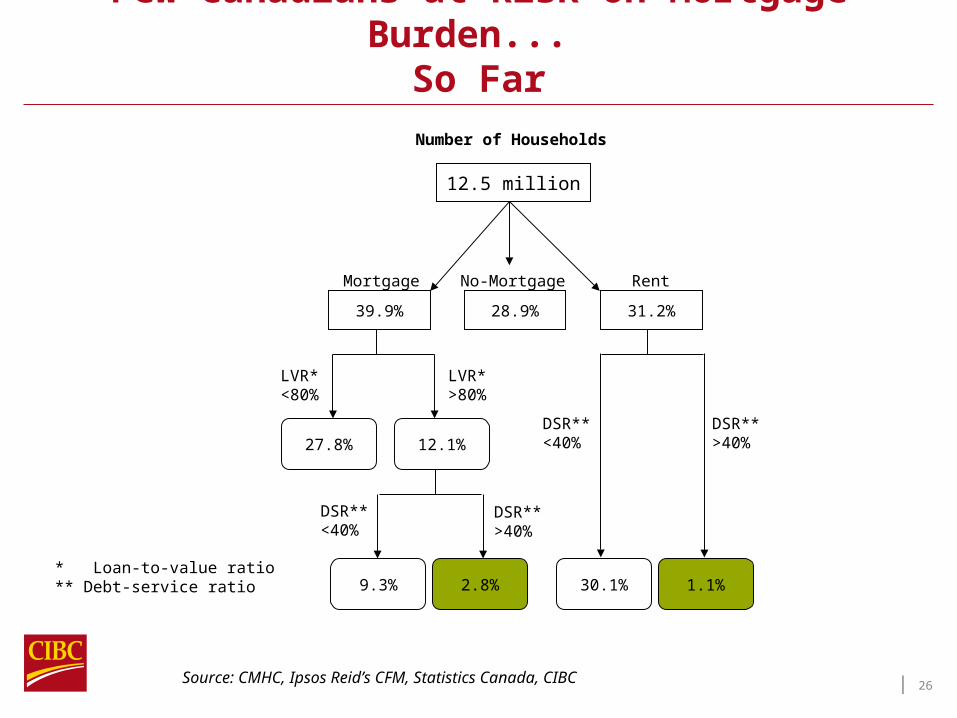

Few Canadians at Risk on Mortgage Burden...

So Far

Source: CMHC, Ipsos Reid’s CFM, Statistics Canada, CIBC

Number of Households

Mortgage

12.5 million

27.8%

31.2%

Rent

DSR**<40%

28.9%39.9%

No-Mortgage

12.1%

* Loan-to-value ratio** Debt-service ratio

LVR*<80%

LVR*>80%

9.3% 2.8%

DSR**>40%

DSR**<40%

DSR**>40%

30.1% 1.1%

| 27

Low Income Canadians Rely Less on VRM

Source: Ipsos Reid’s CFM, CIBC

Share of Variable Rate Mortgage by Income Group

10

15

20

25

30

35

40

< $55k $55k - $70k $70k -$100k

$100k+

%

| 28

Money Market Fund

Out of Cash...

45

50

55

60

65

70

75

80Ja

n-0

8

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

$bn

Money Market

Source: IFIC, CIBC

… Into Bond & Equities

40

50

60

70

80

Jan

-08

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

60

80

100

120

140

160

180

200$bn

Bond & I ncome (L)

Equities(R)

$bn

| 29

10-Year Lagged Cyclically Adjusted TSX PE Ratio

0

10

20

30

40

50

60

70

Long-TermAvg

(23.7)

| 30

Dividend Stocks Have Done Well, Long Term (right) and Recently (left)

45.8

32.2

0

5

10

15

20

25

30

35

40

45

50

TSXC omposite

DividendAristocrats

% Total Return in 2009

800

1100

1400

1700

2000

J un-04 Dec-05 J un-07 Dec-08

TSX C omposite TRDividend Aristocrats TR

Total Return, J un-04 = 1000

Source: S&P, CIBC

| 31

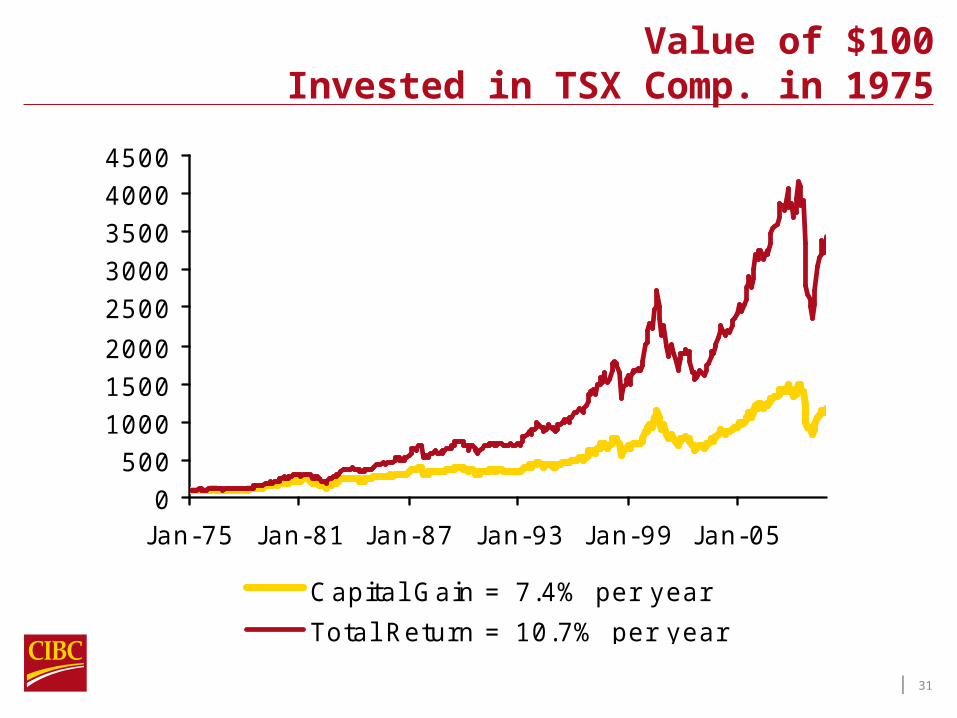

Value of $100 Invested in TSX Comp. in 1975

0500

100015002000

25003000350040004500

J an-75 J an-81 J an-87 J an-93 J an-99 J an-05

C apital Gain = 7.4% per year

Total Return = 10.7% per year

| 32

Eight Highest Yielding TSX Industry Groups

Source: Bloomberg, CIBC

Indicated Dividend Yield (%)

Telecommunication Services 5.5

Utilities 5.1

Real Estate 5.0

Media 4.7

Diversified Financials 4.2

Health Care Equipment & Services 4.0

Banks 4.0

Insurance 3.8

| 33

Question

&

Answer

This material was prepared for investment professionals only and is not for public distribution. It is for informational purposes only and is not intended to convey investment, legal, or tax advice. The material and/or its contents may not be reproduced without the express written consent of Renaissance

Investments.