political economy of china - university of british columbia

TRANSCRIPT

Governments and Markets

Topic 4

Political Economy - Trebbi2

Goals of the Lecture

1) Regulation and Markets

2) Procurement

3) Antitrust

4) Theoretical analysis (cost reimbursement, yardstick competition, regulated prices, etc.)

Suggested readings: Ch.9, 10, 11 Baron (2007).

Political Economy - Trebbi3

Regulation

Political Economy - Trebbi4

Regulation

Regulation is government intervention in economic activity using commands, controls, and incentives.

Regulation is not only an economic instrument (say, aiming at solving market failures), but is also a political instrument (social regulation, say, rent controls, or health and environmental protection).

Regulation is implemented by independent commissions and agencies of the executive branch. In contrast to antitrust, regulation is usually not implemented through judicial institutions.

Participating in regulatory rule making is considered as important as lobbying Congress by 2/3 of special interests groups (Kerwin, 1994).

Can you give me some examples?

Political Economy - Trebbi5

Typical Regulatory Interventions

1. Price controls (e.g. crops, minimum wages, local telephone service, electricity)2. Controlling number of market participants (e.g. broadcast or taxi licenses, )3. Ensuring equal opportunity (e.g. banning discrimination in employment)4. Providing for solvency (e.g. pensions plans, financial institutions, insurance)5. Specifying qualifications (e.g. occupational licensure)6. Requiring pre-marketing approval, testing, labeling, product safety (e.g.

pharmaceuticals, toxic chemicals, cars)7. Allocating scarce public resources (e.g. spectrum allocation, fisheries)8. Controlling toxic emissions and other pollutants (e.g. CO2, sulfur dioxide, emissions

trading)9. Controlling unfair international trade practices (e.g. antidumping)10. Specifying industry boundaries (insurance, investment and commercial banking, stock

brokerage)11. Mandating information disclosure (publicly trade firms accounting and statements)12. Limiting ownership (media, airlines)

Political Economy - Trebbi6

Foundations

In the early 1100s the English monarchy started contracting with private parties for the provision of public goods and services. In common law the contractual agreements between the Crown and a firm provided the legal foundations for regulation.

Early examples: the King allocated rights-of-way to stage lines in exchange of the authority to regulate prices and services.

Political Economy - Trebbi7

Foundations (cont.)

Abuses were common.

Shleifer and Vishny (QJE 1993) report that:

In 1400 there were 60 independently run tolls along the Rhine.

There were so many tolls along the Seine that 20 miles of transportation had a cost equal to the price of the good.

England was free of such tollbooths.

So large differences in early examples of government interventions in markets.

Political Economy - Trebbi8

Legal Foundations

In US common law regulatory jurisdiction is very broad:

“[when] affected with a public interest, [private property] ceases to be juris privati only…When, therefore, one devotes his property to a use in which the public has an interest, he, in effect, grants to the public an interest in that use, and must submit to be controlled by the public for the common good…” Munn v. Illinois (1877)

However, “What a company is entitled to ask is a fair return upon the value of that which it employs for the public convenience.” Smith v. Ames (1898)

This is the basis for cost-of-service regulation in the 1960s and 1970s for instance.

Political Economy - Trebbi9

Regulatory agencies

Two forms:

1) Executive branch agencies;

2) Independent commissions.

Executive branch agencies are direct emissions of the executive, they are directly linked to cabinet departments, and tend to be more partisan.

Independent commissions’ members are usually appointed by the executive but have to be confirmed by the Senate. Tend to be non-partisan (in fact, terms in office are longer than a standard legislature between 7 and 14 years).

Political Economy - Trebbi10

Some Examples

Independent Commissions (Year Est) Agencies (Year, Department)

Federal Reserve System (1913) Food and Drug Administration (1931, HHS)

Federal Trade Commission (1914) Federal Aviation Administration (1948, DOT)

International Trade Commission (1916) National Highway Traffic Safety Administration (1970, DOT)

Federal Energy Regulatory Commission (1916)

Occupational Safety and Health Administration (1973, DOL)

Securities and Exchange Commission (1934)

Environmental Protection Agency (1970 – no cabinet dept.)

Federal Communications Commission (1934)

National labor Relations Board (1935)

Federal Maritime Commission (1961)

Equal Employment Opportunity Commission (1965)

Nuclear Regulatory Commission (1975)

Political Economy - Trebbi11

Regulatory rule-making

All agencies’ main task is regulatory rule-making, a process under the Administrative Procedure Act (1946). Formal or informal.

Informal rule making requires publishing on the Federal Register a Notice of Proposed Rule Making (NPRM) and a request for the submission of comments. Once all comments are collected, the rule is revised and published as final on the Register effective at least 30 days in the future.

Formal rule making is a quasi-judicial process that requires hearings conducted by an administrative law judge, presentation of evidence, witness testimony and cross-examination. The record offers the basis for the regulatory rule and it follows procedural due process.

Parties can sue for judicial review under the APA. Both rule making processes are subject to review by the courts, that assess whether an action exceeds the scope of the mandate of the regulatory agency (substantive due process) or does not follow protocol (procedural due process).

Political Economy - Trebbi12

Regulatory Agency Influences (Checks and Balances)

Special Interests influence the Regulators directly through their testimonies, petitions, and lobbying. Indirectly through lawsuits.

Congress influences the Regulators directly through the definition of mandate and oversightand indirectly through appropriating the Agency Budget.

The President influences the Regulators directly through appointing their heads and steering their policy goals.

The Courts influence the Regulators through judicial reviews of due process (procedural and substantive) and Constitutionality.

Political Economy - Trebbi13

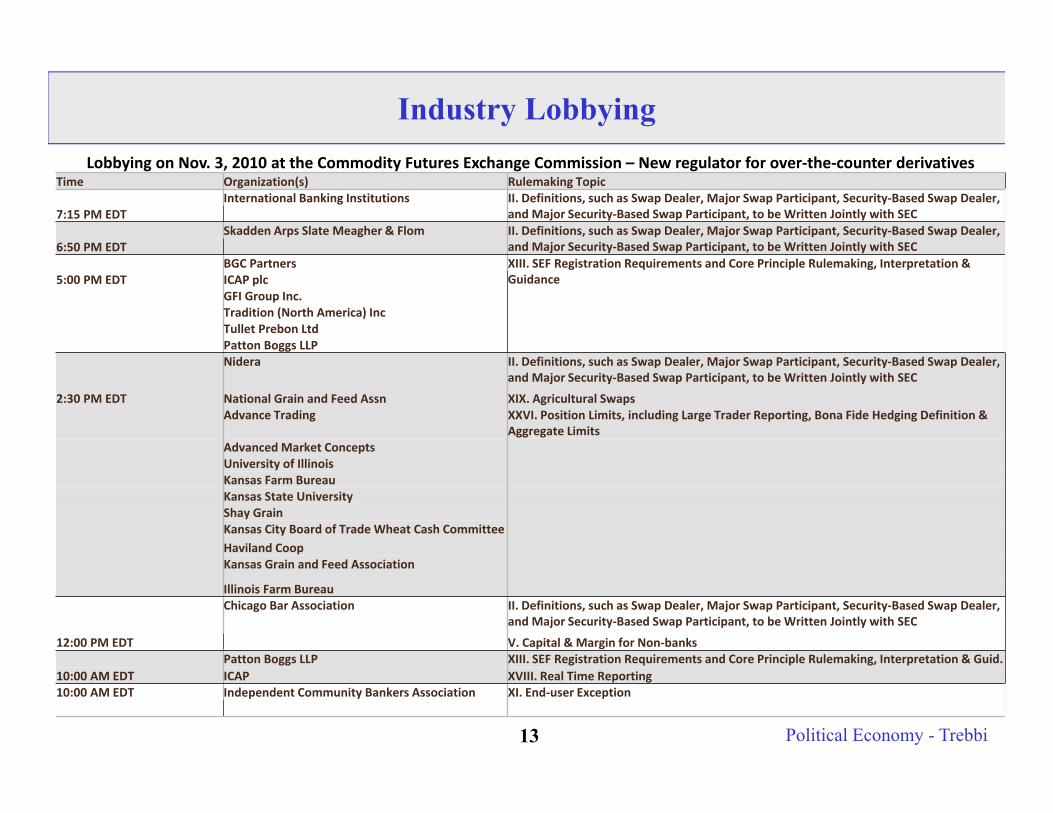

Lobbying on Nov. 3, 2010 at the Commodity Futures Exchange Commission – New regulator for over‐the‐counter derivativesTime Organization(s) Rulemaking Topic

International Banking Institutions II. Definitions, such as Swap Dealer, Major Swap Participant, Security‐Based Swap Dealer, and Major Security‐Based Swap Participant, to be Written Jointly with SEC7:15 PM EDT

Skadden Arps Slate Meagher & Flom II. Definitions, such as Swap Dealer, Major Swap Participant, Security‐Based Swap Dealer, and Major Security‐Based Swap Participant, to be Written Jointly with SEC6:50 PM EDT

BGC Partners XIII. SEF Registration Requirements and Core Principle Rulemaking, Interpretation & Guidance5:00 PM EDT ICAP plc

GFI Group Inc.Tradition (North America) IncTullet Prebon LtdPatton Boggs LLPNidera II. Definitions, such as Swap Dealer, Major Swap Participant, Security‐Based Swap Dealer,

and Major Security‐Based Swap Participant, to be Written Jointly with SEC

2:30 PM EDT National Grain and Feed Assn XIX. Agricultural SwapsAdvance Trading XXVI. Position Limits, including Large Trader Reporting, Bona Fide Hedging Definition &

Aggregate LimitsAdvanced Market ConceptsUniversity of IllinoisKansas Farm BureauKansas State UniversityShay GrainKansas City Board of Trade Wheat Cash CommitteeHaviland CoopKansas Grain and Feed Association

Illinois Farm BureauChicago Bar Association II. Definitions, such as Swap Dealer, Major Swap Participant, Security‐Based Swap Dealer,

and Major Security‐Based Swap Participant, to be Written Jointly with SEC

12:00 PM EDT V. Capital & Margin for Non‐banksPatton Boggs LLP XIII. SEF Registration Requirements and Core Principle Rulemaking, Interpretation & Guid.

10:00 AM EDT ICAP XVIII. Real Time Reporting10:00 AM EDT Independent Community Bankers Association XI. End‐user Exception

Industry Lobbying

Political Economy - Trebbi14

Why do we need regulation?

Answer 1: To correct market imperfection (e.g. negative externalities, asymmetric information, etc.).

Answer 2: We do not. In fact, rent seeking drives regulatory agencies who skim/gain from restricting entry or redistributing gains from trade.

Political Economy - Trebbi15

Typical Market Imperfections

Let’s consider typical situations were government intervention may be useful to solve market imperfections.

1. Natural monopoly – A local energy market where the efficient power plant size is so large that one firm can produce a given amount at lower cost than can any larger number of firms.

2. Asymmetric information. Adverse selection – Private health insurance market

3. Asymmetric Moral Hazard – Car insurance market. Banking.

4. Externalities – CO2 emissions

5. Public goods – Broadcast licenses

Political Economy - Trebbi16

Natural Monopoly

A natural monopoly arises in presence of economies of scale (marginal/average costs are decreasing in the scale of output). Inefficiently low output (at MC=MR there are consumers willing to buy the good at a price above marginal cost) – Deadweight loss.

The government will usually try to lower the price toward p0.

Demand

Marginal Cost

MarginalRevenue

DWL

q

p

p0

p2

Political Economy - Trebbi17

Natural Monopoly (cont.)

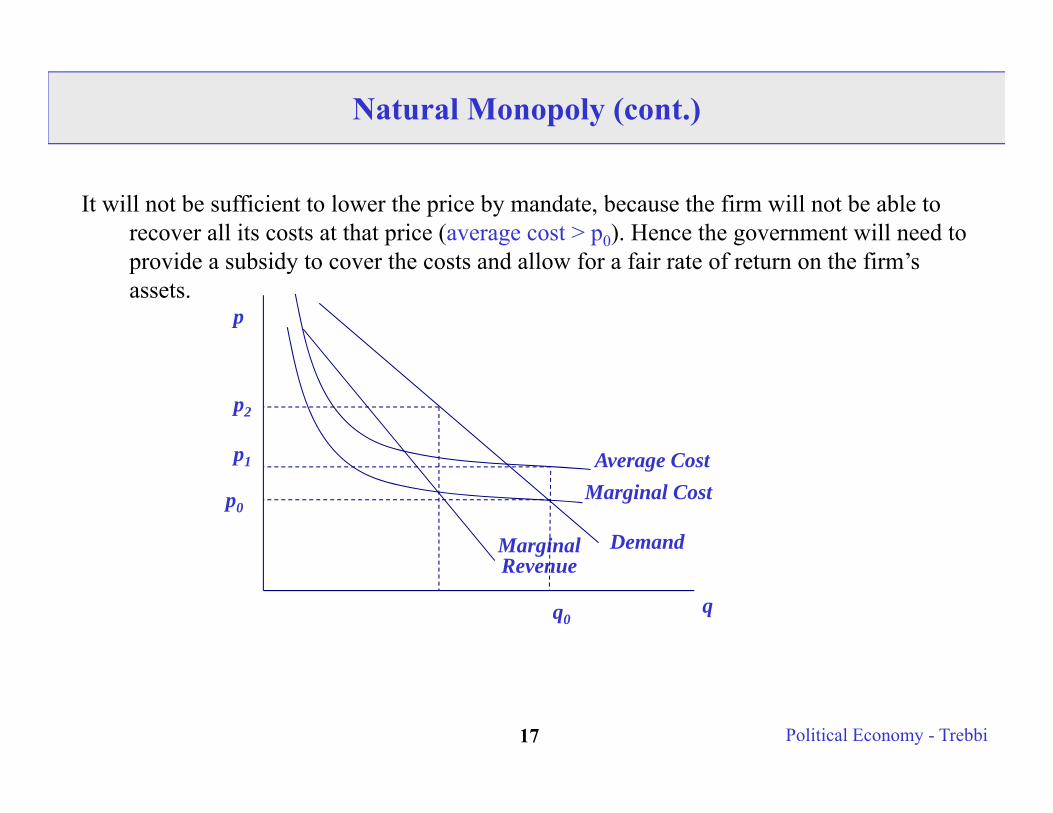

It will not be sufficient to lower the price by mandate, because the firm will not be able to recover all its costs at that price (average cost > p0). Hence the government will need to provide a subsidy to cover the costs and allow for a fair rate of return on the firm’s assets.

Demand

Marginal Cost

MarginalRevenue

q

p

p0

p2

Average Costp1

q0

Political Economy - Trebbi18

Natural Monopoly (cont.)

It will not be sufficient to lower the price by mandate, because the firm will not be able to recover all its costs at that price (average cost > p0). Hence the government will need to provide a subsidy to cover the costs and allow for a fair rate of return on the firm’s assets.

The government will either try to lower the price to p1 or use fixed charges (e.g. monthly fixed charges).

Demand

Marginal Cost

MarginalRevenue

q

p

p0

p2

Average Costp1

q0

Political Economy - Trebbi19

Natural Monopoly (cont.)

Example: Under a cost of service regulation consumers pay monthly charges to cover the fixed costs of electric power plants, including a fair rate of return on capital.

Example: Local telephone companies also are allowed to charge fixed amounts for the same reason.

Also notice:

1. Economies of scale does not mean Natural Monopoly (economies of scale may exhaust at a scale that allows entry of other firms). This seems to be the case even for energy markets.

2. Monopoly may be not so inefficient when there is an entry threat. If the market is contested by potential entrants the incumbent may leave the price as low as to make entry just about inefficient (this means it will increase output and the inefficiency will be low). Also monopolies use nonlinear prices, that decrease the DWL

3. Monopolies are of the natural type also when large fixed costs would be inefficiently duplicated (local telecommunication systems or power grids).

Political Economy - Trebbi20

Adverse Selection & Regulation

Akerlof’s (1970) market for lemons problem.

Suppose I know the value of my used car is x and the distribution of used car values on the market is F(x), with mean xm. Also assume there is a buyer for every car. However, if the car type is difficult to assess for a buyer, a buyer will be willing to pay no more than xm.

So if x > xm, I will not put my car on the market. This means that the pool of available cars will be even worse, and people will be willing to pay even less, because quality is lower on average. The market will fully unravel.

Example: Consider now a health care system that is voluntary. Only patients with bad health will self-select in. Healthy patients will not be willing to pay higher premia than it is actuarially fair for them. So the good types will be crowded out. Rationale for Hillary Clinton’s 2008 presidential platform on health care reform. Universal and Compulsory => increases patients’ pool quality. Barak Obama’s proposal was Universal and Voluntary.

Political Economy - Trebbi21

Moral Hazard & Regulation

If individuals do not bear the full consequence of their actions, because of an asymmetric information issue (say, I cannot observe if a bad outcome is the result of your lack of care or just bad luck – i.e. the action is unobservable or cannot be contracted upon), then you will have a condition of moral hazard.

Typical problem in banking sector regulation.

A bank can take on a very risky project in the hope it turns out well or a safe project, but with a lower expected payoff. If the bank knows it will be bearing the full cost of the risky project even in the bad state, the decision will be first best.

However, if there is the possibility of being bailed out by the government in the bad outcome scenario (say because the government cannot exactly assess the difference between the two projects), and no punishment attached to it, then the bank will take that risky action too often.

Example: Savings and Loans crisis of 1988. Savings and Loans institutions privatizing profits and passing losses to FDIC.

Political Economy - Trebbi22

Externalities may require regulation

Of course almost every action of an economic agent affects other economic agents. If I open up a plant in a city and labor supply is not infinitely elastic, I will raise real wages.

However, demand and supply will be in equilibrium and my marginal cost (the real wage) will equalize the marginal benefit (the worker’s productivity).

The indication of an externality requiring regulation is that the private benefit and costs are different from the social benefits and costs.

Coase’s theorem tells us that if property rights are well defined and transaction costs are null, then there is no need for regulation (i.e. markets will achieve the socially optimal outcomes).

Since such assumptions are not true, governments intervene to make private costs and social costs coincide. This is why we tax polluting firms or we impose environmental standards on cars (Pigouvian taxes).

See bonus material on Environmental Regulation.

Political Economy - Trebbi23

Public Goods & Regulation

Pure public good = consumption by one individual does not reduce its availability for others (nonrival).

Example: National defense, radio broadcast.

Either supplied by the government directly or by private firms, which are then regulated.

The reason why regulation is necessary is that the optimal amount of public good provision is under-funded if left to private parties (Bergstrom, Blume,Varian, JPubE 1986 “On the private provision of public goods”).

Why: Free-rider problem.

Political Economy - Trebbi24

Political Economy Rationale

The Chicago school of Stigler (1971), Peltzman (1976) and Posner (1974). Two different views, both positive, not normative.

A. CaptureRegulation soon forgets the goal of economic efficiency. Regulation evolves over time to

serve the interests of the regulated firms, who profit from entry barriers. The regulated “capture” the regulator.

Example: Mortgage Brokers and Bankers Industry captured the FHA (Federal Housing Administration) and HUD (Dept. Housing and Urban Development) during the sub-prime mortgage expansion of 2000-2006.

B. Rent seeking/Tollbooth Regulation arises in industries where rents accrue copiously. Regulation is supplied through

the political process and benefits politicians that use it to extract rents. Example: Railroads in the 19th century sought regulation to enforce their cartel agreements

that were plagued by defections and cheating. Politicians gladly obliged obtaining rents

Political Economy - Trebbi25

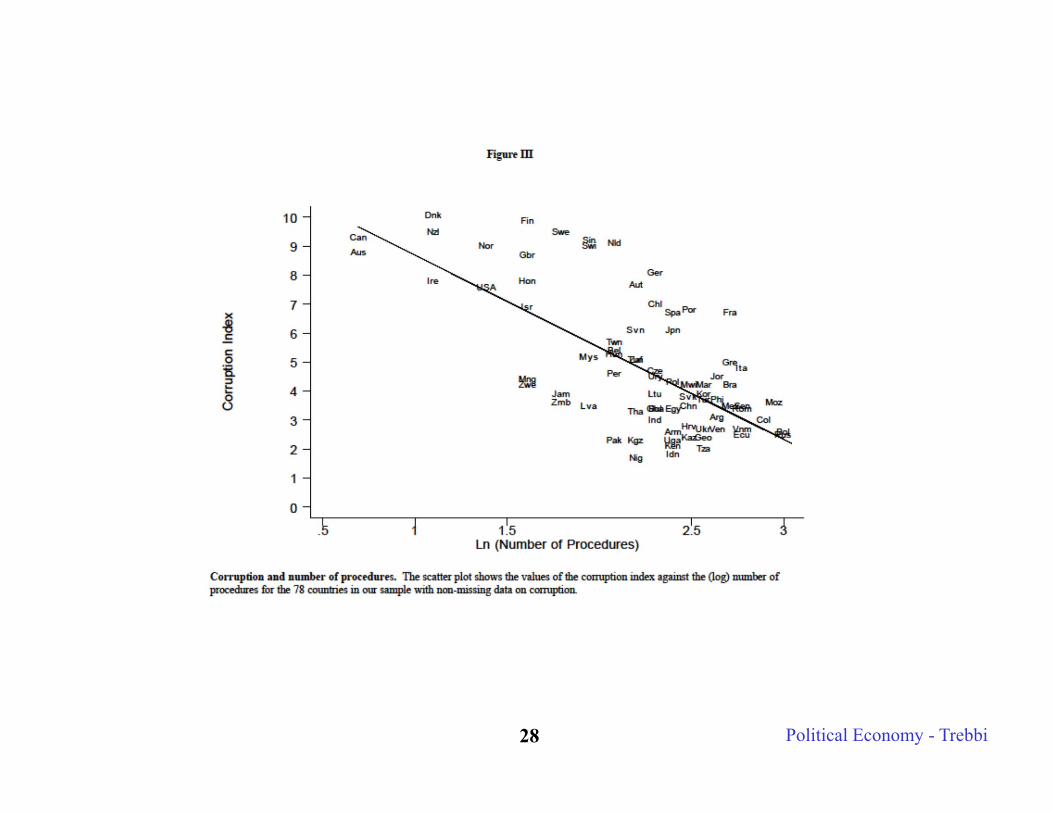

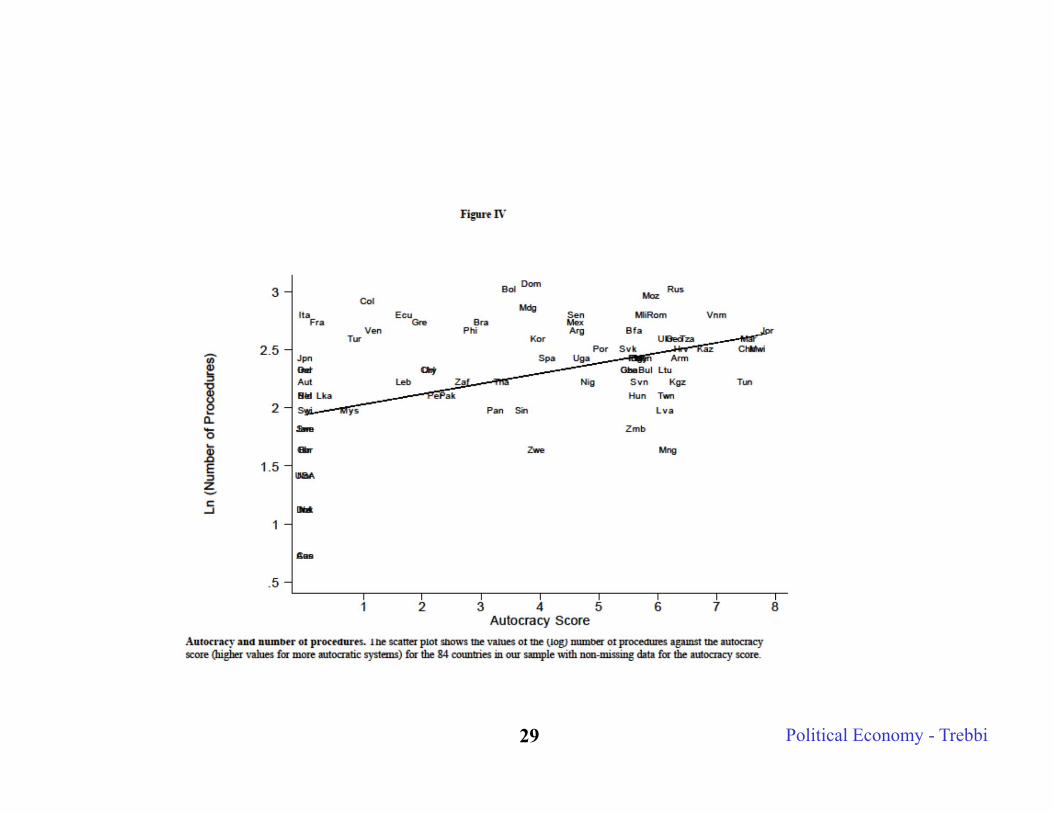

Evidence: Regulation of Entry

De Soto (1990). Djankov, La Porta, Lopez-de-Silanes and Shleifer (QJE 2002) paper.

Regulation of entry of new firms in a cross-section of 85 countries.

The authors look at:i. Number of Proceduresii. Official Timeiii. Official Cost

Evidence favors the public choice view (Stigler, 1971, Peltzman, 1976) that entry regulation benefits politicians and bureaucrats.

a. Heavier regulation is positively correlated with higher corruption.b. Heavier regulation is not correlated with better public goods or more competition.c. More autocratic regimes have heavier regulation (even controlling for GDP per capita).See the following four figures from the paper.

Political Economy - Trebbi26

Political Economy - Trebbi27

Political Economy - Trebbi28

Political Economy - Trebbi29

Political Economy - Trebbi30

(Bad) Examples: Cost-of-Service Regulation

This form of regulation was common in the airline and trucking industry in the 1970s.

Entry was controlled and industry-wide prices were set, with cost increases passed on to consumers in the form of higher prices.

Industry-wide wage increases were passed directly into prices, so weak incentives to resist labor demands. However, this left many firms substantially disadvantaged when markets got deregulated and inefficiently high labor costs started to induce competitive disadvantages.

Cost of service regulation was also used in the telecom business. Since in this sector it is extremely difficult to evaluate the cost structure, regulators allowed firms to simply extract a “fair rate of return” computed on the asset base of the firm. Obviously, telecom firms had an incentive to increase their asset base enormously, with excess capacity and over-investment in inefficient technologies.

Political Economy - Trebbi31

(Bad) Examples: The 3G Telecom Auctions in Europe

The 2000-01 European telecom auctions for third generation (UMTS) licenses were the largest in history. See Klemperer (2002, EER)

Roughly the same per capita value across Western Europe, but differences in auction design and regulatory failure brought in revenues of 20 Euros per capita in Switzerland and 45 in Belgium and Greece to 650 Euros per capita in the UK and 615 Euros in Germany.

300-400 Euros per capita was the estimated revenue. Why these disparities?

Not all auctions were well designed and attracted sufficient entry (especially by non-2G incumbents) or prevented collusions.

Most were ascending auctions (subsequent bid higher than the previous bid) where the number of licenses was equal to the number of (large) incumbents. Entrants were put off. Incumbents ended up having a license each (so no need to compete and bid up).

Political Economy - Trebbi32

The Mother of Bad Examples: Financial Markets and Regulation

Financial sector regulation is dual:

1. Banking regulation (macro-prudential) deals with systemic risk: Cross-bank spillovers and interdependencies.

2. Banking regulation (micro-prudential) deals with safety and soundness of banks for depositors (capital requirements, leverage, etc). Financial securities and commodity regulation focuses on investor protection and disclosure of information.

Hellman, Murdock and Stiglitz (2000)Morrison and White (2005)Dewatripont and Tirole (1994)

Political Economy - Trebbi3333

“In the summer of 2003, leaders of the four federal agencies that oversee the banking industry gathered to highlight the Bush administration's commitment to reducing regulation. They posed for photographers behind a stack of papers wrapped in red tape. The others held garden shears. Gilleran, who succeeded Seidman as OTS director in late 2001, hefted a chain saw.” Source: Washington Post.

Deregulators: OTS, OCC, FDIC, NCUA…

Political Economy - Trebbi34

-3-2

-10

1Fi

nanc

ial D

ereg

ulat

ion

Inde

x

1900 1920 1940 1960 1980 2000 2020year

Note: Replication of Philippon and Reshef (2008) Black and Strahan (2001) Intrastate branching via M&A

US Financial Deregulation

Deregulation in US Financial Markets

Political Economy - Trebbi35

Re-Regulations

Financial regulation and delegation often reactive.

Regulatory patch after the crisis:

• Glass-Steagall Act of 1932 after the onset of Great Depression and 1929.

• Financial Institutions Reform, Recovery and Enforcement Act of 1989 after S&L crisis of 1988.

• Serbanes-Oxley Act of 2002 after the Enron scandal.

Incremental process. Now:

• Dodd-Frank Law of 2010.

Political Economy - Trebbi36

Open Questions

1. Study congressional voting patterns on regulatory and deregulatory bills.

We would like to know who influenced it and how (campaign contributions, lobbying over time).

2. “Divide et Impera” strategy of regulatory fragmentation.

Do we really need an additional regulatory body on top of:

Federal Deposit Insurance Corporation (FDIC)Federal Reserve System (FED)Office of the Comptroller of the Currency (OCC)Office of Thrift Supervision (OTS)State Banking RegulatorsNational Credit Union Administration (NCUA) U.S. Securities and Exchange Commission (SEC)Commodity Futures Trading Commission (CFTC)

and most importantly: What are the consequences of this alphabet soup?

Political Economy - Trebbi37

Financial Market Regulation in the US

0

200

400

600

800

1000

1200

1400

1600Sp

read

(bp

)

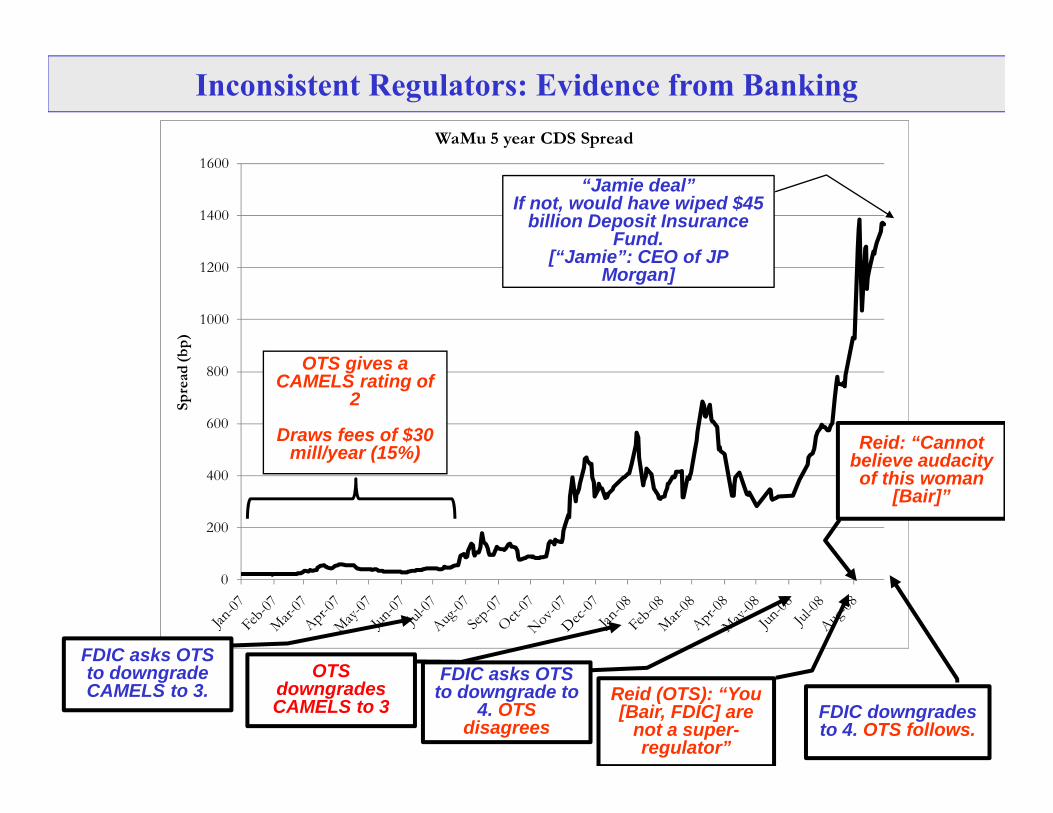

WaMu 5 year CDS Spread

FDIC asks OTS to downgrade CAMELS to 3.

OTS downgrades CAMELS to 3

FDIC asks OTS to downgrade to

4. OTS disagrees

Reid (OTS): “You [Bair, FDIC] are

not a super-regulator”

FDIC downgrades to 4. OTS follows.

“Jamie deal”If not, would have wiped $45

billion Deposit Insurance Fund.

[“Jamie”: CEO of JP Morgan]

Reid: “Cannot believe audacity of this woman

[Bair]”

OTS gives a CAMELS rating of

2

Draws fees of $30 mill/year (15%)

Inconsistent Regulators: Evidence from Banking

39

WaMu is a (costly) anecdote.

Is this behavior systematic?

Within the context of US banking, Agarwal, Lucca, Seru, Trebbi (2012) ask: Do different regulators implement same rules differently? What are the consequences of inconsistent oversight?

Motivation

40

Establishing systematic differences in regulatory and supervisory behavior is hard

Heterogeneity of regulator actions and responsibilities FRB: Macro-prudential regulation, Risk Assessments, LOLR,… State Regulators: Micro-prudential regulation, Supervision,…

Heterogeneity of financial firms regulated Financial firms complex and differ substantially Selection of banks into regulatory environments

Empirical Complications

41

Dual Banking System

42

Selection of banks into regulatory environments not just a theoretical possibility Negatively: Competition for laxity (Chairman Burns, 1974)

“Ability of financial companies to shop for the regulator of their choice weakened their oversight prior to the crisis”

President Obama, 2009

“When Countrywide Financial felt pressured by federal agencies charged with overseeing it, executives at the giant mortgage lender

simply switched regulator to OTS in the spring of 2007” Washington Post, 2008

Empirical Complications

43

Selection of banks into regulatory environments not just a theoretical possibility … or positively: “Checks and balances of a system of more than one

regulatory authority” (Chairman Greenspan, 1993 )

“Charter switching enhances adaptability of the banking system and allows for more innovation”

American Bankers Association, 2009

“State regulators are cheaper….State regulators also advertise their accessibility and say they better understand local conditions and

concerns. ”

Washington Post, 2009

Empirical Complications

44

Heterogeneity of regulator actions: Focus on prudential supervision On-site exams: one of two pillars US banking supervision Culminate in a “CAMELS” rating From 1 [safe] to 5 [failing]

Important rating for several reasons Comparable across regulators

What We Do

45

Heterogeneity of banks: Exploit legally-determined policy Assigns federal and state supervisors to same bank at exogenously

pre-determined time interval

What We Do

46

Legally-determined rotation policy circumvents bank self-selection Riegle Act of 1994: federal agencies required to use state reports as

substitute in alternate 12-month (18-month for small banks) cycles Between State Regulator and FRB for SMBs Between State Regulator and FDIC for NMBs

~80% US commercial Banks covered (30% by assets)

Can track Different regulators behavior when dealing with same bank Bank behavioral response to differential regulator behavior

What We Do

47

Inconsistent regulatory behavior when dealing with same bank Federal agencies twice as likely to issue a downgrade in ratings

Banks respond to differential regulatory behavior Induces variability in operations Federal regulators induce readjustments of capital ratios, NPLs, and

delinquencies, implying lower ROA

Why do these differences exist? Suggestive evidence: Local regulators protect local constituents. Less

evidence on capture.

Main Findings

48

CAMELS Downgrades

SMBs, FRB-STATE rotatingCAMELS upgrade CAMELS downgradeFreq. Percent Freq. Percent

FRB 115 35.83 491 73.28STATE 206 64.17 179 26.72Total 321 100 670 100

Mean SD Mean SD∆CAMELS -1 0 1.091 0.331

NMBs, FDIC-STATE rotatingCAMELS upgrade CAMELS downgradeFreq. Percent Freq. Percent

FDIC 1262 47.14 3376 61.58STATE 1415 52.86 2106 38.42Total 2677 100 5482 100

Mean SD Mean SD∆CAMELS -1 0 1.134 0.391

49

CAMELS Downgrades

49

Federal regulator twice

as likely to downgradethan State

SMBs, FRB-STATE rotatingCAMELS upgrade CAMELS downgradeFreq. Percent Freq. Percent

FRB 115 35.83 491 73.28STATE 206 64.17 179 26.72Total 321 100 670 100

Mean SD Mean SD∆CAMELS -1 0 1.091 0.331

NMBs, FDIC-STATE rotatingCAMELS upgrade CAMELS downgradeFreq. Percent Freq. Percent

FDIC 1262 47.14 3376 61.58STATE 1415 52.86 2106 38.42Total 2677 100 5482 100

Mean SD Mean SD∆CAMELS -1 0 1.134 0.391

5050

Counter-balanced by

upgradesby State

SMBs, FRB-STATE rotatingCAMELS upgrade CAMELS downgradeFreq. Percent Freq. Percent

FRB 115 35.83 491 73.28STATE 206 64.17 179 26.72Total 321 100 670 100

Mean SD Mean SD∆CAMELS -1 0 1.091 0.331

NMBs, FDIC-STATE rotatingCAMELS upgrade CAMELS downgradeFreq. Percent Freq. Percent

FDIC 1262 47.14 3376 61.58STATE 1415 52.86 2106 38.42Total 2677 100 5482 100

Mean SD Mean SD∆CAMELS -1 0 1.134 0.391

CAMELS Upgrades

51

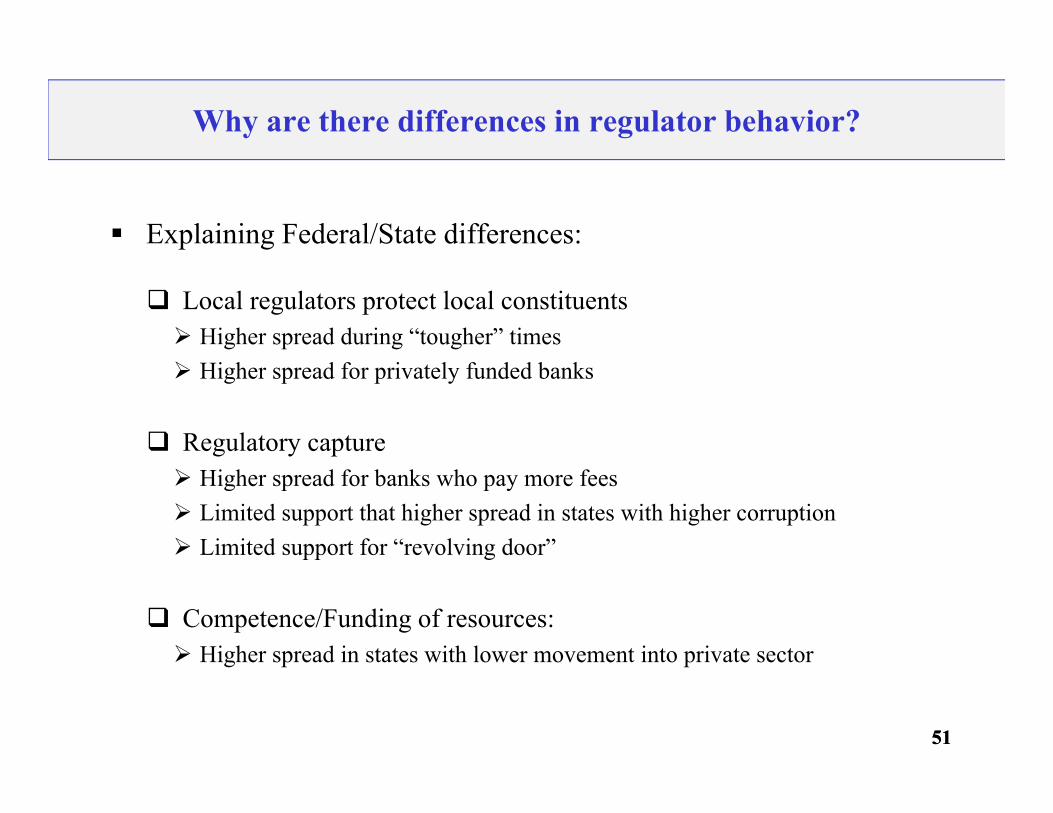

Explaining Federal/State differences:

Local regulators protect local constituents Higher spread during “tougher” times Higher spread for privately funded banks

Regulatory capture Higher spread for banks who pay more fees Limited support that higher spread in states with higher corruption Limited support for “revolving door”

Competence/Funding of resources: Higher spread in states with lower movement into private sector

Why are there differences in regulator behavior?

51

Political Economy - Trebbi52

(Bad) Examples: Deregulation in the (California) Energy market

The energy industry is massive (3% of GDP = telecom+airlines combined).

Large differences in average prices of kilowatt hour across states (9.3 cents in California v. 4 cents in Idaho in 1999). This is due to local supply differences, differentials in environmental regulation, and difficulty of energy transmission (electricity cannot be stored and depletes with distance). The industry was initially regulated on a cost-of-service basis.

However, with the help of new technologies, a wholesale market for electricity slowly developed over time. California-based Enron was one of the first companies to operate on the energy spot market (one traded unit is a 15 minutes energy block).

The existence of this market lead to deregulation. Including in California.

This left many energy plants in California at a huge cost disadvantage, because they were not as economical to operate (for instance, because of tougher environmental regulation).

Political Economy - Trebbi53

(Bad) Examples: Deregulation in the (California) Energy market

The stranded investment in these plants got warranted by the government . Government agencies issued bonds to pay off part of the stranded investment of local power suppliers.

Price went down in California at the end of the 1990s. Also the government imposed a price freeze until 2002.

This led to an increase in demand. However, no additional power plants were built to meet demand (nonmarket pressures played a role) and when a drought in the Northwest reduced the supply of hydroelectric power and increase wholesale prices substantially, Californian utilities could not pass the increase onto consumers (reducing demand).

Not all utilities could afford to meet the electricity bills and shut down. The governor had to bail some of them out in 2001 and signed a secret $43 billion long-term electric power contracts. The following year prices went down but the government got stuck with the bill.

This almost bankrupted the Californian government and the governor was recalled in 2003.

Political Economy - Trebbi54

A failed deregulation:1. Bad assessment of supply volatility (i.e. Northwestern drought).

2. Environmental restrictions stifled deployment of new capacity (constraining supply).

3. Price caps and refusal by the California Public Utility Commission to raise retail prices did not allow demand to adjust and the market to clear.

4. Passing all the risk on public utilities was short-sighted, since they had to be bailed out as soon as they became insolvent.

5. Did not allow utilities to sign long-term contracts with wholesale suppliers (only buy on the spot market). No hedging.

The rules governing energy markets in California changed since.

(Bad) Examples: Deregulation in the (California) Energy market

Political Economy - Trebbi55

Antitrust

Political Economy - Trebbi56

Antitrust Legislation: The origins

Farmers and commodity producers (i.e. oil producers) concerned with monopoly of railroad cartels (the “Robber Barons”). See Josephson (1934).

The Interstate Commerce Act of 1887: First Act of Federal Regulation of Interstate Commerce.

The Sherman Act of 1890: First Antitrust Statute. Focuses of unreasonable restraints on trade and the creation of monopolies. Section 1 covers joint anticompetitive behavior of firms. Section2 individual firm behavior.

The logic of early legislation was that the economic power also requires checks and balances (just like political power).

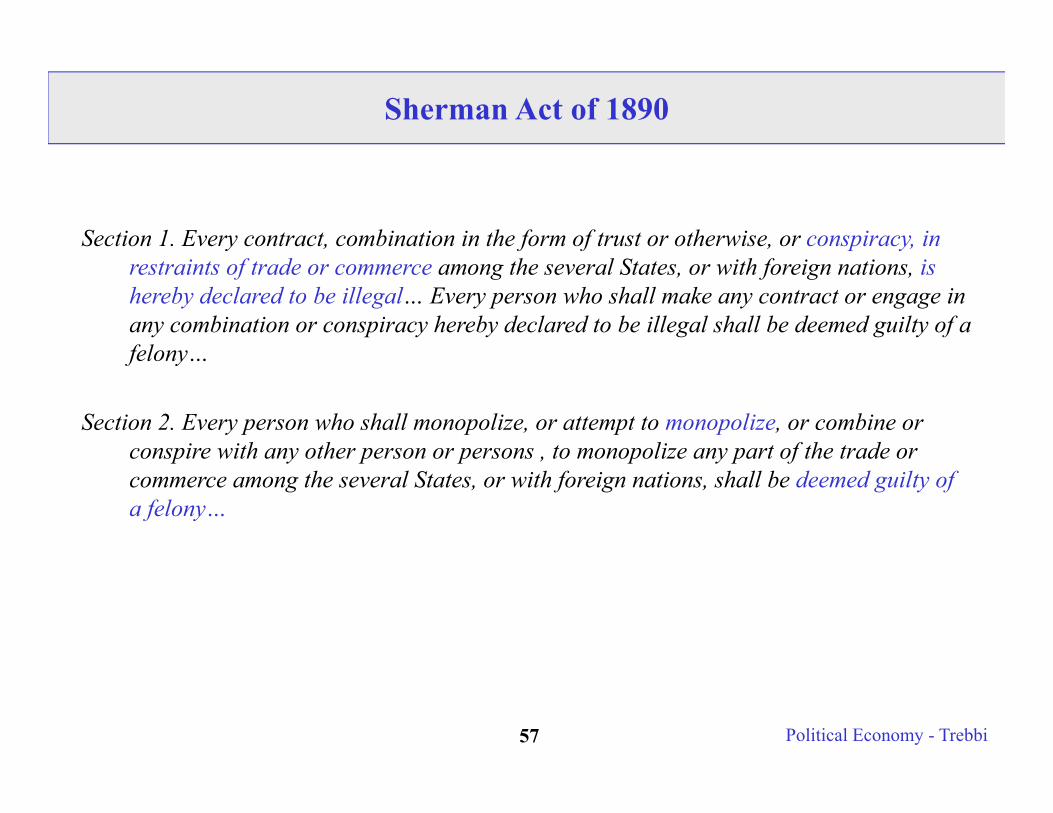

Political Economy - Trebbi57

Sherman Act of 1890

Section 1. Every contract, combination in the form of trust or otherwise, or conspiracy, in restraints of trade or commerce among the several States, or with foreign nations, is hereby declared to be illegal… Every person who shall make any contract or engage in any combination or conspiracy hereby declared to be illegal shall be deemed guilty of a felony…

Section 2. Every person who shall monopolize, or attempt to monopolize, or combine or conspire with any other person or persons , to monopolize any part of the trade or commerce among the several States, or with foreign nations, shall be deemed guilty of a felony…

Political Economy - Trebbi58

Antitrust Legislation: The beginning (cont.)

The Clayton Act of 1914. Monopolization and potentially anticompetitive actions are further specified. Provides for private lawsuits.

The Federal Trade Commission Act of 1914: Prohibits deceiving or unfair methods of competition. Institutes the Federal Trade Commission (FTC) as a main antitrust enforcement and supervisory body.

Note: These Acts are broadly worded and not very specific (“unfair practices”, “restraints on trade”, etc.).

Armies of jurists and economists have helped out designing specific theories to interpret/integrate such wording. Interpretive activity on the parts of the Judiciary has been central in early evolution of precedent. New IO theories have gained weight over time.

Political Economy - Trebbi59

Antitrust Legislation: The beginning (cont.)

Political Economy - Trebbi60

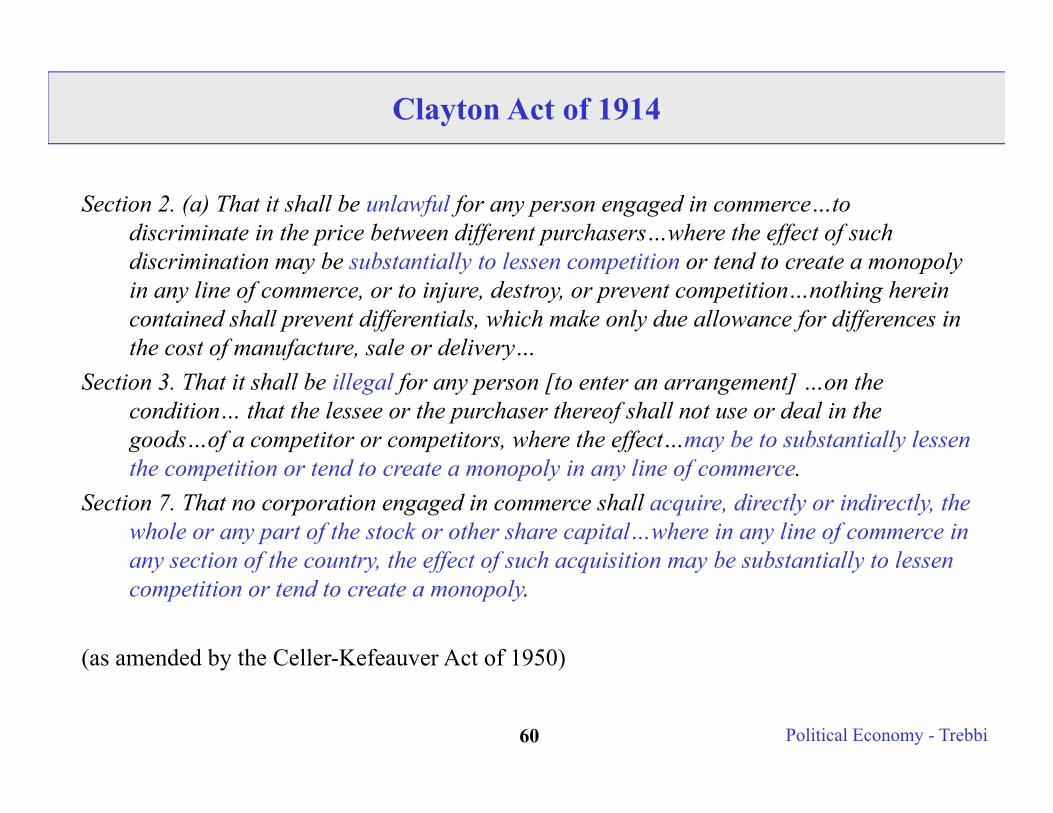

Clayton Act of 1914

Section 2. (a) That it shall be unlawful for any person engaged in commerce…to discriminate in the price between different purchasers…where the effect of such discrimination may be substantially to lessen competition or tend to create a monopoly in any line of commerce, or to injure, destroy, or prevent competition…nothing herein contained shall prevent differentials, which make only due allowance for differences in the cost of manufacture, sale or delivery…

Section 3. That it shall be illegal for any person [to enter an arrangement] …on the condition… that the lessee or the purchaser thereof shall not use or deal in the goods…of a competitor or competitors, where the effect…may be to substantially lessen the competition or tend to create a monopoly in any line of commerce.

Section 7. That no corporation engaged in commerce shall acquire, directly or indirectly, the whole or any part of the stock or other share capital…where in any line of commerce in any section of the country, the effect of such acquisition may be substantially to lessen competition or tend to create a monopoly.

(as amended by the Celler-Kefeauver Act of 1950)

Political Economy - Trebbi61

Federal Trade Commission Act of 1914

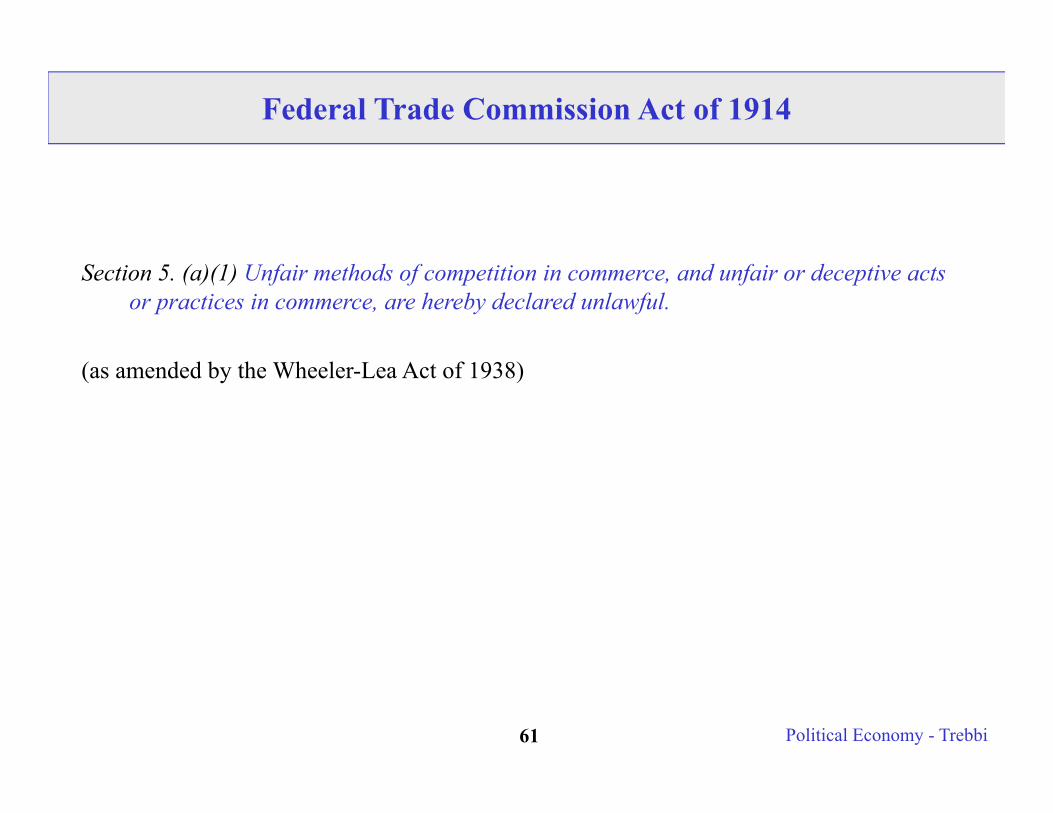

Section 5. (a)(1) Unfair methods of competition in commerce, and unfair or deceptive acts or practices in commerce, are hereby declared unlawful.

(as amended by the Wheeler-Lea Act of 1938)

Political Economy - Trebbi62

Antitrust Legislation: The beginning (cont.)

The Clayton Act of 1914. Monopolization and potentially anticompetitive actions are further specified. Provides for private lawsuits.

The Federal Trade Commission Act of 1914: Prohibits deceiving or unfair methods of competition. Institutes the Federal Trade Commission (FTC) as a main antitrust enforcement and supervisory body.

Note: These Acts are broadly worded and not very specific (“unfair practices”, “restraints on trade”, etc.).

Armies of jurists and economists have helped out designing specific theories to interpret/integrate such wording. Interpretive activity on the parts of the Judiciary has been central in early evolution of precedent. New IO theories have gained weight over time.

Political Economy - Trebbi63

Antitrust Legislation Around the World

Source: Josh Wright, GMU

Political Economy - Trebbi64

Government Enforcement: FTC & DOJ

The Federal Trade Commission (FTC). Enforces the Sherman Act, the Clayton Act and the FTC Act. 5 members appointed by President for 7-years terms.

The Antitrust Division of the Department of Justice (DOJ). Enforces the Sherman Act and the Clayton Act.

Goal: they issue guidelines (e.g. on mergers, on vertical restraints of trade, etc.) and also initiate litigation (usually by industry of competence). Only DOJ brings criminal charges (requiring higher standards of proof).

Political Economy - Trebbi65

Government Enforcement: Criminal and Civil Charges

Criminal charges imply available penalties such as fines and imprisonment.

Civil charges imply contract dissolution, injunctive relief, business units ordered divested.

Example: in 1996 the FTC seeks injunction in federal courts to block the proposed merger between Office Depot and Staples.

Out-of-court settlements between litigants are very common and usually are implemented through Consent Decrees (to remedy antitrust violations and supervised by the court, but do not change precedent because extra-judicial).

Consent decrees can be lifted. Example: in 1956 IBM was a monopolist and some sales and services practices for its mainframes were restricted by consent decree. In 1997 a federal court lifted the consent decree as IBM market share “has substantially diminished”.

Political Economy - Trebbi66

Typical Horizontal Antitrust Practices

Increasing market power within the same industry higher prices & lower competition.

1. Monopolization;

2. Horizontal Mergers;

3. Predatory pricing;

4. Price fixing;

5. Bid rigging;

6. Allocation of customers;

Political Economy - Trebbi67

Examples of Horizontal Antitrust Practices: Early cases

The 1911 case of Standard Oil Co. v. United States broke up the oil industry monopoly. It generated Mobil, Exxon, etc.

The 1911 case of United States v. American Tobacco Co. broke up the tobacco industrymonopoly.

The 1945 case of United States v. Aluminum Co. of America

In this last case the two-step procedure for trial of monopoly was developed by Judge Learned Hand:

First, necessary to prove whether monopoly exists; Second, necessary to prove that anticompetitive or willful practices used to obtain or

maintain monopoly (and not that monopoly exists by superior performance or market characteristics, say Ebay or Ipod).

Political Economy - Trebbi68

Examples of Horizontal Antitrust Practices: AT&T

Founded 1877.

In 1934 a regulated monopoly under the supervision of the Federal Communication Commission. Consent decree in 1956. A de facto monopolist until the mid-1970s

A lawsuit alleging illegal practices by the Bell System finalized at stifling competition in the telecommunication industry was initially filed by the Department Of Justice in 1974 and settled on January 1982.

In 1984 The Bell System was divested.

The Bell System split in 1984 into 7 regional companies plus a residual AT&T company.Verizon is a holding company stemming from Bell Atlantic; AT&T is a holding company

from the long-distance division; QWEST traces back to the Pacific Northwest Bell and Northwestern Bell.

Political Economy - Trebbi69

Examples of Horizontal Antitrust Practices: Microsoft

The Microsoft Antitrust case where the DOJ alleged that Microsoft used anti competitive practices to maintain monopoly of PC Operating System.

Marketing agreements between PC manufacturers and Microsoft restricting the use, licensing, or distribution of non-Microsoft products.

Also DOJ alleged that Microsoft attempted to monopolize the Internet browser market by tying Internet Explorer for free to its Windows OS to put Netscape out of business. Microsoft had initiated a “browser war” and issued “polluted” versions of Java that would only work on Explorer.

Consent Decree (extra judicial agreement validated by the Courts) already in 1995. Lawsuit by DOJ in 1998. Based on market share Microsoft was a monopoly and violated CD.

In 2000 Judge Jackson concluded Microsoft had violated the Sherman Act. Certain practices, when used by a monopolists, (like forcing Compaq not to distribute Netscape) were unreasonable restrictions of competition. Appealed.

Political Economy - Trebbi70

Fines and Damages Paid by Microsoft ($6.83 billion up to 2006)

Source: Todd Bishop, Seattle Post Intelligencer

Owner of Netscape

Political Economy - Trebbi71

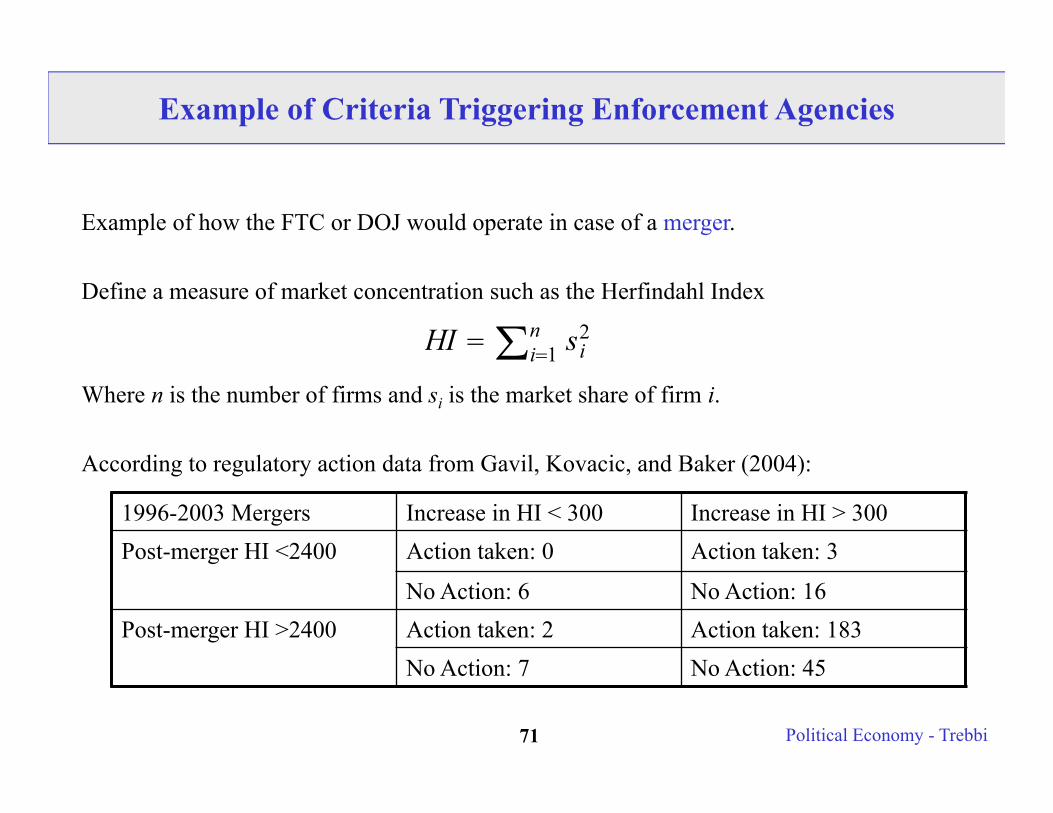

Example of Criteria Triggering Enforcement Agencies

Example of how the FTC or DOJ would operate in case of a merger.

Define a measure of market concentration such as the Herfindahl Index

Where n is the number of firms and si is the market share of firm i.

According to regulatory action data from Gavil, Kovacic, and Baker (2004):

HI ∑i1n si

2

1996-2003 Mergers Increase in HI < 300 Increase in HI > 300Post-merger HI <2400 Action taken: 0 Action taken: 3

No Action: 6 No Action: 16Post-merger HI >2400 Action taken: 2 Action taken: 183

No Action: 7 No Action: 45

Political Economy - Trebbi72

Examples of Horizontal Antitrust Practices: American Airlines

A DOJ’s1999 complaint against American Airlines alleged that American had violated Section 2 of the Sherman Act by engaging in successful predation that involved adding money-losing capacity to drive lower-cost carriers out of four of American's Dallas-Fort Worth Airport routes.

Where low-cost entrants threatened significant expansion of low-cost service, American flooded the routes with additional capacity – more flights, bigger planes, or both.

Former CEO Bob Crandall had stated, “If you're not going to get them out then [there is] no point to diminish profit.”

DOJ alleged […] it made no business sense except for the fact that American stood to gain much more in the long run by eliminating competition and then elevating prices once competition was driven away.

American's conduct made sense only as what Judge Bork has called “an investment in future monopoly profits”.

Source: http://www.justice.gov/atr/public/speeches/201167.htm

Political Economy - Trebbi73

Typical Vertical Antitrust Practices

Supply arrangements or distribution channels across sectors:1. Refusal to deal; Group boycotts;

2. Vertical Mergers;

3. Exclusive territory; Allocation of territories;

4. Exclusive dealing arrangements;

5. Bundling (Tying);

6. Retail price maintenance;

7. Reciprocal arrangements.

Political Economy - Trebbi74

Examples of Vertical Antitrust Practices: Visa&MasterCard

Wal-Mart filed an antitrust lawsuit against Visa and MasterCard in 1996.

Visa and MasterCard had imposed a “honor-all-calls” policy on merchants requiring them to accept debit cards if they accepted credit cards.

Increased the number of transactions over which Visa and MasterCard collected charges.

Wal-Mart alleged illegal tying under Section 1 of Sherman Act. Moreover, attempt to monopolize the debit card market by Visa and MasterCard was a Section2 violation.

Settlement in 2003, Visa paid $2 billion, MasterCard $1 billion to merchants. Revised policy and reduced charges for debit cards.

Political Economy - Trebbi75

Examples of Vertical Antitrust Practices: Mercedes-Benz Parts

DOJ antitrust lawsuit against Mercedes-Benz for requiring its dealers to carry only original Mercedes-Benz auto parts.

Tying.

DOJ later dropped the case because a tying arrangement can only be anticompetitive if based on horizontal market power – if it had restricted competition in the auto parts market (the tied product market), which it did not (the fact that you can only buy Mercedes-Benz parts at a Mercedes-Benz dealer does not mean you cannot buy other parts somewhere else.)

Notice that tying may also aim at maintaining monopoly in the tying market (i.e. auto market). Again obviously not the case here.

Intra-brand (dealers selling the same product from the same firm) vs. Inter-brand (dealers selling products from different firms) competition.

Political Economy - Trebbi76

Examples of Vertical Antitrust Practices: Visa&MasterCard (2)

In 1998 DOJ filed an antitrust case against Visa and MasterCard for exclusionary restrictions. The two companies contractually prevented banks from issuing other credit cards, such as American Express or Morgan Stanley’s Discovery Card.

The district court found against Visa and MasterCard, imposing them to allow commercial banks to issue other cards.

They appealed, but the lower court decision was upheld by the Court of Appeals.

Visa and MasterCard also appealed to the Supreme Court and lost.

Political Economy - Trebbi77

Private Enforcement: Courts

The Courts are the main venue of antitrust activity (570 cases in 1997). Viscusi, Vernon and Harrington (2000): 90% of lawsuits were private over the 1970-1990 period.

Antitrust litigation (initiated by private firms against other private firms) is and has been relevant for shaping antitrust law through the role of legal precedent.

The treble (i.e. triple) damages clause under the Clayton Act provides strong incentive to file a lawsuit.

Usually cases are filed for violations under the Sherman Act. More frequently for vertical antitrust practices than for horizontal. Only 5.4 percent cases go to trial (most settle). Only 30% in favor of plaintiff. Precedents following lawsuits has been fundamental in shaping juridical interpretation.

New economic theories are quickly picked up in courts where both plaintiff and defendants have incentives to make the best case possible.

Political Economy - Trebbi78

Per Se Violation & Rule of Reason in Antitrust

The courts employ a distinction in analyzing antitrust practices:

1. There are actions producing per se antitrust violation because they affect unambiguously structure of market power, the conduct of market participants, and the resulting performance of those markets. The only defense is that the defendant did not commit the act.

Example: Price fixing, output restraints, minimum resale price maintenance, the allocation of customers among competitors are all per se violations of antitrust law.

2. Rule of reason. There are actions producing antitrust violations when the restraint on trade is unreasonable, that is the same action may be reasonable and not deleterious of competition under different circumstances. The two defenses are that the defendant did not commit the act or that the act is a reasonable restriction to competition.

Example: When a manufacturer sets a maximum price that retailers may charge (maximum price resale maintenance) is not per se illegal.

Political Economy - Trebbi79

Examples of Vertical Antitrust Practices & Rule of Reason

Exclusive territorial restrictions were considered per se violations before Continental TV v. GTE Sylvania in 1977

Sylvania (in an effort to revive its market share) had eliminated distributors in the early 1960s and started selling only through franchised retailers in an attempt to have dealers promoting more strongly its TV sets. Sylvania gave out territorial licenses.

Continental TV was agent for San Francisco but wanted to sell in Sacramento. Sylvania refused. Continental sold anyways. Sylvania stopped selling its TV sets to Continental, which sued.

The vertical agreement produced a verdict to the plaintiff. Sylvania appealed and it was reversed on the grounds that this particular vertical restriction was finalized at increasing Sylvania competitiveness, not reducing competition in the TVs market.

Rule of reason was applied. The restriction was not an unreasonable restriction to trade.

Political Economy - Trebbi80

The Theories Influencing the Judiciary

Early decisions emphasized how the structure of markets (market share, concentration, etc.) were the parameter of reference to investigate the presence of antitrust practice (structural approach).

However, after the 1970s this (simplistic) approach got replaced by more emphasis on the effect of antitrust practice on prices. For instance, competition may be vigorous in a market even in presence of oligopoly (think of Bertrand duopoly or a theory of contested monopoly). Also most vertical arrangements seem to foster competition more than stifling it, because they mostly modify intra-brand competition. Some scholars (Baron, 2007) call this the “Chicago School” approach.

Finally, judges started to consider dynamic efficiency implications from new IO, not just static efficiency implications. Think about collusion through repeated interaction. Think about signaling games among competitors (e.g. incumbent versus potential entrants, signaling their cost structure/type). Or network externalities arising from standards of adoption (e.g. Microsoft OS or the “polluted” Java version running only on Windows).

Political Economy - Trebbi81

Contrasting The Theories Influencing the Judiciary (1)

Is predatory pricing (pricing below marginal cost, incurring short term losses to rip the benefit of lower future competition) bad?

Structural approach: definitely, as it reduces the number of firms in a sector and then must reduce competition.

The “Chicago School” approach: Suppose firm A engages in predatory pricing and drives out firm B and then raises prices back up. What does prevent firm C from entering then? Nothing, if there are no barriers to entry. Well, suppose barriers to entry due to sunk costs exist. Even then it is not clear firm C will not enter. It depends for how long firm A could sustain a new price war. So it’s hard ex ante to pin a price cut as “predatory” –most likely the result of healthy competition Antitrust should not stifle.

New IO: Marginal costs are unknown to firms. Asymmetric information about firm A’s costs may induce it to costly signal its type. The price war could be a signal aimed at deterring entrance, even when run by high-costs types trying to mimic efficient producers. In addition, signaling in one market could “protect” other markets.

Political Economy - Trebbi82

Contrasting The Theories Influencing the Judiciary (2)

Should price fixing be a major concern for Antitrust?

Structural approach: definitely, firms will collude whenever possible to decrease competition.

The “Chicago School” approach: Unlikely, suppose firms collude, firms have incentives to undercut each other. Cartels will break down and prices will revert to competitive levels.

New IO: Price fixing is not a one-shot prisoner dilemma. The stage game is repeated over time and, if the players are patient enough, clearly equilibria with collusion (price fixing) are very much possible.

Political Economy - Trebbi83

Special Interests and Antitrust

Powerful special interests like unions, insurance companies, and farmer cooperatives gained statutory exemption from specific antitrust provisions early on.

For Agricultural cooperatives with the Capper-Volstad Act of 1922.

For Unions the Norris-LaGuardia Act of 1932,

For Insurance companies the McCarron-Ferguson Act of 1945,

Political Economy - Trebbi84

Special Interests and Antitrust (cont.)

An egregious example of recent lobbying is the Soft Drink Interbrand Competition Act of 1980. It is a de jure exemption from the Clayton Act for soft drink manufacturers (Coca-Cola, PepsiCo, Canada Dry).

They produce syrup to be sold to bottlers, who are allowed to sell only in specific geographic areas. Exclusive territorial distributorships were deemed anticompetitive in 1978 by the FTC.

Congress was heavily lobbied and passed the act.

The rationale was that there was substantial competition in the soft drink market.

Direct legislative exceptions like this are rare, though.

Political Economy - Trebbi85

Some Theoretical Formalization

Political Economy - Trebbi86

Models of Regulation of a Natural Monopolist

1. Cost Reimbursement of a Monopolist.

2. Yardstick Competition.

3. Regulation of Pricing By A Monopolist.

Note: The best reference for a theoretical treatment of regulation of procurement is “A Theory of Procurement and Regulation” (MIT Press, 1993) By Jean-Jacques Laffontand Jean Tirole. What follows is based on Ch.1 and Ch. 2.

Political Economy - Trebbi87

1. A Simple Model of Cost Reimbursement of a Natural Monopolist

A regulator R is concerned with protecting consumer’s welfare.

R is attempting to force a natural monopolist M to produce a certain good at the lowest cost for taxpayers.

Problem: The regulator does not have specific information about M’s cost structure θ.

Consider the case of two (discrete) states θ = θH with probability 1-β or θL with probability β, and θH > θL > 0. Such distribution is common knowledge.

Define Δθ = θH - θL

Political Economy - Trebbi88

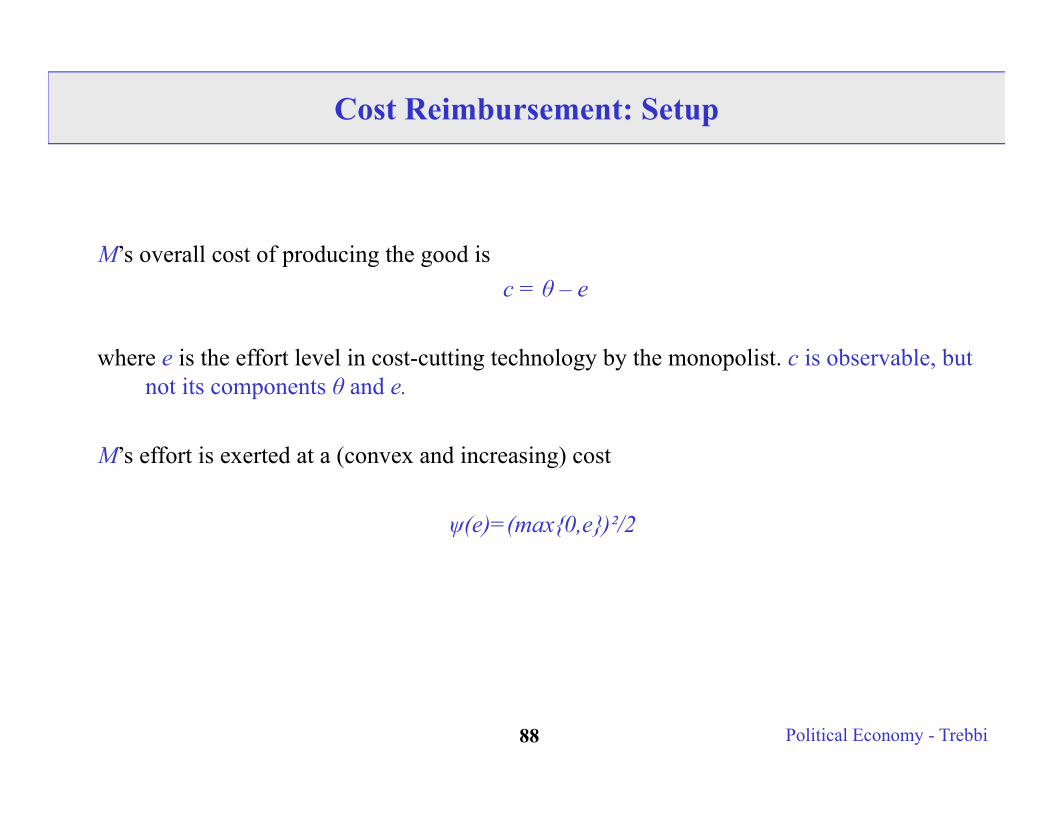

Cost Reimbursement: Setup

M’s overall cost of producing the good isc = θ – e

where e is the effort level in cost-cutting technology by the monopolist. c is observable, but not its components θ and e.

M’s effort is exerted at a (convex and increasing) cost

ψ(e)=(max{0,e})²/2

Political Economy - Trebbi89

Incentives

R wants the good to be produced at the lowest payment P inclusive of subsidies s:

P = s + c

The payoff for the monopolist firm M is:

P – c – ψ(e) = s – ψ(e)

and if M does not produce its outside utility is 0.

Political Economy - Trebbi90

Timing of the game

Sequential structure:

1. State of θ is realized and Monopolist learns it.

2. Regulator offers a menu of contracts for the Monopolist to pick.

3. Monopolist exerts effort e.

4. c is observed.

5. Payoffs realize.

Political Economy - Trebbi91

First Best: Observable Costs

The problem would go away if the asymmetric information about θ were absent.

Then R’s problem would be:

min{P} = min{s + c} = min{s + θ – e}

Subject to the constraint of having M not suffer losses (Participation Constraint)

s - (max{0,e})²/2 ≥ 0

The solution clearly would induce to minimize payments to M, so the participation constraint binds s = (max{0,e})²/2, transforming R’s problem in

min{(max{0,e})²/2 + θ – e}

which is solved at e* = 1 and s* = ½.

Political Economy - Trebbi92

First Best: Observable Costs (cont.)

Marginal cost savings equalized to marginal disutility of effort.

The solution e* = 1 and s* = ½ is true for any cost structure θ.

So the regulator offers a contingent total payment Pi = ½ + θi – 1 for i=L,H.

This is called a PRICE CAP SCHEME (you make the monopolist the residual claimant of the cost-saving effort).

Political Economy - Trebbi93

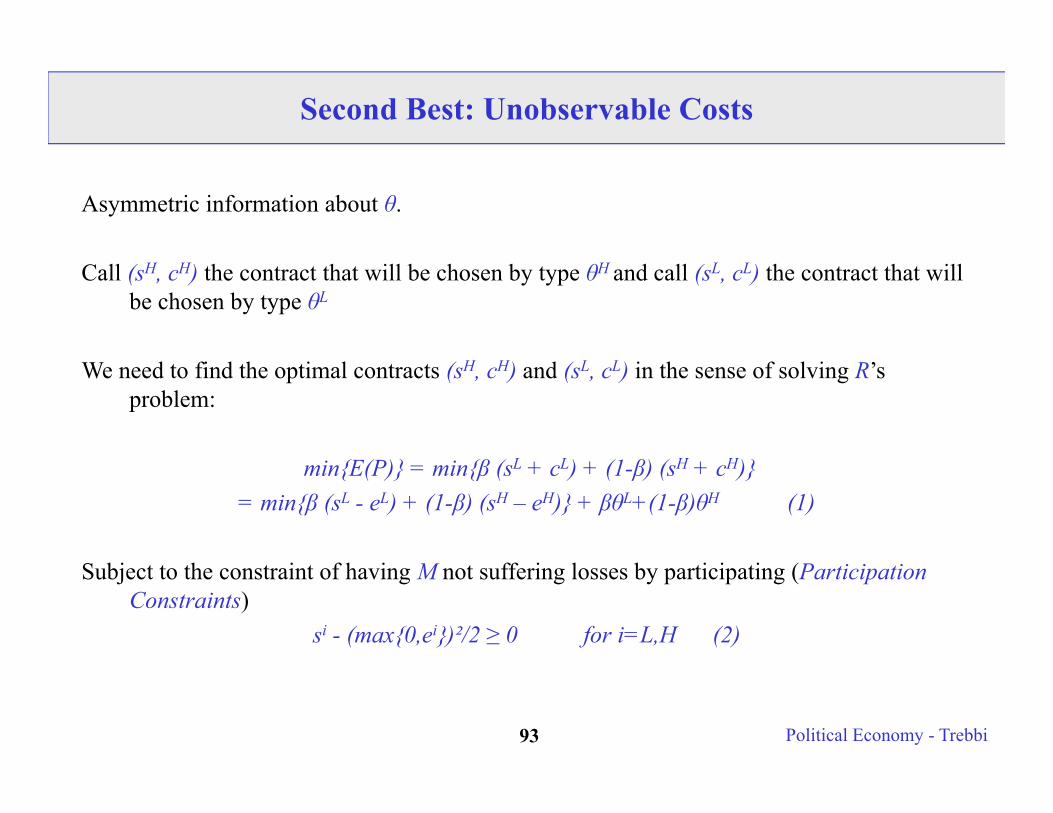

Second Best: Unobservable Costs

Asymmetric information about θ.

Call (sH, cH) the contract that will be chosen by type θH and call (sL, cL) the contract that will be chosen by type θL

We need to find the optimal contracts (sH, cH) and (sL, cL) in the sense of solving R’s problem:

min{E(P)} = min{β (sL + cL) + (1-β) (sH + cH)} = min{β (sL - eL) + (1-β) (sH – eH)} + βθL+(1-β)θH (1)

Subject to the constraint of having M not suffering losses by participating (Participation Constraints)

si - (max{0,ei})²/2 ≥ 0 for i=L,H (2)

Political Economy - Trebbi94

Second Best: Incentive Constraints

And subject to the constraint of having M behaving appropriately depending on the state of the world (Incentive Constraints)

a. In state θ = θL the utility from exercising eL obtaining cL and receiving sL (i.e. obtaining contract (sL, cL) ) must be above the utility from getting contract (sH, cH), hence exercising eH - Δθ in order to obtain cH:

sL - (max{0,eL})²/2 ≥ sH - (max{0,eH - Δθ})²/2 (3)

Note that a credible lie in this case still needs to generate observable costs cH = θL - e

Also the condition cH = θH - eH needs to hold by definition. If you equate the two you see:θL - e = θH - eH

or, as we wrote, e = eH - θH + θL = eH – Δθ [You’d get sH but exercising lower effort]

Political Economy - Trebbi95 Political Economy - Trebbi95

Second Best: Incentive Constraints

b. In state θ = θH the utility from exercising eH and receiving sH must be above the utility from exercising effort eL+Δθ, obtaining cL and receiving sL

sH - (max{0,eH})²/2 ≥ sL - (max{0,eL + Δθ})²/2 (4)

Note: To avoid corner solutions also assume Δθ < θH – cH

Political Economy - Trebbi96

This is not an easy problem to solve, unless you start reducing the number of inequality constraints, looking at which constraints are binding and which are slack.

The relevant Participation Constraint for the high-cost type (2) becomes:sH - (eH)²/2 = 0 (PC)

The equality follows because: i. one PC has to be binding (otherwise R is not saving as much money as possible) and ii. the PC for the low-cost type must be slack because

sL - (max{0,eL})²/2 ≥ sH - (max{0,eH - Δθ})²/2 > sH - (max{0,eH})²/2 ≥ 0 (5)so

sL - (max{0,eL})²/2 > 0

Second Best: Cost Reimbursement Solution

IC Low-cost type PC High-cost type

Political Economy - Trebbi97

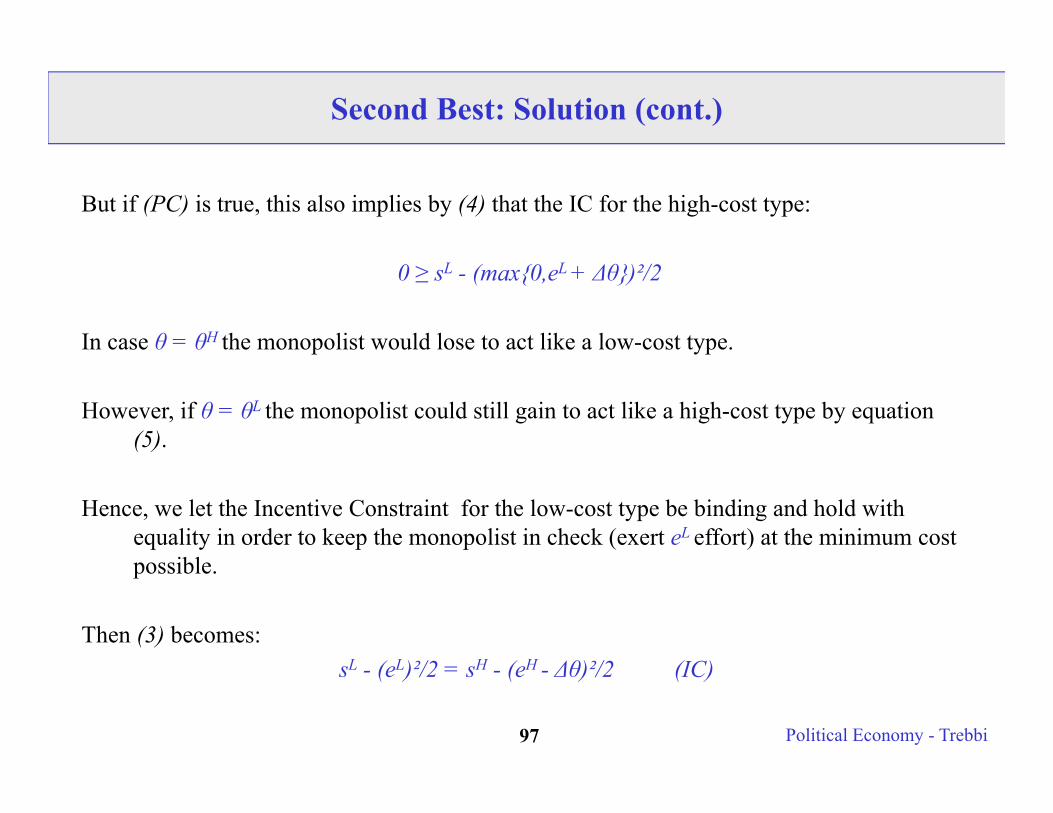

But if (PC) is true, this also implies by (4) that the IC for the high-cost type:

0 ≥ sL - (max{0,eL + Δθ})²/2

In case θ = θH the monopolist would lose to act like a low-cost type.

However, if θ = θL the monopolist could still gain to act like a high-cost type by equation (5).

Hence, we let the Incentive Constraint for the low-cost type be binding and hold with equality in order to keep the monopolist in check (exert eL effort) at the minimum cost possible.

Then (3) becomes:sL - (eL)²/2 = sH - (eH - Δθ)²/2 (IC)

Second Best: Solution (cont.)

Political Economy - Trebbi98

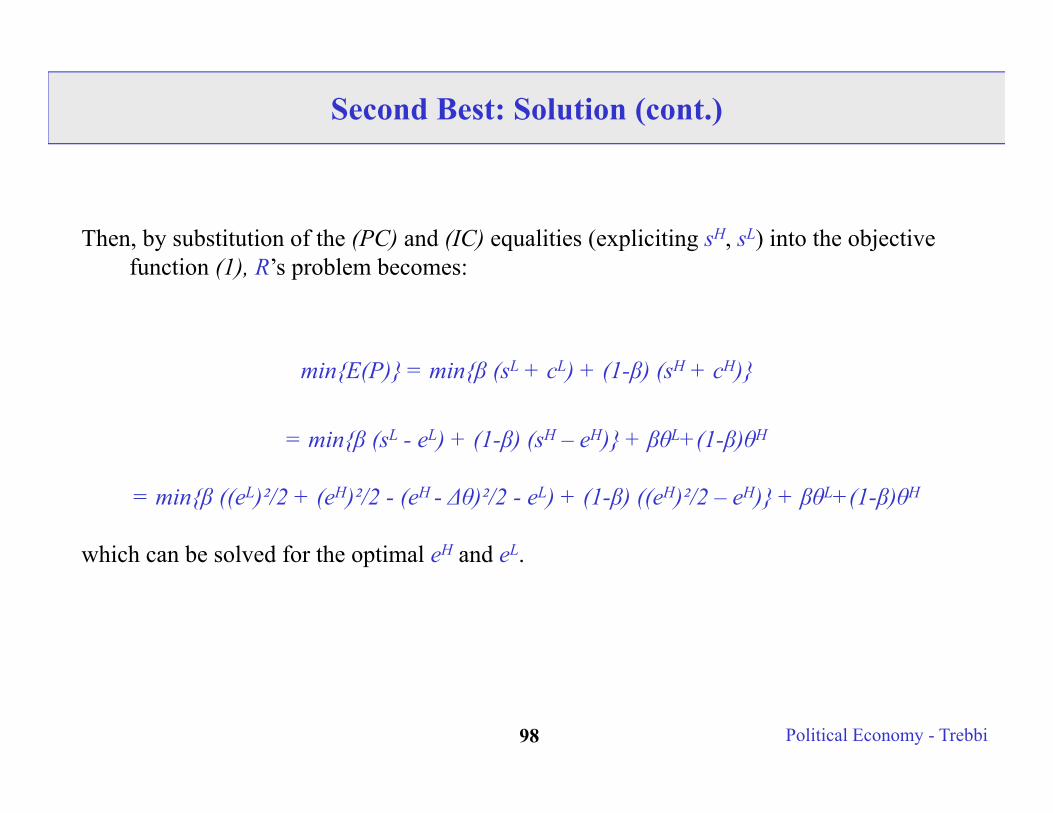

Then, by substitution of the (PC) and (IC) equalities (expliciting sH, sL) into the objective function (1), R’s problem becomes:

min{E(P)} = min{β (sL + cL) + (1-β) (sH + cH)}

= min{β (sL - eL) + (1-β) (sH – eH)} + βθL+(1-β)θH

= min{β ((eL)²/2 + (eH)²/2 - (eH - Δθ)²/2 - eL) + (1-β) ((eH)²/2 – eH)} + βθL+(1-β)θH

which can be solved for the optimal eH and eL.

Second Best: Solution (cont.)

Political Economy - Trebbi99

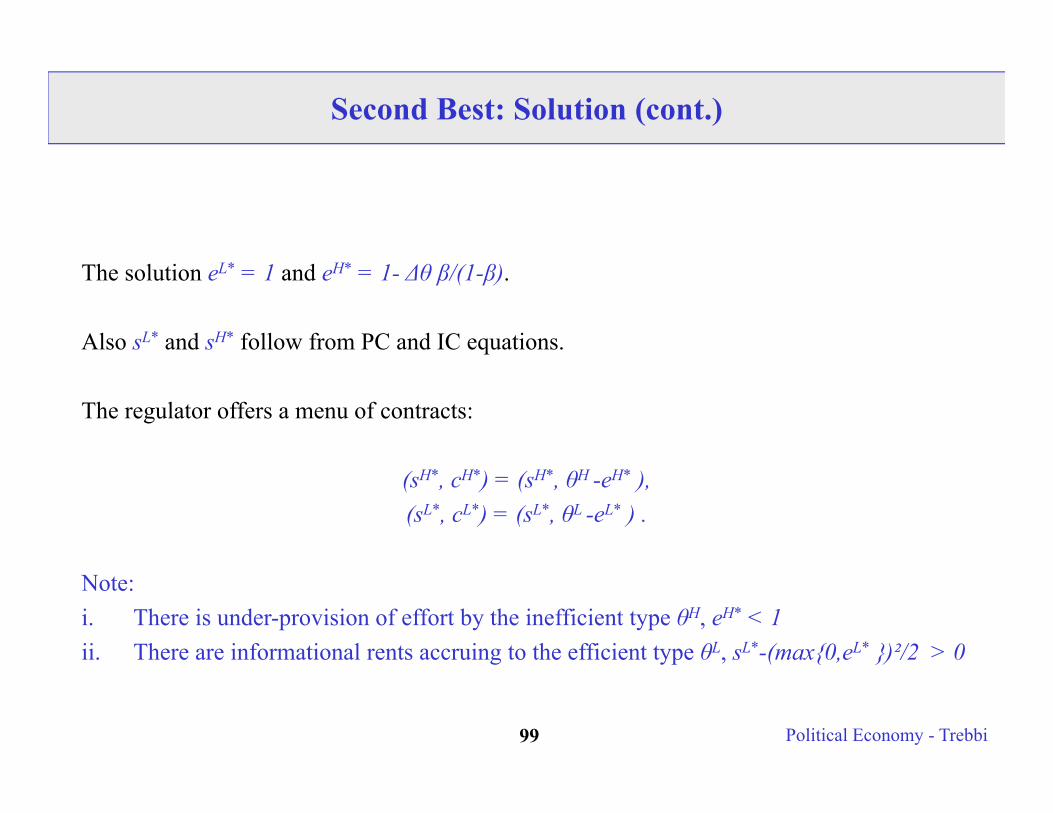

Second Best: Solution (cont.)

The solution eL* = 1 and eH* = 1- Δθ β/(1-β).

Also sL* and sH* follow from PC and IC equations.

The regulator offers a menu of contracts:

(sH*, cH*) = (sH*, θH -eH* ), (sL*, cL*) = (sL*, θL -eL* ) .

Note: i. There is under-provision of effort by the inefficient type θH, eH* < 1ii. There are informational rents accruing to the efficient type θL, sL*-(max{0,eL* })²/2 > 0

Political Economy - Trebbi100

Second Best: Solution (cont.)

Intuition:

R needs to use low-powered incentives for the inefficient guy (θH) because if R were to push the θH types to exert the first best effort eH* =1 ( which is very high effort), I would also pay them more in the pertinent high-cost case cH. But then the incentives for the efficient guy θL of faking to be a high cost guy would be too high for R to control in terms of IC. So R settles for lower powered incentives for a monopolist of type θH

Political Economy - Trebbi101

2. Yardstick Competition and Information

Maintain asymmetric information about θ.

However, now let’s assume we have two producers with identical cost functions:

ci = θi – ei

where ei is the effort level by producer i and each firm has a specific cost parameter.

Political Economy - Trebbi102

Yardstick Competition (cont.)

Let us start from the simple case of idiosyncratic random realizations of cost parameters θi

and θj.

Distributions of θ are uncorrelated.

In this case R cannot learn anything from one firm about the cost structure of the other firm.

The problem remains the same as the one of the previous slides. Second best for both firms.

Political Economy - Trebbi103

Yardstick Competition (cont.)

Consider the opposite case of perfectly correlated realizations of cost parameters θi and θj.

Same θ for both firms. θi = θj = θ

In this case R can learn a lot from one firm about the cost structure of the other firm.

Consider the following contract for firm i reporting cost ci :

si = ψ(e*) – (ci - cj)= ψ(e*) – ((θ –ei) – (θ –ej)),

Notice how the subsidy depends on the costs of both firms.

Political Economy - Trebbi104

Yardstick Competition (cont.)

Relative performance evaluation will help.

To see how, notice that firm i will maximize si - ψ(ei) =

ψ(e*)– ((θ –ei) – (θ –ej)) – ψ(ei) = ψ(e*)+ ei – ej – ψ(ei)

So ei = e* = 1.

and firm j will do the same. Both firms will earn their reservation utility 0.

When yardstick competition can be used, optimal effort can be obtained as in first best, notwithstanding informational asymmetries.

Yardstick competition takes away the informational rents. Incentives to cheat go to zero.

Political Economy - Trebbi105

3. Regulated Prices: Setup

The choice of output and price is another important aspect of regulation.

A regulator R is concerned with protecting consumer’s welfare.

R is attempting to force a natural monopolist M to produce a certain good at the lowest price for taxpayers.

Problem: The regulator does not have specific information about M’s cost structure θ.

The project has a variable scale q. Total cost C of producing quantity q is given by:C = (θ – e)q

So now the marginal cost of producing the good isc = θ – e

Political Economy - Trebbi106

Regulated Prices: First Best

Define V(q) the social surplus generated by the production of output q. Assume it increasing and concave for simplicity.

R will want to increase output and keep payments low.

If costs are observable, R’s problem is the first-best problem:

min{P - V} = minq,e{s + C – V(q)} = minq,e{s + (θ – e)q – V(q)} (6)

Subject to the constraint of making M not suffer losses (Participation Constraint)

s - ψ(e) = s - (max{0,e})²/2 ≥ 0

Political Economy - Trebbi107

First Best Solution

The constraint of making M not suffer losses will hold with equality (no rents, R will try to minimize payments to M)

s - ψ(e) = 0

I will replace it in (6) and differentiate for q and e.

The first-best solution to R’s problem is given by the solution e*, q* of the two first order conditions:

q = ψ’(e) (7)θ – e = V’(q) (8)

which of course will be contingent on the realized state θ.

To get first-best prices I can plug q* into the inverse demand function p = P(q).

Political Economy - Trebbi108

Regulated Prices: Second Best

R’s problem when costs are unobservable is different:

min{E(P - V)} = min{β (sL + CL – V(qL)) + (1-β) (sH + CH – V(qH))}

subject to the participation constraints (make sure the firms wish to operate):

si - (max{0,ei})²/2 ≥ 0 for i=L,Hand the incentive constraints (make sure the firms wish to do the right thing):

sL - (max{0,eL})²/2 ≥ sH - (max{0,eH - Δθ})²/2

sH - (max{0,eH})²/2 ≥ sL - (max{0,eL + Δθ})²/2

Political Economy - Trebbi109

Second Best: Simplified Setup

R’s problem can be simplified by the arguments we used before to:

minqL,qH,eL,eH{E(P - V)} = min{β (sL + (θL – eL)qL – V(qL)) + (1-β) (sH + (θH – eH)qH – V(qH))}

subject to a binding participation constraint for the high-cost type:

sH = ψ(eH) (9)

and a binding incentive constraint for the low-cost type:

sL - ψ(eL) = sH - ψ(eH - Δθ) (10)

Political Economy - Trebbi110

Second Best: Solution

(9) and (10) can be replaced into the minimand to get the unconstrained problem:

min{β (ψ(eL) + ψ(eH) - ψ(eH - Δθ) + (θL – eL)qL – V(qL))+ (1-β) (ψ(eH) + (θH – eH)qH – V(qH))}

The second-best solution to R’s problem is given by the solution eH*, qH* eL*, qL* of the four first order conditions:

qL = ψ’(eL)

θL – eL = V’(qL)

qH = ψ’(eH) + (ψ’(eH) – ψ’(eH - Δθ))β/(1- β)

θH – eH = V’(qH)

Political Economy - Trebbi111

Second Best: Interpretation

Note:

i. Output and effort are the same as under full information for the efficient type θL. ii. There are informational rents accruing to the efficient type θL (PC is slack for the low-

cost type), sL*-(max{0,eL* })²/2 > 0iii. A low-powered incentive scheme is given to the inefficient type to limit the efficient

type’s rents. There is under-provision of effort by the inefficient type θH, eH* is lower than under full information.

iv. In second best we are going to have lower output and higher prices when costs are high relative to first best.

Political Economy - Trebbi112

Conclusions

The issues of antitrust and regulation have been investigated in the light of potential informational asymmetries.

Main empirical and institutional features.

We have seen models of the New Theory of Regulation & Informational models of Regulation and Procurement.

This is a particularly active area of policymaking right now (think about housing market or financial services regulation) and a fruitful avenue of research.