policy uncertainty and corporate debt...

TRANSCRIPT

1

Policy Uncertainty and Corporate Debt Maturity

Dung T.T. Tran

The Robert J. Manning School of Business,

University of Massachusetts Lowell,

1 University Avenue,

Lowell, MA 01854, United States.

Email: [email protected]

Tel.: +1 (857) 222 6154

Hieu V. Phan

The Robert J. Manning School of Business,

University of Massachusetts Lowell,

1 University Avenue,

Lowell, MA 01854, United States.

Email: [email protected]

Tel.: +1 (978) 934 2633

2

Policy Uncertainty and Corporate Debt Maturity

October 2017

Abstract

This study examines the relation between government economic policy uncertainty and

debt contracting of U.S. public firms. We find that policy uncertainty is negatively related to

corporate debt maturity and positively related to the cost of debt and the number of restrictive

debt covenants. These relations are driven by firms with non-investment grade ratings or no

ratings, indicating that external creditors are concerned about the borrowing firms’ payment

ability during the periods of high policy uncertainty, leading them to impose shorter term debt

with less favorable terms and charge higher risk premiums. Further analysis indicates that the

negative relation between policy uncertainty and corporate investments documented by previous

research is stronger for firms with poor credit ratings or no ratings. Overall, our evidence

suggests that policy uncertainty increases the refinancing risk and the cost of debt for firms with

poor credit ratings, leading to their investment delays.

3

1. Introduction

Government economic policies can alter the business environment in which firms operate.

The process of debating and adopting new policies usually takes considerable time and the

outcomes could be unpredictable. Policy uncertainty is harmful for firm operation. Previous

studies document that policy uncertainty adversely affects corporate investments (Gulen and Ion,

2016) and costs of capital (Gilchrist, Sim, and Zakrajsek, 2011; Pastor and Veronesi, 2012). While

the structure of debt maturity, i.e., the use of short-term versus long-term debt, is an important

factor when considering a firm’s financial policy, no previous studies have examined the relation

between policy uncertainty and corporate debt maturity.

In this study, we examine the relation between policy uncertainty and corporate debt

maturity structure of U.S. firms. We present two opposing views about the relation between policy

uncertainty and corporate debt maturity. The supply-side hypothesis is developed based on the

willingness of suppliers of capital to favor lending short-term over long-term when policy

uncertainty is high. Because creditors are exposed to the borrowers’ higher default risks associated

with long-term debt, they can more easily exercise monitoring when lending in short-term (Stulz,

2000; Rajan and Winton, 1995). Alternatively, the demand-side hypothesis is based on the need of

firms to reduce the refinancing risks associated with short-term debt by increasing long-term

borrowing. As short-term debt exposes firms to higher refinancing needs, and thus, higher liquidity

risk (Diamond, 1991; Guedes and Opler, 1996; Custódio et al., 2013), firms should be more

reluctant to borrow in short-term amid high policy uncertainty.

We employ the monthly policy uncertainty index developed by Baker, Bloom, and Davis

(2016; hereinafter labeled BBD index) and construct the annual policy uncertainty measure using

the equal-weighted average of the BBD index of the last six months of the year for analysis. The

4

BBD index comprises of three components: the frequency of news media references to economic

policy uncertainty, the number of federal tax code provisions set to expire in future years, and the

extent of forecaster disagreement over future inflation and federal government purchases. We use

new bond issues data from SDC Platinum to construct our primary variable of debt maturity. The

sample includes 6,433 firm-year observations of 1,051 unique firms over the period 1985-2015.

To test our hypotheses, we first regress the maturity of new debt issue sample on the annual

policy uncertainty measure. We find robust evidence of a negative relationship between policy

uncertainty and debt maturity. The effect of policy uncertainty on debt maturity is also

economically important. Moreover, our finding is consistent with the supply-side explanation but

inconsistent with the demand-side explanation. In particular, firms borrow shorter term debt amid

high policy uncertainty because creditors are not willing to lend long-term debt.

To gain further insight into the relation between policy uncertainty and corporate debt

maturity, we split the samples into two subgroups with investment grade ratings or poor ratings

based on S&P credit ratings or Moody credit ratings, then we compare the differences between the

effects of policy uncertainty on debt maturity structure of the subsample firms. We find that the

negative relation between policy uncertainty and debt maturity structure is more pronounced for

firms with lower credit ratings or without credit ratings, which suggests that financially constrained

firms borrow shorter term debt because creditors might be concerned about these firms’ payment

ability amid high policy uncertainty, leading to their imposition of short-term debt.

To ensure the robustness of our results, we repeat the analysis using different ways to

construct the policy uncertainty measure, such as using the equal-weighted BBD index over the

last three months or twelve months or the value-weighted index over the last three months, six

months, or twelve months of a given year. Our findings are qualitatively unchanged. We also

5

perform analysis with the news-based component of the policy uncertainty index and find that this

component has stronger effects on the maturity of new debt issues than the overall BBD index.

We further conduct similar analyses using alternative measures of short-term debt based on

balance sheet data obtained from Compustat but our findings persist.

We investigate the relation between policy uncertainty and the number of restrictive debt

covenants made to U.S. borrowing firms using the private loan data obtained from the Thomson

Reuter LPC’s Dealscan database. Our loan covenant data include 14,913 firm-year observations

of 4,970 unique firms from 1988 to 2012. Our results indicate that the number of debt covenants

is positively related to policy uncertainty, suggesting less favorable loan terms by banks during

periods of high policy uncertainty. Additional subgroup analysis indicates that the relation between

policy uncertainty and debt covenants is more pronounced for financially constrained firms, i.e.,

those with poor credit ratings or no ratings. Collectively, our evidence suggests that financially

constrained firms are faced with not only difficulty in borrowing long term debt but also stricter

debt terms amid high policy uncertainty.

It is possible, although less likely, that firms with poor credit ratings choose to borrow

short-term debt rather being imposed upon by external creditors during periods of high policy

uncertainty. To explore this possibility, we perform a complementary analysis of the relation

between policy uncertainty and the cost of debt using the generalized method of moments (GMM)

method. The results indicate that yield spread is positively related to policy uncertainty and this

relation is driven by borrowing firms with non-investment grade ratings. Moreover, our estimation

results also indicate a negative relation between the yield spread and bond maturity for non-

investment grade bonds, implying that it is less costly for firms with poor credit ratings to borrow

long-term debt. We note that this finding is consistent with the theoretical prediction of a

6

downward-sloping credit yield curve for risky bonds by Merton (1974), Jarrow, Lando, and

Turnbull (1997), and Longstaff and Schwartz (1995), and the empirical findings of Sarig and

Warga (1989) and Fons (1994). Taken together, our evidence supports the supply side hypothesis

that creditors are concerned about the adverse effects of policy uncertainty on the payment ability

of firms with poor credit ratings, leading them to lend shorter term debt and charge higher risk

premiums.

To the extent that policy uncertainty makes it more difficult for firms, particularly

financially constrained ones, to raise long-term debt financing, it is expected to adversely affect

the level of investment of these firms (Graham and Harvey, 2001; Almeida, Campello, Laranjeira,

and Weisbenner, 2012). We further examine the link between the financing and investment effects

of policy uncertainty. We first replicate the baseline regressions of Gulen and Ion (2016). Our

results confirm the negative effect of policy uncertainty on corporate investment measured by the

ratio of capital expenditures to book value of assets, indicating that high policy uncertainty results

in investment delays. Moreover, when we examine the investment effect of policy uncertainty for

two subgroups of firms sorted on credit ratings, we find that this effect is significantly stronger for

firms with poor credit ratings. This evidence suggests financing, particularly debt maturity

structure, as a possible channel through which policy uncertainty negatively affects corporate

investments.

Our research contributes to the literature in three ways. First, to the best of our knowledge,

this is the first study that establishes the link between policy uncertainty and corporate debt

maturity structure. We show that policy uncertainty is an important determinant of corporate debt

maturity, an integrated component of corporate financial policy. Second, to the extent that

corporate debt maturity structure affects corporate investments, our finding that financially

7

constrained firms are screened out of the long end of the maturity spectrum during the high policy

uncertainty periods offers a plausible explanation for the negative real effects of policy uncertainty

documented by previous research. Finally, our paper provides important implications for policy

makers, corporate managers, and investors given the tremendous policy uncertainty they are

facing.

The rest of our paper proceeds as follows. Section 2 presents literature review and develops

our testable hypotheses. Section 3 provides data, sample, and variable description. Section 4

presents empirical results and discussions. Section 5 presents robustness checks and Section 6

concludes the paper.

2. Literature Review and Hypothesis Development

The economic consequences of policy uncertainty has recently been a topic of increased

interest. One focus of the debate in prior research is the effect of policy uncertainty on corporate

investments. Bernanke (1983) and Rodrik (1991) find that, when investment is irreversible,

uncertainty increases the value of waiting for new information about the profitability of the

projects. Julio and Yook (2012) examine the cycles of firm-level corporate investment associated

with the timing of national elections and report that political uncertainty negatively affects

corporate investment expenditures. Gulen and Ion (2016) document a negative relation between

policy-related uncertainty and both firm- and industry-level investments. Jens (2017) studies the

link between political uncertainty and firm investment using U.S. gubernatorial election as an

exogenous variation in uncertainty and find evidence of investment declines before elections.

Nguyen and Phan (2017) investigate how policy uncertainty influences mergers and acquisitions

8

(M&As) and find a negative relation between policy uncertainty and firm acquisitiveness as well

as a positive relation between policy uncertainty and the completion time of M&A deals.

Previous studies report that policy uncertainty affects corporate financing decisions.

Uncertainty is positively related to the costs of external financing by increasing the risk of default

(Gilchrist, Sim, and Zakrajsek, 2011) and increasing risk premia required by investors (Pástor and

Veronesi, 2012; Kelly, Pástor, and Veronesi, 2016). Francis, Hasan, and Zhu (2013) report a ten

basis point increase in U.S. bank loan spread as a result of a one standard deviation increase in

political uncertainty. The increased cost of external financing can help explain the negative relation

between uncertainty and investment. Cao, Duan, and Uysal (2013) investigate the role of political

uncertainty in firms’ intertemporal capital structure and find a negative relation between political

uncertainty and leverage ratios. They also show that when firms are uncertain about the general

political conditions, they prefer to stay underleveraged for extended periods, suggesting that firms

are more concerned about maintaining financial flexibility during periods of increased political

uncertainty. These authors also report that firms that have access to public debt markets, i.e.,

having bond ratings, are less affected by changes in political uncertainty in their capital structure

decisions. This finding supports the role of having public debt market access in increasing firms’

flexibility in borrowing (Cao et al., 2013). Colak, Flannery, and Öztekin (2014) examine how

uncertainty influences transaction costs and leverage adjustment and find that political uncertainty

increases financial intermediation costs for both new equity issuances and new debt issuances,

which slows down the leverage adjustment process. Moreover, higher adjustment costs due to

political uncertainty also reduce the frequency and volume of new capital issues to alter the capital

structure. Jens (2017) finds that firms delay debt and equity issuances that are tied to investments

during higher political uncertainty. Colak, Durnev, and Qian (2017) study the effects of political

9

uncertainty on initial public offering and document fewer IPOs at states that are scheduled to have

an election, suggesting that when facing high political uncertainty, firms tend to delay their

financing activities. They also find political uncertainty leads to higher cost of capital for firms,

consistent with the earlier argument of Pástor and Veronesi (2012, 2013). The foregoing discussion

suggests that policy uncertainty can affect corporate financing decisions through both the demand

and supply channels.

The maturity structure of corporate debt, i.e., the use of short-term versus long-term debt,

is an integrated part of a firm’s financial policy. Under the corporate governance perspective, short-

term debt can be an effective tool to reduce managers’ incentives to increase risk (Barnea, Haugen,

and Senbet, 1980), mitigate the agency problem of free cash flows (Jensen, 1986), reduce agency

costs associated with underinvestment or asset substitution (Myers, 1977; Jensen and Meckling,

1976; Leland and Toft, 1996), provide a powerful monitoring tool for creditors (Stulz, 2000), and

provide flexibility to creditors in monitoring managers (Rajan and Winton, 1995). From the

investment perspective, short-term debt allows firms to avoid underinvestment induced by the debt

overhang problems (Myers, 1977; Diamond and He, 2014), and increase financial flexibility by

allowing firms to preserve debt capacity for investment in future growth opportunities (Graham

and Harvey, 2001). However, from the liquidity perspective, short-term debt financing exposes

firms to higher liquidity risk because it requires more frequent renegotiations, exposing the

borrowing firms to the risk of insolvency if they fail to honor their debt payment obligations

(Jensen, 1986).

The choice of debt maturity can be driven by firm characteristics. Barclay and Smith

(1995), among others, find that larger firms or firms with fewer growth options use more long-

term debt. Analyzing the trade-off between the borrower’s preference for short-term debt due to

10

an expectation for future credit rating improvement and liquidity risk, Diamond (1991) argues

theoretically that firms with high credit ratings prefer to borrow short-term debt, firms with

somewhat lower ratings prefer to use long-term debt, and firms with lowest ratings can only borrow

short-term debt. These findings suggest that firms’ choice of debt maturity signals private

information to outside investors (Diamond, 1991; Barclay and Smith, 1995).

Furthermore, debt maturity structure has been shown to influence investment decisions.

Aivazian, Ge, and Qiu (2005) documents a negative relation between the percentage of long-term

debt in total debt and investment for firms with high growth opportunities. Almeida et al. (2011)

report that the structure of debt maturity had important real effects for industrial firms during the

2007-2008 financial crisis. In particular, they find that firms with a significant portion of long-

term debt maturing right after the third quarter of 2007 experience a drop in their investment level.

We develop two opposing views regarding the potential effects of policy uncertainty on

debt maturity structure: the supply-side hypothesis and the demand-side hypothesis.

The Demand-side Hypothesis

Theoretical explanations for debt maturity, such as the agency costs, signaling and liquidity

risk, and asymmetric information, largely originate from the demand-side factors. Short-term debt

helps reduce agency costs of debt (Myers, 1977) and asset substitution problems (Jensen and

Mecklings, 1976), serves as a useful mechanism to discipline managers (Brockman, Martin, and

Unlu, 2010), and signals private information to outside investors (Flannery, 1986; Diamond, 1991;

Barclay and Smith, 1995).

The demand-side explanations for how policy uncertainty affects debt maturity structure

relate to the firms’ willingness and ability to borrow rather than the creditors’ willingness and

ability to lend. Liquidity risk is one of the disadvantages of short-term debt financing as suggested

11

by Diamond (1991), Guedes and Opler (1996), and Custódio et al. (2013). Relying on short-term

debt financing means more frequent refinancing needed. Short-term debt creates liquidity risk

when the borrowing firm is unable to refinance, prompting the lenders to liquidate firm assets to

recover their loans. Thus, firms that use short-term debt tend to be more negatively affected by

credit supply shocks and face more financial constraints (Custódio et al., 2013). Therefore, during

the periods of increased policy uncertainty when cash flow volatility increases and it is more

challenging to refinance short-term loans, firms are more likely to reduce short-term debt and

increase long-term debt to mitigate the refinancing risk. A recent study by Alfaro, Bloom, and Lin

(2016) builds a model that shows a negative relation between uncertainty shocks and short-term

debt and suggest that firms reduce short-term debt when uncertainty is high. Following the

foregoing discussions, we state our demand side hypothesis as follows:

H1: Corporate debt maturity is positively related to policy uncertainty.

The Supply-side Hypothesis

Custódio, Ferreira, and Laurean (2013) report a secular decrease in corporate debt maturity

of U.S. firms during the period 1976-2008, which was mainly caused by firms with higher

information asymmetry and newly listed firms in the 1980s and 1990s. They argue that it is the

supply-side factors, rather than the demand-side factors, which drive the documented trend of

corporate debt maturity. In particular, these authors do not find evidence consistent with the

explanations of the agency costs of debt, maturity matching, taxes, signaling or liquidity risk, or

macroeconomic factors for debt maturity. However, they find that credit supply conditions, i.e.,

investor demand, have significant influence on the evolution of debt maturity. Other earlier studies

also find evidence consistent with the supply-side effects on debt financing. Faulkender and

Petersen (2006) show that firms with access to external debt markets (i.e., having credit ratings)

12

can raise more debt. Leary (2009) studies the change in bank credit supply caused by the 1961

emergence of the market for certificates of deposit and the 1966 credit crunch and reports that

following an expansion (contraction) in the availability of bank loans, bank-dependent firms

increase (decrease) their leverage ratios significantly compared to firms with bond market access.

Lemmon and Roberts (2010) take into account the supply shock in the junk bond market caused

by the collapse of Drexel Burnham Lambert and the subsequent regulatory changes in 1989 and

document that limited substitution to bank debt and alternative sources of capital makes net

investment to decline one-for-one with the reduction in net debt issuance. They also emphasize

that even large firms with access to public credit markets are vulnerable to the volatility in the

capital supply.

We argue that creditors may prefer to lend shorter term rather than longer term debt during

the periods of high policy uncertainty for the following reasons. Policy uncertainty can increase

the borrowing firms’ operating risk, leading to more volatile future cash flows that adversely affect

their debt payment ability. Because short-term debt helps creditors to better monitor firm

management (Stulz, 2000) and adds more flexibility to creditors in monitoring managers (Rajan

and Winton, 1995), lending short-term debt is less risky for creditors, particularly during the

periods of high policy uncertainty. In addition, long-term debt typically exposes creditors to higher

default risks than short-term debt does. Therefore, creditors may be less willing to lend long-term

debt when the economic conditions are highly uncertain. Also, the normal upward-sloping yield

curve in the U.S. debt market indicates that bond yields rise as maturity increases. The upward-

sloping yield curve reflects creditor expectations for increasing inflation in the future. To account

for future inflation, creditors demand higher risk premium for debt with longer maturity,

suggesting higher debt cost for longer term debt. Even though borrowing long-term debt reduces

13

the borrowing firms’ refinancing and default risks, the creditors’ unwillingness to supply long-

term debt amid high policy uncertainty may leave the borrowing firms with only the short-term

debt choice. Following these discussions, we state our supply side hypothesis as follows:

H2: Corporate debt maturity is negatively related to policy uncertainty.

3. Data and Sample

Previous studies largely rely on short-term debt ratios calculated from balance sheet data,

which may include the short-term portion of long-term debt that will soon mature, as a proxy for

debt maturity. Using balance sheet short-term debt ratios might raise a concern that short-term debt

ratios are based on some arbitrary cutoff points. In addition, since firms do not recapitalize

frequently (Leary and Roberts, 2005), their leverage ratios and debt maturity could be the result of

their past financing decisions. Thus, to avoid the potential drawback from using balance sheet data,

we focus our analysis on the relation between policy uncertainty and debt maturity structure using

the new debt issue data; however, we also use the debt maturity measures from balance sheet data

to verify the robustness of our results.

We obtain the sample of non-convertible and private new debt issues annually from the

Securities Data Company (SDC) and exclude all asset-backed, mortgaged-backed, and federal

credit agency issues. The annual firm-level accounting data and S&P long-term debt ratings are

obtained from the COMPUSTAT database. The daily and monthly stock returns are obtained from

CRSP database. Following prior literature, we exclude firms from the utility and financial

industries with the four-digit SIC codes from 4,900-4,999 and from 6,000-6,999 respectively

because these firms are highly regulated.

14

We use the U.S. monthly policy uncertainty index developed by Baker, Bloom, and Davis

(2016) as a measure of policy uncertainty in our analysis. The sample period is from January 1985

to December 2015 during which the data on the BBD index are available. The unconsolidated new

debt issues sample consists of 6,433 deals belonging to 1,051 unique firms over the sample period.

Because firms may issue multiple tranches of debt in a given year, we construct two alternative

consolidated samples by aggregating issue-level data to a firm-level data. The equal-weighted

consolidated sample contains 3,474 firm-year observations. The issue size-weighted sample has

3,466 firm-year observations. In addition, the balance sheet sample consists of 77,832 firm-year

observations belonging to 9,783 unique firms.

Measuring Policy Uncertainty

Previous research uses different measures of policy uncertainty which can be classified

into election related and non-election related categories. The election-based policy uncertainty

measures reflect the election-driven uncertainty prevalent before the national elections

(Boutchokova, Doshi, Durnev, and Molchanov, 2012; Durnev, 2012; Julio and Yook, 2012; Colak

et al., 2014). The non-election-based measures capture the government ability to implement its

promised policies (Colak et al., 2014). In addition, recent literature widely adopts the news-based

non-election policy uncertainty index of Baker, Bloom, and Davis (2016), which captures the

policy uncertainty reported in the news media (Cao et al., 2013; Colak et al., 2014; Gulen and Ion,

2016).

To assess the effect of policy uncertainty on the maturity structure of corporate debt, we

use the policy uncertainty index developed by Baker et al. (2016). The BBD index is constructed

as a weighted average of three components that reflect the frequency of news media references to

economic policy uncertainty, the number of federal tax code provisions set to expire in future

15

years, and the extent of forecaster disagreement over future inflation and federal government

purchases.

The first component is a count of search results in 10 large newspapers containing the

following triple: “uncertainty” or “uncertain”; “economic” or “economy”; and “congress”,

“legislation”, “white house”, “regulation”, “federal reserve”, or “deficit” (including variants like

“uncertainties”, “regulatory” or “the Fed”). To meet the criteria, an article must contain terms in

all above three categories. Baker et al. (2016) use 10 leading newspapers: USA Today, Miami

Herald, Chicago Tribune, Washington Post, Los Angeles Times, Boston Globe, San Francisco

Chronicle, Dallas Morning News, New York Times, and Wall Street Journal and search the digital

archives of each paper from January 1985 to get the monthly count of policy uncertainty articles.

The total number of counted articles in each newspaper in each month is normalized by the total

number of articles in that newspaper to adjust for the changing volume of news throughout time.

The second component of the index relates to uncertainty about expiration of tax code

provisions in the future. Based on reports by the Joint Committee on Taxation (JCT), Baker et al.

(2016) get the sum of the discounted number of tax code expirations to obtain an index value for

each January and hold it constant during the calendar year.

The third component of the index captures the uncertainty related to monetary policy and

government spending, using data from the Federal Reserve Bank of Philadelphia’s Survey of

Professional Forecasters. This component measures the forecast dispersion for the CPI and for

purchases of goods and services by state, local, and the federal governments. The dispersion

measures include the interquartile range of each set of inflation rate forecasts in each quarter, and

the ratio of nominal federal purchases to nominal GDP, which is ratio of the interquartile range of

four-quarter-ahead forecasts by the median four-quarter-ahead forecast multiplying by a 5-year

16

backward-looking moving average. The values of the forecast disagreement measures are held

constant within each calendar quarter.

The above three components weights are 1/2, 1/6, 1/3, respectively, in the overall BBD

index. In our regressions, we construct the annual policy uncertainty index of year t as the natural

logarithm of the equal-weighted average of the monthly BBD index of the last three, six, or twelve

months of the year, denoted by PU3, PU6, and PU12. In addition, we compute value-weighted

averages of the index in the last three months, six months, and twelve months of year t, denoted

by PU3W, PU6W, and PU12W, and give more weights to the more recent month. In addition to

the overall index, we examine the news-based component of the BBD policy uncertainty index

separately and construct the variables in a similar manner. To address potential endogeneity

concern, we lag the policy uncertainty measures by one period in our baseline analysis.

Measuring Debt Maturity Structure

We measure the maturity of new debt issues, denoted by Bond Maturity, as the natural

logarithm of the years to maturity of new debt issues in the unconsolidated sample. In the first

consolidated sample, we use the equal-weighted average maturity of multiple debt issues as the

proxy for debt maturity. In the second consolidated sample, we use the issue size-weighted average

maturity of multiple debt issues as the proxy for debt maturity, in which the consolidated maturity

is computed as the weighted average of the total proceeds of multiple debt issues by a firm in a

given year.

To measure the debt maturity of the balance sheet sample, we follow Custódio et al. (2013),

Brockman, Martin, and Unlu (2010) and Dang and Phan (2016) in using the proportions of a

company’s total debt that mature within one, two, three, four, or five years or less, denoted by ST1,

ST2, ST3, ST4, and ST5, respectively, as measures of short-term debt. We also include the ratio of

17

debt in current liabilities, but exclude the current portion of long-term debt, to total debt, denoted

by STNP, as an alternative measure of short-term debt. Total debt is calculated as the sum of debt

in current liabilities and long-term debt.

Control Variables

Following the debt maturity literature, we control for firm characteristics in our debt

maturity model, which include firm size (Scherr and Hulburt, 2001; Guedes and Opler, 1996), the

square of firm size, market leverage, asset maturity, managerial ownership, market-to-book ratio

(Barclay and Smith, 1995), term structure of interest rates, abnormal earnings, asset return

standard deviations or asset volatility, z-score dummy for firms with a high Altman (1977) Z-score,

and rating dummy for firms with S&P credit ratings (Brockman et al., 2010). The Appendix

provides detailed description of the control variables.

3.3. Descriptive Statistics

Table 1 reports the summary statistics of our new debt issues sample. We winsorize all

variables at the 1st and 99th percentiles to reduce the effects of outliers that can bias our results.

The average maturity of new debt issues is 12.07 years. Our sample firms have leverage, asset

maturity, market-to-book, abnormal earnings, asset volatility, and R&D comparable to those in

previous debt maturity studies, such as Brockman et al. (2010) and Dang and Phan (2016), but

larger firm sizes.

[Insert Table 1 about here]

We also generate the descriptive statistics of the variables in the balance sheet sample.

Similar to Brockman et al. (2010), we set all observations of short-term debt ratios that exceed one

to equal one, and set all negative observations of short-term debt ratios to equal zero. The proxy

18

of short-term debt, ST3, has a mean value of 54.8%, which is higher than the mean value of 40%

reported by Brockman et al. (2010), probably due to different sample periods (the descriptive

statistics for the balance sheet sample are not reported for brevity but are available from the

authors).

Figure 1 plots the BBD index measured as the natural logarithm of the equal-weighted

average of the monthly BBD index of the last six months of the year with the equal-weighted

average years to maturity of new debt issues over the sample period 1985-2015. The graph shows

the opposite trends of debt maturity and policy uncertainty as the average years to maturity of new

debt issues increase when the BBD index decreases.

4. Empirical Models, Results, and Discussions

4.1. Policy Uncertainty and Debt Maturity – Baseline Regressions

We begin our analysis by examining the relation between policy uncertainty and the

maturity of the new debt issues while controlling for factors shown to explain debt maturity in

previous studies. Our baseline regression model is as follows:

Bond Maturity i,t = αt + ß PUt-1 + δ Xi, t-1 + ɛi,t (1)

The dependent variable is the natural logarithm of the years to maturity of new debt issues

in the unconsolidated sample. The test variable is the natural logarithm of the average monthly

BBD index over the last six months of a given year. Xi,t-1 is a vector of firm-level control variables.

We control for industry fixed effects by including industry dummies (using two-digit SIC codes).

We control for issuer type fixed effects by adding issuer type dummies that equal to one for R144D

issue and zero otherwise (Brockman et al., 2010), and issue type fixed effects by including issue

type dummies that equal to one for investment grade bonds, and zero otherwise. We note that,

19

since policy uncertainty data are a time-series, which is the same for all firms in a given year, we

do not control for year fixed effects to preserve the explanatory power of policy uncertainty.

[Insert Table 2 about here]

The debt maturity regression results reported in Panel A of Table 2 show that the

coefficients on policy uncertainty are all negative, ranging from -0.094 to -0.07, and statistically

significant at the 1% and 5% levels in all specifications, suggesting that policy uncertainty is

negatively related to debt maturity. The coefficients are economically significant: using the results

reported in column 5 for calculation, we find that a one standard deviation increase in BBD index

is associated with 1.026 years decrease in debt maturity. These results provide preliminary support

for the supply side hypothesis that creditors lend shorter term debt amid high policy uncertainty.

The results of other control variables are generally consistent with those reported in the

literature (e.g., Johnson, 2003; Brockman et al., 2010). For example, firm size is negatively related

to debt maturity in our sample, but square of firm size has a stronger positive relation with maturity,

suggesting a non-monotonic relation between size and maturity of bonds (Diamond, 1991). As the

underinvestment hypothesis argues that firms match the maturity of assets and liabilities, we

observe a positive relation between asset maturity and debt maturity in our sample. The results

also show that market-to-book is negatively related to debt maturity, consistent with Myers’ (1977)

prediction that firms with greater growth opportunities face higher underinvestment problems so

they tend to use more short-term debt.

We conduct several robustness checks for our baseline results. Panel B of Table 2 reports

the results of the firm-level debt maturity regressions. The coefficients on policy uncertainty are

statistically and economically significant across model specifications for both equal-weighted and

20

issue size-weighted maturities. This evidence indicates that our results are robust to firm-level

measures of debt maturity.

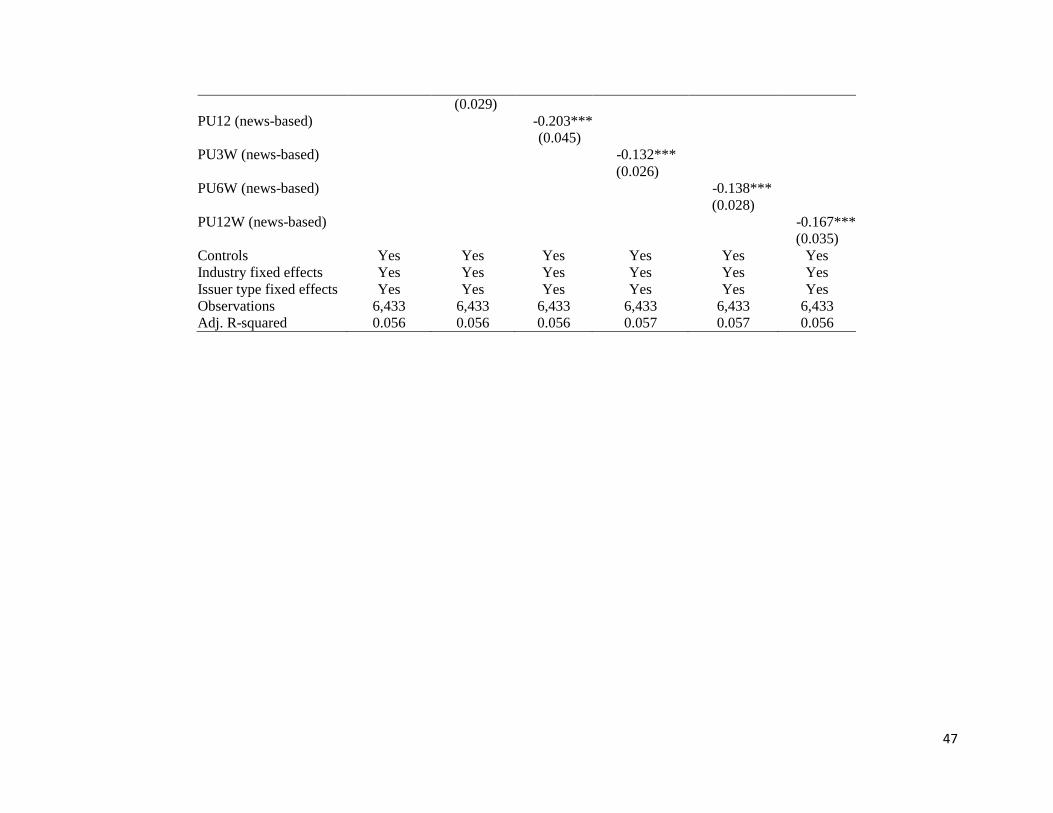

We further try alternative measures of policy uncertainty. In panel A of Table 3, we

substitute the six-month policy uncertainty with three-month, twelve-month equal-weighted

average BBD index, or the three-month, six-month, and twelve-month value-weighted average

BBD index in the regressions with industry and issuer type fixed effects. The results are

qualitatively similar. In panel B of Table 3, we perform a similar analysis using the news-based

component of the BBD index. The direction of the relation between news-based policy uncertainty

and debt maturity is in line with our results using the overall policy uncertainty index.

[Insert Table 3 about here]

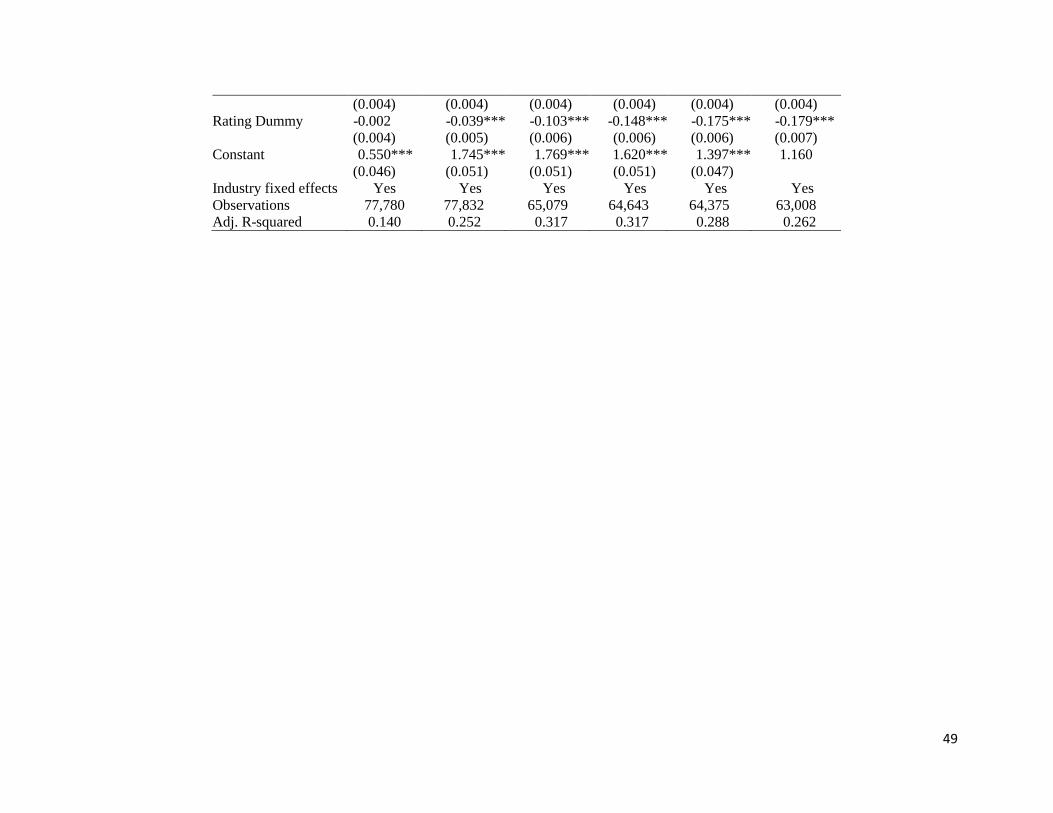

We further investigate the robustness of our results using the balance sheet sample and

report the results in Table 4. The dependent variable is the ratio of notes payable and short-term

debt maturing in one, two, three, four, or five years or less to total debt. The test variable is the

lagged policy uncertainty index measured as the natural logarithm of the equal-weighted average

of the BBD index in the last six months of a given year. We use the same set of control variables

as in our baseline regressions. We find a positive and statistically significant relation between most

of the alternative measures of short-term debt and policy uncertainty, which lends additional

support for a negative relation between debt maturity and policy uncertainty. While we do not

observe significant results for ST2 and ST3, it is noted that using short-term debt ratios calculated

from the balance sheet may bias the analysis results due to arbitrary cutoff points and these ratios

may simply reflect historical financing decisions.

[Insert Table 4 about here]

21

In summary, based on both new debt issues and balance sheet data, we find consistent

evidence of a negative relationship between policy uncertainty and the maturity structure of

corporate debt. This finding is consistent with the supply-side explanation but is inconsistent with

the demand-side hypothesis. Our results indicate that creditors may be reluctant to lend long-term

debt in uncertain policy environment, leading to borrowing firms’ using more short-term debt

financing.

4.2. Policy Uncertainty, Debt Maturity, and Financial Constraints

To assess how financial constraints moderate the relation between policy uncertainty and

debt maturity structure, we split the new debt issues sample into two subgroups based on credit

ratings (Faulkender and Petersen, 2006; Campello, Graham, and Harvey, 2010). The investment

grade subgroup includes issues with S&P ratings equal to or better than BBB- and a Moody ratings

equal to or better than Baa3. The high yield subgroup consists of issues having S&P ratings equal

to or lower than BB+ and a Moody rating equal to or lower than Ba1.1 Out of 6,433 new bond

issues from 1985 to 2015, 5,302 issues have investment grades and 1,131 are high yield bonds.

[Insert Table 5 about here]

Columns 1 and 2 of Table 5 report the regression results for the two subgroups. We find

that while policy uncertainty has a significant negative effect on debt maturity of issuers with non-

investment grade ratings, it does not affect the debt maturity of issuers with investment grade

ratings. This result suggests that the negative effect of policy uncertainty on debt maturity is driven

by firms with poor credit ratings, i.e., financially constrained firms. Columns 3 and 4 of Table 5

examine the two subgroups of firms in our balance sheet sample, using ST3 as the dependent

1 We use SDC Platinum’s issue types that are based on the same classification.

22

variable. We use S&P’s long-term debt ratings to classify firms into two subgroups of which the

investment grade subgroup includes issuers with S&P ratings equal to or better than BBB- and the

high yield subgroup includes firms with S&P ratings lower than BB+. We find even more revealing

results compared to the new debt issues sample. The coefficient on policy uncertainty is positive

and statistically significant for high yield firms, indicating that these firms increase short-term debt

amid high uncertainty. More importantly, the coefficient on policy uncertainty is negative and

statistically significant for investment grade firms, suggesting that these firms reduce (increase)

short-term (long-term) debt amid high policy uncertainty.

We interpret our results as evidence that creditors are less willing to lend long-term debt

when policy uncertainty is high because long-term debt is associated with higher default risks

while short-term debt allows creditors to monitor firm management more easily (Stulz, 2000). The

default risk is significantly higher for financially constrained firms that lack financial flexibility

and are in poor financial conditions. Creditors should be more concerned about the payment ability

of these firms amid high policy uncertainty, leading them to lend short-term debt. Thus, the lack

of access to long-term debt forces these firms to rely more on short-term debt financing amid high

policy uncertainty. On the other hand, creditors may still be willing to provide long-term debt

financing to financially unconstrained firms, i.e., firms with good credit ratings, when policy

uncertainty is high because their healthy financial condition can guarantee debt repayment. This

argument is consistent with Cao et al.’s (2013) finding that capital structure decisions of firms with

better access to public debt are less sensitive to changes in political uncertainty.

4.3. Policy Uncertainty, Financial Constraints, and Debt Covenants

23

We expect that during periods of high policy uncertainty, consistent with the supply side

hypothesis, lenders are not only less willing to lend in long-term but are also more likely to impose

more loan covenants. We use the number of covenants in commercial loan contracts reported in

the Thomson Reuters LPC’s Dealscan database to examine the effect of policy uncertainty on the

number of bank loan covenants made to U.S. firms. Our covenant data covers the period from

1988 to 2012. Our sample includes 14,913 firm-year observations of 4,970 unique firms. Our

covenant regression model has the following form:

NUMBER OF COVENANTSi,t = αt + ß PUt-1 + δ Xi,t-1 + ɛi,t (4)

The dependent variable is the sum of loan covenants imposed by lenders on each deal for

each year. The policy uncertainty variable is the natural logarithm of the six-month equal-weighted

average BBD index. We follow previous studies on loan covenants to include size, leverage,

market-to-book ratio, standard deviation of stock returns, asset tangibility, cash flow volatility,

and deal size as measured by the natural logarithm of deal amount as the control variables

(Demiroglu and James, 2010; Hertzel and Officer, 2012). We include loan purpose fixed effects

in all regressions to control for the cross-sectional variation in the purposes of getting the loans.

We also control for firm fixed effects in the second specification. To examine how the effect of

policy uncertainty on debt covenants differ between financially constrained firms and financially

unconstrained firms, we divide the sample into two subgroups based on S&P long-term credit

ratings. The investment grade subgroup includes issuers with S&P ratings equal to or better than

BBB- and the high yield subgroup includes firms with S&P ratings lower than BB+.

[Insert Table 6 about here]

Columns 1 and 2 of Table 6 present the results of the effect of policy uncertainty on debt

covenants for all firms in the sample. The results indicate that policy uncertainty is positively

24

related to debt covenants as the coefficients on policy uncertainty are positive (0.143 when

controlling for only loan purpose fixed effects, and 0.130 when controlling for both loan purposes

fixed effects and firm fixed effects) and statistically significant at the 1% level.

We then examine how the relation between policy uncertainty and debt covenants is

affected by financial constraints by dividing the debt covenants sample into two subgroups based

on credit ratings. Similarly to previous sections, the investment grade subgroup includes issues

with S&P ratings equal to or better than BBB- and the high yield subgroup consists of issues having

S&P ratings equal to or lower than BB+. There are 11,437 firm-year observations belonging to

financially constrained firms and 2,653 firm-year observations belonging to financially

unconstrained firms. The larger proportion of financially constrained firms suggests that firms with

poor credit ratings are more likely to rely on bank loans while firms with good credit ratings are

more likely to tap the public debt market with more favorable debt terms.

Columns 3 to 6 of Table 6 report the regression results for the two subgroups. We find that

the effect is stronger for firms with non-investment grade ratings or no ratings in both regression

specifications. The findings suggest that financially constrained firms are likely to face more

restrictive covenants on their loans amid high policy uncertainty, probably due to the lenders’

concern about these firms’ payment ability.

4.4. Policy Uncertainty, Debt Maturity, and Cost of Debt

Previous studies find that uncertainty increases cost of external financing due to increased

risk of default (Gilchrist et al., 2011) and increased equity risk premium (Pastor and Veronesi,

2012). In this section, we examine the relation between policy uncertainty and the costs of debt.

25

As policy uncertainty affects the maturity structure of corporate debt, we expect that it also has a

significant effect on debt costs. We estimate the following cost of debt model:

SPREADi,t = αt + ß LMATt + δ PUt-1 + γ Xi,t-1 + λ Zi,t +ɛi,t (3)

Since cost of debt and maturity of debt are likely to be endogenous and jointly determined,

we examine the relationship between cost of debt and policy uncertainty by running the GMM

regressions with instruments, similar to Brockman et al. (2010) and Dang and Phan (2016). 2

Motivated by these studies, we use firm size and the square of firm size as instruments for bond

maturity. We use the yield spread, measured as the daily difference between the corporate bond’s

yield-to-maturity and the linearly interpolated benchmark Treasury bond yield, as a measure for

the cost of debt. We calculate the benchmark Treasury yields based on 1-, 2-, 3-, 5-, 7-, 10-, 20-,

and 30-year constant maturity series. The test variable is the natural logarithm of the lagged equal-

weighted average six-month policy uncertainty index. Xi,t-1 is a vector of firm-level control

variables, which include profitability, leverage, and interest coverage. Zi,t is a vector of issue-level

and market-level control variables, including stock return volatility, bond rating average, coupon

rate, bond issue size, and yield curve slope. The detailed calculation of control variables are

presented in the Appendix. We also include industry and issuer types fixed effects by including

industry dummies and issuer type dummies in the regressions.

[Insert Table 7 about here]

The second-stage GMM regression results reported in column 1 of Table 7 indicate that

the cost of debt increases in policy uncertainty. We present the results for the new debt issue sample

as well as for two separate types of bond issues. While previous research contends that the positive

relation between uncertainty and cost of external financing is driven by the increase in the risk of

2 We also estimate the two-stage least squares regressions and the results are similar to the GMM regressions.

26

default (Gilchrist, Sim, and Zakrajsek, 2011) or the increase in the equity risk premium (Pastor

and Veronesi, 2011), our evidence suggests that the positive relation arises from the increase in

the use of shorter term debt financing, which becomes costlier when policy uncertainty increases.

However, this result only holds for the non-investment grade issues as policy uncertainty is

positive and statistically significant in column 3, but it is negative and statistically significant in

column 2. These results imply that for firms with non-investment ratings, borrowing shorter term

(longer term) debt is costlier (cheaper). Short-term debt also requires more frequent refinancing,

and thus, exposes the borrowing firms to higher liquidity risks. The results further indicate that

creditors might be concerned about these firms’ payment ability and liquidity risks amid high

policy uncertainty, leading them to charge higher risk premium during periods of high policy

uncertainty.

We note that the results in column 1 of Table 7 also indicate that bond maturity is

negatively related to yield spread, which is inconsistent with the normal yield curve of the U.S.

debt market. However, as we investigate the relation between policy uncertainty and cost of debt

for the two separate subgroups sorted on credit ratings, we find a positive relation between yield

spread and bond maturity for investment grade issues, which is consistent with a positive slope of

the yield curve, but a negative relation between yield spread and debt maturity for non-investment

grade issues. The latter finding is consistent with the theoretical arguments for a downward-sloping

credit yield curve for risky bonds (Merton, 1974; Jarrow, Lando, and Turnbull, 1997; Longstaff

and Schwartz, 1995) and previous empirical findings (Sarig and Warga, 1989; Fons, 1994).

4.5. Policy Uncertainty, Financial Constraints, and Corporate Investment

27

To complete our analysis, we investigate the financing-based explanation for Gulen and

Ion’s (2016) findings of a negative relationship between policy uncertainty and capital

investments. Specifically, we examine whether policy uncertainty has different effects on the

investments of financially constrained versus unconstrained firms. Using annual data, we estimate

the following regression model, which is similar to the baseline model in Gulen and Ion (2016):

INVESTMENTi,t = αt + ß PUt-1 + δ Xi,t-1 + λ Zi,t + ɛi,t (5)

The dependent variable is capital investment, calculated as capital expenditures divided by

the beginning of the period total assets. The policy uncertainty variable is the natural logarithm of

the six-month equal-weighted average BBD index. Similar to Gulen and Ion (2016), we control

for three firm-level financial variables (Xi,t-1) and two macroeconomic variables (Zi,t). Tobin’s q is

calculated as the ratio of the market value of equity plus the book value of assets minus book value

of equity plus deferred taxes, to the book value of assets. Cash Flow is measured by the ratio of

net operating cash-flow to lagged total assets. Sales Growth is the year-on-year change in annual

sales. GDP Growth is the year-on-year growth in real GDP. Election Indicator is a dummy variable

that equals one if a presidential election is hold in the current calendar year, and zero otherwise.

All specifications include firm fixed effects. We obtain accounting data from Compustat from

January 1985 to December 2015 period, and winsorized all variables at 1% and 99%. We examine

firms in both the new debt issue sample as well as in the Compustat universe. The debt issue

sample includes 3,423 firm-year observations, and the Compustat universe sample consists of

136,500 firm-year observations. We sort the sample firms into investment grade and high yield

subgroups.

[Insert Table 8 about here]

28

Table 8 presents the results of the relationship between capital investment and policy

uncertainty based on subgroup analysis for the new debt issue sample and the balance sheet sample.

The results indicate that policy uncertainty has more pronounced negative effect on investment of

firms with high yield debt ratings in both samples. This finding is consistent with the argument

that firms with investment grade ratings are financially unconstrained and have better access to

debt market, so they are more likely to have sufficient resources to support investments during

periods of high policy uncertainty. Thus, policy uncertainty has weaker effect on these firms’

investments. On the other hand, firms with non-investment grade ratings or no ratings, i.e.,

financially constrained firms, face greater difficulty in borrowing during the high policy

uncertainty periods. Even if financially constrained firms are successful in raising external debt

financing, they would be reluctant to use the shorter term debt that they can borrow during the

periods of high policy uncertainty to finance long-term investment projects due to the refinancing

risk, leading to more investment delays. This evidence suggests financing constraint, particularly

short-term debt financing, as a possible channel through which policy uncertainty adversely affects

corporate investments.

5. Robustness Checks

In addition to using alternative measures of debt maturity and policy uncertainty in Section

4.1, we conduct additional tests to further confirm the robustness of our results.

Quarterly data, length of the effect, and extreme policy uncertainty

We check for the robustness of our results by rerunning the short-term debt regressions

using quarterly balance sheet data. The quarterly balance sheet data provides only data for the

proportion of debt maturing in one year, but do not report data for the proportion of debt maturing

29

in two, three, four, or five years. We calculate the quarterly policy uncertainty index as the equal-

weighted average of the monthly policy uncertainty in a quarter. Using the similar regression

specifications as in Table 4 for quarterly data, we find that the coefficient on quarterly short-term

debt ratio is positive (0.033) and significant at the 1% level. This result indicates that our finding

of a negative relation between policy uncertainty and debt maturity is robust to quarterly data.

In the next analysis, we examine the evolution of the effect of policy uncertainty on debt

maturity structure by running 12 separate quarterly regressions that includes one of the lags 1-12

of quarterly policy uncertainty measures. We plot the coefficients of policy uncertainty in Figure

2. We find that the effect of policy uncertainty lasts up to three quarters, which is shorter than the

effect of policy uncertainty on firm investment documented by Gulen and Ion (2016) that persists

up to eight quarters. Firms are likely to raise financing first before they can commit to investment,

which could explain the timing gap between the effect of policy uncertainty on debt maturity

structure and investment.

Next, we investigate the effect of extreme policy uncertainty on debt maturity structure by

rerunning regressions with quarterly balance sheet data using a dummy variable for extreme policy

uncertainty. We define extreme policy uncertainty as one if the quarterly policy uncertainty index

belongs to the highest tercile and zero otherwise. We run 12 separate regressions using lags 1-12

of the extreme policy uncertainty dummy. Our unreported result indicates a positive and

statistically significant coefficient of extreme policy uncertainty and that the effect of extreme

policy uncertainty persists up to three periods, which is consistent with the result reported above.

Control for Investment Opportunities

Our results could be subject to an endogeneity concern due to the omitted variable problem.

The reason is that both policy uncertainty and debt maturity might be correlated with unobserved

30

investment opportunities. Therefore, we include proxies for investment opportunities as additional

controls in our analysis.3 The first proxy is the expected GDP growth generated using one-year-

ahead GDP forecasts from the Philadelphia Federal Reserve’s biannual Livingstone survey. We

compute the expected GDP growth as the percentage change between mean GDP forecast and the

current GDP level. The second proxy is the Michigan Consumer Confidence Index from the

University of Michigan to control for consumers’ expectations about future economic prospects.

The third proxy is the monthly Investor Sentiment Index from Baker and Wurgler (2007) to control

for expectations by equity-market participants. The results in Table 1A of the Internet Appendix

indicate that the effect of policy uncertainty on debt maturity is qualitatively unchanged,

confirming the robustness of our results.

Control for Economic Uncertainty

It is possible that policy uncertainty simply picks up the effects of general economic

uncertainty rather than the effect of policy-related uncertainty. To address this concern, we include

measures of macroeconomic uncertainty as suggested by Bloom (2009) as control variables. First,

we use the uncertainty about future economic growth obtained from the Livingstone survey

mentioned above, calculated every June and December as the coefficient of variation in GDP

forecasts obtained from the survey. The second variable is the uncertainty about future

profitability, proxied by the within-year cross-sectional standard deviation of firm-level profit

growth, as the year-on-year change in net profit divided by average sales. The third variable is the

uncertainty perceived by the equity markets, proxied by the monthly cross-sectional standard

deviation of stock returns and the VXO (implied volatility) index from the Chicago Board Options

Exchange. We include these variables in our baseline specifications in addition to the three proxies

3 Gulen and Ion (2016) also control for the forth variable, the Conference Board’s monthly Leading Economic Index

as a proxy for future GDP; however, we have not added this variable due to the availability of data at this time.

31

for investment opportunities variables above. The results reported in Table 1A in the Internet

Appendix indicate that our results continue to hold.

IV Regression

We further use instrumental variable (IV) regression to address potential endogenous

relation between policy uncertainty and debt financing. Similar to Gulen and Ion (2016), we use

partisan polarization in the U.S. House of Representatives and Senate as an instrument for policy

uncertainty. McCarty, Poole and Rosenthal (1997) develop the DW-NOMINATE scores to

measure a legislator’s ideological positions over time. We use the first dimension of the DW-

NOMINATE scores, which relates to the legislator’s positions on government intervention in the

economy, to calculate a polarization measure. The polarization measures are calculated separately

for the House of Representatives and Senate as the differences between the Republican and

Democratic party averages in the first dimension of the DW-NOMINATE scores. The polarization

variable can satisfy the conditions of an instrument for two reasons. First, it is correlated with the

policy uncertainty index. The higher the level of polarization in the House or Senate, the more

disagreement between politicians, the higher the level of uncertainty related to policy decisions,

holding everything else constant. Second, polarization is unlikely to be directly correlated with

debt financing.

To perform the instrument variable analysis, we cannot use the usual two-stage least

squares methodology because both policy uncertainty variable and the instrument are cross-

sectionally invariant. Instead, in the first stage, we run a time-series regression of the policy

uncertainty index on the instrument and control variables. Control variables are the same as those

in our baseline regressions. Then, we use the fitted values from this regression as a surrogate for

policy uncertainty in the baseline regressions.

32

[Insert Table 9 about here]

Columns 1 and 2 of Table 9 presents the first-stage and second-stage results of the debt

maturity IV regression. We find that the negative relationship between policy uncertainty and debt

maturity is virtually unchanged.

Canadian Policy Uncertainty

One might concern that the BBD index does not necessarily proxy for policy-related

uncertainty, but rather reflects non-policy economic uncertainty, which leads to potential

measurement error bias. Gulen and Ion (2016) argue that since the United States and Canadian

economies are tightly linked, the shocks that affect the general economic uncertainty in the U.S.

are likely to have an impact on the general economic uncertainty in Canada. To isolate the policy

uncertainty part of the BBD index, we follow a two-step regression approach. We first run a time-

series regression of the U.S. BBD index on the Canadian BBD index. The control variables in this

time-series regression include the cross-sectional average of the firm-level variables (Tobin’s q,

Cash flow, Sale Growth) used in the investment specifications in Section 4.4, economy-wide

average of the investment irreversibility and dependence on government spending variables used

in Gulen and Ion (2016), election year indication, real GDP growth, and the investment

opportunities variables used in Section 5.1. Then, we obtain the residuals from this regression,

which should represent only U.S. policy-related uncertainty. We use the residuals as a proxy for

U.S. policy uncertainty in our regressions. The results reported in column 3 of Table 9 indicate

that this new proxy for policy uncertainty is negatively related to debt maturity, which is consistent

with our earlier finding.

6. Conclusion

33

Using the policy uncertainty index by Baker, Bloom, and Davis (2016), our study examines

the relation between policy uncertainty and corporate debt maturity structure of U.S. public firms

during the period 1985-2015. We find strong and robust evidence of a negative relation between

policy uncertainty and debt maturity and the finding holds for both maturities of new bond issues

obtained from SDC Platinum as well as short-term debt ratios calculated from the balance sheet

data. The results are robust to several alternative measures of policy uncertainty and debt maturity.

Moreover, policy uncertainty is positively related to the number of debt covenants in loan

contracts. We find that these relations are stronger for financially constrained firms, i.e., those with

non-investment grade credit ratings, as these firms face creditors’ unwillingness to lend long-term

debts when policy uncertainty is high. In addition, our analysis on the cost of debt shows that yield

spread increases amid higher uncertainty for the new debt issue sample, and the result is

concentrated on non-investment grade borrowing firms. We investigate the link between policy

uncertainty and debt maturity and the relation between policy uncertainty and corporate

investment, and find that investment of financially constrained firms is more affected by policy

uncertainty, possibly due to their lack of external debt financing and unfavorable debt terms. Our

finding suggests that the effects of policy uncertainty on debt contracting as one of the channels

through which policy uncertainty adversely affects real investments.

34

References

Aivazian, V.A., Ge, Y. and Qiu, J., 2005. Debt maturity structure and firm investment. Financial

Management, 34(4), 107-119.

Altman, E.I., Robert G.H., Narayanan, P., 1977. ZETATM analysis: A new model to identify

bankruptcy risk of corporations. Journal of Banking and Finance, 1(1), 29–54.

Alfaro, I., Bloom N., Lin, X., 2016. The real and financial impact of uncertainty shocks. Working

paper, The Ohio State University and Stanford University.

Almeida, H., Campello, M., Laranjeira, B., Weisbenner, S., 2012. Corporate Debt Maturity and

the Real Effects of the 2007 Credit Crisis. Critical Finance Review, 1(1), 3-58.

Baker, S.; Bloom, N., Davis, S., 2016. Measuring Economic Policy Uncertainty. Quarterly

Journal of Economics 131, 1593–1636.

Baker, M., Wurgler, J., 2007. Investor Sentiment in the stock market. Journal of Economic

Perspectives 21, 129–152.

Barclay, M.J., Smith, C.W., 1995. The maturity structure of corporate debt. Journal of Finance 50,

609-631.

Barnea, A., Haugen, R.A, Lemma W.S., 1980. A rationale for debt maturity structure and call

provisions in the agency theoretic framework. Journal of Finance 35, 1223-1234.

Bernanke, B.S., 1983. Irreversibility, uncertainty, and cyclical investment. Quarterly Journal of

Economics 98 (1), 85-106.

Bloom, N., 2009. The impact of uncertainty shocks. Econometrica 77, 623–685.

Boutchkova, M., Doshi, H., Durnev, A., Molchanov, A., 2010. Precarious politics and return

volatility. Review of Financial Studies 25 (4), 1111–1154.

Brockman, P., Martin, X., Unlu, E., 2010. Executive compensation and the maturity structure of

corporate debt. Journal of Finance 65, 1123–1161.

Cao, W., Duan, X., Uysal V.B., 2013. Does political uncertainty affect capital structure choices?

Working paper, University of Oklahoma.

Cambello, M., Graham, J.R., Harvey, C.R., 2010. The real effects of financial constraints:

Evidence from a financial crisis. Journal of Financial Economics 97 (3), 470–487.

Custódio, C., Ferreira, M.A., Laureano. L, 2013. Why Are US Firms Using More Short-term Debt?

Journal of Financial Economics 108, 182-212.

35

Colak, G., Flannery, M.J., Öztekinc, Ö., 2014. Political Uncertainty, Transaction Costs, and

Leverage Adjustments: An International Perspective. Working Paper.

Colak, G., Durnev, A., Qian, Y., 2017. Political uncertainty and IPO activity: evidence from U.S.

gubernatorial elections. Journal of Financial and Quantiative Analysis. (forthcoming)

Diamond, D.W., 1991. Debt maturity structure and liquidity risk. Quarterly Journal of Economics

106, 709–737.

Diamond, D.W., He, Z., 2014. A theory of debt maturity: The long and short of debt overhang.

Journal of Finance 69, 719–762.

Dang, V. A., Phan, H. V., 2016. CEO Inside Debt and Corporate Debt Maturity Structure. Journal

of Banking & Finance 70, 38-54.

Faulkender, M., Petersen, M.A., 2006. Does the source of capital affect capital structure? Review

of Financial Studies 19, 45–79.

Fons, J.S., 1994. Using default rates to model the term structure of credit risk. Financial Analysts

Journal, 50(5), 25-32.

Francis, B., Hasan, I., Zhu, Y., 2013. Political uncertainty and bank loan contracting. Working

paper, Rensselaer Polytechnic Institute.

Frank, M., Goyal, V., 2009. Capital structure decisions: Which factors are reliably important?

Financial Management 38, 1–37.

Graham, J. R., Harvey, C. R., 2001. The theory and practice of corporate finance: Evidence from

the field. Journal of financial economics, 60(2), 187-243.

Gilchrist, S., Sim J., Zakrajsek, E., 2011. Uncertainty, financial frictions and investment

dynamics. Working paper, Boston University and NBER, and Federal Reserve Board of

Governors.

Graham, J. R., Harvey, C. R., 2001. The theory and practice of corporate finance: Evidence from

the field. Journal of Financial Economics, 602, 187-243.

Guedes, J., Opler, T., 1996. The determinants of the maturity of corporate debt issues. Journal of

Finance 51, 1809–1833.

Gulen, H., Ion, M., 2016. Policy uncertainty and corporate investment. Review of Financial

Studies, 29(3), 523-564.

Jarrow, R.A., Lando, D., Turnbull, S.M., 1997. A Markov model for the term structure of credit

risk spreads. Review of Financial studies, 10(2), 481-523.

36

Julio, B., Yook, Y., 2012. Corporate financial policy under political uncertainty: International

evidence from national elections. Journal of Finance 67, 45-84.

Jens, C.E., 2017. Political uncertainty and investment: Causal evidence from US gubernatorial

elections. Journal of Financial Economics, 124(3), 563-579.

Jensen, M.C. and Meckling, W.H., 1976. Theory of the firm: Managerial behavior, agency costs

and ownership structure. Journal of financial economics, 3(4), 305-360.

Jensen, M.C, 1986. Agency cost of free cash flow, corporate finance, and takeovers. American

Economic Review 76 (2), 323–329.

Kelly, B., Pástor, Ľ. and Veronesi, P., 2016. The price of political uncertainty: Theory and evidence

from the option market. The Journal of Finance, 71(5), 2417-2480.

Leary, M., 2009. Bank loan supply, lender choice, and corporate capital structure. Journal of

Finance 64, 1143–1185.

Lemmon, M., Roberts, M., 2010. The response of corporate financing and investment to changes

in the supply of credit. Journal of Financial and Quantitative Analysis 45, 555–587.

Lemmon, M., Roberts, M., Zender, J., 2008. Back to the beginning: Persistence and the cross-

section of corporate capital structure. Journal of Finance 63, 1575–1608.

Leland, H.E., Toft, K.B., 1996. Optimal capital structure, endogenous bankruptcy, and the term

structure of credit spreads. Journal of Finance 51, 987–1019.

Longstaff, F.A., Schwartz, E.S., 1995. A simple approach to valuing risky fixed and floating rate

debt. The Journal of Finance, 50(3), 789-819.

McCarty, N.M., 2011. The limits of electoral and legislative reform in addressing polarization.

California Law Review 99, 359–372.

Merton, R.C., 1974. On the pricing of corporate debt: The risk structure of interest rates. The

Journal of finance, 29(2), 449-470.

Myers, S.C., 1977. Determinants of corporate borrowing. Journal of Financial Economics 5,

147–175.

Nguyen, N.H. and Phan, H.V., 2017. Policy Uncertainty and Mergers and Acquisitions. Journal of

Financial and Quantitative Analysis, 52(2), 613-644.

Pastor, L. and Veronesi, P., 2012. Uncertainty about government policy and stock prices. The

Journal of Finance, 67(4), 1219-1264.

37

Pástor, Ľ. and Veronesi, P., 2013. Political uncertainty and risk premia. Journal of Financial

Economics, 110(3), 520-545.

Rajan, R., Winton, A., 1995. Covenants and collateral as incentives to monitor. Journal of Finance

50, 1113–1146.

Rajan, R., Zingales, L., 2012. What do we know about capital structure? Some evidence from

international data. Journal of Finance 50, 1421-1460.

Rodrik, D., 1991. Policy uncertainty and private investment in developing countries. Journal of

Development Economics 36 (2), 229–242.

Sarig, O., Warga, A., 1989. Some empirical estimates of the risk structure of interest rates. The

Journal of Finance, 44(5), 1351-1360.

Stulz, R.M., 2000. Does financial structure matter for economic growth? A corporate finance

perspective. Working paper, Ohio State University.

Sherr, F., Hulburt, H., 2001. The debt maturity structure of small firms. Financial Management 30,

85–111.

38

Appendix

Table A. Variable Definition

Variable Calculation Data sources

Abnormal earnings The ratio of the difference between the income before

extraordinary items, adjusted for common or ordinary

stock (capital) equivalents at time t and t–1, to the market

value of equity.

COMPUSTAT

Asset maturity Property, plant, and equipment over depreciation times the

proportion of property, plant, and equipment in total

assets, plus the ratio of current assets to the cost of goods

sold times the proportion of current assets in total assets.

COMPUSTAT

Asset volatility The standard deviation of the stock return (during the

fiscal year) times the market value of equity, all divided

by the market value of assets.

COMPUSTAT

Average rating Number between 1 and 19 (1 for CCC and 19 for AAA),

using the average of Standard and Poor’s and Moody’s

ratings (if only 1 rating is available, we use that bond

rating)

SDC Platinum

Coupon The coupon rate of the specified bond SDC Platinum

Interest coverage Logarithmic transformation of the pre-tax interest

coverage ratio.

COMPUSTAT

Issue size Natural logarithm of the total proceeds from the bond

issue (in $ million).

SDC Platinum

Leverage The ratio of total debt to the sum of market equity and

total debt, in which market equity is calculated as the

closing stock price times common shares outstanding.

COMPUSTAT

LMAT The time, measured in years, from the date of issuance to

the date of maturity in natural logarithm.

SDC Platinum

Market-to-book ratio Market value of the firm divided by the book value of

total assets

COMPUSTAT

Profitability Operating income before depreciation scaled by sales. COMPUSTAT

S&P credit ratings

dummy

A dummy variable that equals one if a firm has an S&P

rating on long-term debt, and zero otherwise

COMPUSTAT

Size The natural log of (market value of equity + book value of

assets – book value of equity) for firm i in year t

COMPUSTAT

Short-term debt 1 (ST1) The ratio of debt in current liabilities to total debt. COMPUSTAT

Short-term debt 2 (ST2) The ratio of debt in current liabilities plus debt maturing in

two years to total debt.

COMPUSTAT

Short-term debt 3 (ST3) The ratio of debt in current liabilities plus debt maturing in

two or three years to total debt.

COMPUSTAT

39

Short-term debt 4 (ST4) The ratio of debt in current liabilities plus debt maturing in

two, three, or four years to total debt.

COMPUSTAT

Short-term debt 5 (ST5) The ratio of debt in current liabilities plus debt maturing in

two, three, four, or five years to total debt.

COMPUSTAT

Short-term debt NP

(STNP)

The ratio of debt in current liabilities without the current

proportion of long-term debt to total debt.

COMPUSTAT

Term structure of

interest rate

Yield on 10-year government bonds subtracted from the

yield on 6-month government bonds at the year end

FRED at the

Federal Reserve

Bank of St. Louis

Treasury rate Treasury rate that corresponds most closely to the specific

bond’s maturity

FRED at the

Federal Reserve

Bank of St. Louis

Yield curve slope The difference between 10-year and 2-year Treasury rates FRED at the

Federal Reserve

Bank of St. Louis

Z-score Bankruptcy

dummy

A dummy variable that equals one if Altman’s Z-score is

greater than 1.81 and zero otherwise

COMPUSTAT

40

Figure 1: Policy Uncertainty and Average Years to Maturities of New Debt Issues

41

Figure 2: Coefficients of Policy Uncertainty on Quarterly Short-term Debt Ratio with 95%

Confidence Interval

-0.05

-0.04

-0.03

-0.02

-0.01

0

0.01

0.02

0.03

0.04

0.05

1 2 3 4 5 6 7 8 9 10 11 12

Upper bound Coefficient on Policy Uncertainty Lower bound

42

Table 1: Descriptive Statistics

This table reports the descriptive statistics of the variables. The sample consists of new bond issues by

sample firms over the period 1985-2015. Bond Maturity is the natural logarithm of the years to maturity of

new debt issues. Equal-weighted Bond Maturity is the equal-weighted average of the maturities of

multiple debt issues throughout a year. Issue size-weighted Bond Maturity is the weighted average of

the maturities of multiple debt issues throughout a year based on issue size. Measures of policy

uncertainty include the annual policy uncertainty index of year t as the natural logarithm of the