pnp specificationsfiles.afncorp.com/webtrac/ratesheet/pnps/afn-r-ops_handlingvaloans.pdfprossessing,...

TRANSCRIPT

PROSSESSING, UNDERWRITING, DOCS FUNDING PROCEDURE – VA - HANDLING VA LOANS

AFN-R-Ops_HandlingVALoans • 05/09/2016 i

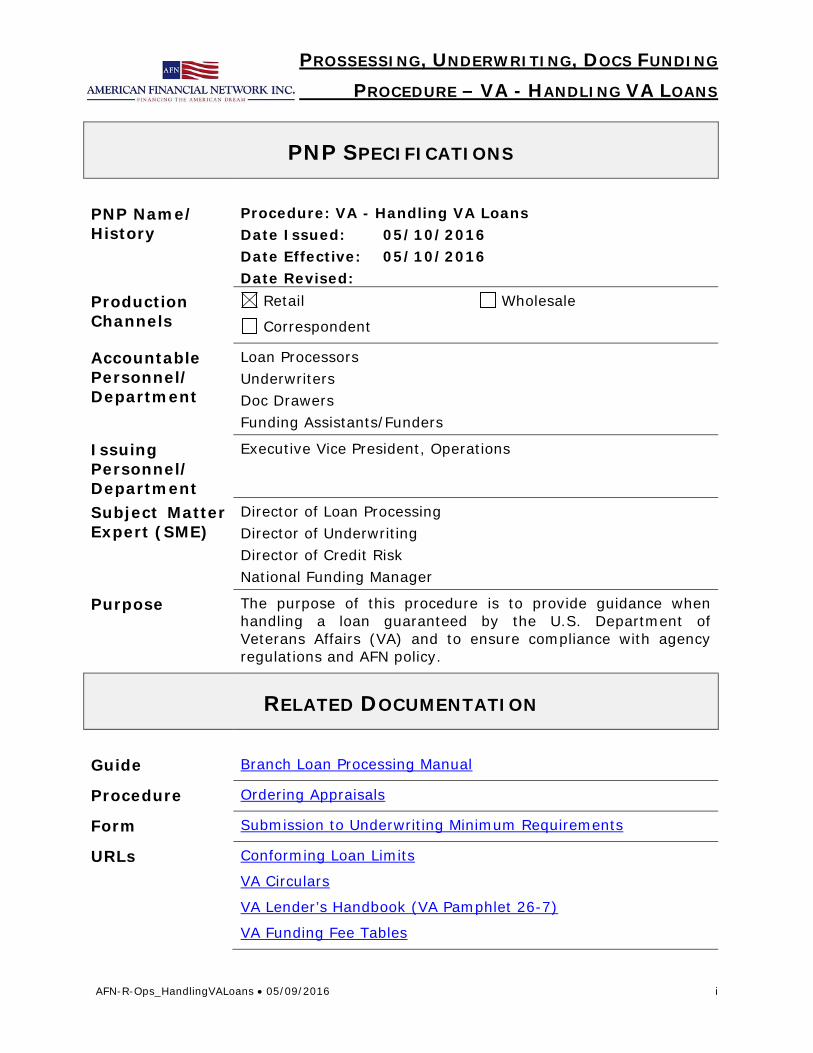

PNP SPECIFICATIONS

PNP Name/ History

Procedure: VA - Handling VA Loans Date Issued: 05/10/2016 Date Effective: 05/10/2016 Date Revised:

Production Channels

Retail Wholesale

Correspondent

Accountable Personnel/ Department

Loan Processors Underwriters Doc Drawers Funding Assistants/Funders

Issuing Personnel/ Department

Executive Vice President, Operations

Subject Matter Expert (SME)

Director of Loan Processing Director of Underwriting Director of Credit Risk National Funding Manager

Purpose The purpose of this procedure is to provide guidance when handling a loan guaranteed by the U.S. Department of Veterans Affairs (VA) and to ensure compliance with agency regulations and AFN policy.

RELATED DOCUMENTATION

Guide Branch Loan Processing Manual

Procedure Ordering Appraisals

Form Submission to Underwriting Minimum Requirements

URLs Conforming Loan Limits

VA Circulars

VA Lender’s Handbook (VA Pamphlet 26-7)

VA Funding Fee Tables

PROSSESSING, UNDERWRITING, DOCS FUNDING PROCEDURE – VA - HANDLING VA LOANS

AFN-R-Ops_HandlingVALoans • 05/09/2016 ii

RELATED DEFINITIONS

VA Home Loan VA helps military Servicemembers, Veterans, and eligible surviving spouses become homeowners by providing a home loan guaranty benefit. VA Home Loans are provided by private lenders, and the VA guarantees a portion of the loan, which allows the lender to provide more favorable terms.

VA Loan Guaranty Monitoring Unit

The mission of the Loan Guaranty Monitoring Unit is to protect the interests of the Government and the veterans by ensuring that lenders process and close VA home loans in accordance with the law, regulations, and program directives.

VA Loan Guaranty Monitoring Unit audits include: • Obtaining refunds to veterans for unallowed charges and

overcharges. • Ensuring the homes that are security for loans meet VA

minimum property standards. • Protecting taxpayers against loss by obtaining

indemnification for loan processing that clearly does not meet program requirements.

• Recovering losses suffered on loan defaults that result from poorly processed loans that should not have been made.

• Educating lenders about program requirements to improve the quality of loans.

VA Lender Appraisal Processing Program (LAPP)

The Lender Appraisal Processing Program (LAPP) expedites loan closing by allowing VA-authorized lenders to receive appraisal reports directly from appraisers and process them without VA involvement. There are four steps to processing LAPP cases:

1. LAPP lender requests VA assignment of a fee appraiser and a VA loan number and identifies the case as LAPP.

2. VA-assigned appraiser sends the appraisal report directly to the LAPP lender’s VA-approved SAR.

3. LAPP lender’s SAR then: a. Reviews the appraisal for completeness and conformity; b. Determines reasonable value of the property and any VA

guaranty conditions that must be met; and c. Sends the veteran buyer a written notice of value (NOV),

which includes any conditions or requirements upon which VA loan guaranty is contingent.

(Continued)

PROSSESSING, UNDERWRITING, DOCS FUNDING PROCEDURE – VA - HANDLING VA LOANS

AFN-R-Ops_HandlingVALoans • 05/09/2016 iii

RELATED DEFINITIONS (CONTINUED)

LAPP (Continued)

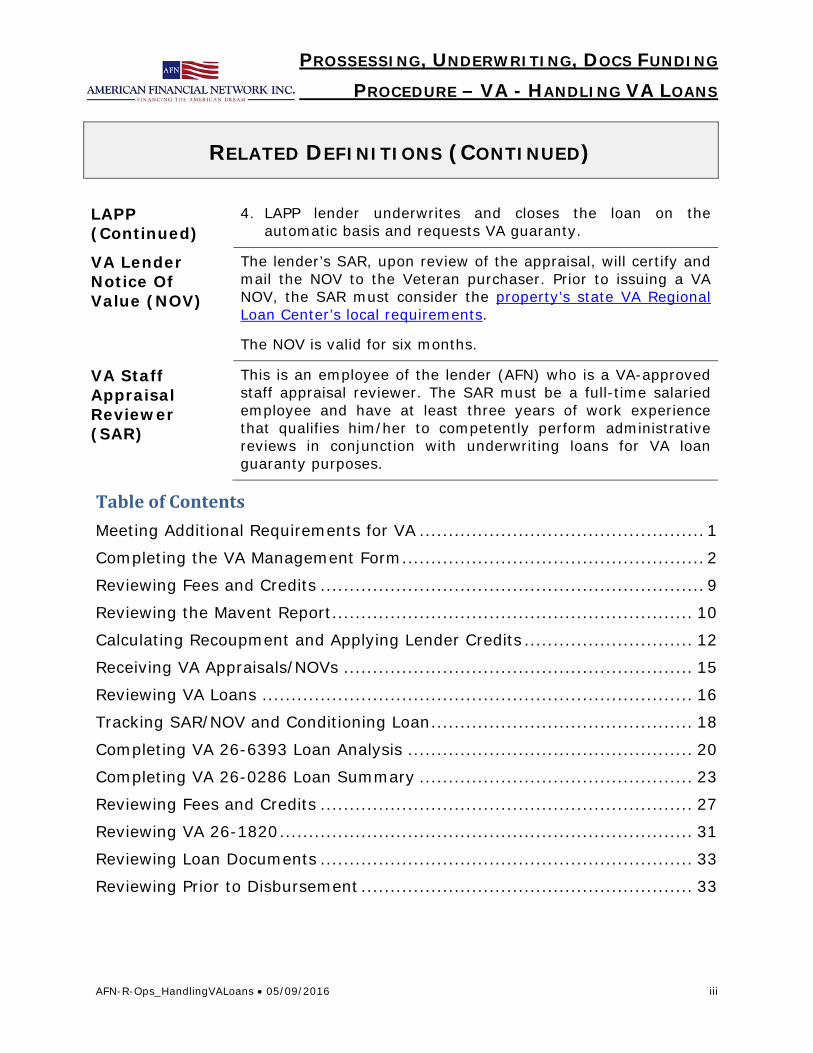

4. LAPP lender underwrites and closes the loan on the automatic basis and requests VA guaranty.

VA Lender Notice Of Value (NOV)

The lender’s SAR, upon review of the appraisal, will certify and mail the NOV to the Veteran purchaser. Prior to issuing a VA NOV, the SAR must consider the property’s state VA Regional Loan Center’s local requirements.

The NOV is valid for six months.

VA Staff Appraisal Reviewer (SAR)

This is an employee of the lender (AFN) who is a VA-approved staff appraisal reviewer. The SAR must be a full-time salaried employee and have at least three years of work experience that qualifies him/her to competently perform administrative reviews in conjunction with underwriting loans for VA loan guaranty purposes.

Table of Contents Meeting Additional Requirements for VA ................................................. 1

Completing the VA Management Form .................................................... 2

Reviewing Fees and Credits .................................................................. 9

Reviewing the Mavent Report .............................................................. 10

Calculating Recoupment and Applying Lender Credits ............................. 12

Receiving VA Appraisals/NOVs ............................................................ 15

Reviewing VA Loans .......................................................................... 16

Tracking SAR/NOV and Conditioning Loan ............................................. 18

Completing VA 26-6393 Loan Analysis ................................................. 20

Completing VA 26-0286 Loan Summary ............................................... 23

Reviewing Fees and Credits ................................................................ 27

Reviewing VA 26-1820 ....................................................................... 31

Reviewing Loan Documents ................................................................ 33

Reviewing Prior to Disbursement ......................................................... 33

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 1 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 1

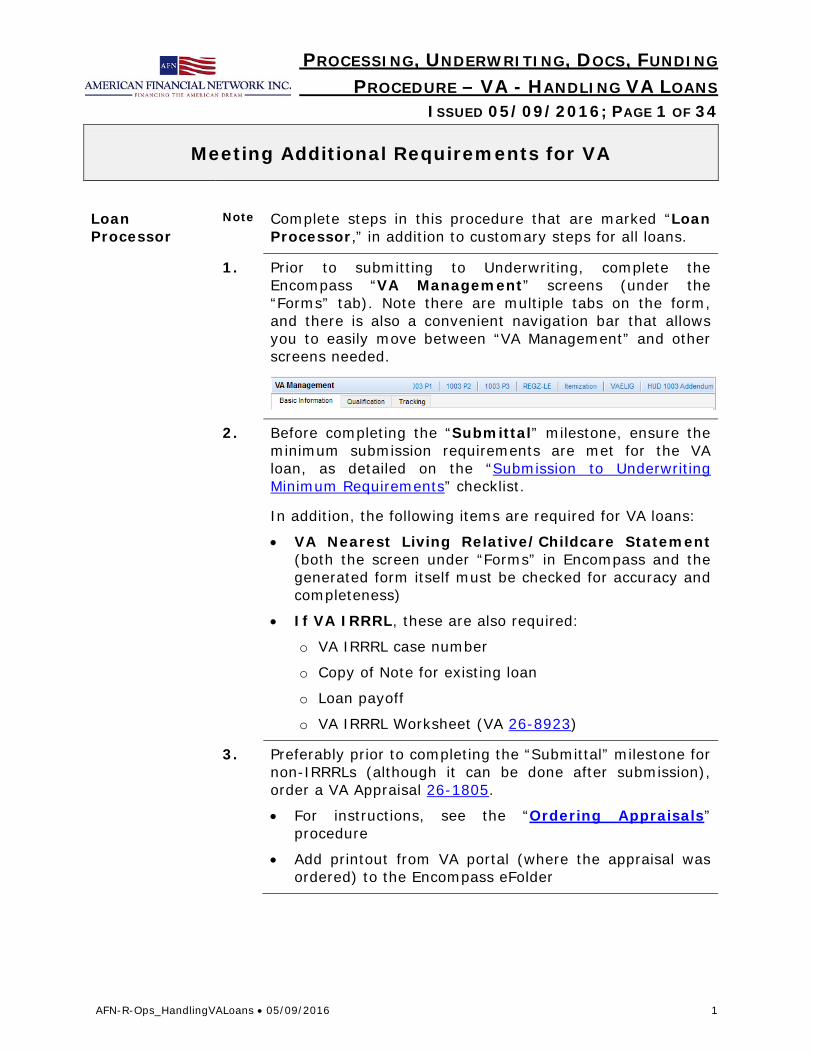

Meeting Additional Requirements for VA

Loan Processor

Note Complete steps in this procedure that are marked “Loan Processor,” in addition to customary steps for all loans.

1. Prior to submitting to Underwriting, complete the Encompass “VA Management” screens (under the “Forms” tab). Note there are multiple tabs on the form, and there is also a convenient navigation bar that allows you to easily move between “VA Management” and other screens needed.

2. Before completing the “Submittal” milestone, ensure the minimum submission requirements are met for the VA loan, as detailed on the “Submission to Underwriting Minimum Requirements” checklist.

In addition, the following items are required for VA loans:

• VA Nearest Living Relative/Childcare Statement (both the screen under “Forms” in Encompass and the generated form itself must be checked for accuracy and completeness)

• If VA IRRRL, these are also required:

o VA IRRRL case number

o Copy of Note for existing loan

o Loan payoff

o VA IRRRL Worksheet (VA 26-8923)

3. Preferably prior to completing the “Submittal” milestone for non-IRRRLs (although it can be done after submission), order a VA Appraisal 26-1805.

• For instructions, see the “Ordering Appraisals” procedure

• Add printout from VA portal (where the appraisal was ordered) to the Encompass eFolder

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 2 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 2

Completing the VA Management Form

Loan Processor

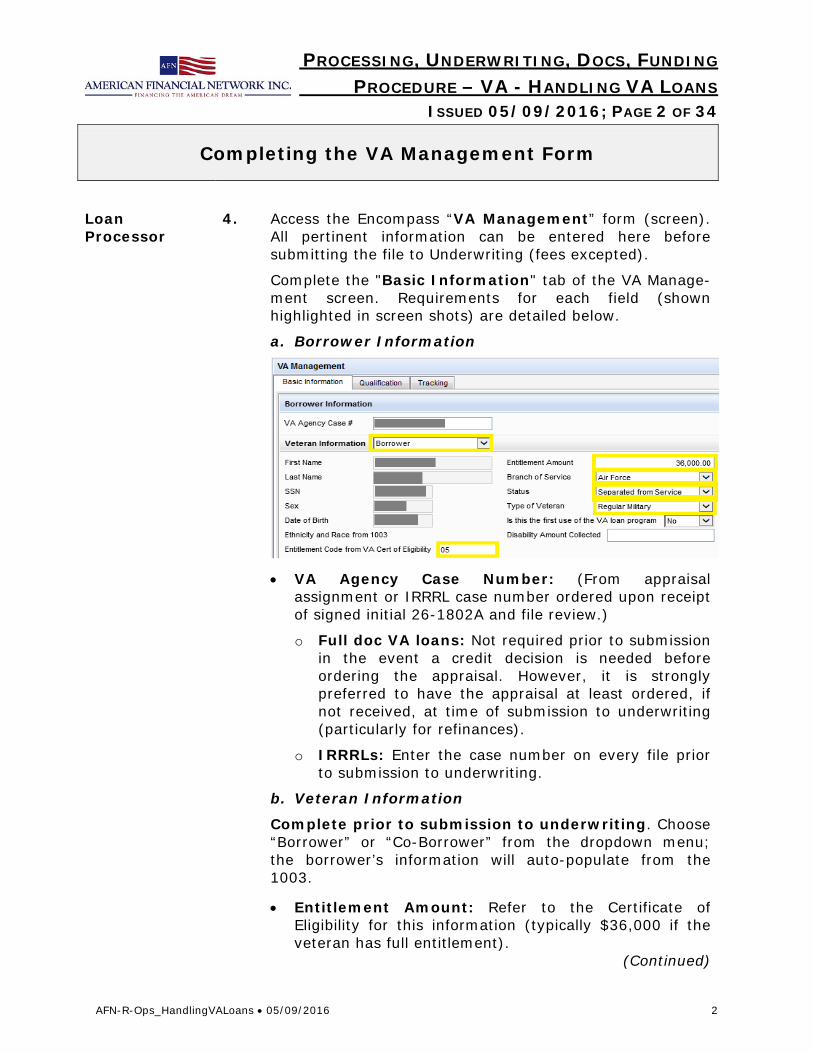

4. Access the Encompass “VA Management” form (screen). All pertinent information can be entered here before submitting the file to Underwriting (fees excepted).

Complete the "Basic Information" tab of the VA Manage-ment screen. Requirements for each field (shown highlighted in screen shots) are detailed below.

a. Borrower Information

• VA Agency Case Number: (From appraisal

assignment or IRRRL case number ordered upon receipt of signed initial 26-1802A and file review.)

o Full doc VA loans: Not required prior to submission in the event a credit decision is needed before ordering the appraisal. However, it is strongly preferred to have the appraisal at least ordered, if not received, at time of submission to underwriting (particularly for refinances).

o IRRRLs: Enter the case number on every file prior to submission to underwriting.

b. Veteran Information

Complete prior to submission to underwriting. Choose “Borrower” or “Co-Borrower” from the dropdown menu; the borrower’s information will auto-populate from the 1003.

• Entitlement Amount: Refer to the Certificate of Eligibility for this information (typically $36,000 if the veteran has full entitlement).

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 3 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 3

Completing the VA Management Form (Continued)

Loan Processor

4. (Cont’d)

Note: If entitlement is less than this amount due to a prior VA loan, you may need to request restoration prior to docs by completing an electronic application through WebLGY in the VA portal.

• Branch of Service: Enter the Branch of Service shown on the veteran’s DD214 or Certificate of Eligibility.

• Status: Select “Separated from Service” to indicate the veteran is retired from the military, or “In Service” if still on active duty.

• Type of Veteran: Select from the available options: o “Regular Military” o “Reserves” or o “National Guard” Note: If Reserves or National Guard, the required service time and documentation for the Certificate of Eligibility may differ; VA funding fee will likely differ as well (except on IRRRLs). Please ensure accuracy.

• Entitlement Code from VA Cert of Eligibility: Enter the code listed on the Certificate of Eligibility. This may trigger a change in the VA funding fee; ensure accuracy.

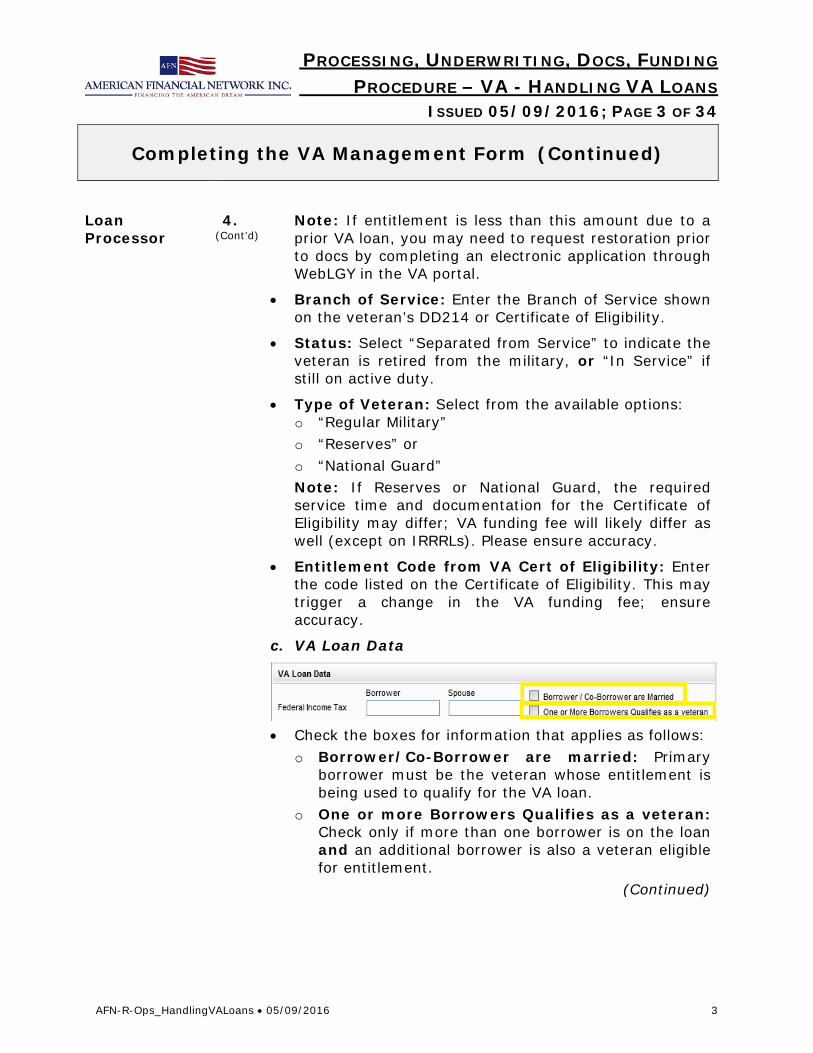

c. VA Loan Data

• Check the boxes for information that applies as follows:

o Borrower/Co-Borrower are married: Primary borrower must be the veteran whose entitlement is being used to qualify for the VA loan.

o One or more Borrowers Qualifies as a veteran: Check only if more than one borrower is on the loan and an additional borrower is also a veteran eligible for entitlement.

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 4 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 4

Completing the VA Management Form (Continued)

Loan Processor

4. (Cont’d)

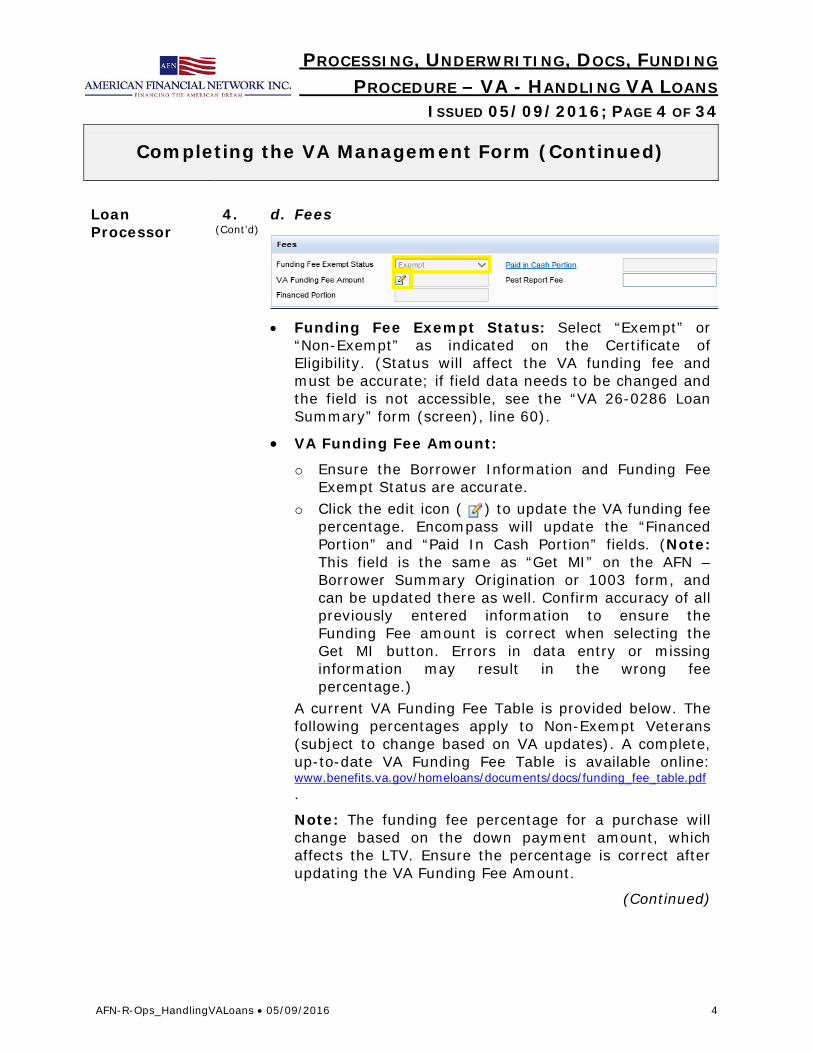

d. Fees

• Funding Fee Exempt Status: Select “Exempt” or “Non-Exempt” as indicated on the Certificate of Eligibility. (Status will affect the VA funding fee and must be accurate; if field data needs to be changed and the field is not accessible, see the “VA 26-0286 Loan Summary” form (screen), line 60).

• VA Funding Fee Amount:

o Ensure the Borrower Information and Funding Fee Exempt Status are accurate.

o Click the edit icon ( ) to update the VA funding fee percentage. Encompass will update the “Financed Portion” and “Paid In Cash Portion” fields. (Note: This field is the same as “Get MI” on the AFN – Borrower Summary Origination or 1003 form, and can be updated there as well. Confirm accuracy of all previously entered information to ensure the Funding Fee amount is correct when selecting the Get MI button. Errors in data entry or missing information may result in the wrong fee percentage.)

A current VA Funding Fee Table is provided below. The following percentages apply to Non-Exempt Veterans (subject to change based on VA updates). A complete, up-to-date VA Funding Fee Table is available online: www.benefits.va.gov/homeloans/documents/docs/funding_fee_table.pdf.

Note: The funding fee percentage for a purchase will change based on the down payment amount, which affects the LTV. Ensure the percentage is correct after updating the VA Funding Fee Amount.

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 5 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 5

Completing the VA Management Form (Continued)

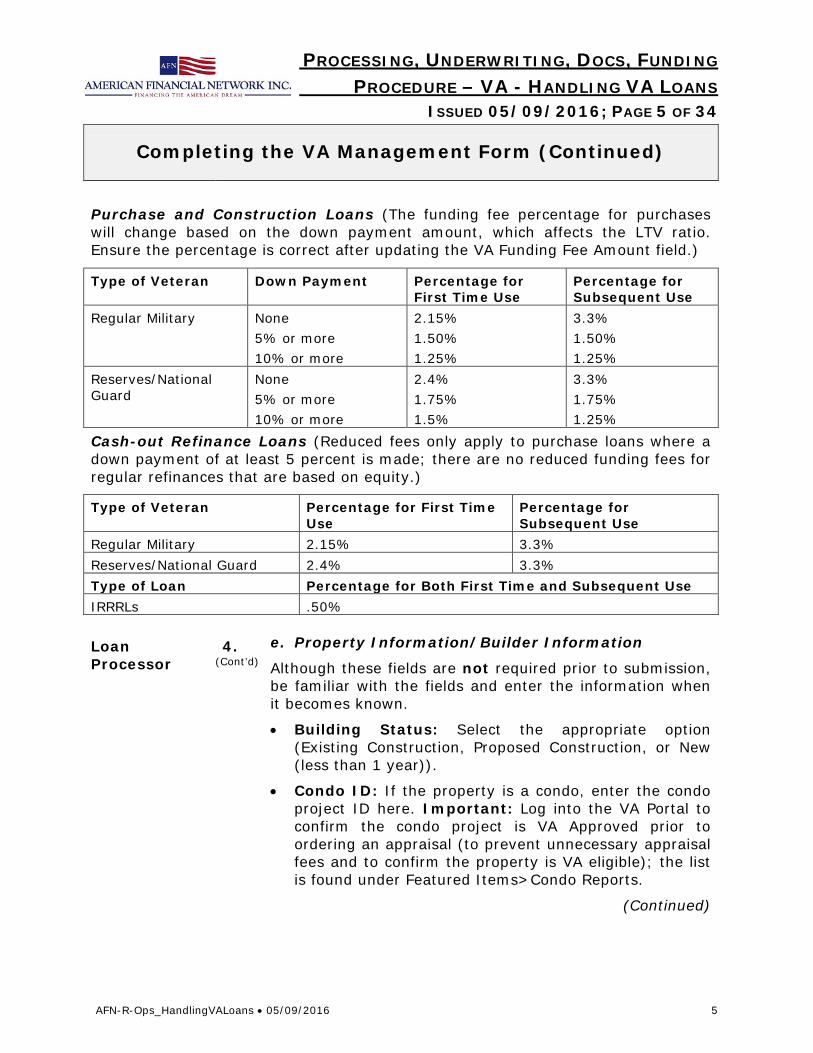

Purchase and Construction Loans (The funding fee percentage for purchases will change based on the down payment amount, which affects the LTV ratio. Ensure the percentage is correct after updating the VA Funding Fee Amount field.)

Type of Veteran Down Payment Percentage for First Time Use

Percentage for Subsequent Use

Regular Military None 5% or more 10% or more

2.15% 1.50% 1.25%

3.3% 1.50% 1.25%

Reserves/National Guard

None 5% or more 10% or more

2.4% 1.75% 1.5%

3.3% 1.75% 1.25%

Cash-out Refinance Loans (Reduced fees only apply to purchase loans where a down payment of at least 5 percent is made; there are no reduced funding fees for regular refinances that are based on equity.)

Type of Veteran Percentage for First Time Use

Percentage for Subsequent Use

Regular Military 2.15% 3.3% Reserves/National Guard 2.4% 3.3% Type of Loan Percentage for Both First Time and Subsequent Use IRRRLs .50% Loan Processor

4. (Cont’d)

e. Property Information/Builder Information

Although these fields are not required prior to submission, be familiar with the fields and enter the information when it becomes known.

• Building Status: Select the appropriate option (Existing Construction, Proposed Construction, or New (less than 1 year)).

• Condo ID: If the property is a condo, enter the condo project ID here. Important: Log into the VA Portal to confirm the condo project is VA Approved prior to ordering an appraisal (to prevent unnecessary appraisal fees and to confirm the property is VA eligible); the list is found under Featured Items>Condo Reports.

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 6 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 6

Completing the VA Management Form (Continued)

Loan Processor

4. (Cont’d)

f. Loan Information Complete this section as indicated below.

• Agency Type: This field will auto-populate based on

the selected loan program; ensure “VA” is indicated here. Note: This field also appears on the HUD 1003 Addendum.

• Title will be Vested in: Before submission to underwriting, select the appropriate option (Veteran Only, Veteran & Spouse, or Other). Note: This field also appears on the HUD 1003 Addendum.

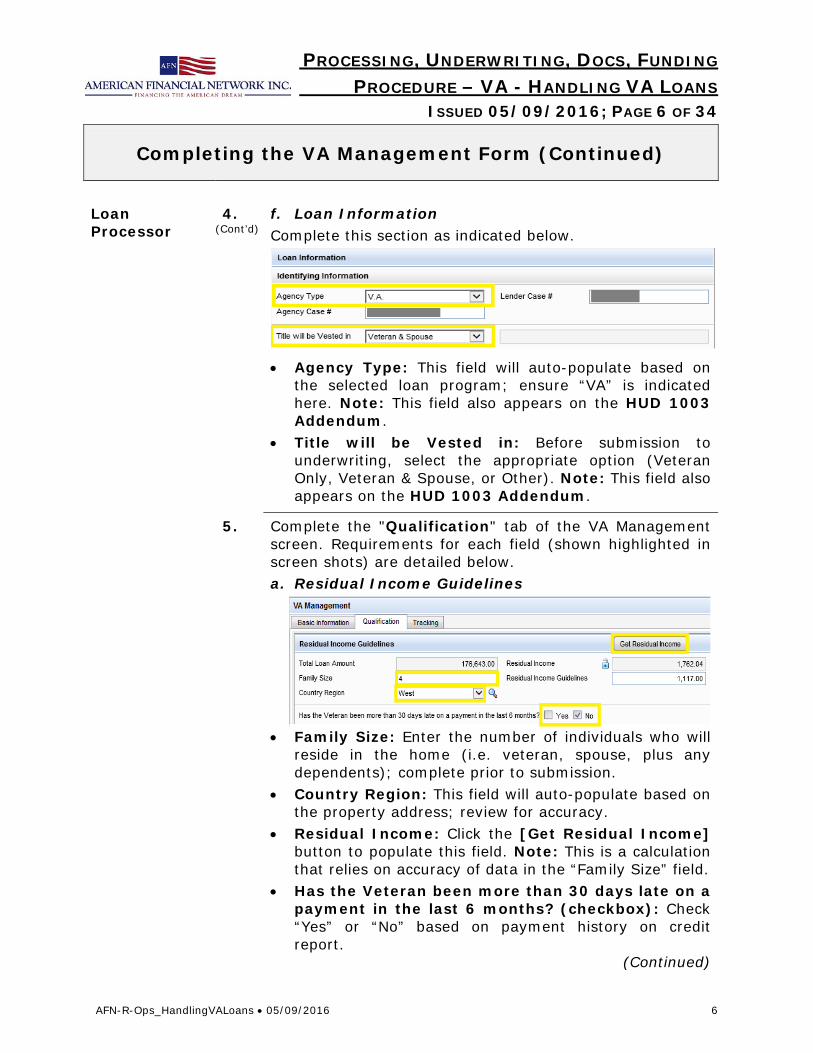

5. Complete the "Qualification" tab of the VA Management screen. Requirements for each field (shown highlighted in screen shots) are detailed below. a. Residual Income Guidelines

• Family Size: Enter the number of individuals who will reside in the home (i.e. veteran, spouse, plus any dependents); complete prior to submission.

• Country Region: This field will auto-populate based on the property address; review for accuracy.

• Residual Income: Click the [Get Residual Income] button to populate this field. Note: This is a calculation that relies on accuracy of data in the “Family Size” field.

• Has the Veteran been more than 30 days late on a payment in the last 6 months? (checkbox): Check “Yes” or “No” based on payment history on credit report.

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 7 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 7

Completing the VA Management Form (Continued)

Loan Processor

5. (Cont’d)

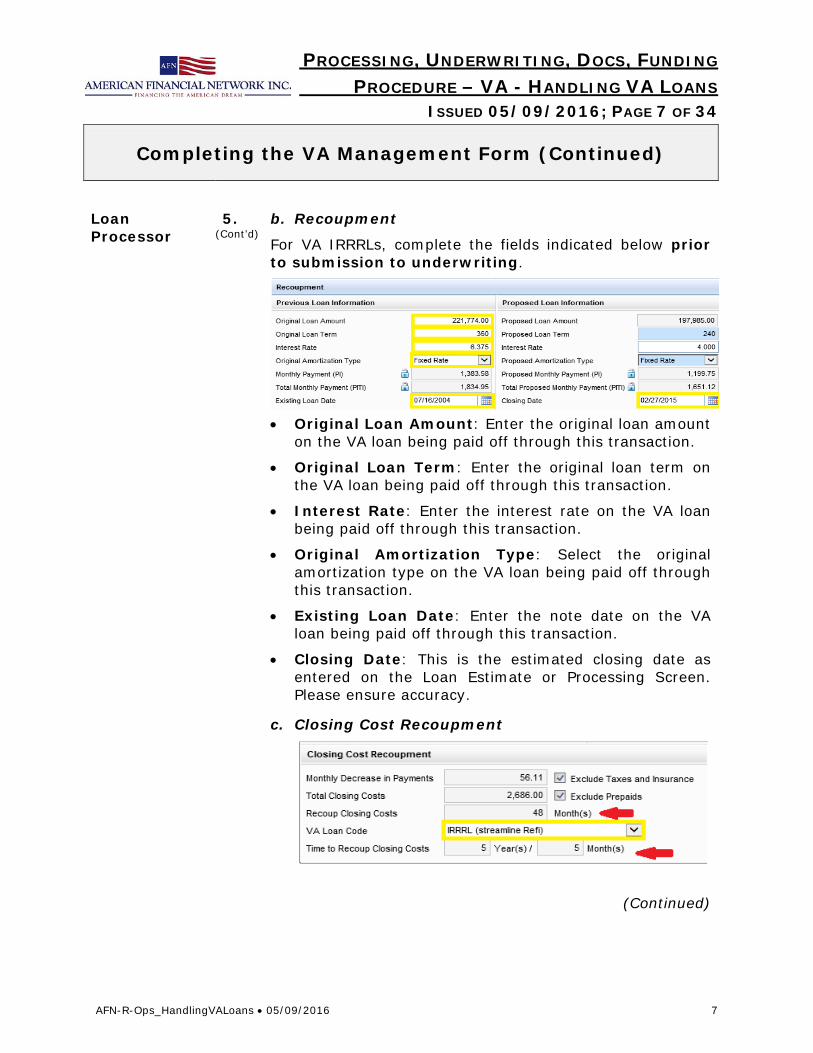

b. Recoupment

For VA IRRRLs, complete the fields indicated below prior to submission to underwriting.

• Original Loan Amount: Enter the original loan amount

on the VA loan being paid off through this transaction.

• Original Loan Term: Enter the original loan term on the VA loan being paid off through this transaction.

• Interest Rate: Enter the interest rate on the VA loan being paid off through this transaction.

• Original Amortization Type: Select the original amortization type on the VA loan being paid off through this transaction.

• Existing Loan Date: Enter the note date on the VA loan being paid off through this transaction.

• Closing Date: This is the estimated closing date as entered on the Loan Estimate or Processing Screen. Please ensure accuracy.

c. Closing Cost Recoupment

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 8 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 8

Completing the VA Management Form (Continued)

Loan Processor

5. (Cont’d)

• Monthly Decrease in Payments: This field will auto-calculate; however, for an IRRRL, it is important to note that monthly savings is a Principal-and-Interest to Principal-and-Interest comparison from the old loan to the new loan. The monthly payment on the existing loan must be broken down on page 2 of the 1003 under present housing expenses (unless a second home or investment property), so that only the principal and interest portion of the total payment is entered on that line, not the full PITI payment, otherwise the comparison and benefit/recoupment calculation will be incorrect.

• Total Closing Costs: This field will auto-calculate. For IRRRL closing cost recoupment cannot exceed 36 mos.

o Review the Itemization to confirm that fees and payment breakdown are accurate.

o Re-run Mavent preview to confirm the loan passes the 36-month requirement. If excessive, discuss adjusting costs on the loan with the Loan Originator (i.e. adding a lender credit, or potentially re-pricing the loan) in order to stay under the maximum 36 months allowed. Refer to the section on "Fees" (Steps 6-10 below) for additional information on fees and updating credits to obtain a "Pass" result for Compliance.

• Time to Recoup Closing Costs: This is the time period between the existing loan and the closing date entered for the new loan. If the existing loan date and estimated closing date are entered in the Recoupment section, this will auto-calculate. Note: If the time lapse is less than 6 months, Mavent will issue an Alert, and the loan will not be eligible for pricing to be sold to most investors (typically GNMA only). This is important when reviewing loan alerts and Mavent.

• VA Loan Code: This field indicates the VA loan type and must be accurate for the system to recognize whether the file is a purchase, cash-out refinance, or an IRRRL. Note: All VA refinances that are not IRRRLs are considered “cash-out” transactions.

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 9 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 9

Reviewing Fees and Credits

Loan Processor

6. Use the navigation bar on the VA Management form to go to the Itemization screen and enter/review fees and credits.

a. The following are VA Allowable Fees (no VA-specific

restrictions or limitations on amounts charged):

• Appraisal • Compliance Inspection (if required by NOV) • Credit Report • Recording Fees/Tax Stamps • Prorated Tax & Insurance Escrow • Hazard Insurance Premium (invoice required) • Survey • Title Insurance and title-related fees (policy, exam,

search, endorsement, preparation) • Environmental Protection Lien Endorsement • 1% Origination Fee (Note: In order to avoid

predatory lending practices AFN does not charge a 1% origination fee; instead, origination charges are itemized by specific fee names.)

• VA Funding Fee • Discount Points • Closing Protection Letter • Well and Septic Inspection Fees

b. Ensure a combined total of all fees listed below (“Unallowable Fees”) does not exceed 1% of the loan amount. • Settlement/Escrow/Closing Fee • Document Preparation • Underwriting • Processing • Application Fee • Attorney Fees (for other than title work) • Assignment Fee • Fax/Copy/Print Fees

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 10 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 10

Reviewing Fees and Credits (Continued)

Loan Processor

6. (Cont’d)

• Email/eDoc Fees • Postage Fees • Notary Signing Fee • Commitment Fee • Trustee Fee • Tax Service Fee Note: Any amounts over 1% must be marked as lender paid and a credit must be approved by the Lock Desk (Branch Manager must request lender credit with the Encompass “Lender Credit Screen” under the Forms tab). An origination credit for rate may not be used to cover the difference over the 1% maximum; a separate lender credit would have to be requested and approved.

c. Ensure the following fees are NOT paid by the veteran, regardless of whether an origination fee, or total of the unallowable fees does not exceed 1%. • Termite/Pest Inspection • Attorney Fee (as a benefit to the Lender) • Mortgage Broker Fee • Realtor Commission • HUD/FHA Inspection Fees (for Builders)

Reviewing the Mavent Report

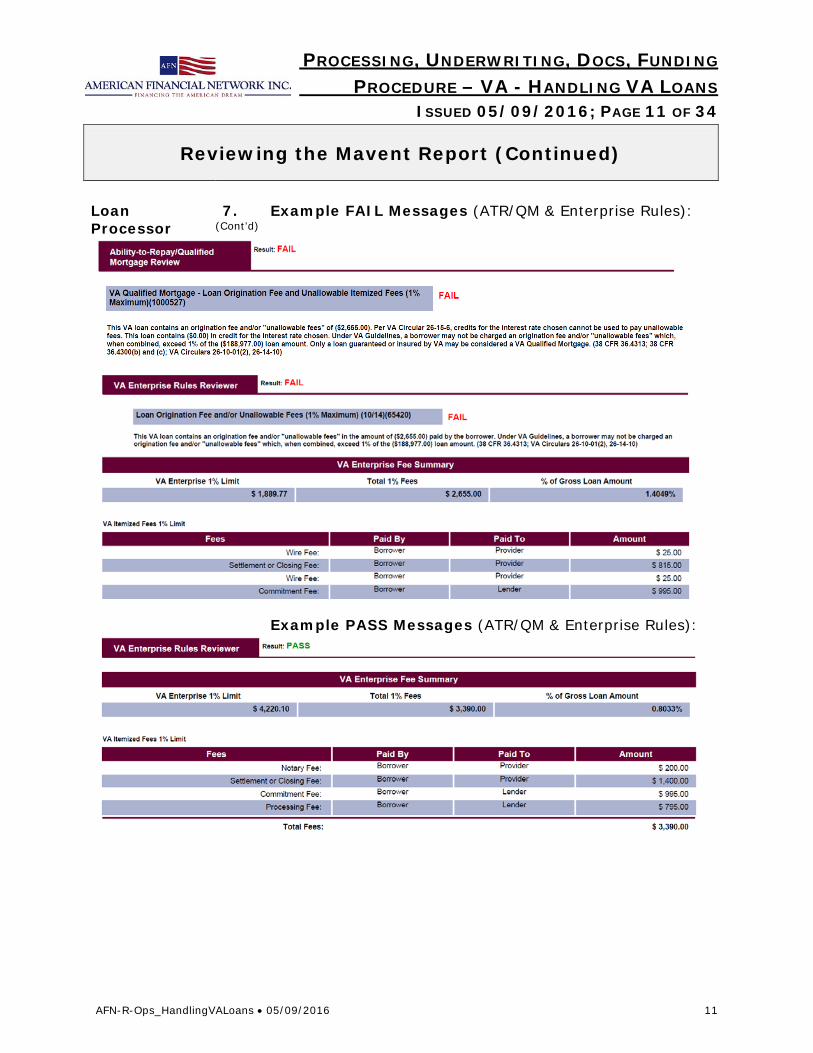

Loan Processor

7. Go to the Encompass Compliance Review tool and review the Mavent report to ensure there are no fee violations present in the fee/credit calculations. Perform this task any time fees and/or credits are added or amended.

See examples of FAIL and PASS below. Note that in both examples a breakdown of the 1% fees is available in the “Enterprise Rules” section of the Mavent report.

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 11 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 11

Reviewing the Mavent Report (Continued)

Loan Processor

7. (Cont’d)

Example FAIL Messages (ATR/QM & Enterprise Rules):

Example PASS Messages (ATR/QM & Enterprise Rules):

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 12 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 12

Calculating Recoupment and Applying Lender Credits

Loan Processor

8. For VAIRRRLs, see the Note and/or Mortgage Statement and ensure data entered in Encompass is correct. a. Ensure Principal & Interest payment figure of the loan

to be paid off is accurate. b. Ensure all fees charged to the borrower on the

Itemization screen are accurate.

9. Calculate recoupment period (cannot exceed 36 months): a. Subtract new loan’s monthly Principal & Interest (ONLY)

from the existing loan’s monthly Principal & Interest (ONLY); the result is the monthly savings amount.

b. Multiply the amount derived in Step 9.a. (monthly savings amount) by 36 (months); the result is the maximum allowed by VA to meet recoupment requirements.

c. Add together all closing costs, discount fees, and the VA funding fee amount (prepaid items such as escrow reserves and per diem interest may be excluded); the result is the total cost of the new loan.

d. Compare the maximum allowed by VA to meet recoupment requirements to the total cost of the new loan. If the total cost is greater than the maximum allowed, a lender credit of the difference is required in order to proceed with the loan. Note: When applying a lender credit, also reduce the loan amount so the borrower does not receive cash to close in excess of program requirements. In making these adjustments, you may need to recalculate and adjust the recoup/savings amount for changes in savings and lender credit calculations. Also note that lender credits, once disclosed, cannot be reduced.

10. If required (and approved by the branch), apply a lender credit as follows: a. From the “VA Management” Form (screen), click

“Itemization” (on the navigation bar).

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 13 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 13

Calculating Recoupment and Applying Lender Credits (Continued)

Loan Processor

10. (Cont’d)

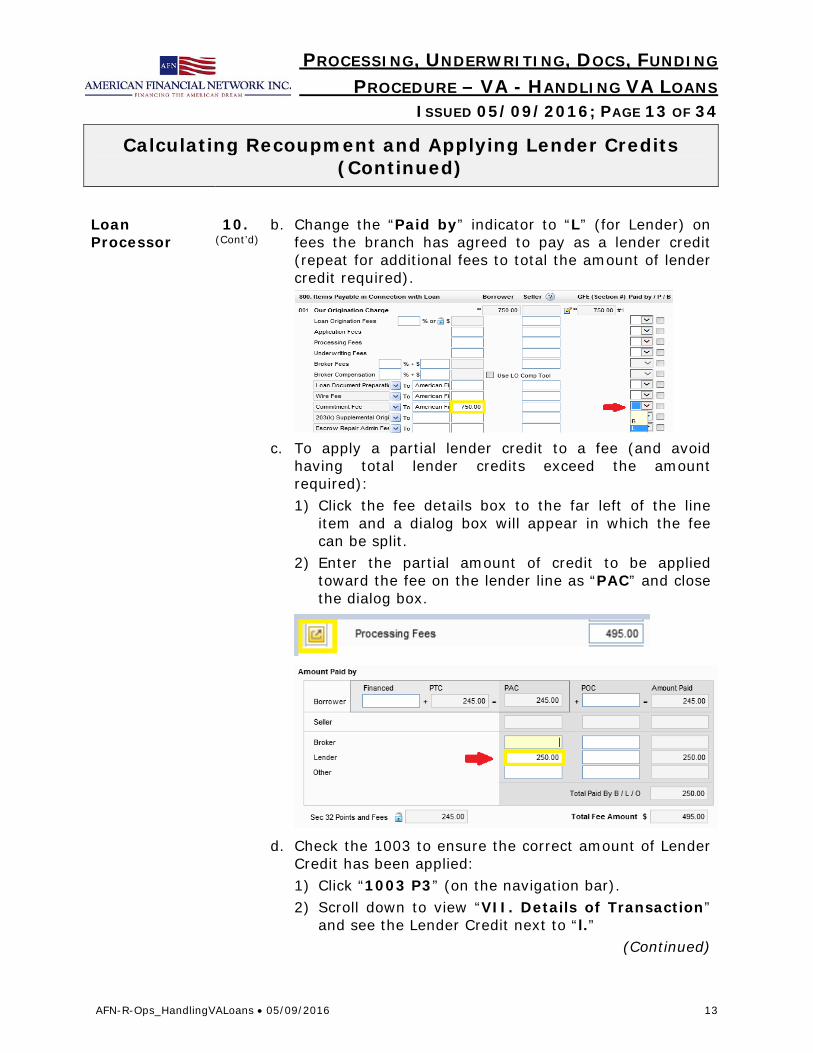

b. Change the “Paid by” indicator to “L” (for Lender) on fees the branch has agreed to pay as a lender credit (repeat for additional fees to total the amount of lender credit required).

c. To apply a partial lender credit to a fee (and avoid

having total lender credits exceed the amount required): 1) Click the fee details box to the far left of the line

item and a dialog box will appear in which the fee can be split.

2) Enter the partial amount of credit to be applied toward the fee on the lender line as “PAC” and close the dialog box.

d. Check the 1003 to ensure the correct amount of Lender

Credit has been applied: 1) Click “1003 P3” (on the navigation bar). 2) Scroll down to view “VII. Details of Transaction”

and see the Lender Credit next to “l.” (Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 14 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 14

Calculating Recoupment and Applying Lender Credits (Continued)

Loan Processor

10. (Cont’d)

e. For VA IRRRLs where a lump sum credit amount appears on line “l.” of Details of Transaction:

1) Remove the lump sum amount; and

2) Apply individually, as detailed in 10.a. – 10.c. above. f. If the loan is locked and a lender credit was applied to

the origination fee for the locked rate:

1) Review “CC paid by Broker, Lender, Oth.” on 1003 P3 under Details of Transaction; manually deduct the amount of the origination fee credit from the total Lender Credit; and

2) Get approval for the credit from the AFN Lock Desk for the difference.

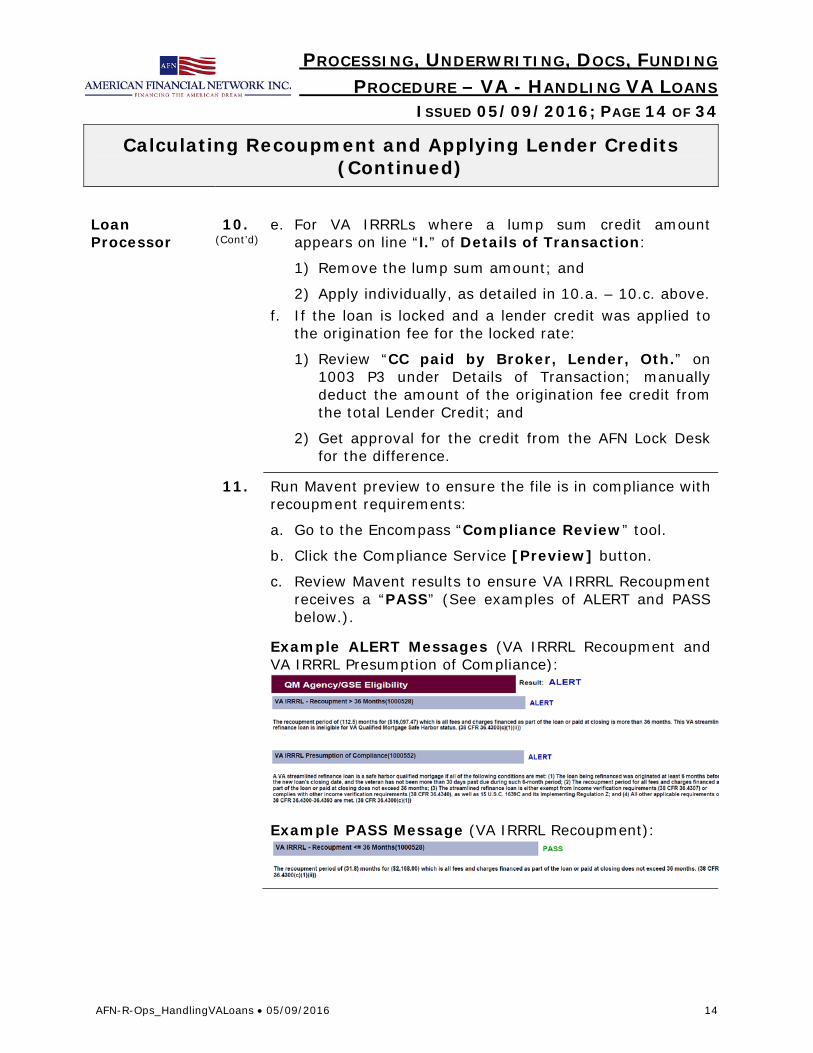

11. Run Mavent preview to ensure the file is in compliance with recoupment requirements:

a. Go to the Encompass “Compliance Review” tool.

b. Click the Compliance Service [Preview] button.

c. Review Mavent results to ensure VA IRRRL Recoupment receives a “PASS” (See examples of ALERT and PASS below.).

Example ALERT Messages (VA IRRRL Recoupment and VA IRRRL Presumption of Compliance):

Example PASS Message (VA IRRRL Recoupment):

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 15 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 15

Receiving VA Appraisals/NOVs

Loan Processor

12. If the VA appraisal is received after conditional loan approval, notify the file Underwriter as soon as possible (the appraisal must be reviewed by the SAR within 5 business days, so it is crucial that Underwriting is informed of receipt of a VA appraisal as soon as possible).

a. Upon SAR review of the appraisal, and issuance of a signed NOV by the Underwriter (which will be placed in the eFolder by the Underwriter) an automated email notification will be received; deliver the NOV and appraisal to the borrower.

b. Review all conditions on the NOV (which Underwriting should list on the conditional approval as well), and request any items needed for final approval.

c. Confirm all conditions have been met per the NOV; address any incomplete items with the Underwriter.

d. Upload all conditions of the NOV to the eFolder and attach conditions following normal protocol so the Underwriter can clear these items at the time of PTD Review.

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 16 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 16

Reviewing VA Loans

Underwriter Note Complete steps in this procedure that are marked

“Underwriter,” in addition to customary steps for all loans.

13. Review data entered by the Loan Processor for accuracy and completeness (per Steps 4 and 5 of this procedure).

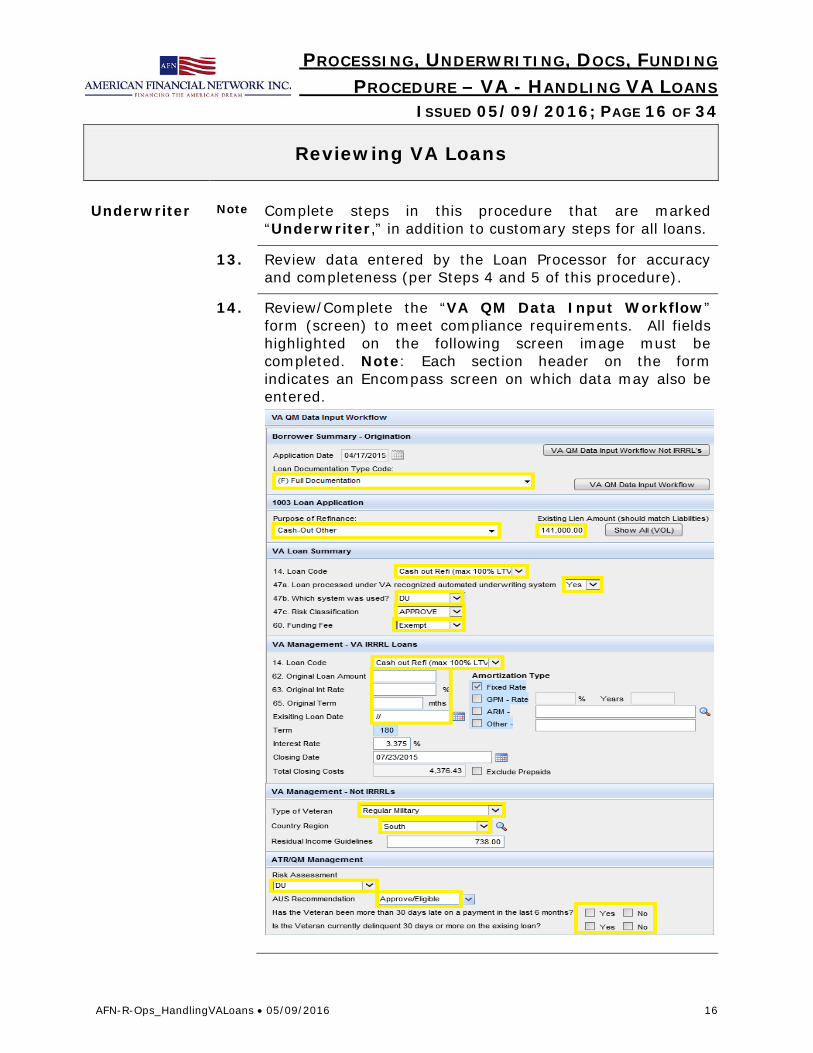

14. Review/Complete the “VA QM Data Input Workflow” form (screen) to meet compliance requirements. All fields highlighted on the following screen image must be completed. Note: Each section header on the form indicates an Encompass screen on which data may also be entered.

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 17 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 17

Reviewing VA Loans (Continued)

Underwriter 15. Check the VA Funding Fee for accuracy:

a. Go to the “VA Management” form (screen). b. Click the edit icon next to the “VA Funding Fee Amount”

field; the Fee Calculation dialog box will appear. c. Click the [Get MI] button and Encompass will refresh/

update the VA Funding Fee information. Note: The VA Funding Fee table in Step 4.d. of this procedure, (also online) shows applicable fee percentages (unless the Veteran is exempt). www.benefits.va.gov/homeloans/documents/docs/funding_fee_table.pdf

Important: The funding fee percentage for a purchase will change based on the down payment amount, which affects LTV. Ensure the percentage is correct after updating the VA Funding Fee Amount. Reduced fees only apply to purchases where a down payment of at least 5% is made; there are no reduced funding fees for regular refinances that are based on equity.

16. Use the navigation bar on the VA Management page to go to the Itemization screen and review fees and credits entered by the Loan Processor for accuracy (see Steps 6—11 of this procedure). If there is a Mavent fail or alert for fees/recoupment as relates to VA restrictions, condition the file, instructing the Processor to make all necessary adjustments prior to PTD Review.

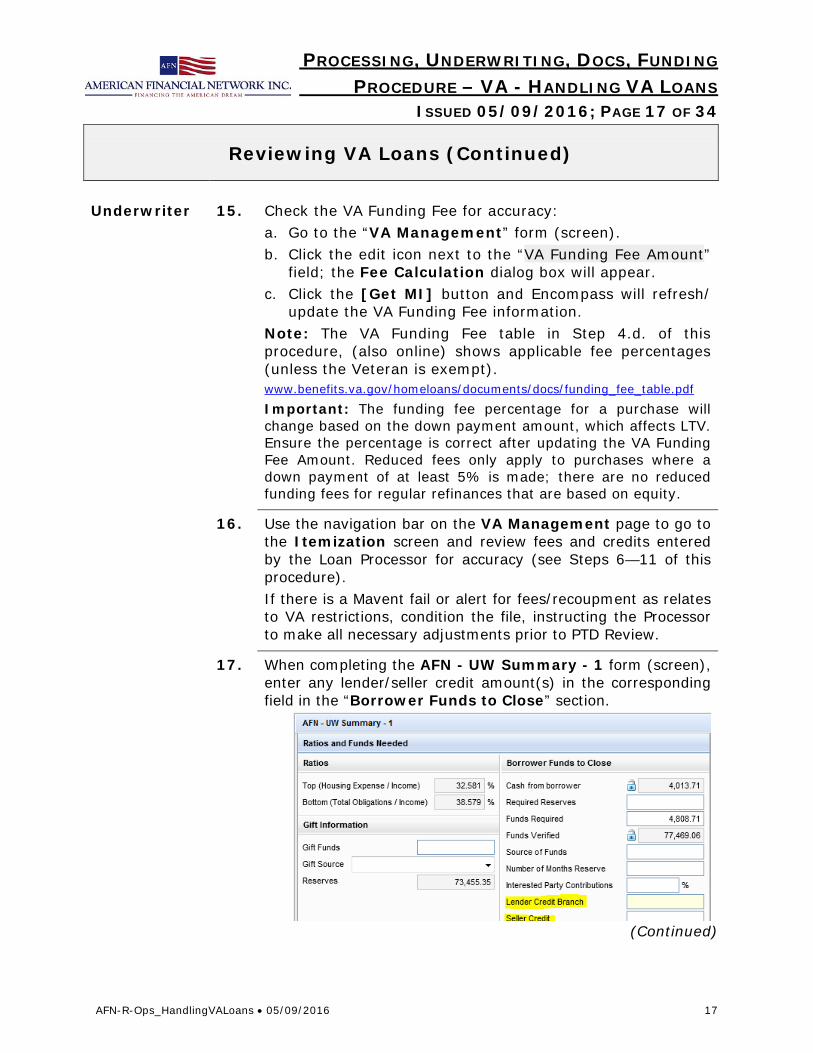

17. When completing the AFN - UW Summary - 1 form (screen), enter any lender/seller credit amount(s) in the corresponding field in the “Borrower Funds to Close” section.

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 18 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 18

Reviewing VA Loans (Continued)

Underwriter 17. (Cont’d)

Note: This is an important step to be completed prior to completing the PTD Review milestone, as it will trigger an alert for the Funder to itemize credits prior to funding.

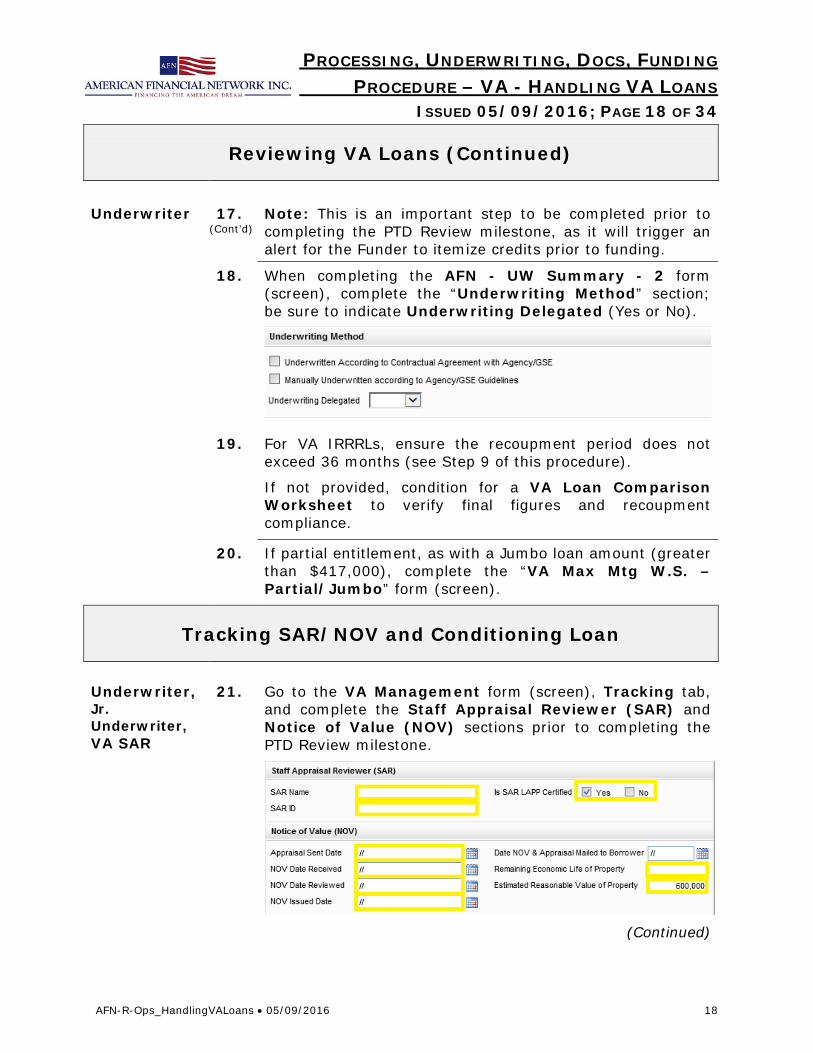

18. When completing the AFN - UW Summary - 2 form (screen), complete the “Underwriting Method” section; be sure to indicate Underwriting Delegated (Yes or No).

19. For VA IRRRLs, ensure the recoupment period does not exceed 36 months (see Step 9 of this procedure).

If not provided, condition for a VA Loan Comparison Worksheet to verify final figures and recoupment compliance.

20. If partial entitlement, as with a Jumbo loan amount (greater than $417,000), complete the “VA Max Mtg W.S. – Partial/Jumbo” form (screen).

Tracking SAR/NOV and Conditioning Loan

Underwriter, Jr. Underwriter, VA SAR

21. Go to the VA Management form (screen), Tracking tab, and complete the Staff Appraisal Reviewer (SAR) and Notice of Value (NOV) sections prior to completing the PTD Review milestone.

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 19 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 19

Tracking SAR/NOV and Conditioning Loan (Continued)

Underwriter, Jr. Underwriter, VA SAR

21. (Cont’d)

a. Jr. Underwriter: 1) Enter the Appraisal Sent Date as the date the

appraisal was received in the VA Portal. 2) Enter the NOV Date Received as the date the loan

was assigned to a VA SAR to review and issue the NOV. b. VA SAR:

1) Enter the NOV Date Reviewed as the date the appraisal was reviewed.

2) Enter the NOV Date Issued as the date the NOV is issued, unless suspended for NOV conditions.

3) Review any conditions required to issue the NOV as received; if requirements met, issue NOV and complete the NOV Date Issued field.

4) Upload the NOV to the Encompass eFolder under “Property - VA Notice of Value.”

c. Underwriter: Review the NOV; itemize any conditions required by the NOV on the conditional loan approval to notify all parties of these requirements, and to prevent delays or mistakes at closing.

22. Ensure the file meets pest inspection requirements: a. For all states except AK, CO, ID, ME, MN, MT, ND, OR,

SD, WI and WY, condition for a satisfactory termite/pest inspection (IRRRLs excepted).

b. For AZ, CA, IL, IA, KS, MO, NE, NM and NV, the V.A. Regional Loan Center (RLC) requires the veteran to sign the termite clearance with the following verbiage: “I, the undersigned veteran, acknowledge receipt of a copy of the pest report at no expense to me.” (“at no expense to me” can be omitted on refinance transactions).

c. Regardless of state requirements, if appraisal indicates evidence of wood-destroying insect damage or an active infestation, condition for a termite/pest inspection.

23. For a PUD or Condominium, ensure that title meets V.A. requirements: a. Any homeowner association assessments must be

subordinate to the VA-guaranteed mortgage. b. Any condo project must be VA approved. (check online:

https://vip.vba.va.gov/portal/VBAH/VBAHome/condopudsearch)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 20 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 20

Completing VA 26-6393 Loan Analysis

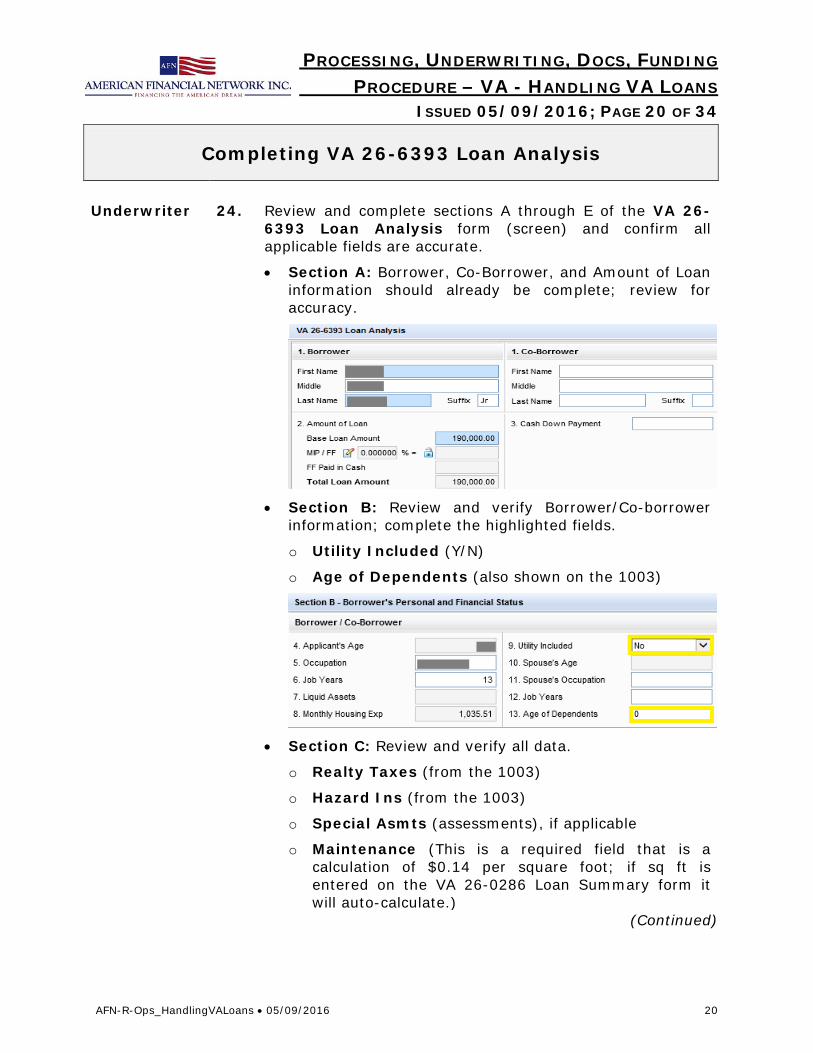

Underwriter 24. Review and complete sections A through E of the VA 26-

6393 Loan Analysis form (screen) and confirm all applicable fields are accurate.

• Section A: Borrower, Co-Borrower, and Amount of Loan information should already be complete; review for accuracy.

• Section B: Review and verify Borrower/Co-borrower

information; complete the highlighted fields.

o Utility Included (Y/N)

o Age of Dependents (also shown on the 1003)

• Section C: Review and verify all data.

o Realty Taxes (from the 1003)

o Hazard Ins (from the 1003)

o Special Asmts (assessments), if applicable

o Maintenance (This is a required field that is a calculation of $0.14 per square foot; if sq ft is entered on the VA 26-0286 Loan Summary form it will auto-calculate.)

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 21 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 21

Completing VA 26-6393 Loan Analysis (Continued)

Underwriter 24.

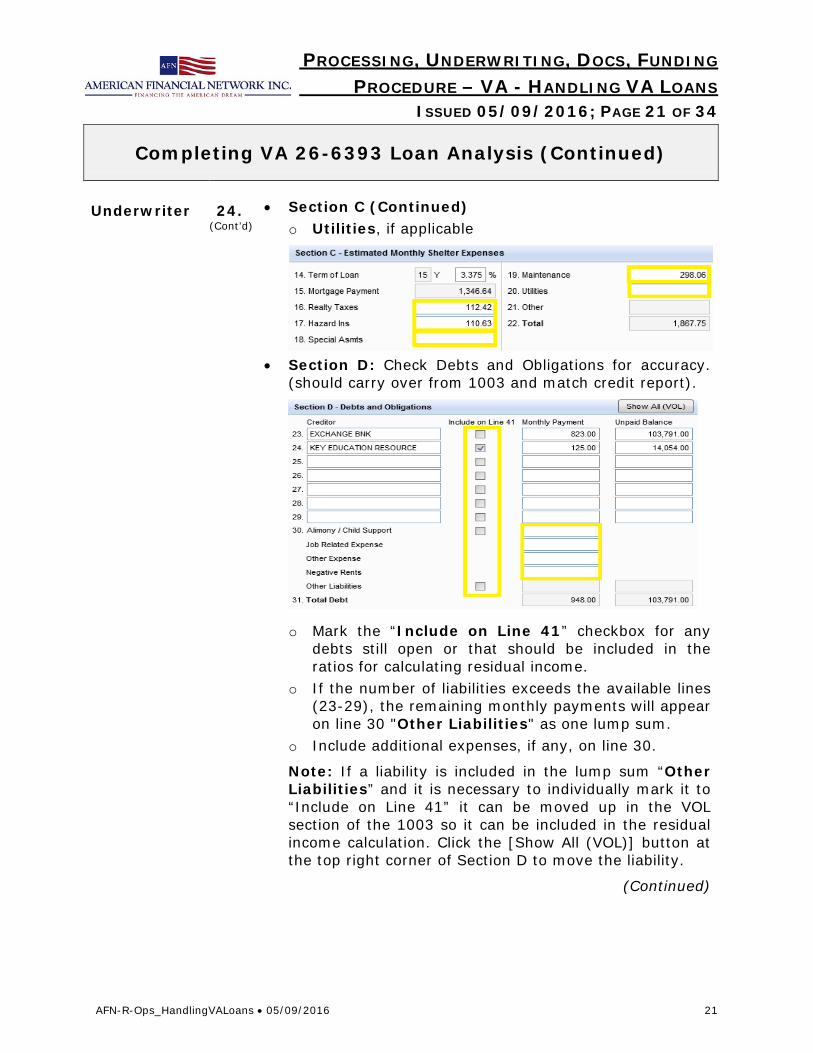

(Cont’d) • Section C (Continued)

o Utilities, if applicable

• Section D: Check Debts and Obligations for accuracy.

(should carry over from 1003 and match credit report).

o Mark the “Include on Line 41” checkbox for any debts still open or that should be included in the ratios for calculating residual income.

o If the number of liabilities exceeds the available lines (23-29), the remaining monthly payments will appear on line 30 "Other Liabilities" as one lump sum.

o Include additional expenses, if any, on line 30.

Note: If a liability is included in the lump sum “Other Liabilities” and it is necessary to individually mark it to “Include on Line 41” it can be moved up in the VOL section of the 1003 so it can be included in the residual income calculation. Click the [Show All (VOL)] button at the top right corner of Section D to move the liability.

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 22 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 22

Completing VA 26-6393 Loan Analysis (Continued)

Underwriter 24.

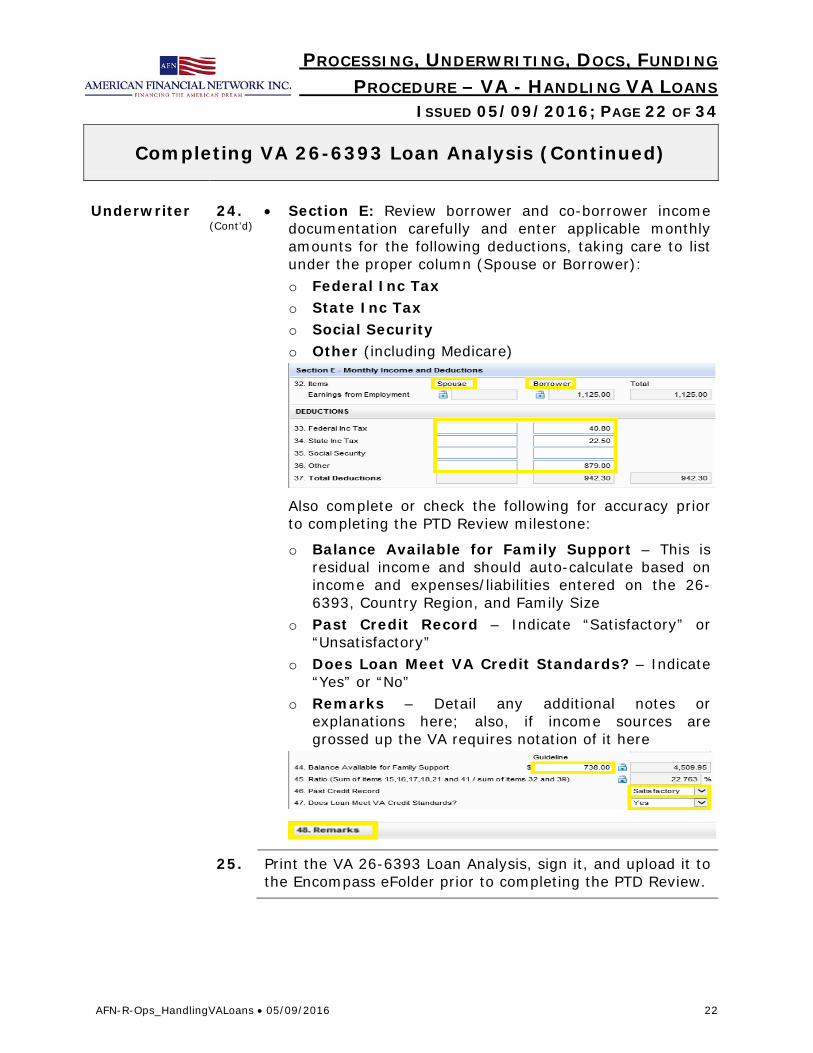

(Cont’d) • Section E: Review borrower and co-borrower income

documentation carefully and enter applicable monthly amounts for the following deductions, taking care to list under the proper column (Spouse or Borrower): o Federal Inc Tax o State Inc Tax o Social Security o Other (including Medicare)

Also complete or check the following for accuracy prior to completing the PTD Review milestone:

o Balance Available for Family Support – This is residual income and should auto-calculate based on income and expenses/liabilities entered on the 26-6393, Country Region, and Family Size

o Past Credit Record – Indicate “Satisfactory” or “Unsatisfactory”

o Does Loan Meet VA Credit Standards? – Indicate “Yes” or “No”

o Remarks – Detail any additional notes or explanations here; also, if income sources are grossed up the VA requires notation of it here

25. Print the VA 26-6393 Loan Analysis, sign it, and upload it to the Encompass eFolder prior to completing the PTD Review.

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 23 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 23

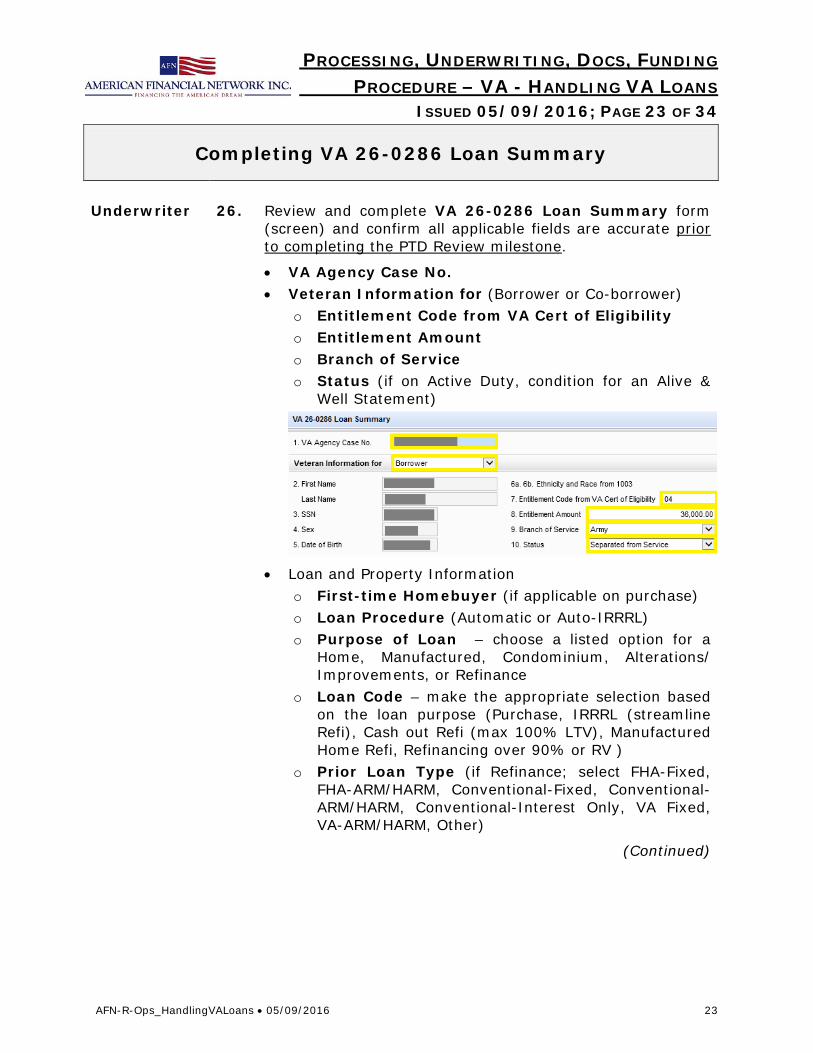

Completing VA 26-0286 Loan Summary

Underwriter 26. Review and complete VA 26-0286 Loan Summary form

(screen) and confirm all applicable fields are accurate prior to completing the PTD Review milestone.

• VA Agency Case No. • Veteran Information for (Borrower or Co-borrower)

o Entitlement Code from VA Cert of Eligibility o Entitlement Amount o Branch of Service o Status (if on Active Duty, condition for an Alive &

Well Statement)

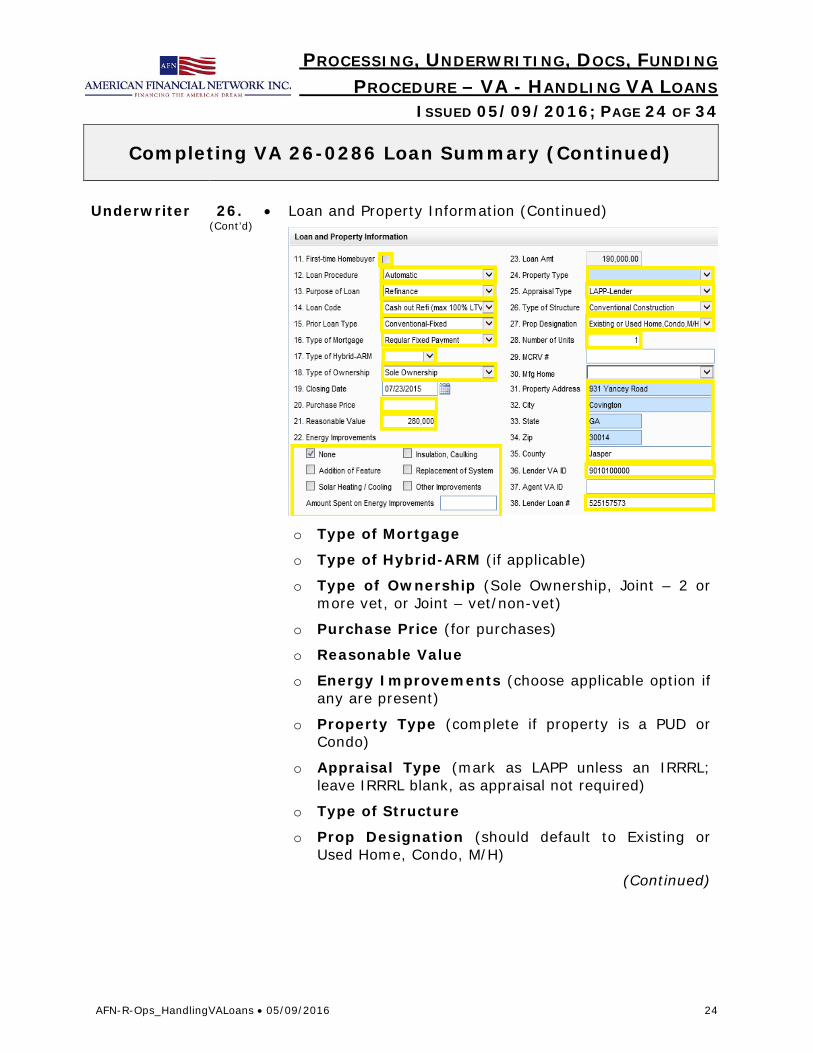

• Loan and Property Information

o First-time Homebuyer (if applicable on purchase) o Loan Procedure (Automatic or Auto-IRRRL) o Purpose of Loan – choose a listed option for a

Home, Manufactured, Condominium, Alterations/ Improvements, or Refinance

o Loan Code – make the appropriate selection based on the loan purpose (Purchase, IRRRL (streamline Refi), Cash out Refi (max 100% LTV), Manufactured Home Refi, Refinancing over 90% or RV )

o Prior Loan Type (if Refinance; select FHA-Fixed, FHA-ARM/HARM, Conventional-Fixed, Conventional-ARM/HARM, Conventional-Interest Only, VA Fixed, VA-ARM/HARM, Other)

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 24 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 24

Completing VA 26-0286 Loan Summary (Continued)

Underwriter 26.

(Cont’d) • Loan and Property Information (Continued)

o Type of Mortgage

o Type of Hybrid-ARM (if applicable)

o Type of Ownership (Sole Ownership, Joint – 2 or more vet, or Joint – vet/non-vet)

o Purchase Price (for purchases)

o Reasonable Value

o Energy Improvements (choose applicable option if any are present)

o Property Type (complete if property is a PUD or Condo)

o Appraisal Type (mark as LAPP unless an IRRRL; leave IRRRL blank, as appraisal not required)

o Type of Structure

o Prop Designation (should default to Existing or Used Home, Condo, M/H)

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 25 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 25

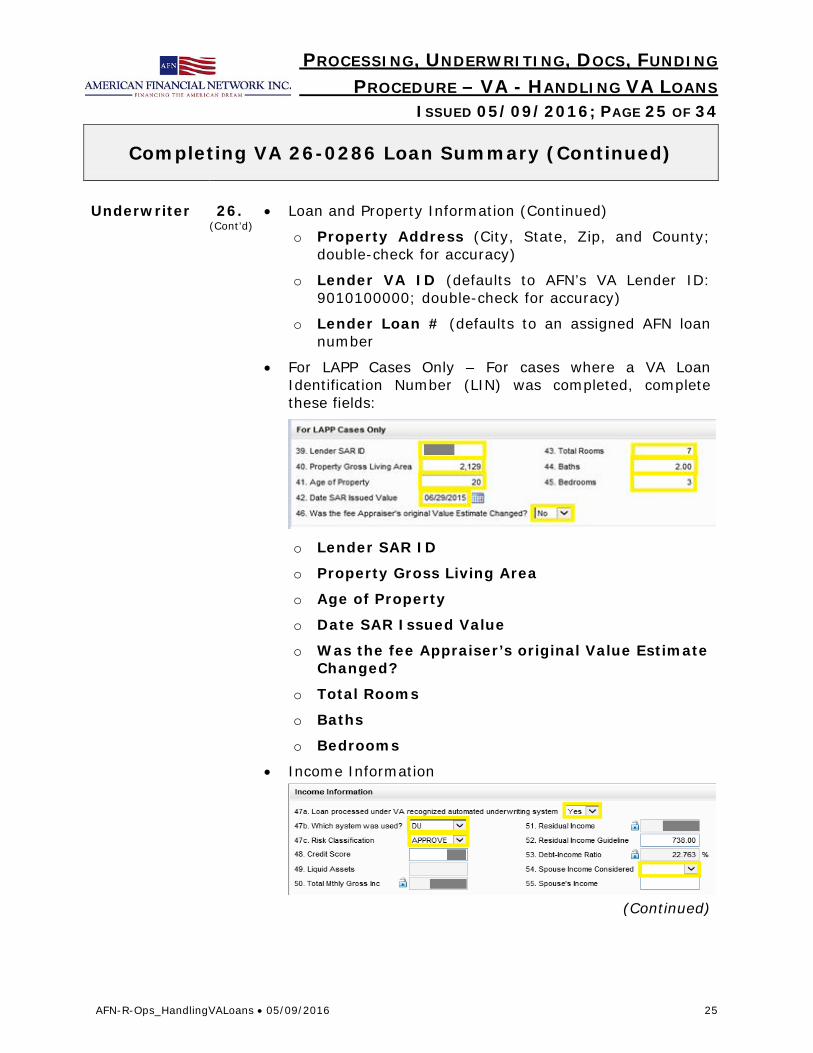

Completing VA 26-0286 Loan Summary (Continued)

Underwriter 26.

(Cont’d) • Loan and Property Information (Continued)

o Property Address (City, State, Zip, and County; double-check for accuracy)

o Lender VA ID (defaults to AFN’s VA Lender ID: 9010100000; double-check for accuracy)

o Lender Loan # (defaults to an assigned AFN loan number

• For LAPP Cases Only – For cases where a VA Loan Identification Number (LIN) was completed, complete these fields:

o Lender SAR ID

o Property Gross Living Area

o Age of Property

o Date SAR Issued Value

o Was the fee Appraiser’s original Value Estimate Changed?

o Total Rooms

o Baths

o Bedrooms

• Income Information

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 26 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 26

Completing VA 26-0286 Loan Summary (Continued)

Underwriter 26.

(Cont’d) • Income Information (Continued) - For loans other than

IRRRLs, complete these fields:

o Loan processed under VA recognized automated underwriting system

o Which system was used? (if applicable)

o Risk Classification (if applicable)

o Spouse Income Considered

• Discount Information

o Funding Fee – verify funding fee status

• For IRRRLs Only

o Paid in Full VA Loan Number (from VA IRRRL case order)

o Original Loan Amount (check for accuracy)

o Original Int Rate (check for accuracy)

o Original Term (check for accuracy)

27. Print the VA 26-0286 Loan Summary, sign it, and upload it to the Encompass eFolder prior to completing the PTD Review milestone.

28. For non-IRRRLs, print, sign and date the VA Loan Quality Certification form and upload it to the Encompass eFolder. This form is available in the Encompass custom forms in the Underwriting folder.

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 27 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 27

Reviewing Fees and Credits

Doc Drawer Note Complete steps in this procedure that are marked “Doc

Drawer,” in addition to customary steps for all loans.

29. Before preparing loan documents, ensure the VA Funding Fee is accurately entered in Encompass. a. Check the “Certificate of Eligibility” to ensure the

veteran is not exempt from paying the funding fee. b. If veteran is not exempt, review the Loan Information

section of the Encompass “Doc Orders” form (screen), taking note of the following fields: • MIP/Funding/Guarantee (%) – verify against the

Certificate of Eligibility and fee percentage table* • MIP/Funding/Guarantee ($) – this will auto-

calculate based on the percentage • Amount Paid in Cash – if Underwriter approved

payment of the VA funding fee in cash, it must be reflected here; this entry must be made prior to adjusting MI (before clicking the “Get MI” button)

*Note: The VA Funding Fee table in Step 4.d. of this procedure, (also online) shows applicable fee percentages (unless the Veteran is exempt). www.benefits.va.gov/homeloans/documents/docs/funding_fee_table.pdf

Important: The funding fee percentage for a purchase will change based on the down payment amount, which affects LTV. Ensure the percentage is correct after updating the VA Funding Fee Amount. Reduced fees only apply to purchases where a down payment of at least 5% is made; there are no reduced funding fees for regular refinances that are based on equity.

30. Review the Closing Disclosure (CD) received from the settlement agent and check fees listed on the Itemization in Encompass for accuracy and compliance. a. The following are VA Allowable Fees (no VA-specific

restrictions or limitations on amounts charged): • Appraisal • Compliance Inspection (if required by NOV) • Credit Report

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 28 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 28

Reviewing Fees and Credits (Continued)

Doc Drawer 30.

(Cont’d) • Recording Fees/Tax Stamps • Prorated Tax & Insurance Escrow • Hazard Insurance Premium (invoice required) • Survey • Title Insurance and title-related fees (policy, exam,

search, endorsement, preparation) • Environmental Protection Lien Endorsement • 1% Origination Fee (NOTE: AFN does not charge a 1%

origination fee in order to avoid predatory lending practices; instead, origination charges are itemized by specific fee names)

• VA Funding Fee • Discount Points • Closing Protection Letter • Well and Septic Inspection Fees

b. Ensure a combined total of all fees listed below (“Unallowable Fees”) does not exceed 1% of the loan amount. Note: Any amounts over 1% must be marked as lender paid and a credit must be approved by the Lock Desk (Branch Manager must request lender credit with the Encompass “Lender Credit Screen” under the Forms tab). An origination credit for rate may not be used to cover the difference over the 1% maximum; a separate lender credit would have to be requested and approved. • Settlement/Escrow/Closing Fee • Document Preparation • Underwriting • Processing • Application Fee • Attorney Fees (for other than title work) • Assignment Fee • Fax/Copy/Print Fees • Email/eDoc Fees • Postage Fees

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 29 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 29

Reviewing Fees and Credits (Continued)

Doc Drawer 30.

(Cont’d) • Notary/Signing Fee • Commitment Fee • Trustee Fee • Tax Service Fee

c. Ensure the following fees are NOT paid by the veteran, regardless of whether an origination fee, or total of the unallowable fees does not exceed 1%. • Termite/Pest Inspection • Attorney Fee (as a benefit to the Lender) • Mortgage Broker Fee • Realtor Commission • HUD/FHA Inspection Fees (for Builders)

d. Enter applicable credits; this will trigger a file alert for the Funder to complete the Closing Disclosure Itemization with all credit breakdowns prior to completing the Funding milestone.

Reminder: VA does not allow rate credits from pricing to be used as a credit for excessive allowable fees. Any credits required for exceeding the 1% allowed by VA for “Unallowable” fees must be a separate lender credit and must be approved by the AFN Lock Desk prior to drawing/ releasing loan documents.

31. Go to the Encompass Compliance Review tool and review the Mavent report to ensure there are no fee violations present in the fee/credit calculations. Resolve any FAILS or ALERTS prior to preparing and releasing loan documents.

See examples of FAIL and PASS on the following page. Note that in both examples a breakdown of the 1% fees is available in the “Enterprise Rules” section of the Mavent report.

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 30 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 30

Reviewing Fees and Credits (Continued)

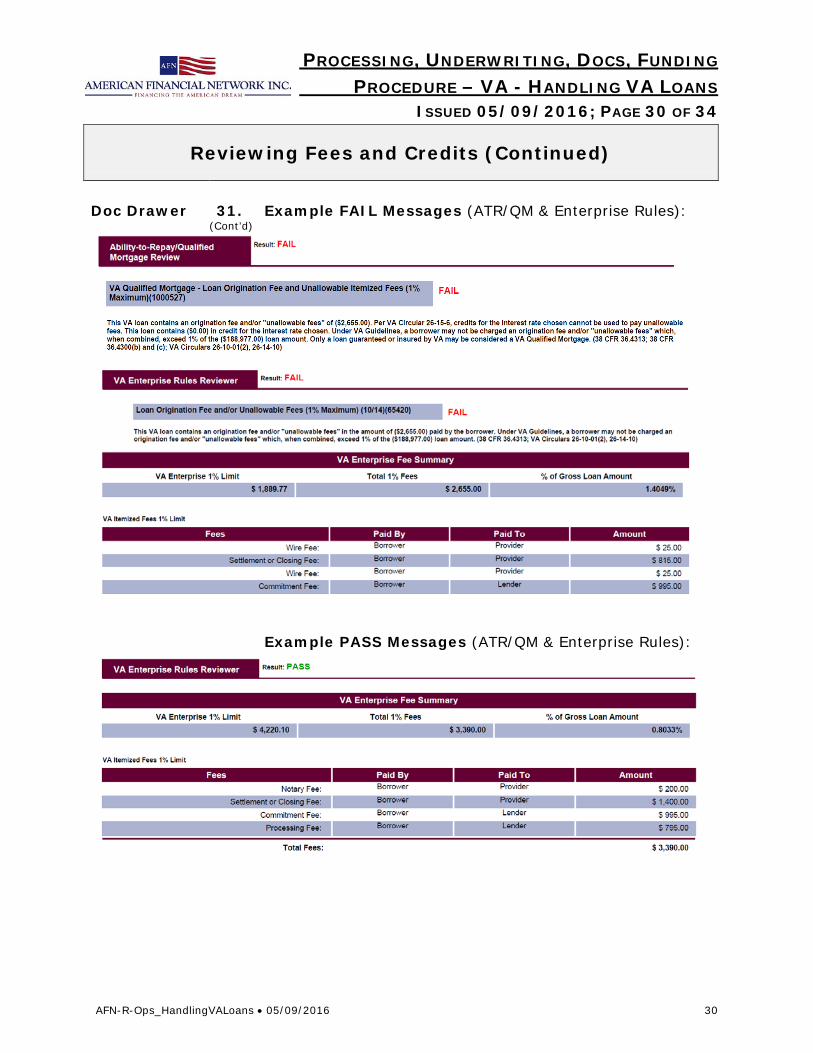

Doc Drawer 31.

(Cont’d) Example FAIL Messages (ATR/QM & Enterprise Rules):

Example PASS Messages (ATR/QM & Enterprise Rules):

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 31 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 31

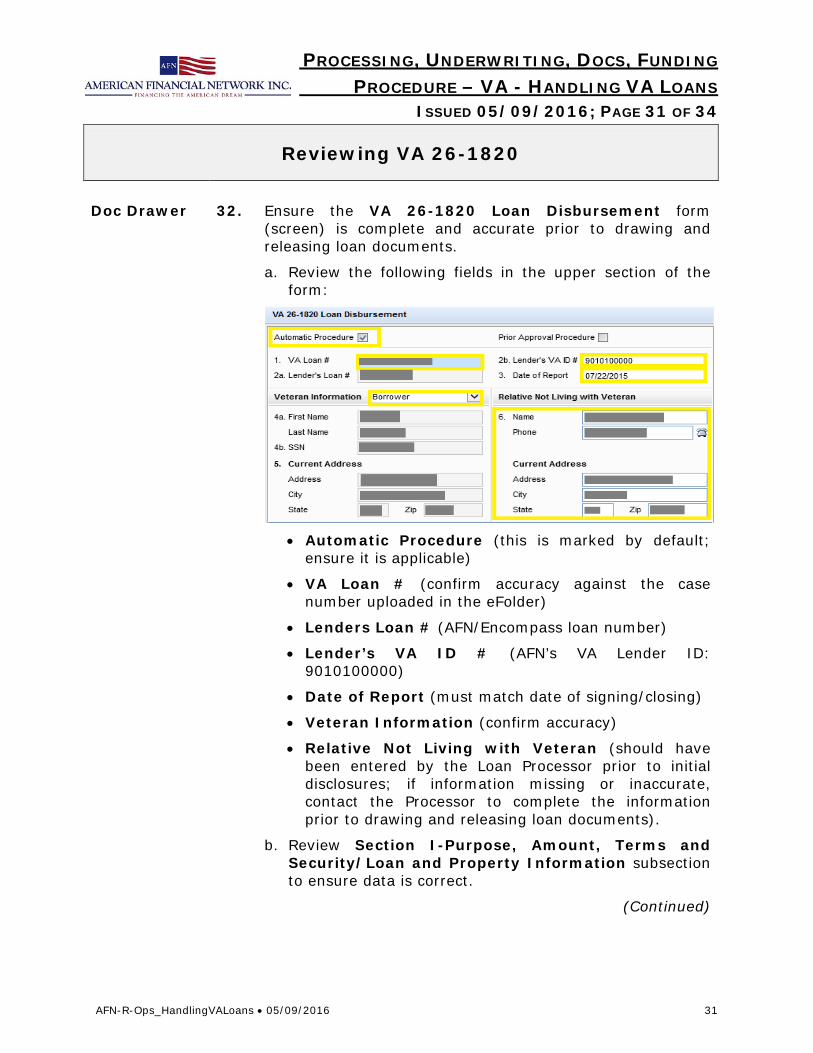

Reviewing VA 26-1820

Doc Drawer 32. Ensure the VA 26-1820 Loan Disbursement form

(screen) is complete and accurate prior to drawing and releasing loan documents.

a. Review the following fields in the upper section of the form:

• Automatic Procedure (this is marked by default;

ensure it is applicable)

• VA Loan # (confirm accuracy against the case number uploaded in the eFolder)

• Lenders Loan # (AFN/Encompass loan number)

• Lender’s VA ID # (AFN’s VA Lender ID: 9010100000)

• Date of Report (must match date of signing/closing)

• Veteran Information (confirm accuracy)

• Relative Not Living with Veteran (should have been entered by the Loan Processor prior to initial disclosures; if information missing or inaccurate, contact the Processor to complete the information prior to drawing and releasing loan documents).

b. Review Section I-Purpose, Amount, Terms and Security/Loan and Property Information subsection to ensure data is correct.

(Continued)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 32 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 32

Reviewing VA 26-1820 (Continued)

Doc Drawer 32.

(Cont’d) c. Review/complete Section I-Purpose, Amount, Terms

and Security, items 10.-23, paying close attention to the following fields.

• Date of Note

• Date of 1st Payment

• Closing Date

• Disbursement Date

• Title of Property is Vested in

• Estate in Property is (verify against title work)

• Annual Real Estate Taxes (based on prelim or tax cert)

• Hazard Face Amount (based on Coverage A amount listed on hazard policy)

• Flood Face Amount (if flood insurance is required, enter based on coverage amount listed on the flood policy)

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 33 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 33

Reviewing Loan Documents

Funding Assistant

Note Complete steps in this procedure that are marked “Funding Assistant,” in addition to customary steps for all loans.

33. Verify all required documents, including VA-specific forms, are present and fully executed. This includes and is not limited to the following forms, which must be signed by the veteran and an AFN representative: • VA 26-1820 Loan Disbursement • VA 26-1802a Addendum (final)

34. Upload documents to the Encompass eFolder as follows: • VA 26-1820 Loan Disbursement – file in the “Closing –

VA Form 1820” placeholder • VA 26-1802a – file in the “Gen – 92900 A or 26-1802a

(final)” placeholder • Move any unsigned pages to the “Trash” folder

Reviewing Prior to Disbursement

Funder Note Complete steps in this procedure that are marked

“Funder,” in addition to customary steps for all loans.

35. Review the file in accordance with standard procedures for reviewing final conditions, preparing funding figures, and preparing the wire; include the following VA-specific steps: a. Confirm all conditions have been met per the NOV;

address any incomplete items with the Underwriter. b. When signing off the termite clearance, ensure any loan

for a property in AZ, CA, IL, IA, KS, MO, NE, NM, or NV includes the following verbiage: “I, the undersigned veteran, acknowledge receipt of a copy of the report at no expense to me.” (The “at no expense to me” phrase can be omitted on refinance transactions.)

c. Confirm the termite inspection fee is not charged to the veteran.

d. Check fees and any lender credits for accuracy (see Steps 6—11 of this procedure for instructions).

PROCESSING, UNDERWRITING, DOCS, FUNDING PROCEDURE – VA - HANDLING VA LOANS

ISSUED 05/09/2016; PAGE 34 OF 34

AFN-R-Ops_HandlingVALoans • 05/09/2016 34

Reviewing Prior to Disbursement (Continued)

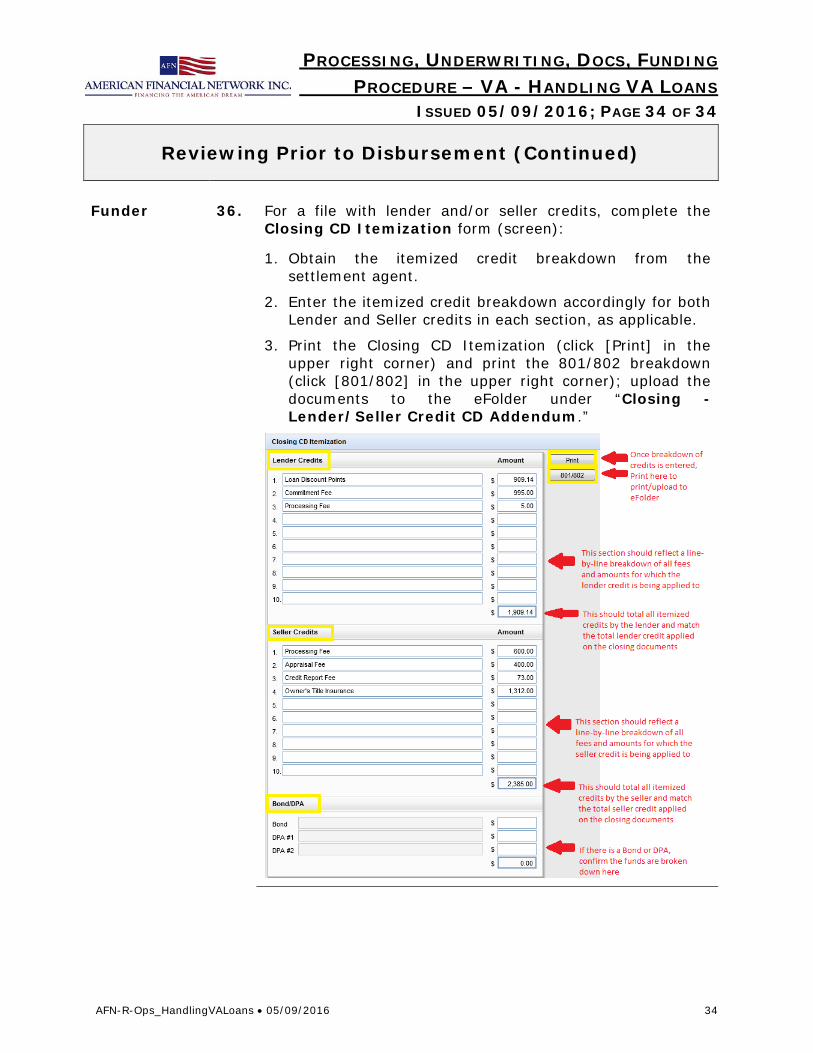

Funder 36. For a file with lender and/or seller credits, complete the

Closing CD Itemization form (screen):

1. Obtain the itemized credit breakdown from the settlement agent.

2. Enter the itemized credit breakdown accordingly for both Lender and Seller credits in each section, as applicable.

3. Print the Closing CD Itemization (click [Print] in the upper right corner) and print the 801/802 breakdown (click [801/802] in the upper right corner); upload the documents to the eFolder under “Closing - Lender/Seller Credit CD Addendum.”