plg trb workshop cbr v gb 010915 final

TRANSCRIPT

Logistics Engineering Supply Chain

Moving Crude Oil By Rail

Graham BrisbenCEO

PLG Consulting

January 11, 2015

2

Boutique consulting firm with team members throughout North America

Established in 2001

Over 100 clients and 250 engagements

Practice Areas Logistics

Engineering

Supply Chain

Consulting services Strategy & optimization

Logistics assets & infrastructure development

Supply Chain design & operationalization

M&A/investments/private equity

Industry verticals Energy

Bulk commodities

Freight rail

Institutional investors and private equity

About PLG Consulting

Moving Crude Oil By Rail

Partial Client List

3

Deep rail industry experience

• Operational

• Commercial

• Design & engineering

• Equipment market

Broad CBR industry client experience over

past four years

• E&P companies

• Refiners

• Terminal developers

• Investors – private equity, hedge funds,

investment banks

• Government agencies, industry trade groups

• Equipment leasing

PLG’s Crude By Rail Industry Qualifications

Moving Crude Oil By Rail

Diverse projects• CBR supply chain optimization

• Rail commercial negotiations

• Rail car acquisition – commercial & technical inspection

• Comprehensive design & engineering – rail, marine, tankage, product handling, and related facilities

• EH&S training

• Investment advising

• Industry’s only long term, CBR volume forecast with complimentary rail tank car forecast

Recognized industry thought leader on CBR and tank car markets

• Numerous industry presentations, articles and advising

4

ssSource: CAPP, About Oil Sands

Source: EIA, May 2014

US Shale

Unconventional Energy Resources and Extraction Technologies

Moving Crude Oil By Rail

Western Canadian (WC)

Oil Sands

Source: www.epmag.com

SAGDHorizontal Drilling & Hydraulic Fracturing

Source: Marathon, February 2014

“Moore’s Law” at play:

Exponential advances in technology, resulting in

Declining costs

Surging production

5

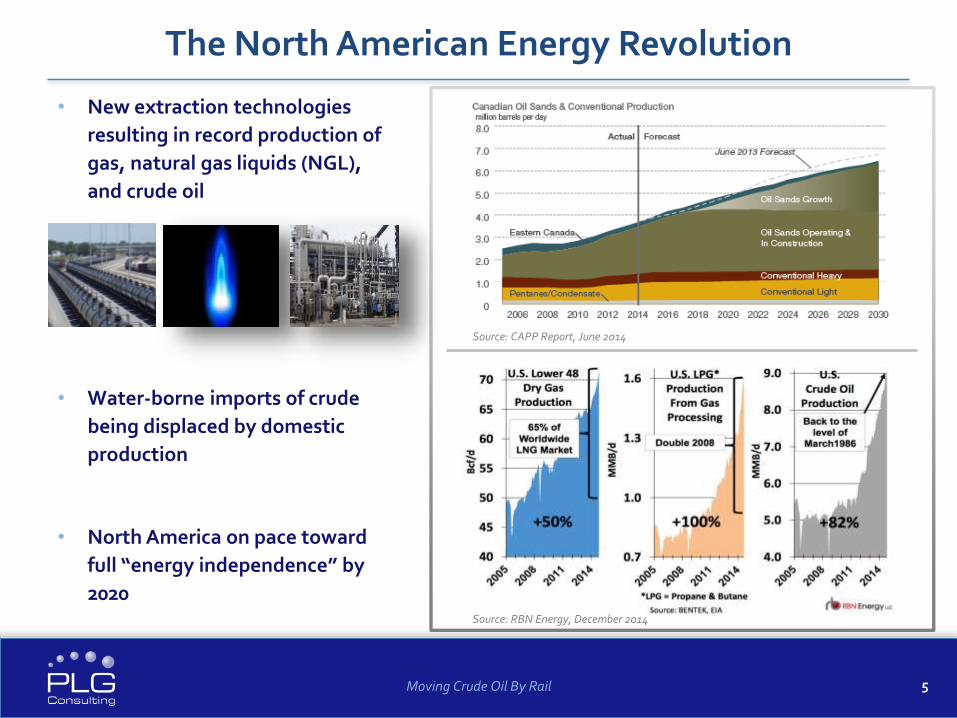

• New extraction technologies

resulting in record production of

gas, natural gas liquids (NGL),

and crude oil

• Water-borne imports of crude

being displaced by domestic

production

• North America on pace toward

full “energy independence” by

2020

The North American Energy Revolution

Moving Crude Oil By Rail

Source: CAPP Report, June 2014

Source: RBN Energy, December 2014

6

Shale Supply Chain and Downstream Impacts

Feedstock (Ethane)

Byproduct (Condensate)

Home Heating (Propane)

Other Fuels

Other Fuels

Gasoline

Gas

NGLs

Crude

Proppants

OCTG

Chemicals

Water

Cement

Generation

Process Feedstocks

All Manufacturing

Steel

Fertilizer (Ammonia)

Methanol

Chemicals

Petroleum Products

Petro-chemicals

Inputs Wellhead Direct

Output Thermal Fuels Raw Materials

Downstream Products

Moving Crude Oil By Rail

Impacts to-date include: Dramatic reduction in crude imports,

lower electricity costs, lower gasoline prices, increased refined products exports

The next wave: Manufacturing renaissance in the US based on

abundant, low cost energy and feedstocks

7

Over $120B of New Shale-Related Manufacturing Investments Have Been Announced

Moving Crude Oil By Rail

Ethylene and Propylene

Ammonia and Derivatives

Methanol

Polymers and Resins

Chlor-alkali

OtherSource: American Chemistry Council and PLG analysis

8

NA Crude Logistics Pre-2010

Moving Crude Oil By Rail

Sources: EIA, PLG analysis (Google Earth)

Light/Sweet

Heavy/Sour

Pacific Northwest Refiners

California Refiners

2,525kbpd

PADD VDemand

Midwest Refiners

3,375kbpd

PADD II Demand

East Coast Refiners

PADD I Demand1,075kbpd

LA Gulf Coast Refiners

TX Gulf Coast Refiners

PADD III Demand

8,150kbpd

Permian

ANS

Imports

Imports

Rail

Pipeline

Marine

Oil Sands

Imports GOM

9

NA Crude Logistics Today

Moving Crude Oil By Rail

Sources: EIA, PLG analysis (Google Earth)

Light/Sweet

Heavy/Sour

Pacific Northwest Refiners

California Refiners

2,525kbpd

PADD VDemand

Midwest Refiners

3,375kbpd

PADD II Demand

East Coast Refiners

PADD I Demand1,075kbpd

LA Gulf Coast Refiners

TX Gulf Coast Refiners

PADD III Demand8,150

kbpd

Eagle Ford

Permian

Bakken

Rail

Pipeline

Marine

Oil Sands

GOM

10

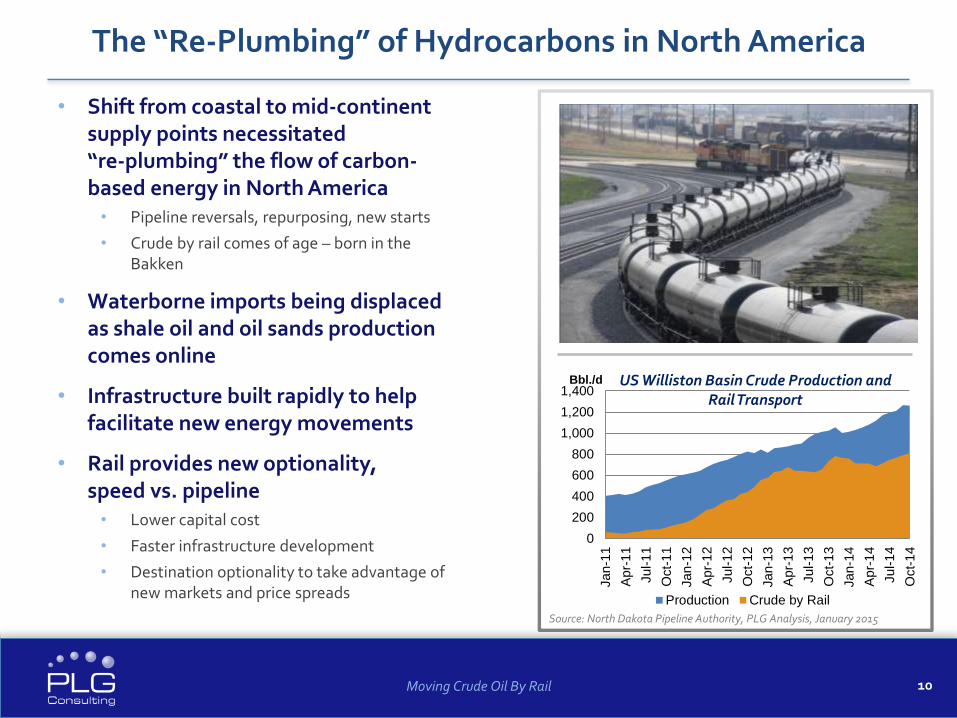

• Shift from coastal to mid-continent supply points necessitated “re-plumbing” the flow of carbon-based energy in North America• Pipeline reversals, repurposing, new starts

• Crude by rail comes of age – born in the Bakken

• Waterborne imports being displaced as shale oil and oil sands production comes online

• Infrastructure built rapidly to help facilitate new energy movements

• Rail provides new optionality, speed vs. pipeline• Lower capital cost

• Faster infrastructure development

• Destination optionality to take advantage of new markets and price spreads

The “Re-Plumbing” of Hydrocarbons in North America

Moving Crude Oil By Rail

0

200

400

600

800

1,000

1,200

1,400

Jan-1

1

Apr-

11

Jul-1

1

Oct-

11

Jan-1

2

Apr-

12

Jul-1

2

Oct-

12

Jan-1

3

Apr-

13

Jul-1

3

Oct-

13

Jan-1

4

Apr-

14

Jul-1

4

Oct-

14

Bbl./d US Williston Basin Crude Production and Rail Transport

Production Crude by Rail

Source: North Dakota Pipeline Authority, PLG Analysis, January 2015

11

The Three Phases of Crude-by-Rail Growth in North America

Moving Crude Oil By Rail

0

200

400

600

800

1,000

1,200

US CrudeOriginations

Williston CrudeOriginations

Source: NDPA, STB, PLG

Analysis, January 2015

Crude by Rail Volumes (kbpd)

2009-2011

• CBR developed from the Bakken to bridge the gap until pipelines are built

• First unit train shipment in Dec. 2009

• Destination market: Cushing, OK WTI trading hub

2011-2013

• Ascendancy of trading as main growth driver in CBR; WTI-Brent-LLS differentials are key

• St. James, LA LLS hub becomes most attractive destination

• Coastal refineries begin rail receipt infrastructure build-out

• Tank car market overheats, becomes main growth constraint

2013-current

• CBR from Bakken assumes long-term structural role in crude oil market

• Bakken CBR transitioning to east and west coast markets; LLS and WTI converge as Permian and Eagle Ford growth floods USGC

• Canadian CBR build-out begins; tank car market reorienting to coiled/insulated car types (~2/3 of CBR fleet order backlog)

12

Low Oil Price Case North American CBR Forecast Overview

Moving Crude Oil By Rail

Bakken & Oil Sands are main drivers of

CBR volumes, accounting for ~87% of NA

movements in 2017

Other plays such as Niobrara and

Permian are seeing increasing CBR

activity but will be adequately

served by pipelines long-term

0

100

200

300

400

500

600

700

800

900

1,000

2013 2014 2015 2016 2017 2018 2019

Low ($<65/bbl) Case Crude by Rail Volumes (kbpd)

Williston

Oil Sands

Niobrara

Permian

Source: PLG Crude by

Rail & Tank Car

Forecast, Nov. 2014

13

Low Oil Price Case: Bakken Production and Takeaway

Moving Crude Oil By Rail

0

200

400

600

800

1,000

1,200

1,400

2014 2015 2016 2017 2018 2019

Low Case ($<65/bbl) Takeaway (kbpd)

Pipeline Forecast

Crude by Rail Forecast

Local Refinery Forecast

CBR share of production expected to be remain strong and long lasting due to the optionality it provides and the lack of pipeline options to the key markets on West and East Coast

Source: PLG Crude by

Rail & Tank Car

Forecast, Nov. 2014

14

Low Oil Price Case: Western Canada Production and Takeaway

Moving Crude Oil By Rail

Proportion of production handled by rail expected to ramp up through 2017 and then drop back as pipeline

capacity starts to develop

At its peak in 2017, rail will handle ~ 18% of production and

then fall back to ~ 6% by 2019

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2014 2015 2016 2017 2018 2019

Low Case ($<65/bbl) Takeaway (kbpd)

Pipeline Forecast

Crude by Rail Forecast

Local Refinery Forecast

Source: PLG Crude by

Rail & Tank Car

Forecast, Nov. 2014

Logistics Engineering Supply Chain

Thank You !For follow up questions and information,

please contact:

Taylor Robinson, President+1 (508) 982-1319 / [email protected]

This presentation is available for download at:http://plgconsulting.com/category/presentations/