plastic money

TRANSCRIPT

INTRODUCTION

Plastic money is here, there & everywhere:

The concept of ‘Buy Now, Pay Later’ dates back the to late 1960s & 70s with the

introduction of plastic money in the western nations. It originated because the people

wanted a convenient and rapid means of accessing their bank accounts. Also, the

exorbitant price of money changing hands between the consumer, merchants and the

banks led to the diffusion of this concept in the banking system.

For spendthrifts and habitual borrowers plastic money induces spontaneous and on-the-

spur spending. But its advantages in terms of convenience, flexibility and safety far

outweigh its pitfalls. Provision for easy repayment gives the card the liquidity of cash

along with the accountability of credit card.

In the past 20 years these cards have proliferated the world market so successfully that

they have altered the face of retail banking. With the power of plastic ruling the world,

India cannot remain behind. With a slow and steady move towards scrip less trading the

country is moving towards cashless transactions.

The plastic money market is bubbling with activity with both Indian and foreign banks

vying to expand their market presence. While the foreign banks have been hogging the

limelight Indian banks are the slumbering giants. The latter have the advantage of a

1

large customer base, branch network along with low service charges. These

advantages need to be tapped to realize the full potential of these banks.

2

OBJECTIVE

The main purpose to serve on this topic under the Dissertation is to discover the

accurate dimensions of the Plastic Money.

As every project has its own specific purpose, my project is to: -

1) Find out that how the credit card may help in the development of an economy like

ours a developing economy.

2) Find out what is required to do for a credit card market and to establish credit card as

a special security tool.

3) Find out the reasons of fear in the mind of the customers during the acceptance of

the credit cards.

4) To understand the toughness of the credit card market due to emerging competition.

5) To know the credit cards procedure, documentation and the growth of credit cards in

Indian context.

6) To know the credit cards division of the Banking Industry very closely.

7) To understand the impact of credit cards in the purchasing power of consumers.

8) To determine whether consumers are aware of credit card and its advantages.

9) To determine the consumers acceptability and likeness towards credit card.

10) To find out the features, which attract consumers towards credit cards and the

parameters, they use to compare the credit cards.

3

CREDIT CARD AND ITS FUNCTIONS.

For starter, a credit card is as good as bank behind it. A form of 'near money' these

cards are issued by commercial bank to people whose creditworthiness has been

ascertained. Instead of carrying unmanageable weds of cash, the card holder enjoy the

flexibility and safety of purchasing any thing from groceries, cosmetics, petrol to high

value items like refrigerators, television, and washing machines by using his credit card.

Banks ask for TDS certificate or income tax returns document before enrolling a

member.

Credit Card provides the card holder with authorized line of credit of some specified

amount. Such cards may be used for following purposes:-

Purchase of air, rail and road tickets for traveling

For the Settlement of hotel bills.

For Cash withdrawals.

For the Settlement of club bills.

For the Payment of purchase bills.

For the Payment of insurance premium.

Refilling the fuels in vehicles.

Payment of phone, water and electricity bills.

Payment of school/ education expenses.

4

WHAT ARE CREDIT CARDS?

A Credit Card is referred to as 'plastic money'. Carrying a lot of cash on you can be

cumbersome, risky and sometimes, you run short of it, just when you most need it.

(Remember the SALE at your favorite ready-mades store?). A Credit card is the smart

solution to these problems. It is a convenient and safe alternative for cash.

Besides, it says things about you. Most people associate a credit card with a prestige,

which it most certainly bestows on you, but more importantly, it says that you have

taken the onus of being responsible - to be extended credit! So, when you get yourself a

card, remember that, because your bank does!

SALIENT FEATURES OF CREDIT CARDS

ANNUAL FEE

All credit card issuers charge an annual fee which is payable at the start of the year.

The start of the year, of course, is your membership year, and not the calendar year.

So, if you got yourself a card in March, you can expect to be billed the annual fee every

March until you cancel your card. As a privilege, this fee is sometimes waived the first

time. When the time comes for renewal of your card, you can even use the reward

points you have accumulated from using the credit card over the year to settle your

annual fee.

FORWARDING BALANCE (OR REVOLVING)

The most attractive feature of a credit card is that you need not pay off your dues in

whole. You can opt to pay 5% of the total amount on or before the due date, every

month, the rest is carried forward. But there's a price to pay for this extended credit -

interest! Normally, interest varies between 2.5% and 3% per month.

5

APR OR ANNUAL PERCENTAGE RATE

The interest rate that reflects the yearly cost of the interest the outstanding on your card

is called the annual percentage rate. This rate is charged to the card holder on the

amounts carried forward beyond the due date for the payment of balances. Most card

issuers will tell you their monthly rate of interest. It might sound low at 3%, but when you

look at the interest rate over the year, it turns out to be as high as 43%.

CASH ADVANCE

An important feature - lets you withdraw cash from designated ATMs using your credit

card. Use discretion when withdrawing cash on your credit card because the charges

for this facility are high, around 2.5% to 3% per transaction.

THE NECESSITY OF CREDIT CARDS

If it is for the convenience of not carrying cash then a debit card can suffice. And, if it is

for the free credit that the companies claim they give, then last week we had highlighted

6

the high cost of using such credit where the customer ends up paying more than 5 per

cent interest per month depending on the amount of credit due on the card.

For those who want to use the credit facility at a reasonable cost then we suggest that

they use facilities like overdraft against salary accounts or loan against fixed deposits or

shares. Rolling credit on the card is not feasible as the interest paid on credit cards is

phenomenally higher than what is charged on overdraft facilities.

Going a step further, in case you don't have the cash to pay off your credit card bill in

one month then it makes more sense to take an overdraft for that amount to repay the

bill because the interest on the overdraft works out far cheaper than what the card

company will levy on you if the payment is not made in time.

Almost all banks offer overdraft facilities at reasonable rates to customers who have

salary accounts with the said bank, as well as to the general public. Salary account

holders can avail of the overdraft without any collateral, which is called a clean

overdraft. For the general public, banks provide overdraft facilities against collateral like

NSCs, shares, fixed deposits, etc. For overdraft against salary accounts the rates being

quoted in the market are very competitive and are as low as 1% per month on a

reducing balance. Similarly, one can avail an overdraft facility against NSCs at 13% p.a.

and up to 65% of the face value or against fixed deposits at 9% p.a. up to 90% of the

value.

Then why should a customer pay 2.95% interest per month on an amount of Rs. 40,000

to a credit card company when he can pay 1% interest per month on the overdraft

against the salary account or 8.5% per annum for overdraft against fixed deposits?

ADVANTAGES OF HAVING A CREDIT CARD

1. If you pay by credit card there is implicit guarantee of satisfaction because as a

customer one can stop payment.

7

2. If a airline ticket is booked on a credit card and especially if you are going overseas,

the travel insurance is covered, that could otherwise be a lot of money.

3. Free airfare mileage based on point system that can take you or your family to a

destination of your choice if you can accumulate points. This is quite easy as the

shopping can be done on credit card and the points are accumulated that can be

encased for gifts or travel.

4. The best part is that you can get statement of all expenses and you can keep a track

of your expenses at a glance.

5. It helps to establish a credit history and can help in getting loan if needed.

6. There are a number of innovative credit cards that help benefit the customer. There

are cards that help accumulating points towards reducing the cost of your new car.

7. On internet it is the preferred option and you can also participate in on line auctions if

you have good credit rating.

8. You can get cash advance anywhere at so many cash outlets.

9. Some cards have your picture on it that is as good as a identification paper.

REASONS OF FEAR DURING ACCEPTANCE OF

PLASTIC MONEY

1. There is a temptation to acquire more and more cards. Some have more than their

share of cards. They can loose track of payments and be in difficulty.

8

2. Some credit cards have conditions that may put you in difficulty if you have not read

the fine print.

3. Then there is a danger of someone can get hold of your credit card number and

misuse it.

4. There are a number of cases of double dipping done at your expense when paying at

an outlet by credit card.

5. Static’s are available that the domestic violence increases after the festive season in

the credit card user societies when the credit card bills arrive.

6. Using credit card exposes one to the possibility of some companies profiling and

lobbying you based on your spending pattern. Some governments also take interest in

the spending patterns of individuals and credit card statements make their job easier.

There are always dangers when money matters are involved but one has to live with the

necessary evil. The happy are those credit card users that pay up and take advantage

of the free credit days that the credit card companies provide.

So being a good creation and instrument of financial market it is risky too, so there

are several things to be kept in mind and people should take in using it.

RISKS IN THE BUSINESS

TO THE BANKS:

9

Banks excited at the projected 40% growth rate1 in the plastic money industry are

apprehensive about the potential corresponding increase in fraud cases. Some banks

register upto 7% fraudulent case in a year.

1. Default in payments - Currently banks have huge amounts of funds blocked with

willful defaulters. Lack of reliable data / infrastructure to check the credit worthiness of

individuals has led to the situation where people without sufficient resources have

become eligible for availing credit facilities. The marketers in India find it more cost

effective to just right-off the unpaid amount in their balance sheets, after trying to

recover it for six months, than to pursue it throughout the litigation labyrinths.

2. Multiple Imprints or Record of Charge (ROC) Pumping - It refers to the expedient

system by which merchants make multiple charge slips instead of the relevant number

when a cardholder gives in his plastic card.

3. Lost/Stolen Cards - These account for 60% of fraud in India. In case of loss all

multinational banks and some Indian banks limit the liability of the cardholder upto Rs. 0

(for Gold card) and Rs. 1000 (for Classic card) if card is used after lost / stolen card has

been reported. These banks transfer their risks to insurance companies and generally

replace the lost card within three days. Some banks carry the risk themselves and

investigate the loss before determining the liability of cardholders. These banks take

about a month to replace the missing card.

To combat this, banks have started the Photo card Option which provides the

photograph of the cardholder on the card. They are also providing information about the

lost/stolen cards .

Through the Hot Card Bulletin which is continuously upgraded and sent to merchant

establishments to provide them with the current status. But the success of this measure

is debatable.

1

10

A majority of the credit card losses are skewed towards the issuer as the risk on the

cards is carried by the issuer. Visa and MasterCard have a formal set of guidelines

known as charge back rules. Once a card holder has informed the bank of the loss of

the card, he is subject only to a minimum liability, which most banks fix at Rs.1000

regardless of how much the card is used fraudulently. Before the hot card date, the

fraud loss is the issuer’s responsibility. However, if a merchant accepts a hot listed card,

the issuer is entitled to ‘charge back’ the transaction to the merchants, through the

acquirer. If a merchant is found guilty of willful fraud, his bank is liable.

Visa offers its members a national merchant alert service which acquiring banks can

refer to in order to check on the credentials of the merchants whose business they woo.

It also has its risk identification service which monitors every single transaction through

Visa Net. This enormous database helps zero in on cardholders and locations prone to

fraudulent activity.

Master Cards security and risk management team organizes regular training programs

for banks and member establishments on fraud prevention.

Delivering new cards to members by courier has drastically cut fraud arising from non-

receipt of cards.

TO CARD HOLDERS:

The main problem with credit card is that it is easy to get in over the head. A majority of

card users utilize their maximum limit. Credit cards charge higher interest than some of

the other forms of borrowing. While a credit card offers convenience, that convenience

can be expensive if the card holder is slow in paying off his outstanding dues. In terms

of the annual percentage rate that an individual is charged towards paying off his debt,

the figure ranges from anywhere between 22% to 34% p.a. depending upon the roll

over period ( 30 / 45 days ).Tocombatthese problems potential card owners decide

upon the mode of payment before selecting a card. In India, for the majority of people

who believe in paying off their balances in full, the prerequisites would include a card

with a low or no annual fee and long grace period

11

PARTIES INVOLVED IN CREDIT CARD BUSINESS.

There are five parties involved in credit card business:

THE CARD ISSUER.

When one applies and is issues the card.

THE CARD HOLDER.

When the customer applies to the bank for a credit card, the bank checks the credit

worthiness of the customers and once the application is approved, the bank issues

credit card with a specified credit limit. The customers then becomes a card holder and

can use the credit card to purchase goods or services from a merchant. Each month the

12

cardholder receives a bill from the card issuer for the amount the cardholder incurred

with the credit card, as well as finance charges if any.

THE MERCHANT.

When the cardholder uses the credit card to pay for goods and services at retail shops,

restaurants, hotels, airlines or any establishments that accept the credit card , the

establishment is a merchant. A merchant should be of good reputation and be

financially responsible.

THE ACQUIRER.

In order for an establishment to be a merchant, it must be accepted by a financial

institution who is a member of Master card/ or visa. There financials institutions is the

acquirer. When a merchant accepts visa or mastercard as a mean of payment, he is

bound by a written agreement with the acquirer.

THE ASSOCIATES.

Master card international and visa international are known as Associates. They are

owned or controlled by a group of member institutions. For financial institutions to be a

member of Master card or Visa, they have to meet the criteria set by the associates.

13

AGE OF PLASTIC MONEY

Banking has evolved a long way from the days of the medieval moneylenders counting

coins on the bench to the present scenario, where it is hard to trace the trail of money

from the beginning to the end.

The trail starts right from the small saver leaving a few rupees in his local bank to the

billions of rupee loans raised by a syndicate banks and financial institutions, capable of

financing projects in any country in the world. Still, these banking majors are heavily

dependent upon their retail home base of savers and borrowers. Most of the bankers

14

began focusing on this retail market segment as global competition intensified in late

seventies and early eighties.

Credit cards, one of the banking products that cater to the needs of retail segment has

seen its number grow in geometric progression in recent years. This growth has been

strongly supported by the development in the field of technology, without which this

could not have been possible.

The history of phenomenal growth in the credit card segment traces way back to in

1950, the time when ‘Diners Club’ was established. The card provided select members

with credit at 22 restaurants in New York and collected a commission for paying the bills

promptly. The credit card industry got a further boost with the arrival of American

Express in the arena in 1958. American Express began selling their card as a prestige

to hotels, restaurants, shops or airlines in America and slowly expanded the network

across the world.

The success of these two players attracted many other banks to join the credit card

business. The entire breed of new players saw a fresh opportunity of granting

unsecured loans at high interest rates to those credit cardholders who did not pay their

bills on time. These banks were not so concerned with collecting commissions from

shops but were thriving on high interest income from those who did not pay their bills on

time.

Starting from ‘Diners Club’, some 50 years ago, the card industry has been growing with

a rapid pace world over and so has been the growth in the domestic card industry. With

only two players in domestic card industry, HSBC and Citibank in the early 80s, the

number swelled to over 25 in the year 2001. Credit cards in India, made their debut in

1981, and are on the verge of an unprecedented boom. Between 1987 and 2001, the

market has virtually grown to over 4 million cards with over 25-30% of compounded

annual growth in new cardholder’s base.

15

Its not that only the card numbers have increased, but even the types of cards on offer

have seen a surge. Today the domestic card industry is flooded with different types of

cards ranging from gold, silver, global, co-branded credit cards, smart to secure,.the list

is endless. Foreign banks have shouldered the major responsibility of increasing the

card base and adding value-added services to the card products in the past. This is also

evident from the fact that the market share of these foreign banks is estimated to be

well over 70%. But the scenario has changed dramatically in the last of couple of years

with the entry of State Bank of India (SBI), a domestic major in the banking sector. More

and more nationalized banks and private sector banks like ICICI and HDFC Bank are

aggressively launching credit card with value added features.

There is immense growth potential in the domestic card industry. A glance at the Indian

population reveals that India’s middle/upper middle class (target segment) represents a

population of over 10 m. There are only 2 to 3 m cardholders, each possessing an

average of 2 cards. This is a very low figure given India’s huge middle to upper class

population. There is no doubt that the domestic card industry has to yet to mature and

offers significant long-term growth potential.

Given the lack of maturity of the domestic card industry, its growth will depend upon

building core retail business, with more sophisticated products. In the expansion of

domestic credit card market, the existing foreign players, SBI, other nationalized banks

and the new domestic private sector banks are expected to play important role with

complementary strategies.

Foreign banks with the advantage of technology and industry experience are expected

to concentrate on increasing card spending and customer loyalty in the major cities.

SBI, on the other hand is expected to capitalize its superior distribution network to

expand card acceptance in the smaller towns. The new private sector banks would have

the opportunity to capture significant market share by combining the strengths of foreign

banks and nationalized bank like SBI.

16

Although at present the card market is mainly limited to India’s relatively bigger cities

and tourist locations only, there is also a potential in smaller cities. Domestic banks,

owing to their vast network and reach to smaller cities, can easily tap this potential.

They would be better off, penetrating into smaller cities and bringing credit card to the

masses rather than cannibalizing other foreign banks’ existing cardholder base.

The efforts of these banks to increase the card base is going to be wholeheartedly

supported by the residents of these smaller cities with their higher disposable income,

changing lifestyle, increasing travel and the growth in the entertainment sector.

The age of plastic money seems to be here to stay. A recent American Express `Share

of Wallet' study among cardholders across the six cities of Delhi, Mumbai, Kolkata,

Chennai, Bangalore and Hyderabad reveals that card usage is highest for dining and

shopping, while it is also popular for travel-related expenses such as air tickets, hotels

and car rentals.

The result of the Indian survey is in line with the other markets in the Asia Pacific region

that were surveyed. Cardholders in countries such as Singapore, New Zealand,

Thailand, Malaysia, Hong Kong and Australia spend 10-30 per cent more on the same

services.

While travel and entertainment-related expenses continue to be "big ticket" expenditure

items, Indian consumers are increasingly using the plastic alternative for everyday

spends such as petrol, hospitals, telephone services, home furnishing and good old

eating.

The survey indicates that consumers in the country are increasingly looking to use

credit cards to pay school dues for their kids. In fact, this has spurred American Express

to tie up with the Delhi Public group of schools to facilitate parents to pay by card. Right

now, India is at a low 11 per cent in comparison to other countries in the Asia-Pacific

region when it comes to using plastic money for recurring bills such as utilities,

17

subscriptions and insurance. In this category, Malaysia tops at 42 per cent, Taiwan at

31 per cent, both even higher than Hong Kong and Australia.

According to the wallet study, the frequency of card usage is expected to go up in the

forthcoming months. About 32 per cent of the consumers surveyed anticipate using the

card more frequently in the next six months, while 18 per cent said that they would add

more credit cards to their wallets.

Interestingly, 39 per cent consumers in Thailand also anticipated increased card spends

while about 19 per cent expected to acquire more credit cards in the next six months.

However, in the developed markets of Australia, Singapore, Hong Kong and New

Zealand, the number of credit cards are expected to remain the same, obviously due to

saturation.

But corporate cards continue to have good potential. According to American Express,

there are about 30,000 mid-market companies in India, with sales revenues from Rs 5

crore to Rs 500 crore incurring a total travel and entertainment expenditure is $2.7

billion. This expense in India is expected to grow at the rate of 8 per cent and is

estimated to exceed $5 billion by year 2006. The use of corporate cards can bring

savings up to 40 per cent for the middle market companies through process savings

and purchase savings.

The credit card market in India, according to American Express, is growing at 20-25 per

cent per annum. From the half-a-million cardholders in 1992, the population is at a

whopping nine million today. Also, the total billings on cards are estimated at over Rs

10,000 crore, growing at 20 per cent per annum.

Australia began printing plastic notes in 1988. Since then Securency has spread its

ambit to 23 countries—Bangladesh to Vietnam, Nepal to Mexico, and now Singapore.

‘‘A 24th country has just signed on,’’ said a Securency official, ‘‘but the name is

confidential.”

18

Securency prints its notes on a polymer substrate called Guardian, which it has

patented. ‘‘While polymer notes cost 1.5 to two times more than paper notes,’’ said

Curtis, ‘‘they are more durable and difficult to counterfeit. Against a counterfeit rate of 68

per million for notes in Europe and 100 per million in the US, Australia has only nine

counterfeit notes per million.’’

In India, where the velocity of money—the number of times it changes hands—is high, it

is longevity that is emphasised. Low-denomination paper currency, such as the Rs 10

note, usually survives six months. Securency’s experience with polymer suggests a life

of almost four years. As for higher denominations, Aus $50 notes issued in 1995 are still

going strong.

Securency first spoke to RBI in 1999. Sample Rs 10 and Rs 100 polymer notes were

produced but the idea was perhaps still too novel. About nine months ago, Securency

presented its case afresh, pointing out that polymer notes did not get dirty, tear or

crumple, were never rejected by teller machines—and were a huge cost saver.

The Australian firm quoted the example of Brazil’s 10 reais polymer notes, issued in

April 2000 and roughly analogous to India’s Rs 10 note. ‘‘There are 250 million 10 reais

polymer notes in circulation,’’ said a Securency official, ‘‘a Brazilian government study in

2003 calculated that in three years they had saved the central bank $17 million.’’ India

issues seven billion Rs 10 notes a year. Just do the calculation.

Securency’s tentative offer to India includes a joint venture ‘‘with an Indian entity of the

government’s choice’’ to produce the polymer substrate locally. Asked what sort of an

investment by Securency this would entail, Curtis was evasive. ‘‘May be between $25-

50 million.’’

On their part, Indian officials said: ‘‘the polymer technology is good but no final decision

has been taken. These things take time.’’

19

Delay would appear perfectly explicable. The banknote industry has conservatism and

secrecy written all over it. Change is unusual.

In the US—seen by some as ‘‘the final frontier for polymer notes’’—the dollar is printed

on special paper, 75 per cent cotton and 25 per cent linen, supplied to the Federal

Reserve by a family-run firm for the past 125 years.

Based in Dalton, Massachussetts, Crane and Company patented this paper in 1879. In

2003, it signed a four-year contract with the Treasury, agreeing to supply paper worth

$336 million. The company’s chairman, Lansing E Crane, is one of America’s wealthiest

men, even if few have heard of him.

For 50 years, free India printed its rupees on machines bought from De La Rue Giori,

run by the Swiss family Giori and till recently said to control 90 per cent of the banknote

printing business.

The Giori saga has an unfortunate Indian subtext. In December 1999, M Roberto Giori,

eldest of the Giori brothers and company chairman, was among those hijacked to

Kandahar. If the Taliban had figured out who this economy class passenger was, he

would have been the uber hostage.

Giori never recovered, insiders say. In 2001, he sold his business to Koenig & Bauer, a

German firm.

In the 1990s, India diversified. Turning away from De La Rue Giori, it bought machines

from Japan’s Komori for the RBI’s new presses. That decision was taken when

Manmohan Singh was finance minister. As PM, will he take the next leap to plastic? At

Securency, they’re betting their polymer on it

20

ORIGIN OF CREDIT CARDS

The credit card has its beginning in an embarrassing incident that took place in the early

1950’s in America. The story goes that Mr. McNamara; a New York businessman took

his friends out to dinner. The end of meal he discovered that he had forgotten his wallet

at home; the proprietor was kind enough to allow him a later settlement of bill. As

McNamara stepped out of the restaurant he had the brainwave for the introduction of

credit cards - system of availing instant credit upon confirming the identity of card

holder. Thus was born the Diners Club Cards, the pioneer of today’s multibillion dollar

plastic money business. Diners club adopted a promising approach by recruiting various

Hotels and restaurants to act as member establishment for accepting the cards. Not

only did these establishments pay a commission on member’s purchases but the

members also paid an annual subscription fee. Diners Club vetted its members for

credit worthiness and guaranteed payment to participating establishment. Thus was

born the first ‘Travel and Entertainment Card’. It was followed by American Express

which is now a dominant force in the Travel and Entertainment cards industry, and by

1959 by Carte Blanche, after many vicissitudes is now a part of Citi Bank Empire

Together With Diners Club. In the present time American Express leads the travel and

entertainment (T&E) card industry.The next great leap-forward came from Bank of

America, which in other banks. Such card holders could use their card 1966 offered to

21

license its successful blue, white and gold Bank America card to at any accepting

merchant establishments around the globe. Later in 1977 all the national and

international Bank America licenses were pulled together under the single name of Visa.

Not to be outdone, a rival group of American Banks came together in 1966 under the

name of Interbank, later renamed Master Charge and later still Master Card. Ever since

Master Card and Visa and their affiliates have carved the world credit card market.

In the 1980s credit card concept was launched in India through the Diners Club card,

and soon, within a couple of months both Visa and Master card entered into the Indian

market.

HISTORY OF CREDIT CARDS

Since the beginning of history man has been involved with trade and commerce. As this

area has expanded and become more important, different medium of exchange has

been developed. Barter gave way to the advance of money, and money in turn has

faced the advance of checks.

Now both are feeling the advance of credit card. In this age of rapid technological

advances it is only natural that man should seek out a new and more efficient system of

carrying on trade and commerce. This system seems to be credit card.

Again, credit cards are not new. They, or some equivalent, have existed since the early

part of this century. Some time before1920 some large department stores began to

issue "credit coins". These coins were a small piece of metal which displayed the name

of the merchant and the series of merchant identifying the customers account. These

coins were issued to good customers and allowed them to purchase merchandise on

credit in the store.

In 1950, the Diners club, introduced the first independent credit card plan. This plan

involved a agreement between the club and the merchants. The members agreed to

pay the club to obtain the card and then agreed to pay each monthly billing as it came in

22

. The merchant agreed to honor the card and then forward his credit voucher to Diners

club for payment once a month. The member there by were able to get service from

many type of establishments by carrying only one card and were able to pay for it at the

end of the month.

The merchant on the other hand, were relieved of having to have his own plan and was

also likely to increase the volume of his business since card holding members would

find it more convenient to deal with him then with a merchant who wouldn't honor is

card. The success of Diners club pan was such that the American Express company

entered the field in 1958, while Hilton Credit Corporation initiated the "carte blanche"

plan the following year.

In 1951, the first National bank of long island became the first bank to offer its

customers a credit card plan. This area was not very important, however, until the late

1950s when the bank of America and the Chase Manhattan bank issued there cards. In

1966, the Midwest bank card system was started.

By at least the beginnings of the 1970s the personal credit card had become a fixture in

the nation’s economy. Today more than 60 million credit card accounts exist in the

United States, and seven out of ten households possess at least one credit card. By

1986 out standings balance on credit card account total more than $80 billion

23

SOME TERMINOLOGY USED IN CONCERN WITH

CREDIT CARDS

Before we go any further, why not become familiar with the various terms and jargons

used by the credit card industry.

Credit Card – A credit card is a financial instrument, which can be used more than once

to borrow money or buy products and services on credit. Banks, retail stores and other

businesses generally issue these.

Credit limit – The maximum amount of charges a cardholder may apply to the account.

Annual fee – A bank charge for use of a credit card levied each year, which ranges

depending upon the type of card one possesses. Banks usually take an initial fixed

amount in the first year and then a lower amount as yearly renewal fees.

Revolving Line Of Credit - An agreement to lend a specific amount to a borrower and to

allow that amount to be borrowed again once it has been repaid. Most credit cards offer

revolving credit.

24

Personal Identification Number (PIN) - As a security measure, some cards require a

number to be punched into a keypad before a transaction can be completed. The

number can usually be changed by the cardholder.

Teaser Rate - Often called the introductory rate, it is the below-market interest rate

offered to entice customers to switch credit cards.

Joint Credit - Issued to a couple based on both of their assets, incomes and credit

reports. It generally results in a higher credit limit, but makes both parties responsible

for repaying the debt.

TYPES OF CARDS

MasterCard – MasterCard is a product of MasterCard International and along with

VISA are distributed by financial institutions around the world. Cardholders borrow

money against a line of credit and pay it back with interest if the balance is carried over

from month to month. Its products are issued by 23,000 financial institutions in 220

countries and territories. In 1998, it had almost 700 million cards in circulation, whose

users spent $650 billion in more than 16.2 million locations.

VISA Card – VISA cards is a product of VISA USA and along with MasterCard is

distributed by financial institutions around the world. A VISA cardholder borrows money

against a credit line and repays the money with interest if the balance is carried over

from month to month in a revolving line of credit. Nearly 600 million cards carry one of

the VISA brands and more than 14 million locations accept VISA cards.

25

Affinity Cards - A card offered by two organizations, one a lending institution, the

other a non-financial group. Schools, non-profit groups, pro wrestlers, popular singers

and airlines are among those featured on affinity cards. Usually, use of the card entitles

holders to special discounts or deals from the non-financial group.

Standard Card– It is the most basic card (sans all frills) offered by issuers.

Classic Card– Brand name for the standard card issued by VISA.

Gold Card/Executive Card– A credit card that offers a higher line of credit

than a standard card. Income eligibility is also higher. In addition, issuers provide extra

perks or incentives to cardholders.

Platinum Card – A credit card with a higher limit and additional perks than a gold

card.

Titanium Card – A card with an even higher limit than a platinum card.

Secured Card – A credit card that a cardholder secures with a savings deposit to

ensure payment of the outstanding balance if the cardholder defaults on payments. It is

used by people new to credit, or people trying to rebuild their poor credit ratings.

Smart Card – Smart cards, sometimes called chip cards, contain a computer chip

embedded in the plastic. Where a typical credit card's magnetic stripe can hold only a

few dozen characters, smart cards are now available with 16K of memory. When read

by a special terminals, the cards can perform a number of functions or access data

stored in the chip. These cards can be used as cash cards or as credit cards with a

preset credit limit, or used as ID cards with stored-in passwords.

26

Charge Card – Falls between a debit and credit card. Works like the latter and you

don't have to be an accountholder. Just pay up in full when the bill arrives with the mail.

No outstanding are allowed, in other words, no revolving credit facility either. American

Express and Diners are providers.

Rebate Card – This is a card that allows the customer to accumulate cash,

merchandise or services based on card usage.

Co-Branded Card – This is a marriage of convenience between two service

providers who want a trade-off with the other's strengths. Specific facilities are made to

members through these tie-ups. So, Times Bank and Citibank have a co-branded card

that allows concessional rates for add-on cards or telephone banking. Stan chart and

Hindustan Lever Limited have a co-branded card to sell Aviance beauty products. SBI-

GE Capital has a co-branded card for retail loans.

Cash Card – Cash cards, similar to pre-paid phone cards, contain a set amount of

value, which can be read by a special cash card reader. Participating retailers will use

the reader to debit the card in increments until the value is gone. The cards are like

cash -- they have no built-in security, so if lost or stolen, they can be used by anyone.

Travel Card – These work mostly as debit cards for the limited purpose of travel.

Citibank Dollar Card, American Express, Bobcard Global and Hongbank Bank Thomas

Cook International Card are among the players in this section.

cardS

27

METHODOLOGY IN CREDIT CARDS BUSINESS

Following methodology is used for credit card business:

Credit Card bank advertises or approaches the prospective cardholder.

Prospective card holders apply for credit card membership by filling the prescribed form

which normally contains personal and financial particulars.

Issuer of credit card evaluates the form and issues the credit card and fixes the money

limit for use of such credit card.

Cardholder puts the signature on the prescribed place on the card before putting it to

use and starts using it.

Member establishment prepares a charge slip (for cost to be recovered) gets it signed

by the card holder, tallies the signature, and return, on the copy of charge slip of charge

slip to the credit card holder. The second copy is sent to the issuer for recovery of

money and he retains third copy.

Card issuer receives the bill and charge slip and makes payment to the member

establishment.

28

Card issuer prepares an account statement and sends it to card holder for payment to

bank directly or through its authorized collection centers.

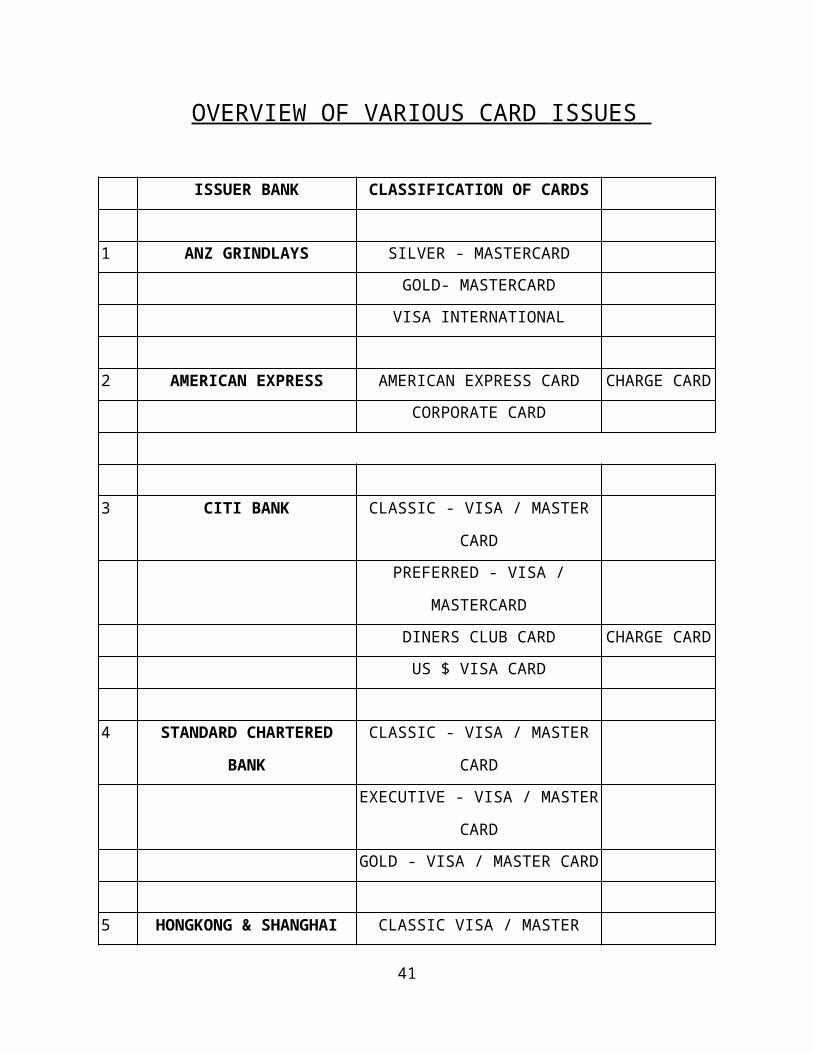

OVERVIEW OF VARIOUS CARD ISSUES

ISSUER BANK CLASSIFICATION OF CARDS

1 ANZ GRINDLAYS SILVER - MASTERCARD

GOLD- MASTERCARD

VISA INTERNATIONAL

2 AMERICAN EXPRESS AMERICAN EXPRESS CARD CHARGE

CARD

CORPORATE CARD

3 CITI BANK CLASSIC - VISA / MASTER

CARD

PREFERRED - VISA /

MASTERCARD

DINERS CLUB CARD CHARGE

CARD

US $ VISA CARD

4 STANDARD CHARTERED

BANK

CLASSIC - VISA / MASTER

CARD

29

EXECUTIVE - VISA / MASTER

CARD

GOLD - VISA / MASTER CARD

5 HONGKONG & SHANGHAI

BANK

CLASSIC VISA / MASTER CARD

GOLD VISA / MASTER CARD

US $ MASTER CARD

6 BANK OF BARODA BOB CARD CHARGE

CARD

BOB SILVER

BOB EXCLUSIVE

BHARAT BOB CARD PREMIUM

BOB CARD GLOBAL

7 CENTRAL BANK OF INDIA CENTRAL MASTER CARD

8 BANK OF INDIA INDIA MASTER CARD

TAJ CARD CHARGE

CARD

9 CANARA BANK CANCARD VISA / MASTER CHARGE

CARD

CANCARD PROPRIETOR CHARGE

CARD

10 VIJAYA BANK VIJAYA GOLD CHARGE

CARD

VIJAYA CLASSIC CHARGE

30

CARD

11 ANDHRA BANK ANDHRA GOLD CHARGE

CARD

ANDHRA CLASSIC CHARGE

CARD

12 ICICI BANK CLASSIC - VISA / MASTER

CARD

EXECUTIVE - VISA / MASTER

CARD

GOLD - VISA / MASTER CARD

13 STATE BANK OF INDIA CLASSIC - VISA / MASTER

CARD

EXECUTIVE - VISA / MASTER

CARD

31

HOW TO CHOOSE A CREDIT CARD

With the credit card truly becoming an international citizen, issuers have begun

highlighting the value added features offered along with the basic product. While some

of them are offering attractive interest rates, others are luring customers by their reward

schemes. With a plethora of choices on offer it is not easy to come to a decide on any

particular card. However, a comparison on the basis of a few basic parameters is will

help us make an informed choice.

First, there's the credit limit. All banks have different limits set for customers depending

upon the type of card in their possession. Even within a particular type of card, limits

may vary depending upon the credit worthiness of the individual. This depends, among

other things, on the gross income of the individual and the period for which he/she is

using the card. However, some banks like Citibank and American Express have cards

which have no set credit limit. Amex, for e.g., has a charge card which has no upper

limit and allows one to spend as much as one likes (provided the holder repays the

amount at one go).

A second criteria could be the lost card liability. If one is travelling and has lost his/her

credit card then reporting the loss will not be much of a problem. HSBC, Citibank,

Stanchart and Amex can be reached from any corner of the world for information on

one's card as well as for reporting the loss. However, except for Amex, all others will

mail a replacement card to the holder's mailing address. Amex will replace the card

within 48 hours free of cost. Liability for a lost card is nil for Citibank, HSBC, Amex

(once the bank is informed about the loss) and the Stanchart photo card. However, the

non-photo card carries a liability of Rs1,000.

32

Nowadays, almost all cards come with various goodies attached. These include airline

ticket booking and insurance benefits on lost luggage and accidental deaths. HSBC, for

e.g., offers discounts of 3.5% on domestic air fares and 6.5% on international ones if

tickets are charged

to their cards. The latest in line of value added features are the rewards programs. Here

a card holder earns a certain number of points by spending a particular sum of money.

Stanchart, for e.g., uses a conversion of Rs125 (spent in India) or Rs80 (spent abroad)

for one point. HSBC, on the other hand, only allows points collected to be squared

against a discount on the annual fees. A minimum of 350 points is needed to get a

discount on the

annual fee. Citibank awards one point on spending Rs100.The table below gives an

indication of the various value added services on offer from various banks.

Value Added Features Citibank Stanchart HSBC Amex

Hotel discounts - - - Yes

Travel fare discounts Yes Yes Yes Yes

Free global calling card Yes (G) - Yes Yes

Lost baggage insurance Yes Yes Yes -

Accident insurance Yes Yes Yes -

Insurance on goods purchased Yes Yes Yes -

Waiver of payment in case of accidental

death- - Yes* -

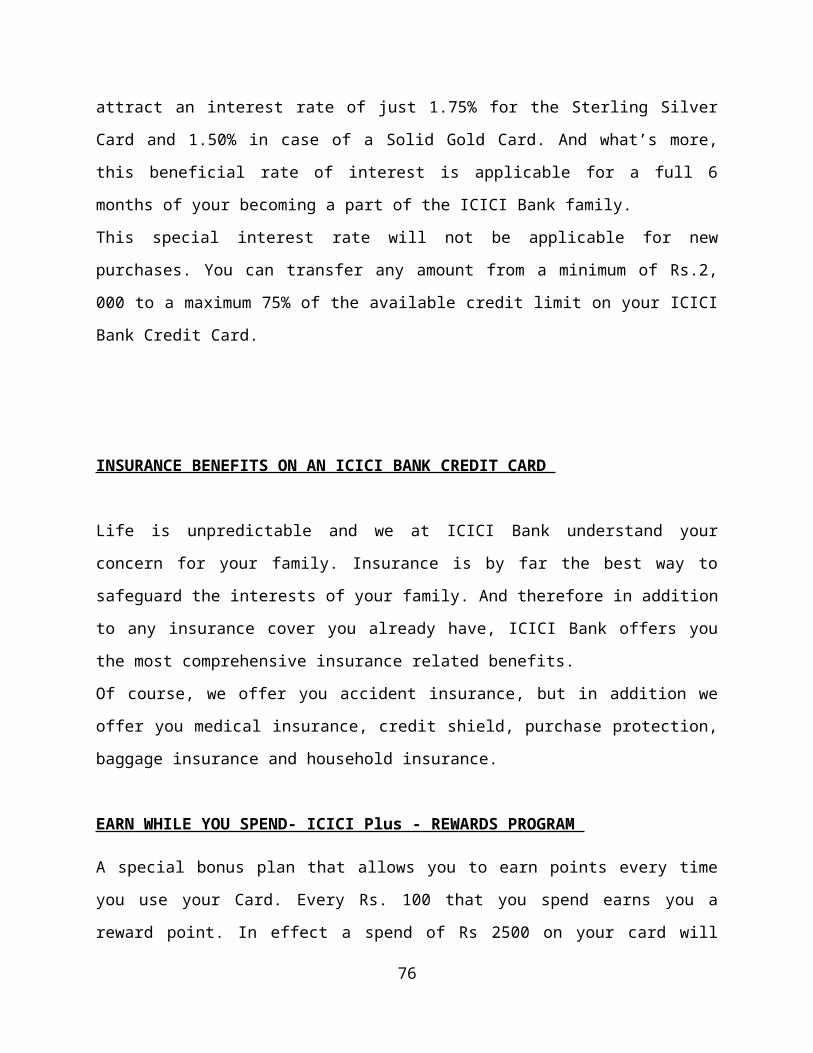

An innovative scheme offered by American Express, called Balance Transfer Service,

helps the cardholder to pay off out standings on other credit cards. Amex will pay the

card issuer and transfer the amount due to the Amex card. And for the first six months

the Amex card holder gets the benefit of a lower interest rate of 1.99% per month as

compared to 2.95% for most other banks. For frequent users,

Amex has a scheme for waiving the annual fees if the cardholder spends more than Rs45,000 in

the preceding 12 months.

33

Another new thing on the horizon are the so-called co-branded cards. Several of them have been

have been launched recently. Companies like Indian Oil Corporation have tied up with Citi bank

to launch Indian Oil Citibank card. With this card one does not require to pay a transaction fee

for purchasing petrol at any Indian Oil outlet. The card holder gets a 5% discount on all AMCO

and Exide make batteries from authorized dealers and Rs1,000 off at select outlets for MRF auto

coat car painting charges.

There is also the Times card and Bharat Petroleum BOB card. These cards give you discounts at

several outlets. For example the Mahindra Stan chart card gives you priority check-in and check-

out facilities at Guest line hotels (run by Mahindras).

34

DIFFERENT TYPES OF CREDIT CARDS BY DIFFERENT BANKS

As the undisputed leader in the Cards business, Citibank has more than 70 million card

member accounts worldwide. Growth has continued through the acquisition of the AT&T

Universal Card Services business, introduction of the Driver's Edge and Sony Citibank

cards, and expansion of the Citibank-American Airlines partnership. The merger adds

more than one million credit card accounts, principally with members of professional

associations and other affinity groups, including Salomon Smith Barney clients.

The Citibank Advantage card, now in 25 countries, is the most successful co-branded

card in the industry.

Citibank has 25 million cards, including affiliates, in force in Latin America, Asia,

Central and Eastern Europe, and the Middle East. In most of these markets we have

double-digit share: 43 percent in Puerto Rico, 11 percent in Argentina and Chile, and

more than 20 percent in Hong Kong and Taiwan. In Poland, where Citibank launched a

card in late 1997, we have 20,0000 card holders today.

In the United States, Citibank is strongly committed to maintaining Cards as one of the

great success stories of the bank. Acquisition of the AT&T Universal Card increased our

market share of total U.S. card receivables from 11 percent to 15 percent.

35

CITIBANK CREDIT CARDS

DINERS CLUB CREDIT CARD

Diners Club was the first card in the Indian market. Launched in 1960, just after 10

years it was launched in the market of United States. It was the firs charge card in the

world. The early eighties saw the launch of credit cards in India by some Indian banks,

viz. Central bank, Andhra bank et. , with Visa and Master Card affiliations. The size of

the credit card market was around 300,000 in 1990. Credit Card was a status symbol for

upscale individuals who had high travel and entertainment needs. More than 40,000-

business establishments in the country now accept credit cards. The total credit they

provided in 2004- 05 was Rs. 80000 crore.

FEATURES OF THE CARD

Your lifestyle demands complete financial flexibility and convenience. Unlike other Card,

the Diners Club Card does not restrict you with a pre-set spending limit. At Diners Club,

you’re spending and payment patters and personal resources determine how much you

can charge. So, over time, you set your own limit.

Club Assurance

As a Diners Club Member, you are insured against loss of life in an air accident for

Rs.30 laky, or Rs.2 laky in any other accident. This insurance is available to you,

wherever you are in the world.

Club Protection

Household Insurance this cover protects household articles (excluding jeweler and

valuables) for a value of upto Rs. 1,00,and 000/- per annum. This insurance is on first

loss basis that insures articles for the entire sum insured.

Baggage Insurance

Baggage Insurance protects your baggage against theft or loss for upto Rs. 40,000/- in

India and upto Rs. 60,000/- while traveling abroad.

36

Delayed Baggage

If your baggage is not delivered within 12 hours of arrival of a flight, you will be

reimbursed for purchase of essential clothing of upto Rs.5,000/- in India and Rs.

10,000/- when abroad.

Delayed Flight

If you miss an onward flight due to late arrival of an incoming flight, and if there is no

alternative flight within 6 hours (of actual arrival time) or the airline do not provide

accommodation, you will be entitled to Rs.15,000 reimbursement for hotel

accommodation.

Loss of Passport/Ticket

If you lose your passport in a foreign country, you can claim upto Rs.25,000/- towards

the cost of obtaining a fresh Passport. If you lose your air tickets you will be reimbursed

for it upto Rs.5,000/-

Purchase Protection

Under International Purchase Protection, purchases on your card are insured against

loss or damage due to fire or theft, for a period of 180 days, from the time of purchase

up to a value of Rs. 50,000/-

Club Rewards - with Fast Track option

With Diners Club Card, you also get the most powerful rewards program in the country.

For every Rs.100 spent on the Diners Club Card, you earn one Club

Rewards Point. You can redeem the Rewards Points you have earned for fabulous

travel packages and delightful gifts. Moreover, these Points are 'evergreen', which

means you can encash them whenever you want.

Besides Diners Club has tied up with Flying Returns, India's No.1 frequent flyer program

from Indian Airlines and Air India. Which means you can now redeem your Points for

free miles!

37

Finally, your Club Rewards Points can also be converted to Oberoi Top Points and

Welcome Award Stars - the rewards programs of the Oberoi Group and Welcome group

respectively.

Club Perks

Club Perks is a unique promotional offer exclusively for Diners Club Members. Club

Perks gives you special discounts at your favorite restaurants, hotels, car rentals and

retails across the country. It also gives you complimentary into some of the most

prestigious discotheques in the country. All you have to do is charge your bill to your

Diners Club Card every time you visit any of these places.

Club Lounges

Relax between flights.

You can now relax in plush airport lounges, designed exclusively for Diners Club

Members. There are more than 74 such lounges located at various international

airports. In India, you have complimentary access to airport lounges located at the

domestic departure areas in Mumbai, New Delhi, Chennai and Bangalore.

Club Cash

The Diners Club Card gives you the convenience of drawing cash in an emergency, 24

hours a day, 7 days a week! You can access up to Rs.20,000 through Club Cash

through our extensive network of Automated Teller Machines.

Club Privileges-Phone Home, Global One Calling Card

Finally, Diners Club offers you an exclusive range of international privileges.

The GlobalOne Calling Card, the international calling card which enables you to call

from 60 countries to over 300 countries whenever you travel overseas, and pay later in

Indian Rupees through your Diners Club Card. This facility is available absolutely free.

Citibank international gold card

High Credit Limit

38

For someone as powerful as you, only the most powerful Card in the world will do - the

Citibank International Gold Card. A true reflection of your power, this Card gives you the

ultimate financial freedom in India and everywhere in the world. The best part is this

Card is yours at no additional cost, and comes with the advantage of spending in

International currencies and paying back in Indian Rupees!

Comprehensive Insurance Benefits *

PersonalAccidentInsuranceuptoRs.20lakh

Whether you are traveling in India or overseas, your Card comes with FREE Personal

Accident Insurance (uptoRs.20lakh)

Free House hold Insurance

This cover protects household articles (excluding jewelry and valuables) for a value of

up to Rs.75,000/- per year. This is valid for primary Card members only.

Free Baggage Insurance

This unique insurance protects your baggage against theft or loss for up to Rs. 40,000/-

in India and up to Rs. 60,000/- while traveling abroad.

Free Delayed Flight Insurance

If you miss an onward flight due to late arrival of an incoming flight, and if there is no

Alternative flight within 6 hours (of actual arrival time) or the Airlines does not provide

accommodation, you will be entitled to Rs.15,000/- as reimbursement for hotel

accommodation.

FreePassportLossInsurance

If you lose your passport in a foreign country, you can claim up to Rs.25,000/- towards

cost of obtaining a fresh passport. On loss of an air ticket, you will be reimbursed for up

toRs.5000/-.

FreeGlobalPurchaseProtection

Under International Purchase Protection, purchases on the Card are insured against

39

loss or damage due to fire or theft for a period of 180 days from the time of purchase for

a value of upto Rs. 40,000/-.

Unique reward program.

Every time you use your Card you earn Citibank Rewards Points that can be exchanged

for many exclusive privileges like Free Air Miles, free Hotel Nights, leather accessories

and much more. You can exchange your Citibank Rewards Points for miles on airline

frequent flyer programs and fly free to your dream destination and stay free at hotel

properties

participating in our Rewards Program. You can also choose to pay your Card Renewal

Fee (in part or full) using your Rewards Points as well. What's more, your Citibank

Rewards Points are evergreen and never lapse.

Revolving Credit Facility

With Citibank's powerful Revolving Credit Facility you can choose to buy high-value

items now and pay later in parts. And pay as little as 5% of your total outstanding every

month.

Free GlobalOne Calling Card

The next time you make an international call from overseas, you do not need to use

precious foreign exchange or hunt for loose change. The Global One Calling Card

makes international calling absolutely easy. The Global one Calling Card charges will

be conveniently billed later to your Citibank International Gold Card and itemized call

details will appear on your monthly statement.

Special Discounts on Travel

India's leading travel management company Travel House (a member of the ITC Group)

brings you 3.5% off on basic domestic air fares and 7% off on basic International air

fares

when you buy tickets on your Citibank International Gold Card. In fact your tickets will

be delivered to you at no extra cost.

40

Free Phone Home facility

In case of an emergency or for any urgent clarification on your Card, while you are

overseas, you can use FREE Phone Home Facility.

24- hour ATMs

While travelling overseas you can access cash (up to 60%**** of your Credit Limit) at

over 12,50,000 Visa/MasterCard ATMs across the globe. There are 24-Hour ATMs in

Ahmedabad, Bangalore, Calcutta, Chennai, Delhi, Hyderabad, Mumbai and Pune too.

You can also draw cash from any Citibank branch.

24- hour CitiPhone

CitiPhone, the revolutionary phone banking service ensures that Citibank is just a phone

call away from you. From the minute you dial in, the world-class Interactive Voice

Response (IVR) Service will guide you right through. Call our courteous CitiPhone

Officers standing by to assist you. 24 hours a day, and 7 days a week.

Worldwide Assistance

The Visa/MasterCard Global Assistance Services can be used for reporting lost or

stolen Cards, requesting for an emergency Card replacement or for emergency Cash

Advances. A wide range of miscellaneous information is also available for your benefit.

Additional Card

You can share the power of your Citibank International Gold Card with your family. Your

Citibank International Gold Card Membership entitles you to Additional Cards for two

members of your family, over 18 years of age, at a special price of Rs.1000/- p.a. per

Card.

Citibank silver card.

Exciting gifts with Citibank Rewards

Every time you use your Card, you earn valuable Citibank Rewards Points that can be

exchanged for fabulous gifts. Choose from a wide range of gifts - cosmetics to cameras,

41

CDs to wallets. You can also exchange your Citibank Rewards Points to pay your Card

Renewal Fee (in part or full). What's more your Citibank Rewards Points are evergreen

and never lapse.

COMPETITION IN CREDIT CARD BUSINESS

With the emergence of plastic money (credit cards) as a social security tool and the

modest way to come under transactions with time saving the customers are widely

looking and accepting credit cards for their transactions. No doubt due to several

advantages of it, is gaining its market and competency. Due to wide acceptance in the

market every institution in financial market whether it public sector or private sector

42

institution are engaged in this discipline with better customer focused strategy to

capture the untapped market soon.

Banks like ICICI, HDFC, CITI BANK, SBI, PNBwith the multinational banks like HSBC,

IDBI and STANDARD CHARTERED are engaged and competing for the market

capitalization. Every banking company is ready to serve with better schemes, rates,

terms and conditions which can suit the customers’ requirements.

To be an active player of the financial market every institution is issuing

several types of cards like the life time free cards with extended date to pay the amount

back to the banks. They have good strategies and workforce with many reputed direct

sales associates and direct sales teams to fetch good sales and to win the consumers

faith. The government of India is also taking initiative to protect the consumer rights in

this credit cards division.

So this market is now a days a global market which is gaining its growth like anything.

INTRODUCTION OF ICICI BANK

1995: The Industrial Credit and

Investment Corporation of India

Limited (ICICI) incorporated at the

initiative of the World Bank, the Government of India and representatives of Indian

industry, with the objective of creating a development financial institution for providing

43

medium-term and long-term project financing to Indian businesses. Mr. A. Ramaswami

Mudaliar elected as the first Chairman of ICICI Limited. ICICI emerges as the major

source of foreign currency loans to Indian industry. Besides funding from the World

Bank and other multi-lateral agencies, ICICI also among the first Indian companies to

raise funds from International markets. 1956: ICICI declared its first Dividend at 3.5%.

1958: Mr. G. L. Mehta was appointed the 2nd Chairman of ICICI Ltd. 1960: ICICI

building at 163, Backbay Reclamation was inaugurated. 1961: The first West German

loan of DM 5 million from Kredianstalt was obtained by ICICI. 1967 : ICICI made its first

debenture issue for Rs.6 crore, which was oversubscribed. 1969 : First two regional

offices in Calcutta and Madras were opened. 1972 : Second entity in India to set-up

merchant banking services. : Mr. H. T. Parekh appointed as the third Chairman of ICICI.

1977: ICICI sponsors the formation of Housing Development Finance Corporation.

Managed its first equity public issue 1978: Mr. James Raj appointed as the fourth

Chairman of ICICI. 1979: Mr. Siddharth Mehta appointed as the fifth Chairman of ICICI.

1982: Becomes the first ever Indian borrower to raise European Currency Units. : ICICI

commences leasing business. 1984 : Mr. S. Nadkarni appointed as the sixth Chairman

of ICICI. 1985 : Mr.N.Vaghul appointed as the seventh Chairman and Managing

Director of ICICI. 1986 : ICICI first Indian Institution to receive ADB Loans. First public

issue by an Indian entity in the Swiss Capital Markets. : ICICI along with UTI sets up

Credit Rating Information Services of India Limited, (CRISIL) India's first professional

credit rating agency. : ICICI promotes Shipping Credit and Investment Company of India

Limited. (SCICI) : The Corporation made a public issue of Swiss Franc 75 million in

Switzerland, the first public issue by any Indian equity in the Swiss Capital Market. 1987

: ICICI signed a loan agreement for Sterling Pound 10 million with Commonwealth

Development Corporation (CDC), the first loan by CDC for financing projects in India.

1988 : ICICI promotes TDICI - India's first venture capital company. 1993 : ICICI sets-up

ICICI Securities and Finance Company Limited in joint venture with J. P. Morgan. :

ICICI sets up ICICI Asset Management Company. 1994 : ICICI sets up ICICI Bank.

1996 : ICICI becomes the first company in the Indian financial sector to raise GDR. :

ICICI announces merger with SCICI. 1997 : ICICI was the first intermediary to move

away from single prime rate to three-tier prime rates structure and introduced yield-

44

curve based pricing. : The name "The Industrial Credit and Investment Corporation of

India Limited " was changed to "ICICI Limited". : ICICI announces takeover of ITC

Classic Finance. 1998+ : Introduced the new logo symbolizing a common corporate

identity for the ICICI Group. : ICICI announces takeover of Anagram Finance. 1999 :

ICICI launches retail finance - car loans, house loans and loans for consumer durables.

: ICICI becomes the first Indian Company to list on the NYSE through an issue of

American Depositary Shares. 2000: ICICI Bank becomes the first commercial bank

from India to list its stock on NYSE. : ICICI Bank announces merger with Bank of

Madura. 2001: The Boards of ICICI Ltd and ICICI Bank approved the merger of ICICI

with ICICI Bank. 2002 : Moodys' assign higher than sovereign rating to ICICI. : Merger

of ICICI Limited, ICICI Capital Services Ltd and ICICI Personal Financial Services

Limited with ICICI Bank.

OVERVIEW

ICICI Bank is India's second-largest bank with total assets of about Rs.146,214 crore at

December 31, 2004 and profit after tax of Rs. 1,391 crore in the nine months ended

December 31, 2004 (Rs. 1,637 crore in fiscal 2004). ICICI Bank has a network of about

505 branches and extension counters and about 1,850 ATMs. ICICI Bank offers a wide

range of banking products and financial services to corporate and retail customers

through a variety of delivery channels and through its specialised subsidiaries and

affiliates in the areas of investment banking, life and non-life insurance, venture capital

and asset management. ICICI Bank set up its international banking group in fiscal 2002

to cater to the cross-border needs of clients and leverage on its domestic banking

strengths to offer products internationally. ICICI Bank currently has subsidiaries in the

United Kingdom and Canada, branches in Singapore and Bahrain and representative

offices in the United States, China, United Arab Emirates and Bangladesh.

ICICI Bank's equity shares are listed in India on the Stock Exchange, Mumbai and the

National Stock Exchange of India Limited and its American Depositary Receipts (ADRs)

are listed on the New York Stock Exchange (NYSE).

As required by the stock exchanges, ICICI Bank has formulated a Code of Business

Conduct and Ethics for its directors and employees.

45

At October 31, 2004, ICICI Bank, with free float market capitalization* of about Rs.

220.00 billion (US$ 5.00 billion) ranked third amongst all the companies listed on

the Indian stock exchanges.

ICICI Bank was originally promoted in 1994 by ICICI Limited, an Indian financial

institution, and was its wholly-owned subsidiary. ICICI's shareholding in ICICI Bank was

reduced to 46% through a public offering of shares in India in fiscal 1998, an equity

offering in the form of ADRs listed on the NYSE in fiscal 2000, ICICI Bank's acquisition

of Bank of Madura Limited in an all-stock amalgamation in fiscal 2001, and secondary

market sales by ICICI to institutional investors in fiscal 2001 and fiscal 2002. ICICI was

formed in 1955 at the initiative of the World Bank, the Government of India and

representatives of Indian industry. The principal objective was to create a development

financial institution for providing medium-term and long-term project financing to Indian

businesses. In the 1990s, ICICI transformed its business from a development financial

institution offering only project finance to a diversified financial services group offering a

wide variety of products and services, both directly and through a number of

subsidiaries and affiliates like ICICI Bank. In 1999, ICICI become the first Indian

company and the first bank or financial institution from non-Japan Asia to be listed on

the NYSE.

After consideration of various corporate structuring alternatives in the context of the

emerging competitive scenario in the Indian banking industry, and the move towards

universal banking, the managements of ICICI and ICICI Bank formed the view that the

merger of ICICI with ICICI Bank would be the optimal strategic alternative for both

entities, and would create the optimal legal structure for the ICICI group's universal

banking strategy. The merger would enhance value for ICICI shareholders through the

merged entity's access to low-cost deposits, greater opportunities for earning fee-based

income and the ability to participate in the payments system and provide transaction-

banking services. The merger would enhance value for ICICI Bank shareholders

through a large capital base and scale of operations, seamless access to ICICI's strong

corporate relationships built up over five decades, entry into new business segments,

higher market share in various business segments, particularly fee-based services, and

access to the vast talent pool of ICICI and its subsidiaries. In October 2001, the Boards

46

of Directors of ICICI and ICICI Bank approved the merger of ICICI and two of its wholly-

owned retail finance subsidiaries, ICICI Personal Financial Services Limited and ICICI

Capital Services Limited, with ICICI Bank. The merger was approved by shareholders of

ICICI and ICICI Bank in January 2002, by the High Court of Gujarat at Ahmedabad in

March 2002, and by the High Court of Judicature at Mumbai and the Reserve Bank of

India in April 2002. Consequent to the merger, the ICICI group's financing and banking

operations, both wholesale and retail, have been integrated in a single entity.

*Free float holding excludes all promoter holdings, strategic investments and cross

holdings among public sector entities.

SOCIAL INITIATIVES

Bring together participants in the development process to widen and deepen the

discourse informing development practice. Interactive features include discussion

boards and facilities to post papers, articles or other resources.

Publish research related to innovations and significant problems within the identified

thematic areas.

Enable online application for funding.

Address for Correspondence:

Social Initiatives Group

ICICI Bank Towers

ICICI Bank Ltd

Bandra Kurla Complex

Mumbai 400 051

Phone no:+91 22 2653 1414

Fax no:+91 22 2653 1164

47

Major area of social initlatives Mission Statement

Strategy

Focus Areas

Related Interests

ICICI Bank and the Social Sector

Publications

1. Aneesa Arur and Shilpa Deshpande (2002), Infant Health at Birth, Working Paper

Series, ICICIsocialinitiatives.org.

2. Tara Beteille (2002), Elementary Education in India, Working Paper Series,

ICICIsocialinitiatives.org.

http://203.199.32.111/icicisig/Microfinance/upload/MFS DI2(2).doc 3. Bikram Duggal,

Bindu Ananth and Kartikeya Saboo (2002), Micro Finance: Building the Capacities of

the Poor to Participate in the Larger Economy, icicisocialinitiatives.org

Abstract: This paper traces the relationships between the provision of financial services

to the poor and their ability to participate in the larger economy. Poor households

progress from a stage of securing themselves from the day-to-day risks they face to

establishing and enhancing their livelihoods. The paper outlines the role of micro-

financial services in enabling mobility along this continuum.

4. Amit Singhal and Bikram Duggal (2002), Extending Banking to the Poor in India,

icicisocialinitiatives.org

Abstract: The paper articulates the key issues in extending banking to the rural and

poor populations in the country and provides recommendations for the Reserve Bank of

India and the Government of India in order to resolve some of the issues.In the paper,

banking has been viewed as consisting of two elements: cash management and

48

management of databases. Given this perspective, the paper highlights some of the

regulatory issues that impede the progress of banking along the lines suggested.

5. Bindu Ananth and Soju Annie George (2003), Scaling up Micro Financial Services:

An Overview of Challenges and Opportunities, icicisocialinitiatives.org

Abstract:This paper attempts to examine specific issues in the delivery of micro

financial services and outlines some new approaches towards scaling up. Section I

reiterates the crucial role of micro finance in reducing vulnerability and enhancing the

prospects of growth for poor households. Section II examines the broad challenges in

micro finance; Section III provides an overview of the various micro financial services

(insurance, savings and investment, credit and other risk management instruments).

Section IV examines the issues specific to Micro Finance Institutions (MFI) in India and

Section V concludes the paper by identifying the key areas for further research and

debate.

6. Bindu Ananth (2002), Emerging Perspectives in Corporate Social Responsibility,

ICICIsocialinitiatives.org.

Mission Statement

The mission statement of the SIG is "to identify and support initiatives designed to

improve the capacities of the poorest of the poor to participate in the larger economy".

The SIG believes that the three fundamental capacities any individual should possess to

be able to participate in the larger economy are in the areas of health, education and

access to basic financial services. Within these broad areas, infant health at birth,

elementary education and micro financial services define the areas in which the SIG’s

work focuses.

Strategy

At a very basic level, the programmes and projects supported by the SIG are required to

cater to the poorest. They should enable them to become active and informed

49

participants in socio-economic processes as opposed to passive observers. These

initiatives must be output oriented, with a focus on producing measurable outcomes that

meet a minimum quality requirement. The initiatives also need to be cost-effective. This

is in recognition of the fact that resources are limited and their efficient use is imperative

if the maximum number is to benefit. Cost-effectiveness also facilitates the adoption of

the initiative in other contexts.

The initiative must be scalable. Scalability implies the ability to draw upon important

elements of a programme and adapt them to suit the needs of a specific situation. It

should be possible to do so at a national level. Even if the programme itself is not

directly scaleable, it should be possible to take away significant lessons from it in order

to enrich work in other settings.

All supported initiatives should have the potential for both near and long-term impact.

Consequentially, it is important that the impact of these programmes, in the near and

long term, be carefully understood and analyzed in a rigorous manner and not through

anecdotes. It is critical to clearly understand how an initiative is performing in terms of

its predetermined goals and in comparison to alternatives. There is little doubt that a

complex of factors, very often beyond the control of the programme/ organization, will

influence the outcome. Yet, serious and regular impact analysis can only make the

programme richer and is essential. The SIG assigns greater value to programmes/

organizations that carefully examine the short-term and long-term implications of their

actions.

In pursuit of its goals in the three focus areas, the SIG tends to support reasonably

large-sized initiatives so that issues such as cost-effectiveness, scalability and impact

assessment can be dealt with more directly. These initiatives not only have the potential

to provide key research inputs to other programmes, but also tend to have a large

impact that benefits the communities they work with. The approach of the SIG may thus

be characterized more broadly as ‘action research’, to distinguish it from pure academic

research. However, in its research work and impact assessment, the SIG seeks to

adhere to the highest standards of academic rigour. It often works in partnership with

academic institutions such as Institute of Rural Management Anand, KEM,

50

Massachusetts Institute of Technology, Tata Institute of Social Sciences, University of

California, Berkeley and the University of Southampton.

It is crucial that the programmes supported by SIG be time-bound. This lends clarity to

the aim of the programme and prevents its intent from getting diluted over time.

The SIG works by identifying gaps in knowledge and practice in its focus areas and

locating initiatives that address these gaps in a manner consistent with the SIG’s

mission. The identification of research needs is followed by an in-depth analysis of the

short-term and long-term implications of various forms of action. Among other things,

this requires taking a comprehensive overview of work already done in the country and

outside. The SIG, thus, seeks to answer certain fundamental questions in its focus

areas through the projects it supports and, thereby, contribute to findings that help the

sector. It should be pointed out that the SIG does not function as a rollout agency.