planningfor future ferroalloy production in...

TRANSCRIPT

VON BELOW. M.A. Planning for the futurc ferroal1oy production in South Africa. INFACON 6. Pro(:eellillg.\· oj fIJe 61h 111IenUll;olla{

Fcrroalloy.\· COlIgre.\·s, Cape Tow/!. Volume 1. Johannesburg. SA1MM, 1992. pp. 261-268.

Planning for Future Ferroalloy Production inSouth Africa

M.A. VON BELOW

University afthe Witwatersrand, Johannesburg, South Africa

Planning for long-term projects such as the establishment of new ferroalloy plantsnecessitates proper environmental scan.ning that will identify the strategic factorsdetermining a project's feasibility. Once identified, these factors need to be placed in aproper strategic-planning framework, and then analysed as to their relative importancein determining economic feasibility.

The strategic factors identified in the external societal environment are marketopportunities, local market interdependence, international trade, and exchange rates. Inthe external task environment, actions by the State, and capital and production costs arethe major determinants of a project's feasibility. Mineral raw materials, industrystructure, manpower, and technology are the factors in the internal businessenvironment warranting priority attention when future ferroalloy ventures are planned.

South Africa, with its vast reserves of economically exploitable ferrous-metal oresand coal. has the potential to substantially expand its production of ferroaJloys. Theproper planning for such expansions will ensure that this potential is turned into reality.

IntroductionAn economic analysis of ferroalloy production hasidentified the key success factors that determine financialand competitive feasibility. These factors, known asstrategic factors, indicate those aspects which need priorityattention when industrial expansions are contemplated.The barriers of entry into ferroalloy production areprimarily access to the markets and an understanding ofhow they operate, secure access to raw materials, knowhow, skilled personnel, and availability of capital.

This paper identifies the factors determining thefeasibility of future fen'oalloy ventures in South Africa andproposes a strategic-planning framework that incorporatesthese strategic factors.

Theoretical EvaluationEconomic theory facilitates a better understanding of thedeterminants influencing the establishment of newferroalloy production capacity. Of pmticular interest i.n thisrespect are the modern dynamic trade theories, the theoryof tnineml supply, and the location theory.

Modern Dynamic Trade TheoriesModern trade theories such as the technology-gap, productlifecyc]e, and scale-economy theories are also known as theneo-technology theories. They refer to technologicaldifferences between trading partners in explaining tradepatterns I. These theories also shed some light on thefeasibility of future industrial expansions in differenteconomic regions.

The nco-technology theories recognize influencesaffecting trade patterns. Such int1uences involve mainly thedifferences between countries in efficiency and technology,hke the introduction of new and improved products andprocesses, and the realization of scale economies in thedomestic market.

The dramatic growth in the South African ferrochromiumindustry supports the theory that technological change willchange trade patterns. The advent of the argon-oxygendecarburization (AOD) process in stainless-steel productionmade it possible to utilize charge chromium produced fromlow-grade South African chromites. Prior to this technological breakthrough, the suitability of local chromium oresfor the production of stainless steel was limited by their lowchromium-to-iron ratios.

If South African companies are prepared to invest intechnology, the neo-technology trade theories suggest thatthey could successfully establish additional ferroalJoyproduction capacity to supply the international market.These theories. however, also suggest that the availabilityof vast local ore deposits alone does not give localbeneficiators a comparative advantage in supplying refinedcommodities. The considerable tonnages of byproductchromite [mes generated by platinum producers mining theUG-2 Reef have little economic value unless technology isdeveloped to enable them to utilize these reserves. Theanswer might lie in perfecting the Plasmasmelt technology.Only by employing the best technology and ensuring thatoptimal production efficiency is maintained can localproducers hope to compete successfully on the internationalmarket.

PLANNING FOR FUTURE FERROALLOY PRODUCTION IN SOUTH AFRICA 261

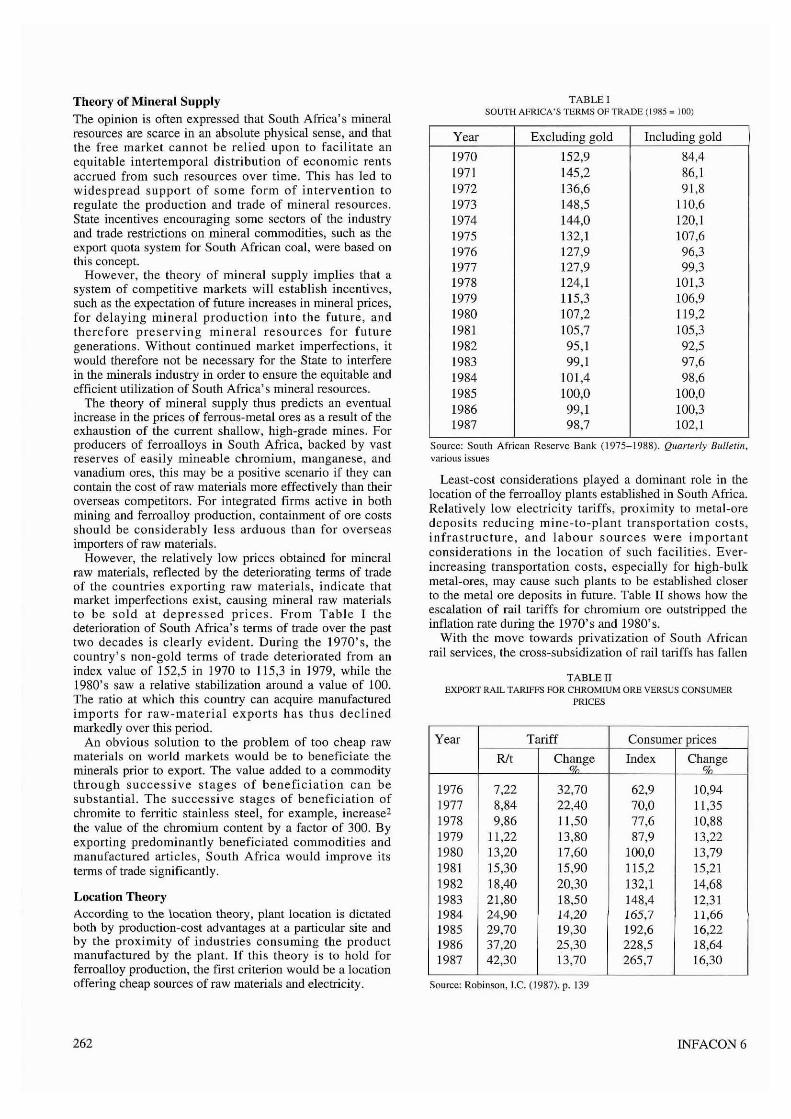

Theory of Mineral SupplyThe opinion is often expressed that South Africa's mlneralresources are scarce in an absolute physical sense, and thatthe free market cannot be relied upon to facilitate anequitable intertemporai distribution of economic rentsaccrued from such resources over time. This has led towidespread support of some form of intervention toregulate the production and trade of mineral resources.State incentives encouraging some sectors of the industryand trade restrictions on mineral commodities, such as theexport quota system for South African coal, were based onthis concept.

However, the theory of mineral supply implies that asystem of competitive markets will establish incentives,such as the expectation of future increases in mineral prices,for delaying mineral production into the future, andtherefore preserving mineral resources for futuregenerations. Without continued market imperfections, itwould therefore not be necessary for the State to interferein the minerals industry in order to ensure the equitable andefficient utilization of South Africa's mineral resources.

The theory of mineral supply thus predicts an eventualincrease in the prices of ferrous-metal ores as a result of theexhaustion of the current shallow, high-grade mines. Forproducers of ferro alloys in South Africa, backed by vastreserves of easily mineable chromium, manganese, andvanadium ores, this may be a positive scenario if they cancontain the cost of raw materials more effectively than theiroverseas competitors. For integrated fIrms active in bothmining and ferroalloy production, containment of ore costsshould be considerably less arduous than for overseasimporters of raw materials.

However, the relatively low prices obtained for mineralraw materials, reflected by the deteriorating terms of tradeof the countries exporting raw materials, indicate thatmarket imperfections exist, causing mineral raw materialsto be sold at depressed prices. From Table I thedeterioration of South Africa's terms of trade over the pasttwo decades is clearly evident. During the 1970' s, thecountry's non-gold terms of trade deteriorated from anindex value of 152,5 in 1970 to 115,3 in 1979, while the1980's saw a relative stabilization around a value of 100.The ratio at which this country can acquire manufacturedimports for raw-material exports has thus declinedmarkedly over this period.

An obvious solution to the problem of too cheap rawmaterials on world markets would be to beneficiate theminerals prior to export. The value added to a commoditythrough successive stages of beneficiation can besubstantial. The successive stages of beneficiation ofchromite to ferritic stainless steel, for example, increase2

the value of the chromium content by a factor of 300. Byexporting predominantly beneficiated commodities andmanufactured articles, South Africa would improve itsterms of trade significantly.

Location TheoryAccording to the location theory, plant location is dictatedboth by production-cost advantages at a particular site andby the proximity of industries consuming the productmanufactured by the plant. If this theory is to hold forferroalloy production, the first criterion would be a locationoffering cheap sources of raw materials and electricity.

262

TABLE ISOUTH AFRICA'S TERMS OF TRADE (1985 == 100)

Year Excluding gold Including gold

1970 152,9 84,41971 145,2 86,11972 136,6 91,81973 148,5 110,61974 144,0 120,11975 132,1 107,61976 127,9 96,31977 127,9 99,31978 124,1 101,31979 115,3 106,91980 107,2 119,21981 105,7 105,31982 95,1 92,51983 99,1 97,61984 101,4 98,61985 100,0 100,01986 99,1 100,31987 98,7 102,1

Source: South Afncan Reserve Bank (1975-1988). Quarterly Bulfeflll,various issues

Least-cost considerations played a dominant role in thelocation of the ferroalloy plants established in South Africa.Relatively low electricity tariffs, proximity to metal-oredeposits reducing mine-to-plant transportation costs,infrastructure, and labour sources were importantconsiderations in the location of such facilities. Everincreasing transportation costs, especially for high-bulkmetal-ores, may cause such plants to be established closerto the metal ore deposits in future. Table II shows how theescalation of rail tariffs for chromium are outstripped theinflation rate during the 1970's and 1980's.

With the move towards privatization of South Africanrail services, the cross-subsidization of rail tariffs has fallen

TABLE IIEXPORT RAIL TARIFFS FOR CHROMIUM ORE VERSUS CONSUMER

PRICES

Year Tariff Consumer prices

Rlt Ch~~ge Index Ch~~ge

1976 7,22 32,70 62,9 10,941977 8,84 22,40 70,0 11,351978 9,86 11,50 77,6 10,881979 11,22 13,80 87,9 13,221980 13,20 17,60 100,0 13,791981 15,30 15,90 115,2 15,211982 18,40 20,30 132,1 14,681983 21,80 18,50 148,4 12,311984 24,90 14,20 165,7 11,661985 29,70 19,30 192,6 16,221986 37,20 25,30 228,5 18,641987 42,30 13,70 265,7 16,30

Source: Robinson, I.e. (1987). p. 139

INFACON6

away. Through this system. the erstwhile South Africantransport services subsidized the transportation of lowvalue ferrous metal ores from large profits on thetransportation of low-bulk higher-valued commodities suchas ferroalloys. on the principle of charging what the productcould bear. The location of the most recent ferrochromiumplants close to the chromium mines near Rustenburg, andof Samancor's manganese sinter plant at the MamatwanMine. arc cases in point.

The impuct of a local consuming market on the locationof ferroalloy plants in South Africa is exhibited in theestablishment of a ferrosilicon dense-medium plant to servethe local mining industry. The need for improved methodsof diamond recovery provided the initial stimulus on whicha whole new industry was founded in South AfricaJ . Theproximity of a consuming market appears to have been anincentive to initially locate ferroalloy plants close to steelmills in the industrialized countries. Higher transportationcosts for higher-value commodities and better consumerproducer liaison between firms situated in the same countrymay have been the re..1sons for this.

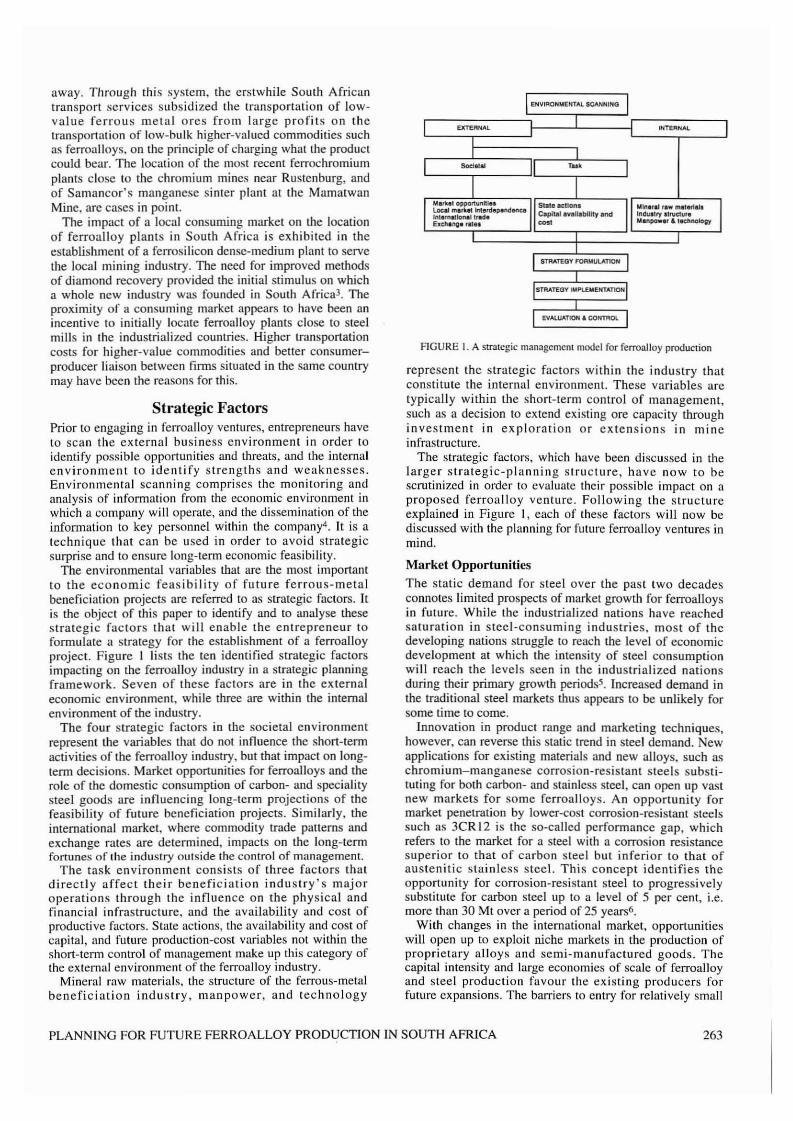

Strategic FactorsPrior La engaging in ferroalloy ventures, entrepreneurs haveto scan the external business environment in order toidentify possible opportunities and threats, and the internalenvironment to identify strengths and weaknesses.Environmental scanning comprises the monitoring andanalysis of infoonation from the economic environment inwhich a company will operate, and the dissemination of theinformation to key personnel within the company4. It is atechnique that can be used in order to avoid strategicsurprise and to ensure long-term economic feasibility.

The environmental variables that are the most importantto the economic fCHsibility of future ferrous-metalbeneficiation projects arc referred to as strategic factors. Itis the object of this paper to identify and to analyse thesestrategic factors that will enable the entrepreneur toformulate a strategy for the establishment of a ferroalloyproject. Figure I lists the ten ident.ified strategic factorsimpacting on the ferroalloy industry in a strategic planningframework. Seven of these factors are in the externaleconomic environment, while three are within the internalenvironment of the industry.

The four strategic factors in the societal environmentrepresent the variables that do not influence the short-termactivities of the ferroalloy industry, but that impact on longterm decisions. Market opportunities for ferroalloys and therole of the domestic consumption of carbon- and specialitysteel goods are influencing long-term projections of thefeasibility of future beneficiation projects. Similarly, theinternational market, where commodity trade patterns andexchange rates are determined, impacts on the long-termfortunes of Ihe indusl-ry outside the control of management.

The task environment consists of three factors thaidirectly affect their beneficiation industry's majoroperations through the influence on the physical andfinancial infrastructure, and the availability and cost ofproductive factors. State actions, the availability and cost ofcapital, and future production-cost variables not within theshort-teon control of management muke up this category oflhe external environment of the ferroalloy industry.

Mineral raw materials. the structure of the ferrous-metalbeneficiation industry, manpower, and technology

EHVIRO"'MENTAl, SCAN"'I ...G

....TEA...At.

Iollnlr" rl. mltllt1...InlNllry .1nKluflManpowlf & ledlntllogy

STRATEGY FOFUlUViT'O...

STRAT£GY IMPl.£MENTATlO...

EVAlUATlON .. COHmOl

AGURE I. A strategic m:lI1agcmenl model for fcrroalloy production

represent the strategic factors within the industry (hatconstitute the internal environmenL. These variables aretypically within the short-term control of management,such as a decision to extend existing ore capacity throughinvestment in exploration or extensions in mineinfrastructure.

The strategic factors, which have been discussed in thelarger strategic-planning structure, have now to bescrutinized in order to evaluate (heir possible impact on aproposed ferroalloy venture. Following the structureexplained in Figure I, each of these factors wiII now bediscussed with the planning for future ferroalloy ventures inmind.

Market Opportunities

The static demand for steel over the past two decadesconnoles limited prospects of market growth for ferroalloysin future. While the industrialized nations have reachedsaturation in steel-consuming industries. most of thedeveloping nations struggle to reach the level of economicdevelopment at which the intensity of steel consumptionwill reach the levels seen in the industrialized nationsduring their primary growth periodsS. Increased demand inthe traditional steel markets thus appears to be unlikely forsome time to come.

Innovation in product range and marketing techniques,however. can reverse this static trend in steel demand. ewapplications for existing materials and new alIoys, such aschromium-manganese corrosion-resistant steels substituting for both carbon- and stainless steel, can open up vastnew markets for some ferroalloys. An opportunity formarket penetration by lower-cost corrosion-resistant steelssuch as 3CR 12 is the so-called performance gap, whichrefers to the market for a steel with a corrosion resistancesuperior to that of carbon steel but inferior to that ofaustenitic stainless steel. This concept identifies theopportunily for corrosion-resistant steel to progressivelysubstitute for carbon steel up to a level of 5 per cent. Le.more than 30 Mt over a period of25 years6.

With changes in the international market, opportunitieswill open up to exploit niche markets in the production ofproprietary alloys and semi-manufactured goods. Thecapital intensity and large economics of scale of ferroalloyand steel produclion favour the existing producers forfuture expansions. The barriers to entry for relatively small

PLANNING FOR FUTURE FERROALLOY PRODUCTION IN SOUTH AFRICA 263

newcomers to these activities restrict their participationmainly to mining and the fabrication of final products.

However, opportunities exist for smaller risk-takingentrepreneurs to exploit innovative financing, management,and marketing strategies to establish new ferroalloyventures. John Vorster's Chromecorp Technology andVanadium Technology are examples of this type of venture.Once they have been proved to be economically feasible,the larger institutions may choose to take over suchoperations, as happened in the cases of Batlhako and Purity.

Local Market Interdependence

The shift of ferroalloy production capacity away fromconsumption centres in industrialized countries suggeststhat local-market interdependence no longer plays a veryimportant role in the location of ferroalloy plants. Theavailability of smelting technology and efforts towards theminimization of production costs have played a moreimportant role in the location of ferroalloy plants over thepast two decades.

However, for the fabrication of ferrous-metal consumerarticles, the presence of a domestic market proves to be adetermining factor for the economic feasibility of abeneficiation industry. Such a market not only provides asecure outlet for sales; it is also conducive to thedevelopment of the technological and marketing know-hownecessary to penetrate export markets7.

The locational interdependence of firms or demandforces is evident in the local market for mining equipmentand for the materials consumed in mining and mineralsprocessing. Atomized and milled ferrosilicon weredeveloped in South Africa for the dense-medium separationof heavy minerals such as diamonds and andalusite.Opportunities for supplying the extensive local miningindustry with con-asian-resistant steel could be investigatedfor future niche markets. In 1989, the gold mines who aremembers of the Chamber of Mines consumed 37,4 millionrands' worth of steel sections, of which only 4 per cent wasstainless steels.

International Trade PatternsThe consumption of ferroalloys in South Africa is verylimited compared with that of the world as a whole.Mineral-beneficiation operations typically exhibit largeeconomies of scale, necessitating marketing on the largerinternational market. International trading in ferroalloysensures the economic feasibility of mining andbeneficiation activities in South Africa. In order to optimizethe gains from the country's natural resources in the fonnof vast are deposits, a sophisticated marketing strategy forferro alloys needs to be planned and executed.

The deteriorating terms of trade faced by exporters ofraw materials point to the urgent need for a strategy ofbeneficiation prior to export. South Africa's poor economicgrowth over the past decade, coupled with the need foremployment opportunities and economic advancement ofthe masses, necessitates a poljcy of adding value to exports.Economic aspirations kindled by political reform will haveto be addressed in the short term. Policies on inwardindustrialization alone will not enable this country toacquire wealth-generating capital equipment from abroad.

Exchange RatesA deteriorating rand exchange rate during the 1980's was amixed blessing for ferroalloy producers in South Africa.Over this period, the rand was devalued far more than was

264

necessary to offset the rise of the domestic inflation rate,mainly due to a deterioration in the country's internationalpolitical standing. While this impacted positively on therand returns from ferroalloy exports, it had the oppositeeffect on the rand costs of capital-equipment imports tosustain the growth of ferroalloy production capacity. Thecconornic feasibility of greenfields ferroalloy ventures, bynew entrants in particular, was compromised by adeteriorating rand exchange rate.

Furthermore, South African firms have had to contendwith an exceptionally unstable rand exchange rate since therand was allowed to float freely in September 1983.Exchange-rate movements in excess of 5 per cent haveoccurred on single days since the inception of the freelynoating rand. Volatile exchange rates create an element ofuncertainty in projecting future income and expenditurescenarios, which in turn cast a doubt on project feasibiLity.By stabilizing the rand exchange rates, the South Africanauthorities could create an environment more conducive lofuture expanded ferroalloy production.

State Actions

The role of the State in future ferroalloy projects shouldprimarily be that of creating a level of competence in thenational labour force to support an expanded fen'ous-metalbeneficiation industry. The allocation of resources to thetraining and schooling of technologists and engineers willachieve more in promoting exports of value-added productsthan expensive export incentives.

Such incentives have failed to playa major role in theestablishment of new felToalloy plants9. A recent study bythe National Productivity Institute showed lhat 85 per centof the companies surveyed were not motivated to export bythe General Export Incentive Scheme, and 95 per centindicated that they rely on their own efforts to secure exportorders 10. The companies surveyed included prominentferroalloy and steel producers of South Africa.

Feasibility studies into the establishment of multi-millionrand projects such as ferroalloy smelters tend to concentrateon sound economic factors such as production costs andmarket opportunities, with Stale incentives regarded only asmarginally influential variables. Apart from creating adomestic level of competence, the State could create aneconomic milieu conducive to the establishment ofbeneficiation activities by relaxing regulatory restrictionson fabricating activities. Small-scale fabricators of steelcommodities may well be the ultimate incentive for localferroalloy production.

Capital Availahility and Cost

Capital scarcity for long-term capital-intensive investmentsmay prove to be one of the major constraining factors of anexpanded ferroalloy industry in South Africa. A flighl ofcapital due to economic sanctions and low real domesticinterest rates resulting from State manipulation have to becountered to resolve this problem. Existing corporations inthe ferroalloy industry utilizing retained earnings thereforehave little competition from newcomers, creating amonopolistic structure.

Relatively high levels of investor expectations andcorporate tax rates cause the cost of capital in South Africato be higher than in most of the other major ferroalloyproducing countries. According to a study by the SouthAfrican Chamber of Business, the cost of capital in Soulh

INFACON6

Sourl'C: Von Relow. M.A. (11)1)0). p. 235NoH:: Rophuthutsw:lIl:l's sharc of Imdc i" cxcluded after 1977

-

Year Chromium Iron Manganese

1960 6.8 87.0 -1965 20,9 79.3 -1970 24,4 66,7 -1975 37,4 74,4 19.71976 42,9 74,6 29,01977 45,5 41.2 30.5197~ 43.2 41,0 36.01979 50.8 38,6 34.91980 51.8 45.9 33.71981 47.3 45.8 36.41982 48.4 47.4 36,21983 63.7 54.2 29.81984 M.O 44,0 27.61985 58,0 51,0 34,31986 67,4 54.5 40.019~7 64,7 55,8 49,71988 60.8 50,8 37.1

TABLE IIIl.OCAL IlENEF1CIATIUN RATIOS OF f-""ERROUS-METAL ORES

(LOCAL SALE MASS AS'~ UI· TOTAl SALE MASS)

manganese mining industries \Vcre developed for the exportmarket. [t therefore follows that most of the locally minediron ore was processed into iron and stecl mainly by Iscorin 1960, while only 6.8 per cent of the locally milledchromium ore was processed in South Africa during thesame year.

The opposing trends in thc chromium and mangancseindustries. on the one hand. und the iron industry. on (heother. retlect the different reasons for their csrablishment.

The South African steel industry, in the form of Iscor,was established by the State mainly for strategic reasons.making South Africa self-sufficient in steel and creating adomcstic level of competence in metallurgical know-how.The profit motive was thus not a major factor, evidenct:d bythe reluctance of local entrepreneurs and Jarriel' mininu. c ccompames (Q establish largc-scale Slccl mills after thediscovery of the large iron-ore deposits at Sishen andThabazimbi_

The profitable internation;,d market for chromium :'lI1dmanganese ore. however. encouruged private companies toexploit such ore deposits soon after their discovery. Whilemaking profits by expol1ing orcs, these companies had littleincentive to engage in complicated pyrometallurgicalbeneliciation processes. As their knowledge of the marketand Ihe required tcchnology expanded. these companiesrecognized the market opportunities for ferroalloys, andexpanded their opero:ttions into thc smelting of chromiullland manganese ores.

Figure 2 Clc~lrly inuil:ates lhe lrends mentioned and alsosuggests a f1allening uut or local bencficiation ratios foriron and manganese :.H about 50 per ccnt for iron and justbelow 40 per cent fur manganese. Even though SOlullAfrica has the iron-orc exporting infrastrucl"ure in theSishcn-Saldanha scheme to further penetrate theinternational iron-ore market. intense competition fromcountries such as Brazil and Australia will CJ1.'mre thmiron's local bcneficiation ratio will not decline much below50 per cent. The local benefit;iation or manganese could,

AfricOl is 3/./ per cent. which means Ihat, for each R I nooused in the funding of working capital and capital stock. amargin of R31 I would be required lO service the cost ofcapital ". This compares with 14,5 per cent in Australia,I 1,4 per cent in the USA. and 3.4 per cent in Japan.

It is therefore clem that measures will have to be trlken toaddress this imbalance if invcstors are to be attracted tocapital-intensive ferroalloy projects. The State's acceplilnceof the measures in Scction 37E of the Income Tax Act of1962 is a positive development in this respect. Section 37Eallows for accelerated capital write-offs on new projectsinvolving mineral benelieiation for the export market.

Production Costs

Trends in future production costs. including transport~llion

costs. suggest changes in the design and location of futureferroalloy plants. Increasing electricity costs with thedemise of the power-rebate scheme will favour prereduction technology. Large-scale electricity consumers inSouth Africa are in an enviable position in that they aresupplied by a low-cost producer with a well-developedinfrastructure and an overcapacity in dectricity-generatingfacilities. Eskom has indicated lhat it is willing to negotiatefavourable long-term power tariffs with large consumerssuch us ferroalloy plants.

The incorporation of more effective pollution-abatementequipment in the design of future plants has becomemandatory in our society. where the protection or theenvironment enjoys increasing support. The costs of suchequipment contribute significantly to the capital costs ofnew plants. while the retrolitting of existing plants can beeven more expensive. The recycling of waste products suchas slag and flue dust may present producers with costsaving opportunities.

Higher transportation costs for ferrolls-melal orcsresulting from the abolition of rail-tariff cross-subsidizationwill favour beneficiation prior to export and Ihe location offerroulloy plants closer to the metal-ore deposits. Thisfollows a general shift in domestic policy from a policyfavouring raw-material production and export to one ofadding value to locally produced commodities.

Mineral Raw Materials

The availability of large reserves uf easily exploitableferrous metal and coal reserves gives Soulh Africanferroalloy producers a compurative advantuge oninternational markets. The question needs to be askedwhether the producers. in fact, capitalize on this advantage.The analysis of ferrous-mctal trade statistics gives someindication of the level of development of the South Africanferroulloy industry 12.

I f the percentage of total annual ore sales represented bylocal sales is calculated. a clear trend in the localconsumption of ferrous metals in primarily ferroaHoy andslee! production call be obtained. Table III and Figure 2show the local beneficiation ralios of the three ferrousmetals saleable in both r<.lW and beneficiated form. i.e.chromium, iron. and manganese. Nickel. silicon. andvanudium ure not normally Ir<tded as ores and cannot beanalysed in the same way.

Up to the 1980s. iron displayed a declining trend in thelocal beneliciution ratio compared with the increasing localbeneficiation of chromium and manganese. Whereas thelocal iron-ore mining induslry was esti.lblished primarily tosustain the local steel industry, the chromium and

PLANNING FOR FUTURE FERROALLOY PRODUCTION IN SOUTH AFRICA 265

%

Manpower and Technology

Inadc4uate local manpower and technologicalinfrastructure will severely impair future developments inthe South African ferroalloy industry. The lack of skilledmanpower and the dearth of resources allocated to researchand development of innovative metallurgical technologyhave a constraining effect on new ferrous-metalbeneficiation projects. International trade theory andhistorical example, such as the impetus given to the localferrochromium industry by the development of AGOtechnology, emphasize the importance of technologicaldevelopment.

The StiHe's role in the education and training of adequatemanpower and the allocation of more resources to researchand development should be more pronounced in future. Aconstructive role in this respect would be more beneficiallothe ferroalloy industry than ad hoc export incentives merelyrepresenting the re-allocation of resources in the localeconomy.

Samancor and Purity by eMI supports the contention thatthe larger firms have an advantageous position in theproduction of ferroalloys.

Locnl producers have to maintain 11 competitive capacily.i.e. the ability to compete, owing to the availability oftechnical know-how and physical infrastructure, in theirefforts (owards international competitiveness l3 . Again,those companies well established in ferroalloy, produclionhave an advantage over new entrants on the basis ofcompetitive capacity.

Relative Importance of Strategic Factors

An analysis of the relative importance of the factorsdetermining the economic feasibility of future ferrousmetal beneficiation projects may prove to be crucial in theselection .1I1d location of projects. By knowing whichfactors are considered to be more important in thedetermination of project feasibility, entrepreneurs canallocate priority attention to them when contemplating newventures.

Table IV depicts the results of a survey among theproduction and marketing managcment of the SouthAfrican ferrous-metal beneficiation industry. According lothis survey. the most important consideration in theplanning of new projects is the projected market conditionsfor the saleable product, with a 23 per cenl weighting. Theavailability of domestic metal-ore and low-cost energysupplies is ranked next, with a 15 and 14 per cent weightingrespectively. Following these factors are the exchange-rateprojections, at 10 per cent weighting, and the availabilityand cosl of capital, at 8 per cenl. The remaining factors are

AnalysisAfter the first planning stage of a project, when thestrategic factors have been identified and put into astrategic-planning framework, the assumptions behindthese factors should be analysed and a financial valuationof the project made.

The first can be achieved by the gathering of analyseddata from experts in the industryl-l. In this study, aquestionnaire was sent out to selected individuals requestingtheir considered opinion on the relative importance of thestrategic factors identified in this paper.

-Manganese-Chromium - Iron

80,-----------------------,

however, increase towards 50 per cent if new beneticiationopportunities, such as the market acceptance of manganesebased stainless steels and new manganese chemicals. arerealized.

The beneficiatjon of chromium is still experiencing agrowth phase in the South African industry, and could leveloff to the processing prior to export of around 80 per centof aU locally mjned chromium orc. The recent expansionsin fCITochromium capacity by South African producers andthe establishment of new facilities such as Ballhako,Chromecorp Technology. and CMl Rustenburg (Purity) areindicative of this trend.

The economic virtues of a diversified export marketshould be kept in mind in <lny consideration of thc level oflocal beneficiation for ferrous-metal ores. To some, theefforts towards 100 per cent local beneficiation ofdomestically mined raw materials represent optimality, buta level of beneficiation dictated by the free market willsatisfy the prerequisites of optimality. If it' seemseconomically feasible to export 20 per cent of locallymined chromium ore without any beneficiation, the absenceof restrictions on such trade will result in a Pareto-optimalchromium trade for this country. A diversified export tradeoperating in the markets for both raw and beneficiatedcommodities 1s also less vulnerable to any severefluctuations in one particular market.

However, the presence of substantial ferrolls-metaldeposits does not automatically lead to the conclusion thatlocal beneficiation activities would be economicallyfeasible. Production-cost elements other than those formetal ores and coal, such as those for capital and skilledmanpower, may prove to be significant determinants of thefeasibility of beneficiation projects. Vertical integration offerrous-metal mining and beneficiation activities couldprovide South African companies with a larger flexibility incost controls, and assure them of supply security. Thesefactors may prove to be valuable in the future ferroalloymarket of tbe world.

Industry StructureThe vertically integrated structure of South Africa's ferrollsmetal beneficiation industry favours companies currentlyproducing ferroalloys to engage in future exp'lllsions ofbeneficiation capacity. Funhermore, the capital intensityand large economies of scale of ferroalloy plants favourfirms with the financial backing of larger institutions suchas the mining houses. The takeover of Batlhako by

o,:97:::S"719;:"::6-,;;,:C77;-;:19~':-'::19:":-'-:'::'80:::-"719::,:::,-:,-=,,",:-:::19:C83;;-::19::';84::-:'-!""S'--,",:C";;-::19::';'"C:'""19::!"

FIGURE 2. LOI.:al beneficiation ratios(Source: Table III)

2OjL ---1

266 INFACON 6

Conclusion

feasibility of ferrochromium projects will be particularlysensitive to the costs of electricity, transportation. are. andcarbon material.

The expert survey and cost analysis used in the evaluationof the strategic factors detennining the economic feasibilityof ferrous-metal projccts show a significant correlation ofresults. The questionnaire indicated that marketopportunities (weighting indcx 23) and exchange rates(weighting index 10) arc eon<idered by experlS in theindustry to be very import3nt to the economic feasibility ofprojects. A strong demand for the product and a favourableexchange rate will result in relatively high rand prices forlocal producers. From DCF sensitivity analyses conductedby the author, variations in product prices were shown to bethe major detenninant of a project's feasibility 16.

The survey among experts in the industry indicated Ihalthe costs of rilW materials (weighting index 15) and energy(weighting index 14) deserve close sCnltiny in the planningof future ferrous-metal projects. The production costs inTable V indicate that these variables are impoJ1ant in thedetermination of a project's feasibility.

perceived to be of lesser imporlance. receiving evaluationswith a weighti ng of bel ween I and 7 per cenL

Financial Vnluationferroalloy projects can be evaluated by usc of severalanalytical methods. Conventional approaches includevariou< derivative. of the discounted cash flow (DCF)anaIY!'iis. which assumes that a project's value i~ determinedby the present value of the project's incremental cash newsdiscounted at an appropriarc cost of capital. The pro !omwcash flows are then subjected to risk analyses such as asensitivity analysis and the Monte Carlo simulation.

A sensitivity analysis investigates the effect of changes incrucial variables on the nel present value (NPY) andinternal rate of return (fRR). The Monle Carlo simuhllionconsiders changes on all variables simuhaneously, based onspecified probability distributions for those variables. Theprobability distribution of the variable is then sampledrandomly, and the samples are combined according to thecash-tlow stnlcture. After several sets of samples have beencomputed (say 500 to 1000 iterations), stable probabilitydistributions of annual cash flows are simulated.

The DCF methods, however, break down when appliedto cyclical projects subject to active management. as in thecase of ferroull oys l5. The flexibility of managerial response The contention that South Africa's ferroalloy industry canto external developments, such as price fluctuations, is not be expanded in future is supported by both theoretical and

I d I F I Practical considerations. Taken thut future marketconsidered adequately in the DCF met 10 oogy. or ong-term ferroalloy projects. management rarely stays within opportunities represent thc major determinant of thcthe operating plans assumcd for the feasibility study. feasibility of a beneficiation project, the inlernationaltrendManagers may modify their capacity ill response to price lowards durable consumer commodities and lifecyclefluctuations, or may implement alternative technology as it costing for capital projccts impacts positively on futurebecomes available, expansions of corrosion-resistant sleels that utilize

In contrast to traditional DCF melhods, options-based chromium, nickel, and, to a lesser extent, manganese. It istechniques of projecl valuation or conlingent claims analysis believed that the increasing concern for the environment(CCA) take managerial Oexibility into account. CCA is will result in an increased demand for materials suitable forbased on the principle of traded options, which gives recycling, such as stainless steels, and an ever-increasingmanagement the right. but not the obligation, to engage in rejection of materials pcrceived 10 pollute the environment,future transactions. However. this approach of project such as plastic consumer articles,valuation is not yel sufficicntly developed to provide a In the ferroalloy industry in panicular, there is scope forpractical substitute for the DCF analysis. the pre-reduction and sintering of ferrous-metal orcs.

The cost structure of a typical South African fcrro- Samancor's manganese-ore sintcring phmt near Hotazel haschromium plant (Table V) show~ the relative importance of proved to be a successful expansion in lhis sector'scost variables. It clearly indicates lhat the financial beneficiation industry. The resultant increase in

TABLE tVFACTORS DETERMINING THE FEASIBILITY OF FUTURE FERROUS-METAL BENEFICIATION FACIUTIES

FactorPercentage weighting

I 2 3 4 5 Av

Market opportunities for the saleable product 10 25 20 30 30 23Local metal-ore deposits 25 5 20 10 15 15Energy costs and energy availability 25 20 10 5 10 14Exchange-rate projections 5 15 10 10 10 10Capital costs and capital availability 10 10 5 5 10 8Escalation in other produclion and Lransport costs 10 5 5 to 5 7State export incentives 5 10 5 5 5 6Skilled-manpower availabilily 5 5 5 10 5 6Technologicul innovation and its availability 5 5 5 10 5 6Domestic consumption of the final product 0 0 10 5 5 4Other factors (taxation, labour relations, elc.) 0 0 5 0 0 I

Total 100 100 100 100 100 100

Note: A nlJ1dolll sample oj five fcrroalloy productlun and Illllrkellng manager S opInIons was used Il1lhls analysn;. alld the average ofthclr pcrccllIagcweighting was taken to be rcprcscl1l,llivc or tile South Afric:lIl ferrous-llletal beneficiation inuustry.Source: Von Below, M.A. (1990). p. 294

PLANNING FOR FUTURE FERROALLOY PRODUCTION IN SOUTH AFRICA 267

TABLE VPRODUCTION COSTS FOR A SOUTH AFRICAN FERROCHROMIUM PLANT

IN 1991

Cost component US$/t

Electricity (4390 kWh per ronnel 135

Transport (plant 10 market) 122

are 75

Carbon materials 58

Labour 36

Fluxes, electrodes, etc. 16

Working capital 10

Other direct costs 97

Note: Costs are expressed in 1991 US dollars per lonne of chargechromium producedSource: Confidential industry sources and :lurbor's estimates

ferromanganese-smelling efficiency by use of the sinterproduct created a substantial international demand for theproduct. A similar increased smelting efficiency. achievedthrough the pre-reduction of chromium and iron ores, hasestablished such beneficiation practices for futureexpansions.

An exciting opportunity for the expansion ofbeneficiation may lie in the production of fabrication alloysthrough the promotion and large-scale production ofmanganese-containing stainless steels l? The excellentcorrosion-resistant, high-strength, and low-cost properliesof these steels will act in favour of market development andthe creation of international demand to warrant theestablishment of large-scale mills for their production. Thelocal beneficiation of South Africa's chromium, iron,manganese, and nickel resources will be substantiallyenhanced by the creation of an industry producingmanganese-containing stainless steel.

The question of what needs to be done to facilitate newferroalloy ventures can best be answered by an analysis ofthe State's role in the promotion of local beneficiation. Anevaluation of the State's export incentives and exchangerate policy, for example, has indicated that past policies hadlittle effect in creating an environment conducive to theestablishment of new private-industry projects on thebeneficiation of ferrous metals, with the possible exceptionof the rebate on electrical power that was applicable insome instances 18 . The promotion of manpowerdevelopment and technological research and developmentwill prove to be more beneficial to future industrial growththan the ad hoc incentives propagated so far. The creationof a more stable socio-economic environment will have apositive impact on the future availability of capital for newprojects, and will open up markets for beneficiatedproducts that are currently subject to economic sanctions.Furthermore, the South African monetary authorities andpoliticians should be made aware of the importance ofexch'lIlge-rate stability for long-term planning.

The analysis of ferroalloy production costs suggests anumber of policy considerations for South Africanmanagers. Innovation in technology, product range, andmarketing will playa major role in keeping the industrycompetitive in a dynamic international market. Escalationsin the cost of electricity will make pre-reduction more

268

economic, while pollution-abatement technology will haveto be improved if it is to be more effective and cheaper.Escalations in transportation costs dictate that ferroalloyplants (first-stage beneficiation) should be located closer tothe metal-ore mines. However, plants that are fabricatingalloys should be at consuming centres, as dictated by theconcept of market-area locarional interdependence.

The ten strategic factors identified in this environmentalstudy indicate that South Africa finds itself in a competitiveposition to expand its ferroalloy production capacity infuture. In addressing these strategic factors scientifically,the South African ferroalloy industry will ensure itscontinued economic feasibility.

ReferencesI. Reddy, M. (1979). Dynamic theories of international

trade. Unpublished M.Com. dissertation in economics,University of South Africa, Pretoria, pp. 13-34.

2. Robinson, I.C., and Von Below, M.A. (1990). The roleof the domestic market in promoting the beneficiationof raw materials in South Africa. l.S. Afr. Illst. Min.Metall., vol. 90, p. 92.

3. Ibid., p. 94.

4. Wheelen, T.L., and Hunger, J.D. (1989). Strategicman.agement and business policy. 3rd ed,Massachusetts, Addison-Wcsley, pp. [-50.

5. Von Below, M.A. (1986). The market for SouthAfrica's ferrous metals and ferroalloys. UnpublishedM.Phi!. dissertation in mineral economics, RandAfrikaans University, Johannesburg, p. 117.

6. Armitage, K. Chromium. (1988). Paper presented at theTESSA Conference, Base metal prospects, p. 3.

7. Robinson, I.e., and Yon Below, M.A. 01'. cit., pp. 9697.

8. Chamber of Mines of South Africa. (1990). Statisticaltables 1989, p 40.

9. Von Below, M.A. (1990). The strategic factorsinfluencing future ferrous metal beneficiation in SouthAfrica. Unpublished Ph.D. thesis in mineral economics,University of the Witwatersrand, Johannesburg, pp.123-169.

10. Anon. (1991). Export promotion. Worth all the money?Financial Mail, 6 Sep., p. 68.

II. Hatty, P.R., and Lockwood, K.A. (1991). A concept forthe development of a new industrial policy for SouthAfrica. A Soulh African Chamber of Business view.Johannesburg, pp. 20-24.

12. Yon Below, MA (1990). 01'. cit., pp. 234-238.13. Robinson, I.e., and Von Below, M.A. 01'. cit., p. 96.14. Yon Below, M.A. (1990). 01'. cit., pp. 292-293.

15. Guzman, J. (1991). Evaluating cyclical projects.Resources policy. Butterworth-Heineman Ltd, pp. 114123.

16. Yon Below, M.A. (1990). 01'. cit., pp. 293-302.17. Wellheloved, D., and Stanko, J. (1989). Manganese as a

possible substitute for nickel. 7th Metal Bull.etinFERROALLOY Conference, Monte Carlo, pp. I-II.

18. Yon Below, MA (1990). 01'. cit., pp. 152-169.

INFACON6