planashland housing visioning meeting, 1/12/15

TRANSCRIPT

Ashland Housing Production PlanVisioning Public Forum

Monday, January 12, 2015

Presented by the Metropolitan Area Planning Council

Tonight’s Agenda

1. Purpose of a Housing Production Plan (HPP)

2. Affordable Housing & How It Works

3. Housing Needs & Demand in Ashland

4. Local Housing Goals, Barriers, & Opportunities

5. Next Steps in the HPP Process

Purpose of a Housing Production Plan

Purpose of a Housing Production Plan

M.G.L. Chapter 40B

• Encourages affordable housing development in

cities and towns throughout the Commonwealth

• Goal of at least 10% of a community’s housing is

affordable and recorded on the Massachusetts

Subsidized Housing Inventory

3.59% 3.66% 4.03% 4.43%

6.17%

8.33%

10.15% 10.26% 10.46%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

Source: DHCD, April 2014

Ashland Has Achieved 3.66% on the Subsidized Housing Inventory

Subsidized Housing Inventory, MetroWest Sub-Region, 2014

Purpose of a Housing Production Plan

Source: DHCD, April 2014

Town Has 241 Affordable Units

Subsidized Housing Inventory, Ashland, 2014

Purpose of a Housing Production Plan

2010 Census Year-Round

Housing UnitsSHI Units

Rental Units

Expiring Units

2017-2054

6,581 241 (3.66%) 226 (90%) 172 (71%)

Purpose of a Housing Production Plan

A Housing Production Plan (HPP) not only helps

communities meet the State’s mandatory 10%

affordable housing target , but also:

• understand local housing needs and demand

• influence the type, amount, and location of housing

• set a numerical goal for annual low- and

moderate-income housing production

HPPs include:

• a comprehensive housing needs assessment;

• analysis of development constraints and opportunities

• affordable housing goals and objectives; and

• implementation strategies

Purpose of a Housing Production Plan

To date, Ashland meets housing needs and

demand through multiple strategies, including:

• Affordable Housing Trust

• Community Preservation Act

• Development incentive for affordable housing

Purpose of a Housing Production Plan

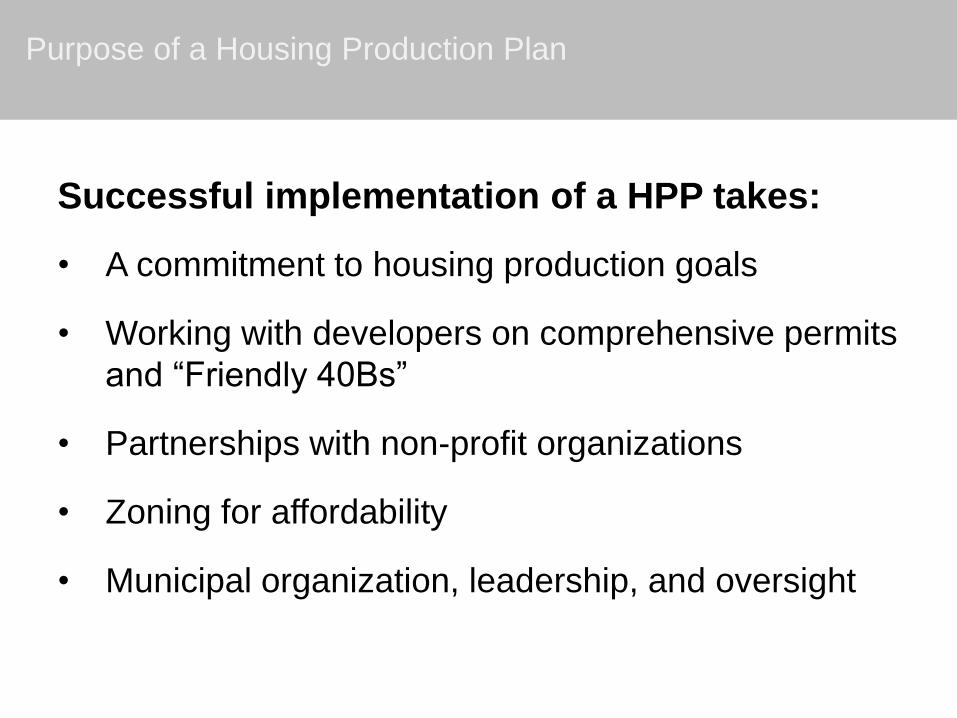

Successful implementation of a HPP takes:

• A commitment to housing production goals

• Working with developers on comprehensive permits

and “Friendly 40Bs”

• Partnerships with non-profit organizations

• Zoning for affordability

• Municipal organization, leadership, and oversight

Purpose of a Housing Production Plan

Affordable Housing & How It Works

Affordable Housing Financing

• There are many ways a community can fund its affordable housing, including the use of state or federal funding programs.

• Most projects require financial support from public sources (federal, state, local), and the funds generally come with restrictions and requirements.

• Financing options vary depending on the type of housing (rental or ownership) and the characteristics of the households a program or project is to assist (e.g., income, household size, disability status).

• Project feasibility depends upon:

– Reduced development costs and debt service (using zoning, grants, equity investments, or low-cost or soft loans)

– Reduced operating costs

– Increased rental or sales income (by renting/selling some units as market-rate)

Affordable Housing & How It Works

Affordable Housing Financing

• Financing for homeownership units depends on barriers to entry for prospective buyers.

• In a community with a supply of moderately priced housing, down-payment requirements may be the primary barrier, and assistance, or "soft-second" financing programs, may suffice.

• Other communities may choose to “buy down” existing units—including tax title and foreclosed properties—and resell them at a lower price, using subsidy funds to pay the difference.

• Others construct new affordable units, usually in small or mixed-income developments.

• There are fewer state and federal funding sources available for ownership programs. Most use conventional financing or a shallow subsidy program that provides an interest rate discount or other modest subsidy.

• Frequently used sources are from the Federal Home Loan Bank of Boston and MassHousing.

Affordable Housing & How It Works

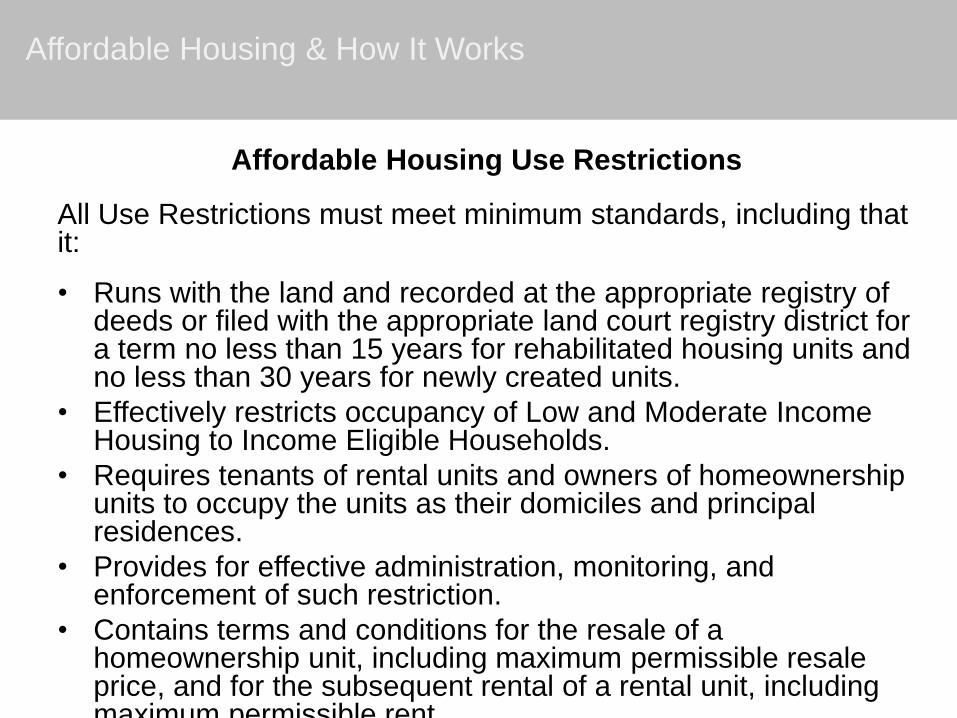

Affordable Housing Use Restrictions

All Use Restrictions must meet minimum standards, including that it:

• Runs with the land and recorded at the appropriate registry of deeds or filed with the appropriate land court registry district for a term no less than 15 years for rehabilitated housing units and no less than 30 years for newly created units.

• Effectively restricts occupancy of Low and Moderate Income Housing to Income Eligible Households.

• Requires tenants of rental units and owners of homeownership units to occupy the units as their domiciles and principal residences.

• Provides for effective administration, monitoring, and enforcement of such restriction.

• Contains terms and conditions for the resale of a homeownership unit, including maximum permissible resale price, and for the subsequent rental of a rental unit, including maximum permissible rent.

Affordable Housing & How It Works

Affordable Housing Use Restrictions

Units are subject to an Affirmative Fair Housing Marketing and

Resident Selection Plan. These plans:

• Create fair and open access to affordable housing and are designed to promote compliance with state and federal civil rights obligation.

• Apply to the full spectrum of activities that culminate with occupancy, including but not limited to means and methods of outreach and marketing through to the qualification and selection of residents.

• Include a resident selection plan, marketing, administering the initial lottery process, and determining the qualification of potential buyers and/or tenants.

• Projects must be in compliance with the Bedroom Mix Policy as set forth in the “Interagency Agreement Regarding Housing Opportunities for Families with Children.”

Affordable Housing & How It Works

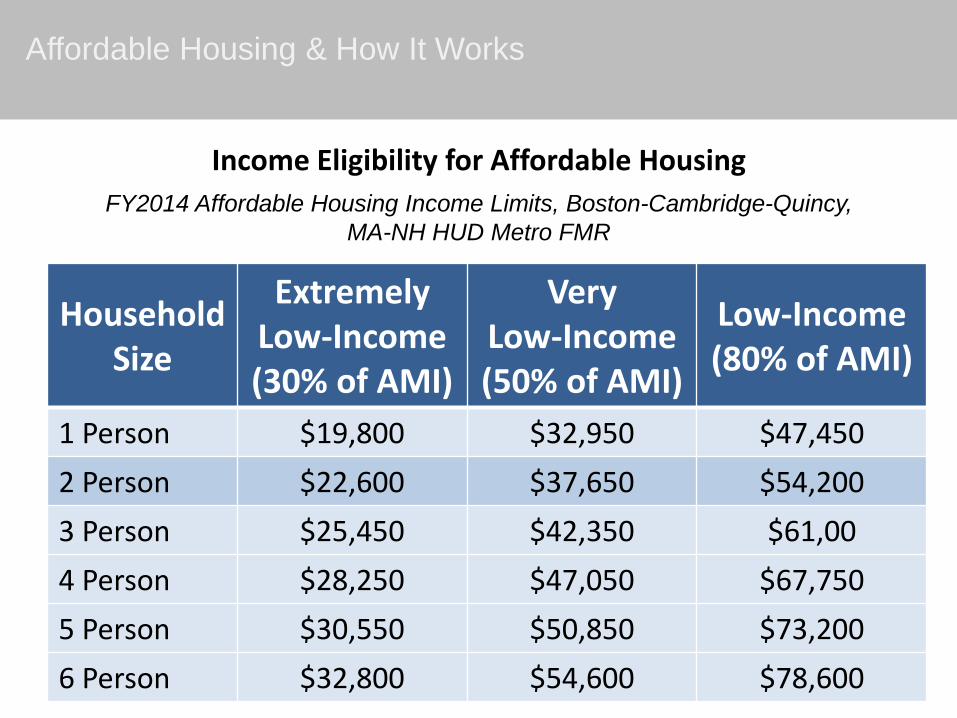

Income Eligibility for Affordable Housing – Household

Income

• An eligible household may not earn more than 80% of the area median income in order to rent or purchase a restricted unit.

• Limitations on household assets for income-eligible households:

– For age-restricted homeownership projects, household assets shall not exceed $275,000 in value, including equity in a dwelling (to be sold).

– For non-age restricted homeownership units, household assets shall not exceed $75,000 in value.

– For rental units, the greater of the following will be added to income: the income derived from the assets or an imputation of value calculated in a manner consistent with HUD requirements in place at the time of marketing.

– If a potential purchaser divests him/herself of an asset for less than full and fair cash value of the asset within twoyears prior to application, the full and fair cash value of the

Affordable Housing & How It Works

Affordable Housing & How It Works

Household Size

Extremely Low-Income (30% of AMI)

Very Low-Income (50% of AMI)

Low-Income (80% of AMI)

1 Person $19,800 $32,950 $47,450

2 Person $22,600 $37,650 $54,200

3 Person $25,450 $42,350 $61,00

4 Person $28,250 $47,050 $67,750

5 Person $30,550 $50,850 $73,200

6 Person $32,800 $54,600 $78,600

Income Eligibility for Affordable Housing

FY2014 Affordable Housing Income Limits, Boston-Cambridge-Quincy,

MA-NH HUD Metro FMR

Income Eligibility for Affordable Housing – Housing Cost

Generally, a housing subsidy program (through its statutory basis, regulations, or guidelines) establishes maximum monthly housing cost. Otherwise, the following provisions apply:

• Rental: Monthly housing costs (inclusive of utilities) may not exceed 30% of monthly income for a household earning 80% of AMI adjusted for household size, including Assisted Living Facilities.

Affordable Housing & How It Works

Income Eligibility for Affordable Housing – Housing Cost

• Homeownership:

– The downpayment must be at least 3% of the purchase price.

– Mortgage must be a 30-year fully amortizing mortgage for no more than 97% of the purchase price with a fixed interest rate no more than 2% above the current MassHousing interest rate (www.masshousing.com).

– Monthly housing costs (inclusive of principal, interest, property taxes, hazard insurance, private mortgage insurance and condominium or homeowner association fees) shall not exceed 38% of monthly income for a household earning 80% of AMI, adjusted for household size.

Affordable Housing & How It Works

Local Preference

A Local Preference Program:

• Demonstrates the need for local preference in the marketing plan.

• Justifies the extent of the local preference (the percentage of units proposed to be set aside for local preference).

• Demonstrates that the proposed local preference will not have a disparate impact on protected classes.

The Subsidizing Agency, DHCD, and the municipality must approve a local preference scheme as part of the marketing plan.

Local preference may not exceed 70% of the affordable units in a project.

Affordable Housing & How It Works

Local Preference

Allowable Preference Categories:

• Current residents: A household in which one or more members is living in the city/town at the time of application. Documentation of residency should be provided (rent receipts, utility bills, street listing or voter registration listing).

• Municipal Employees: Employees of the municipality, such as teachers, janitors, firefighters, police officers, town hall employees.

• Employees of Local Businesses: Employees of businesses located in the municipality.

• Schoolchildren: Households with children attending the locality’s schools, including METCO students.

Affordable Housing & How It Works

Resale of Affordable Housing

All resales of homeownership units must maintain ongoing Affirmative Fair Housing and Marketing Plan Requirements. In addition, units are subject to the following resale process:

• Owner provides notice regarding the sale.

• Deed riders contain strict timelines regarding resale. Once notified of a resale, the municipality must act swiftly to locate an income-eligible buyer.

• Additional requirements include a Resale Plan, working from a Ready-Buyer List, and calculating any Capital Improvements.

• A “ready-buyer” list of eligible buyers may be created through local, regional, and statewide resources. It should continually be analyzed, maintained, and updated (through additional marketing) so that it remains consistent with the objectives of the housing program and is adequately representative of the racial, ethnic, and other characteristics of potential applicants in the housing market.

Affordable Housing & How It Works

Affordable Housing & How It Works

Questions?

Housing Needs & Demand in Ashland

Housing Needs & Demand in Ashland

40s & 50skids move out, travel, save for

retirement?

30smarried,

employed,kids?

20ssingle, career

development?

70+age in place?

60sretire,

downsize?

1. When did you move

to Ashland and into

what kind of home?

2. What kind of home

do you live in

today?

3. What kind of living

situation will you

want in the future?

Key Findings:

1. Demographics

2. Housing Stock

3. Affordability

Housing Needs & Demand in Ashland

Housing Needs & Demand – Demographics

Town Population and the Number of Households Are Increasing

Population and Households, Ashland, 2000-2030

Source: U.S. Census Bureau & MAPC Projections

5,7206,385

7,4048,437

14,674

16,59318,134

19,902

0

5,000

10,000

15,000

20,000

25,000

2000 2010 2020 2030

Households

Population

Housing Needs & Demand – Demographics

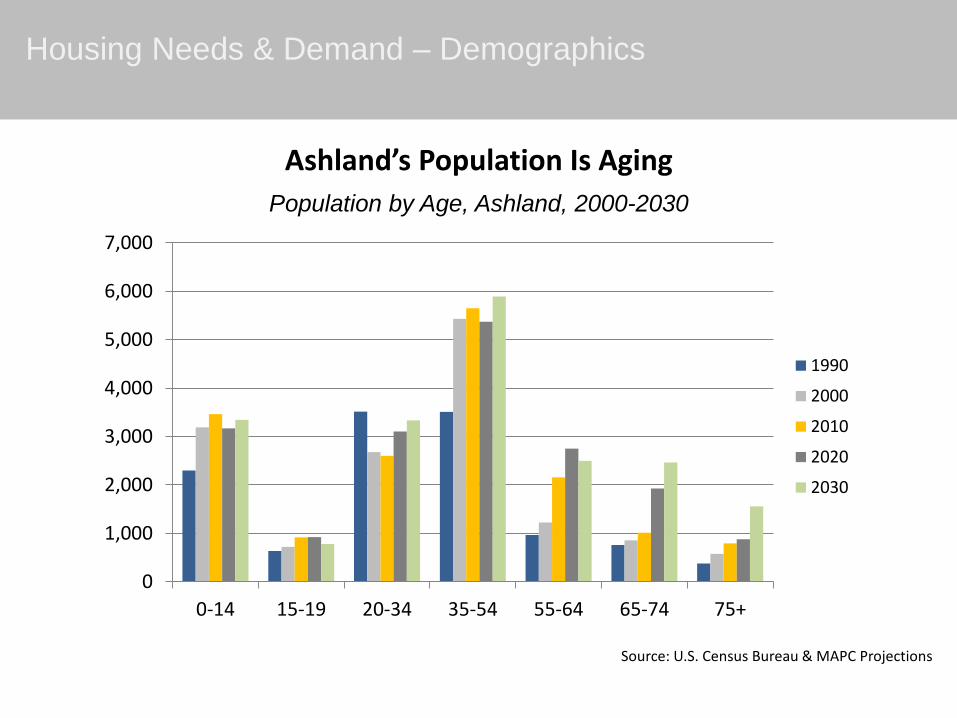

Ashland’s Population Is Aging

Population by Age, Ashland, 2000-2030

Source: U.S. Census Bureau & MAPC Projections

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

0-14 15-19 20-34 35-54 55-64 65-74 75+

1990

2000

2010

2020

2030

Housing Needs & Demand – Demographics

School Enrollment Has Decreased

School Enrollment, Ashland, 2003-2014

Source: MA Department of Primary and Secondary Education

2,590

2,629

2,654 2,653

2,671

2,630 2,640

2,624

2,584 2,573

2,581

2,520

2,540

2,560

2,580

2,600

2,620

2,640

2,660

2,680

Housing Needs & Demand – Demographics

Source: U.S. Census Bureau, 2009-2013 American Community Survey

The Young and Seniors Tend to Rent, Middle-Aged Tend to Own

Housing Tenure by Age of Householder, Ashland

397

990

1,657

777608 533

300

15786

243

157

326

57123 144

100

390

500

1,000

1,500

2,000

2,500

15-24 25-34 35-44 45-54 55-59 60-64 65-74 75-84 85+

Owner-Occupied Renter-Occupied

Almost Half of Households Earn $100,000 or More Annually

Source: U.S. Census Bureau, 2009-2013 American Community Survey

Housing Needs & Demand – Demographics

Household Income Distribution, Ashland

8.4%

11.3%

10.7%

9.9%

12.1%

47.6%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0%

Less than $20,000

$20-39,9999

$40-59,999

$60-74.999

$75-99,999

$100,000+

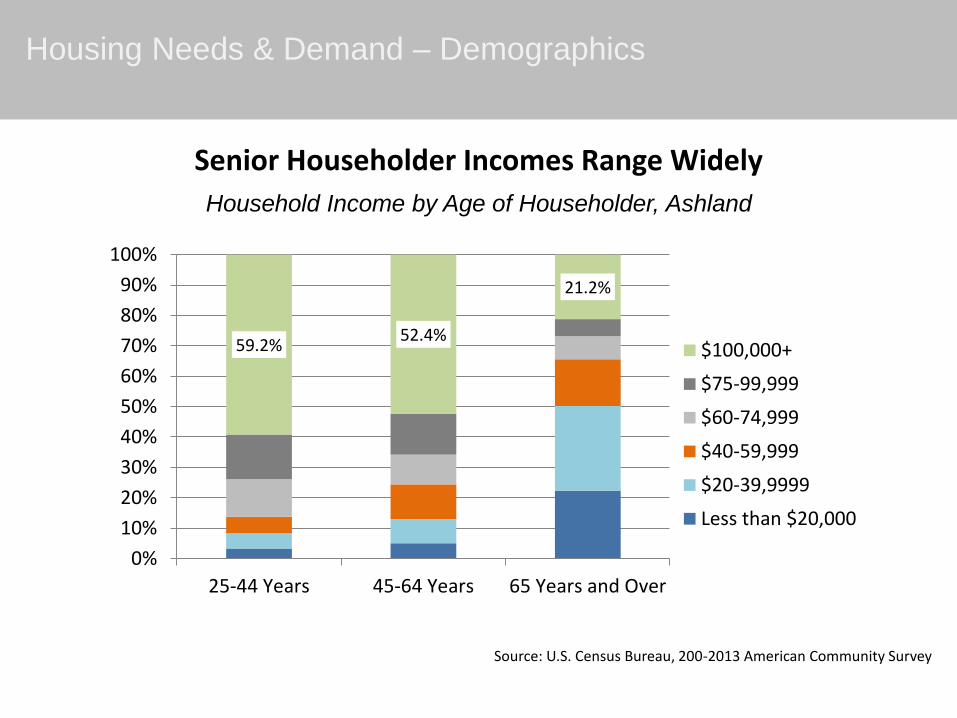

Senior Householder Incomes Range Widely

Source: U.S. Census Bureau, 200-2013 American Community Survey

Housing Needs & Demand – Demographics

Household Income by Age of Householder, Ashland

59.2%52.4%

21.2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

25-44 Years 45-64 Years 65 Years and Over

$100,000+

$75-99,999

$60-74,999

$40-59,999

$20-39,9999

Less than $20,000

Housing Needs & Demand – Housing Stock

Source: U.S. Census Bureau, 2009-2013 American Community Survey

Three-Quarters of the Housing Stock is Single-Family

Housing Units by Type, Ashland

76.0%

4.9%

11.0%

2.9%4.6%

Single-Family

Two-Family

3-4 Units

5-9 Units

10-19 Units

20+ Units

Housing Needs & Demand – Housing Stock

Source: Census Building Permit

According to Permits Issued, Ashland has Increased Its Housing Stock by 15% Since 2000

Housing Units Permitted, MetroWest Sub-Region, 2000-2013

388 405479 486

582

850

1,022

1,2981,393

0

200

400

600

800

1,000

1,200

1,400

1,600

Housing Needs & Demand – Housing Stock

Source: MAPC Projections

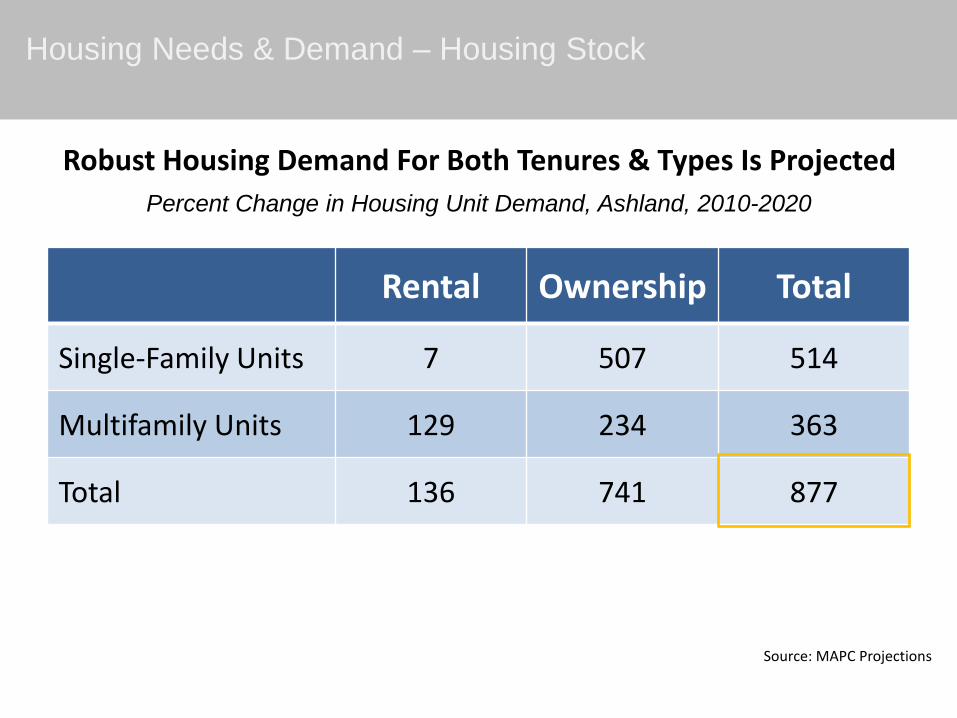

Rental Ownership Total

Single-Family Units 7 507 514

Multifamily Units 129 234 363

Total 136 741 877

Robust Housing Demand For Both Tenures & Types Is Projected

Percent Change in Housing Unit Demand, Ashland, 2010-2020

Housing Needs & Demand – Affordability

Source: The Warren Group, 2014, adjusted to 2014 $

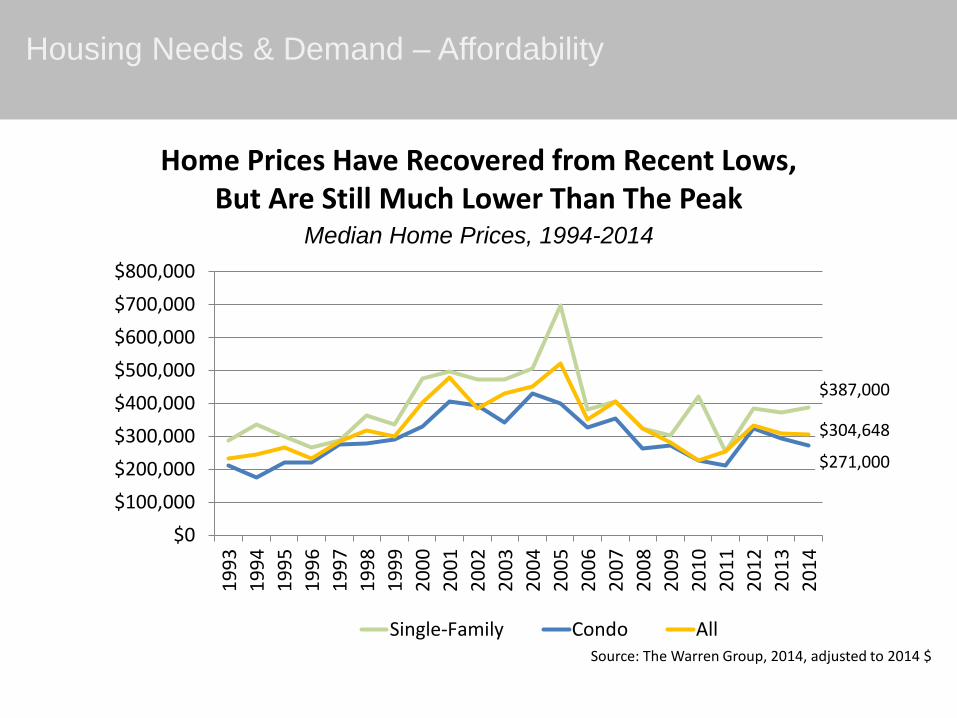

Home Prices Have Recovered from Recent Lows, But Are Still Much Lower Than The Peak

Median Home Prices, 1994-2014

$387,000

$271,000

$304,648

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Single-Family Condo All

Housing Needs & Demand – Affordability

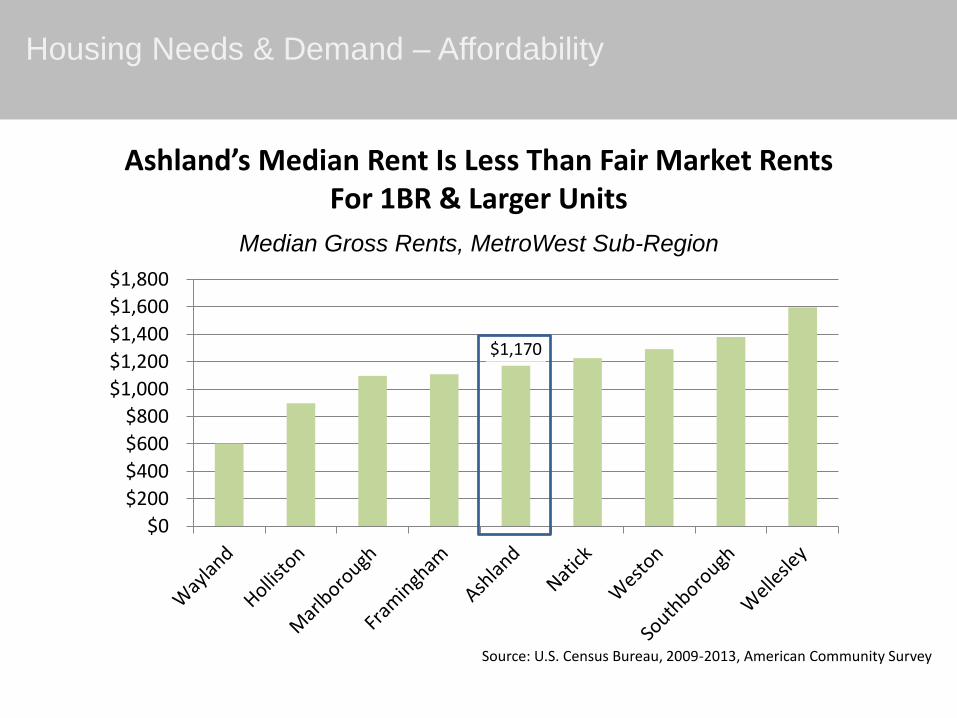

Source: U.S. Census Bureau, 2009-2013, American Community Survey

Ashland’s Median Rent Is Less Than Fair Market Rents For 1BR & Larger Units

Median Gross Rents, MetroWest Sub-Region

$1,170

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

Housing Needs & Demand – Affordability

Source: Comprehensive Housing Affordability Strategy (CHAS), 2007-2011

More Than a Quarter of Households are Low Income & Qualify For Housing Assistance

Percent of Low-Income Households by Type/Size, Ashland

35%

69%

11%

17%

36%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Elderly FamilyElderly Non-FamilySmall Related Large Related Other

Housing Needs & Demand – Affordability

Cost-Burdened

% of All Households 33%

% of Low-Income Households 65%

% of Owners 26%

% of Renters 7%

Source: U.S. Census Bureau, 2009-2013 American Community Survey

More Than A Third of Households are Cost Burdened, Paying More Than 30% of Income on Housing

Cost-Burdened Households by Tenure, Ashland

Housing Needs & Demand

Questions?

Discussion:

Local Housing Goals, Barriers, & Opportunities

Based on what you have heard this evening, what do you think Ashland’s housing goals should be?

Local Housing Goals, Barriers, & Opportunities

What are the local barriers to achieving these housing goals?

Local Housing Goals, Barriers, & Opportunities

Are there specific housing opportunities that exist for redevelopment, preservation, or new housing?

What about partnerships, resources, and support?

Local Housing Goals, Barriers, & Opportunities

1. Develop housing production goals

2. Establish plan implementation strategies

3. Public forum to share goals and

strategies

4. Discussion with Town staff

5. Adoption of HPP by Planning Board and

Board of Selectmen

6. Submission of HPP to DHCD and

subsequent approval

Next Steps

Thank You!

Please join us for our next meeting to discuss

implementation strategies! Date to be determined.

For more information, please contact:

Jenny Raitt,

Assistant Director of Land use & Chief Housing Planner617-933-0754 | [email protected]

Karina Milchman,Housing Planner

617-933-0738 | [email protected]

www.mapc.org

@MAPCMetroBoston