pipv: at inflection point - motilal oswal · at inflection point momentum in defense orders would...

TRANSCRIPT

Satyam Agarwal ([email protected]) +91 22 3982 5410

Pooja Kachhawa ([email protected]) +91 22 3982 5585

Pipavav Defence & Offshore

At inflection point

2 March 2012

Initiating Coverage | Sector: Defense

Pipavav Defence

22 March 2012

PIPV: At inflection point

Page No.

Summary ..............................................................................................................3

India's growing defense expenditure presents a huge opportunity ............... 4-7

PIPV is suitably positioned ............................................................................ 8-15

Expect steady growth in earnings ............................................................... 16-17

Appendix I: Largest Maritime Infrastructure in India ....................................18

Appendix II: Defense procurement procedure, 2011 .......................................19

Appendix III: Aspects of India's Defence Procurement Categories ...............20

Appendix IV: Offsets mechanism ............................................................... 21-22

Financials and valuation .............................................................................. 23-24

At inflection pointMomentum in defense orders would result in re-rating; Buy

PIPV enjoys early mover advantage and best-in-class infrastructure in the defense

shipbuilding segment. It has strong strategic partnerships with international players

and a robust order book of INR67b (4.5x TTM revenue).

Key events to monitor: JV with Mazgaon Dock, ongoing negotiations with friendly

countries for naval exports, 'offset' opportunity, attempt to emerge as an integrated

defense player (including army and airforce). Increased visibility on these opportunities

will lead to re-rating possibilities, while there could be volatility in the interim period.

The stock is available at a market capitalization of INR50b, below its replacement cost

of INR67b. We initiate coverage with a Buy rating.

India's growing defense expenditure presents a huge opportunity: Given the

~USD200b expected allocation to defense capital expenditure for the period

2012-2017, India is set to ramp up its naval capabilities meaningfully. With its

'Buy Indian, Make Indian' initiative, the Ministry of Defense (MOD) is increasing

stress on indigenization. The Ministry also envisages a greater role for the private

sector, which should benefit established players like PIPV.

PIPV is suitably positioned - has first mover advantage, strong international tie-

ups: PIPV enjoys first mover advantage and best-in-class infrastructure in the

shipbuilding segment. It operates the second largest shipbuilding capacity in

the world. PIPV uses modular construction technology, with two 600MT Goliath

cranes, which enables it to reduce the construction and delivery time of vessels.

Further, it enjoys strong strategic partnerships with several international players,

which should aid robust warship order booking in the near future. MOD's growing

stress on indigenization and its Mazgaon JV should boost order intake.

Capacity utilization increasing; expect revenue CAGR of 40% over FY12-14: PIPV's

current capacity, which is currently USD1.7b (in terms of revenue potential), is

likely to shoot up to USD2.5b once the second dry dock becomes operational by

2014. In FY11, capacity utilization stood at USD170m (10% of total capacity). We

now expect capacity utilization of USD360m (22% of total capacity) in FY12. We

expect revenue to grow at a CAGR of 40% over FY12-14. Our earnings estimates

largely factor in execution of the existing order book of USD1.3b. We have not

factored in possibilities of increased defense orders.

Initiating coverage with a Buy rating: We believe that PIPV is well placed to

exploit the massive opportunity that India's defense sector offers in the next

few years. It has global-sized assets and best-in-class tie-ups. Also, PIPV offers

the only credible large-size exposure for investors to India's defense business.

We estimate net profit at INR532m for FY12 and INR809m for FY13, translating

into an EPS of INR0.8 for FY12 and INR1.2 for FY13. We value PIPV based on

replacement cost method at INR67b (INR100/sh). Initiate coverage with a Buy.

Stock performance (1 year)

Shareholding pattern % (Dec-11)

Bloomberg PIPV IN

Equity Shares (m) 665.8

52-Week Range (INR) 93/50

1,6,12 Rel. Perf. (%) 4/5/-5

M.Cap. (INR b) 50.7

M.Cap. (USD b) 1.0

Y/E March 2011 2012E 2013E

Sales (INR b) 8.6 18.2 24.6

EBITDA (INR b) 1.5 4.2 6.1

NP (INR b) 0.4 0.5 0.8

EPS (INR) 0.6 0.8 1.2

EPS Gr. (%) -181.3 33.9 52.2

P/E (x) 127.9 95.5 62.7

P/BV (x) 2.9 2.6 2.3

EV/EBITDA (x) 43.7 18.2 12.8

EV/ Sales (x) 7.8 4.2 3.2

RoE (%) 2.3 2.9 3.9

RoCE (%) 4.9 7.7 9.1

Domestic

Inst, 19.1

Others,

22.4

Foreign,

15.1

Promoter,

43.3

3

Pipavav Defence & Offshore

CMP: INR76 TP: INR100 BuyBSE Sensex S&P CNX

17,584 5,340

2 March 2012

Initiating Coverage | Sector: Defense

506274

8698

Feb

-11

May

-11

Au

g-11

Nov

-11

Feb

-12

Pipavav DefenceSensex - Rebased

Pipavav Defence

42 March 2012

India's growing defense expenditure presents a hugeopportunityMinistry of Defense stressing on indigenization, welcoming private sector

Apart from the ~USD200b allocated to defense capital expenditure for the period 2012-

2017, India is set to spend ~INR600b over the next five years on improving its military

infrastructure and another INR600b on the Mountain Strike Corps.

With its 'Buy Indian, Make Indian' initiative, the Ministry of Defense is increasing stress on

indigenization. It intends to increase procurement from Indian companies from the current

30% to 70% in the next five years.

The Ministry also envisages a greater role for the private sector, which should benefit

established players like PIPV.

The approval of the guidelines for the formation of JVs between state-owned defense

entities and private sector organizations by the Union Cabinet will help accelerate the

process.

Geopolitical challenges underscore need for stronger defense capabilitiesGrowing geopolitical challenges have made the Government of India realize the vital

need to strengthen its defense capabilities. India is located at a prime position in the

Indian Ocean, with over 7,517km of coastline. In addition to the challenge of protecting

its sea-facing boundaries, India also shares long, contested borders with two nuclear-

armed neighbors - Pakistan to the West, and China to the East.

Recently, China entered into an agreement with Seychelles, which will allow the

Chinese navy to re-supply and recuperate its vessels there. Due to its strategic location

just off the coast of Africa/Madagascar, this base will give China direct access to the

West Coast of India. In addition, China has a naval base in Myanmar and is building a

commercial port in Sri Lanka. Recognizing these threats, the Government of India is

continuously making efforts to ensure its naval security in the Indian Ocean, which in

turn will lead to demand for better quality defense vessels.

Indian sea trade accounts for ~90% by volume and ~77% by value of India's aggregate

trade. The Indian economy is dependent on the sea for oil & gas exploration and

production, commercial trade, etc. Thus, the stability of the Indian sea trade is

becoming increasingly important. Protecting India's maritime assets is more crucial

than ever before.

India's growing defense expenditure presents a huge opportunityIndia is set to spend ~INR600b over the next five years on improving its military

infrastructure. It is spending another INR600b on the new Mountain Strike Corps in

the North East. Both these outlays are in addition to the estimate of ~USD200b

allocated to defense capital expenditure for the period 2012-2017. Due to the 'Buy

Indian, Make Indian' policy put in place by the MOD, a large part of this sum will go to

domestic companies. Even in case of imports, there is an offset clause that benefits

domestic companies. For any defense contract for capital purchases of over USD60m

(INR3b), the foreign vendor is required to allocate 30% of the contract value to Indian

players, primarily in the defense, internal security and civil aerospace sectors.

According to the Ministry of Defense (MOD), there could be an offset opportunity of

USD15b over the next five years.

China-growing nautical danger

According to the Ministry

of Defense (MOD), there

could be an offset

opportunity of USD15b

over the next five years.

Pipavav Defence

52 March 2012

Sizable opportunity prevails in defense spaceTo meet the massive geopolitical challenges, the Indian Armed Forces are likely to

order military hardware worth USD200b over the next five years.

Navy: The present fleet of the Indian Navy has ~120 ships on active duty, with an

additional 36 ships in the process of being built. The Indian Navy needs over 100

ships of diverse variety, including submarines, aircraft carriers, landing platform

docks, destroyers, frigates, corvettes, patrol vessels, etc. There also exist

significant opportunities abroad, as foreign friendly nations drift down to low

cost defense equipment providers.

Army: The Indian Army has the largest share of India's defense outlay. It is

currently looking to procure Heavy Artillery Systems (towed and self propelled)

worth over USD5b. Private sector participation in the ambitious Future Infantry

Combat Vehicle (FICV) is a first and will be an opportunity worth USD8b-10b over

the next 5-8 years. Besides this, the Indian Army is in the process of upgrading a

number of its legacy combat systems such as BMP2 (infantry vehicles) and T-72

tanks amounting to ~USD5b. The Indian Army will also be looking at private

industry for the maintenance, repair and overhauling (MRO) of its major systems.

Air Force: The Indian Air Force gets the second largest defense outlay after the

Indian Army. It is in the process of finalizing the largest fighter jet procurement

in the world, the Medium Multi Role Combat Aircraft (MMRCA), expected to be

worth USD20b. Besides this, it is also in the market for Strategic Heavy and Tactical

Cargo Aircraft, Airborne Early Warning Systems, Aerial Refuelers, Heavy, and

Medium, Light and Attack Helicopters. There is also huge tri-services requirement

for Air Defense Radar and Missiles, which will be procured from global industry

majors, but will be manufactured under transfer-of-technology in India.

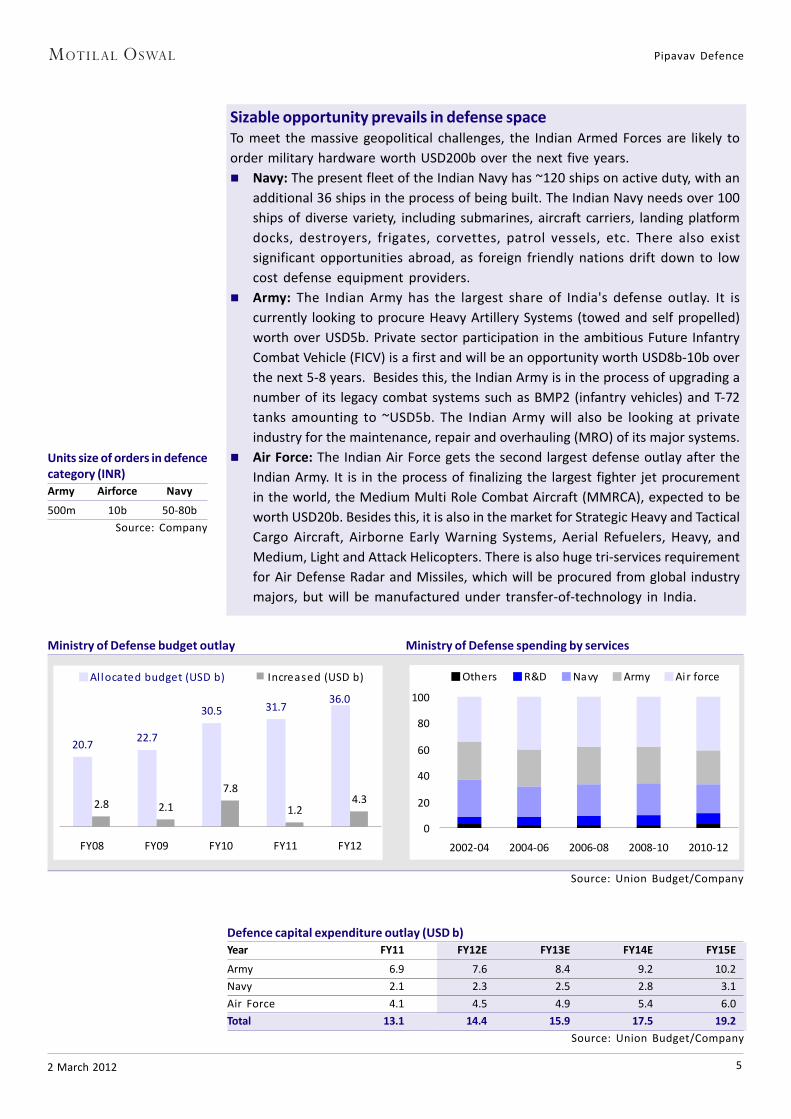

Ministry of Defense budget outlay Ministry of Defense spending by services

Source: Union Budget/Company

Defence capital expenditure outlay (USD b)

Year FY11 FY12E FY13E FY14E FY15E

Army 6.9 7.6 8.4 9.2 10.2

Navy 2.1 2.3 2.5 2.8 3.1

Air Force 4.1 4.5 4.9 5.4 6.0

Total 13.1 14.4 15.9 17.5 19.2

Source: Union Budget/Company

Units size of orders in defencecategory (INR)

Army Airforce Navy

500m 10b 50-80b

Source: Company

20.722.7

30.5 31.7

2.8 2.1

7.8

1.24.3

36.0

FY08 FY09 FY10 FY11 FY12

Al located budget (USD b) Increased (USD b)

0

20

40

60

80

100

2002-04 2004-06 2006-08 2008-10 2010-12

Others R&D Navy Army Air force

Pipavav Defence

62 March 2012

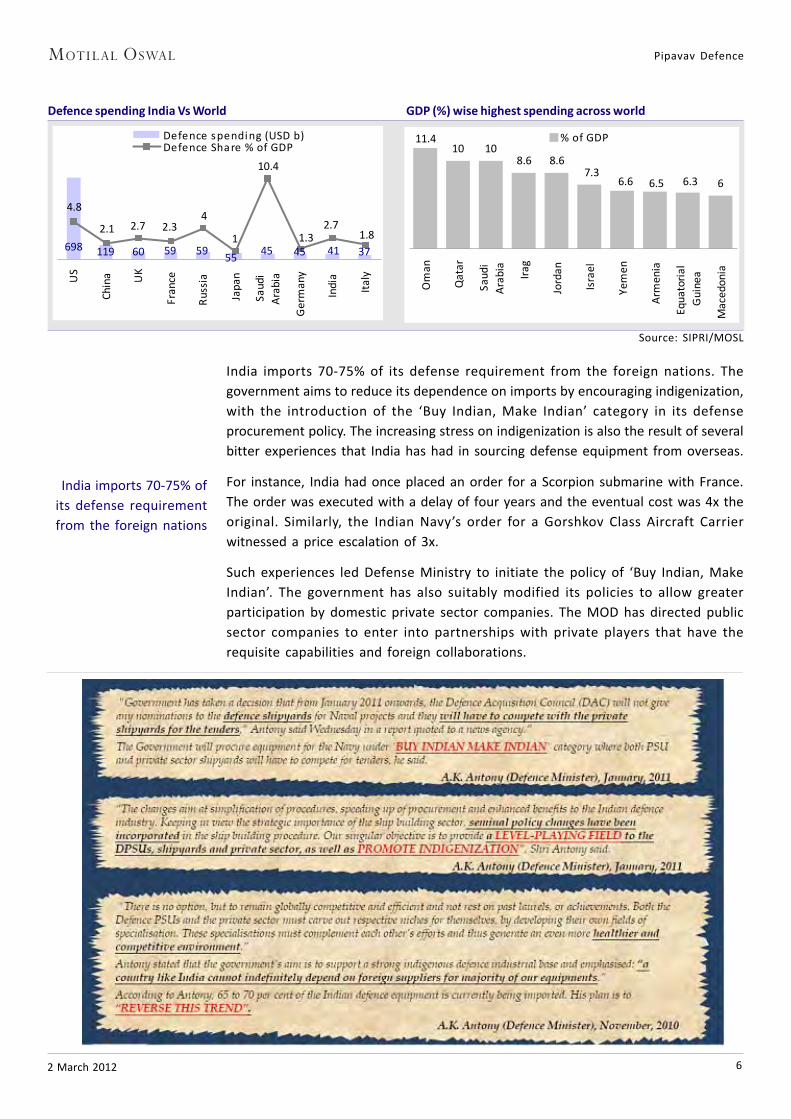

India imports 70-75% of its defense requirement from the foreign nations. The

government aims to reduce its dependence on imports by encouraging indigenization,

with the introduction of the ‘Buy Indian, Make Indian’ category in its defense

procurement policy. The increasing stress on indigenization is also the result of several

bitter experiences that India has had in sourcing defense equipment from overseas.

For instance, India had once placed an order for a Scorpion submarine with France.

The order was executed with a delay of four years and the eventual cost was 4x the

original. Similarly, the Indian Navy’s order for a Gorshkov Class Aircraft Carrier

witnessed a price escalation of 3x.

Such experiences led Defense Ministry to initiate the policy of ‘Buy Indian, Make

Indian’. The government has also suitably modified its policies to allow greater

participation by domestic private sector companies. The MOD has directed public

sector companies to enter into partnerships with private players that have the

requisite capabilities and foreign collaborations.

Defence spending India Vs World GDP (%) wise highest spending across world

11.410 10

8.6 8.6

67.3

6.6 6.5 6.3

Om

an

Qat

ar

Sau

di

Ara

bia

Irag

Jord

an

Isra

el

Yem

en

Arm

enia

Equ

ator

ial

Gui

nea

Mac

edo

nia

% of GDP

Source: SIPRI/MOSL

698 3741454555

595960119

1.82.7

1.3

10.4

1

42.32.72.1

4.8

US

Chi

na UK

Fra

nce

Rus

sia

Jap

an

Saud

i

Ara

bia

Ge

rman

y

Indi

a

Ital

y

Defence spending (USD b)Defence Share % of GDP

India imports 70-75% of

its defense requirement

from the foreign nations

Pipavav Defence

72 March 2012

Increasing role of private sector playersIn addition to its 'Buy Indian, Make Indian' initiative, the government has also suitably

modified its policies to allow greater participation by domestic private sector

companies. For instance, the MOD has decided to liquidate the piling orders of

government shipyards to private players like PIPV and L&T. The cumulative order

book of government shipyards, which have a combined execution capacity of USD1b,

is USD28b. Restricting defense orders to government shipyards would have severely

constrained the growth of India's naval fleet. Mazgaon Dock, which has the largest

order book (of USD22b) among the government shipyards, has a JV with PIPV. We

expect significant order flows to this JV.

Media article

The cumulative order

book of government

shipyards, which have a

combined execution

capacity of USD1b, is

USD28b

Pipavav Defence

82 March 2012

PIPV is suitably positionedFirst mover advantage, strong international tie-ups

PIPV enjoys first mover advantage and best-in-class infrastructure in the shipbuilding segment,

including:

- The world's second largest drydock with a capacity of 662x65(mtr)

- Modular technology, with two Goliath cranes and combined capacity of 1,200mt

- Strong international tie-ups

It has a robust order book of INR67b (4.5x TTM revenue).

MOD's growing stress on indigenization, Mazgaon JV, and growing demand from non-defense

segments should boost order intake in the near term.

Enjoys first mover advantagePIPV is well placed to capitalize on its first mover advantage in the shipbuilding

segment. It has a capacity to build ships upto 400,000DWT, which is the second highest

in the world. Any new private player would need 8-10 years to set up a comparable

facility. Land acquisition, required environment clearances, construction, license

procurement and technology tie-ups can take an average of 10 years. This gives an

established player like PIPV an added advantage.

Second largest shipbuilding capacity in the world after HyundaiPIPV operates the second largest shipbuilding capacity in the world, capable of

constructing vessels up to 400,000DWT. Hyundai Heavy, the largest shipbuilder has a

total capacity of 1,000,000DWT. PIPV intends to become the world's largest shipbuilding

company after completing the conversion of its second wet dock facility to a dry dock.

It has a shipbuilding, ship repair and offshore fabrication complex spread over 750

acres with ~720 meters of sea front and 685 meters of outfit quay, including two

Goliath cranes of 600 tons each, which service the dry dock and the adjoining pre-

erection berth, enabling PIPV to handle up to 1,200 tons of pre-outfitted ship blocks.

A host of other technologically advanced infrastructure makes PIPV one of the most

modern shipyards in the world.

State-of-the art

Infrastructure

Strategic key

tie-ups

Efforts to secure license &

robust order pipeline

5 years 2 years 3 years

A 10 Year cycle

+ +

Ahead of the

curve

High entry

barriers

A new player will take ~10 years to establish itself

Source: Company/MOSL

Pipavav Defence

92 March 2012

Uses modular technology - cost effective; able to deliver 4-5x fasterPIPV uses modular construction technology, which enables it to reduce the

construction and delivery time of vessels, as it is able to simultaneously work on

different orders. It has a separate shipbuilding facility, which breaks down a complete

ship into separate blocks for construction, which include cutting, forming, blasting,

painting, steel stacking, treatment and welding. The dock is used to only assemble

mega blocks with the help of two installed Goliath cranes.

A Comparison of Indian Docks (mtr)

Source: Company/MOSL

Capacity comparison: Pipavav v/s private shipyards & public sector shipyards (mtr)

Hyundai Pipavav Pipavav Private Sector Shipyards Public Sector Shipyards

Heavy 1 2* ABG Bharati Cochin Mazgaon Hindustan Garden reach Goa

Dry Dock

Length (mtr) 700 662 740 155 176 270 150 240 155 176

Width (mtr) 92 65 90 30 33 45 18.9 53 30 33

Commercial vessels (max vessel size)

Dry Bulk Carrier 1,000,000 400,000 1,000,000 120,000 100,000 110,000 [] [] 120,000 100,000

Crude Tanker 1,000,000 400,000 1,000,000 120,000 100,000 110,000 [] [] 120,000 100,000

Product Tanker 1,000,000 400,000 1,000,000 120,000 100,000 110,000 [] [] 120,000 100,000

* Pipavav2: Second drydock conversion expected to be completed in 2014 Source: Company/MOSL

155x30 155x19 162x25

240x53 270x45

662x65

740x90ProposedAddition

ABGShipyard

MazgoanDock

GardenReach

HindustanShipyard

CochinShipyard

PipavavShipyard

PipavavShipyard

680x60

DR

Y D

OC

K

WET

DO

CK

Pipavav Defence

102 March 2012

Source: Company

Expect robust order booking in both defense and non-defense segmentsPIPV has a robust order book of INR67b (4.5x TTM revenue). The order book includes

INR30b from defense, INR4.9b from offshore, and INR36b from commercial

shipbuilding. We expect its order book to grow significantly, driven by orders from

both the defense and non-defense segments.

The only 'MODULAR' shipbuilding facility in India - a huge paradigm shift

Substantial reduction in production time

Enables simultaneous production of

multiple ships

Order book break up as at 31 Dec 12

(INR m) (USD m)

Defence 29,000 100.8

% of total orders 42 42

Offshore 5,040 580.0

% of total orders 7 7

Shipbuilding 33,390 667.8

% of total orders 51 51

Total order book 67,430 1,348.6

Source: Company

Pipavav order book details

Segment and Clients Vessel Type No of vessels

Defence (Navy) NOVP (Naval Offshore Patrol Vessels) 5

Offshore & Engineering (ONGC) OSV (offshore support vessels) 12

Commercial Export order

* Panamax bulk-carrier (74,500 DWT) 4

* Panamax 17

Total Order-book 38

Source: RHP/Company

Growing indigenization, Mazgaon JV to boost order booking from defenseWe expect PIPV's defense order book to be boosted by:

MOD's increasing stress on indigenization - 'Buy Indian, Make Indian' policy: The

Ministry intends to increase procurement from Indian companies from the current

30% to 70% in the next five years. We believe this will turn out to be a major boon

for private sector players like PIPV.

MOD's decision to liquidate the piling orders with government shipyards to private

sector players like PIPV and L&T: The cumulative order book of government

shipyards, which have a combined execution capacity of USD1b, is USD28b.

Mazgaon Dock has the largest order book of USD22b and PIPV's JV with Mazgaon

Dock should give it an edge.

Pipavav Defence

112 March 2012

Defence PSUs can have JVs with CosCabinet nod may increase chancess for obtaining foreign technology

Date: 10 Feb 2012

The government on Thursday made a significant step for bolstering domestic defence industrial base by clearing

of guidelines for its defencePSUs to establish joint ventures with private firms. This could increase opportunities

for obtaining advanced technologies from foreign sources. However, though the defence sector was opened up

in 2001-02 to 100% private investment, with up to 26% FDI, it did not have the desired impact on the performance

of the eight defence PSUs.

"The Union Cabinet today approved the guidelines for establishing Joint Venture Companies by Defence Public

Sector Undertakings(DPSUs). The guidelines contain provisions for important matters that are critical from a

national security perspective," an official release said. "The ministry will issue the guidelines to harness the

emerging dynamism of the private sector in India and increasing opportunities to obtain advanced technologies

from foreign sources through adoption of appropriate partnership approaches by DPSUs," it said. There was

urgency in laying down guidelines as the government is in the process of negotiating over 40 offset contracts

worth Rs 50,000 crore with global armament firms. Besides, the $20 billion MMRCA project will have 50% offsets.

JVs were allowed in the Defence Production Policy released last year but was put on hold by the ministry after

the Mazagon Dockyards (MDL) tied up with a private shipyard, which was opposed by rival companies. Officials

said the guidelines would help in "enhancing fairness and transparency in the selection of the JV partner" by

DPSUs while ensuring a "well-defined nature and scope" of the tie up. According to the guidelines, DPSUs will

retain the "affirmative rights" for taking key decisions in the JV company.

"Retention of the affirmative right of DPSU for prior approval to key joint venture decisions, such as amendments

to the articles of association of the JV company, declaration of dividend, sale of substantial assets, and formation

of further subsidiaries," the release said.

The guidelines provide a "streamlined, fair and transparent framework for entering into JVs by DPSUs, with the

ultimate objective of better risk-management and shorter time frames for delivery to meet the increasing

demands of our armed forces." They said the new framework would also help in enhancing self-reliance in the

defence sector as a whole.

According to the guidelines approved by the Cabinet, DPSUs will have the "exit" provision in the joint venture

companies.Source: Economic times

Pipavav Defence

122 March 2012

Significant opportunity in non-defense segments as wellThere is significant opportunity in non-defense segments, as well, which PIPV is well

placed to exploit.

Growing demand for ship repair: In India, ~50% of the commercial fleet is more

than 15 years old and Indian ship owners are expected to spend ~USD4b to replace

old ships during FY10-15. While PIPV stands to gain from increasing domestic

demand for commercial shipbuilding and repair, we expect it to garner significant

overseas orders as well. International MRO facilities are running at overcapacity

and are looking to offload work to low cost destinations like India. PIPV's

infrastructure is comparable with Chinese and Korean players.

Huge demand for offshore supply vessels: The demand for high-end offshore

facilities such as drill ships and floating production storage platforms amounts to

USD20b-40b. With rising oil prices, this segment is gaining importance. Higher

demand for offshore assets would lead to a consequential increase in demand for

offshore supply vessels (OSVs) required to service them.

Ship repair a large opportunity

Source: Aero Strategy report "Air Transport MRO Outlook". April, 2009

60-70% of the

maintenance and

repair work is

contributed by the

North America and

Europe.

India will now

become the next

destination for the

huge replacement

market.

Pipavav Defence

132 March 2012

Partnering company

KOMAC (Korea)

SembCorp (Singapore)

SAAB (Europe)

Northrop Grumman

Babcock

Rosoboron Export

DCNS - Ministry of Defense

Thyssenkrupp

Airbus

Oto Melara

Sagem

Scope of partnership

Design support, material support

Technical support , ship repair, ship building,

ship conversion, rig building, offshore

engineering and construction

Product services and solutions for military

defense and civil security

Providing products in the aerospace,

electronics, information systems and

shipbuilding segments, and technical services

to government and commercial customers

worldwide

Focusing on defense, telecommunications,

energy and transportation. This includes

building next generation aircraft carriers for

Indian Navy.

Export and import of defense-related products,

technologies and services

Helicopter carriers and submarines

Specializes in integrated materials and

technology; will also provide complete

systems solutions and innovative services

France to develop state-of-the-art MRO

facilities in India

Leading manufacturer of artillery and

ammunition systems

Leading manufacturer of defense electronics,

navigation systems and optronics

Partner Profile

Established naval architects and marine engineers

Global leader in marine & offshore engineering

bus iness

Sweden-based industrial and technology giant

Leading US defense major, with annual revenue of

USD35b

UK's leading engineering and naval warship

services

State intermediary agency for Russian Defense

Exports

France Ministry of Defense Company

German industrial conglomerate, with deep

presence in defense

EADS parent company of airbus, allows to utilize

technology to both civil and defence applications

Part of USD25b Finmeccanica Group (Italy)

Part of France's leading defense conglomerate,

Safran Group.

Global partnerships contribution to the business

Source: Company

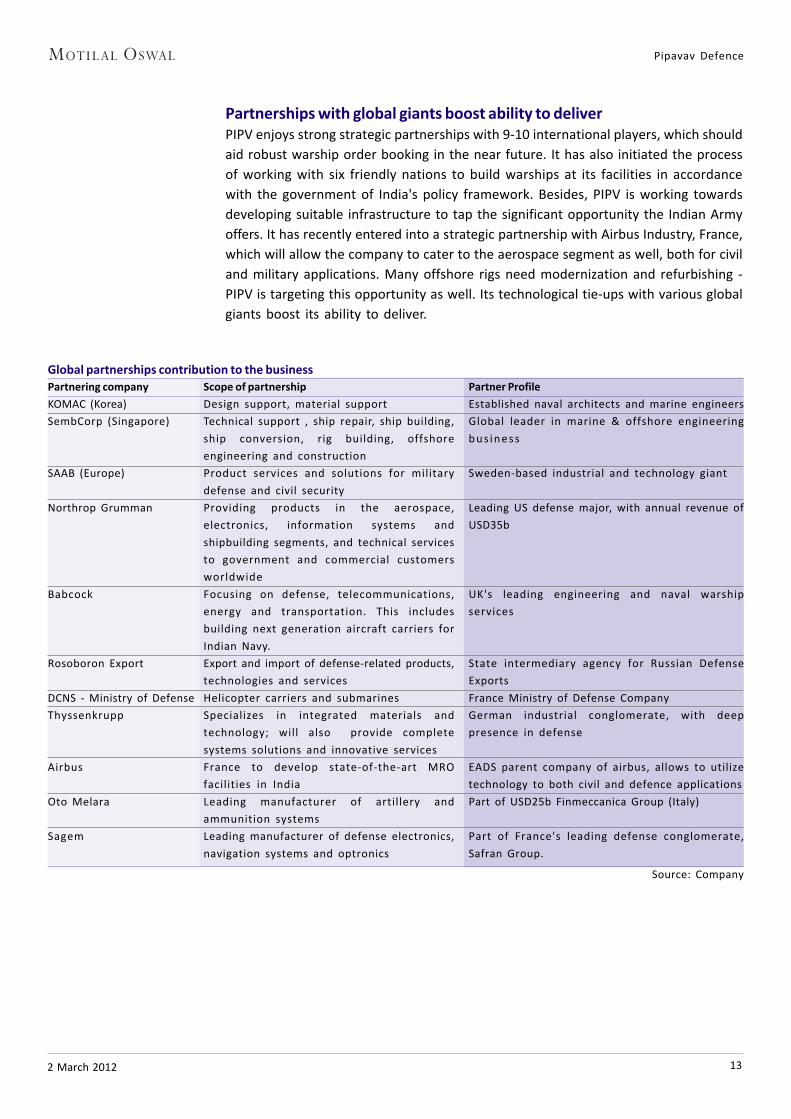

Partnerships with global giants boost ability to deliverPIPV enjoys strong strategic partnerships with 9-10 international players, which should

aid robust warship order booking in the near future. It has also initiated the process

of working with six friendly nations to build warships at its facilities in accordance

with the government of India's policy framework. Besides, PIPV is working towards

developing suitable infrastructure to tap the significant opportunity the Indian Army

offers. It has recently entered into a strategic partnership with Airbus Industry, France,

which will allow the company to cater to the aerospace segment as well, both for civil

and military applications. Many offshore rigs need modernization and refurbishing -

PIPV is targeting this opportunity as well. Its technological tie-ups with various global

giants boost its ability to deliver.

Pipavav Defence

142 March 2012

PIPAVAV global partnerships provide a technological edge

Source: Company

Pipavav Defence

152 March 2012

Strategically located to garner huge ship repair and commercial shipbuilding contracts

On the West Coast of India (Gujarat), Gulf of Cambay

Spread over 782 acres of land, 150 nautical miles from Mumbai

Adjacent to Pipavav's sea port, road, rail and logistics infrastructure

Only shipyard in an integrated format

Natural breakwater, short navigation channel and deep draught, which results in

significant savings in logistics cost

Block making engineering complex is in a notified SEZ, leading to fiscal advantage,

tax breaks, etc

Pipavav Defence

162 March 2012

Expect steady growth in earningsBuy with a target price of INR100

We believe that PIPV is well placed/ahead of the curve to exploit the massive opportunity

that India's defense sector offers in the next few years.

We estimate net profit at INR532b for FY12 and INR809b for FY13, translating into an EPS of

INR0.8 for FY12 and INR1.2 for FY13.

We initiate coverage with a Buy rating and a replacement cost-based target price of INR100.

Rightly placed to capture defense order opportunityThe private sector defense business is at a nascent stage in India. Given the various

government initiatives encouraging indigenization and private sector participation,

we believe defense orders offer immense opportunity to private sector players. PIPV

is well placed/ahead of the curve to exploit this opportunity in the next few years. It

has global-sized assets and best-in-class tie-ups. Also, PIPV offers the only credible

large-size exposure for investors to India's defense business.

Capacity utilization increasing; expect revenue CAGR of 40% over FY12-14PIPV's current capacity, which is currently USD1.7b, (in terms of revenue potential) is

likely to shoot up to USD2.5b once the second dry dock becomes operational by 2014.

In FY10, capacity utilization stood at USD13m (7% of total capacity), which grew to

USD170m (10% of total capacity) in FY11. We now expect capacity utilization of

USD360m (22% of total capacity) in FY12. We expect revenue to grow at a CAGR of 40%

over FY12-14. With pick-up in utilization levels, we expect significant boost to revenue

growth and margin expansion, going forward.

We have forecasted EBITDA margin at 23% for FY12 and 25% for FY13. We estimate net

profit at INR532m for FY12 and INR809m for FY13, translating into an EPS of INR0.8 for

FY12 and INR1.2 for FY13. Our earnings estimates largely factor in execution of the

existing order book of USD1.6b. We have not factored in possibilities of increased

defense orders (including from Mazgaon Shipyard JV, offset clauses, exports to friendly

countries, strategic tie-ups with several defense majors, positioning as an integrated

defense player, etc). Some of these orders could materialize in FY13, leading to serious

earnings upgrades (we currently factor in capacity utilization of just 28% in FY13).

Pipavav: Financials snapshot

Operational capacity FY11 FY12E FY13E

Operational capacity (b USD) 1.7 1.7 1.7

Reveune (b USD) 0.17 0.36 0.48

% Utilization 10.2 21.1 27.9

Revenue (INR)

OSV Type -1500 DWT 1,680 1,260 2,100

OPV Type - 2500 DWT - 6,960 10,440

Bulker Category- 75,000 DWT 5565 7,950 9,540

Defence category (I) - - -

Defence category (II) - - -

Subsidy income (26%) 1,354 2,067 2,480

Total Revenue 8,599 18,237 24,560

Source: Company/MOSL

Pipavav Defence

172 March 2012

Replacement cost the appropriate measure of fair value; BuyWe believe that PIPV is well placed/ahead of the curve to exploit the massive

opportunity that India's defense sector offers in the next few years. It has global-

sized assets and best-in-class tie-ups. Also, PIPV offers the only credible large-size

exposure for investors to India's defense business. We believe that the near term

stock performance is more a function of macro news flows and order intakes. Hence,

an earnings based valuation approach may not be the correct representative of the

fair value for PIPV, given the low capacity utilization in the interim period. We thus

value PIPV based on replacement cost method at INR67b (INR100/sh). We initiate

coverage with a Buy rating.

Replacement cost valuation

New Factor

PIPV Entrant (x) Remarks

Land 2,233 22,330 10.0 Contagious land availability with a large

waterfront is the key challenge; Land

Acquisition, Rehabilitation and Resettlement

Bill will lead to a meaningful increase in

land acquisition & R/R cost

Machinery 16,574 20,717 1.3 PIPV had ordered large parts of the

machinery in FY07-09; and since then

the costs have increased meaningfully

Infrastructure, 16,193 40,483 2.5 Increased wages and material costs

Others (particularly cement and steel) have led to

a manifold increased in setting up cost

Project Cost 35,000 83,530

Less: Project Debt 17,000

Equity Value 66,530

PIPV (INR/Sh) 100

Source: MOSL

Note: Our workings do not factor in:

(1) Cost of delays in obtaining requisite clearances and certification from various

defense departments.

(2) Technology tie-ups with global players.

Pipavav Defence

182 March 2012

Appendix I: Largest Maritime Infrastructure in India

The offshore supply vessels ready for their journey – at Pipavav The largest ship ever built in India

Fit out berth (684 meters of berthing space) Converting adjacent wet dock into the largest dry dock

Largest panel line in the World Two goliath crane with combined lifting capacity of 1,200 tons

Source: Company/MOSL

Pipavav Defence

192 March 2012

Appendix II: Defense procurement procedure, 2011

BackgroundThe Defense Procurement Procedure - 2002 (DPP- 2002) came into effect from 30

December 2002 and was applicable for procurements flowing out of 'Buy' decision of

Defense Acquisition Council (DAC). The scope of the same was enlarged in June 2003

to include procurements flowing out of 'Buy and Make' through Imported Transfer of

Technology (TOT) decision. The Defense Procurement Procedure has since been revised

in 2005, 2006, 2008 and 2009 enhancing the scope to include 'Make' Procedure, and

'Buy and Make (Indian)'categories.

As part of the review exercise and on basis of experience gained in the procurement

process, Defense Procurement Procedure has now been revised to DPP-2011.

AimThe objective of this procedure is to ensure expeditious procurement of the approved

requirements of the Armed Forces in terms of capabilities sought and time frame

prescribed by optimally utilizing the allocated budgetary resources.

ScopeThe DPP-2011 will cover all Capital Acquisitions, (except medical equipment)

undertaken by the MOD and Indian Coast Guard both from indigenous sources and

ex-import. Defense Research and Development Organization (DRDO), Ordnance

Factory Board (OFB) and Defense Public Sector Undertakings (DPSUs) will, however,

continue to follow their own procedures for procurement.

Capital AcquisitionsCapital Acquisitions are categorized as under: -

Acquisitions Covered under the 'Buy' Decision: Buy would mean an outright

purchase of equipment. Based on the source of procurement, this category would

be classified as 'Buy (Indian)' and 'Buy (Global)'. 'Indian' would mean Indian vendors

only and 'Global' would mean foreign as well as Indian vendors. 'Buy Indian' must

have minimum 30 % indigenous content if the systems are being integrated by an

Indian vendor.

Acquisitions Covered under the 'Buy & Make' Decision: Acquisitions covered under

the 'Buy & Make' decision would mean purchase from a foreign vendor followed

by licensed production / indigenous manufacture in the country.

Acquisitions Covered under the 'Buy & Make (Indian)' Decision: Acquisitions

covered under the 'Buy & Make (Indian)' decision would mean purchase from an

Indian vendor including an Indian company forming joint venture / establishing

production arrangement with OEM followed by licensed production / indigenous

manufacture in the country. 'Buy & Make (Indian)' must have minimum 50 %

indigenous content on cost basis.

Acquisitions Covered under the 'Make' Decision: Acquisitions covered under the

'Make' decision would include high technology complex systems to be designed,

developed and produced indigenously.

Pipavav Defence

202 March 2012

Appendix III: Aspects of India's Defence ProcurementCategories

Pipavav Defence

212 March 2012

Appendix IV: Offsets mechanism

ScopeThe offset clause would be applicable for all procurement proposals where indicative

cost is INR3b or more and the schemes are categorized as:- 'Buy (Global)' involving outright purchase from foreign / Indian vendors and 'Buy and Make with

Transfer of Technology' i.e. Purchase from foreign vendor followed by Licensed Production.

A uniform offset of 30% of the estimated cost of the acquisition in 'Buy (Global)'

category acquisitions and 30% of the foreign exchange component in 'Buy and Make'

category acquisitions will be the minimum required value of the offset. Offset

obligations may be discharged only with reference to "eligible" products and eligible

services.

The procedure for implementing the offsets provisions is:

Defence Products

Small arms, mortars, cannons, guns, howitzers, anti tank weapons and their

ammunition including fuze.

Bombs, torpedoes, rockets, missiles, other explosive devices and charges, related

equipment and accessories specially designed for military use, equipment

specially designed for handling, control, operation, jamming and detection.

Energetic materials, explosives, propellants and pyrotechnics.

Tracked and wheeled armored vehicles, vehicles with ballistic protection designed

for military applications, armored or protective equipment.

Vessels of war, special naval system, equipment and accessories.

Aircraft, unmanned airborne vehicles, aero engines and air craft equipment,

related equipment specially designed or modified for military use, parachutes

and related equipment.

Electronics and communication equipment specially designed for military use

such as electronic counter measure and counter measure equipment surveillance

and monitoring, data processing and signaling, guidance and navigation

equipment, imaging equipment and night vision devices, sensors.

Specialized equipment for military training or for simulating military scenarios,

specially designed simulators for use of armaments and trainers.

Forgings, castings and other unfinished products which are specially designed for

products for military applications and troop comfort equipment.

Miscellaneous equipment and materials designed for military applications,

specially designed environmental test facilities and equipment for the

certification, qualification, testing or production of the above products.

Software specially designed or modified for the development, production or use

of above items. This includes software specially designed for modeling, simulation

or evaluation of military weapon systems, modeling or simulating military

operation scenarios and Command, Communications, Control, Computer and

Intelligence (C4I) applications.

High velocity kinetic energy weapon systems and related equipment.

Direct energy weapon systems, related or countermeasure equipment, super

conductive equipment and specially designed for components and accessories.

Pipavav Defence

222 March 2012

Products for Internal Security

Arms and their ammunition including all types of close quarter weapons.

Protective Equipment for Security personnel including body armor and helmets.

Vehicles for internal security purposes including armored vehicles, bullet proof

vehicles and mine protected vehicles.

Riot control equipment and protective as well as riot control vehicles.

Specialized equipment for surveillance including hand held devices and unmanned

aerial vehicles.

Equipment and devices for night fighting capability including night vision devices.

Navigational and communications equipment including for secure

communications.

Specialized counter terrorism equipment and gear, assault platforms, detection

devices, breaching gear, etc.

Training aids including simulators and simulation equipment.

Civil Aerospace Products

All types of fixed wing as well as rotary aircraft including their air frames, aero

engines, aircraft components and avionics.

Aircraft design and engineering services.

Technical publications.

Raw material and semi-finished goods.

Flying training institutions and technical training institutions (excluding civil

infrastructure).

Pipavav Defence

232 March 2012

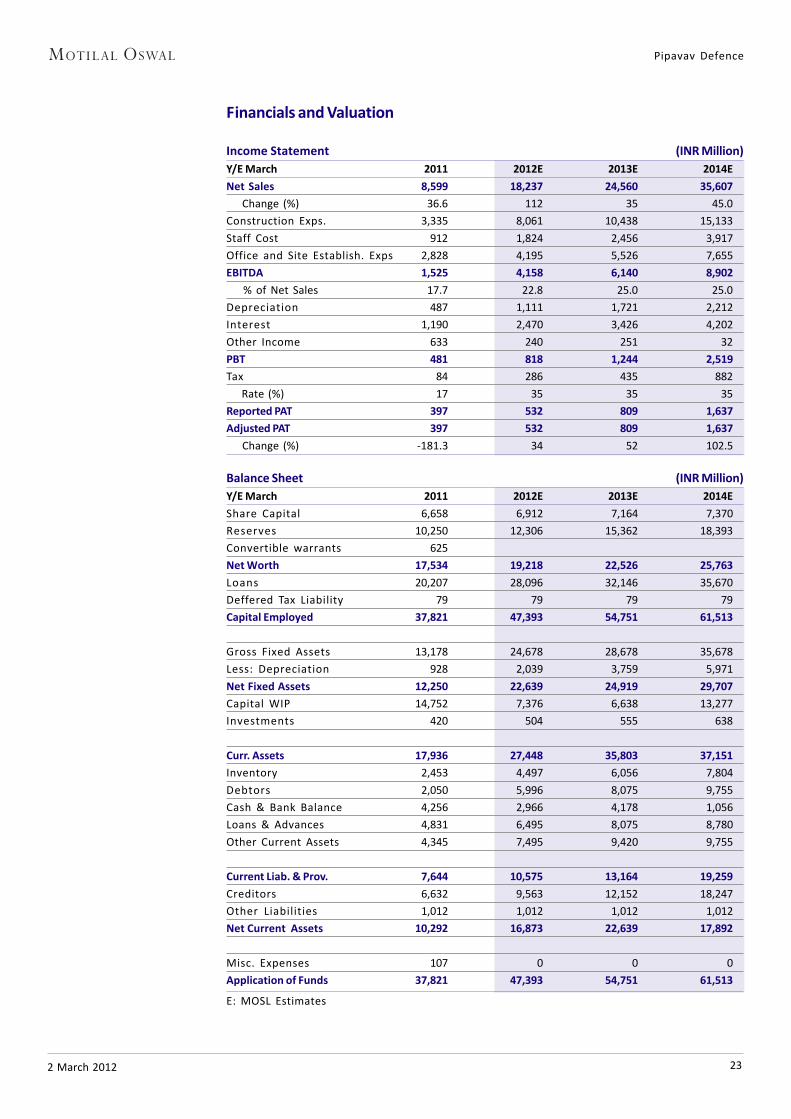

Financials and Valuation

Income Statement (INR Million)

Y/E March 2011 2012E 2013E 2014E

Net Sales 8,599 18,237 24,560 35,607

Change (%) 36.6 112 35 45.0

Construction Exps. 3,335 8,061 10,438 15,133

Staff Cost 912 1,824 2,456 3,917

Office and Site Establish. Exps 2,828 4,195 5,526 7,655

EBITDA 1,525 4,158 6,140 8,902

% of Net Sales 17.7 22.8 25.0 25.0

Depreciation 487 1,111 1,721 2,212

Interest 1,190 2,470 3,426 4,202

Other Income 633 240 251 32

PBT 481 818 1,244 2,519

Tax 84 286 435 882

Rate (%) 17 35 35 35

Reported PAT 397 532 809 1,637

Adjusted PAT 397 532 809 1,637

Change (%) -181.3 34 52 102.5

Balance Sheet (INR Million)

Y/E March 2011 2012E 2013E 2014E

Share Capital 6,658 6,912 7,164 7,370

Reserves 10,250 12,306 15,362 18,393

Convertible warrants 625

Net Worth 17,534 19,218 22,526 25,763

Loans 20,207 28,096 32,146 35,670

Deffered Tax Liability 79 79 79 79

Capital Employed 37,821 47,393 54,751 61,513

Gross Fixed Assets 13,178 24,678 28,678 35,678

Less: Depreciation 928 2,039 3,759 5,971

Net Fixed Assets 12,250 22,639 24,919 29,707

Capital WIP 14,752 7,376 6,638 13,277

Investments 420 504 555 638

Curr. Assets 17,936 27,448 35,803 37,151

Inventory 2,453 4,497 6,056 7,804

Debtors 2,050 5,996 8,075 9,755

Cash & Bank Balance 4,256 2,966 4,178 1,056

Loans & Advances 4,831 6,495 8,075 8,780

Other Current Assets 4,345 7,495 9,420 9,755

Current Liab. & Prov. 7,644 10,575 13,164 19,259

Creditors 6,632 9,563 12,152 18,247

Other Liabilities 1,012 1,012 1,012 1,012

Net Current Assets 10,292 16,873 22,639 17,892

Misc. Expenses 107 0 0 0

Application of Funds 37,821 47,393 54,751 61,513

E: MOSL Estimates

Pipavav Defence

242 March 2012

Financials and Valuation

Ratios (INR Million)

Y/E March 2011 2012E 2013E 2014E

Basic (INR)

Adjusted EPS 0.6 0.8 1.2 2.5

Growth (%) -181.3 33.9 52.2 102.5

Cash EPS 1.3 2.5 3.8 5.8

Book Value 26.3 27.8 31.4 35.0

Valuation (x)

P/E (standalone) 127.9 95.5 62.7 31.0

Cash P/E 57.4 30.9 20.1 13.2

EV/EBITDA 43.7 18.2 12.8 9.6

EV/Sales 7.8 4.2 3.2 2.4

Price/Book Value 2.9 2.6 2.3 2.0

Dividend Yield (%) 0.0 0.0 0.0 0.0

Profitability Ratios (%)

RoE 2.3 2.9 3.9 6.8

RoCE 4.9 7.7 9.1 11.6

Turnover Ratios

Debtors (Days) 87 120 120 100

Inventory (Days) 104 90 90 80

Creditors. (Days) 370 290 280 290

Asset Turnover (x) 0.3 0.4 0.5 0.6

Leverage Ratio

Debt/Equity (x) 1.2 1.5 1.4 1.4

Cash Flow Statement (INR Million)

Y/E March 2011 2012E 2013E 2014E

PBT before Extraordinary Items 481 818 1,244 2,519

Add : Depreciation 487 1,111 1,721 2,212

Interest 1,190 2,470 3,426 4,202

Less : Direct Taxes Paid 84 286 435 882

(Inc)/Dec in WC -7,255 -7,872 -4,554 1,626

CF from Operations -5,181 -3,760 1,401 9,678

(Inc)/Dec in FA -3,122 -4,124 -3,262 -13,638

(Pur)/Sale of Investments -152 -84 -50 -83

CF from Investments -3,275 -4,208 -3,313 -13,721

(Inc)/Dec in Networth 193 1,153 2,499 1,600

(Inc)/Dec in Debt 6,908 7,888 4,050 3,524

Less : Interest Paid 1,190 2,470 3,426 4,202

CF from Fin. Activity 6,311 6,678 3,124 922

Inc/Dec of Cash -2,145 -1,291 1,212 -3,122

Add: Beginning Balance 6,401 4,256 2,966 4,178

Closing Balance 4,256 2,966 4,178 1,056

E: MOSL Estimates

Motilal Oswal Company Gallery

DisclosuresThis report is for personal information of the authorized recipient and does not construe to be any investment, legal or taxation advice to you. This research report does not constitute an offer, invitation or inducementto invest in securities or other investments and Motilal Oswal Securities Limited (hereinafter referred as MOSt) is not soliciting any action based upon it. This report is not for public distribution and has beenfurnished to you solely for your information and should not be reproduced or redistributed to any other person in any form.

Unauthorized disclosure, use, dissemination or copying (either whole or partial) of this information, is prohibited. The person accessing this information specifically agrees to exempt MOSt or any of its affiliates

or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold MOSt or any of its affiliates or employees responsible for any such misuse and further agrees to hold MOStor any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.

The information contained herein is based on publicly available data or other sources believed to be reliable. While we would endeavour to update the information herein on reasonable basis, MOSt and/or itsaffiliates are under no obligation to update the information. Also there may be regulatory, compliance, or other reasons that may prevent MOSt and/or its affiliates from doing so. MOSt or any of its affiliates or

employees shall not be in any way responsible and liable for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report . MOSt or any of its affiliatesor employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitnessfor a particular purpose, and non-infringement. The recipients of this report should rely on their own investigations.

This report is intended for distribution to institutional investors. Recipients who are not institutional investors should seek advice of their independent financial advisor prior to taking any investment decision

based on this report or for any necessary explanation of its contents.

MOSt and/or its affiliates and/or employees may have interests/positions, financial or otherwise in the securities mentioned in this report. To enhance transparency, MOSt has incorporated a Disclosure of InterestStatement in this document. This should, however, not be treated as endorsement of the views expressed in the report.

Disclosure of Interest Statement Pipavav Defence & Offshore Engineering Company1. Analyst ownership of the stock No2. Group/Directors ownership of the stock No3. Broking relationship with company covered No4. Investment Banking relationship with company covered No

Analyst CertificationThe views expressed in this research report accurately reflect the personal views of the analyst(s) about the subject securities or issues, and no part of the compensation of the research analyst(s) was, is, orwill be directly or indirectly related to the specific recommendations and views expressed by research analyst(s) in this report. The research analysts, strategists, or research associates principally responsiblefor preparation of MOSt research receive compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors and firm revenues.

Regional Disclosures (outside India)This report is not directed or intended for distribution to or use by any person or entity resident in a state, country or any jurisdiction, where such distribution, publication, availability or use would be contrary tolaw, regulation or which would subject MOSt & its group companies to registration or licensing requirements within such jurisdictions.

For U.K.This report is intended for distribution only to persons having professional experience in matters relating to investments as described in Article 19 of the Financial Services and Markets Act 2000 (Financial

Promotion) Order 2005 (referred to as "investment professionals"). This document must not be acted on or relied on by persons who are not investment professionals. Any investment or investment activity towhich this document relates is only available to investment professionals and will be engaged in only with such persons.

For U.S.MOSt is not a registered broker-dealer in the United States (U.S.) and, therefore, is not subject to U.S. rules. In reliance on the exemption from registration provided by Rule 15a-6 of the U.S. Securities Exchange

Act of 1934, as amended (the "Exchange Act") and interpretations thereof by the U.S. Securities and Exchange Commission ("SEC") in order to conduct business with Institutional Investors based in the U.S.,Motilal Oswal has entered into a chaperoning agreement with a U.S. registered broker-dealer, Marco Polo Securities Inc. ("Marco Polo").

This report is intended for distribution only to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the Exchange Act and interpretations thereof by SEC (henceforth referred to as "major institutionalinvestors"). This document must not be acted on or relied on by persons who are not major institutional investors. Any investment or investment activity to which this document relates is only available to major

institutional investors and will be engaged in only with major institutional investors.

The Research Analysts contributing to the report may not be registered /qualified as research analyst with FINRA. Such research analyst may not be associated persons of the U.S. registered broker-dealer, MarcoPolo and therefore, may not be subject to NASD rule 2711 and NYSE Rule 472 restrictions on communication with a subject company, public appearances and trading securities held by a research analyst account.

Motilal Oswal Securities Ltd3rd Floor, Hoechst House, Nariman Point, Mumbai 400 021

Phone: (91-22) 39825500 Fax: (91-22) 22885038. E-mail: [email protected]