photovoltaic grid parity in the tertiary sector

TRANSCRIPT

PV Grid Parity Monitor for Commercial

Consumers

Financial Advisory Strategy Consulting Market Intelligence Policy Consulting

Leonardo ENERGY Webinar Series

April 11, 2014 - 10:00 CET

David Pérez, Partner

María Jesús Báez, Associate

GPM 3rd Issue

Platinum sponsors:

• ECLAREON

• Grid Parity Monitor (GPM)

- Introduction

- Definitions and Methodology

- Results

- Conclusions

Agenda

2

Platinum sponsors:

3

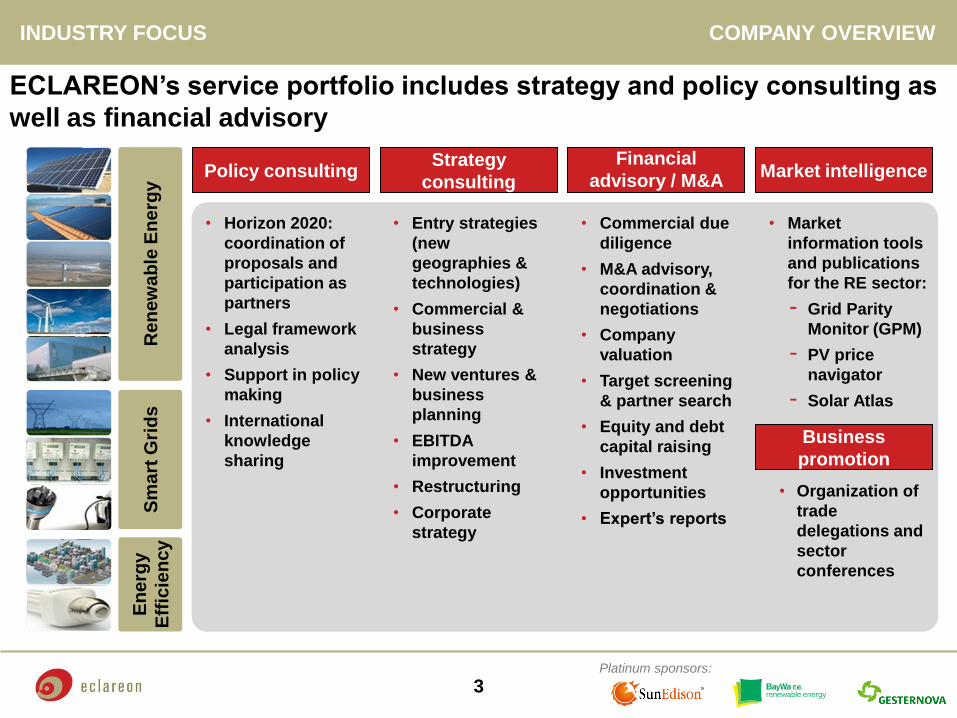

ECLAREON’s service portfolio includes strategy and policy consulting as

well as financial advisory

COMPANY OVERVIEW INDUSTRY FOCUS

• Entry strategies

(new

geographies &

technologies)

• Commercial &

business

strategy

• New ventures &

business

planning

• EBITDA

improvement

• Restructuring

• Corporate

strategy

• Market

information tools

and publications

for the RE sector:

- Grid Parity

Monitor (GPM)

- PV price

navigator

- Solar Atlas

• Organization of

trade

delegations and

sector

conferences

• Commercial due

diligence

• M&A advisory,

coordination &

negotiations

• Company

valuation

• Target screening

& partner search

• Equity and debt

capital raising

• Investment

opportunities

• Expert’s reports

• Horizon 2020:

coordination of

proposals and

participation as

partners

• Legal framework

analysis

• Support in policy

making

• International

knowledge

sharing

Strategy

consulting Market intelligence

Financial

advisory / M&A Policy consulting

Business

promotion

Re

ne

wa

ble

En

erg

y

Sm

art

Gri

ds

En

erg

y

Eff

icie

ncy

Platinum sponsors:

4

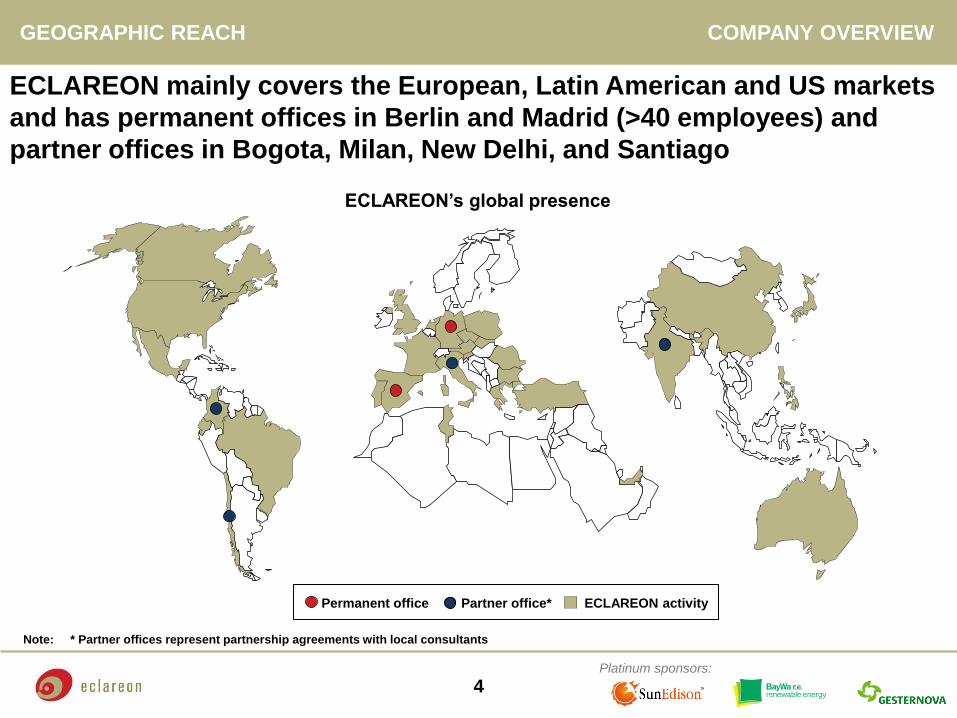

ECLAREON mainly covers the European, Latin American and US markets

and has permanent offices in Berlin and Madrid (>40 employees) and

partner offices in Bogota, Milan, New Delhi, and Santiago

ECLAREON’s global presence

Note: * Partner offices represent partnership agreements with local consultants

COMPANY OVERVIEW GEOGRAPHIC REACH

Permanent office Partner office* ECLAREON activity

Platinum sponsors:

• ECLAREON

• Grid Parity Monitor (GPM)

- Introduction

- Definitions and Methodology

- Results

- Conclusions

Agenda

5

Platinum sponsors:

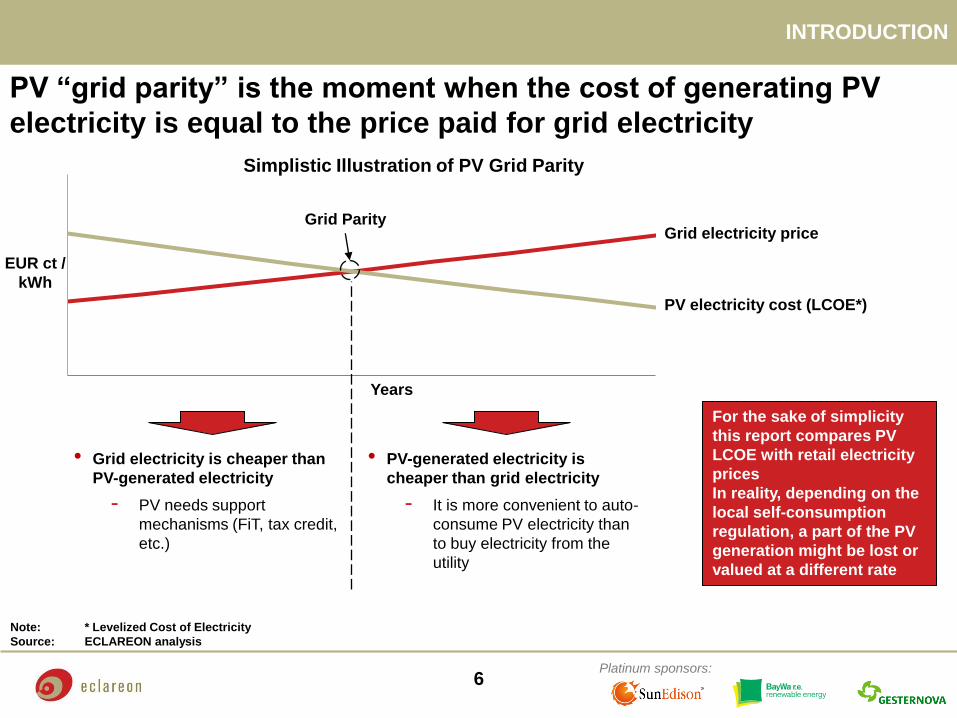

PV “grid parity” is the moment when the cost of generating PV

electricity is equal to the price paid for grid electricity

For the sake of simplicity

this report compares PV

LCOE with retail electricity

prices

In reality, depending on the

local self-consumption

regulation, a part of the PV

generation might be lost or

valued at a different rate

Note: * Levelized Cost of Electricity

Source: ECLAREON analysis

INTRODUCTION

Grid electricity price

PV electricity cost (LCOE*)

EUR ct /

kWh

Grid Parity

Years

Simplistic Illustration of PV Grid Parity

• Grid electricity is cheaper than

PV-generated electricity

- PV needs support

mechanisms (FiT, tax credit,

etc.)

• PV-generated electricity is

cheaper than grid electricity

- It is more convenient to auto-

consume PV electricity than

to buy electricity from the

utility

6

Platinum sponsors:

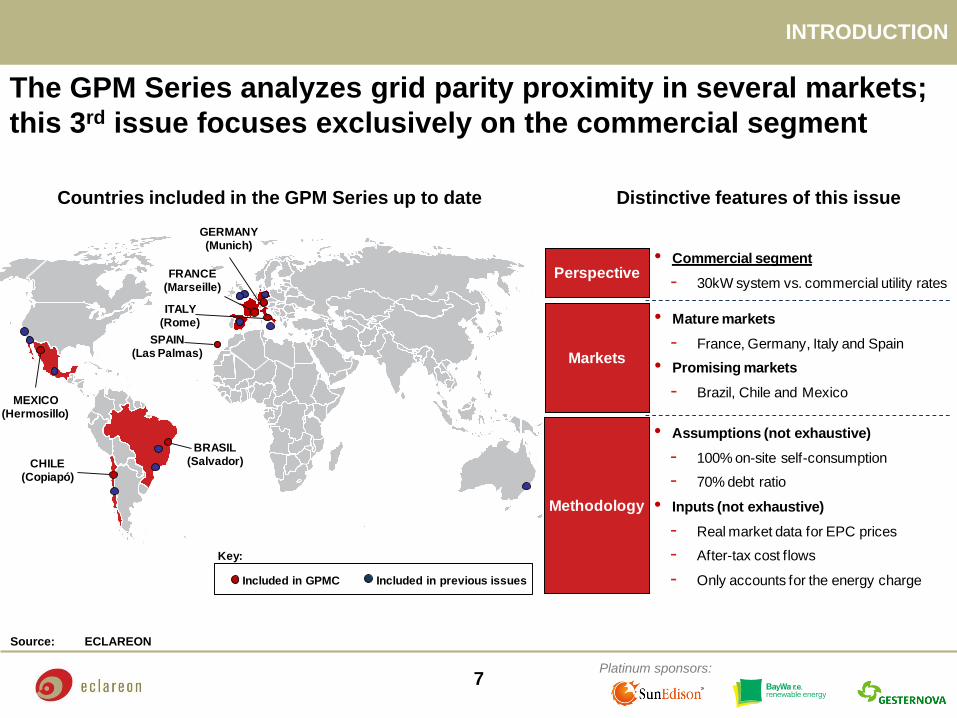

The GPM Series analyzes grid parity proximity in several markets;

this 3rd issue focuses exclusively on the commercial segment

INTRODUCTION

Countries included in the GPM Series up to date

Source: ECLAREON

7

Distinctive features of this issue

Included in GPMC Included in previous issues

BRASIL(Salvador)

MEXICO(Hermosillo)

SPAIN(Las Palmas)

ITALY(Rome)

FRANCE(Marseille)

GERMANY(Munich)

CHILE(Copiapó)

Key:

Perspective• Commercial segment

- 30kW system vs. commercial utility rates

Markets

• Mature markets

- France, Germany, Italy and Spain

• Promising markets

- Brazil, Chile and Mexico

Methodology

• Assumptions (not exhaustive)

- 100% on-site self-consumption

- 70% debt ratio

• Inputs (not exhaustive)

- Real market data for EPC prices

- After-tax cost flows

- Only accounts for the energy charge

Platinum sponsors:

The PV Grid Parity Monitor is sponsored by renowned international

companies

• Platinum Sponsors

• Gold Sponsors

INTRODUCTION SPONSORS

8

Platinum sponsors:

Platinum sponsors:

The PV Grid Parity Monitor is supported by relevant FV partners in

each market

• Partner Associations

• Supported by

INTRODUCTION PARTNERS

9

Platinum sponsors:

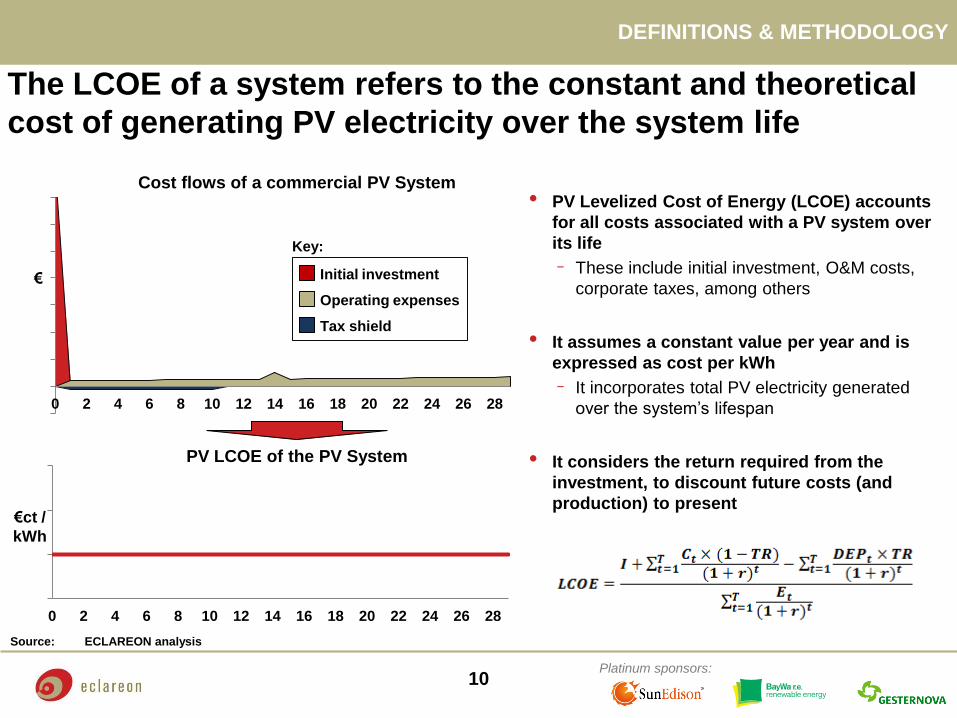

The LCOE of a system refers to the constant and theoretical

cost of generating PV electricity over the system life

DEFINITIONS & METHODOLOGY

Cost flows of a commercial PV System

Source: ECLAREON analysis

10

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28

€

Initial investment

Operating expenses

Key:

Tax shield

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28

€ct /

kWh

PV LCOE of the PV System

• PV Levelized Cost of Energy (LCOE) accounts

for all costs associated with a PV system over

its life

- These include initial investment, O&M costs,

corporate taxes, among others

• It assumes a constant value per year and is

expressed as cost per kWh

- It incorporates total PV electricity generated

over the system’s lifespan

• It considers the return required from the

investment, to discount future costs (and

production) to present

Platinum sponsors:

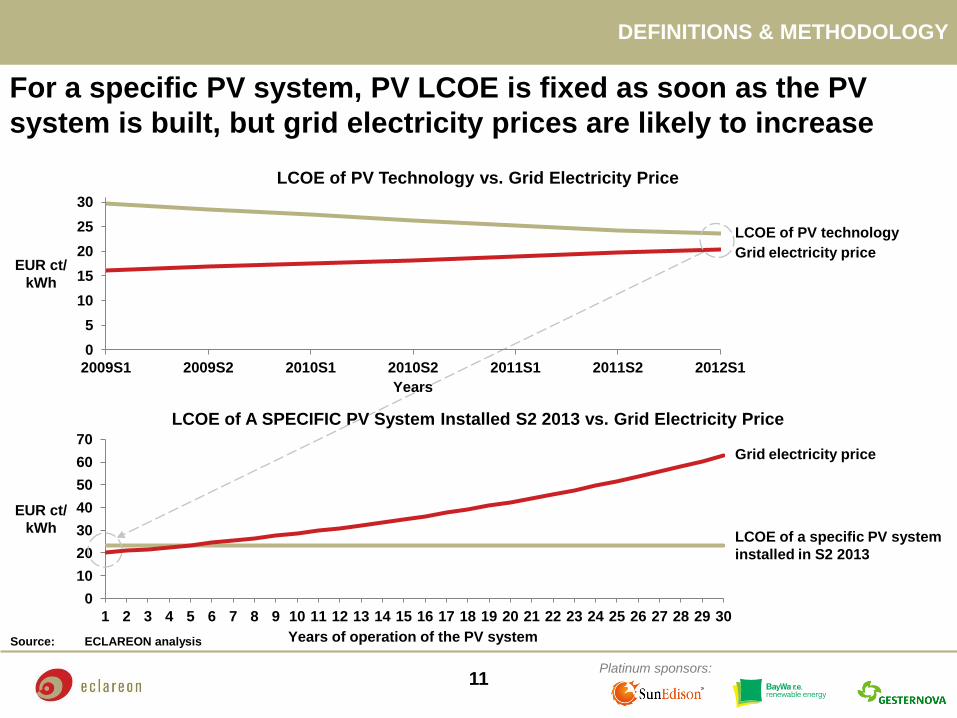

For a specific PV system, PV LCOE is fixed as soon as the PV

system is built, but grid electricity prices are likely to increase

LCOE of PV Technology vs. Grid Electricity Price

0

5

10

15

20

25

30

2009S1 2009S2 2010S1 2010S2 2011S1 2011S2 2012S1

Years

EUR ct/

kWh

LCOE of PV technology

Grid electricity price

0

10

20

30

40

50

60

70

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

EUR ct/

kWh

Years of operation of the PV system

Grid electricity price

LCOE of a specific PV system

installed in S2 2013

LCOE of A SPECIFIC PV System Installed S2 2013 vs. Grid Electricity Price

Source: ECLAREON analysis

DEFINITIONS & METHODOLOGY

11

Platinum sponsors: 12

Note: Data from the second half of 2013

Source: ECLAREON analysis

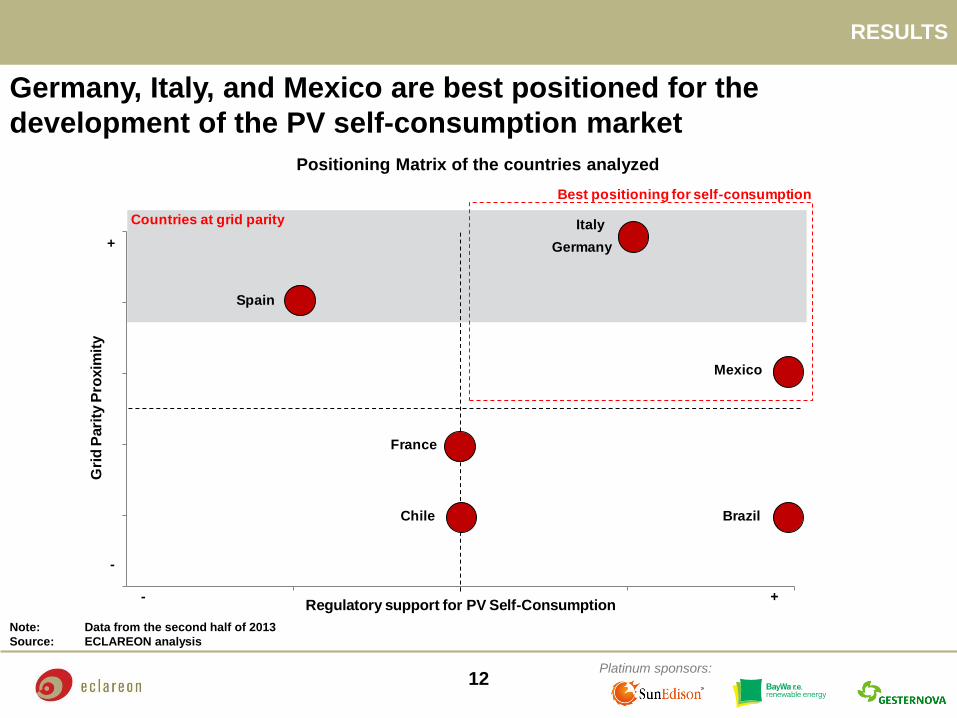

RESULTS

Germany, Italy, and Mexico are best positioned for the

development of the PV self-consumption market

Positioning Matrix of the countries analyzed

Note: Data from the 2nd half of 2013Source: ECLAREON Analysis

0,0

0,2

0,4

0,6

0,8

1,0

- +Regulatory support for PV Self-Consumption

-

+

Gri

d P

ari

ty P

roxim

ity

BrazilChile

France

Germany

Italy

Mexico

Spain

Countries at grid parity

Best positioning for self-consumption

Platinum sponsors:

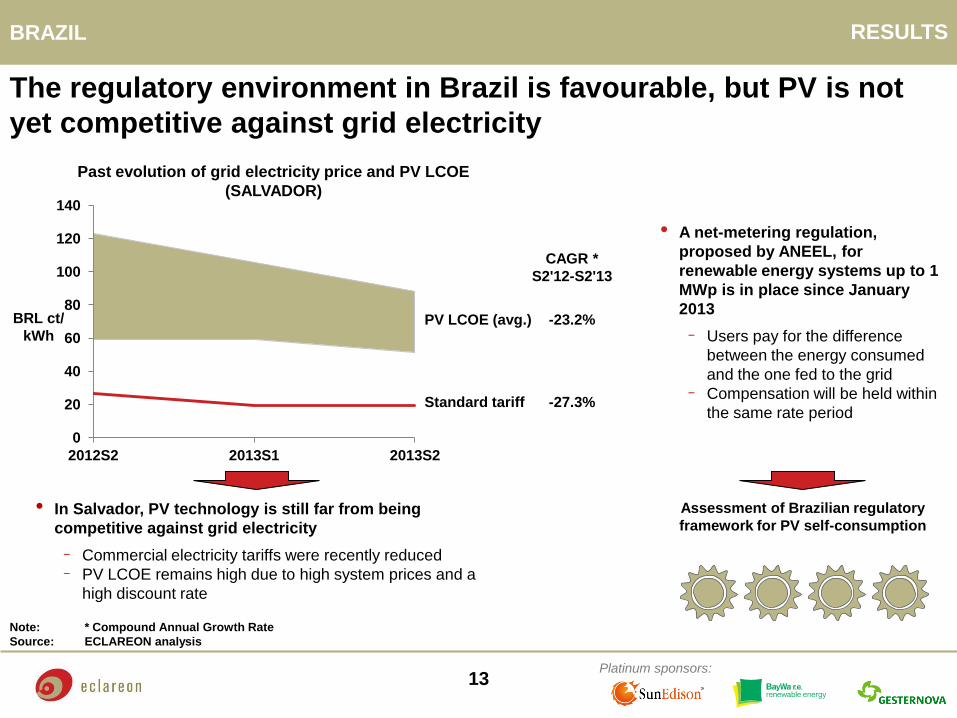

RESULTS BRAZIL

The regulatory environment in Brazil is favourable, but PV is not

yet competitive against grid electricity

Note: * Compound Annual Growth Rate

Source: ECLAREON analysis

Past evolution of grid electricity price and PV LCOE

(SALVADOR)

• A net-metering regulation,

proposed by ANEEL, for

renewable energy systems up to 1

MWp is in place since January

2013

- Users pay for the difference

between the energy consumed

and the one fed to the grid

- Compensation will be held within

the same rate period

Assessment of Brazilian regulatory

framework for PV self-consumption

13

0

20

40

60

80

100

120

140

2012S2 2013S1 2013S2

PV LCOE (avg.)

CAGR *

S2'12-S2'13

Standard tariff

-23.2%

-27.3%

BRL ct/

kWh

• In Salvador, PV technology is still far from being

competitive against grid electricity

- Commercial electricity tariffs were recently reduced

- PV LCOE remains high due to high system prices and a

high discount rate

Platinum sponsors:

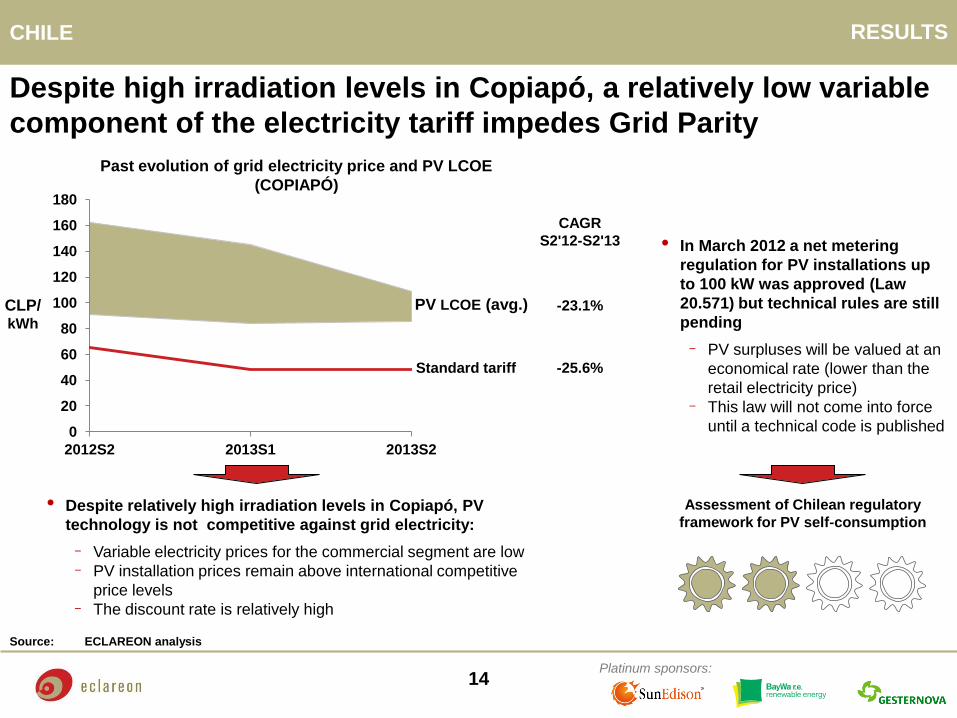

RESULTS CHILE

Despite high irradiation levels in Copiapó, a relatively low variable

component of the electricity tariff impedes Grid Parity

Past evolution of grid electricity price and PV LCOE

(COPIAPÓ)

• In March 2012 a net metering

regulation for PV installations up

to 100 kW was approved (Law

20.571) but technical rules are still

pending

- PV surpluses will be valued at an

economical rate (lower than the

retail electricity price)

- This law will not come into force

until a technical code is published

Assessment of Chilean regulatory

framework for PV self-consumption

Source: ECLAREON analysis

14

0

20

40

60

80

100

120

140

160

180

2012S2 2013S1 2013S2

PV LCOE (avg.)

CAGR

S2'12-S2'13

-23.1%

-25.6% Standard tariff

CLP/ kWh

• Despite relatively high irradiation levels in Copiapó, PV

technology is not competitive against grid electricity:

- Variable electricity prices for the commercial segment are low

- PV installation prices remain above international competitive

price levels

- The discount rate is relatively high

Platinum sponsors:

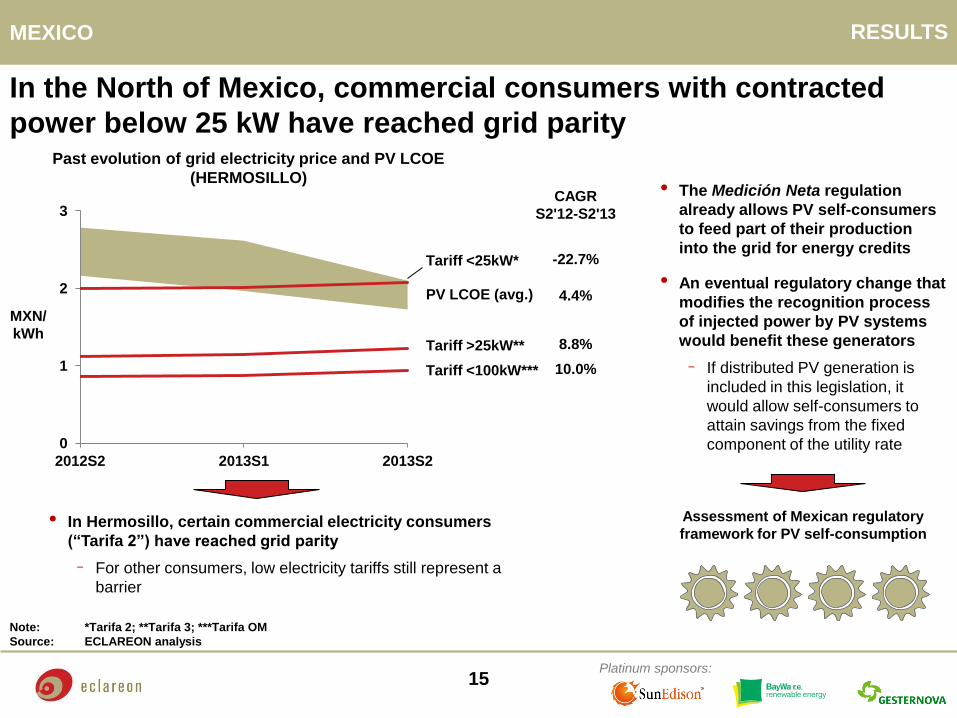

RESULTS MEXICO

In the North of Mexico, commercial consumers with contracted

power below 25 kW have reached grid parity Past evolution of grid electricity price and PV LCOE

(HERMOSILLO) • The Medición Neta regulation

already allows PV self-consumers

to feed part of their production

into the grid for energy credits

• An eventual regulatory change that

modifies the recognition process

of injected power by PV systems

would benefit these generators

- If distributed PV generation is

included in this legislation, it

would allow self-consumers to

attain savings from the fixed

component of the utility rate

Assessment of Mexican regulatory

framework for PV self-consumption

Note: *Tarifa 2; **Tarifa 3; ***Tarifa OM

Source: ECLAREON analysis

15

PV LCOE (avg.)

CAGR

S2'12-S2'13

-22.7%

4.4%

Tariff <25kW*

8.8% Tariff >25kW**

Tariff <100kW*** 10.0%

MXN/

kWh

0

1

2

3

2012S2 2013S1 2013S2

• In Hermosillo, certain commercial electricity consumers

(“Tarifa 2”) have reached grid parity

- For other consumers, low electricity tariffs still represent a

barrier

Platinum sponsors:

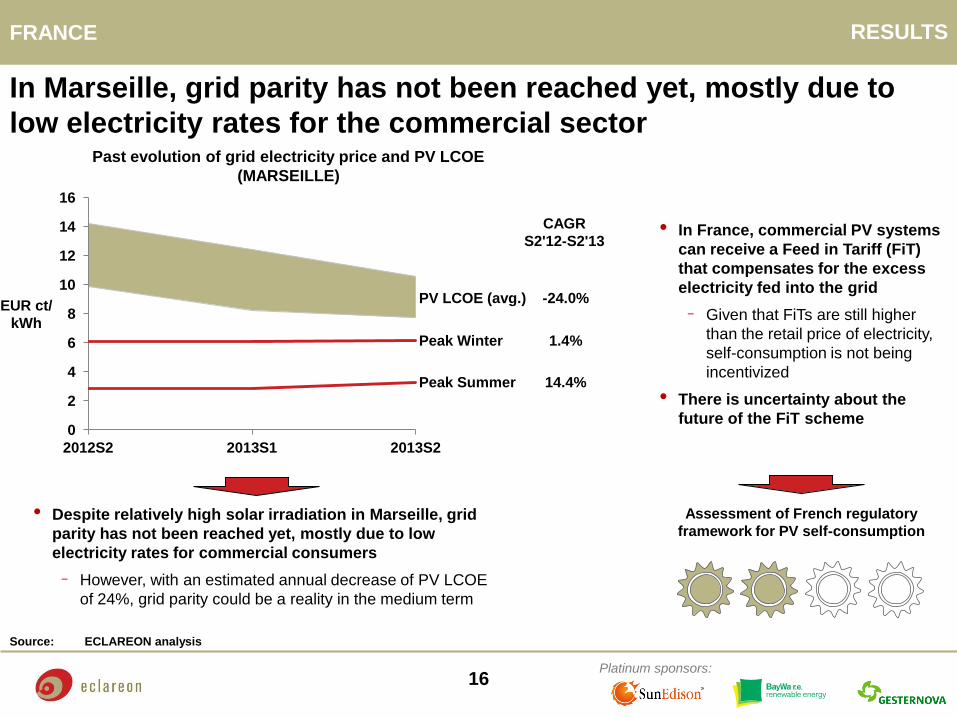

RESULTS FRANCE

In Marseille, grid parity has not been reached yet, mostly due to

low electricity rates for the commercial sector Past evolution of grid electricity price and PV LCOE

(MARSEILLE)

• In France, commercial PV systems

can receive a Feed in Tariff (FiT)

that compensates for the excess

electricity fed into the grid

- Given that FiTs are still higher

than the retail price of electricity,

self-consumption is not being

incentivized

• There is uncertainty about the

future of the FiT scheme

Assessment of French regulatory

framework for PV self-consumption

Source: ECLAREON analysis

16

0

2

4

6

8

10

12

14

16

2012S2 2013S1 2013S2

PV LCOE (avg.)

CAGR

S2'12-S2'13

Peak Summer

Peak Winter

-24.0%

1.4%

14.4%

EUR ct/

kWh

• Despite relatively high solar irradiation in Marseille, grid

parity has not been reached yet, mostly due to low

electricity rates for commercial consumers

- However, with an estimated annual decrease of PV LCOE

of 24%, grid parity could be a reality in the medium term

Platinum sponsors:

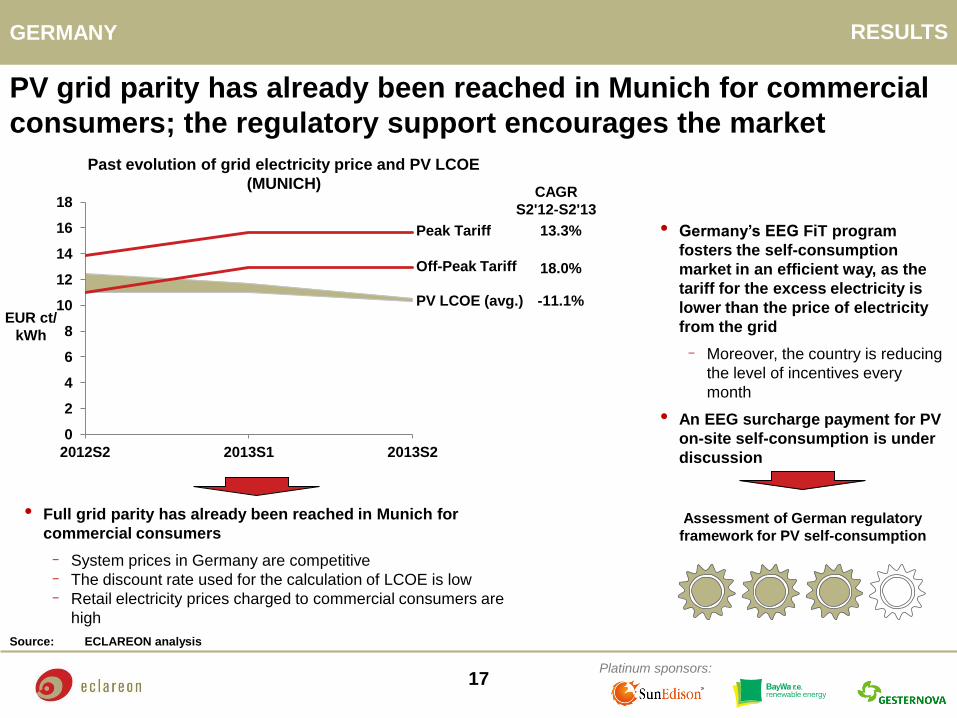

RESULTS GERMANY

PV grid parity has already been reached in Munich for commercial

consumers; the regulatory support encourages the market

• Germany’s EEG FiT program

fosters the self-consumption

market in an efficient way, as the

tariff for the excess electricity is

lower than the price of electricity

from the grid

- Moreover, the country is reducing

the level of incentives every

month

• An EEG surcharge payment for PV

on-site self-consumption is under

discussion

Assessment of German regulatory

framework for PV self-consumption

Source: ECLAREON analysis

17

0

2

4

6

8

10

12

14

16

18

2012S2 2013S1 2013S2

PV LCOE (avg.)

CAGR

S2'12-S2'13

Off-Peak Tariff

Peak Tariff 13.3%

18.0%

-11.1% EUR ct/

kWh

Past evolution of grid electricity price and PV LCOE

(MUNICH)

• Full grid parity has already been reached in Munich for

commercial consumers

- System prices in Germany are competitive

- The discount rate used for the calculation of LCOE is low

- Retail electricity prices charged to commercial consumers are

high

Platinum sponsors:

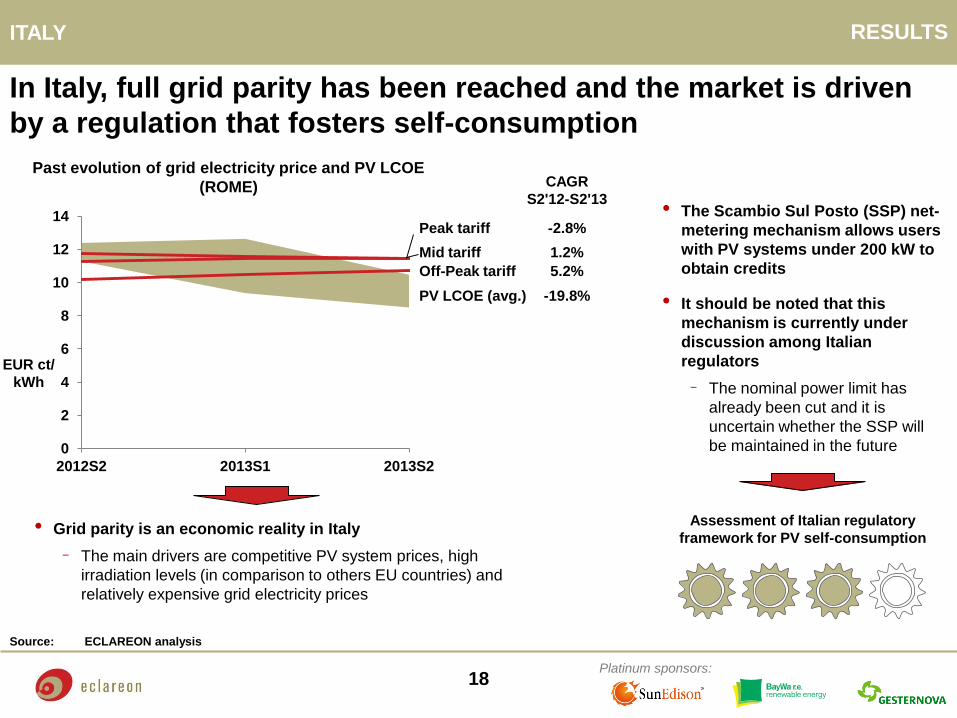

RESULTS ITALY

In Italy, full grid parity has been reached and the market is driven

by a regulation that fosters self-consumption

Past evolution of grid electricity price and PV LCOE

(ROME)

• The Scambio Sul Posto (SSP) net-

metering mechanism allows users

with PV systems under 200 kW to

obtain credits

• It should be noted that this

mechanism is currently under

discussion among Italian

regulators

- The nominal power limit has

already been cut and it is

uncertain whether the SSP will

be maintained in the future

Assessment of Italian regulatory

framework for PV self-consumption

Source: ECLAREON analysis

18

0

2

4

6

8

10

12

14

2012S2 2013S1 2013S2

PV LCOE (avg.)

CAGR

S2'12-S2'13

-2.8%

5.2%

-19.8%

Peak tariff

Mid tariff

Off-Peak tariff

1.2%

EUR ct/

kWh

• Grid parity is an economic reality in Italy

- The main drivers are competitive PV system prices, high

irradiation levels (in comparison to others EU countries) and

relatively expensive grid electricity prices

Platinum sponsors:

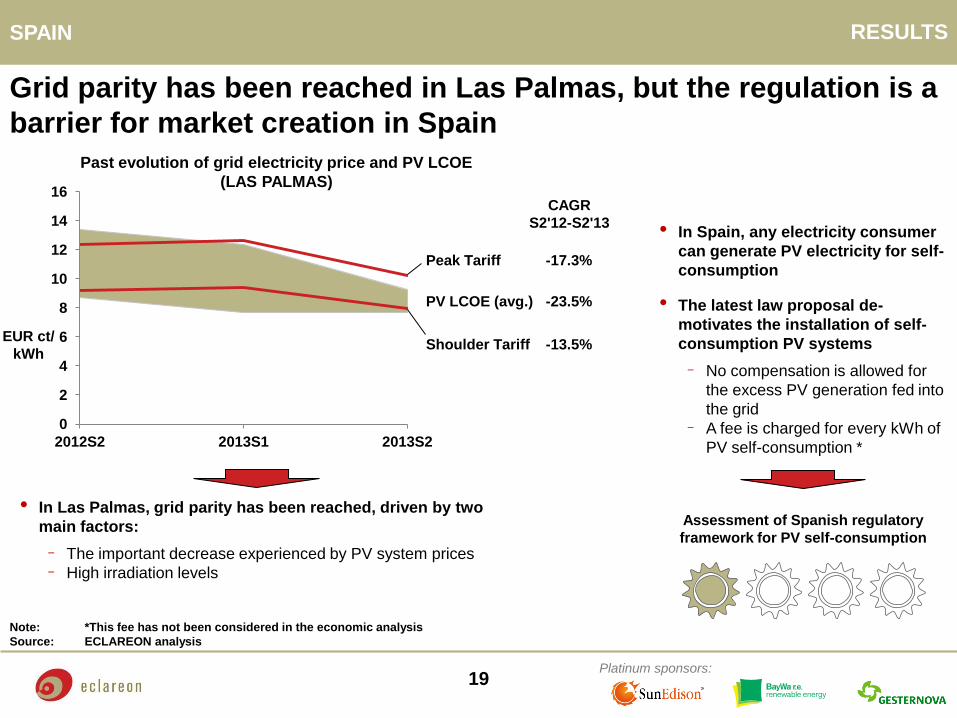

RESULTS SPAIN

Grid parity has been reached in Las Palmas, but the regulation is a

barrier for market creation in Spain

• In Spain, any electricity consumer

can generate PV electricity for self-

consumption

• The latest law proposal de-

motivates the installation of self-

consumption PV systems

- No compensation is allowed for

the excess PV generation fed into

the grid

- A fee is charged for every kWh of

PV self-consumption *

Assessment of Spanish regulatory

framework for PV self-consumption

Note: *This fee has not been considered in the economic analysis

Source: ECLAREON analysis

19

0

2

4

6

8

10

12

14

16

2012S2 2013S1 2013S2

CAGR

S2'12-S2'13

Shoulder Tariff

Peak Tariff

-23.5%

-17.3%

-13.5% EUR ct/

kWh

PV LCOE (avg.)

Past evolution of grid electricity price and PV LCOE

(LAS PALMAS)

• In Las Palmas, grid parity has been reached, driven by two

main factors:

- The important decrease experienced by PV system prices

- High irradiation levels

Platinum sponsors:

CONCLUSIONS

Main conclusions

• Grid parity for the commercial sector has been reached in major markets: Germany, Italy, Spain, and

Mexico *

• The results of the analysis show that the main driver of PV grid parity is the reduction of PV system

prices, one of the main parameters that determine LCOE

- LCOE has decreased the least in Germany (11% annual decrease) and the most in France (24%)

• Grid parity by itself is no guarantee of market creation, as PV self-consumption will only be fostered if

grid parity is combined with governmental regulatory support

- Germany, Italy, and Mexico are best positioned for PV self-consumption to represent a cost-effective and

sustainable alternative

• With PV already competitive against grid electricity in several markets, new trends are posing

challenges on grid parity

- In Germany, the idea of extending the EEG to on-site self-consumption is under discussion

- In Spain, the latest proposal on self-consumption includes a fee on self-consumption (called “peaje de

respaldo”) to cover grid charges

Note: * Commercial consumers under “Tarifa 2”

Source: ECLAREON

20

Platinum sponsors: 21

COMING SOON – New issue of the GPM Series focused on Utility

Scale PV Plants in various countries

Do you want more information about the GPM?

Click on the envelope to send us an email

• The GPM reports are massively distributed

- Specialized magazines: PV Magazine and others

- Specialized websites: Leonardo Energy with 1.4 million visits a

year and with over 70,000 subscribers

- Professional social media

- Senior PV professionals: last GPM issue was emailed to >18,500

professionals

- PV associations: collaborating associations distribute the GPM to

all their partners

Available @

http://www.leonardo-energy.org/

http://www.eclareon.eu/en/GPM

BE THE NEXT SPONSOR OF THE GPM

Contact us:

Davide Sabatino

+34 913 950 155