phosphate market outlook - the mosaic company · · 2017-07-21phosphate market outlook 1 society...

TRANSCRIPT

Phosphate Market Outlook

1

Society for Mining, Metallurgy and Exploration

Regional ConferenceOctober 12, 2016

Andy JungDirector, Market and Strategic Analysis

The Mosaic Company

This document contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements

include, but are not limited to, statements about the Wa’ad Al Shamal Phosphate Company (also known as MWSPC) and other proposed or

pending future transactions or strategic plans and other statements about future financial and operating results. Such statements are based upon

the current beliefs and expectations of The Mosaic Company’s management and are subject to significant risks and uncertainties. These risks

and uncertainties include but are not limited to risks and uncertainties arising from the ability of MWSPC to obtain additional planned funding in

acceptable amounts and upon acceptable terms, the timely development and commencement of operations of production facilities in the

Kingdom of Saudi Arabia, the future success of current plans for MWSPC and any future changes in those plans; difficulties with realization of

the benefits of our long term natural gas based pricing ammonia supply agreement with CF Industries, Inc., including the risk that the cost

savings initially anticipated from the agreement may not be fully realized over its term or that the price of natural gas or ammonia during the term

are at levels at which the pricing is disadvantageous to Mosaic; customer defaults; the effects of Mosaic’s decisions to exit business operations

or locations; the predictability and volatility of, and customer expectations about, agriculture, fertilizer, raw material, energy and transportation

markets that are subject to competitive and other pressures and economic and credit market conditions; the level of inventories in the distribution

channels for crop nutrients; the effect of future product innovations or development of new technologies on demand for our products; changes in

foreign currency and exchange rates; international trade risks and other risks associated with Mosaic’s international operations and those of joint

ventures in which Mosaic participates, including the risk that protests against natural resource companies in Peru extend to or impact the Miski

Mayo mine; changes in government policy; changes in environmental and other governmental regulation, including expansion of the types and

extent of water resources regulated under federal law, greenhouse gas regulation, implementation of numeric water quality standards for the

discharge of nutrients into Florida waterways or efforts to reduce the flow of excess nutrients into the Mississippi River basin, the Gulf of Mexico

or elsewhere; further developments in judicial or administrative proceedings, or complaints that Mosaic’s operations are adversely impacting

nearby farms, business operations or properties; difficulties or delays in receiving, increased costs of or challenges to necessary governmental

permits or approvals or increased financial assurance requirements; resolution of global tax audit activity; the effectiveness of Mosaic’s

processes for managing its strategic priorities; adverse weather conditions affecting operations in Central Florida, the Mississippi River basin, the

Gulf Coast of the United States or Canada, and including potential hurricanes, excess heat, cold, snow, rainfall or drought; actual costs of various

items differing from management’s current estimates, including, among others, asset retirement, environmental remediation, reclamation or other

environmental regulation, Canadian resources taxes and royalties, or the costs of the MWSPC, its existing or future funding and Mosaic’s

commitments in support of such funding; reduction of Mosaic’s available cash and liquidity, and increased leverage, due to its use of cash and/or

available debt capacity to fund financial assurance requirements and strategic investments; brine inflows at Mosaic’s Esterhazy, Saskatchewan,

potash mine or other potash shaft mines; other accidents and disruptions involving Mosaic’s operations, including potential mine fires, floods,

explosions, seismic events, sinkholes or releases of hazardous or volatile chemicals; and risks associated with cyber security, including

reputational loss, as well as other risks and uncertainties reported from time to time in The Mosaic Company’s reports filed with the Securities

and Exchange Commission. Actual results may differ from those set forth in the forward-looking statements.

Safe Harbor

The Mosaic Company Today

Mosaic helps the world grow the food it needs by mining

phosphorus (P) and potassium (K) minerals and refining these

ores into plant nutrient products essential for global agriculture.

Our North American operations typically dig, pump, cut, convey

and hoist 105 million tonnes of raw P&K ores from the earth

each year. We remove the sand, clay, salt and other elements

to produce roughly 26 million tonnes of refined ores.

We then process these refined ores into about 19 million

tonnes of finished products using an additional six million

tonnes of purchased or manufactured raw materials such as

sulphur and anhydrous ammonia.

The Largest P&K Company in the World

Mosaic – Leading Miner of Agricultural Minerals

Based on 2015 production

P2O5 production based on PACID and SSP production

K2O production based on MOP, SOP, and KMS production

Source: Company reports, IFA, CRU, and Mosaic

0.0 2.0 4.0 6.0 8.0 10.0

Mosaic

PotashCorp

Uralkali

Belaruskali

OCP

K+S

ICL

Yuntianhua

Qinghai Salt Lake

Agrium

Million Nutrient Tonnes

K2O P2O5

The Mosaic Company Today

U.S. Phosphate Operations

Offshore Phosphate Operations 35% equity stake in Bayovar phosphate rock mine in Peru

25% equity stake in Ma’aden II mine and chemical complex

under development in Saudi Arabia (2017)

53%47%

Phosphate Sales2012-15

North America Offshore

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

2010 2011 2012 2013 2014 2015

Mil TonnesU.S. Phosphate Production

DAP/MAP/MES Feed

5

Ag Market Outlook

Click to edit Master title style

6

Wild swings in agricultural commodity markets

▪ U.S. agriculture story− Key crop prices have declined notably since mid-June

• Ample supplies outpacing demand

• Record key U.S. crops

• Overall strength of the dollar

− Though 2017 prices (for which fertilizer is being purchased now) have been less volatile

3.00

3.25

3.50

3.75

4.00

4.25

4.50

US$ BU

New Crop Corn PriceDaily Close Dec '16 Contract

Source: CME

8.50

9.00

9.50

10.00

10.50

11.00

11.50

12.00

US$ BU

New Crop Soybean PriceDaily Close Nov '16 Contract

Source: CME

4.25

4.50

4.75

5.00

5.25

5.50

5.75

6.00

US$ BU

New Crop HRW Wheat PriceDaily Close Jul '17 Contract

Source: CME

Data through October 7, 2016

Click to edit Master title style

7

Wild swings in agricultural commodity markets

But the U.S. crop is only part of

the story- Prices of some other globally important crops

remain strong

• Sugar (+60%), coffee (+22%), cotton (+34%), palm

(+32%) are up notably from 2016 lows

- Currency fluctuations affect demand:

• Strong Dollar ► Advantage Brazil

And corn and soybeans account

for just 16% and 4% of global

fertilizer use!

Corn & Other Coarse Grains

21%

Wheat16%

Rice14%

Fruits & Veg.15%

Oilseeds11%

Other23%

Global Fertilizer Use

by Crop

Source: IFA

Use in 2010/11

We believe the future of the sector remains brightFood story not in vogue today, but still solidly intact

The global harvest will need to increase by more than the current combined harvests of Argentina, Brazil and

Canada (the ABCs) to meet projected grain and oilseed demand this decade…

…And demand is projected to increase the equivalent of ABC output plus Australia during the next decade

Farmers will need to plant record area and reap record yields, year after year, in order to meet the projected

demand for agricultural commodities during this decade and beyond

1.75

2.00

2.25

2.50

2.75

3.00

3.25

3.50

3.75

4.00

750

775

800

825

850

875

900

925

950

975

80 85 90 95 00 05 10 15 20 25 30

MT HaMil Ha World Harvested Area and Average Yield

Actual Area Forecast Area Actual Yield

Required Yield 1980-12 Yield Trend

Source: USDA and Mosaic

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

80 85 90 95 00 05 10 15 20 25 30

Mil Tonnes

Source: USDA and Mosaic

World Grain and Oilseed Use

Actual Biofuels Forecast Biofuels Actual G&O Forecast G&O

Phosphate Industry Review and Outlook

Click to edit Master title style

10

100

200

300

400

500

600

700

90 92 94 96 98 00 02 04 06 08 10 12 14 16

$ MT

DAP Pricesfob Tampa

Source: Fertecon and British Sulphur

Phosphate price cycles 1990-2016

Break-up of the

former Soviet

Union (FSU)

A drop in Indian

demand due to

subsidy changes

Strong agricultural

commodity prices;

steady China demand

U.S. industry

consolidation

High crop

prices in wake

of 2012 droughtPinnacle of U.S.

production and

trade (1995-2000)

China builds its

phosphate industry;

weak crop prices

Commodity super-

cycle; biofuels

exponential growth

Great global

recession and

financial crisis

Lower crop prices;

record Chinese

exports; ramp-up of

new capacity

Click to edit Master title style

11

The evolution of the U.S. phosphate industry (Phosphoric Acid Facilities/Capacity)

Capacity (mmt P2O5)

Percent NA Capacity

12

20

12.3

4

12

8.8

5.4

61%

1.9

22%

0.8

9%

0.7

8%

18

21

10.9

Firms:

Facilities:

Capacity (mmt P2O5):

Click to edit Master title style

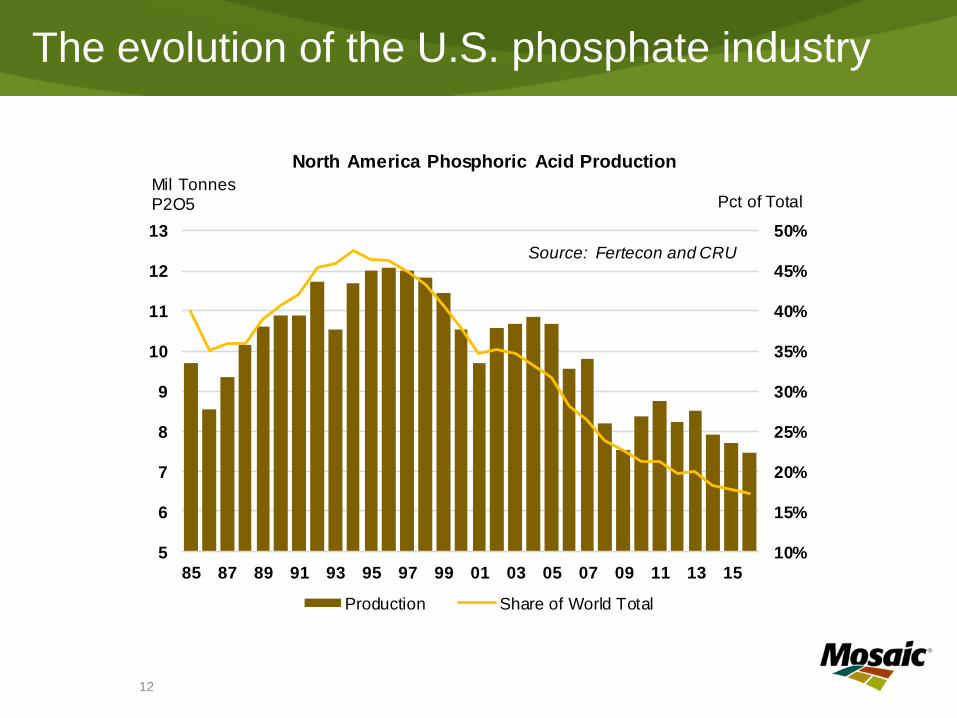

12

The evolution of the U.S. phosphate industry

10%

15%

20%

25%

30%

35%

40%

45%

50%

5

6

7

8

9

10

11

12

13

85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15

Pct of TotalMil TonnesP2O5

Source: Fertecon and CRU

North America Phosphoric Acid Production

Production Share of World Total

Click to edit Master title style

13

The evolution of the U.S. phosphate industry

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

60%

65%

3

4

5

6

7

8

9

10

11

12

13

14

85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15

Pct of TotalMil TonnesDAP/MAP/TSP

Source: Fertecon and CRU

North America Phosphate Exports

Exports Share of World Total

Fertilizer Year data (ending June 30)

Click to edit Master title style

14

Large (and growing) low-cost competitors

0

4

8

12

16

20

24

28

32

36

-6

-4

-2

0

2

4

6

8

10

12

85 90 95 00 05 10 15

Mil TonnesProduction

Mil TonnesNet Exports

China DAP/MAP/TSPProduction and Net Exports

DAP/MAP/TSP Net Exports DAP/MAP/TSP Production

Source: Fertecon and CRU

0.0

1.0

2.0

3.0

4.0

5.0

6.0

00 02 04 06 08 10 12 14 16F

Morocco DAP/MAP/TSP Exports

DAP MAP NPS TSP

Mil Tonnes

Source: CRU and Mosaic

0.0

0.5

1.0

1.5

2.0

2.5

3.0

00 02 04 06 08 10 12 14 16F

Saudi Arabia DAP/MAP/TSP Exports

DAP MAP

Mil Tonnes

Source: CRU and Mosaic

OCP in Morocco aiming to achieve 50%

of global phosphate growth and are in the

process of investing $20B to do so

China exports remain a wildcard but

Chinese expansion has plateaued

Ma’aden Phase II in Saudi Arabia

expected to produce DAP/MAP in 2017

Click to edit Master title style

15

Cautious sentiment in 2016, but demand poised to set a record (and positive outlook for 2017)

Modest rebound in shipments in 2016 before posting a more pronounced recovery in 2017

– Moderate prices

– Nutrients need to be replenished after

multiple massive crops depleted the

soil

– Strong uptake in India stemming from

decent monsoon and reservoir storage

going into 2017

– Strong pull from Brazil continues

– Offsets destocking taking place in 2016

65-6666-68

30

35

40

45

50

55

60

65

70

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15E16F17F

Global Phosphate ShipmentsMMT ProductDAP/MAP/NPS*/TSP

Source: CRU and Mosaic

* NPS products containing 45 or more combined units of N and P2O5

Click to edit Master title style

16

Longer Term Outlook

Balanced supply/demand

outlook during the next five

years

− Positive demand outlook

− Few projects in the pipeline

behind the large OCP and

Ma’aden projects

But fundamentals and behaviors

are changing

− New capacity during the next

two years

− New OCP strategy/behavior

− Restructuring of the large

Chinese industry

50

55

60

65

70

75

10 11 12 13 14 15 16F 17F 20F 21F

Global Phosphate Shipments

Actual High Forecast Low Forecast Likely Forecast CRU - Jul 2016

MMT DAP/MAP/NPS/TSP

Source: Mosaic and CRU Phosphate Outlook July 2016

Questions?

Phosphate Market Outlook

Society for Mining, Metallurgy and Exploration

Regional ConferenceOctober 12, 2016

Andy JungDirector, Market and Strategic Analysis

The Mosaic Company