phoenix solar ag · phoenix solar ag . excellence in global solar pv solutions . december 2016 ....

TRANSCRIPT

Phoenix Solar AG Excellence in Global Solar PV Solutions

December 2016

Invenergy Luning NV Project 65 MWp – COD 01/2017 Site view Sept. 28th, 2016

Phoenix Solar Delivers High Quality PV Power Plants International Track Record: > 800 MWp Installed

2

Selected reference projects

Duke Energy, 2015 Location: Fayetteville, North Carolina (USA) Completion time: 28 weeks System power: 32.1 MWp IPP: Duke Energy

Solar Park Kayseri, 2015 Location: Kayseri (Turkey) Completion time: 18 weeks System power: 6.9 MWp IPP: Turkish Industry Consortium

Solar Park Solarco, 2013 Location: Sai Yai (Thailand) Completion time: 36 weeks System power: 36.0 MWp IPP: Solarco

LTA Singapore Rooftop, 2016 Location: LTA-Gali Batu MRT Depot, Singapore Completion time: 10 weeks System power: 1.0 MWp IPP: Land Transport Authority Singapore

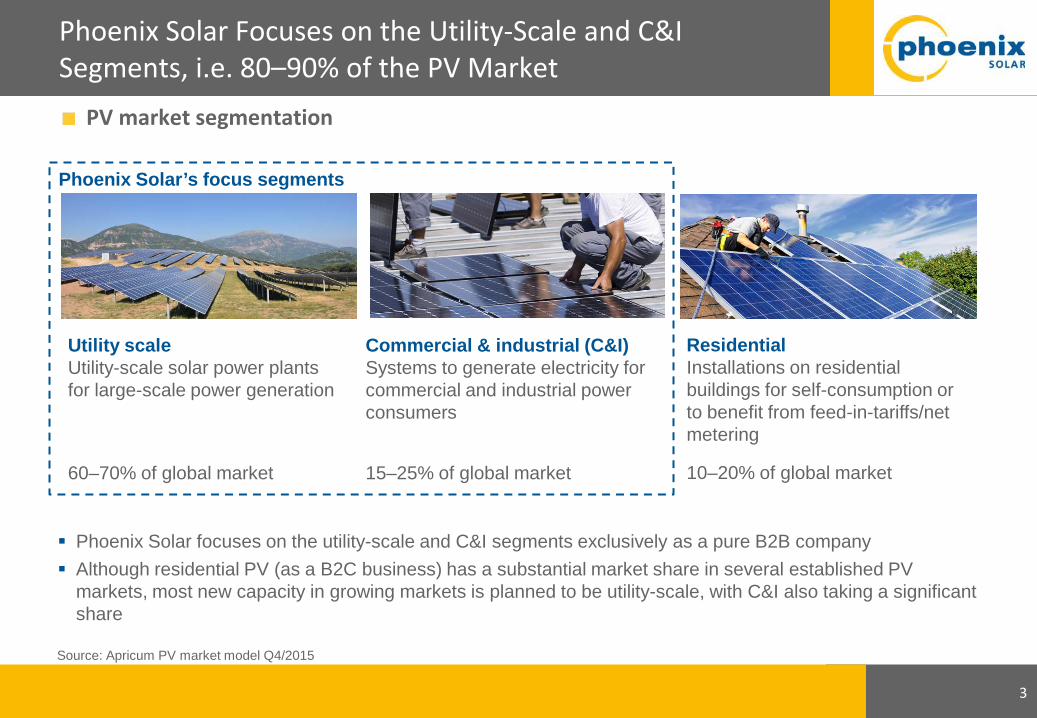

Phoenix Solar Focuses on the Utility-Scale and C&I Segments, i.e. 80–90% of the PV Market

3

PV market segmentation

Utility scale Utility-scale solar power plants for large-scale power generation 60–70% of global market

Commercial & industrial (C&I) Systems to generate electricity for commercial and industrial power consumers 15–25% of global market

Residential Installations on residential buildings for self-consumption or to benefit from feed-in-tariffs/net metering 10–20% of global market

Phoenix Solar’s focus segments

Phoenix Solar focuses on the utility-scale and C&I segments exclusively as a pure B2B company Although residential PV (as a B2C business) has a substantial market share in several established PV

markets, most new capacity in growing markets is planned to be utility-scale, with C&I also taking a significant share

Source: Apricum PV market model Q4/2015

Phoenix Solar is a Pioneer of the Photovoltaic Industry Mainly Focused on the Engineering of Power Plants

The predominant business model is „EPC“ of photovoltaic power plants – both, roof-top and green-field.

4

Customers Industrial, commercial and institutional investors, utilities

Sales

Operations

Suppliers Diverse local sales agents

in: progressional milestone payments

Engin- eering

Procure- ment

Construc- tion

Manufacturer independent: always best price-performance ratio for customer

in: long term contracts monthly/annual fees

Operation &

Mainten- ance (intl.)

Cash Flows

out: personnel and materials

Proposal Project Finance

Design & Engineering

Construction & Commissioning

Due Diligence Origination Operations &

Maintenance

Project Development EPC Skills O&M

5

Plant Design optimization is key to our

services. LCOE analysis to determine

right technology for the right use

Site studies: Geotechnical studies,

permitting, environmental, Phase I, PPA

negotiations, Interconnection Studies

Utility like safety standards are our

number one priority. Executing on time,

on budget and with an excellent

attention to detail based on high quality

German Engineering

Financial advisory work related to

arranging of construction and

permanent financing, financial model

review and 2 set of eyes for closing

documents

Director O&M oversees group.

Strong management, operations

and monitoring capabilities to

reduce overall ownership costs

Helping clients

select the optimal

sites in regards to

project execution

& production

Comprehensive,

competitive and

customized

proposal

depending on

customer needs

Phoenix Solar: Comprehensive „EPC+“ Capabilities

Phoenix has a truly global presence: Clear focus on fast growing, accessible markets

6

All 100% owned subsidiaries, except Phoenix Solar Singapore (75%), Phoenix Solar Malaysia (75%) and Phoenix Solar Oman (70%)

Phoenix Solar M.E.P.E., Greece (Since June 2008)

Phoenix Solar AG, Germany (Since Nov. 1999)

Phoenix Solar S.L., Spain (Since Apr. 2006)

Phoenix Solar SAS, France (Since Sept. 2009)

Phoenix Solar L.L.C., Oman (Since Dec. 2009)

Phoenix Solar Inc., USA (Since Sept. 2010)

Phoenix Solar Sdn Bhd, Malaysia (Since Sept. 2010)

Phoenix Solar Philippines Inc., Manila (Since Sep. 2015)

Phoenix Solar Pte Ltd., Singapore (Since Sep. 2006)

82%

7% 7% 4%

Revenue split 2015

Americas Middle East

Asia Pacific Europe Office locations

Phoenix Solar Delivers High-Quality PV Systems on Time and on Budget with High Customer Benefit

7

Customer focus

Differentiated approach Local partners

Flexible value chain position

Reliable quality at competitive pricing

On time and on budget Problem solvers

Experienced team

Lean structure

Agile reaction to markets

Lean and agile organization

Every market is different

Ultimate Goal: Create sustainable value for owners and investors globally through reliable engineering and execution of high performance power plants

0

20

40

60

80

100

120

140

160

Solar PV - CSi

Solar PV - thin film

Geothermal Wind Biomass Nat. Gas - Combined

Cycle

Coal Nuclear

low high

Lazard LCoE Study – 9th Iteration Levelized Cost of Energy: all-in production cost / unsubsidized

8

Quelle: Lazard, Levelized Cost of Energy Analysis, 11/2015 UNSUBSIDIZED

$US / MWh

The Global Solar PV Market is Expected to Continue its Rapid Growth

The global solar PV market is expected to continue its rapid growth, with annual installations more than doubling from 2014 to 2019

Annual investments in new PV installations amounted for approximately $90B in 2014 and are expected to reach $125–170B in 2020

Improving economics and ever-expanding grid parity are becoming more important drivers than subsidies in many countries

At the same time, a global push to phase out fossil fuels remains a strong tailwind for renewable energy, including solar

For growing economies with a strong growth in power demand, PV is the best way to quickly add new capacity

9

Projected annual global solar PV market [GWp]

31 39 42

58 62

66

77 85

94

2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

Source: Apricum PV market model Q4/2015, center scenario – revised after ITC extension

≈$90B

≈$125–170B

15%

CAGR ’12–’20

In the Selected Countries and Segments, Phoenix has a Large Potential Volume to Address

10

Total addressable market volume forecast in target regions [GW]

Source: Apricum Market Model Q4/2015 center scenario, revised after ITC extension (high and low cases shown for totals); only target segments shown (utility, C&I, where applicable and no residential)

3.9 5.0 9.0 7.6 9.1 10.3 12.0 1.5

1.4 1.6

1.9 2.5

3.2

1.1 1.8 2.2

2.6

2.9

1.0

1.3 1.5

1.5 1.5

1.5

2014 2015 2016 2017 2018 2019 2020

= range between high and low case

7.9

12.7 12.5

14.8

17.0

19.6

5.4 North America

Southeast Asia

MENA

Europe

Development since start of restructuring

11

Return to growth since 2015 – shift to 100% project business entails new challenges

2012/2013: Focus on Power Plants segment in growth regions (USA, MENA, Asia Pacific)

2014: German business completely discontinued.

2015: Shift to growing the business again, comprehensive sales focus

2012-2014: Headcount reduced by >270 within 1.5 years. Cost reduction by 60% in personnel and other operating expenses compared to 2011 realized break even level more than halved.

152.5 83.0 84.5 .16,5 113.5

241.0

72.4 56.7 17.3 5.9

2011A 2012A 2013A 2014A 2015A

Power Plants Components & Systems

2011A 2012A 2013A 2014A 2015A

-84.7

-31.8

-1.4 -4.6 -1.6

Sales (€M) EBIT (€M)

9M/2015 9M/2016

Revenue Growth and Earnings Improvement Continue

Revenues (€M)

82,202

108,334

FY 2014 FY 2015

+253%

33,783

119,407

EBIT (€M)

12

EBITDA (€M)

9M/2015 9M/2016

+88.6%

-3,503 -400

FY 2014 FY 2015

+66%

-4,616 -1,579

9M/2015 9M/2016

+€3mn

-2,508 427

FY 2014 FY 2015

+92%

-3,047 -237

9M/2015-2016 and full year development 2014–2015

+31.8%

Free order backlog at EUR 130.3 mn; weighted project pipeline holds 286 MWp; growth in all phases; weak order intake (project delays)

Highlights for the third quarter and the nine months of 2016: Q3: net profit, strong cash flow, improved gross margin

13

Strong backlog and pipeline

Gross margin improved

Q3 : net profit EBIT: 2.0 mn

Positive op. cash flow

Sale of Bâti-solaire PP

Higher efficiency: In spite of attributing operating personnel to project cost, gross margin improved to 8.8% in 9M/16 (up from 7.9%).

Business generates cash: CF from operations EUR 6.3 mn in 9M

Proceeds were used to repay debts: Net debt reduced to EUR 21 mn (09/30/16), down from EUR 34 (12/31/15)

Revenue growth

Revenues grew 32% in the nine months, 30% in the 3rd quarter; driven by all three core regions US, Middle East, Asia/Pacific

With positive EBIT in Q3 - operating loss close to zero for the 9M: EBIT: EUR -0.4 mn (9M/16) vs. EUR -3.5 mn (9M/15)

2014 A 2015 A 2016 E (prev.)

2016 E (rev.)

2016 Guidance revised due to project delays: Revenues to grow by 30 % / Operating profit of 0.5 to 2 €M

Revenues (€M)

14

EBIT (€M)

Revenues and EBIT for 2014/15 (actual) and 2016 (original and revised forecast)

2014 A 2015 A 2016 E (prev.)

2016 E (rev.)

33.8

119.4

180

210

2.0

4.0

-1.6 - 4.6

Careful cost management: Reduce cost per MWp

annually → increase gross margin Carefully adapt work-

force to revenue growth, flexible solutions Further reduce other

expenses after end of restructuring Mid-term: improve

financial result

150

135

2.0

0.5

Phoenix Solar Group CEO Direction & Vision Strong focus continues on building the foundation

15

Phase I 2015: Turnaround

Volume: from €34 to €120 mio

Turnaround, stabilization Global pipeline process

& growth Bank refinance 03/2016:

allows for both investor scenario and/or organic growth

Get last skeletons out of the cupboard (Altlasten)

Phase II 2016: Build Foundation Volume: from €120 mio

to > € 180 mio, + 50% Geography:

1) Strengthen 3 core Regions (NA, ME, AP) & 2) Expand to selected new markets

HR/Org Development Process Organization:

Efficiency, Best Practice Supply Chain: Cost +

Strategic Partnerships Value Chain: From EPC

to Project Development

Phase III Steady, Profitable Growth 2017-20

Volume: Consistent, rapid growth

Become a differentiated, global Solar PV Solutions Provider

Achieve significant market share in selected markets, segments

System 2020: drive technology

Further strategic fine-tuning t.b.d.

Phoenix Solar Group CEO Direction & Vision Strong focus continues on building the foundation

16

Phase I 2015: Turnaround

Volume: from €34 to €120 mio

Turnaround, stabilization Global pipeline process

& growth Bank refinance 03/2016:

allows for both investor scenario and/or organic growth

Get last skeletons out of the cupboard (Altlasten)

Phase II 2016: Build Foundation Volume: from €120 mio

to > € 180 mio, + 50% Geography:

1) Strengthen 3 core Regions (NA, ME, AP) & 2) Expand to selected new markets

HR/Org Development Process Organization:

Efficiency, Best Practice Supply Chain: Cost +

Strategic Partnerships Value Chain: From EPC

to Project Development

Phase III Steady, Profitable Growth 2017-20

Volume: Consistent, rapid growth

Become a differentiated, global Solar PV Solutions Provider

Achieve significant market share in selected markets, segments

System 2020: drive technology

Further strategic fine-tuning t.b.d.

Phoenix Solar Group CEO Direction & Vision Strong focus continues on building the foundation

17

Phase I 2015: Turnaround

Volume: from €34 to €120 mio

Turnaround, stabilization Global pipeline process

& growth Bank refinance 03/2016:

allows for both investor scenario and/or organic growth

Get last skeletons out of the cupboard (Altlasten)

Phase II 2016: Build Foundation Volume: from €120 mio

to > € 180 mio, + 50% Geography:

1) Strengthen 3 core Regions (NA, ME, AP) & 2) Expand to selected new markets

HR/Org Development Process Organization:

Efficiency, Best Practice Supply Chain: Cost +

Strategic Partnerships Value Chain: From EPC

to Project Development

Phase III Steady, Profitable Growth 2017-20

Volume: Consistent, rapid growth

Become a differentiated, global Solar PV Solutions Provider

Achieve significant market share in selected markets, segments

System 2020: drive technology

Further strategic fine-tuning t.b.d.

34,0

131,1

102,1

85,5

195,7 189,4 182,4

130,3

7,8

93,2

4,3 24,7

144,9

2,0

38,6

4,0

Dec 14 Mar 15 Jun 15 Sep 15 Dec 15 Mar 16 Jun 16 Sep 16

Free Order Backlog / Order Intake

Free order backlog Order Intake

18

Free Order Backlog is a Strong Indicator for Future Revenues

Close to 75% of Phoenix Solar’s Pipeline is Contracted / Under Construction

19

7

107 63

34 53 61 72 88

44

20

178 95 65

74 40

70

91

108

114 110

139

Mar 15 Jun 15 Sep 15 Dec 15 Mar 16 Jun 16 Sep 16

M3 On short list M4 Contract M5 Construction

MWp per milestone – weighted

135

221

174

320

262 235

286

20

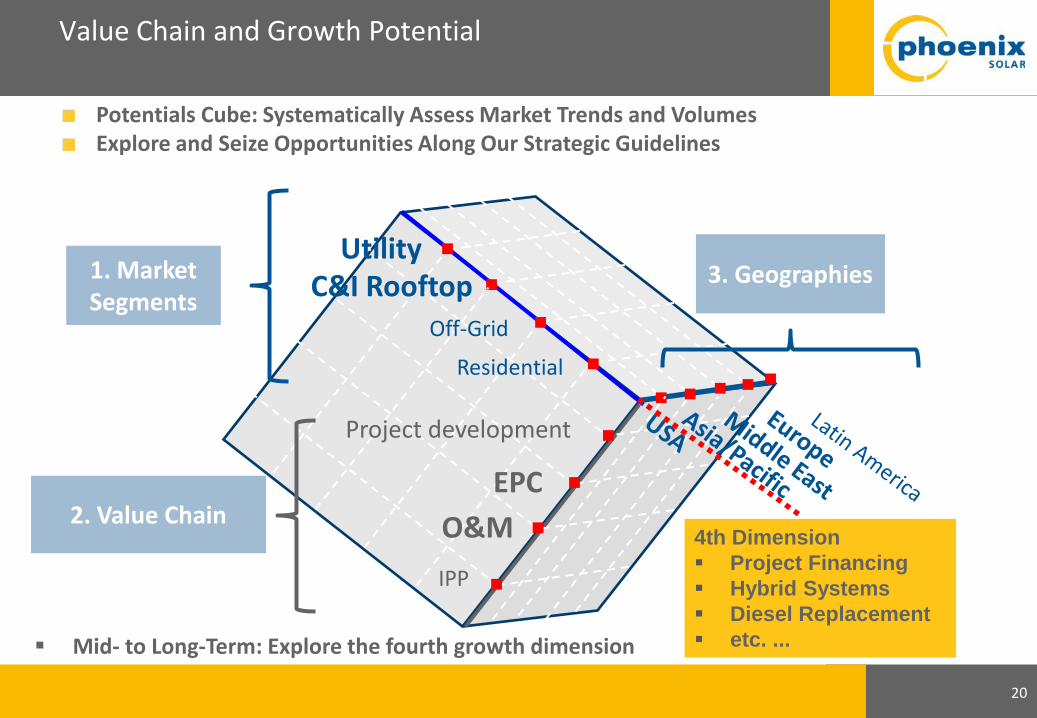

1. Market Segments

3. Geographies

2. Value Chain

EPC O&M IPP

Residential

Off-Grid

C&I Rooftop Utility

Project development

Value Chain and Growth Potential

Potentials Cube: Systematically Assess Market Trends and Volumes Explore and Seize Opportunities Along Our Strategic Guidelines

4th Dimension Project Financing Hybrid Systems Diesel Replacement etc. ... Mid- to Long-Term: Explore the fourth growth dimension

Strengthen footprint in three target regional clusters by further enhancing sales activities in high-growth markets in which Phoenix has already established itself Expand global reach by

entering into new markets within the three target regions (e.g., Mexico, Australia, Morocco)

Expand into project development

Improve competitiveness

Phoenix Solar’s Expansion and Growth: Poised to Enable a Step Change in Valuation

21

Expand to new geographies

Value creation for shareholders by investment in Phoenix

Build project development business leveraging broad expertise gained from EPC offering Enable Phoenix to hold

developed projects in emerging markets until risk perception of long-term project investors improves and projects can be sold at a better valuation

Increase attractiveness to clients and partners requesting a strong balance sheet and thereby increasing competitiveness Build global supply chain

capabilities to achieve 6–8% relative system cost savings annually Introduce process

organization to ensure efficiency, measurability and exchange of best practice

Phoenix Solar AG

“Excellence in Global Solar PV Solutions”

23

Full Service EPC: High quality EPC services at a competitive price

EPC +: Value-added services upstream: skills in project development & financing, downstream: O & M track record and skills

German-engineered, on-time, on-budget delivery of quality systems

Integrity, transparency, good Corporate Governance

Our core strengths

Customers do not look for price alone but rather for price/performance. Demand for reliable, experienced, global

EPC partners remains healthy.

Global presence

1.2 GWp track record

Bankability

Global network: suppliers, sub-contractors, financing partners

Team: qualified, seasoned industry professionals

Focus on ground mount & C&I rooftops

B2B customers and investors

Solar seen as “the future’s default technology” – the bright prospects for solar are widely accepted

24

“80% of countries are expected to be at grid parity by the end of 2017.”

Deutsche Bank – Jan 2015

Analyst market coverage

“Despite the recent drop in oil price, we expect solar electricity to become competitive with retail electricity in an increasing number of markets globally due to declining solar panel costs as well as improving financing and customer acquisition costs.”

Deutsche Bank – Mar 2015

“For the first time, the cost of generating electricity from the sun can compete with traditional sources of power in a number of key markets.”

Morgan Stanley – Jan 2015

“We believe solar will eventually replace nuclear and coal, and [be] establish[ed] as the default technology of the future to generate and supply electricity.”

UBS – Jun 2015

“The price of solar continues to move further toward grid parity – at utility scale, not just at the socket. “

HSBC – Mar 2014

“We commend world leaders for the ambitious pledges made [at COP21], which is sure to accelerate deployment of solar and boost investor confidence – sending a strong message that the low-carbon economy is real and already well underway."

Solar Power Europe – Dec 2015

Broad experience in growth - oriented

business development, general

management and leadership with

international businesses. Expert for the

technical, sales-related, commercial and

financial aspects of utility-scale and

commercial rooftop solar PV systems.

With extensive experience in financial

affairs, Manfred Hochleitner takes the

responsibility for Controlling, Treasury,

Group Accounting, Tax functions and he

plays a significant role in Group financing.

Expert in the field of photovoltaics since

1994. Lead a wide range of international

renewables & storage projects on behalf

of the European Commission & European

Parliament. CEO of the European

Photovoltaic Industry Association (EPIA)

2000 to 2003 and a board member since.

Tim P. Ryan CEO since 01/2015

Manfred Hochleitner CFO since 01/2015

Dr. Murray Cameron Founder, Member of the Executive Board (2003)

25

Major Responsibilities:

Corporate Strategy

Business Development and Sales

USA, Asia Pacific, Middle East Regions

Corporate Communications

Major Responsibilities:

Finance and administration

Internal Audit, Legal and Compliance

Europe Region

Investor Relations

Major Responsibilities:

Global Partner Network

Global Procurement

Strategy Projects

Phoenix Solar’s management consists of a well-balanced mix of industry and functional experts

Appendix

The Phoenix Solar Share: Key Data

5,4% 1,1%

93,6%

Volker Wiewer

Management & supervisory board Free float

PS4 share price development (1 yr)

Share details

Capital market data*

Shareholder structure ISIN / WKN DE000A0BVU93 / A0BVU9 Symbol PS4 Number of shares issued and outstanding

7,372,700 no-par bearer shares

Share capital € 7,372,700 Treasury shares none Authorized share capital € 3,686,350 Market segment Deutsche Börse Prime Standard Trading XETRA, Frankfurt (Prime Standard),

Munich (M:access), Stuttgart, Berlin, Dusseldorf, Hamburg, Hanover, Tradegate Exchange

Financial year end 31 December Designated sponsor Oddo Seydler

0 100 200 300 400 500 600 700

0

2,00

4,00

6,00

8,00

Jun-

15

Jul-1

5

Aug-

15

Sep-

15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb-

16

Mar

-16

Apr-

16

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct

-16

Volume ('000) Share Price (€)

26 Appendix

Share price (in €) 2.423 52-w-high / -low 5.000 / 2.276

30-day avg. share price absolute / volume weighted 2.691 / 2.526

90-day avg. share price absolute / volume weighted 2.965 / 2.8655

180-day avg. share price absolute / volume weighted 3.286 / 3.2624

30-day avg. trading volume (in shares) 16,441 90-day avg. trading volume 12,301 180-day avg. trading volume 14,940 No. of shares outstanding (in ’000) 7,372.7 Market capitalization (in €M) 17.9

* as of Nov. 14, 2016

27

13,6*14,88

Share Price Development (Jun 5, 2016 – Dec 4, 2016)

Appendix

28

The content of this presentation is solely for information purposes and is not intended to constitute a recommendation for investment or a solicitation to subscribe or an offer to buy or sell securities of the company. Phoenix Solar AG shall undertake no liability whatsoever for any loss in connection with this presentation or the information contained therein. This also applies particularly to any eventual loss in connection with the shares of Phoenix Solar AG. This document contains forward-looking statements on future developments which are based on management’s current assessment. Words such as “anticipate”, “assume”, “believe”, “estimate”, “expect”, “intend”, “can/could”, “plan”, “project”, “forecast”, “should”, and similar terms are indicative of such forward-looking statements. Such statements are subject to certain risks and uncertainties which are mainly outside the sphere of influence of Phoenix Solar AG, but which have an impact on the business activities, the success, the business strategy and the results. These risks and factors of uncertainty include, for instance, climatic change, changes in the state subsidisation of photovoltaics, the introduction of competitor products or technologies of other companies, the development of the planned internationalisation of business activities, fierce competition as well as rapid technological change in the photovoltaic market. If one of these or other factors of uncertainty or risks should occur, or if the assumptions underlying the statements should prove incorrect, the actual results may diverge substantially from the results in these statements or implicit indications. Phoenix Solar AG does not have the intention nor will it undertake any obligation to realise forward-looking statements on an ongoing basis or at a later point in time as this is entirely dependent on circumstances prevailing on the day of their release. In some countries the dissemination of this presentation and the information contained therein may be restricted or prohibited under the law. This presentation is therefore expressly not intended for persons resident in legal systems under which such an offer or solicitation is not permissible, or for persons for whom such an offer or invitation would constitute a breach of the law.

Appendix

Disclaimer

29

Phoenix Solar AG Dr. Joachim Fleïng Hirschbergstraße 4 D-85254 Sulzemoos Germany Phone +49 8135 938-315 Fax +49 8135 938-429 www.phoenixsolar-group.com [email protected]

Appendix

Contact Details