phoenix - reiacreiac.org/pdfs/sw_2017_11_15-peterlinneman.pdf · actual vs. trend real gdp: ......

TRANSCRIPT

Phoenix

Dr. Peter LinnemanLinneman AssociatesNovember 15, 2017

5

7

9

11

13

15

17

19

21

23

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

$ Tr

illio

ns

Actual Trend (1969-2007)

Actual vs. Trend Real GDP:Still A Huge Gap Due To SF Housing

Data points through Q2 2017

$3.2 T

2

0

10

20

30

40

50

60

70

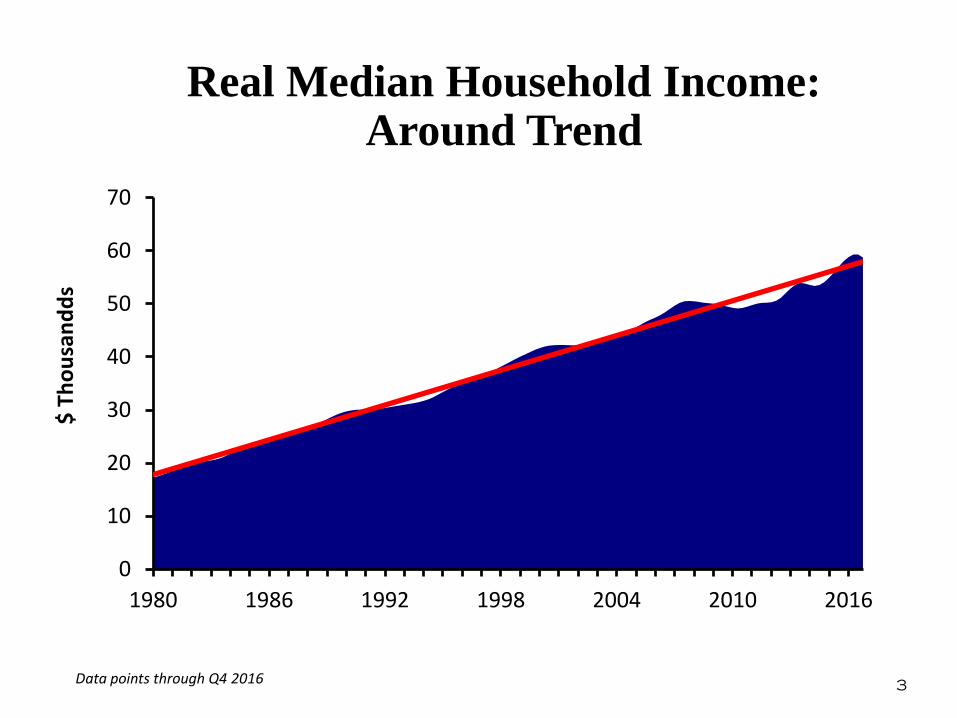

1980 1986 1992 1998 2004 2010 2016

$ Th

ousa

ndds

Real Median Household Income:Around Trend

Data points through Q4 2016 3

0

20

40

60

80

100

120

140

160

1977 1982 1987 1992 1997 2002 2007 2012 2017

Consumer Confidence Index: Post-Election Pop Continues

4Data points through September 2017

80

85

90

95

100

105

110

1986 1990 1994 1998 2002 2006 2010 2014

Small Business Optimism Index: Post-Election Surge Continues

5Data points through September 2017

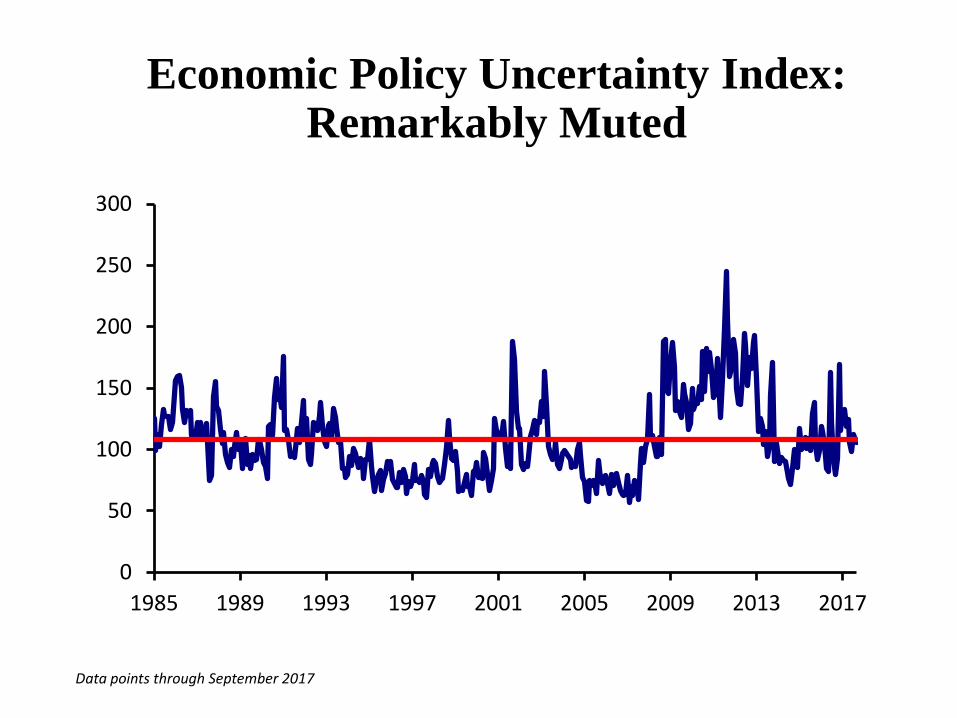

0

50

100

150

200

250

300

1985 1989 1993 1997 2001 2005 2009 2013 2017

Economic Policy Uncertainty Index: Remarkably Muted

Data points through September 2017

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

$ Bi

llion

s

Profits After Tax Distributed Profits

Real Corporate Profits:High But Tough To Grow

Data points through Q2 2017

Private Sector Employment:All Time High

0

20

40

60

80

100

120

140

1939 1946 1954 1961 1969 1976 1984 1991 1999 2006 2014

Mill

ions

Pre-Recession Peak

8Data points through September 2017

0

5

10

15

20

25

30

1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

Perc

ent

All Workers 16-19 Year Olds

Civilian Unemployment Rate: Nearing Lows

9Data points through September 2017

0

100

200

300

400

500

600

700

800

1967 1973 1980 1987 1994 2001 2008 2015

Thou

sand

sWeekly Initial Unemployment Insurance Claims: Very Strong

Data points through Oct 14, 2017 10

64

66

68

70

72

74

76

78

80

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Data points through 2015 11

U.S. Life Expectancy At Birth:We Live 6 Weeks Longer Per Year

Labor Force Participation Rate 65+:And Choose To Work Longer

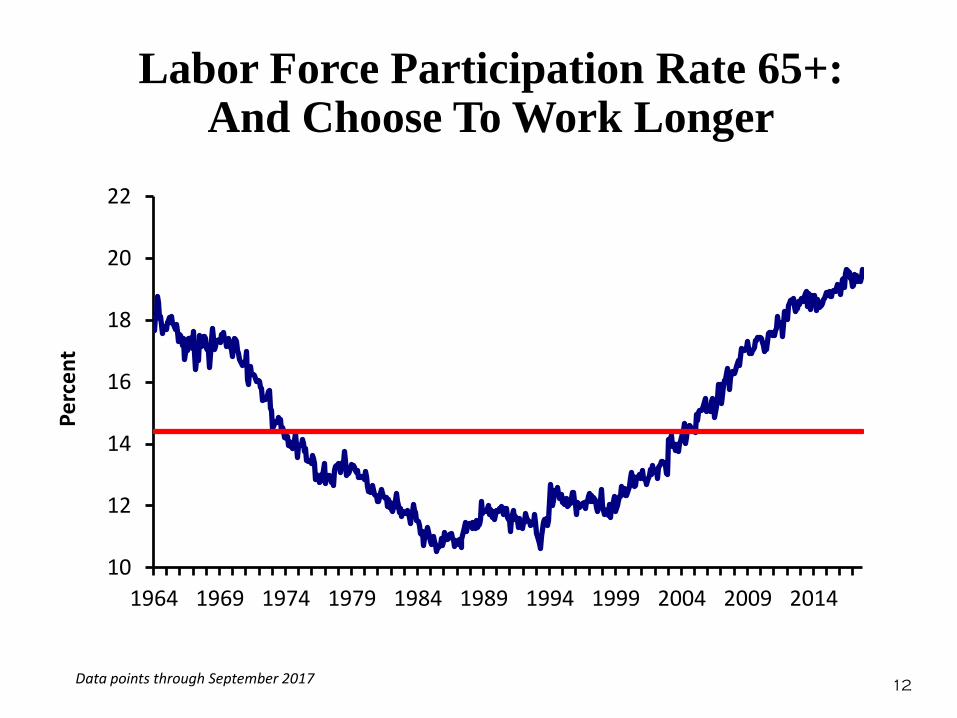

10

12

14

16

18

20

22

1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

Perc

ent

12Data points through September 2017

-15

-10

-5

0

5

10

15

20

25

1957 1963 1969 1975 1981 1987 1993 1999 2005 2011

Perc

ent

Real U.S. Net Worth Per HouseholdPercent Gap Above (Below) Trend: Not Crazy

13Data points through Q2 2017

50

75

100

125

150

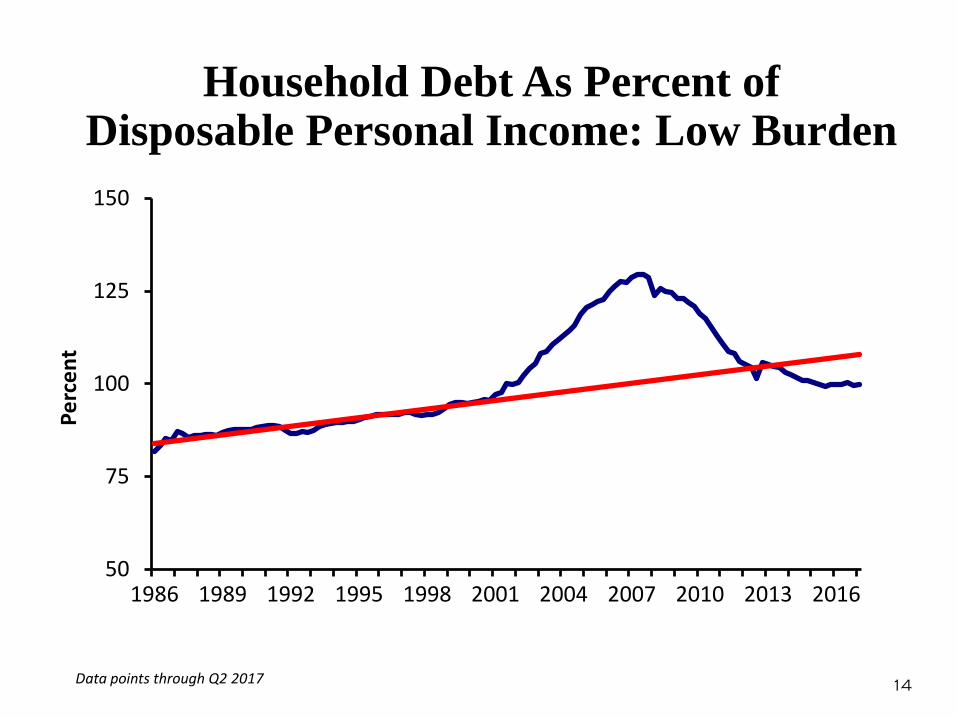

1986 1989 1992 1995 1998 2001 2004 2007 2010 2013 2016

Perc

ent

Household Debt As Percent of Disposable Personal Income: Low Burden

14Data points through Q2 2017

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2006 2008 2010 2012 2014 2016

$ Tr

illio

ns

Credit Card Auto Loans Student Loans Other

Real U.S. Consumer Debt: Student Loans Have Replaced Credit Cards

15Data points through Q2 2017

0

1

2

3

4

5

6

2001 2003 2005 2007 2009 2011 2013 2015 2017

Perc

ent

30-Day T-Bill 10-Year Treasury

Treasury Yields: Low Rates Kill The Economy, By Killing Housing And Cash Hoarding

Data points through September 2017

1.0

1.1

1.2

1.3

1.4

1.5

1.6

2004 2006 2008 2010 2012 2014 2016

$ Tr

illio

ns (S

AAR)

Real Income from Interest Payments: Savers Have Been Robbed By The Fed

$2.2 Trillion Lost Interest Payments

Data points through August 2017

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

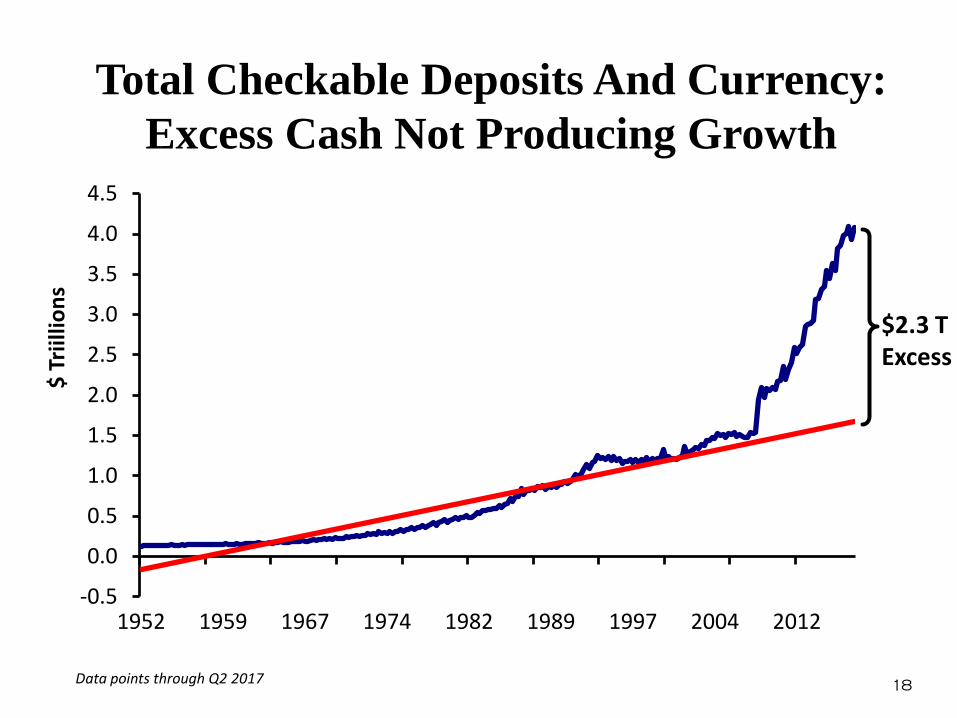

1952 1959 1967 1974 1982 1989 1997 2004 2012

$ Tr

iillio

nsTotal Checkable Deposits And Currency:

Excess Cash Not Producing Growth

18Data points through Q2 2017

$2.3 TExcess

-1,200

-1,000

-800

-600

-400

-200

0

2002 2004 2006 2008 2010 2012 2014 2016

Thou

sand

sCumulative Shortage of Multifamily Starts:

Still High

931 KGap

Data points through September 2017

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Thou

sand

sSingle Family Home Starts: Up 100% And Still 134,000 Units Below Average

20Data points through September 2017

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

2002 2004 2006 2008 2010 2012 2014 2016

Thou

sand

s

Cumulative Shortage of Single-Family Starts: Huge And Growing

Compared to 1971-2001 Average. Data points through September 2016

2.8 MGap

21

0

50

100

150

200

250

300

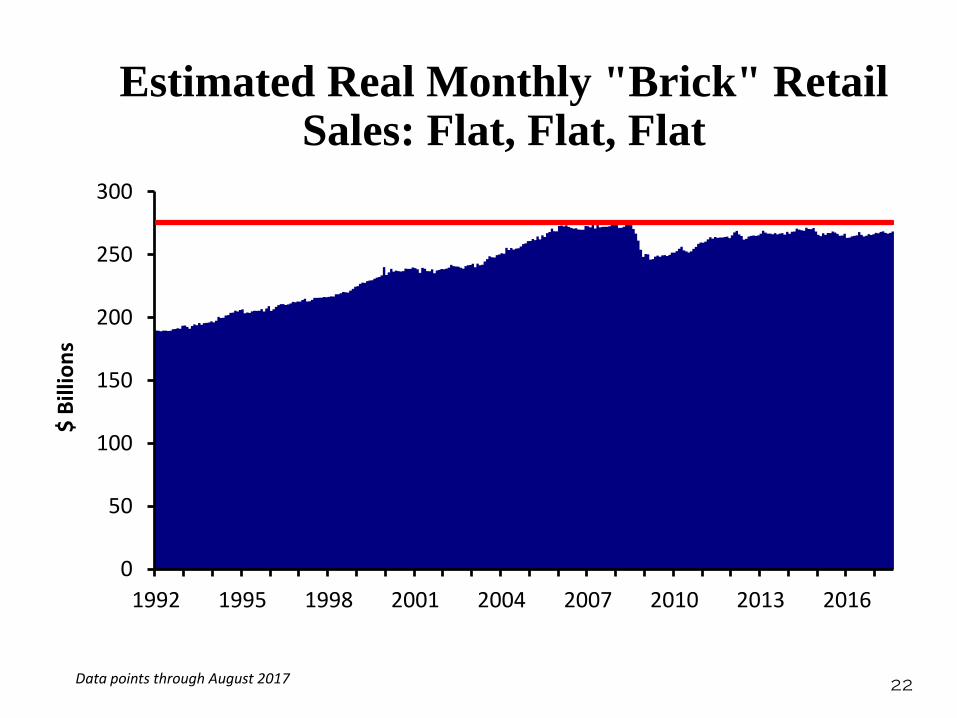

1992 1995 1998 2001 2004 2007 2010 2013 2016

$ Bi

llion

sEstimated Real Monthly "Brick" Retail

Sales: Flat, Flat, Flat

22Data points through August 2017

-202468

1012141618

1992 1995 1998 2001 2004 2007 2010 2013 2016

$ Bi

llion

sEstimated Real Monthly Internet Sales:

Rapidly Rising But Still Only 5.7% Of Sales

23Data points through August 2017

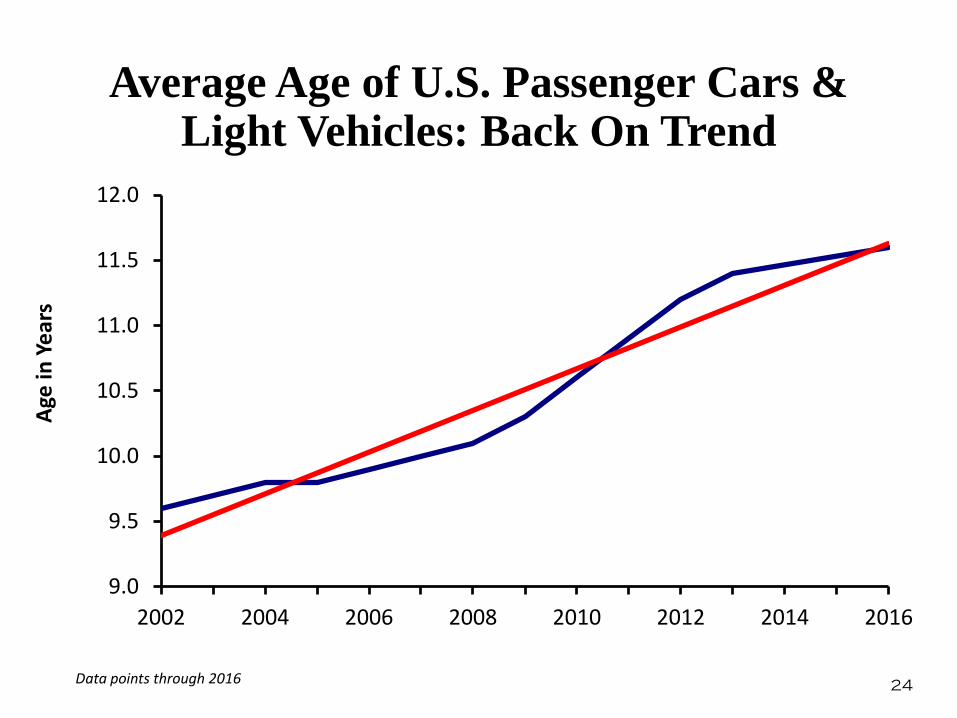

Average Age of U.S. Passenger Cars & Light Vehicles: Back On Trend

9.0

9.5

10.0

10.5

11.0

11.5

12.0

2002 2004 2006 2008 2010 2012 2014 2016

Age

in Y

ears

24Data points through 2016

-

5

10

15

20

25

30

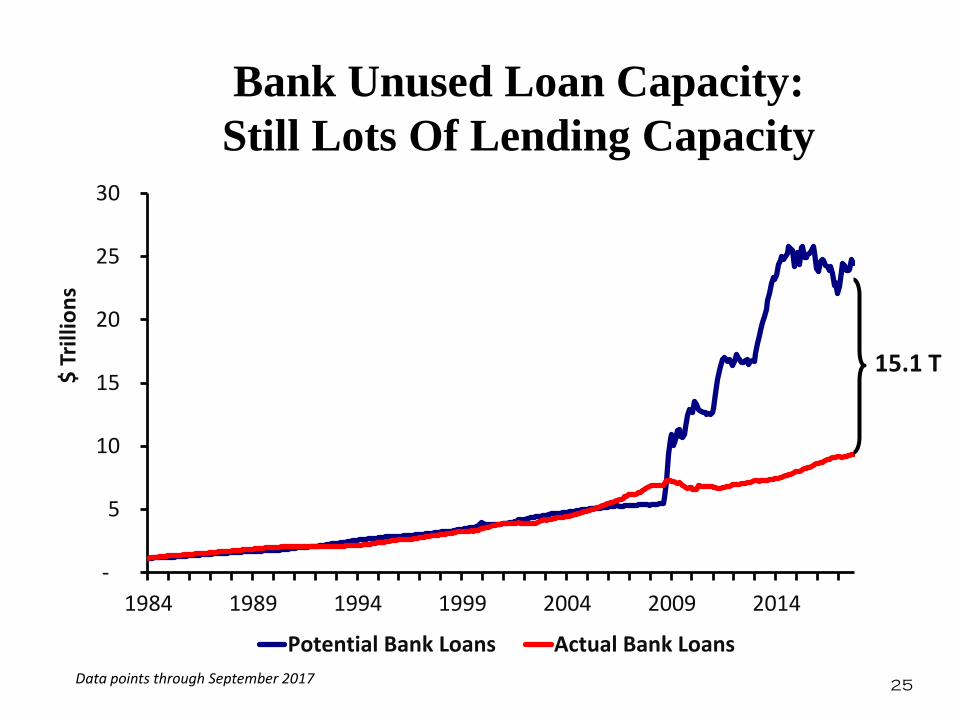

1984 1989 1994 1999 2004 2009 2014

$ Tr

illio

ns

Potential Bank Loans Actual Bank Loans

Bank Unused Loan Capacity: Still Lots Of Lending Capacity

25Data points through September 2017

15.1 T

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1947 1954 1962 1969 1977 1984 1992 1999 2007 2014

$ Tr

illio

ns

Commercial & Industrial Mortgages

Real Loans Held by Banks: Lending To Real Estate But Below Peak

26Data points through Q3 2017

0

25

50

75

100

125

150

1963 1968 1973 1978 1983 1988 1993 1998 2003 2008 2013

Mill

ions

of S

quar

e Fe

etCommercial & Industrial Construction

Contracts: Footage Amazingly Restrained

27Data points through Q2 2017

0

100

200

300

400

500

600

700

1 17 33 49 65 81 97 113 129 145 161

Basi

s Poi

nts

Multifamily

Easy Tight Easy Easy

Tigh

t

REIT Implied Cap Rate Spread over 10-Year Treasury: Not Crazy

28Data points through September 2017

0

300

600

900

1200

1500

1800

2100

2400

2700

1960 1966 1972 1978 1984 1990 1996 2002 2008 2014 2020

Empl

oym

ent (

thou

sand

s)

Actual Employment LL Forecast Long-Term Trend Linear Trend

Phoenix Employment

Data points through Q2 2017 29

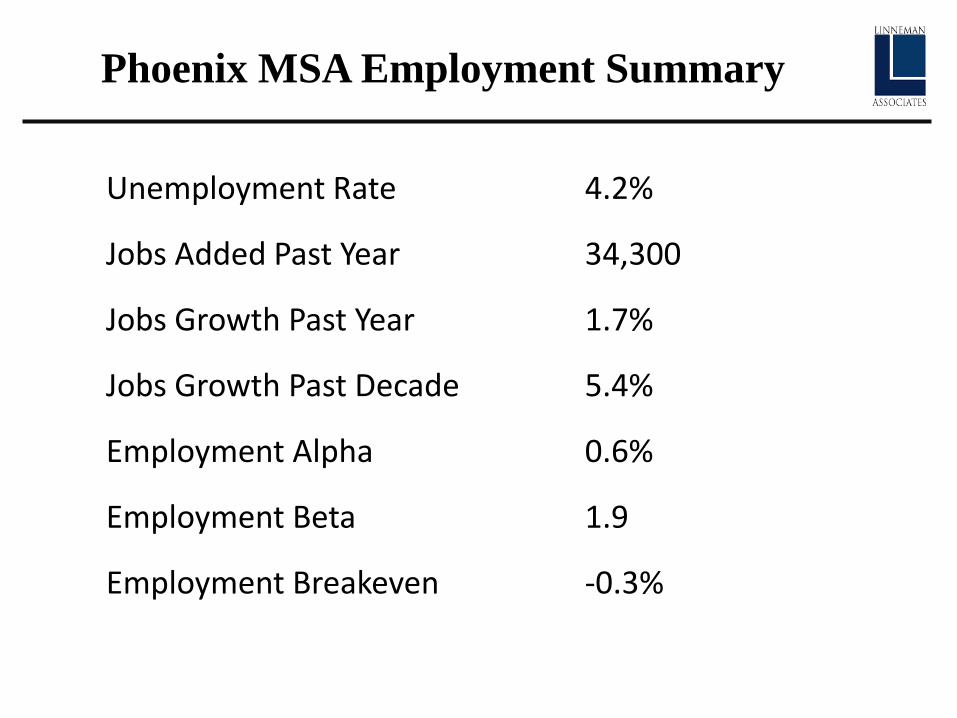

Phoenix MSA Employment Summary

Unemployment Rate 4.2%

Jobs Added Past Year 34,300

Jobs Growth Past Year 1.7%

Jobs Growth Past Decade 5.4%

Employment Alpha 0.6%

Employment Beta 1.9

Employment Breakeven -0.3%

For Now Lots Of Canaries Are Still Chirping

• PIK Debt

• Massive mortgage growth

• Spec development boom

• First replaces mezz

• Mezz replaces equity

• Narrow spreads and rising LTVs

• Record buyout deals

• Empty space worth more than full space