philippine manufacturing industry roadmap and global value chains rafaelita m. aldaba ateneo de...

TRANSCRIPT

PHILIPPINE MANUFACTURING INDUSTRY ROADMAP and

GLOBAL VALUE CHAINS Rafaelita M. Aldaba

Ateneo de Manila UniversityProfessional Schools, Rockwell, Makati City

November 12, 2014

1

Outline

Objective: implications of GVCs on the growth & development of PH manufacturing • Global Value Chains• Manufacturing Performance• Philippine Manufacturing Industry Roadmap• Services Vision and Strategy• Future Implications

2

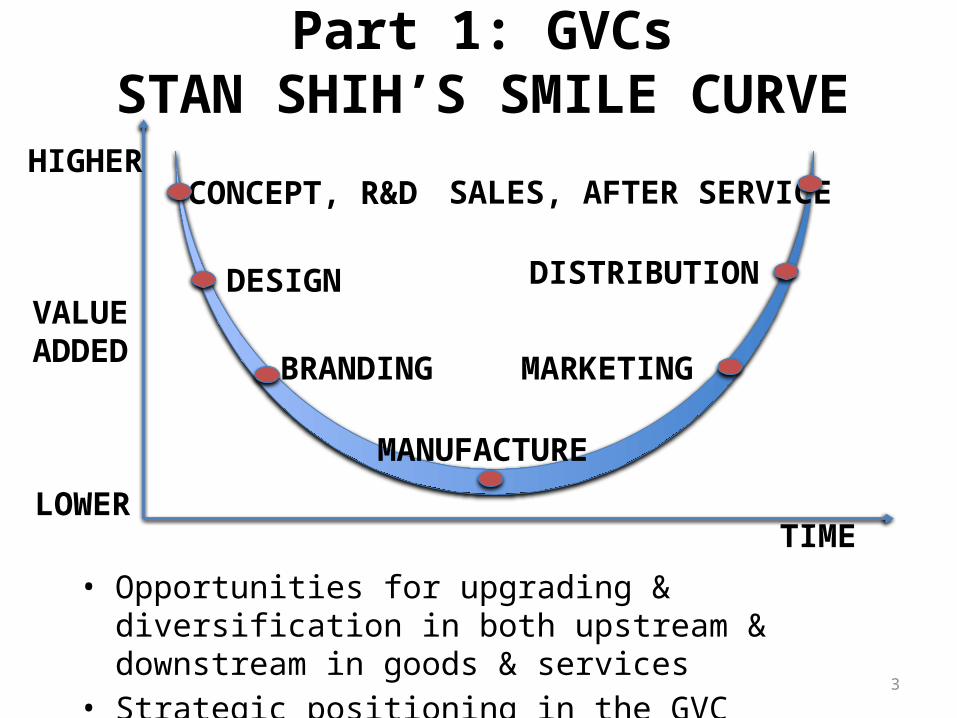

Part 1: GVCsSTAN SHIH’S SMILE CURVE

• Opportunities for upgrading & diversification in both upstream & downstream in goods & services

• Strategic positioning in the GVC

HIGHER

VALUE ADDED

LOWER

MANUFACTURE

MARKETINGBRANDING

DESIGN DISTRIBUTION

TIME

SALES, AFTER SERVICECONCEPT, R&D

3

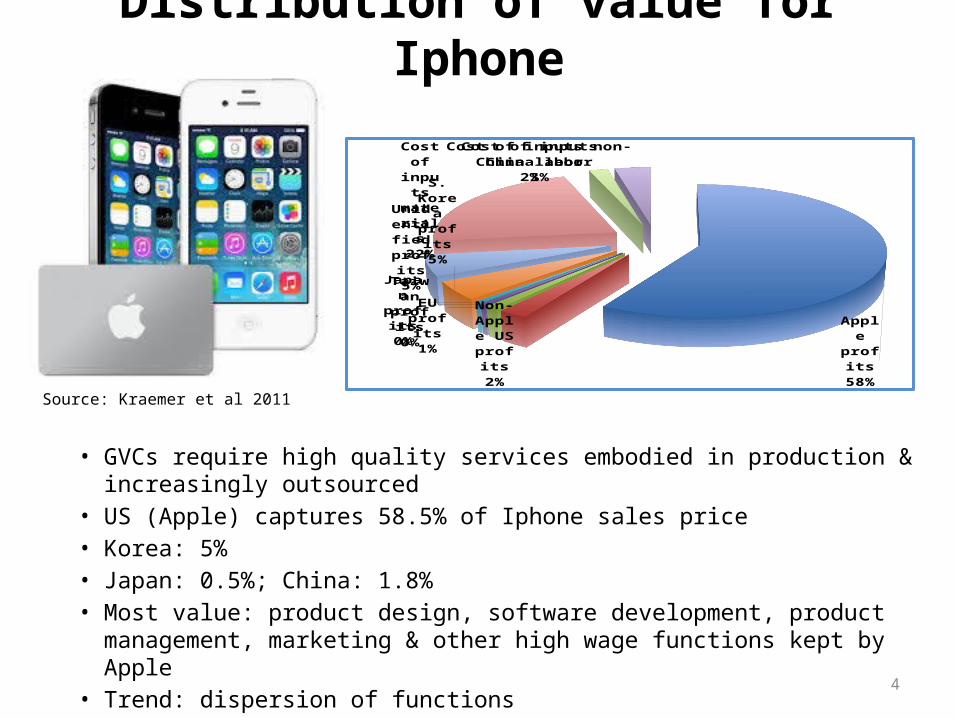

Distribution of value for Iphone

• GVCs require high quality services embodied in production & increasingly outsourced

• US (Apple) captures 58.5% of Iphone sales price• Korea: 5%• Japan: 0.5%; China: 1.8%• Most value: product design, software development, product management,

marketing & other high wage functions kept by Apple• Trend: dispersion of functions

Source: Kraemer et al 2011Apple profits

58%

Non-Apple

US profits

2%

EU profits

1%

Tai-wan

profits0%

Japan profits

0%

S. Ko-rea

profits5%

Unidentified profits

5%

Cost of in-puts ma-teri-als

22%

Cost of inputs China labor2%

Cost of inputs non-China labor

3%

4

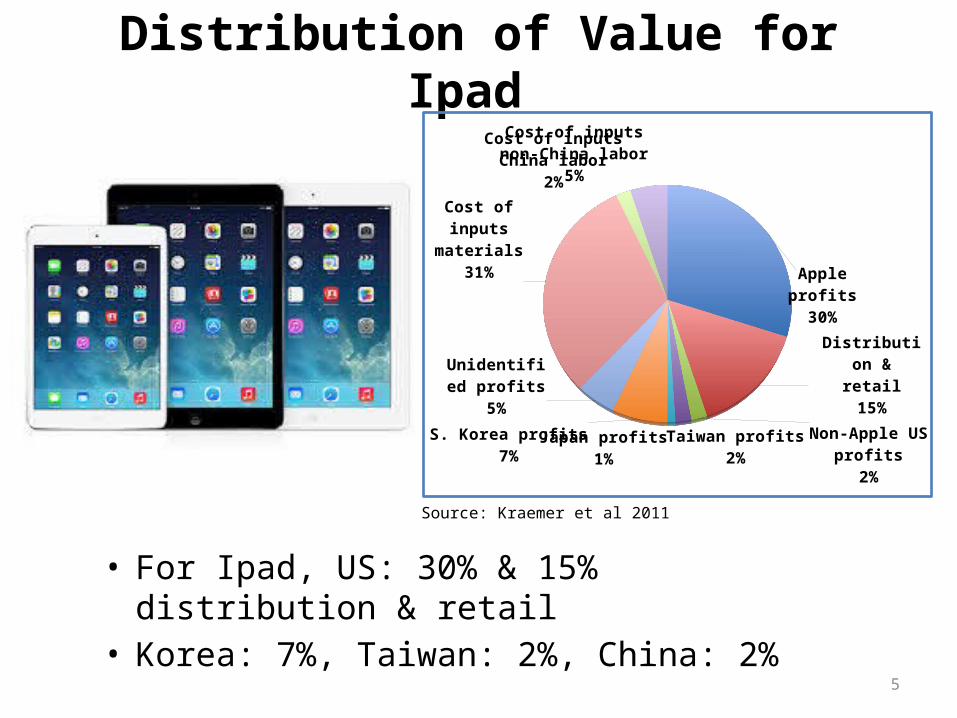

Distribution of Value for Ipad

• For Ipad, US: 30% & 15% distribution & retail• Korea: 7%, Taiwan: 2%, China: 2%

Source: Kraemer et al 2011

Apple profits30%

Distribution & retail

15%

Non-Apple US profits2%

Taiwan profits2%

Japan profits1%

S. Korea profits7%

Unidentified profits

5%

Cost of in-puts mate-

rials31%

Cost of inputs China labor

2%

Cost of inputs non-China labor

5%

5

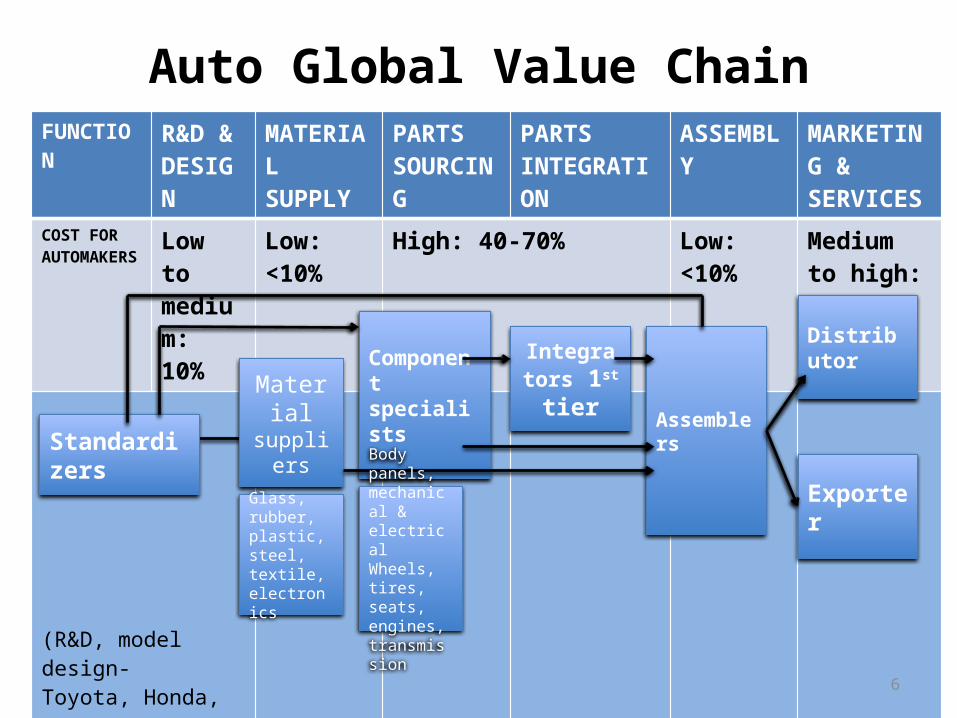

Auto Global Value ChainFUNCTION R&D &

DESIGNMATERIAL SUPPLY

PARTS SOURCING

PARTS INTEGRATION

ASSEMBLY MARKETING & SERVICES

COST FOR AUTOMAKERS

Low to medium: 10%

Low: <10% High: 40-70% Low: <10% Medium to high: 20%

(R&D, model design-Toyota, Honda, etc.)Standardizers

Material suppliers

Component specialists

Integrators 1st tier

Assemblers

Distributor

ExporterGlass, rubber, plastic, steel, textile, electronics

Body panels, mechanical & electrical Wheels, tires, seats,engines, transmission

6

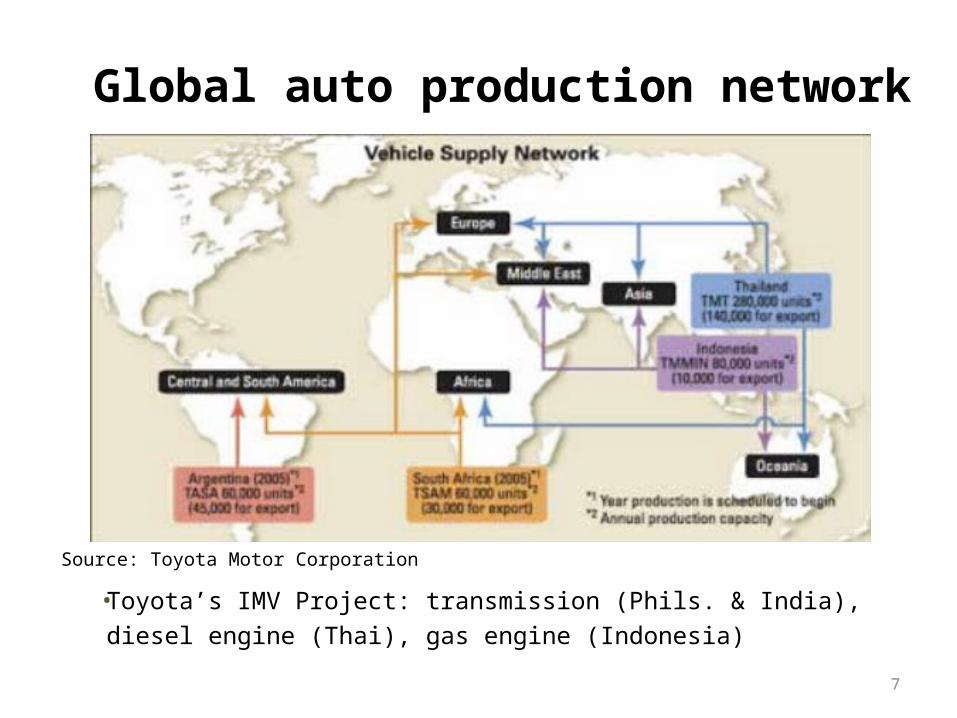

Global auto production network

• Toyota’s IMV Project: transmission (Phils. & India), diesel engine (Thai), gas engine (Indonesia)

Source: Toyota Motor Corporation

7

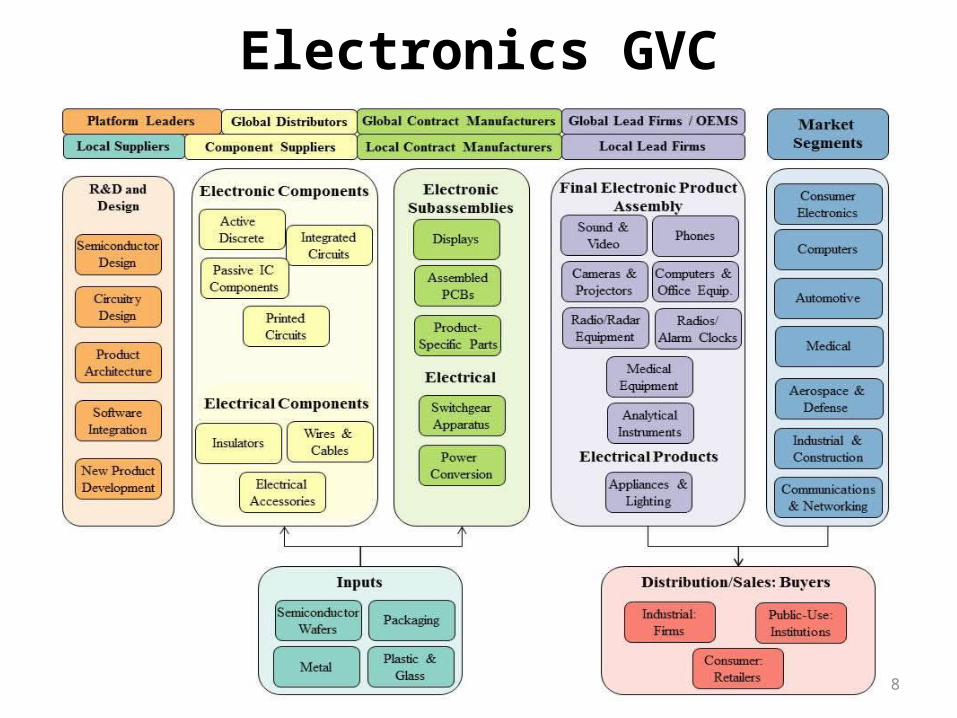

Electronics GVC

8

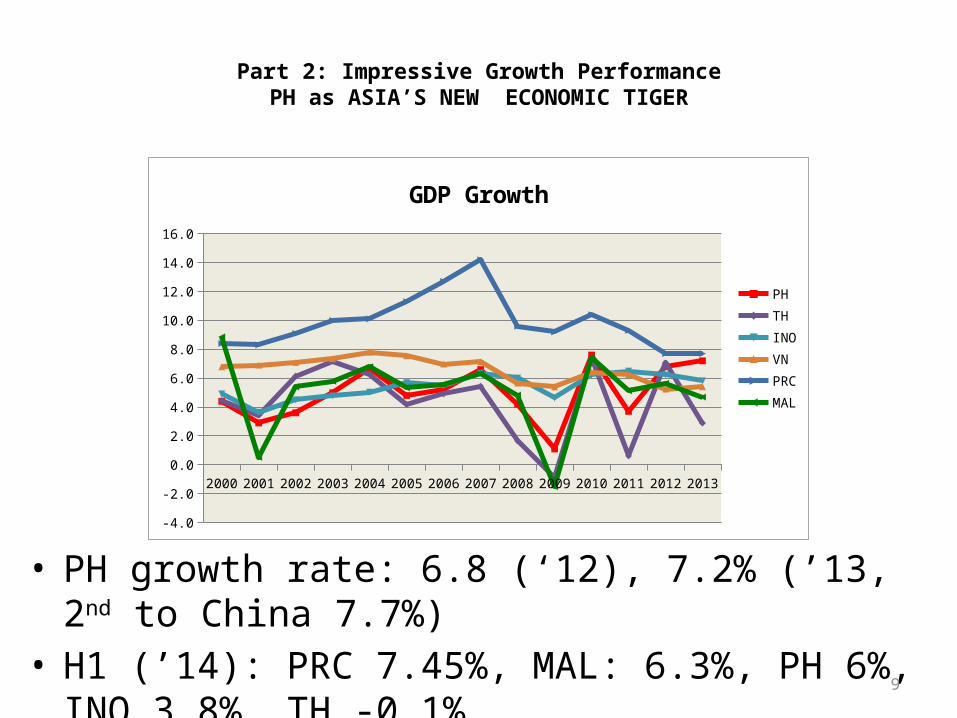

Part 2: Impressive Growth PerformancePH as ASIA’S NEW ECONOMIC TIGER

• PH growth rate: 6.8 (‘12), 7.2% (’13, 2nd to China 7.7%)• H1 (’14): PRC 7.45%, MAL: 6.3%, PH 6%, INO 3.8%, TH -

0.1%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

GDP Growth

PHTHINOVNPRCMAL

9

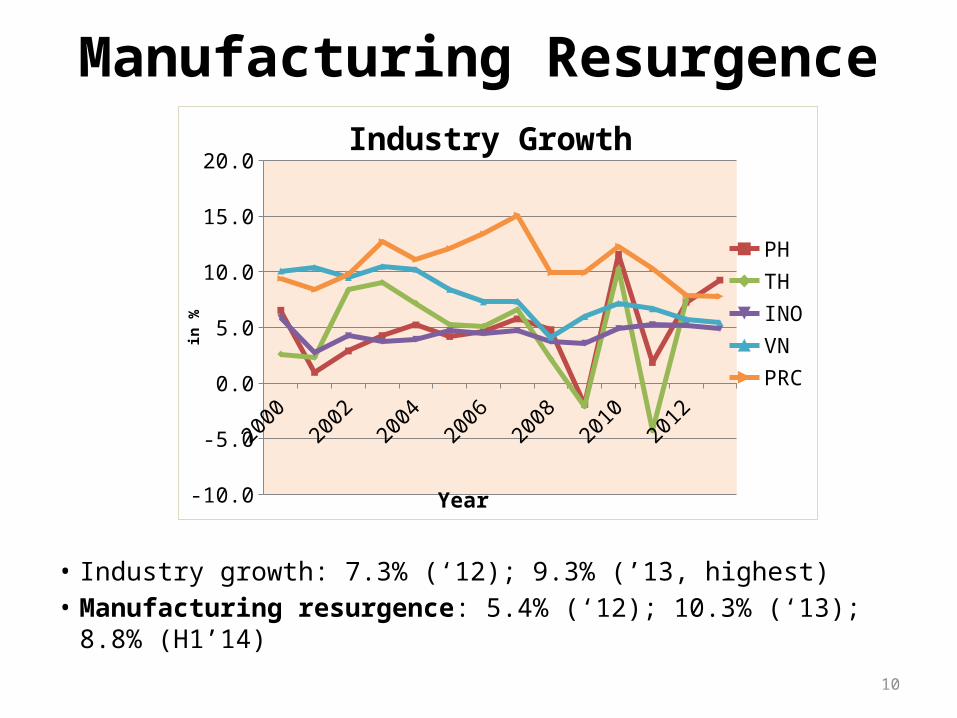

Manufacturing Resurgence

• Industry growth: 7.3% (‘12); 9.3% (’13, highest)• Manufacturing resurgence: 5.4% (‘12); 10.3% (‘13); 8.8%

(H1’14)

20002001

20022003

20042005

20062007

20082009

20102011

20122013

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0Industry Growth

PHTHINOVNPRC

Year

in %

10

WHAT MAKES PH DIFFERENTMarket Opportunities• Growing market & middle class: demographic sweet spot Labor• Young, English speaking, highly trainable workforce• Moderate wage increasesOperating Environment• Strong macroeconomic fundamentals• Political stability, business/consumer confidencePolicy Focus• New Industrial Policy & a more pro-active Government• Industry programs to support manufacturing resurgence• Philippine Economic Zone Authority, Board of Investments, Subic,

Clark: investment facilitation, investor careImproved competitiveness ranking (World Economic Forum)• Rank #52 in 2014-15 from rank #59 11

Part 3: Roadmap for Structural Transformation

Vision: globally competitive manufacturing

-Rebuild capacity existing industries, strengthen emerging industries, maintain competitiveness of comparative advantage industries

-Participate as hubs in regional & global production networks for auto, electronics, machinery, garments, food

-Shift to high value added activities,investments in upstream industries -Link & integrate industries-SMEs & large enterprises

Phase I 2014-2017

Phase II 2018-2021

Phase III 2022-2025

12

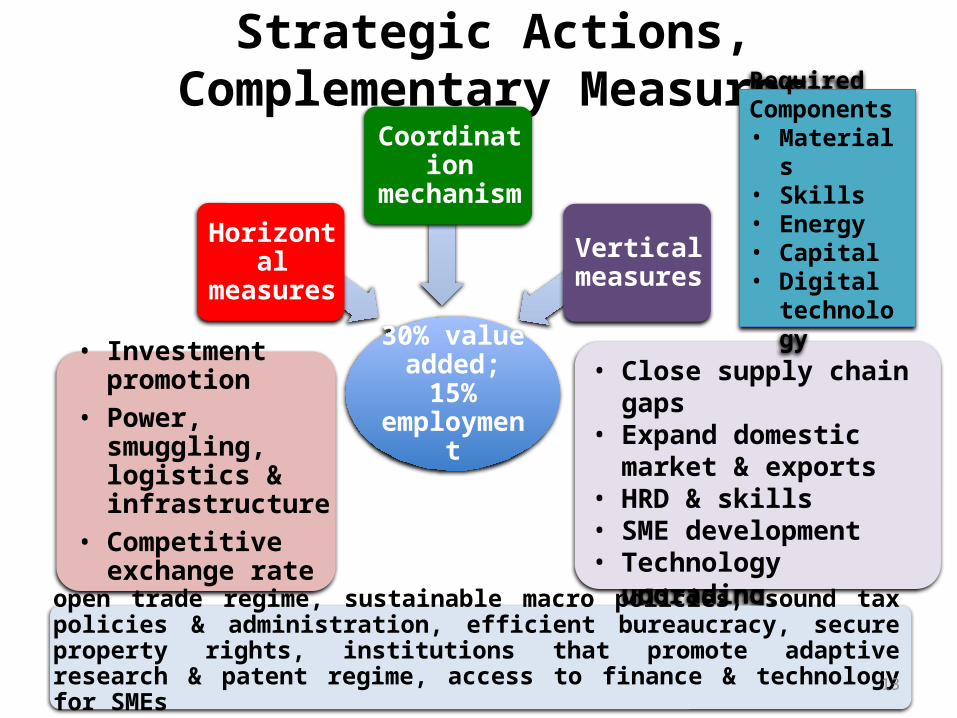

Strategic Actions, Complementary Measures

30% value added; 15% employment

Horizontal measures

Coordination mechanism

Vertical measures

• Close supply chain gaps• Expand domestic market &

exports• HRD & skills• SME development• Technology upgrading,

innovation, green growth

• Investment promotion

• Power, smuggling, logistics & infrastructure

• Competitive exchange rate

open trade regime, sustainable macro policies, sound tax policies & administration, efficient bureaucracy, secure property rights, institutions that promote adaptive research & patent regime, access to finance & technology for SMEs

Required Components• Materials• Skills• Energy• Capital• Digital

technology

13

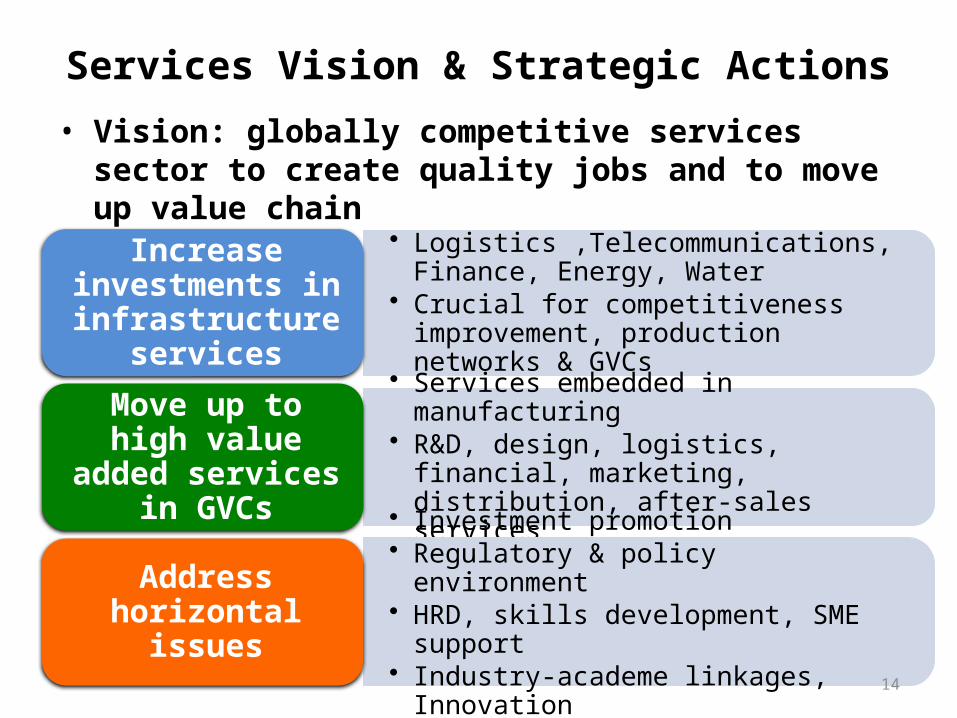

Services Vision & Strategic Actions• Vision: globally competitive services sector to create quality

jobs and to move up value chain

• Logistics ,Telecommunications, Finance, Energy, Water

• Crucial for competitiveness improvement, production networks & GVCs

Increase investments in infrastructure

services

• Services embedded in manufacturing• R&D, design, logistics, financial, marketing,

distribution, after-sales services

Move up to high value added services

in GVCs

• Investment promotion• Regulatory & policy environment• HRD, skills development, SME support • Industry-academe linkages, Innovation

Address horizontal issues

14

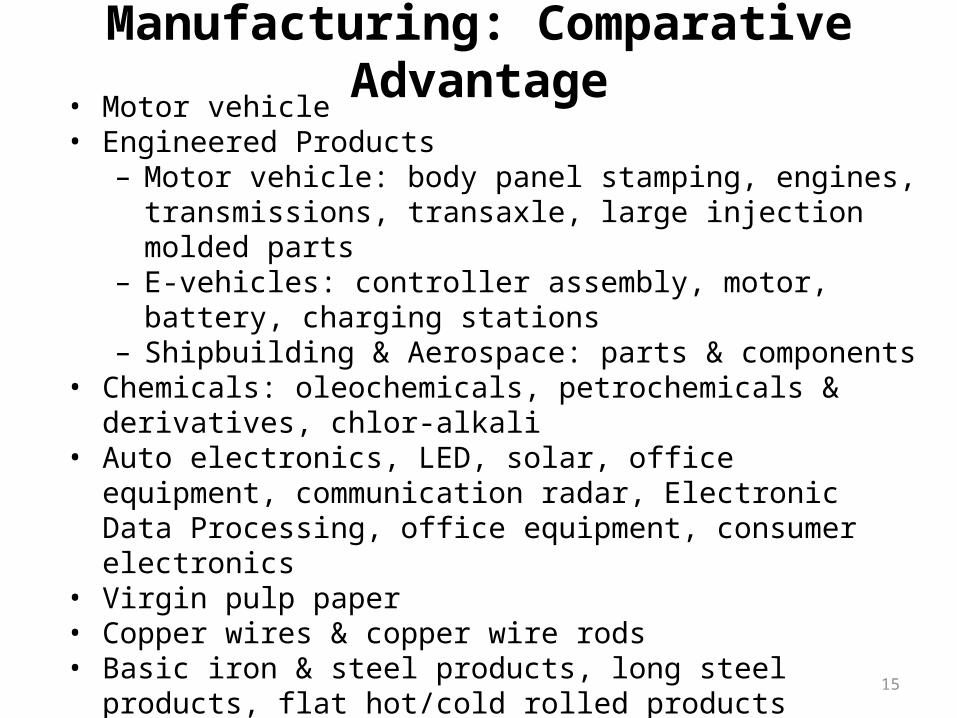

Manufacturing: Comparative Advantage• Motor vehicle• Engineered Products

– Motor vehicle: body panel stamping, engines, transmissions, transaxle, large injection molded parts

– E-vehicles: controller assembly, motor, battery, charging stations– Shipbuilding & Aerospace: parts & components

• Chemicals: oleochemicals, petrochemicals & derivatives, chlor-alkali • Auto electronics, LED, solar, office equipment, communication radar,

Electronic Data Processing, office equipment, consumer electronics• Virgin pulp paper• Copper wires & copper wire rods• Basic iron & steel products, long steel products, flat hot/cold rolled

products• Tool & die: simple, compound, & progressive dies for metal stamping

& forging; molds for die casting, plastic injection or blow molding; jigs & fixtures for metal cutting & forging

• Food Processing/Manufacturing15

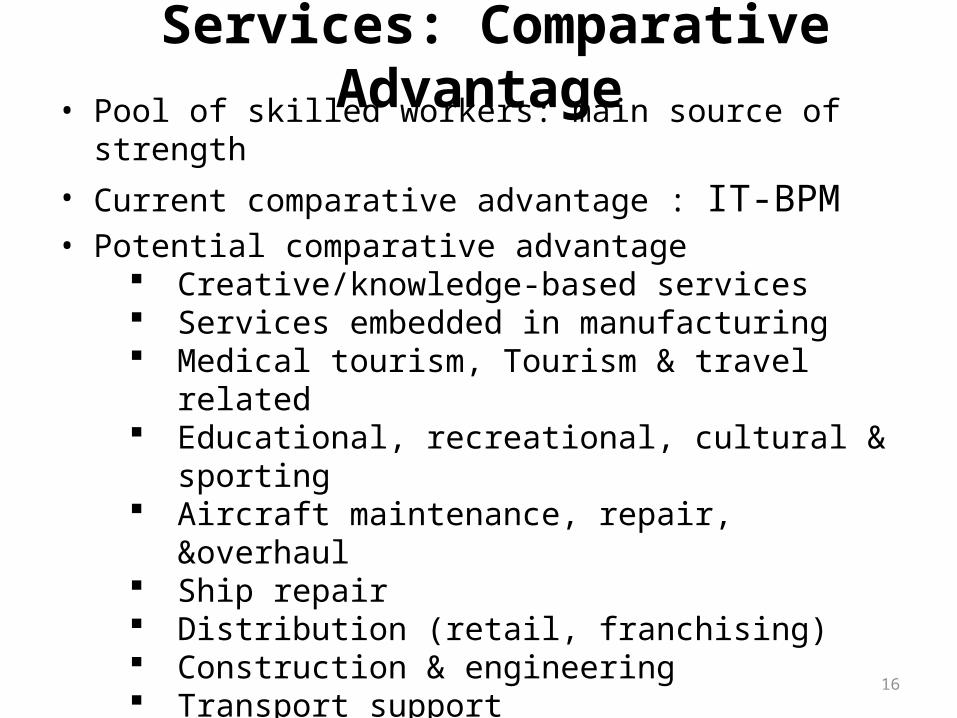

Services: Comparative Advantage • Pool of skilled workers: main source of strength• Current comparative advantage : IT-BPM• Potential comparative advantage

Creative/knowledge-based services Services embedded in manufacturing Medical tourism, Tourism & travel related Educational, recreational, cultural & sporting Aircraft maintenance, repair, &overhaul Ship repair Distribution (retail, franchising) Construction & engineering Transport support

Energy, Public infrastructure & logistics, Public Private Partnership projects

16

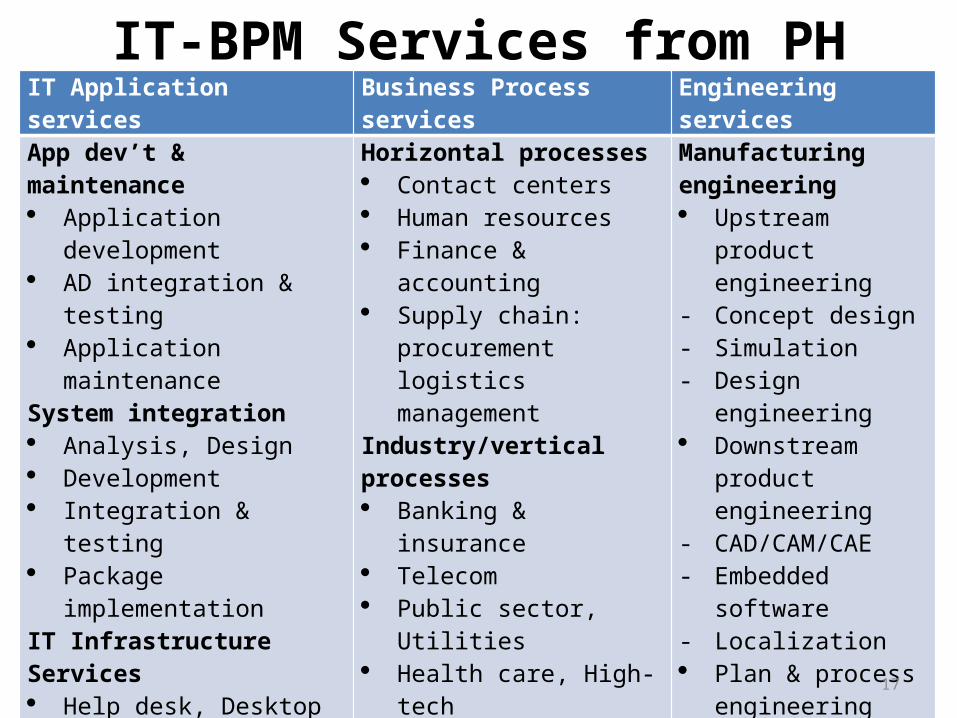

IT-BPM Services from PHIT Application services Business Process services Engineering services

App dev’t & maintenance Application development AD integration & testing Application maintenanceSystem integration Analysis, Design Development Integration & testing Package implementationIT Infrastructure Services Help desk, Desktop support Data centre services Mainframe Network operations IT consultingSoftware product development New product development System testing Localization/Support Gaming

Horizontal processes Contact centers Human resources Finance & accounting Supply chain: procurement

logistics managementIndustry/vertical processes Banking & insurance Telecom Public sector, Utilities Health care, High-tech Oil & Gas, Consumer prodsKnowledge Process Outsourcing Business research, financial

research Animation Data analytics Legal process & patent

research Other high-end processes

Manufacturing engineering Upstream product

engineering- Concept design- Simulation- Design engineering Downstream product

engineering- CAD/CAM/CAE- Embedded software- Localization Plan & process

engineeringArchitecture design Design process Building

Management models

17

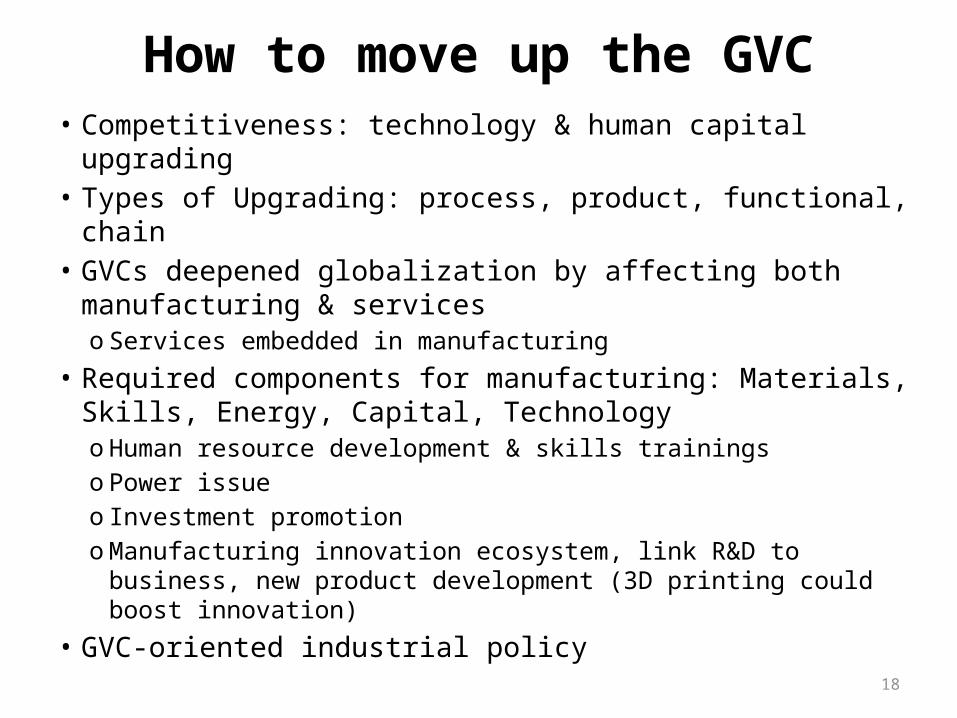

How to move up the GVC• Competitiveness: technology & human capital upgrading• Types of Upgrading: process, product, functional, chain• GVCs deepened globalization by affecting both

manufacturing & serviceso Services embedded in manufacturing

• Required components for manufacturing: Materials, Skills, Energy, Capital, Technologyo Human resource development & skills trainingso Power issueo Investment promotion o Manufacturing innovation ecosystem, link R&D to business, new

product development (3D printing could boost innovation)• GVC-oriented industrial policy

18

With or without AEC, we need to pursue a new industrial policy to make our industries

competitive and create an environment conducive to private sector development.

This could lead to more investments, increased competition, more innovation,

increased productivity, sustainable & inclusive growth, & more & better jobs!

THANK YOU!

19