philippine country report - asia securities forum · · 2014-12-162011-01-17 · slide 2 outline:...

TRANSCRIPT

Slide 1

Philippine Country Report

Ismael G. CruzPresident

Philippine Association of Securities Brokers and Dealers, Inc

Slide 2

Outline: Philippine Country Report

Ä The Philippine Economy

§ Growth despite global recession In 2009

§ Strong growth in 1Q10

§ Benign inflation and supportive monetary environment

§ Surge in BoP Surplus, large current account surplus narrower traded deficit and record GIR

§ Manageable fiscal situation and reduced burden

§ Special deposit accounts

§ Strengthening of the peso

§ Overall assessment

§ 2010 and 2011 forecasts

Ä The Philippine Stock Market

§ Robust market performance and above-average volume turnover

§ More capital raised

§ Strong first-quarter earnings growth

§ Attractive P/E valuation

§ Key developments

• New trading system

• ASEAN exchange hub

Ä The Philippine Fixed Income Exchange

§ Integrated and diversified products and services

§ Diverse ownership and clear mandate

§ Building market infrastructure

§ High trading-volume growth

§ Wave of corporate bond issuances

Ä Capital Market Trends and Regulatory Policy

§ New products

• PERA, Derivatives, ETFs, REITs

§ Regulatory policy:

• DST, MRD Spin-off

§ New legislation

• FRIA, CISA, CISL, FinTax

Slide 3

The Philippine Economy

Slide 4

The Philippine Economy: Growth Despite Global Recession

Ä Growth despite global recession

§ In the face of global recession, the economy grew by 0.9% in 2009, compared with average growth of 5.5% over the previous 5 years (2004-2008)

§ GDP maintained slight growth throughout 2009, picking up in the fourth quarter, as industrial output rebounded from a slump

§ GNP, which included remittances from nearly 9m OFWs, rose by 3.0%

Ä Private and public consumption spending offset weakness in investment and trade

§ Private consumption grew 3.8%, buoyed by OFW remittances and remained the biggest contributor to GDP on the demand side

§ Significantly higher government consumption spending (up by 8.5%) and a fiscal stimulus package helped support aggregate demand

§ On the supply side, services, which accounted for 50% of GDP in 2009, expanded by 3.2% and was the only production sector to contribute to GDP growth

Annual GDP %

Quarterly GDP % (Y-Y)

Slide 5

The Philippine Economy: Resilience And Gradual Growth

5.5% 5.8%5.3%

8.7%

5.1%

6.3% 6.2%7.1%

8.2%

4.9%

6.0%

4.6%3.8%

1.4%

2.5%

4.5%

-1.7%

1.1%

-2.0% -2.3%

5.5% 5.3%

3.8%

6.3%

4.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Indonesia Malaysia Philippines Singapore Thailand

2006 2007 2008 2009 2010F

Slide 6

4.5%

5.1%4.7%

5.4%5.7% 5.5%

5.1%5.5%

7.1%7.5%

6.6%

7.4%

3.8% 3.7%

4.6%

2.8%

0.5%

1.2%

0.2%

2.1%

7.3%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10

The Philippine Economy: 1Q10 GDP Grew At The Fastest Pace Since 4Q07

5-year average

5-year (2005-2009)quarterly average: 4.5%

Quarterly GDP Growth (Y-Y)

Slide 7

The Philippine Economy:Surge In Investments, Trade, And Industry; Improvement In All Components, Except Agriculture

4Q09 1Q10

Q-Q Y-Y % of Total Q-Q Y-Y % of

Total

Private consumption +18.2% +5.0% 82.3% -15.4% +5.9% 77.2%

Investments +9.2% +5.8% 15.6% +19.5% +24.2% 20.6%

Government spending -8.9% +13.7% 5.8% +22.8% +18.5% 7.9%

Exports -26.1% -6.7% 31.8% +15.5% +17.9% 40.7%

Imports +7.1% +6.8% 44.8% -14.9% +20.3% 42.3%

4Q09 1Q10

Q-Q Y-Y % of Total Q-Q Y-Y % of

Total

Agriculture +28.9% -2.6% 19.1% -15.5% -2.5% 17.9%

Industry +12.3% +0.4% 31.4% -6.2% +15.4% 32.6%

Services +11.5% +4.3% 49.0% -9.1% +5.9% 49.4%

Quarterly Growth Of Demand And Supply Side Components (Q-Q, Y-Y)

Slide 8

The Philippine Economy: Benign Inflation And Supportive Monetary Environment

Ä Inflation has risen but remains low

§ Inflation averaged 3.2% in 2009 pulled down by lower international prices for oil and commodities, coupled with soft domestic demand

§ Consumer prices picked up to 4.4% in December, on the back of rising prices oil and food

Ä Interest rates have been kept at low levels to support growth

§ As the economy sagged and inflation waned, BSP lowered interest rates by 200 bp from December 2008 and July 2009, taking the overnight borrowing rate to 4.0%

§ BSP also supported banking system liquidity and depositor confidence by reducing commercial bank reserve requirements and increasing the ceiling on deposit insurance

Monthly Inflation (Y-Y)

Inflation (Y-Y) And Interest Rates

Slide 9

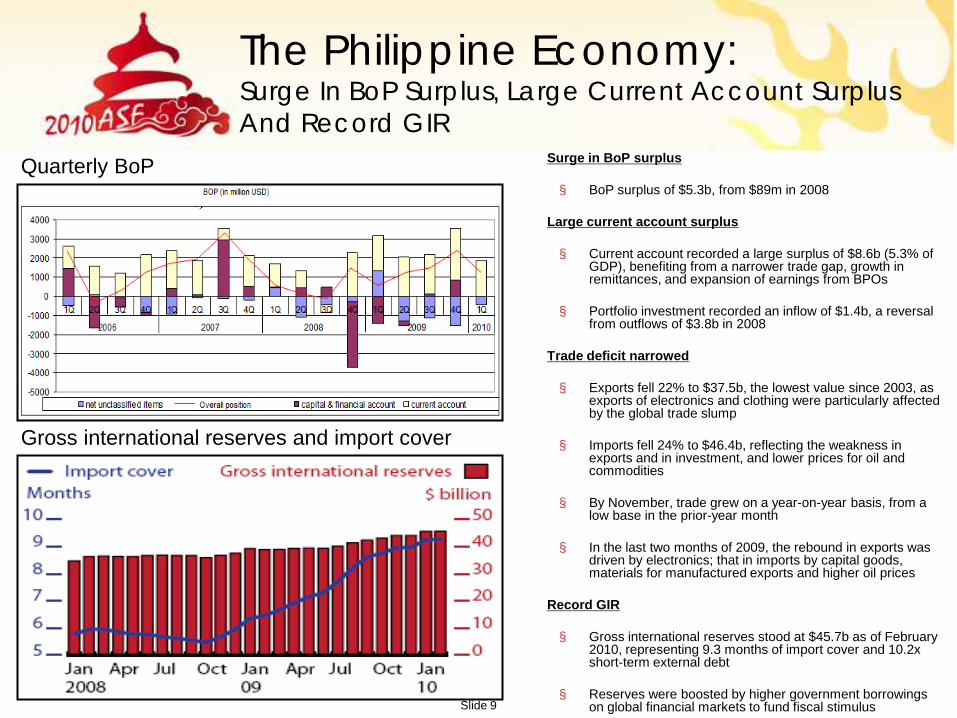

The Philippine Economy: Surge In BoP Surplus, Large Current Account Surplus And Record GIR

Ä Surge in BoP surplus

§ BoP surplus of $5.3b, from $89m in 2008

Ä Large current account surplus

§ Current account recorded a large surplus of $8.6b (5.3% of GDP), benefiting from a narrower trade gap, growth in remittances, and expansion of earnings from BPOs

§ Portfolio investment recorded an inflow of $1.4b, a reversal from outflows of $3.8b in 2008

Ä Trade deficit narrowed

§ Exports fell 22% to $37.5b, the lowest value since 2003, as exports of electronics and clothing were particularly affected by the global trade slump

§ Imports fell 24% to $46.4b, reflecting the weakness in exports and in investment, and lower prices for oil and commodities

§ By November, trade grew on a year-on-year basis, from a low base in the prior-year month

§ In the last two months of 2009, the rebound in exports was driven by electronics; that in imports by capital goods, materials for manufactured exports and higher oil prices

Ä Record GIR

§ Gross international reserves stood at $45.7b as of February 2010, representing 9.3 months of import cover and 10.2x short-term external debt

§ Reserves were boosted by higher government borrowings on global financial markets to fund fiscal stimulus

Quarterly BoP

Gross international reserves and import cover

Slide 10

The Philippine Economy: Manageable Fiscal Balance And Reduced Debt Burden

Ä Stimulative fiscal policy

§ The fiscal deficit widened to 3.9% of GDP, from 0.9% of GDP in 2008

§ Stimulus focused on extra spending for infrastructure and for social protection measures

§ Government expenditure, other than for interest payments on large public debt, rose to 14.9% of GDP from 13.5% in 2008

Ä Stable sovereign outlook

§ In July 2009, Moody’s upgraded the country’s credit rating from B1 to Ba3 with stable outlook- after 4 years at B1, citing resilience of the financial system and of the external payments position during the global recession

Ä NG debt of P4,443b (57.3% of GDP) at end 2009 from 77.3% in 2003

Budget deficit

National Government Debt

Slide 11

The Philippine Economy:SDAs Are Attracting Liquid Capital

Special Deposit Accounts (in Php bn)

585

834

-100200300400500600700800900

1H09 1H10

+43%

Slide 12

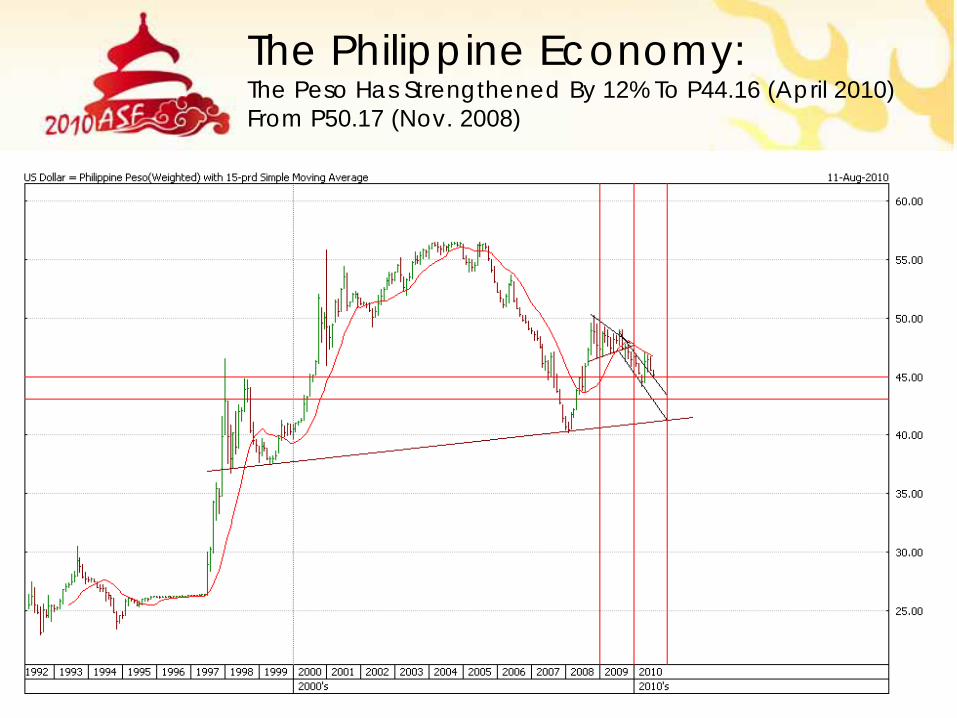

The Philippine Economy: The Peso Has Strengthened By 12% To P44.16 (April 2010) From P50.17 (Nov. 2008)

Slide 13

The Philippine Economy: Underpinned By Strong Economic Fundamentals

Positive FactorsÄ The Philippines avoided recession in 2009 with growth of 1.1%

Ä 1Q10 GDP grew 7.3%, the fastest pace since 4Q07, and full-year is forecasted to grow 5% to 6%

Ä Inflation rate slowed to 3.9% in June, from 4.3% the previous month, the lowest in seven months

Ä Interest rates are at a record low of 4% and 6% for borrowing and lending, respectively

Ä OFW remittances in the 5M10 rose 7% to $7.4b, and forecasted to grow 8% this year

Ä Balance of payments surplus grew 46% to $3.2b in 1H10, driven by strong OFW remittance and forex inflows

Ä Exports rose 39% to $19.2b in 5M10, better than full-year forecast of +15%

Ä FDI in 1Q10 rose 19% to $319M, better than full-year forecast of -8%

ÄPeso has appreciated as much 6% this year against the US dollar, and YTD appreciation of +3%

ÄSuccessful automated elections and new leadership

Negative Factors

Ä Trade deficit grew 16% y-y in 5M10 to $2.9b, due to a sharper rise in imports

ÄBudget deficit was revised upwards to P325b or 3.6% of GDP, from P300b or 3.5%

Ä External debt is at 57.3% Debt-to-GDP ratio in 2009, among the highest in the region. (Regional average: 37.8% Debt-to-GDP ratio)

Slide 14

The Philippine Economy:2009 and 2010 Forecasts

Economic Indicator 2010F 2011F

GDP +5% to +6% +7% to +8%

Inflation rate 3.5% to 5.5% 3.0% to 5.0%

Gross international reserves $49b to $50b -

OFW remittances +8% to $18.8b -

FDI -8% to $1.8b -

Balance of Payments -30% to $3.7b surplus -

Budget deficit P325b or 3.6% of GDP P285b or 3.3% of GDP

Exports +15% to $43.1b +13% to $48.7b

Imports +20% to $55.7b+16% to +18%

($64.6b to $65.7b)

*Source: Various Philippine government agencies

Slide 15

The Philippine Stock Market

Slide 16

PSEi Growth (in %)

42%

26%

15%

42%

21%

-48%

63%

15%

-60%

-40%

-20%

0%

20%

40%

60%

80%

2003 2004 2005 2006 2007 2008 2009 YTD

The Philippine Stock Market: Robust Stock Market Performance And Above-Average Volume Turnover

Average Daily Turnover (in Php bn)

0.590.84

1.56

2.32

5.48

3.11

4.11

3.2

0

1

2

3

4

5

6

2003 2004 2005 2006 2007 2008 2009 YTD

7-year average

P2.6b

1

2

3

7th annual rise in the past 8 years

Slide 17

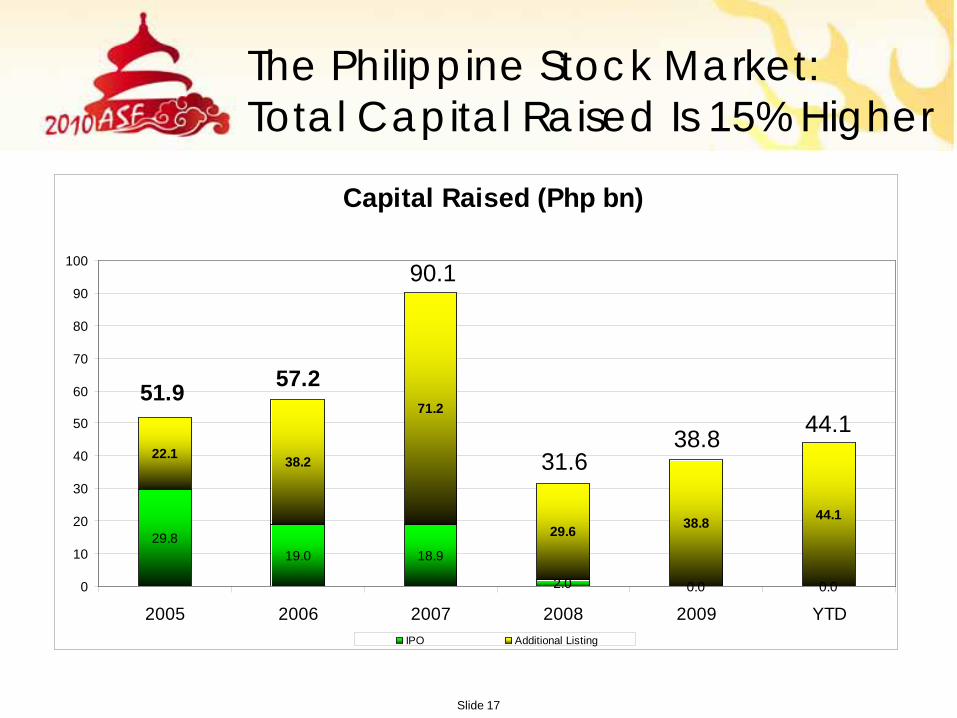

The Philippine Stock Market: Total Capital Raised Is 15% Higher

Capital Raised (Php bn)

29.819.0 18.9

2.0 0.0 0.0

22.1 38.2

71.2

29.6 38.8 44.1

0

10

20

30

40

50

60

70

80

90

100

2005 2006 2007 2008 2009 YTDIPO Additional Listing

51.9 57.2

90.1

31.638.8 44.1

Slide 18

-59% -54% -58% -61% -60% -55%

67% 65% 68% 68% 71%

102%

-2%

2% 1% 2% 1%15%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%MSCI World Dow S&P 500 Euro Stoxx MSCI Asia PSEi

October 2007 High to March 2009 Low March 2009 Low to Recent High YTD%

The Philippine Stock Market: Bull Market Continues

BULL

BEAR

As of August 10, 2010

Slide 19

The Philippine Stock Market: Global Markets Have Bounced-Off From Their Recent Lows PSEi: Weaker Correction And Stronger Recovery

Max.

Current

-17.4%

-13.3%-15.3%

-18.0%-14.9% -16.0% -16.0%

-19.7%

-14.7%

-8.1%-7.4%-5.1%

-7.6%-5.8%

-3.9%-7.3% -6.7% -5.4%

-17.6%

-13.7%

-3.1%

13.8%

-25.1% -26%-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

World Dow

S&P500

Euro Zone

Euro Stoxx

600 UK

MSCI Asia

Ex-Japa

n

Shangha

i

Shenze

n HK

Philippines

*as of August 5

Recent Correction and Recovery (April to July, July to date)

Slide 20

The Philippine Stock Market: PSEi First-Quarter Earnings Growth Of 56% Exceeded Market Expectations And Full-Year Forecast Of 17%

IndustryNumber of stocks

% index weightProfit growth

Reported Recurring

Telcos 2 23.7% 6% -7%

Banks 7 16.8% 25% 25%

Conglomerates 7 19.7% 314% 128%

Utilities 6 13.7% 221% 267%

Properties 6 13.3% 15% 14%

Consumer 5 3.9% 164% 72%

Media 2 1.8% 181% 120%

Resources 2 1.8% 50% 50%

Aggregate 37 94.6% 100% 56%

Aggregate ex-power 31 77.6% 26% 20%

Source: Philippine Equity Partners

2003 2004 2005 2006 2007 2008 2009 2010F

PSEiEarnings Growth (%)

30.8 14.7 16.7 14.8 Flat 4.0 17.0

Slide 21

The Philippine Stock Market:Attractive Valuation Of PSEi Relative To Global Peers And 2003, The First Year Of Recovery

31

18

25

39

65

37

28

40

62

15

25

1614

17

2723

13

22

17

30

52

1612

62

0

10

20

30

40

50

60

70

World DowS&P

Euro zone

Euro 600 UK

Asia

Ex Japan

Shanghai

Shenzen

Hong Kong

Philippines

2003 2010

Slide 22

The Philippine Stock Market:PSEi Trading At 12x P/E, Still Among The Lowest In Asia

Global Market PEs

15 14

18

23

14 1412

11 10

21

26

17 1615 15 14 14

1211 10

0

5

10

15

20

25

30

Wor

ld

Dow

S&P

Euro

Sto

xx

Fran

ce

Italy

Germ

any

UK

Spai

n

MSC

I Asi

a

Japa

n

Indi

a

Indo

nesi

a

Taiw

an

Mal

aysi

a

Sing

apor

e

Hong

Kon

g

Phili

ppin

es

Sout

h Ko

rea

Thai

land

WorldUSEuropeAsia

Slide 23

2750

1685

The Philippine Stock MarketThe PSEi May Challenge 3800 By End 2010

3800

3300

2003: +42%

2004: +26%

2005: +15%

2006: +42%

2007: +21%

2008: -48%

2009: +63%

YTD: +15%

3500

Slide 24

The Philippine Stock Market: Key Developments: New Trading System And ASEAN Exchange Hub

Initiative Update

PSE New Trading System

The NSC Trading System Core Products, developed by NYSE Euronext, is equipped to trade a wide range of cash, debt and derivatives instrumentsIt replaced the Maktrade system which was in use since 1993

Launched on July 26, 2010

ASEAN Exchange Hub

The ASEAN stock exchanges formally entered into an MOU in February 2009 to proceed with the discussions in developing an ASEAN trade linkage and in establishing an ASEAN Board

The Agreement was entered into by Bursa Malaysia, Indonesia Stock Exchange, PSE and Singapore Exchange The Stock Exchange of Thailand, and later in September 2009, the Ho Chi Minh Stock Exchange

The e-trading link, through one single access point, will allow intra-ASEAN cross-border trading and will attract more international funds into the ASEAN.

Expected to go online in 2010

PSE- Shenzhen Stock Exchange, Ho Chi Minh Stock Exchange and The Korea Stock Exchange Memorandum of Understanding

To explore mutual cooperation through information and experience sharing.

Signed on April 23, 2009

Slide 25

The Philippine Fixed Income Exchange

Slide 26

Phil. Dealing System Holdings Corp. (PDS)

TradingRegistry, Depository

and CustodyClearing and

Settlement Infrastructure

• Nomineeship & Trusteeship• Guardianship• Agency Function• Value Management• Centralized Collateral

Management

• National Payment Highway

• Information Highway• Multi-currency Facilities

• Price Transparencyand Discovery

• Trade execution• SRO

The Philippine Fixed Income ExchangeIntegrated And Diversified Products And Services

Designed to seamlessly link market activities from trading, clearing & settlement up to post-settlement disposition

Slide 27

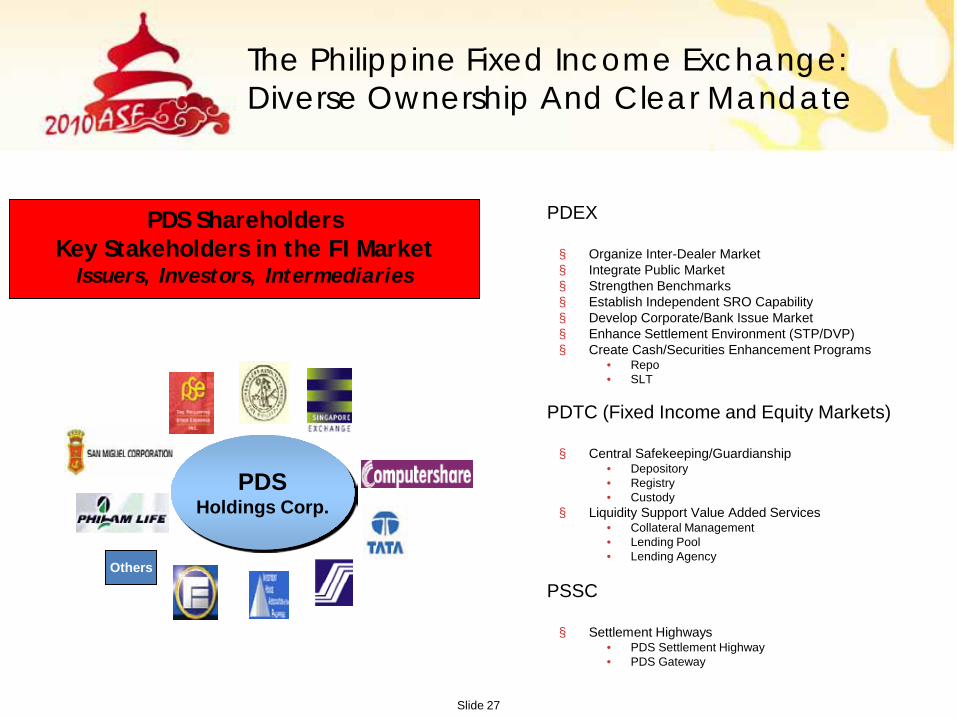

PDS Shareholders Key Stakeholders in the FI Market

Issuers, Investors, Intermediaries

Computershare

PDSHoldings Corp.

Banks

Investment Houses

PSE

SSSFINEX

Philam

SMC

Tata Consultancy

SGX

Others

The Philippine Fixed Income Exchange:Diverse Ownership And Clear Mandate

Ä PDEX

§ Organize Inter-Dealer Market§ Integrate Public Market§ Strengthen Benchmarks§ Establish Independent SRO Capability§ Develop Corporate/Bank Issue Market§ Enhance Settlement Environment (STP/DVP)§ Create Cash/Securities Enhancement Programs

• Repo• SLT

Ä PDTC (Fixed Income and Equity Markets)

§ Central Safekeeping/Guardianship• Depository• Registry• Custody

§ Liquidity Support Value Added Services• Collateral Management• Lending Pool• Lending Agency

Ä PSSC

§ Settlement Highways• PDS Settlement Highway• PDS Gateway

Slide 28

May 2010

Operation of US$

delivery versus

payment

August 2008Entry of

Cash Liquidity Facilities

through the Inter-

Professional Repo

Program

August 2008

Entry of private

debt issuers to the issuer

community

May 2010

Listing of US$ Gov’t Securities

June 2009

Launch of Fixed

Income Broker

Internet Order System

enabling real time

nationwide access to

the market

The Philippine Fixed Income Exchange:Building Market Infrastructure

Slide 29

The Philippine Fixed Income Exchange:High Growth Of Trading Volume

437.74787.40

1,564.04 1,567.95 1,769.211,296.69

160.55

58.41

367.39

651.85

382.65

100.00%

100.00%

100.00% 81% 69%75%

6%

3%

19%

25%

22%

0

500

1,000

1,500

2,000

2,500

3,000

2005 2006 2007 2008 2009 Year-to-June

Dealer Qualified Investor Broker

Volume 437.74 787.40 1,564.04 1,935.34 2,581.61 1,737.75

Growth 79.88% 98.63% 23.74% 33.39%

Ave. Daily Vol. 2.32 3.24 6.41 7.87 10.62 14.36

Turnover 0.4x 0.8x 1.3x 1.4x 1.7x 1.02x

Slide 30

0

20

40

60

80

100

120

140

160

180

June 2009 June 2010

AC

ALI

EDC

FLI

GLO

JGS

MBT

MEG

MWC

PSALM

RCB

RLC

SMB

The Philippine Fixed Income Exchange:Wave Of Corporate Bond IssuancesTotal Market Value Of Listed Corporate Securities Grew 362%

37.5 B

173.3 B June 2010 (PhpBn)

Share (%)

AC 16.0 9.2

ALI 4.0 2.3

MWC 4.0 2.3

MBT 18.5 10.7

GLO 5.0 2.9

RCB 16.0 9.2

SMB 38.8 22.4

MEG 5.0 2.9

EDC 12.0 6.9

RLC 10.0 5.8

FLI 5.0 2.9

PSALM 30.0 17.3

JGS 9.0 5.2

Total 173.3

Slide 31

Monthly Corporate Bond Trade Volume

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2009 Jan Feb Mar Apr May Jun

AC

ALI

EDC

FLI

GLO

JGS

MBT

MEG

MWC

PSALM

RCB

RLC

SMB

The Philippine Fixed Income Exchange:Ten-fold Increase In Trading Volume Of Corporate Bonds

8,843

967752

226

5,054

YTD Corporate Bond Volume (PhpMn)

AC 467.69 2.23%

ALI 150.00 0.72%

EDC 1,176.69 5.62%

FLI 19.30 0.09%

GLO 95.88 0.46%

JGS 4.68 0.02%

MBT 141.64 0.68%

MEG 1.00 0.00%

MWC 2.45 0.01%

PSALM 17,567.40 83.87%

RCB 71.40 0.34%

RLC 23.10 0.11%

SMB 1,224.77 5.85%20,945.99

5,104

2,205

Slide 32

Capital Market Trends And Regulatory Policy

Slide 33

Capital Market Trends: New Products

Initiative Update

Personal Equity Retirement Account (PERA)

Promotes voluntary long-term savings, through investments in PERA products designed to be locked for at least 5 years until retirement age of investor

Signed into law on August 22, 2008

IRR approved on October 21, 2009 by BSP, SEC and DoF and BIR

Council private sector members submitted comments on the draft Revenue Regulations

Feasibility Study of Equity Derivatives Trading

Engaged CBM Group, Inc. to develop a strategic plan to introduce derivatives and commodities trading on the PSEThe results of the study showed potential for developing a derivatives market in the Philippines particularly for index-based futures. The study also revealed, however, that the tax structure for trading for derivatives products needs to be reviewed.

Concluded in 2009

Exchange-Traded Fund Listing Rules

Will allow local and foreign ETFs, with minimum asset size of P250m and $10m, respectively, to list on the PSE

Approved by the PSE on April 2008 and submitted to the SEC for approval

Real Estate Investment Trust (REIT)

Seeks to provide a legal and regulatory framework and create a favorable market environment for real estate investment companies The REIT Act of 2009 requires REITs to list its shares on the PSE. The REIT must distribute 90% of its income as dividends to avail of tax incentives

Lapsed into Law on December 17, 2009; Implementing Rules and Regulations issued by SEC on May 13, 2010; Awaiting BIR Implementing Rules and Regulations

Slide 34

Capital Market Trends: Regulatory Policy

Initiative Update

Abolition of Documentary Stamp Tax on Secondary Trading

Permanently exempts stock trades through the PSE from the Documentary Stamp Tax (P0.75 per P200 par), with retroactive effect to March 20, 2009

Signed into law on June 30, 2009

Spin-off of Market Regulation Division

The PSE Board approved the spin-off of the Market Regulation Division into a wholly-owned and self-regulatory company to be known as Philippine Securities Regulation Company, Inc. that will monitor the activities of trading participants.

Approved by PSE Board on May 28, 2010

Slide 35

Capital Market Trends: New Legislation

Initiative UpdateFinancial Rehabilitation and Insolvency Act (FRIA)

Aims to update the outdated legal framework of insolvency proceedings under the Insolvency Law of 1909. The law provides financially distressed companies with four different remedies: 1) Court-supervised rehabilitation 2) Pre-packaged Rehabilitation 3) Out-of-court or informal restructuring agreement 4) Liquidation

Adopted by Congress on February 2, 2010

Credit Information System Act (CISA)

Aimed at establishing a comprehensive credit information system, allowing financial institutions ready access to accurate and up-to-date credit information thru the proposed Central Credit Information Corporation

Signed into law on October 31, 2008; Implementing Rules and Regulations for Approval by Congress

Collective Investments Schemes Law (CISL) formerly referred to as the Revised Investment Company Act (RICA)

Seeks to institute reforms in the domestic investment company industry, including mutual funds and aims to establish a comprehensive regulatory framework to enable investment companies to play a key role in capital formation

Joint Committee meetings/hearings were conducted on April 16, 2009 and May 19, 2009

No bill filed at House of Representatives

Financial Sector Taxation Reform (Fin Tax)

Meant to rationalize taxation to level the playing field as regards applicable tax on similar financial instruments offered by different financial institutions, thereby avoiding tax arbitrage

Legislative Committee report under preparation

Slide 36

End Of Presentation

Thank You!