phd house, new delhi september 24, 2009 presentation to petrofed members policy & regulations on...

Post on 19-Dec-2015

214 views

TRANSCRIPT

PHD House, New Delhi September 24, 2009

Presentation to Petrofed Members

Policy & Regulations on Natural Gas Pipelines

& way forward…

Presentation covers…

drivers for gas markets & models

gas market development stages

Indian gas market

downstream regulatory framework

way forward…

drivers for gas markets & models

context… drivers for gas markets

discovery of substantial quantities of gas in association with oil drilling (USA) or large discoveries of non-associated gas in industrial nations (Europe)

strong desire to reduce urban pollution caused by coal or heavy fuel oil (UK, Germany) supported by GDP levels & personal affluence to make gas a fuel of choice

strong support from government (all countries)

comparative shorter transport distances boosted development of pipelines (Netherlands & UK)

existing coal based “town gas” grids facilitated market penetration (UK, USA & Germany)

gas was priced competitively against existing fuels (Germany & Netherlands)

use of more polluting fuels was discouraged (UK & Netherlands)

countries that are substantial net importers of energy wish to diversify primary energy supply (Korea & Japan post 1970’s Gulf oil crisis)

three principal models of market development…

gas industry development model 1

private monopolies(multiple networks)

regulation deregulation

open access

“private Monopoly” (or oligopoly) model is typical of USA (FERC) & to some extent Germany (Self regulated basis)

local town gas grids are connected by multiple, privately owned gas networks

gas transportation typically takes place on a monopoly or occasionally “contract carriage” basis

regulation of market becomes a necessity to promote orderly development, private investment, long term consumer gain & to encourage responsible operators

long-run regulation tends to create distortions & inefficiencies, leading to deregulation & development of open access regimes, typically on a “contract carriage” basis

isolated grids

gas industry development model 2

development of State-owned monopolies has occurred in a number of countries, notably UK & France

nationalisation

state monopolies(single networks)

privatisation

open access

liberalisation

isolated grids

local town gas grids declined, following development of electric lighting, were later nationalised & consolidated by post-war governments

introduction of natural gas in 60s’ & 70s’ sees state funded development of transmission networks & conversion programmes

privatisation of state assets seen in UK & South America (now under consideration in France) …typically after up to 30 years of state ownership

UK model has evolved to fully open access…partial access in France

hybrid monopolies(mixed private/ state)

open access

public/ private development

liberalisationseparation

gas industry development model 3

isolated grids

In a number of countries a partnership between State & private industry has driven developments…as seen in Netherlands

development of industry viewed by government as a national priority

government takes an equity stake along gas chain or is heavily engaged as facilitator or guarantor

no privatisation…government retains stake in assets prior to adoption of an open access system typically 30 – 40 years later

gas market development stages

classification of gas industries

gas industry of any country can generally be defined on two axes of infrastructural or market sophistication

Basic Emerging Emerging/Restructuring

Sub-Mature MatureSub-Mature/Restructuring

1 – 2 gas sources. Some high pressure transmission pipelines with <10 off take points to power generation or primary/secondary industry

2+ gas sources. High pressure transmission with <100 off-take points for power generation and industrial usage. Some LDCs in major cities but with limited penetration into domestic energy sector

…so for emerging but requiring significant refurbishment & modernisation. Significant capital injection required

4+ gas sources. Nationally extensive transmission system with significant industrial& commercial market share. Growing need for integrated grid control with seasonal load balancing needs beyond use of line pack. Distribution networks in all major towns with significant domestic market penetration

…so for sub-mature but requiring significant refurbishment & modernisation. Significant capital injections required

multiple gas sources, flexible & integrated gas grid. Approaching saturation in geographical coverage to “economic” customers. Ongoing maintenance & capacity expansion programmes

Infrastructural Maturity

same applies to market sophistication

state monopoly private monopoly emerging (competitive)

emerging (restructuring)

liberalised

state owned transmission assets, municipal ownership of local distribution grids. Strong horizontal & where appropriate, vertical integration. De facto regulation by government ministries

significant private ownership of transmission & distribution assets. National monopoly or regionally focused oligopoly in transmission, distribution & supply. Limited negotiated TPA to transmission networks. Regulation by statute &/ or state ministry

governmental or supra-governmental drive for competition & break-up of monopolies. Negotiated access to capacity, rudimentary energy balancing/ settlement mechanism. Government appointed independent regulator and/ or supra-national body

so for “Emerging Competitive” but including partial (accounting) or legal separation transportation & shipping. Developing non-discriminatory access to capacity, cost reflective energy balancing & settlement mechanism. Independent regulatory body focused on promoting competition & limiting monopoly powers

ranging from partial (Industrial & commercial) to full (including residential sector) liberalisation. Full separation between transportation & supply. Horizontal integration with dual fuel suppliers. Fully non-discriminatory access code with mature energy balancing & settlement regime. Regulatory emphasis shifts from competition towards incentivising network efficiency

classification of gas industries

plotting relationships - markets & regulation

no two gas markets are exactly alike, but high level classification is possible along two axes – parabolic relationships

statemonopoly

privatemonopoly

emergingcompetitive

liberalised

basic

emerging

sub-mature

mature

mar

ket/

infr

astr

uctu

re

ownership/ regulation

(restructuring)

(restructuring)

infrastructure & market maturity

structure

different stages of development

nonestate

monopolyprivate

monopolyemerging

competitiveliberalised

none

basic

emerging

sub-mature

mature

mar

ket/

infr

astr

uct

ure

ownership/ regulation

(restructuring)

(restructuring)

Chile

Venezuela Turkey

SingaporeEgypt

Brazil

IndiaChina

TaiwanSaudi Arabia

Philippines

Bangladesh

USAUK

Spain Norway

Netherlands

New Zealand

Korea

Italy

Germany

Belgium

Australia

Argentina

Ukraine

JapanRussia

France

relative position of gas markets

gas market development case studies

UK

StateMonopoly

PrivateMonopoly

EmergingCompetitive

Liberalised

Basic

Emerging

Sub-Mature

Mature

Nationalisation of private gas companies

19

48

- 1

98

6

1986 - 1992 1992 - 1998

Full unbundling of transportation

& supply Full I&C and

residential competition

Privatisation and limited TPA

evolution of UK gas market

UK is now an advanced liberalised gas market… but how did it get there?

extensive town gas system dating back to 1860s’

nationalised in 1948 small natural gas network

created early 1960s for Algerian LNG

gas discovered in North Sea 1965

national transmission system constructed 1967 – 1973… town gas systems converted

British Gas privatised -1986 full I&C competition - 1992 full residential competition -

1998 now bedevilled by

regulatory complexity

EU gas market is not what it used to be…

recent past

emergent markets

exclusive rights (infrastructure & supply)

national monopolies

demarcation zones

no gas-to-gas competition

gas prices contractually linked to oil

vertically integrated companies

near future

mature but growing markets

equality of market rights

freedom to invest and sell

several players in all markets

integrated market with TPA

gas-to-gas competition

gas prices also a function of gas-to-gas competition (market-based)

legal separation of transportation

….transition towards a new world with new roles, business models & risks

European gas market maturity

during past 30 years, Europe has matured into a large, integrated gas market

PragueBrussels

Algiers

Vienna

Athens

Warsaw

Rome

Munich

Belgrade

Uzhgorod

Lisbon

Oslo

Paris

Sofia

Stockholm

HamburgBerlinLondon

Helsinki

BarcelonaMadrid

Fos-sur-Mer

La Spezia

Lyon

BernBudapest

Essen

Emden

Canvey

Le Havre

1970

Minsk

St. Petersburg

Bratislava

Berlin

Rome

LjubljanaZagreb

Oslo

Algiers

Madrid

Cordoba

London

Copenhagen

Prague

Warsaw

Vienna

Stockholm

Helsinki

Athens

Paris

Essen

Lisbon

Budapest

Tunis

Brussels

Sofia

Bern

Lyon

Belgrade

Dublin

Bucharest

Emden

H u elvaC artag en a

B arc elo n a

F o s-su r-M er

L a S p ezia

M on to ir

Z eeb ru g g e

Tyra

E ko fisk

Kårsto

KollsnesTro ll

G u llfaksStatfjo rd

H eim d a lF rig g

S le ip n e r Stavanger

O seb erg

W'haven

Belfast

Minsk

St. Petersburg

Bratislava

Rome

LjubljanaZagreb

Oslo

Algiers

Madrid

Cordoba

London

Copenhagen

Prague

Warsaw

Vienna

Stockholm

Helsinki

Athens

Paris

Lisbon

Budapest

Tunis

Brussels

Sofia

Bern

Lyon

Belgrade

Dublin

Bucharest

H u elvaC artag en a

B arc elo n a

F o s-su r-M er

L a S p ezia

M on to ir

Z eeb ru g g e

Tyra

E ko fisk

Kårsto

KollsnesTro ll

G u llfaksStatfjo rd

H eim d a lF rig g

S le ip n e r Stavanger

O seb erg

W'haven

Belfast

ArzewSkikda

B ilb ao

Is tan b u l

S in es

K rk

R o vig o

E l F erro l

Va le n cia

2000

maturity of infrastructure allows progress towards more liberalised market models

evolution of US gas market

StateMonopoly

PrivateMonopoly

EmergingCompetitive

Liberalised

Basic

Emerging

Sub-Mature

Mature

USA

19

40

- 1

98

6

1986 - 2002

different development path in USA - huge geographical scale with strong free market ethics

parallel evolution of natural gas & town gas since early 20th century

rapid expansion post 1945 via competition between private monopolies

strict regulation of prices & development introduced to curb excess & manage development

deregulation of interstate pipelines under FERC 501 in 1986 with progressive deregulation of pipelines

different states moving towards fully liberalised markets at varying speeds

regulatory model adapting to meet security of supply issues

gas pipelines in USA (Lower 48)

Interstate Pipelines

Legend

Intrastate PipelinesTexas

Oklahoma

Arkansas

Kentucky

Mississippi

Alabama

Louisiana

Delaware

Maryland

ConnecticutNew JerseyPennsylvania

Rhode Island

Massachusetts

New Hampshire

Vermont

Maine

New York

Kansas

Wyoming

New Mexico

Florida

South Dakota

IowaOhio

Virginia

North Carolina

Georgia

South Carolina

Tennessee

Michigan

Indiana

Illinois

Wisconsin

Minnesota

Colorado

Missouri

Arizona

North DakotaMontana

Idaho

California

Nevada

Washington

Oregon

Utah

West Virginia

Interstate Pipelines

Legend

Intrastate PipelinesTexas

Oklahoma

Arkansas

Kentucky

Mississippi

Alabama

Louisiana

Delaware

Maryland

ConnecticutNew JerseyPennsylvania

Rhode Island

Massachusetts

New Hampshire

Vermont

Maine

New York

Kansas

Wyoming

New Mexico

Florida

South Dakota

IowaOhio

Virginia

North Carolina

Georgia

South Carolina

Tennessee

Michigan

Indiana

Illinois

Wisconsin

Minnesota

Colorado

Missouri

Arizona

North DakotaMontana

Idaho

California

Nevada

Washington

Oregon

Utah

West Virginia

USA enjoys a substantially mature gas pipeline network, linking demand centres with traditional sources of supply

FERC regulates interstate pipelines & SERCs’ regulate intrastate pipelines

evolution of Dutch gas market

Dutch market model follows lines of a unique private industry/ state collaboration

StateMonopoly

PrivateMonopoly

EmergingCompetitive

Liberalised

Basic

Emerging

Sub-Mature

Mature

Netherlands

1963

- 1

998

1998 - 2002

Gasunie unbundled in 2004

small legacy town gas industry

super-giant gas discovery at Groningen in 1959

state/ private entities of Gasunie, NAM and Maatschaap created in 1963

main pipeline construction phase (internal & export) 1970 - 1980

rapid penetration achieved by competitive pricing against other fuels

implementation of EU competition directives saw unbundling of Gasunie

evolution of German gas market

Germany

StateMonopoly

PrivateMonopoly

EmergingCompetitive

Liberalised

Basic

Emerging

Sub-Mature

Mature

19

63

- 1

99

8

1998 - 2002 ?2002 - 2008

German gas market is unusual in Europe, having no direct State involvement, but self regulation

conventional town gas origins, first imports of natural gas in early 1960s

Germany has always been heavily dependent upon imports

no direct State participation but heavy involvement as facilitator & guarantor

multiple transporters, distributors & LDCs…main period of infrastructure growth 1975 – 1995, undergoing consolidation

ongoing liberalisation under EU directive though with a weak regulatory model (energy regulation has been made a sub-department of the telecom regulator)

StateMonopoly

PrivateMonopoly

EmergingCompetitive

Liberalised

Basic

Emerging

Sub-Mature

Mature

Korea

19

87

- 2

00

3

evolution of South Korean gas market

Partial privatisationsplit of KOGAS in 2003

Korean gas market is entirely LNG based around State owned transportation infrastructure & private LDCs

KOGAS formed in 1983 to develop industry…first LNG imports in 1987

varied State, private & municipal ownership

3 LNG import terminals, 20 separate LDCs’

strong government involvement in providing subsidy & fiscal relief for infrastructure development, in building regulations & for bus conversion

driven by need for supply diversity & environmental improvements

planned privatisation & separation of KOGAS into 3 separate supply companies in 2003 but considerable difficulties exist due to political & union resistance

generic gas industry development Path

Ownership / Regulation

StateMonopoly

PrivateMonopoly

EmergingCompetitive

Liberalised

Basic

Emerging

Sub-Mature

Mature

Mar

ket

/ In

fras

tru

ctu

reat a high level, similar patterns emerge around the world

there is no example of a substantial gas market emerging from a fully liberalised market

theoretical economic attraction is not borne out by evidence

Indian gas market

natural gas demand: latest outlook

Latest outlook as per 11th plan document

(MMSCMD)

Sector 2009-2010 2010-2011 2011-2012

Power 100 112 125

Fertilizer 52 79 79

City gas 14 15 16

Industrial 17 18 20

Petrochemicals/ refineries/ others/ internal consumption 29 31 33

Sponge iron/ steel 7 7 8

Total 219 263 281

Indian gas industry

Power & fertilizer prime consumers (70%)

Captive & industrial consumption (30%)

42%

13%4%

28%

3%

10%

POWER

FERTILISER

PETROCHEM/ LPG

STEEL

INDUSTRIES

CITY GAS/ CNG

projected imports of natural gas

© OECD/IEA

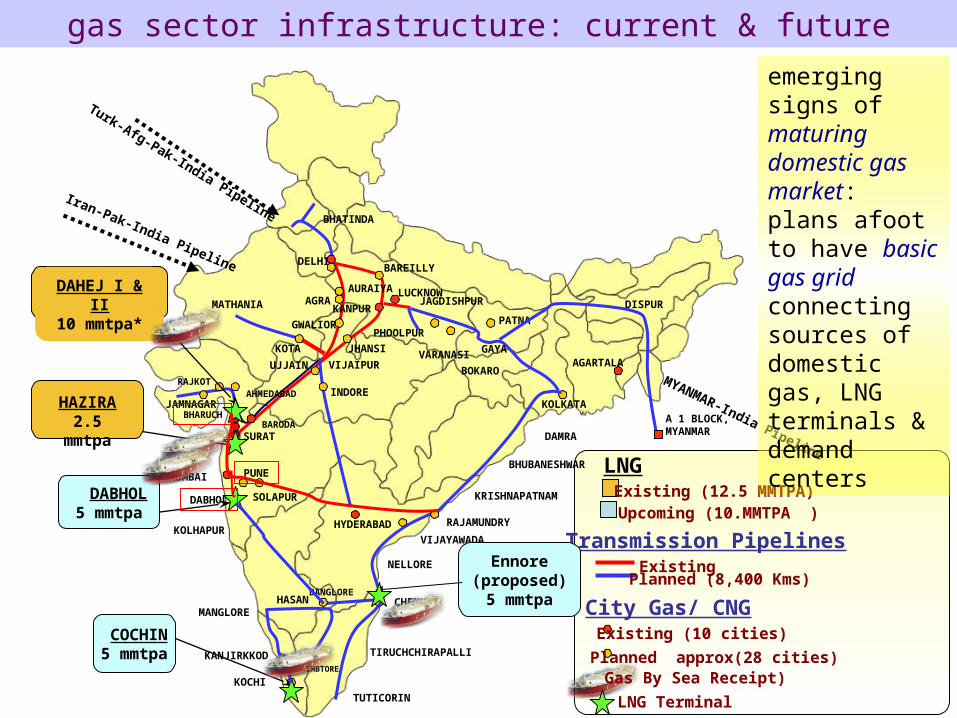

LNG sources: India

LNGExisting (12.5 MMTPA)

Transmission PipelinesExisting

JAGDISHPUR

PHOOLPUR

BHATINDA

JAMNAGAR

BAREILLY

DISPUR

DELHI

AGARTALA

BARODASURAT

KANPUR

LUCKNOW

PATNA

AHMEDABADRAJKOT

KOTA

MATHANIA

GWALIOR

VIJAIPUR

INDORE

UJJAIN

AGRA

KOLKATA

GAYA

BOKARO

VARANASIJHANSI

Iran-Pak-India Pipeline

Turk-Afg-Pak-India Pipeline

DAHEJ I & II10 mmtpa*

HAZIRA2.5 mmtpa

DABHOL5 mmtpa

COCHIN5 mmtpa

MYANMAR-India Pipeline

A 1 BLOCK, MYANMAR

Upcoming (10.MMTPA )

Planned (8,400 Kms)

City Gas/ CNGExisting (10 cities)

Planned approx(28 cities) Gas By Sea Receipt)

LNG Terminal

COIMBTORE

MANGLORE

MUMBAIBHUBANESHWAR

KRISHNAPATNAM

NELLORE

CHENNAI

TUTICORIN

TIRUCHCHIRAPALLI

PUNE

BHARUCH

DABHOL

HASANBANGLORE

KOLHAPURHYDERABAD

SOLAPUR

RAJAMUNDRY

VIJAYAWADA

DAMRA

KOCHI

KANJIRKKOD

AURAIYA

gas sector infrastructure: current & future

Ennore(proposed)5 mmtpa

emerging signs of maturing domestic gas market: plans afoot to have basic gas grid connecting sources of domestic gas, LNG terminals & demand centers

downstream regulatory framework…

natural gas pipelines

seek orderly sectoral growth & entry control

promote efficiency

productive: competition & reasonable cost

allocative: who remains in market ?

signaling role of price: cost reflective pricing

equity

fair play: access to natural monopoly assets

managed transition: legacy of controlled market (with state ownership) to robust segmented market

compliance – all stakeholders to adhere to rules & regulations, minimum service obligations & civic norms

regulatory design: objectives…

govt. policy on gas pipelines…

upfront provisioning of tax incentive u/s 80-IA (4) for infrastructure benefits: however, IT Act provides for 25% extra capacity, which is at variance with that in GOI policy for pipelines (33% extra capacity)

interchangeable use of common carrier or contract carrier in policy document & PNGRB Act, 2006- yet internationally gas markets have first been contract carriage systems before graduating into mature common carriage or hybrid systems

time frame for unbundling, which is key to creation of independent “shipping interest” not firmed-up

covers pipelines including spur line for transport of natural gas along with connected equipments & facilities, but excludes

dedicated pipelines for transporting natural gas to specific customer to meet specific requirements (& no re-sale)

pipelines in a CGD network

EOI followed by bidding route (or Suo Motu by Board)

does provide enabling platform with

minimum technical qualification requirements

net worth & bid bond linkage with pipeline length ensures serious bidding

authorization process…

PNGRB may modify or accept EOI depending upon gas availability or need to expand an existing pipeline & guided by objective (s) of:

promoting competition among entities;

avoiding infructuous investment;

maintaining or increasing supplies or for securing equitable distribution;

ensure adequate availability of natural gas throughout the country;

protection of customers’ interest in terms of availability of natural gas at reasonable natural gas pipeline tariff;

incentivizing rapid development of natural gas pipeline infrastructure

authorization process…

authorization process…

bidding criteria (25 years economic life):

lowness of PV of tariff bid for each year (70% weightage)

highness of PV of natural gas volumes (in MMSCMD) proposed to be transported (30% weightage)

Notes:

tariff to be bid zone-wise (TZn >= TZn-1) with 40% weight for TZ1 20% weight for %age increase over first zone 10% weight for %age increase over TZ2 (constant % thereon)

PV to be determined by using discount rate of 12%

bids to be consistent with assumptions considered in approved DFR of project

entity with highest composite score is successful

bidding process…illustratedBid A Bid B Bid C

TZ I II III IV Vol TZ I II III IV Vol TZ I II III IV Vol

Yr 10% 80% Yr 15% 90% Yr 0% 100%

8% 6.4% 14% 12.2% 0% 0.0%

1 1.30 1.43 1.54 1.64 48 1 1.20 1.38 1.57 1.76 50 1 1.50 1.50 1.50 1.50 54

2 1.33 1.46 1.58 1.68 56 2 1.26 1.45 1.65 1.85 60 2 1.53 1.53 1.53 1.53 63

3 1.36 1.50 1.62 1.72 72 3 1.29 1.48 1.68 1.88 70 3 1.56 1.56 1.56 1.56 81

4 1.39 1.53 1.65 1.76 80 4 1.32 1.52 1.73 1.93 90 4 1.59 1.59 1.59 1.59 90

5 1.42 1.56 1.68 1.79 80 5 1.39 1.60 1.82 2.04 90 5 1.62 1.62 1.62 1.62 90

10 1.57 1.73 1.87 1.99 80 10 1.77 2.04 2.32 2.60 90 10 1.77 1.77 1.77 1.77 90

15 1.72 1.89 2.04 2.17 80 15 2.26 2.60 2.95 3.31 90 15 1.97 1.97 1.97 1.97 90

20 1.91 2.10 2.27 2.41 80 20 2.88 3.31 3.76 4.21 90 20 2.17 2.17 2.17 2.17 90

25 2.11 2.32 2.51 2.67 80 25 3.68 4.23 4.80 5.38 90 25 2.40 2.40 2.40 2.40 90

PV 11.83 13.01 14.05 14.95 80 PV 13.18 15.16 17.20 19.30 90 PV 13.49 13.49 13.49 13.49 90

54 578 65 637 54 651

Tariff Criteria Vol

Wt 40% 20% 10% 30%

Bid Score Tot

A 11.83 10% 80% 578 A 45% 0% 10% 27% 82%

B 13.18 15% 90% 637 B 40% 0% 9% 30% 79%

C 13.49 0% 100% 651 C 39% 20% 8% 31% 98%

Min 11.83 0% 80% 651

short & medium term: expected participation from gas producers only- guided by desires to timely reach markets to match gas monetization plans & surety on capacity utilization!

extra capacity provisions…

provision for extra capacity in natural gas pipeline to be made available for use as common carrier by any third party on open access & non-discriminatory basis

capacity of natural gas pipeline = A + B + CA. capacity requirements of entity (?)B. firmed-up contracted capacity with other entitiesC. at least 33% of (A) & (B) = extra capacity

(?) should entity’s own requirement be clubbed with that of requirement of its own affiliate as well (provisions in PNGRB Act, 2006 does not envisage so; yet authorizations of some of pipelines do not suggest so…)

extra capacity provisions…

both government policy & PNGRB have same objective of having competitive gas markets – key is progressive unbundling along gas value chain

to create new authorization on ‘bundled basis’ only to be ‘unbundled’ later may have serious consequences in future

clubbing provision may have potential of serious monopoly abuse, in case authorized entity were to create an affiliate to be used as surrogate for blocking capacity booking by others

consumer may have only bundled contract option restricting it to either authorized entity or its affiliate

provisions in affiliate code of conduct may come in conflict when affiliate capacity requirements are to be assessed

section 21 of the PNGRB Act 2006 emphasizes need for fair competition & availability of natural gas

extra capacity provisions…

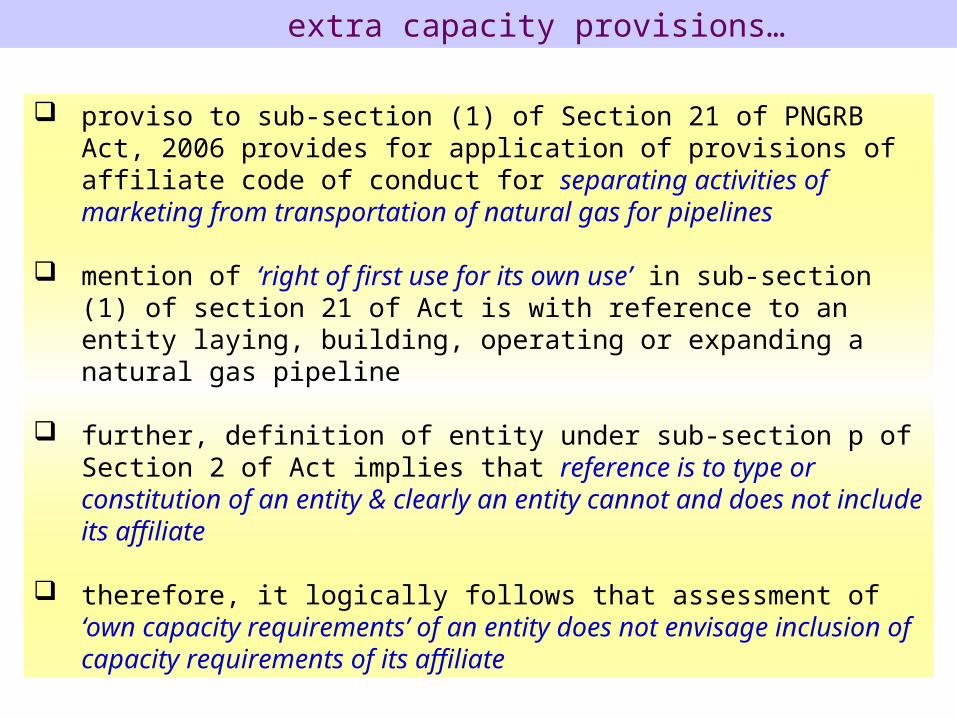

proviso to sub-section (1) of Section 21 of PNGRB Act, 2006 provides for application of provisions of affiliate code of conduct for separating activities of marketing from transportation of natural gas for pipelines

mention of ‘right of first use for its own use’ in sub-section (1) of section 21 of Act is with reference to an entity laying, building, operating or expanding a natural gas pipeline

further, definition of entity under sub-section p of Section 2 of Act implies that reference is to type or constitution of an entity & clearly an entity cannot and does not include its affiliate

therefore, it logically follows that assessment of ‘own capacity requirements’ of an entity does not envisage inclusion of capacity requirements of its affiliate

tariff determinationtariff model: cost of service (discounted cash flow)

historical cost of assets to be considered on “rolling basis”

efficiently incurred capex & opex with linkage with capacity (existing pipeline capacity determination an issue ?) & operating parameters of pipeline: to be considered over economic life of project (replacements factored)

norms for capacity utilization & variable costs linked to actual throughput

returns linked to12% post-tax on capital employed (implying project funding & fund re-engineering flexibilities available)

infrastructure benefits u/s 80-IA allowed to be retained: shall incentivize pipeline investments

capital employed = net fixed assets (gross fixed assets less depreciation at SLM rates as per Companies Act + normative working capital (30 days of opex: at variance with product pipelines at 20 days during APM days’)

tariff determinationtariff model: cost of service (discounted cash flow)

no change in tariff in case of capacity expansion by up to 10%

in case of capacity expansion >10%, entity to submit proposal to PNGRB & same may be allowed provided entity agrees to reduction in tariff by sharing fifty percent of proposed incremental tariff revenue calculated based on applicable tariff before expansion & incremental volumes

non-discriminatory charge of tariff & tariff to be reflected in invoice in energy equivalence terms (Rs./ MMBTU) making system more transparent from consumers’ standpoint

PNGRB, in medium term, should focus on evolving best standards & practices in pipeline laying, building & operations to enable development of benchmarks for efficient capex & opex in pipelines

tariff recovery system… potential disconnect

300 km each

TZ 1 TZ 2 TZ 3 TZ 4 TZ 5

50 km band

Interconnecting pipeline

1.20 1.35 1.45 1.53 1.60

1.20 1.35 1.451.351.45

two-way gas flows physical impossibility- may result in unofficial swap positions

inadvertently netback advantage could flow away from inter-connected pipeline into interconnecting pipeline resulting in:

pre-mature gas-to-gas competition interconnecting pipeline opts for

postalized tariff for entire pipeline length & customer closer to starting point suffers

customer pays different tariffs based on gas source in same pipeline in same zone!

new pipeline development gets adversely impacted as two-way gas flows cannot be envisaged in economics of pipeline design as volume flows may not be same in each tariff zone

rationale of tariff recovery similar to a railway line where passenger getting-off closer to starting point does not want to pay fare for distance not traveled

flexibility of volume variations in tariff zones allowed as pass-through in tariff

principle based on “pay for distance traveled alone” may make inter-connection proposition unattractive for inter-connected pipeline….maybe tariff recovery system should be dynamic to gas grid concept & not vice-versa…

Injection point

way forward…

some issues in way forward…

calibrated movement required (considering nascent stage of Indian gas market) from zonal postalized basis to full fledged entry-exit model for tariff recovery system, which is hallmark of most developed gas markets (Netherlands & U.K.)

regional network of pipelines may sometimes resemble CGD networks, yet CGD regulations cannot be applied due to legacy issues & impracticability, like, AGCL’s NE network of pipelines catering to small tea gardens; Charottar co-operative catering to small villages in an area along small industrial customers belt; Vadodra municipal corporation’s pipeline network catering only domestic PNG segment, etc.

applicability of tariff system yet to be articulated for regional network of pipelines, like GAIL’s pipeline network in KG basin

some issues in way forward…

monitoring mechanism for ensuring transparent contracting based on access code provisions

impact analysis of provisions of direct tax code on new natural gas pipeline projects

notification still awaited on regulations for basis of capacity determination for existing pipelines & declaration of pipelines as common carrier or contract carrier as envisaged in PNGRB Act, 2006 & in pipeline authorization regulations

thoughts on evolving trading platform for trading in pipeline capacity & gas supply contracts…

way forward for India…

Ownership / Regulation

StateMonopoly

PrivateMonopoly

EmergingCompetitive

Liberalised

Basic

Emerging

Sub-Mature

Mature

Mar

ket

/ In

fras

tru

ctu

re

possible alternative routes to be guided by degree of

non-discriminatory access allowed to CC capacity

effective unbundling of transportation & marketing activities

…& during such period, adherence to ACOC provisions, regulatory maturity in handling complex access code issues & GOI’s forward looking policies shall be keenly followed by industry…

Current

Thanks

views contained in this presentation are expressed in personal capacity

Vijay Duggal, DGM Commercial (CGD), BPCL [email protected]