pg 42. interview: dhruv goel, md, steelmint pg 45....

TRANSCRIPT

15TH – 30TH Nov 2014 . Vol 1 Issue 11 . For Private Circulation Only

pg 42. INTERVIEW: Dhruv Goel, MD, SteelMint

pg 45. Indian Economy – Trend indicators

3GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 2

VOL 1 . ISSUE 11 . 15TH - 30TH NOV 2014

Vineet Bhatnagar- Managing Director and CEO

EDITORIAL BOARD:Naveen Kulkarni Manish AgarwallaKinshuk Bharti Tiwari Dhawal Doshi

COVER & MAGAZINE DESIGN Chaitanya Modak, www.inhousedesign.co.in

FOR EDITORIAL QUERIES:PhillipCapital (India) Private LimitedNo. 1, 18th Floor, Urmi Estate, 95 Ganpatrao Kadam Marg, Lower Parel West, Mumbai 400 013

RESEARCH Automobiles Dhawal Doshi, Priya Ranjan

Banking, NBFCs Manish Agarwalla, Pradeep Agrawal, Paresh Jain

Consumer, Media, Telecom Naveen Kulkarni, Jubil Jain, Manish Pushkar

Cement Vaibhav Agarwal

Economics Anjali Verma

Engineering, Capital Goods Ankur Sharma, Hrishikesh Bhagat

Infrastructure & IT Services Vibhor Singhal, Varun Vijayan

Metals Dhawal Doshi, Ankit Gor

Mid-caps Vikram Suryavanshi

Oil & Gas, Agri Inputs Gauri Anand, Deepak Pareek

Pharmaceuticals Surya Patra

Retail, Real Estate Abhishek Ranganathan, Neha Garg

Technicals Subodh Gupta

Production Manager Ganesh Deorukhkar

Database Manager Vishal Randive

Sr. Manager – Equities Support Rosie Ferns

SALES & DISTRIBUTION Kinshuk Tiwari, Ashvin Patil, Shubhangi Agrawal, Kishor Binwal, Sidharth Agrawal, Bhavin Shah, Dipesh Sohani, Varun Kumar

CORPORATE COMMUNICATIONS Zarine Damania

GROUND ZERO - PREVIOUS ISSUES

16th Aug 2014 Issue 8

1st Sep 2014 Issue 9

1st July 2014 Issue 6

1st Aug 2014 Issue 7

16th June 2014 Issue 5

1st Oct 2014 Issue 10

3GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 2

LETTER FROM THE MANAGING DIRECTORThe latest buzz in retail is ecommerce or etailing

as many call it and it has already reached most

cities in India, even the smaller ones. The Indian

ecommerce market has grown at a rapid pace over

the last couple of years and customers are excited,

investors are bullish, and competition is now taking

it very very seriously. What was once considered

the ‘little brother’ of Indian retail now seems a lot

bigger, accounting for nearly 10% of organised re-

tail in a fragmented market. In October 2014, US$

300mn worth of goods are estimated to have been

sold in a series of big online shopping events held

by major etailers in India.

With ecommerce grabbing headlines in India like

never before and offline retailers raring to go on-

line, we publish our cover story on ecommerce and

omni-channel retailing. The story “Offline retail:

‘Omni’ous or Oblivious to Online?” penned by re-

tail analysts Abhishek Ranganathan and Neha Garg

is an interesting analysis of the Indian ecommerce

market, the business models of these players, and

the way ahead for offline retailers. The story pro-

vides insights on the dynamics of etailing in India

as well as China and the lessons that may lead to

the evolution of a sustainable business model. Until

then, let’s enjoy the deep discounts.

Along with the etail story, we have interviewed Mr

Dhruv Goel, MD SteelMint. He highlights various

challenges and logistical constraints faced by the

steel industry due to the mining restrictions in vari-

ous states in India.

Best Wishes

Vineet

4. COVER STORY: Offline retail: ‘Omni’ous or Oblivious to Online?

Ground Zero evaluates the ecommerce business models, the dynamics, the threats and opportunities to offline. With many offline retailers looking to bridge the ‘online’ gap, we look at the viability of an omni-channel strategy

42. INTERVIEW: Dhruv Goel, MD, SteelMint

Highlights operating challenges for steel producers post mining restrictions in iron ore

45. Indian Economy – Trend indicators

47. PhillipCapital Coverage Universe: Valuation Summary

CONTENTS

5GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 4

Various shopping apps now bring the store to the consumer anywhere and anytime

5GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 4

COVER STORY

Online retailing or ecommerce is catching fire in India — while it is less than 1% of overall

Indian retail, it is already 10% of organized retail and many predict it will be 8% of the total

retail market by 2020!! Chinese online ecommerce giant Alibaba’s success seems to have

spurred Indian ecommerce players. As the competition hots up, we take a good look at

the Indian ecommerce market, its leading players, and their business models including

the viability of what all of us love — discounts. We try to understand if Alibaba’s business

model may have lessons for Indian retailers. We came across uncanny similarities between

offline and online retailers, despite their many differences. The fundamentals of doing

business online are not radically different from offline and the laws of economics will catch

up with the former as well. With many offline retailers looking to bridge the ‘online’ gap,

we looked at the viability of an omni-channel strategy, deployed successfully in developed

countries. The competition to offline is real and business models will have to evolve — it

will be an ominous threat to those who are oblivious. The online retailers’ products may be

delivered in a day, but a winner will not emerge so quickly — out of the rollercoaster ride

of discounts, mega sales, and promotions may emerge a business model that is unique to

India, just as Alibaba’s is unique to China.

BY ABHISHEK RANGANATHAN & NEHA GARG

pg. 6 Ecommerce in India Drivers of e-biz models: opportunities and discounts galore___________________________________________pg.18 The Chinese Ecommerce Market Lessons from Alibaba for Indian retailers – offline & online___________________________________________pg.24 Building an Omni Channel Necessity driven by competition but is it for every offline retailer?___________________________________________pg.30 Ecommerce vs. Physical stores The battle has just begun - discounts and funding to continue___________________________________________pg.34 Every battle has its winners & losers Shop till you drop or till the website drops – sustainability remains ignored___________________________________________

7GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 6

The words ‘retail therapy’ or ‘going

shopping’ were long associated with

physical, brick-and-mortar retail. But

with stores and brands going clicky

(websites) and appy (mobile apps) these terms

have already widened to accommodate online

shopping. Over the last couple of years, the

Indian ecommerce space has filled up with home-

grown players such as Flipkart, Snapdeal, and the

big daddy of ecommerce, Amazon. Online shop-

ping has captured the imagination and attention

of consumers, media, brick-and-mortar players,

brands, and of late, even the tax authorities and

the government.

Various studies estimate Indian ecommerce to

be about US$ 3bn as of now, which is just 0.8%

Drivers of e-biz models: opportunities and discounts galore

E C O M M E R C E I N I N D I A

of the Indian retail market. However, this share is

expected to increase rapidly as more people shop

online. Of the 200mn people in India who access

the internet, 28-30mn (less than 3% of India’s

population) shop online. However, this number

can move up to touch 100mn by 2015 and a

whopping 200mn by 2017, which is the same as

the number of Indian internet users in India today.

Nitin Bawankule, Director, Google India Ecom-

merce, says that, “Even now, there are at least

200mn people who can purchase online in India”.

The market is redefining itself rapidly as etailers

advertise, reach out, and offer deals and discounts

to consumers.

Growth drivers for ecommerce — growing internet users Current online spending

So how big is the Indian Retail market?

During GOSF 2013 (held over three days in December 2013), over 60mn people visited online shopping sites and 16mn unique customers shopped at the event. Myntra.com claimed that it made over 100,000 shipments for orders placed in those three days.

Sour

ce: E

urom

onito

r Int

erna

tiona

l

Source: KPMG

7GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 6

An interesting example of increasing online shop-

ping is the Great Online Shopping Festival (GOSF)

hosted by Google. During GOSF 2013 (held over

three days in December 2013), over 60mn people

visited online shopping sites and 16mn unique cus-

tomers shopped at the event. Myntra.com claimed

that it made over 100,000 shipments for orders

placed in those three days.

The average Indian online buyer is between the

ages of 25 and 30 and ‘affluent’ — he/she has

access to websites seamlessly through personal

computers and smart phones. Interestingly, the

share of tier-2 and tier-3 cities is higher for most

online players. Snapdeal claims that over 60% of

the orders to its website are from tier-2 and tier-3

Rise in internet penetration

Particulars 2009 2010 2011 2012 2013 2017-20(E)

E-tailing ($ bn) 3.8 5.3 7 9.5 12.6 40-50% CAGR

E-commerce 0.4 0.6 1 1.5 2.3 10-20% CAGRSource: Crisil, IAMAI, PwC analysis and Industry experts

Industry growth forecast for e-commerce

Who is buying online?

cities. Even in the case of pure-play apparel players

such as Jabong, these statistics hold true — 62% of

Jabong’s shipments in Q2FY14 were to tier-2 and

tier-3 markets. This demand is driven by the fact that

many of the brands have limited presence in tier-2

and tier-3 markets due to shortage of quality retail

space or unviable economics, given limited popula-

tion in a location.

Interestingly, the share of tier-2 and tier-3 cities is higher for most online players .62% of Jabong’s shipments in Q2FY14 were to tier-2 and tier-3 markets.

No. of SKUs 139,000

Brands 1,600

Lifestyle Category 9

Facebook followers (mn) 3.2

Postal codes covered 12,000

Order rate on same day delivery 70%

Share of Tier-2 & 3 cities 62%

Current share of sales from smart phones 27%

Monthly average visits using mobile devices (mn) 14 Source: Company, PhillipCapital research

Snapshot of Jabong’s operations

Jabong’s growing orders per day

Sour

ce:

KPM

G

Sour

ce: C

ompa

ny, P

hilli

pCap

ital r

esea

rch

9GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 8

What are Indians buying online?

Electronics and CDIT (consumer durables informa-

tion technology) products dominate the current

online buying space. In terms of value, electronics is

the largest category — it has a 47% share of the on-

line retail market. Within electronics, mobile phones,

laptops, tablets, and cameras are big purchases. A

large logistics company that partners with ecom-

merce players for deliveries said that electronics (and

particularly mobiles) form a very large share of their

deliveries. Reports said that Flipkart sold over half a

million mobiles in just one day on its Big Billion Day

sale on 6th October. Flipkart and Snapdeal list over

3,000 stock-keeping units (SKUs) and 5,000 SKUs of

mobiles respectively on their portals. The average

ticket size in electronics is estimated to be Rs 5,000.

Apparels, footwear, and accessories are the next

largest categories bought online, with a 31% share.

While this category has a lower share (in value

terms) than electronics, it clocks the highest volume

amongst all categories. The average ticket size in

this segment is around Rs 2,000. The rest of the

online pie is fragmented between books, home

furnishing, baby products and others.

Share of overall retail market, 2013

Online retail market-Category break-up (by value), 2014

Jabong has had the number of its unique visitors double in the last 2 years

Sour

ce: C

ompa

ny, P

hilli

pCap

ital r

esea

rch

Source: KPMG

Source: Technopak Analysis

Jabong’s category wise revenue-mix

Source: Company, PhillipCapital research

9GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 8

Reports said that Flipkart sold over half a million mobiles in just one day on its Big Billion Day sale on 6th October.

Number of SKUs on offer by Flipkart

Large number of SKUs on offer

11GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 10

India’s online market comprises of various players

with different models. Players that retail pretty much

everything from electronics to FMCG products

follow a version of the ‘marketplace’ model. Amazon

and Snapdeal operate on this kind of a model where

their role is to facilitate the sale and fulfil it — that is

handle logistics, deliveries, and returns. In this mod-

el, the portals do not hold any inventory on their

books. Flipkart used to operate on a hybrid model,

where it held its own inventory and also acted as a

The categories, the major players, and business models

Number of SKUs on offer by Snapdeal

marketplace. However, it has now moved to a mar-

ketplace model, albeit with far lower sellers/vendors

than Amazon or Snapdeal, since WS Retail (erstwhile

Flipkart group company) still contributes a significant

portion of its sales. Vendors and sellers usually sign

up with these marketplace online retailers for a fee,

depending on the category.

Players such as Myntra and Jabong, which are

primarily apparel portals, have an inventory model.

They have moved to a hybrid market place, but it is

still skewed towards the inventory-led model.

Mobiles is a major category here as well

Vendors and sellers usually sign up with these marketplace online retailers for a fee, depending on the category.

11GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 10

So what is the revenue model?

The marketplace etailers in India operate on a

commission-based model, under which they receive

a fee for listing plus commission on sales depending

on the category. Amazon calls it referral fee. The fee

is charged when an order is placed and the amount

is disbursed a few days after shipping.

“These portals are not retailers but technology

companies and are built on sound technology

platforms,” says a senior executive of one of India’s

largest retail chains. “Being pure technology com-

panies, their platforms are well integrated with their

back-end”. he adds.

Commissions are usually a function of Gross Mer-

chandise Value (GMV) — the value of goods listed

(note inventory is not carried by the companies) and

sold on these portals. In a hybrid model, the reve-

nues are more conventional as far as the e-tailers

own inventory goes.

GMV is one of the benchmarks that retailers use for

equity funding. But the GMV is seldom reflected in

Online retailers: Different operating models

Sell on Amazon Fees / Rate *Promotional Standard

Monthly Subscription Free Rs.499

Closing Fee (per Unit Sold) Rs.10 Rs.10

Referral Fee

Books, Music & Movies 5% 12%

Video Games - Console 5% 8%

Video Games - Games 5% 12%

Consumer Electronics (includes Camera) 5% 8%

Electronic Accessories 5% 12%

Mobile Phones 4% 5%

Personal Computers, Laptops & Tablets 4% 5%

Toys & Baby Products 5% 15%

Personal Care Appliances 5% 15%

Health & Personal Care 5% 15%

Beauty 5% 15%

Pet Supplies 5% 15%

Fashion Jewellery 8% 15%

Watches 8% 15%

Home & Kitchen 5% 15%

Shoes 8% 15%

Sporting Goods 5% 15%

Apparel 8% 15%

Handbags & Luggage 8% 15%

Eyewear 8% 15%

Consumable Physical Gift Cards 5% 5%

Fees charged by Amazon.in

*till

31s

t Dec

201

4

Source: KPMG

Sour

ce: a

maz

on.in

13GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 12

their books of accounts due to either the holding

structure (complicated in the case of Flipkart and

Myntra) or because revenue recognised is purely

commission based (Snapdeal). However, numbers

do talk and the numbers of some of the players

talk more and give us an interesting insight into the

operations of the sector.

GMV - Grossly misstated value?

GMV is before all discounts, couponing, vouchers,

and taxes. So when we read about a GMV of US$

100mn in a day or US$ 1bn, it is the gross value

of products before discounting and couponing.

But what the customer pays is net of all discounts,

vouchers, and coupons. GMV is open to interpreta-

tion and different retailers may compute it different-

ly. India, unlike many developed countries, follows

a maximum retail price (MRP) regime for sale of

goods. Discounts are offered on MRPs. But then,

one company may choose to compute GMV on MRP

while another may compute GMV on the list price

(MRP minus discounts that the brands/seller offers).

While MRP is relevant in most consumer products

sold anywhere in the country, it’s the least relevant

in electronics. When was the last time anyone sold

a mobile or a television or home appliance at MRP?

Since electronics form nearly 50% of the e-tail in

India, it is natural that the GMV calculated on MRP

will be skewed. GMV is reported on the current run

rate rather than the achieved figure. So GMVs for

Flipkart and Snapdeal could be misleading given the

high mix of electronics.

In e-tail shopping, there is almost always a coupon –

a coupon or a voucher code is essentially a discount

over and above the listed price, which may or may

not be discounted. These are at the discretion of the

e-tailer and not under the control of the brand. It’s

more commonly used by apparel e-tailers such as

Jabong and Myntra. It’s noteworthy that Flipkart and

Amazon seldom use couponing. One of the industry

observers said that, “Coupons are a mechanism of

customer acquisition and in apparels, the customer

doesn’t necessarily visit the website very frequently,

and to get him/her to do this, coupons are offered

regularly.”

Marketplaces such as Flipkart and Amazon, catering

to a large variety of products, rarely offer coupons

as the customer ends up visiting the site for some

category or the other. Apparels/fashion have the

maximum margin. Interestingly, GMV includes the

value of vouchers/coupons as well, which means

it is calculated before any coupons are offered to

the customer. As one of India’s largest retailers puts

it, “If it were net of any of these discounts then it

should be called net merchandising value not GMV.”

As one of India’s largest retailers puts it, “If it were net of any of these discounts then it should be called net merchandising value not GMV.” “If you don’t want a good price, we will still offer you a coupon.”

Portal Alexa Rankings for India

Categories Model No of Registered users (mn)

No of products on offer (mn)

GMV Rs mn)

Flipkart.com 5 Electonics, Apparel, Accessories, Footwear, General Merchandise, FMCG

Marketplace 22 15 40,000

Amazon.in 7 Electonics, Apparel, Accessories, Footwear, General Merchandise, FMCG

Marketplace 15 17 na

Snapdeal.com 10 Electonics, Apparel, Accessories, Footwear, General Merchandise, FMCG

Marketplace 20 5 30,000

Jabong.com 14 Apparel, Footwear and Accessories Hybrid 2.9 0.139 6,000

ebay.in 16 Electonics, Apparel, Accessories, Footwear, General Merchandise, FMCG

Marketplace 2.1 NA na

Myntra.com 30 Apparel, Footwear and Accessories Hybrid 1mn 0.05 4,000Source: Similarweb.com, media reports, PhillipCapital research

Website traffic for Indian e-commerce websites and product offering

13GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 12

How to avail of couponing…

How couponing happens …

Discounting at cart level by couponing

No discount at brand level

15GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 14

Couponing between rival portals is continuous. An

offline retailers said, “If you don’t want a good price,

we will still offer you a coupon.” What this means is

that even if a product is displayed on full price, the

customer is still offered a discount coupon when he

checks out his purchases (just before the payment

stage).

Show me the money

The underlying revenue model of most of the enti-

ties that operate e-tailing portals are commissions

and gross profits — if they also follow the hybrid

model. But the costs of e-tailing are intriguing and

they cause of a lot of heartburn to offline retailers as

well as brands. Contrary to perception that online

retail entails lower costs as there are no costs asso-

ciated with operating stores, these businesses have

high costs in the form of discounts, free delivery for

products (where cost of the product is sometimes

lower than delivery costs), and customer returns. In

e-tailing parlance, some of these costs are known as

‘customer acquisition costs’.

Customer acquisitions cost: In-fact, the largest cost

for e-tailers in a nascent ecommerce market such as

India is customer acquisition costs — this is because

it includes discounts offered on owned merchandise

or the cost of funding discounts in a marketplace

model. These discounts are offered over and above

the discounts offered by brands or sellers of the

product and are usually offered to customers in the

form of coupons. They are known as cart discounts

because they can be availed once the customer adds

the product to his or her cart. The discounts some-

times tantamount to losses at the gross level (trans-

action level) in the hybrid model; in a marketplace

model, they sometimes exceed the commissions that

the e-tailer earns. E-tailers bear these losses for cus-

tomer acquisition. However, these discounts are not

limited to a one-time purchase and are often open

for all — they don’t distinguish between old and

new customers. This implies that they are given not

only for customer acquisition but also for customer

retention. Of course, there are cases where coupons

are offered for registering on the portal. Clearly, the

e-tailers’ losses are the customer’s gains.

“The Prime Minister says ‘make in India’ ….but given

the recent funding the e-tailers have received, one

would imagine it’s the best time to Buy in India. It’s a

Investee company Amount raised (US$ mn)

Snapdeal 902

Flipkart 2,090

Amazon 2,000

Myntra 70

Jabong 240Source: Media Reports

Funding received till date by leading ecommerce players

“The Prime Minister says make in India….but given the recent funding the e-tailers have received, one would imagine it’s the best time to Buy in India. It’s a direct benefit transfer – from shareholders to customers,” says a senior executive of one of India’s largest retail chains.

Promotions to use mobile apps

15GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 14

For FY14 *Flip-kart

Myntra Snapdeal Jabong **Home shop 18

Revenue (Rs mn) 30,252 2,635 1,682 4,386 2,441

GMV (Rs mn) 40,000 4,000 30,000 6,000 9,988

Profit/Losses of E-tailers

(7,163) (26) (2,646) (2,934) (1,546)

Source: Company, Media reports, PhillipCapital Research. **FY13

Key metrics of leading ecommerce players

direct benefit transfer – from shareholder to custom-

ers,” says a senior executive of one of India’s largest

retail chains.

Discounting is the key driver to buy today. A

consumer will buy standardised products for con-

venience but the first greed is price. Mr Biyani of

Future Group explains, “Anything which sells in a

matter of seconds is usually a product where the

price is lower than the perceived value. For exam-

ple a Xiaomi mobile (which usually gets sold out in

seconds).”

But customer acquisition costs don’t end here. The

other significant costs are Search Engine Marketing

(SEM) costs. These are costs that ecommerce players

incur to direct traffic to their portals on leading

search engines such as Google. Typically, searches

for key words associated with the merchandise on

offer on a portal will direct the traffic to the portal.

For e.g., if one searches for ‘buy shoes’ online, the

search results will throw up names of portals that sell

shoes and to ensure that the e-tailer’s name appears

in the top-5 search results, or in the first page of

search results, these portals incur search engine

marketing costs.

“The Prime Minister says make in India….but given the recent funding the e-tailers have received, one would imagine it’s the best time to Buy in India. It’s a direct benefit transfer – from shareholders to customers,” says a senior executive of one of India’s largest retail chains.

Jabong (FY14) *Homeshop18 (FY13)

Revenue (Rs mn) 4,386 460

GMV (Rs mn) 6,000 3,056

Gross Profit (Rs mn) (447) 140

Gross Margins (rhs) -10% 30%

EBITDA (2,492) (259)

EBITDA Margins -57% -56%Source: Company, PhillipCapital Research *only internet segment

Operating metrics of Jabong and Homeshop18

One of the most interesting cases of SEM costs is

when flipkart.com ran its big billion day sale on 6th

October 2014. When one searched for “big billion

day” on Google the search actually led to amazon.

in instead of Flipkart!! – it seems like Amazon paid

Google to direct the search to their website.

Logistics costs

One of the peculiarities of the Indian ecommerce

market is the high share of cash on delivery (CoD)

orders. Unlike most other countries, the share of

prepaid orders is very low in India for many reasons.

Most buyers either don’t have a credit card or net

banking (not really surprising for a country where

more than 40% of the population doesn’t have bank

accounts). More than 50% of the orders that are

placed on Indian ecommerce websites are CoD

orders says Mr Bawankule of Google India. CoD

has inherent problems — it allows customers to

change their mind after their purchase has been

shipped and sometimes couriers have to wait for

customers to make a payment, which in some cases

may not happen quickly for want of ready cash.

Homeshop18’s return rate for COD and non-COD

Customer acquisition cost (as % of GMV) for HomeShop18 (internet segment) and gross commision as % of GMV

More than 50% of the orders that are placed on Indian ecommerce websites are CoD orders says Mr Bawankule of Google India.

Sour

ce: H

omes

hop1

8, P

hilli

pCap

ital R

esea

rch

*Flipkart (India) Pvt. Ltd. & Flipkart Internet Pvt. Ltd.

17GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 16

transactions was approximately 21.4% and 2.8% in

FY13, respectively. A logistics company executive

states that there are instances when the customer

doesn’t have ready cash at home and the courier

has to wait till he withdraws cash and returns home

for collecting the payment.

Adding to this complication is the reach of logistics

companies to various parts of the country. A KPMG

report estimates that most logistics companies ser-

vice around 6,000 area pin codes out of the 22,000

area pin codes in India (less than 30%). To overcome

this problem of reach, some online players such as

Flipkart and Amazon have established their own

logistics team alongside using third-party logistics

companies. However, the rationale for establishing

their own logistics network is not reach alone — an

executive with a leading logistics player said that

CoD deliveries (by third party logistics vendors) cost

more because they are more time consuming and

need checks and balances (given the cash handling).

Some of the checks and balances include mid-day

reconciliation and deposit of cash collected. There-

fore, the logistics companies are unable to make

optimum number of deliveries and this cost is billed

into the CoD orders. Moreover, air shipments (more

expensive) still constitute over 80% of the total

shipments.

This does make one wonder if operating your own

logistics is viable? The logistics executive’s view on

the matter is, “Actually own logistics is not profita-

ble as there is a fixed cost involved and it is seldom

able to make optimum orders given the complica-

tions of CoD. Our operations are tuned to make de-

liveries across a designated area irrespective of who

the shipper is, hence our efficiencies will be high.

The fundamental reason why ecommerce players

get into their own delivery logistics apart from han-

dling COD orders is working capital requirements.

Logistics companies can take anywhere between

5 days to 15 days to remit the cash collected on

delivery to the ecommerce players and that robs

them of working capital.” Given that most ecom-

merce companies are operating on losses, working

capital management becomes imperative. Mr Basrur,

Head eCommerce at Raymond Ltd (also one of

the founding members of Quikr.com – a classifieds

website) observes, “In-house logistics capabilities of

ecommerce players are not going to be too different

from those of third-party vendors. It’s a function of

where the product is (known as fulfilment centre) and

where the customer is. However, costs still may not

be justified for own logistics as number of deliveries

made are likely to be sub-optimum.”

Discounts, free delivery, cash on delivery, easy

returns — who wouldn’t want to be an online con-

sumer. But one of the main reasons why consumers

continue to flock online is the range of products

and the convenience of not having to step out of

your home and buying everything under one roof,

says Mr Bawankule of Google. While for a consumer

in developed markets convenience and range are

most important, for the Indian consumer it’s price

and range. Online stores, especially marketplaces,

literally bring the store to the consumers’ desktop or

mobile. The variety and categories on offer at a click

or touch are unparalleled. And to top it all, there are

apps and websites which guide you on best pricing

Need more reasons to buy online?

“Actually own logistics is not profitable as there is a fixed cost involved and it is seldom able to make optimum orders given the complications of CoD. Our operations are tuned to make deliveries across a designated area irrespective of who the shipper is, hence our efficiencies will be high.”

The fundamental reason why ecommerce players get into their own delivery logistics apart from handling COD orders is working capital requirements. Logistics companies can take anywhere between a 5 days to 15 days to remit the cash collected on delivery to the ecommerce players and that robs them of working capital.”

17GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 16

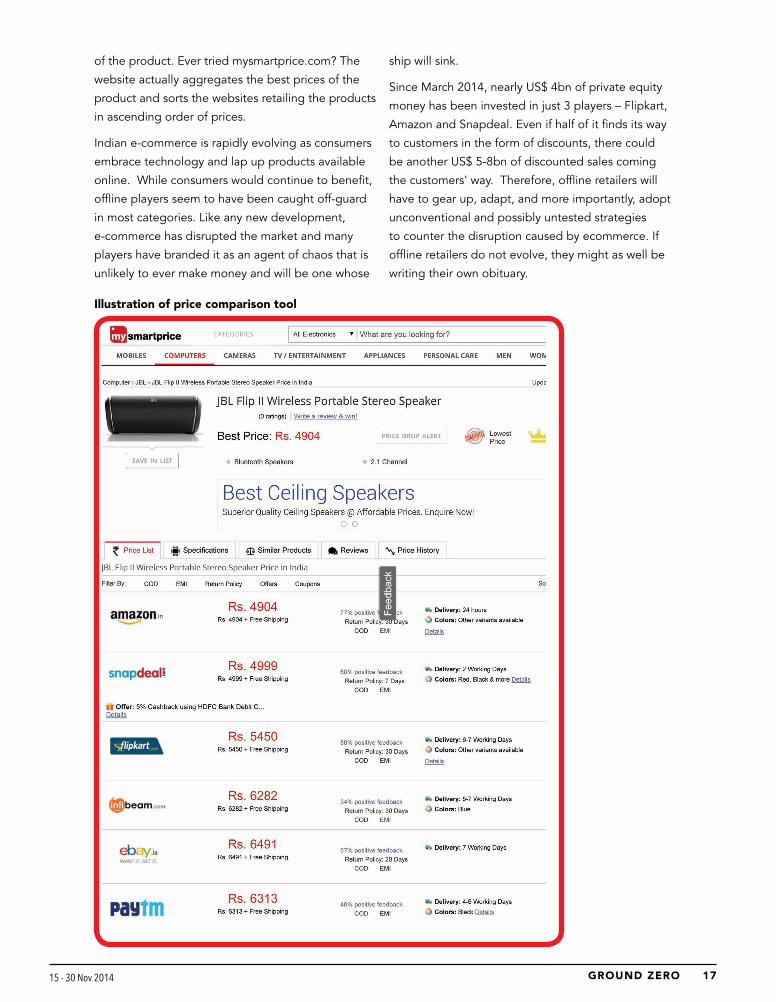

of the product. Ever tried mysmartprice.com? The

website actually aggregates the best prices of the

product and sorts the websites retailing the products

in ascending order of prices.

Indian e-commerce is rapidly evolving as consumers

embrace technology and lap up products available

online. While consumers would continue to benefit,

offline players seem to have been caught off-guard

in most categories. Like any new development,

e-commerce has disrupted the market and many

players have branded it as an agent of chaos that is

unlikely to ever make money and will be one whose

ship will sink.

Since March 2014, nearly US$ 4bn of private equity

money has been invested in just 3 players – Flipkart,

Amazon and Snapdeal. Even if half of it finds its way

to customers in the form of discounts, there could

be another US$ 5-8bn of discounted sales coming

the customers’ way. Therefore, offline retailers will

have to gear up, adapt, and more importantly, adopt

unconventional and possibly untested strategies

to counter the disruption caused by ecommerce. If

offline retailers do not evolve, they might as well be

writing their own obituary.

Illustration of price comparison tool

19GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 18

T H E C H I N E S E E C O M M E R C E M A R K E T

Lessons from Alibaba for Indian retailers – offline & online

Alibaba Group’s FY14 GMV was more

than Amazon’s and Ebay’s combined

GMV (US$ 158bn). The group sold a

GMV of US$ 296bn, which is nearly

60% of the overall Indian retail market. The com-

pany enjoys EBITDA margins of 48% (FY14) while

Amazon made operating margins of just 1% and

Ebay made 21%. It is pertinent to highlight that

Alibaba operates as a pure ecommerce facilita-

tor while Amazon is a B2C player. Also, so far,

Alibaba has had lesser competition than others

have had in markets outside China; so it has

benefited from operating leverage on the scale it

has achieved.

The Chinese ecommerce giant also shares its

name with one of the famous Arabian Nights fa-

bles – Alibaba and the 40 Thieves. The Indian mar-

ket may turn out to be more competitive than the

Chinese one (in fact, it already is) and the chase for

the consumers’ wallet share may well hold some

yet untold lessons for the entire retail space — not

just its subset, the ecommerce industry.

The Chinese Ecommerce Market

Internet users in China grew from 298mn (23% of

China’s total population) in 2008 to 618mn (46%)

in 2013, according to CNNIC, the administrative

agency responsible for internet affairs under the

Ministry of Information Industry of the People’s

Republic of China. The agency reckons there

were 302mn Internet shoppers in China in 2013,

representing 49% of its total internet users. Mobile

Internet population ( Dec 2013) 618mn

Online shoppers (Dec 2013) 302mn

Broadband Accounts 130 mn

Mobile Internet user 500mn

Size of e-tailing market ($ billion) $190–$210

E-tailing as % of retail 5-6%

Marketplaces’ share of e-tailing (%) 90%

C2C’s share of e-tailing >70%

Biggest product category Apparel

Mobile commerce’s share of e-tailing 2%

Smartphone penetration in population 10%

Coverage of next-day delivery by major express delivery companies

Mostly in Tier 1 and Tier 2 cities

Cash on delivery by independent B2C Common

Third-party payment systems/bank cards Majority

Dynamics of the Chinese e-com market

China online retail market: category break-up

(USD$ mn) Amazon Ebay Alibaba

Revenue 74,452 16,047 8,583

EBITDA 3,998 4,771 4,351

Net Profit 274 2,856 3,826

ROE (%) 3.1% 12.8% 40.2%

GMV 100,000 83,330 296,000 Source: Company, Media reports

Operating metrics

Source: McKinseySour

ce: C

NNIC

, McK

inse

y Glo

bal I

nstit

ute

anal

ysis

19GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 18

shoppers will bypass the conventional mode of

internet purchases and make it more convenient for

purchasing online. China’s mobile internet user base

reached 500mn as of December 31, 2013, according

to CNNIC. Smartphone shipments in China reached

351mn in 2013 and will exceed 435mn in 2014,

according to projections by IDC (International Data

Corporation). Market research company iResearch

believes that online shopping, which represented 8%

of China’s total consumption in 2013, is projected to

grow at a CAGR of 36% from 2013 to 2016, as more

consumers shop online and e-commerce spending

per consumer increases.

Tapping the opportunity in smaller towns and

cities

According to Euro monitor International, the top-20

offline retailers in China had a combined market

share of approximately 11.6% in 2013 vs. 40% in

the United States. This sort of fragmentation in

the market is favourable for creating a large online

marketplace. For China too (like in India), the online

opportunity is not restricted to its big cities. In 2012,

approximately 60% of China’s online retail sales were

in regions outside of tier-1 and tier-2 cities (National

Macro indicators of tier-1 and tier-2 cities and other regions in China

Online consumption per online shopper

The growth of ecommerce in China and Alibaba

Alibaba’s GMV has seen a breakneck speed of 56%

CAGR over 2011-14. During this period, the Chinese

ecommerce market grew by 52%. Leadership in mo-

bile commerce has played a vital role in its growth.

Alibaba is the leader in mobile commerce in China in

terms of mobile retail GMV, with mobile GMV trans-

acted on its China retail marketplaces accounting for

86% of the total mobile retail GMV in China (in the

three months ended June 30, 2014, according to

iResearch).

Bureau of Statistics of China).

In addition to the 35 tier-1 and tier-2 cities that have

populations of over 1 million each, there are 92

other cities with population greater than one million

as of December 31, 2012, according to the Na-

tional Bureau of Statistics of China. In these smaller

cities and towns, China’s offline retail market faces

significant challenges due to few nationwide brick-

and-mortar retailers, an underdeveloped physical

retail infrastructure, limited product selection, and

inconsistent product quality.

According to Euro monitor International, the top-20 offline retailers in China had a combined market share of approximately 11.6% in 2013 vs. 40% in the United States.

Sour

ce: M

cKin

sey

Sour

ce: M

cKin

sey

21GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 20

Alibaba’s mobile monetization

Taobao (similar to Amazon, C2C retail) and Tmall

(sells branded goods, B2C retail) are Alibaba’s retail

market places — they generated revenues of RMB

500bn for Q1FY15 and RMB 1.83tn in the 12 months

ended June 2014 (GMV of US$ 296bn). These

marketplaces contributed to 82% of Alibaba’s FY14

The gateway to Alibaba’s treasure – Taobao and Tmall

revenues. Their revenue model is primarily marketing

fees and commission, which complement each other.

For example, Tmall sources a significant amount of

buyer traffic from Taobao’s marketplace, thereby

substantially reducing its customer acquisition costs.

Sellers on Tmall may acquire buyer traffic through

Taobao Marketplace Tmall Juhuasuan

Local Sellers

– Pay for performance

marketing fees: bid for

key words

– Display markeing fees:

bid for display position

– Taobaoke commis-

sions: using Alipay

– Storefront fees

– Pay for performance

marketing fees

– Display markeing fees

– Taobaoke commis-

sions

– Commission

– Pay for performance

marketing fees

– Display markeing fees

– Taobaoke commissions

– Commissions

– Placement fees: purchase

of promotional slots

Local SellersTmall Merchants Tmall Merchants Tmall

Alibaba‘s revenue model

Alibaba’s GMV and mobile penetration

Sour

ce: C

ompa

ny, P

hilli

pCap

ital R

esea

rch

Sour

ce: C

ompa

ny, P

hilli

pCap

ital R

esea

rch

21GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 20

Tmall’s website and a glimpse of brand stores listed on it

online marketing services displayed on Taobao’s

marketplace.Taobao means search for treasure in

Chinese. This marketplace is a free platform for

buyers to explore and discover products and sellers

to establish a low-cost online presence. According

to iResearch, Taobao was the number one C2C mar-

ketplace in terms of gross merchandise volume in

China in 2013. Major physical-product categories on

Taobao’s marketplace include apparel and accesso-

ries, electronics and appliances, home furnishings

and maternity and baby products. The substantial

majority of products listed on Taobao consist of new

merchandise. During the twelve months ended June

30, 2014, 173.3 million active buyers, or approxi-

mately 62% of all active buyers on China’s retail mar-

ketplaces, were located outside of tier-1 and tier-2

cities, while approximately 4.5 million sellers, or 52%

of total active sellers on China’s retail marketplaces,

were located outside of tier-1 and 2 cities.

Tmall is an online platform featuring brands and

retailers who operate their own stores on the Tmall

platform with unique identities and look and feel,

enabling sellers to control their own branding and

merchandising. According to Alibaba, the strong

buyer traffic, autonomy, and flexibility for sellers to

operate their own stores, and the fact that Tmall

23GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 22

Alibaba (FY14)

JD.com (CY13)

GMV ($ Bn) 270 20.7

No of Employees (as on 31 March 2014) 22,072 50,122

EBITDA % 50.7% (0.4%)

Capital Employed ($mn) 13,103 1,627

RoE 40.2% NA

Comparison between Alibaba and JD

Amazon China 24

Ebay China 1,081

JD.com 34

Taobao 2

Website traffic ranking of popular e-com-merce websites

does not operate a direct sale business to compete

for customer traffic, makes it the platform of choice

for brands and retailers.

Major physical product categories on Tmall include

apparel and accessories, electronics and appliances,

home furnishings, home appliances and materni-

ty and baby products. Sellers on Tmall and Tmall

Global pay commissions based on pre-determined

percentages (0.3% to 5% depending on the product

category) of GMV for transactions settled through

Alipay. Sellers also pay an annual upfront service fee,

up to 100% of which may be refunded depending

on sales volume achieved by the seller within each

year.

For all of Alibaba’s success, Indian ecommerce

companies seem to follow JD.COM

Alibaba’s next biggest (though distant) competitor is

JD.com, China’s largest online direct sales company.

JD clocked a GMV of US$ 20.7bn (63% electron-

ics) in 2013 – less than 10% of Alibaba’s GMV. The

fundamental difference is that JD procures and

manages its own inventories, sells products directly

to consumers online, and provides delivery and af-

ter-sales services. It is modelled on Amazon with the

addition of making the last-mile delivery itself. It had

over 50,000 employees in April 2014 and nearly half

of those were for delivery of products. JD reported

an operating loss of US$ 96mn on a turnover of US$

11.45bn for the calendar year 2013. Interestingly, its

gross margin increased from 8.4% in 2012 to 9.9% in

2013, primarily due to the increase in net revenues

from services and others attributable to its online

marketplace and higher share of general merchan-

dise.

JD is an important reference point for the Indian

context, says an expert. He explained that players

such as Flipkart and Amazon are replicating the JD

model of last-mile delivery. It possibly explains why

Flipkart may end up with 25,000 employees on a

US$ 3bn GMV for FY15. The expert gives further in-

sight into Amazon’s strategy in India. He says that in

the US, Amazon doesn’t make the last-mile delivery

— however, for the Indian market it seems to have

picked up the strategy from JD and is building its

own delivery network.

But why is there no model like Alibaba? An ex-

pert explains that, “Taobao, a C2C market place

like Ebay, succeeded in China because of its huge

manufacturing base and export market. In a C2C

model, even an individual can sell his product on

the platform unlike in a B2C, which restricts itself

to vendors and businesses.” Alibaba succeeded

because it connected Chinese suppliers with over-

seas buyers. China has a huge manufacturing base

and most households manufacture something — it

could be toys, furniture, sports goods, just about

anything. Hence there are multiple sellers that have

a large variety of products, thus attracting buyers

to the marketplace. Taobao is the platform for such

producers and buyers. Our expert suggests that in

India, software is our biggest exports and we need

to have a strong manufacturing base for an Indian

Taobao to evolve.

Alibaba’s competitors misread the market and went

with the wrong business model. What went wrong

for Ebay and Amazon in China? The expert ex-

plains that Ebay failed to understand local market

demands and payment systems, which Taobao

leveraged on. Alipay, Alibaba’s payment solutions

platform is fundamental to its success. For a market

where cash-on-delivery payments are high (33% for

JD in 2013), Alipay, which functions as an escrow

account for buyers and sellers, changed the game.

Buyers preferred CoD, whereas sellers were unwill-

ing to ship the products until they were assured that

Sour

ce: C

ompa

ny, B

loom

berg

, Phi

llipC

apita

l Res

earc

hSo

urce

: Ale

xa

23GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 22

The Indian ecommerce market is smaller at about

US$ 4bn and is more competitive. In the Arabian

Nights, Alibaba had to contend with the 40 thieves

vying for the treasure. The Indian ecommerce market

is no different. While almost every player aspires to

be the Indian version of the Alibaba Group, there are

many learnings for the players in Indian market, both

online and offline.

n Competition – There are over 30 active ecom-

merce sites vying for consumers’ wallets and

models are evolving. The market is big, un-

tapped, and more importantly, open. Amazon

was nowhere in the picture till 2013 and has

rapidly scaled up operations in India, adopting

a marketplace model, something it hasn’t been

able to do in China.

n Alibaba is a pure market place – As highlight-

ed in the earlier section, the Indian market has

many hybrid models or companies that have

evolved from hybrid models. Snapdeal and

Ebay seem to be pure-play marketplace models.

Amazon is reported to have an indirect stake in

some of its vendors. In any case, all Indian com-

panies are already building up scale. Alibaba,

with US$ 300bn GMV had around 26,000 em-

ployees in China as on June 2014. Flipkart (with

a US$ 1bn GMV in FY14) has 13,000 employees

and plans to add another 12,000 employees in

FY15. Snapdeal has around 1,300 employees

and plans to double the headcount soon.

n Mobile is the way ahead – Access to smart-

phones bridges the gap of internet availability

to India’s 150mn (and growing) mobile internet

users just as it is has in China. Businesses have

to evolve beyond ecommerce – they have to be

ecommerce ready - be it mobile websites (web-

sites which are optimised for viewing in smart

phones) or mobile apps. The share of Jabong’s

mobile transactions increased from 4.4% in

the first quarter of 2013 to 27% in the second

quarter of 2014, while its monthly average visits

using mobile devices increased from 1.8 million

to 13.5 million over the same period.

n Striking similarities – India and China both have

underpenetrated retail markets. The opportunity

becomes even larger in tier-3 cities and beyond.

Technology is the new and one-stop store for

these locations. Opening stores rapidly is passé

— reaching through technology is the future.

n The competition for offline is only going to

intensify — Alibaba’s success has increased

investors’ risk appetite to invest in ecommerce

companies in India. And these investors are will-

ing to back some players in the hope of winner

takes it all. This means funding (that has already

touched US$ 4bn in 2014) will only increase.

Indian smartphone penetration

Lessons for the Indian market – China possibly didn’t have the 40 thieves but India sure has

payment was forthcoming. This lack of trust posed

a stifling challenge for the development of online

commerce in China. Alipay introduced its escrow

service as a solution to this problem. Alipay is Aliba-

ba’s password to the treasure cave.

Amazon entered China by acquiring joyo.com;

however, it faced integration issues and this perhaps

explains why it set up its business from scratch in

India instead of acquiring an existing entity.

Sour

ce: E

urom

onito

r Int

erna

tiona

l

25GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 24

Necessity driven by competition, but is it for every offline retailer?

B U I L D I N G A N O M N I C H A N N E L

In developed markets such as the US, ‘om-

ni-channel’ was a response to the threat posed

by low-cost online retailers. Retailers such as

Macy’s, John Lewis , and Burberry successfully

implemented an omni-channel strategy.

“Omni channel is a multi-channel touch point.

It combines brick and mortar with virtual chan-

nels - be it the website or mobile,” says Sanjay

Chakravarti, CFO, Shoppers Stop. Both formats,

i.e., brick and mortar and virtual, are seamlessly

synchronised in omni-channel retailing. If the cus-

tomer doesn’t get a particular product in the store,

he or she can browse for it on a kiosk or on the

website/app and complete the order.

What is omni channel retailing?

Omni-channel illustration

“Customers are becoming increasingly agnostic

to the channels they are buying from. It’s going

to be an integrated market, but the reality is that

we haven’t reached there yet in India,” says an

industry expert. The industry participants that we

interacted with, including leading ecommerce

practitioners (each involved in some major initia-

tive) concur that going forward, omni is the future.

When asked whether they were already behind

the curve, most of them said that it’s just the

beginning. Mr Rakesh Biyani, Jt MD Future Retail,

says, “We are going online because the custom-

er wants this. Businesses have to fundamentally

adapt to technology. We initiated the process

over a year ago, when the buzz in Indian online

was nowhere near what it is today.” He goes on

to say that, “consumers’ perception of technol-

ogy and service has undergone a change and it

is only evolving. Consumers today want to shop

from anyplace and anywhere, and interestingly,

are willing to wait for the product. Online play-

ers haven’t triggered any decision making for us.

The reason we adopted omni-channel is because

we had already migrated our operations to run a

centralised warehouse/distribution centre, assort-

Why Omni?

Mr Rakesh Biyani, Jt MD Future Group, says, “We are going online because the customer wants this. Businesses have to fundamentally adapt to technology. We initiated the process over a year ago, when the buzz in Indian online was nowhere near what it is today. ”

25GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 24

ment approach, and back end — it just happened to

coincide with the noise around ecommerce. We felt

the need to invest in technology to move to the next

leg.”

“Omni channel makes sense for any brand which

has a large retail presence”, says Mr Vijay Basrur

of Raymond. The 89-year old brand has been one

of the few Indian brands to have launched its own

ecommerce venture Raymondnext.com. The Aditya

Birla group has launched trendin.com which retails

its brands including some of India’s largest brands

such as Louis Philippe. But no one is anywhere close

to creating a great shopping experience, says Mr

Bawankule of Google.

Nevertheless, Omni Channel has multiple benefits

when executed well. Even in the developed markets

(US and UK) 85-90% retail is still offline. The reality

is that most of the retail is anchored around physical

assets of manufacturing, product strategy, stores,

and distribution set up. Omni-channel brings real

assets to compliment online stores so that they don’t

eat into each other’s sales but rather, complement

each other — sales strategies under omni-channel

include click-and-pick, reserve the product, and

shipping from the store instead of the distribution

centre.

A solution to one of the biggest challenges for

retailers – Inventory

A brick-and-mortar retailer holds inventory in the

store as well as at the distribution centre (DC). The

Advantages of Omni Channel

assortment in the store is limited due to space con-

straints. The supply chain runs once a day to twice a

month depending on the type of store (format, loca-

tion). Hence, there is limitation to turn the inventory

better. Omni-channel gives access to the product

(listed on website/app) in the system, store as well

as DC, to a customer — it also does this to custom-

ers who are beyond the (physical) catchment of the

store and possibly where there are no stores. Thus,

it helps improve the stock turns. Mr Biyani offers a

deeper insight into this. He explains that, “With the

omni-approach and by delivering the product to the

consumer’s home, the replenishment system chang-

es to a certain extent. We can pick a single product

from the system (be it a store or the DC) to fulfil a

customer’s order. Thereby, the space constraint in

the store reduces and we can offer twice the assort-

ment (variety) by cutting the depth (number of piec-

es) and making less of the same product available.

Thus, we can improve the store performance.”

Logistics and warehousing

Logistics is easier for a store network. “Shipping

from a store is cheap,” says Mr Vinay Bhatia, Head of

Ecommerce & Customer Loyalty Program, Shopper’s

Stop. Mr Basrur of Raymond concurs and says,

“Delivery times are dramatically cut short and are at

lower costs as deliveries can be made by the nearest

store as there are logistic partners in place. From

logistics perspective, there will be cost savings. If

the product is there in the city, then it will get dis-

patched locally.”

Sale of a product is piece by piece (a shirt, a dress, pair of shoes) basis but replenishment in the store is in batch-es (economic order quantity). If a single product can be picked to fulfil an order made online then the same capability can be created for the store. The store is also a customer. Extending this capability to the top-performing stores we can maximise the assortment in these stores and use the others to take orders (through website or kiosks or through tablets that showcase the entire range), creating a hub-and-spoke model. This is known as the endless aisle concept in which shelf space is extended to the brand’s full catalogue of products.

Omni-channel brings real assets to compliment online stores so that they don’t eat into each other’s sales but rather, complement each other.

27GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 26

Most retailers would be keen to popularise click-

and-pick, which essentially means that the customer

can buy online and opt to collect it from the nearest

store. It helps the customer get the product quicker

— more so if it’s already in a nearby store. A custom-

er is also likely to make more purchases when he or

she comes to the shop to collect the order. And of

course, there are no shipping costs.

While click-and-pick would be an ideal scenario, it is

a function of reach. Not all chains are present across

most places in India, and the reality is that to satiate

demand from locations where there are no stores or

distribution centres, third-party logistics will have to

be used. Even for orders from locations where stores

are present, retailers may have to use third-party

logistics to fulfil orders until the time click-and-pick

gets more popular (may have to incentivise the

customer). However, Mr Biyani believes that the ex-

isting employees in a store can be used to fulfil the

delivery to customers in location that have stores.

The only incremental cost could be the addition of a

few 2-wheelers to facilitate local delivery.

Going omni channel, results in warehousing efficien-

cies and lower costs. Logically, by more sweating

of the store inventory, warehousing needs should

reduce. However, it depends on the stage of the

business and the format, i.e., brand or third-party

retailer, says Mr Basrur. Brands have multiple distri-

bution channels and hence will have a centralised

inventory for its online business. So initially, ware-

housing capacity will be high for brands — this will

reduce as they go omni and the stores come into

play. Departmental stores are enablers and hence

stock more inventories in the store unlike brands as

they have longer and diverse supply chains.

Particulars Lifestyle Panta-loons

Shoppers Stop

Trent Central

Tier-1 71% 44% 54% 39% 38%

Tier-2 & 3 29% 56% 46% 61% 62%

Total stores 42 86 71 80 29

No. of cities 26 47 32 53 15Source: Company, PhillipCapital Research

Geographical dispersion of leading departmental stores in India

Capturing more wallet share

Mr Bhatia of Shoppers Stop states the real ben-

efit from this strategy is from increased customer

spreads as the assortment is wider. Internationally,

there is enough data to show that omni-channel cus-

tomers spends are twice single-channel customers’.

According to IDC, multi-channel shoppers spend on

an average 15-30% more with a retailer than some-

one who uses only one channel — and omni-channel

shoppers will spend 15-30% more than multi-chan-

nel consumers.

Mr Biyani of Future Group explains how having a

wider variety helps. He gives us “The Dinner Set”

example:

Typically in a store we can offer 4-20 designs due to

space constraints. But I can have 50 designs in the

backend. So a customer may see some colours of a

design on display and others on a screen or tablet

in the store. If the piece is not in the store, it will get

shipped from the backend where the customer will

have the option of picking it up from the store or get

it delivered home.

Mr Basrur of Raymond explains how Burberry has

optimised this channel. “One can walk into any

Burberry store and the customer can see the entire

collection. One can select the SKUs online and

Burberry can make the SKU available at the near-

est store. Burberry has almost all of its collection

in all its stores in a city. Since it is a luxury brand it

doesn’t have too many SKUs – this helps.”

To go omni, brands and retailers have to make

changes in the backend, technology, and above all,

their strategic mind-set. Mr Bawankule of Google

surmises, “Brick-and-mortar players have to make

technology investments and create internet plat-

forms. Importantly, it (omni) has to be treated as a

new business or a new store in a new location.”

What will it take to go omni?

27GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 26

Integrating the existing offline business with online is

a three-part process:

1. Going digital/setting up a website, thereby

allowing consumers to buy online. A brand can

also sell without a proper back-end. Fila sells

online in India through a distributor. Managing

website traffic is a function of technology capa-

bility. Most companies today rely on amazon web

services or cloud services or hosted solutions

for managing this. Therefore, scaling up and

handling increase/spikes in website traffic is not a

major challenge.

2. Centralisation of data/finance. Most of the offline

retailers have IT systems that are tuned for brick-

and-mortar operations. Once they start selling

online, there has to be synchronisation and data

has to be viewed real-time as customers buy

across channels at different times of the day. That

data has to be integrated into in the company’s

IT system so that it knows where the stock is.

Another aspect is stock movement — inventory is

in the store and as it gets sold it has reflect in the

system real-time so that a consumer shopping

online will know if the stock is available or not at

any given point of time.

How is it done? A master data management

(MDM) layer is used to integrate old systems. It is

essentially a middleware that talks to legacy sys-

tems sitting in the stores. The integration is not

an easy process and it is not real time to begin

with. ERP, designed for stores, was used for end-

of-the day processing (e.g. stock taking).

3. Going omni and servicing the customer from the

nearest store.

Mr Bawankule of Google surmises, “Brick-and-mortar players have to make technology investments and create internet platforms. Importantly, it (omni) has to be treated as a new business or a new store in a new location.”

Inventory Inventory

Pricing

WebSphere

Enterprise

Service BUS

(WESB)

Mediation

Module

Pricing

Order Order

Promotions Promotions

Web channel

online Store

Direct Calls

MIDDLE WARE

FR

ON

T-E

ND B

AC

K E

ND

WebSphere

Commerce

Sterling Order

Management

JMS Queues

Call Centre Store

Illustration of the front end, back end and middleware for omni channel

Sour

ce: I

BM

29GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 28

While middleware is an important cog in the

omni-channel wheel, Future Group opted for the

alternative, i.e. seamless integration (no middle layer

between existing systems and website) using Hybris,

a SAP enterprise. A seamless interface using Hybris

is possible if one is on SAP. However, not everyone

is on SAP and many brands say that it is expensive

in the context of their size and operations. However,

for an entity like Future Group, when the number of

SKUs is high, complexities of integration increase —

it deals with over 40,000 SKUs (Shoppers Stop deals

with 2,500), seamless integration is preferred over

middleware. The others have the option of choosing

different vendors for middleware and the front-end

— e.g., IBM Websphere (for front end), Oracle ATG

(for front end), IBM0 sterling management (middle-

ware).

Warehousing investments

Most brands have large warehousing capabili-

ties as they deal with multiple channels – dealers,

departmental stores, franchisees. However, these

warehouses may not necessarily support sin-

gle-piece-picking to satisfy orders from distribution

centres (DCs). They need to do so as retailers go

omni and establish an online presence. Online pres-

ence can be established even before the company

goes omni and to service this one would need a

new-age DC that can fulfil single-piece picking.

Therefore, brands may make short-term (outsource)

investments in warehousing. For brands, the

warehousing requirement will increase in the short

term, as the online channel will be serviced through

new-age DCs; but as stores come into play to fulfil

orders, the requirement will come down. However,

for departmental stores such as Shoppers Stop, most

of the stock is in store, and its warehousing require-

Macy’s omni-channel in a nutshell: Macy’s website installs 24 different tracking cookies on a visitor’s browser. Its TV ads (inci-dentally, featuring teenage pop sensation Justin Bieber) urge people to download its mobile app, which tells them which of the chain’s stores is closest to their location. Once customers are inside the store, they can use the app to get customer reviews and can also scan the QR code to watch videos, visit URLs, and find out more about a product or a promotion for anything — a pillowcase or a pair of shoes. Online orders now ship from the backrooms of 500 Macy’s stores that this year began acting as mini distribution centres.

Source: Beyond the check-out cart, MIT Technology Review

ment will only increase when online crosses 10-15%

of their topline; therefore, in the short term, it won’t

need additional investment for warehousing, says Mr

Bhatia of Shoppers Stop.

John Lewis, UK’s largest departmental store, faced

competition from online players in the UK and

subsequently invested in going omni. However,

the journey wasn’t easy as it integrated its stores as

well as Waitrose stores as fulfilment centres. John

Lewis offers added incentives such as free Wi-Fi so

customers can check out prices — it has a policy of

never knowingly offering a price that is higher than

a national high-street competitor. The extended

reach of Waitrose stores (over 300) is an important

factor in John Lewis’s successful implementation of

omni-channel.

Things John Lewis did in chronological order:

2009 - 35% increase in the lines offered on the web-

site; started click and collect

2010 - Increased the number of lines available and

started express delivery.

2011 - Increased the number of products sold

online. Invested further in the development of dis-

tribution facility. Extended services such as Click &

Collect to all 29 John Lewis branches.

2012 - Online trade fully integrated into the John

Lewis multi-channel operations. At the year end,

‘Click & collect’ was available in all 35 John Lewis

shops and 94 Waitrose branches. Two-thirds of

its shops had free Wi-Fi to enable customers to

check prices as they shop. Launched over 30 new

John Lewis Case Study

29GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 28

brand introductions, new own-brand ranges, and

more designer collaborations. There was a £ 34.1m

decline in profits as a result of the decision to

ensure there was absolutely no compromise on

quality, service or value for customers.

2013 - Nearly two thirds of all transactions involved

customers visiting both shops and online channels.

Click & collect, available in all 39 John Lewis and

193 Waitrose outlets, was a key part of this change

in shopping behaviour. Orders almost doubled

year-on-year, with 43% of purchases collected from

Waitrose branches.

John Lewis’s share of online sales in revenue-mix and LTL growth

John Lewis’s online sales growth

2014 - The ‘my John Lewis’ membership card was

launched with 500,000 members joining in just four

months. Click & collect grew by 57%, with the con-

venience of being able to pick up from Waitrose be-

ing particularly appreciated. Collect+ (offering click

and pick at corner shops and petrol stations) was

successfully launched. Visits from phones and tablets

accounted for 50% of traffic to johnlewis.com.

China may be a better example than US to gauge

the potential of omni-channel in India

Most players and brands seem to believe that going

omni is the way forward; but then, the dynamics in

India are very different from the developed world.

Retailers who implemented omni-channel strategy in

the US and UK have successfully evolved and coun-

tered ecommerce. However, the most fundamental

aspect for omni-channel is reach and stores. In the

US and UK, organised retail is 80% of the market,

and per-capita availability of retail assets (i.e. stores)

is amongst the highest in the world. This made it

easy for retailers and brands who decided to adopt

omni-channel, as they are well spread out and logis-

tically offer more convenience to customers. The

reach of branded or departmental stores in India is

nowhere near what it is in developed countries.

Hence, departmental stores such as Macy’s in US

and John Lewis in UK have been successful — both

were sizeable (high share of organised retail) when

they went omni.

Availability of retail space worldwide (per capita in sq meters)

Sour

ce: C

ompa

ny, P

hilli

pCap

ital R

esea

rch

Sour

ce: C

ompa

ny, P

hilli

pCap

ital R

esea

rch

Sour

ce: E

urom

onito

r Int

erna

tiona

l

31GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 30

E C O M M E R C E V S . P H Y S I C A L S T O R E S

The battle has just begun - discounts and funding to continue

The battle between ecommerce and

offline retailers in India intensified after

Flipkart’s big billion day sale, where

the online retailers faced allegations of

undercutting and selling below costs. Ecommerce

has been branded as a discounting channel by

most of its offline peers. The availability of FDI

(foreign direct investment) in the form of private

equity to ecommerce players through compli-

cated corporate structures is another bone of

contention for offline players. Mr Biyani of Future

Retail says, “Online market places are funded

by foreign money and Indian players don’t have

access to it.”

But not everyone agrees with this. “Online is

just another competition, but the way you react

to it is different,” says Mr Bawankule of Google.

“Everyone is saying price is the bogie, but if that

were the only case then physical retail should

close down as it would lose significant business

to online. Ecommerce players also have to make

a strategy to acquire customers, then retain them

using loyalty, pricing, service, etc.”

A catchment area of an offline retailer can be easi-

ly disturbed even in physical retail when a com-

petitors sets shop there or for that matter in many

“Online is just another competition, but the way you react to it is different,” says Mr Bawankule of Google.

Screen grabs of Raymond fabrics from Snapdeal

Raymond fabrics sold by re-sellers on Snapdeal

31GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 30

Similarities between online and offline

In many ways, the offline competition from unorgan-

ised players is spilling over into online. For example,

any MBO (multi-brand outlet) can sell online.

The physical world will mirror itself on the online

world. The difference is that the customer will come

to the online store instead of the offline store.

The share of national apparel brands online is not

significant and it is the same in the offline world,

even though these brands have existed for years.

Mr Basrur from Raymond says, “It is just that the

unorganised segment has got a bit more authenticity

selling online.” A significant portion of the turnover

of online players such as Myntra and Jabong will be

from smaller brands (which in the offline world would

pass off as unorganized) and private labels, says an

industry observer.

Mr Basrur adds, “Doing business online has its own

set of costs — warehousing, logistics. The advan-

tage is that it has the ability to showcase the entire

inventory to the customer”. But customer acquisi-

tion online is the most challenging part. Just as for

physical stores, a brand or retailer tries to draw the

customer from another brand or store by advertising

or through new stores and offers, online players have

to draw customers. They also incur costs for market-

ing (website), advertisement, and search engine op-

timisation. In fact, customers have high expectations

from online players such as discounts, free deliveries,

and returns. Thus cost of doing business online is

mirroring offline. Online is more efficient only if there

is vast product range.

Inventory challenges exist both offline and online.

Aggressive expansion by offline players to expand

their retail footprint resulted in high inventory and

debt levels. Some large ecommerce players face

these issues too.

However, all said and done, brands need online

channels as much as online players need them. A

brand cannot survive only on own exclusive brand

outlets — most already depend on departmental

The physical world will mirror itself on the online world. The difference is that the customer will come to the online store instead of the offline store.

such catchments. The retailer (rather than reacting

and complaining), then has to respond by chang-

ing his strategy (product mix, promotions etc.) to

counter competition. Therefore, businesses have to

evolve and respond to competition rather than react.

Lesser known brands retailed on Amazon.in...

33GROUND ZERO GROUND ZERO 15 - 30 Nov 2014 15 - 30 Nov 2014 32

stores. Similarly, a brand cannot grow only using its

own website — they will need to use major ecom-

merce players as they offer reach into 2/3-tier cities,

which will help brands penetrate deeper without

investing in stores.

The offline marketplace is getting replicated

online

An industry expert explains the disruptive aspects

of ecommerce in the context of physical retail —

he says ecommerce is disruptive on two counts

— technology to reach the consumer anywhere

and disintermediation. Explaining further, he says,

ecommerce has disruptive power as it can reach any

customer, anywhere, and anytime. Therefore it can

threaten the fundamentals of the offline business-

es — for example, books chains across the world

have been wiped out because of online sales. The

same thing is happening to mobiles. The degree of

invasion will vary and brands have to be careful how

they engage online.

There was a time when Target and Macy’s were part

of Amazon but they didn’t benefit and went their

separate ways, after which they had to build online

platforms from scratch and play catch up. The sec-

ond aspect is disintermediation - if there are three

channel partners sharing total 30% margin, then by

reducing the chain, the customer benefits. But it kills

the physical stores. Departmental stores and small

Jabong’s reach compared with the distribution of urban population in India

Source: Company, PhillipCapital research

One of Jabong’s private labels