performance of swiss private banks - the widening gap

TRANSCRIPT

Performance of Swiss Private Banks

The widening gap

25 August 2015

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

2

Agenda

WelcomeAndreas HammerHead of Corporate Communications

Economic and regulatory issues of Swiss Private BanksPhilipp RickertHead of Financial Services andMember of the Executive Committee

Performance of Swiss Private BanksChristian HintermannHead of Advisory Financial Services

Q&A

Economic and regulatory issues of Swiss Private Banks

Philipp RickertHead of Financial Services and Member of the Executive Committee

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

4

There is a gap, but why?

External Developments Response Capabilities… such as … Large Private Banks Small Private Banks• Accelerated wealth creation

Asia, US, etc.• Build onshore presence• Tailored service offerings

• Dependent on market access, limited in growth

• Equity boom, chase for yield • Lombard lending• Mortgage products

• No lending capabilities

• FX volatility & new currency pair • Structured products• Trading capabilities

• No product and trading capabilities

• Innovation in technology • Global reach for talents • Disconnected from innovation

• Regulatory changes • Knowledge and financial resources for rapid adoption & compliance

• Risk of failure is threat to capital

• CHF strength • Off-shore capabilities• FX balance revenues and

costs

• Cost in CHF, revenues in EUR

• Digitalization • Significant investments in digital transformation

• Lack of financial resources

• Tax transparency • Ability to attract tax compliant money off- and onshore, investment capabilities

• Unclear whether declared assets come back

+

-

Performance of Swiss Private Banks

Christian HintermannHead of Advisory Financial Services

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

6

Methodology and basis

Since 2006, quantitative analyses based on originary private banking database by KPMG.

Collaboration with the Institute of Business Administration from the University of St. Gallen (IfB-HSG).

The study assessed the 2014 annual reports of 91 private banks (2013: 97) representing AuM of CHF1’509 billion and 25,987 full time employees.

Approx. 70% of the 91 banks managed less than CHF10 billion in AuM in 2014. Conversely, 30% of banks managed 89% of AuM. This distribution gap would be even wider if Credit Suisse Group and UBS were included.

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

7

The widening gap

Sample by cluster (in %)

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

8

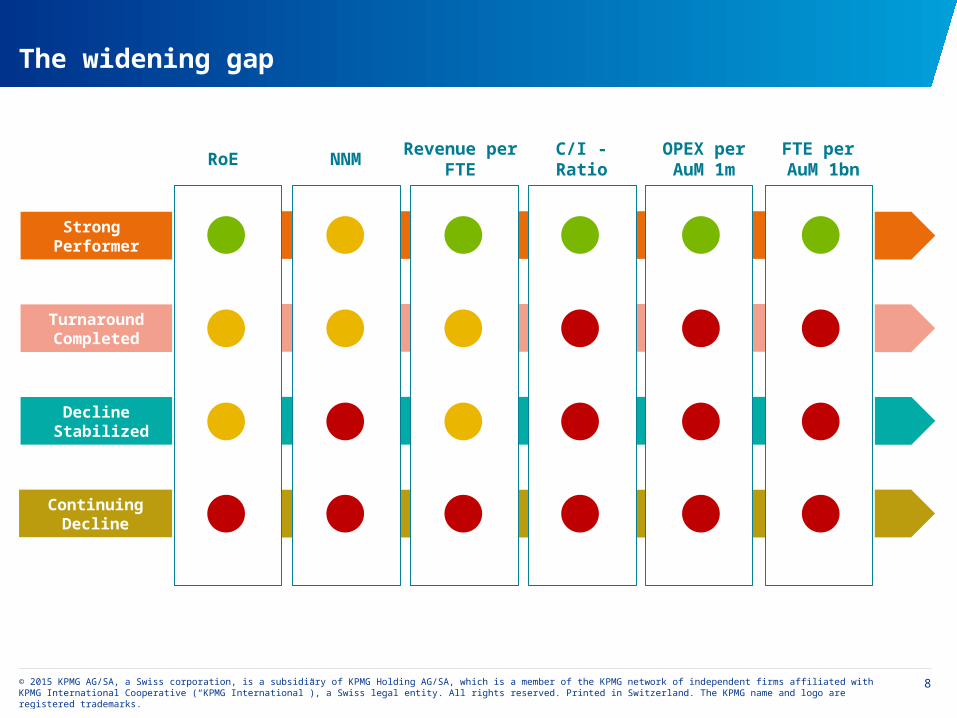

The widening gap

RoE

Strong Performer

Turnaround Completed

Decline Stabilized

Continuing Decline

NNM Revenue per FTE C/I - Ratio OPEX per

AuM 1mFTE per

AuM 1bn

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

9

Strong Performers continue to pull ahead

Ability to sustain healthy and stable profitability and RoE

Capability to grow through NNM, M&A and good performance on AuM

Despite lower net revenue margins, higher revenue per FTE, showing

greater productivity and economies of scale

Operating costs to serve CHF1 million of AuM at CHF5,000 - at other clusters

at about CHF8,000

Strong Performers’ success factors

No magic formula for the strategic success of Strong Performers. They seem to have found an optimal balance between strategic measures regarding the business model or

revenue, and those relating to the operating model or costs. May have started transformation earlier and therefore the gap to target model may have been smaller.

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

10

RoE is unsustainably low

Reported RoE remained very low at 3.5% as banks were unable to improve their performance despite the positive development of financial markets.

The proportion of loss making banks fell from 39.2% in 2013 to 28.6% in 2014, driven by less provisions for US tax program.

Median RoE of banks that made significant acquisitions between 2010 and 2013 rose by around 1.4 percentage points in the two years following the acquisition.

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

11

Significant RoE differences in 2014 by cluster and size of bank

Strong Performers with significant higher RoE in 2014, compared to the other clusters. Large banks reported higher RoE (5.4%) than small banks (2.6%), being a wider gap than 2013. The effect of extraordinary items on RoE appears significantly higher for banks in Continuing Decline compared

to other clusters.

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

12

AuM growth is market driven with insignificant NNM

No meaningful NNM has been generated since 2008 despite overall growth in global private wealth. This illustrates the erosion of Swiss private banks’ global market share.

Strong Performers and banks in Turnaround Completed reported CHF24.9 billion net inflow while the other two clusters reported net outflows of CHF17.9 billion.

In 2014, eight banks in our sample reported the closure of eight deals with total acquired AuM of CHF19.3 billion.

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

13

Positive market developments and foreign exchange effects boosted AuM in 2014

Positive performance in 2014 was mainly due to the contribution of positive equity market developments and strong appreciation of the USD.

Strong Performers have reported better AuM performance in 2014 at 7.1%, compared to 5.1% for the other clusters, mainly as a result of:

- greater proportion of client assets invested- higher proportion of deposits denominated in USD- better asset management capabilities?

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

14

Erosion of net revenue margin continues, net profit margin stable

The erosion of net revenue margins continued in 2014 by four basis points to 93bps, mainly due to the low interest rate environment and ongoing pressure on commission margins.

Gross and net profit margins were stable at 17bps and 9bps respectively, mainly due to lower provisions. Higher revenue margin no guarantee for better profitability.

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

15

Efficiency varies hugely between clusters

Net revenue per Average FTE constantly increased over the last three years after the low in 2011. Strong Performers and Turnaround Completed banks were able to lower their FTE to AuM billion ratio without

materially reducing their employee base. Banks in Continuing Decline and Decline Stabilized both experienced a decline in net revenue per average FTE

despite reducing headcount.

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

16

Cost-income ratio remains high – limited impact of cost savings measures

Cost-income ratio remained high at 81.2% as the industry was unable to reduce its cost base. In addition, the industry was impacted by increased regulatory compliance and remediation costs, including those relating to the US Tax Program.

40 banks managed to reduce their cost-income ratios in 2014. These reductions were greater than five percentage points for 21 banks (23% of our sample).

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

17

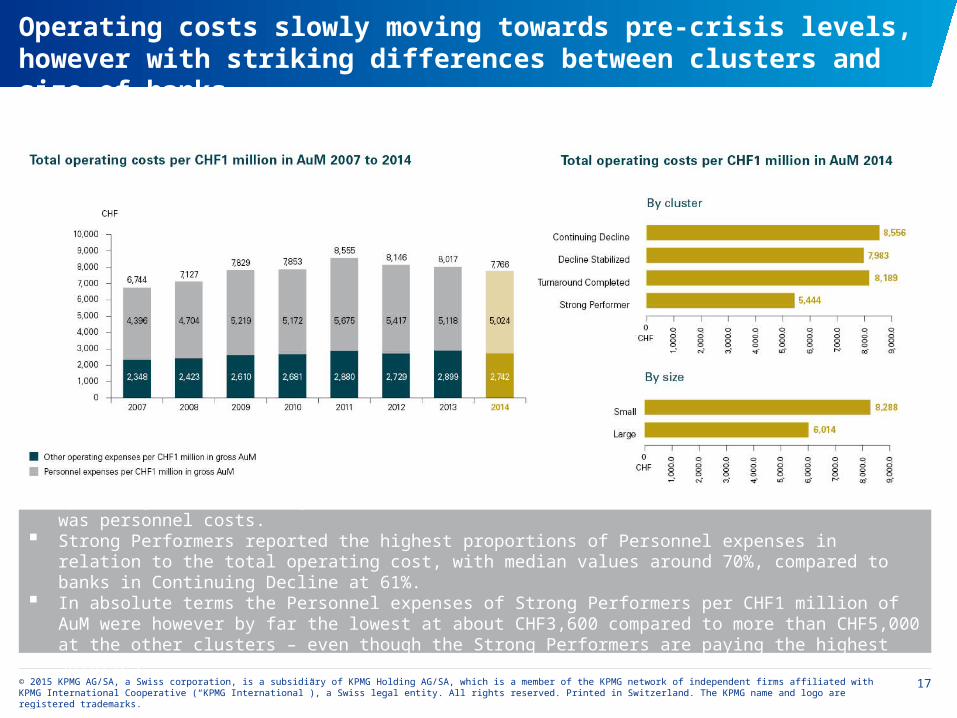

Operating costs slowly moving towards pre-crisis levels, however with striking differences between clusters and size of banks

Operating costs to manage CHF1 million of AuM were around CHF7,800, of which 64.7% was personnel costs. Strong Performers reported the highest proportions of Personnel expenses in relation to the total operating cost,

with median values around 70%, compared to banks in Continuing Decline at 61%. In absolute terms the Personnel expenses of Strong Performers per CHF1 million of AuM were however by far

the lowest at about CHF3,600 compared to more than CHF5,000 at the other clusters – even though the Strong Performers are paying the highest salaries.

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

18

Strong Performers: More efficient set-up and greater economies of scale resulting in significant lower FTEs required to serve AuM

An average of 23 FTEs is employed to serve CHF1 billion of AuM, with significant differences between small and large banks, regions and performance clusters.

Compared to 2011 the median bank needs nearly 4 FTEs less to service CHF1 billion of AuM. Economies of scale and minimum size of bank are key drivers for more efficient operations.

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

19

34% of sample banks changed CEO twice or more, but returns are far from guaranteed

Two thirds of banks changed CEO at least once in the past nine years. 48% of banks in Continuing Decline changed their CEO at least twice between 2006 and 2014, compared to 12% of Strong Performers.

There is little evidence that changing the CEO will improve the financial performance – the issues of some of the banks can not be solved just by replacing the CEO.

Out of a total 193 CEOs over the period, only eight were women. There are currently five female CEOs in office.

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

20

Flight or fight? Many of Switzerland's Private Banks seem undecided

Pressure on small banks to decide on either exiting the market or staying and changing their business and operating models intensified in 2015.

The discontinuing of the EUR/CHF minimum exchange rate as well as the negative interest environment will hit profitability further.

Additional regulations including Automatic Exchange of Information will continue to increase regulatory costs, absorb more management time and result in asset outflows and possibly lower revenue margins.

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

21

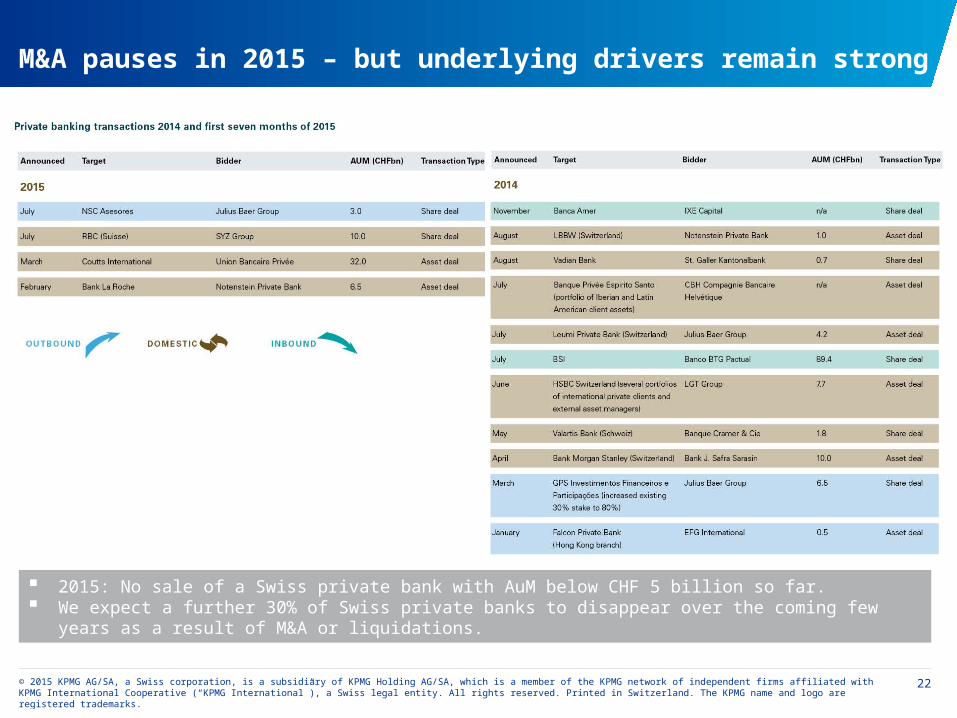

M&A pauses in 2015 – but underlying drivers remain strong

Following a very active 2014, a slowdown in M&A activity in the first seven months of 2015 yielded only four Swiss private banking transactions.

Wholly-owned Swiss subsidiaries of foreign banks are clearer on their direction, with many pursuing an exit from the Swiss market (2015: Coutts, RBC).

Supprisingly not many sellers in the market, buyers are wary of legacy risks.

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

22

M&A pauses in 2015 – but underlying drivers remain strong

2015: No sale of a Swiss private bank with AuM below CHF 5 billion so far. We expect a further 30% of Swiss private banks to disappear over the coming few years as a result of M&A or

liquidations.

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.

23

Key messages

Strong Performer continue to pull ahead

Overall RoE level increased in 2014, however still unsustainably low with significant differences across the clusters and by size of bank

AuM growth in 2014 was driven by the positive market and foreign exchange trends while NNM was insignificant

Flight or fight? Especially small banks need to take a clear decision to either exit the market or stay and change their business and operating models

Efficiency varies hugely between clusters, with significantly higher Revenue per FTE for Strong Performers and clearly lower number of employees required to serve AuM

Banks that added scale through a significant acquisition saw their net revenue per FTE as well as their median RoE rise in the following one to two year

M&A pauses in 2015 but underlying drivers remain strong

34% changed CEO twice or more, but returns are far from guaranteed

Performance of Swiss Private Banks

The widening gap

25 August 2015

© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name and logo are registered trademarks.