performance management ch. 3 performance management...

TRANSCRIPT

Performance Management

Ch. 3 – Performance Management Systems Chiara Demartini

UNIVERSITY OF PAVIA

Master in International Business and Economics

A PMS is the set of “evolving formal and informal mechanisms, processes, systems, and networks used by organizations for conveying the key objectives and goals elicited by management, for assisting the strategic process and ongoing management through analysis, planning, measurement, control, rewarding, and broadly managing performance, and for supporting and facilitating organizational learning and change” (Ferreira and Otley 2009: 264).

A definition of Performance Management System

2

Contingency Framework

3

Contingency Variables

C. Demartini – Performance Management

• Broad scope and timely information

• Subjective evaluation style

• Less reliance on incentive-based pay

• More reliance on open, flexible, non-financial control style

• Participative budgeting

• Mix of formal and informal control mechanisms

• Reduced emphasis on budget

External environment

4

1

Contingency Variables

C. Demartini – Performance Management

• Highly specialized, non-standard, differentiated products require flexible responses (organic/social/informal control mechanisms)

• Formal controls are more suited for standard production sets

Technology: How the organization’s

work processes operate (the way tasks transform inputs into outputs)and includes

hardware (such as machines and tools),

materials, people, software and knowledge

COMPLEXITY, TASK UNCERTAINTY, INTERDEPENDENCE

5

2

Contingency Variables

C. Demartini – Performance Management

•Formal v informal mechanisms

•Participative budgeting

•Leadership style: Budget emphasis

Organisational structure:

Formal specification of different roles for

organizational members, or tasks for groups, to

ensure that the activities of the organization are

carried out. DIFFERENTIATED V

INTEGRATED

MECHANISTIC V ORGANIC

BUREAUCRATIC V NON-BUREAUCRATIC

6

3

Contingency Variables

C. Demartini – Performance Management

• Level of sophistication of management control

• Administrative in large v personal controls in small firms

• Participative budget and formal communication

Size

LARGE v SMALL

7

4

Contingency Variables

C. Demartini – Performance Management

• Conservative orientation, defenders, harvest and cost leadership are best served by centralized control systems, specialized and formalized work, simple coordination mechanisms and attention directing to problem areas

• Strategies characterized by an entrepreneurial orientation, prospectors, build and product differentiation are linked to lack of standardized procedures, decetralized and results oriented evaluation, flexible structures and processes, complex co-ordination of overlapping project teams, and attention directing to curb excess innovation.

Strategy:

It is not an element of context, rather it is the means whereby man-

agers can influence the nature of the external

environment. PROSPECTERS-

ANALYSERS-DEFENDERS

BUILD-HOLD-HARVEST

PRODUCT DIFFERENTIATION-COST

LEADERSHIP 8

5

Contingency Variables

C. Demartini – Performance Management

• Mixed results

• Budget emphasis in evaluation and either job related tension or job satisfaction (Australian v Singapore)

• Role ambiguity and superior/subordinate relationships and both participation in budgeting and in performance evaluation were stronger in foreign subsidiaries than local Singapore entities

• Japanese, compared to US, companies experience less explicit controls and more implicit controls in monitoring, evaluation and rewarding

Culture: Different countries possess

particular cultural characteristics. This

predisposes individuals from within these cultures to

respond in distinctive ways to MCS.

POWER DISTANCE, INDIVIDUALISM VS.

COLLECTIVISM, UNCERTAINTY AVOIDANCE,

MASCULINITY VS. FEMININITY,

CONFUCIAN DYNAMISM 9

6

Overall areas of interest in the contingency framework

C. Demartini – Performance Management

Equifinality approach (package of control mechanisms)

Parenting style and Value creation

Outsourcing decisions and Trust

R&D activities

10

Relevance Lost and Recent Performance Measurement Systems

C. Demartini – Performance Management 11

The financial reporting system is “too late, too aggregated, and too distorted to be relevant for managers’ planning and control decisions”

(Kaplan and Norton, 1987: 1).

Data from financial reporting system is: • Backward

looking • Aggregated • Financial-

based

Balanced Scorecard

C. Demartini – Performance Management 12

The Balanced Scorecard is “ a comprehensive framework that translates a company’s strategic objectives into a coherent set of performance measures”

(Kaplan and Norton, 1993: 4).

Return-on-Capital-Employed

Cash Flow

Project Profitability

Profit Forecast Reliability

Sales Backlog

Financial Perspective

% Revenue from New Services

Rate of Improvement Index

Staff Attitude Survey

N. Of Employee Suggestions

Revenue per Employee

Innovation and LearningPerspective

Pricing Index

Customer Ranking Survey

Customer Satisfaction Index

Market Share

Customer Perspective

Hours with Customers on New Work

Tender Success Rate

Rework

Safety Incident Index

Project Performance Index

Project Closeout Cycle

Internal Business Perspective

Return-on-Capital-Employed

Cash Flow

Project Profitability

Profit Forecast Reliability

Sales Backlog

Financial Perspective

Return-on-Capital-Employed

Cash Flow

Project Profitability

Profit Forecast Reliability

Sales Backlog

Financial Perspective

% Revenue from New Services

Rate of Improvement Index

Staff Attitude Survey

N. Of Employee Suggestions

Revenue per Employee

Innovation and LearningPerspective

% Revenue from New Services

Rate of Improvement Index

Staff Attitude Survey

N. Of Employee Suggestions

Revenue per Employee

Innovation and LearningPerspective

Pricing Index

Customer Ranking Survey

Customer Satisfaction Index

Market Share

Customer Perspective

Pricing Index

Customer Ranking Survey

Customer Satisfaction Index

Market Share

Customer Perspective

Hours with Customers on New Work

Tender Success Rate

Rework

Safety Incident Index

Project Performance Index

Project Closeout Cycle

Internal Business Perspective

Hours with Customers on New Work

Tender Success Rate

Rework

Safety Incident Index

Project Performance Index

Project Closeout Cycle

Internal Business Perspective

1

2 3

4

Balanced Scorecard

C. Demartini – Performance Management 13

Return-on-Capital-Employed

Cash Flow

Project Profitability

Profit Forecast Reliability

Sales Backlog

Financial Perspective

% Revenue from New Services

Rate of Improvement Index

Staff Attitude Survey

N. Of Employee Suggestions

Revenue per Employee

Innovation and LearningPerspective

Pricing Index

Customer Ranking Survey

Customer Satisfaction Index

Market Share

Customer Perspective

Hours with Customers on New Work

Tender Success Rate

Rework

Safety Incident Index

Project Performance Index

Project Closeout Cycle

Internal Business Perspective

Return-on-Capital-Employed

Cash Flow

Project Profitability

Profit Forecast Reliability

Sales Backlog

Financial Perspective

Return-on-Capital-Employed

Cash Flow

Project Profitability

Profit Forecast Reliability

Sales Backlog

Financial Perspective

% Revenue from New Services

Rate of Improvement Index

Staff Attitude Survey

N. Of Employee Suggestions

Revenue per Employee

Innovation and LearningPerspective

% Revenue from New Services

Rate of Improvement Index

Staff Attitude Survey

N. Of Employee Suggestions

Revenue per Employee

Innovation and LearningPerspective

Pricing Index

Customer Ranking Survey

Customer Satisfaction Index

Market Share

Customer Perspective

Pricing Index

Customer Ranking Survey

Customer Satisfaction Index

Market Share

Customer Perspective

Hours with Customers on New Work

Tender Success Rate

Rework

Safety Incident Index

Project Performance Index

Project Closeout Cycle

Internal Business Perspective

Hours with Customers on New Work

Tender Success Rate

Rework

Safety Incident Index

Project Performance Index

Project Closeout Cycle

Internal Business Perspective

Strategy-measure link

Balanced approach to short v long-term measures

Balanced approach on financial v non-financial measures

Cause-and-effect relationships

Four perspectives

C. Demartini – Performance Management 14

CUSTOMER PERSPECTIVE: “How do customers see us?”;

INTERNAL PERSPECTIVE: “What must we excel at?”

INNOVATION AND LEARNING PERSPECTIVE: “Can we continue to improve and create value?”

FINANCIAL PERSPECTIVE: “How do we look at shareholders?”

KEY PERFORMAN

CE INDICATORS

(KPIs) or DRIVERS

Lagging and Leading Indicators

C. Demartini – Performance Management 15

LAGGING INDICATORS are typically “output” oriented, easy to measure but hard to

improve or influence

LEADING INDICATORS are typically input oriented, hard

to measure and easy to influence

LAGGING INDICATOR: To be compliant with the SLA’s (service level agreements) to resolve high priority incidents within 48 hours.

LEADING INDICATORS: - % of incidents not worked on for 2 hours. - % of open incidents older then 1 day. - % of incidents dispatched more then 3 times. - Average backlog of incidents per agent

Example: IT OUTSOURCING COMPANY

A BSC example: Electric Co.

C. Demartini – Performance Management 16

The Strategy Map

C. Demartini – Performance Management 17

The Strategy Map is a common visual framework [...] that embeds the different items on an organization’s balanced scorecard into a cause-and-effect chain,

connecting desired outcomes with the drivers of those results (Kaplan and Norton 2000: 52). ”

Strategy developm

ent

• translation of vision into an integrated set of objectives.

Communication

• this set of objectives and linking it to reward systems

Business planning

• through the setting of priorities and resource allocation, in order to achieve business and financial integration.

Feedback and

learning

• Develops the strategic learning process,in that the achievement of shortterm financial targets is analysed together with the other

three perspectives measures in order to address whether or not the strategy in use is effective in achieving organizational long-

term survival

Software Company Strategy Map

C. Demartini – Performance Management 18

BSC: Pros and Cons

C. Demartini – Performance Management 19

Pros Cons Issue in identifying LEADING

INDICATORS

BSC: Fads or Fashion?

C. Demartini – Performance Management 20

• Short-term v Long-term balance

• Financial v Non-financial balance

First and widespread BALANCED performance measurement system

STRATEGY-PERFORMANCE link

• Need for customisation

• Best practices by consultants

Lack of IMPLEMENTATION SPECIFICATION

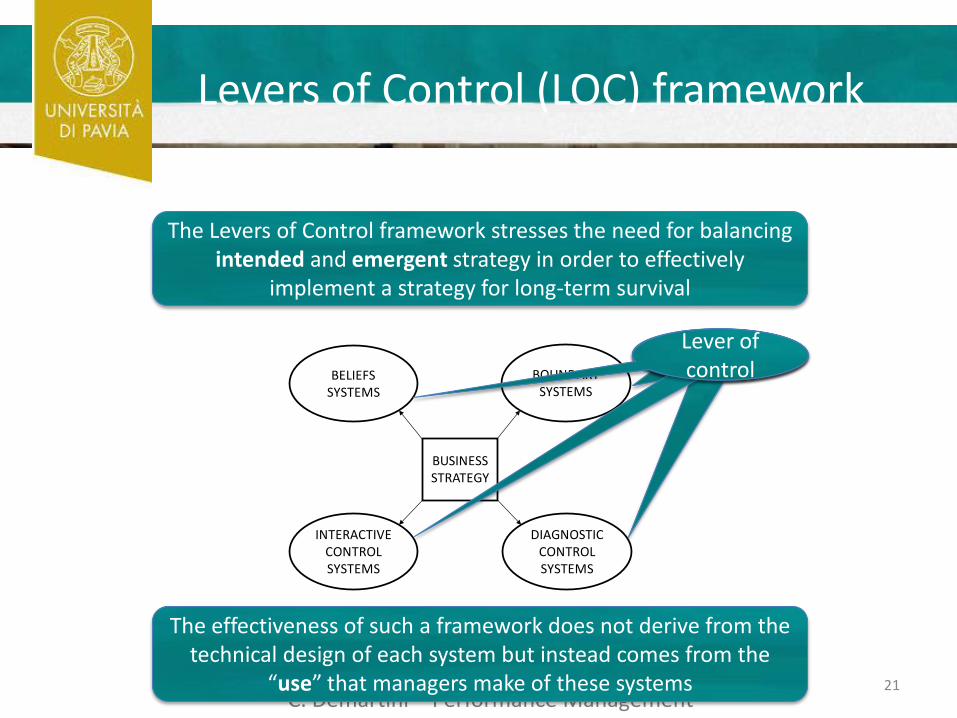

Levers of Control (LOC) framework

C. Demartini – Performance Management 21

BUSINESS STRATEGY

BOUNDARY SYSTEMS

DIAGNOSTIC CONTROL SYSTEMS

INTERACTIVE CONTROL SYSTEMS

BELIEFS SYSTEMS

The Levers of Control framework stresses the need for balancing intended and emergent strategy in order to effectively

implement a strategy for long-term survival

The effectiveness of such a framework does not derive from the technical design of each system but instead comes from the

“use” that managers make of these systems

Lever of control Lever of control Lever of control Lever of control

Diagnostic Control Systems

C. Demartini – Performance Management 22

Diagnostic Control Systems are formal information systems that managers use to monitor organizational

outcomes and correct deviations from present standards of performance

They could be Business plans, budgets, standard cost accounting systems and management-by-objectives

They perform intended strategy

Diagnostic control systems assure the achievement of predictable goals, and prevent innovation and opportunity-seeking

BUSINESS STRATEGY

BOUNDARY SYSTEMS

DIAGNOSTIC CONTROL SYSTEMS

INTERACTIVE CONTROL SYSTEMS

BELIEFS SYSTEMS

Aims of Diagnostic Control Systems

C. Demartini – Performance Management 23

Implement Strategy

Save managerial attention

BUSINESS STRATEGY

BOUNDARY SYSTEMS

DIAGNOSTIC CONTROL SYSTEMS

INTERACTIVE CONTROL SYSTEMS

BELIEFS SYSTEMS

Set and negotiate goals

Select Performance Measures

Set rewards Perform Variance analysis

Take actions to correct deviations

Risks to be avoided in using Diagnostic Control Systems

C. Demartini – Performance Management 24

BUSINESS STRATEGY

BOUNDARY SYSTEMS

DIAGNOSTIC CONTROL SYSTEMS

INTERACTIVE CONTROL SYSTEMS

BELIEFS SYSTEMS

Measure wrong

performance

Non-challenging

targets

Gaming Manipulation of Information

Illegal behaviour

Adjustments on activity

management

Interactive Control Systems

C. Demartini – Performance Management 25

Interactive control systems favour innovation development since they stimulate search and learning,

allowing new strategies to emerge as participants throughout the organization respond to perceived

opportunities and threats

ICSs identify strategic uncertainties

They perform emergent strategy

And challenge intended strategy

BUSINESS STRATEGY

BOUNDARY SYSTEMS

DIAGNOSTIC CONTROL SYSTEMS

INTERACTIVE CONTROL SYSTEMS

BELIEFS SYSTEMS

Strategic Uncertainties

C. Demartini – Performance Management 26

BUSINESS STRATEGY

BOUNDARY SYSTEMS

DIAGNOSTIC CONTROL SYSTEMS

INTERACTIVE CONTROL SYSTEMS

BELIEFS SYSTEMS

Strategic uncertainties are emerging threats and opportunities that could invalidate the assumptions upon which the current strategy is based

- Changes in competitive dynamics and internal competencies

- They cannot be known in advance

- Emerge unexpectedly over time

Strategic Uncertainties v Key Performance Indicators

C. Demartini – Performance Management 27

BUSINESS STRATEGY

BOUNDARY SYSTEMS

DIAGNOSTIC CONTROL SYSTEMS

INTERACTIVE CONTROL SYSTEMS

BELIEFS SYSTEMS

Strategic uncertainties

• Focus: Identification and analisys of new strategies

• Motivation: Executive managers’ tension

• Objective: Disruptive change

Key Performance Indicators

• Focus: Implementation of the intended strategy

• Motivation: Achievement of organisational goals

• Objective: Efficiency and effectiveness

Aims of Interactive Control Systems

C. Demartini – Performance Management 28

Identify STRATEGIC UNCERTAINTIES

Foster INNOVATION

BUSINESS STRATEGY

BOUNDARY SYSTEMS

DIAGNOSTIC CONTROL SYSTEMS

INTERACTIVE CONTROL SYSTEMS

BELIEFS SYSTEMS

1) An intensive use by senior management

2) An intensive use by operating managers

3) The pervasiveness of face-to- face challenges and debates

4) The focus on strategic uncertainties

5) A non-invasive and facilitating involvement.

Which Control Systems should be used interactively?

C. Demartini – Performance Management 29

BUSINESS STRATEGY

BOUNDARY SYSTEMS

DIAGNOSTIC CONTROL SYSTEMS

INTERACTIVE CONTROL SYSTEMS

BELIEFS SYSTEMS

Strategic Uncertainty High level of uncertainty Low level of uncertainty

TECHNOLOGY Focus on New emerging technology

Focus on Customers’ needs

LEGAL SYSTEM AND MARKET STRUCTURE

Focus on socio-political opportunities and threats

Focus on competitive opportunities and threats

COMPLEXITY OF THE VALUE CHAIN

Reliance on Accounting measures (profit planning)

Reliance on input/output measures

DEGREE OF COMPLEXITY IN TACTICAL RESPONSE

Short-tem planning Long-term planning

Beliefs Systems

C. Demartini – Performance Management 30

Beliefs systems assure that the relationship between strategy and organizational values is

coherent

Explicit set of organizational definitions

Senior managers communicate them formally and reinforce systematically

They are aimed at providing basic values, purpose, and direction for the organization

BUSINESS STRATEGY

BOUNDARY SYSTEMS

DIAGNOSTIC CONTROL SYSTEMS

INTERACTIVE CONTROL SYSTEMS

BELIEFS SYSTEMS

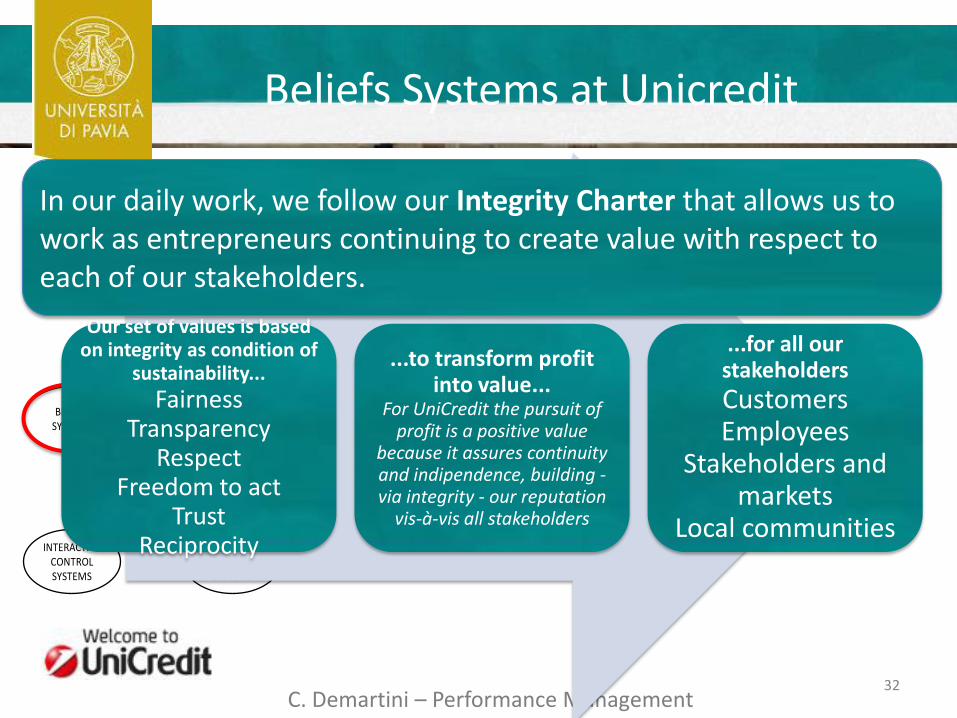

Beliefs Systems at Google

C. Demartini – Performance Management 31

BUSINESS STRATEGY

BOUNDARY SYSTEMS

DIAGNOSTIC CONTROL SYSTEMS

INTERACTIVE CONTROL SYSTEMS

BELIEFS SYSTEMS

1. Focus on the user and all else will follow.

2. It's best to do one thing really, really well.

3. Fast is better than slow.

4. Democracy on the web works.

5. You don't need to be at your desk to need an answer.

6. You can make money without doing evil.

7. There's always more information out there.

8. The need for information crosses all borders.

9. You can be serious without a suit.

10. Great just isn't good enough.

C. Demartini – Performance Management 32

BUSINESS STRATEGY

BOUNDARY SYSTEMS

DIAGNOSTIC CONTROL SYSTEMS

INTERACTIVE CONTROL SYSTEMS

BELIEFS SYSTEMS

Beliefs Systems at Unicredit

Our set of values is based on integrity as condition of

sustainability...

Fairness Transparency

Respect Freedom to act

Trust Reciprocity

...to transform profit into value...

For UniCredit the pursuit of profit is a positive value

because it assures continuity and indipendence, building - via integrity - our reputation

vis-à-vis all stakeholders

...for all our stakeholders

Customers Employees

Stakeholders and markets

Local communities

In our daily work, we follow our Integrity Charter that allows us to work as entrepreneurs continuing to create value with respect to each of our stakeholders.

Boundary Systems

C. Demartini – Performance Management 33

Boundary systems manage the “risks to be avoided” and confine managerial action by setting limits to the creativity that managers could use in finding new solutions to problems or discovering unpredictable opportunities to create organizational value.

Balances the benefits and dysfunctionalities from managerial creativity

It is linked to sanctions and punishment

BUSINESS STRATEGY

BOUNDARY SYSTEMS

DIAGNOSTIC CONTROL SYSTEMS

INTERACTIVE CONTROL SYSTEMS

BELIEFS SYSTEMS

Based on 1999 Otley’s framework:

1. Strategy formulation and implementation

2. Key strategic objectives

3. Target setting

4. Reward systems

5. Information system

The Overall Framework

34

1. Mission and vision

2. Key success factors

3. Organisational structure

4. Performance evaluation

5. PMS use

6. PMS Change

7. Interaction and strength in the performance management parts

The Overall Framework 7 New Questions

35

The PMS as a package framework

36 C. Demartini – Performance Management

Loose coupling PMS and innovation

37

Loose coupling approach provides a balance between the autonomy and coordination (i.e. control) of the elements within the system.

These elements are both coordinated in achieving the organizational goals, because they are linked to one another by coupling relationships that assure a certain degree of causality, and

autonomous, since their linkages are loose and they can perform their individual goals in very different configurations, thereby experiencing a high degree of flexibility

Loose coupling is a situation in which “events are responsive, but […] each event also preserves its own identity” (Weick, 1976, p. 3)

C. Demartini – Performance Management

Loose coupling PMS Pros and Cons

38 C. Demartini – Performance Management

Pros

• Flexibility

• Sensing mechanism

• Autonomy and responsibility

• Less expensive than tightly coupled PMSs

Cons

• Lack of strategic orientation

• Faddish responses

Context variables: environment, the type of control and the technology

Firm as an efficient system of transformations

39 C. Demartini – Performance Management

Firm as an efficient system of transformations

40 C. Demartini – Performance Management

Economictransformation

Financial transformation

Productivetransformation

QF

CP = pP * QF

IC = E + D

QP

RP = pV * QP

OI = I + R

pP

OI = RP - CP

Entrepreneurialtransformation

ExternalInformation

Decisions

Operations

Objectives

Firm as an efficient system of transformations

41 C. Demartini – Performance Management

Conclusions

42

The loose coupling approach enables both efficiency (short-term effectiveness), and innovation (long-term viability). From the outlined literature review on PMS design, some topics emerged: 1. effective design of PMS design is contingent to both external

and internal variables; 2. financial performance measures are more and more assessed

together with non-financial performance measures; 3. the link between PMS and strategy should be enacted trough

different kind of PM mechanisms (or levers); 4. PMS is a dynamic package of PM mechanisms; 5. loose coupled PMS develops both control and flexibility,

which result in efficiency and innovation purposes. C. Demartini – Performance Management