perfect competition monopolistic … eco/ch-9.pdf · monopolistic competition oligopoly duopoly...

TRANSCRIPT

__________________________________________________________________

147

PERFECT COMPETITION MONOPOLISTIC COMPETITION MONOPOLY OLIGOPOLY DUOPOLY

__________________________________________________________________

148

__________________________________________________________________

149

MARKET STRUCTURES

Market Structure means the way in which a market is organized. The theory of market focuses especially on those aspects of market structure, which have an important influence on the behavior of firms, buyers and on the performance of market. Structural features, which have a major strategic importance in relation to market conduct and performance, include the following: -

1. Degree of seller and buyer concentration as measured by the number of sellers and

buyers whether there are many sellers/buyers in the market or a few or only one and what is their relative size distribution.

2. Condition of entry to the market, the extent to which established suppliers have

advantages over potential new entrants because of barriers to entry into the business. 3. Nature of the product supplies, whether it is a homogenous product or there is

product differentiation. 4. Extent to which firms produce their own input requirements or own distribution

outlets/channels for their products.

5. Extent to which firms operate in a number of markets rather than just in one market.

6. Market structure is also affected by market conduct and market performance.

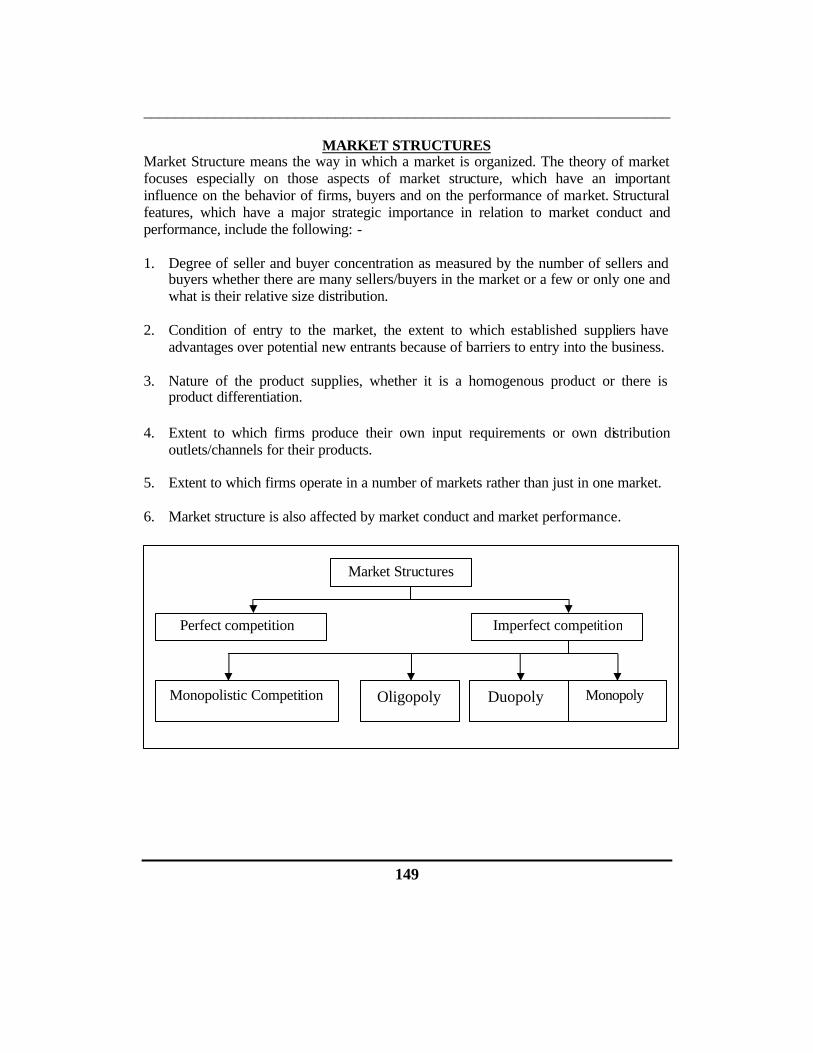

Market Structures

Perfect competition Imperfect competition

Monopolistic Competition Monopoly Oligopoly Duopoly

__________________________________________________________________

150

PERFECT COMPETITION

1. In this market structure there are a large number of buyers and sellers. No single seller or single buyer can influence the price and output of the market. With a small increase in price of a single seller, the buyers will immediately move to another seller, hence the seller is a price-taker and not a price- maker.

2. The product of all sellers is homogeneous, particularly the agricultural farm products

such wheat.

3. Any firm can enter into the industry for profit and can leave the industry to avoid losses.

4. The seller/ firm’s aim is to maximize his profit. 5. All sellers and buyers know the prevailing prices of the good in the market.

6. Transport cost is ignored; if the cost of transport is there then prices must be different. 7. All factors of production are mobile; this helps the firms in adjusting their supply as

per demand. 8. There is no Government interference by way of price control or rationing etc. sellers

can sell their goods to any buyer and in any quantity. 9. The price is equal to average revenue and average revenue is equal to marginal

revenue. Price =AR = MR and demand curve is a straight parallel to the base line. It means demand curve is perfectly elastic or fairly elastic..

10. The firm can continue its business in short run even in losses. MONOPOLY 1. It is one of the types of Imperfect Competition.

2. There is only one firm/producer in the market or only one firm controlling over 80% market share.

3. There are no close substitutes of the firm’s product.

4. In the market situation firm and the industry is one and the same thing.

5. The market is closed for the entry of other firms, may be on the basis of heavy cost structure or due to highly sophisticated technology such as Pakistan Steel Mills. No private firm can compete with this business unit.

__________________________________________________________________

151

6. Monopoly situation may occur due to the following: ? Copy rights ? Patents registration ? Trade Marks.

7. Government may put restrictions in the entry of business such as previously private sector was not allowed to operate domestic flights in Pakistan to compete with PIA.

8. Firm may have control over the supply of raw material such as Sui Southern Gas

Company has the monopoly for the supply of natural gas. KESC has the monopoly for supply of electricity in Karachi.

9. Monopolist may exploit customer by charging excessive prices. Monopolist used to

do that but generally, he do not do that rather reduces prices to enhance the total sale thus increasing the total profit. Price or average revenue of the firm slopes downward, likewise marginal revenue also slops downward. Price = AR but AR is not equal to MR rather MR is below AR and demand curve moves from left to right downward.

10. The monopolist has to lower the price on the last unit to sell it because he is facing

downward sloping demand curve and the only way to move down the demand curve is to lower the price on all units. Thus his total revenue will be greater than before as shown in the table below.

Price Demand Total revenue Rs.1 100 units Rs.100.00

Rs.0.90 125 units Rs.112.50

Monopoly is a firm that has great control over the price of a good. In the extreme case, a monopoly is the only seller of a good or service. The word monopoly brings to mind notions of a business that gouges the consumer, sells faulty products, gets rich and other negative thoughts but the fact is that it is not so.

MONOPOLISTIC COMPETITION

1. It is one of the types of imperfect competition. In this market structure there are many sellers/ firms but none of them have a large share of the market thus individual firm has only a very small amount of control over the whole market.

2. People i.e. buyers want to save their time and they avoid going to the big shops,

mandis and super markets. They prefer shopping at the nearby locations. This is the reason that most small retail shopkeepers operate in monopolistically competitive markets.

__________________________________________________________________

152

3. The products are not homogenous but are close substitutes. Each firm has a

monopoly on its branded product. It however faces competition with similar products such as various types of shampoos and tooth pastes like Colgate, Forhans, and McLean’s compete with each other. This situation is called Product Differentiation. The products are differentiated by: -

1 Different brand names 2 Trade marks. 3 Labeling and packaging. 4 Designing. 5 Product coloring.

4. Each seller has his own price policy hence prices are different in the market.

5. For any current monopolistic competitor, potential competition is always lurking in

the background, which means get ready to enter in to the market. The easier and the less costly entry is, the more a current monopolistic competitor must worry about losing his business because any new firm can enter into the bus iness or any existing firm may go out of business at any moment. Too much advertising is done in this market to attract the customers for a particular brand. Brand-loyalty is created by the following techniques: -

1 Provision of efficient services 2 After sale service 3 Discounting 4 Prize coupons

6. Individual customer feels proud in using a particular brand of his choice.

7. There are many firms and each firm acts independently of the other firms. No firm

attempts to take into account the reaction of all its rival firms; rather it would be impossible to do so with so many rival firms. Rivals reactions to output and price changes are largely ignored in this market structure.

8. In order to promote sells individual firm reduces its price therefore its average

revenue curve slopes downward and its marginal revenue curve also faces downward sloping and is below the demand or average revenue curve. Price = AR but AR is not equal to MR, rather AR is above MR

Product differentiation is main characteristic of monopolistic competition

__________________________________________________________________

153

OLIGOPOLY

1. In this market structure there are few large firms (usually 3 to 6) who dominate the entire industry.

2. These few firms are inter-dependent, each firm knows that other firms will react to its change in prices, quantities and qualities. Haleeb milk, Milk- pack and Candia Pepsi-cola, Coca-cola, Fanta and Sprite, or Arial, Surf and Bright are good examples in this regard.

3. In this market situation product may be homogeneous or differentiated. 4. In perfect competition each firm ignores the reactions of other firms; in monopoly

there is no fear of reaction because there is no rival. In Oligopoly the managers of the firms are like generals in a war, they must attempt to predict the reaction of rival firms. It is therefore a strategic game.

5. Since the firms are big and large ones, there exists the economies of scale; their doubling the output results in less than doubling the total cost. Firms that are not efficient leave the business.

6. Patent rights restrict the entry of other firms in the business therefore oligopoly develops and progresses.

7. Advertising plays an important role in this market structure and potential rivals remain away from this business. They have to face high entry cost due to the necessity of waging a massive advertising campaign.

8. Mergers of few small firms of the same business also create oligopoly, which then creates a greater ability to control the market price for its product.

COMPARING MARKET STRUCTURES

Perfect

Competition Monopolistic Competition

Oligopoly Monopoly

Number of sellers Numerous Many Few One

Unrestricted Entry & Exist Yes Yes Partial No

Ability to Set price None Some Some Considerable

Longrun Economic Profits possible

No Not for Most firms

Yes Yes

Product differentiation

None Too much Frequent None (Product Is unique)

Non-price competition None Yes Yes Yes

Examples Wheat production

Toothpaste Soap, retail trade

Cigarettes Electric Co. Gas Co

__________________________________________________________________

154

EQUILIBRIUM OF A FIRM UNDER PERFECT COMPETITION

(IN SHORT PERIOD)

(A)- Equilibrium is a situation when a firm is interested neither to increase nor to decrease its output. Output of a firm is determined at a point where marginal cost curve cuts marginal revenue curve from below and MC must also cut AC at its the lowest point. The equilibrium of a competitive firm has four possibilities. In order to explain this topic, three graphs will be drawn.

1-----Having super normal profit 2-----Having normal profit. 3-----Having losses. 4-----Shut down point. (B). Short run is a time period in which: - 1-----Variable factors of production such as raw material and labor can be altered to

change production. 2-----Fixed factors such as plant and machinery and building of production cannot be

changed. 3-----New firms do not enter into the industry. 4-----Existing firms do not leave the industry (C ). In Perfect Competition: - 1-----There are too many firms. 2-----Commodity is homogenous. 3-----One firm cannot change price

4-----Demand is elastic and Price =AR=MR=MC 5-----Firm continues business even in losses in short period of time.

6-----Output is determined at a point where MC=MR, 7-----MC curve is also called supply curve. 8-----Any firm can enter and leave the industry. 9-----Buyers and sellers know prevailing prices.

SUPER NORMAL PROFIT

MC cuts MR at N, therefore output OA Total cost OAMB Total revenue OANC Position Super Normal Profit BMNC

__________________________________________________________________

155

In the above graph firm is able to cover-up the variable cost, that is expenses incurred on raw material, labor charges, gas, electricity, transport etc as well as fixed cost Since its average cost curve is below its average revenue curve, therefore the firm is making super normal profit.

NORMAL PROFIT MC cuts MR at M , therefore is output OA Total cost OAMB Total revenue OAMB Position Normal profit ----

In above graph, firm’s total cost is OAMB, which is just equal to its total revenue OAMB hence, firm is making normal profit. When firm is making normal profit it means that minimum percentage of profit for businessman for his managerial services are already included in cost of production.

LOSS MC cuts MR at M, therefore output OA Average cost

AM + MN (AVC) (AFC)

Average Revenue AM Average Loss per unit

MN (AFC)

M

R.

AR

. A

C, M

C

Output 0

MC

A

AC

AR=MR C

B M

N

Output 0

MC

A

AC

AR=MR M

AR

MR

, AC

, MC

B

__________________________________________________________________

156

In above case firm is able to cover up all variable costs, that is expenses incurred on raw material, labor charges, gas, electricity etc. because its average variable cost curve is just equal to its average revenue curve. Firm is not covering any part of fixed cost. In short run firm will continue to do business and shall bear fixed cost which it is already bearing, with the hope of better prospects in future. In case it closes its business it will not only bear fixed expenses but will also loose clients and business reputation. As compared with the previous graph, in the present graph the position of the firm is very bad, since no portion of the fixed cost is being covered up.

HEAVY LOSSES AND SHUT DOWN POINT MC cuts MR at M, therefore output OA Total cost

OAKC + CKND (TVC) (TFC)

Total Revenue OAMB Total Loss

BMKC + CKND VC (TFC)

In above case firm is able to cover variable costs, that is expenses incurred on raw material, labor charges, gas, electricity etc. because its average variable cost curve is just

AR

M

R

AC

MC

Output 0

MC

A

AC

AVC K

AR=MR M B

D

C

N

A

R-M

R-A

C-M

C

Output 0

MC

A

AC AVC

AR=MR B

N

M

__________________________________________________________________

157

equal to its average revenue curve. Firm is not meeting any part of fixed expenses. If firm stops its production, in short run it will loose much because firm will have to bear all fixed cost. In short run firm will continue to do business and shall bear fixed cost, with the hope of better prospects in future. In case it closes its business it will not only bear fixed expenses but will also loose clients and business reputation. In the present graph position of firm is worse, since no portion of fixed cost is being covered up. If price is so low that an individual firm cannot even cover its variable costs, then that particular firm will windup its business, being unable to sustain this type of loss even in short period of time. The firm must cover the expenses of variable nature; whatever may be the time period and nature of business.

EQUILIBRIUM OF A FIRM UNDER PERFECT COMPETITION (IN LONG RUN) (A). Equilibrium is a situation when the firm is interested neither to increase nor to decrease its output. The long run equilibrium of the firm takes place when firm is just getting Normal profit. The equilibrium of the firm has only one possibility that is having normal profit and only one graph will be drawn. (B). Long run is a time period in which: - 1-----Variable factors of production can be altered to change the production. 2-----Fixed factors of production can also be changed. 3-----New firms can enter into the industry. 4-----Existing firms can leave the industry. (C). In Perfect Competition long run: 1-----There are too many firms. 2-----Commodity is homogenous. 3-----One firm cannot change its price 4-----Demand is elastic and Price = AR= MR 5-----Firm cannot continue business in losses in long period of time. 6-----P = AR 7-----AR = MR 8-----MR = MC ( for determination of output this requirement is a must ) 9-----MC = AC ( see cost relation topic ) 10----Therefore P = AR = MR = MC = AC 11----If P is above AC firm will make super normal profit 12----If P is below AC firm will make losses.

__________________________________________________________________

158

Output OA OB OC Price AM BE CY Average Revenue AM BE CY Average Cost AR BE CY + YZ

Profit per unit RM Equilibrium Loss per unit YZ Super Normal Profit Normal Profit Loss

Position

More firms will enter in this business

In long run this will continue

Many inefficient firms will left business

SUPPLY CURVE: - MC is cutting MR at Y, E, and M, therefore MR is also called supply curve because below these points output/supply is being determined. 1-----At price AM (p-1) firms will earn super normal profits, since it is a long period of time new firms will be attracted to the industry to reap the super normal profits, this will increase supply of the goods, therefore prices will decrease and super normal profits will be wiped out. 2-----When price goes down to BE ( p-2) then at this point AR, MR, AC, MR are equal at Point E. All firms of the industry will be getting normal profits. New firms will not be attracted to this industry and the existing firms will not be inclined to leave this business. 3-----When the price further goes down to CY (p-3), then at this stage firms will be running into losses to the extent of YZ since it is a long period and losses can not be borne for a long time, some inefficient firms will leave the industry in search of good luck in some other business. 4-----The above graph shows that in long run only those firms will remain in the bus iness whose marginal costs are equal to their average costs and average costs are equal to the prevailing prices and each firm will be getting only normal profit. Neither existing firms will leave the industry nor new ones will be attracted to this line of bus iness.

PR

ICE

AR

,MR

, AC

, MC

0

MC

C

AC

B A

P=AR=MR

P=AR=MR

P=AR=MR

Out- put

P-1

R

M

Z

Y P-3

P-2 E

__________________________________________________________________

159

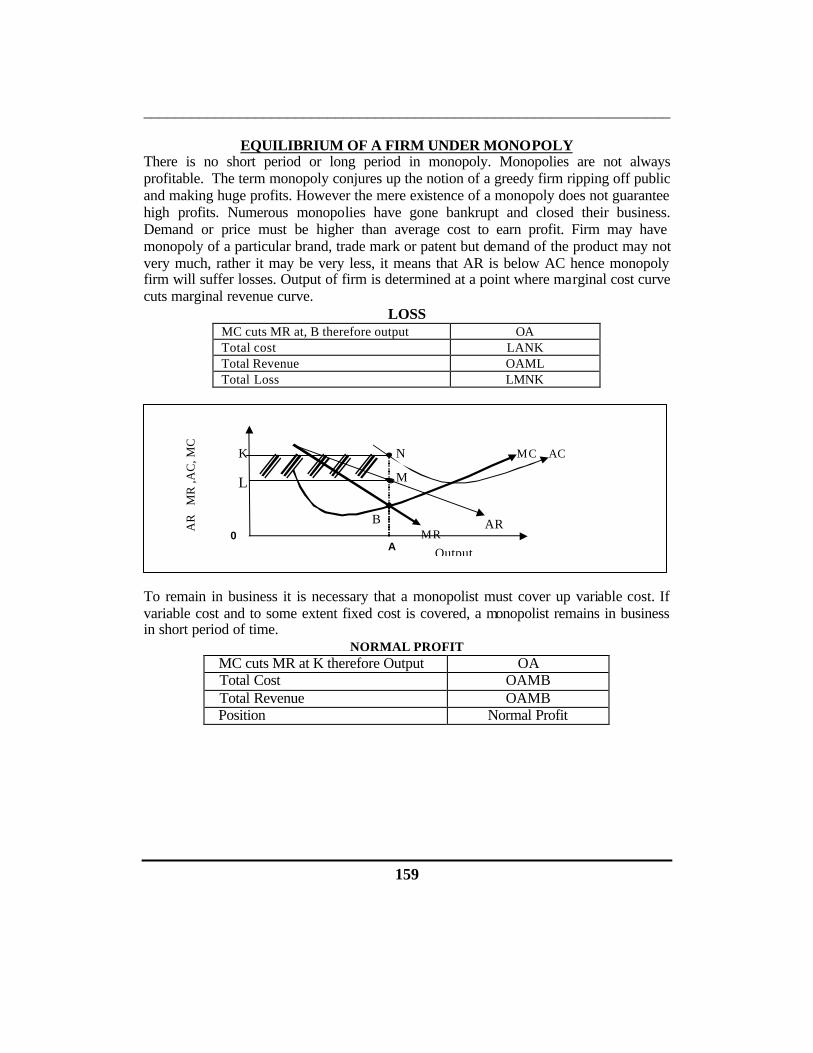

EQUILIBRIUM OF A FIRM UNDER MONOPOLY

There is no short period or long period in monopoly. Monopolies are not always profitable. The term monopoly conjures up the notion of a greedy firm ripping off public and making huge profits. However the mere existence of a monopoly does not guarantee high profits. Numerous monopolies have gone bankrupt and closed their business. Demand or price must be higher than average cost to earn profit. Firm may have monopoly of a particular brand, trade mark or patent but demand of the product may not very much, rather it may be very less, it means that AR is below AC hence monopoly firm will suffer losses. Output of firm is determined at a point where marginal cost curve cuts marginal revenue curve.

LOSS MC cuts MR at, B therefore output OA Total cost LANK Total Revenue OAML Total Loss LMNK

To remain in business it is necessary that a monopolist must cover up variable cost. If variable cost and to some extent fixed cost is covered, a monopolist remains in business in short period of time.

NORMAL PROFIT MC cuts MR at K therefore Output OA Total Cost OAMB Total Revenue OAMB Position Normal Profit

AR

M

R ,A

C, M

C

Output 0

MC

A AR

AC

MR

M

N K

L

B

__________________________________________________________________

160

PROFIT MC cuts MR at, B therefore output OA Total cost OAML Total Revenue OAML + LMNK Total Loss LMNK

Many people think that a monopolist always charges the highest price but this is not true. A monopolist tries to maximize total profits, not price. He produces where MR=MC and then charges a high price consistent with that output. A monopolist cannot charge any price and cannot sell any amount of his choice. He must choose an output (where MC=MR) and have selling price determined at a point where that quantity intersects demand curve/AR. Another misconception is that a monopolist always earns profit, which is not true. If his average cost curve lies above demand curve/AR he will incur losses. Output of firm is determined at a point where MC cuts MR and MC also cuts lowest point of AC.

AR

MR

, A

C ,

MC

Output

MC

A

AC

0

AR

MR

K

L

N

M

B

K

M

B

LAC

PR

ICE

,AR

, MR

C,M

C

0

MC

A

MR AR

Output

K

M AC

B

__________________________________________________________________

161

In order to accomplish profit maximization, monopolist must continue to expand output as long as increase in revenue exceeds the increase in cost. Marginal revenue is the increase in total revenue when firm sells one more units, whereas marginal cost is increase in total cost incurred for producing an additional unit. Hence he produces that output where marginal revenue equals marginal cost and maximizes profit.

EQUILIBRIUM OF A FIRM UNDER MONOPOLISTIC COMPETITION

(IN SHORT PERIOD) (A). Equilibrium is a situation when firm is interested neither to increase nor to decrease

its output. The equilibrium of a monopolistic competition has three possibilities and in order to explain this topic, three graphs will be drawn.

1. Having super normal profit. 2. Having normal profit. 3. Having losses. (B). Short run is a time period in which: - 1. Variable factors of production can be altered to change production. 2. Fixed factors of production cannot be changed. 3. New firms do not enter into the industry. 4. Existing firms do not leave the industry. (C ). In Monopolistic Competition: - 1. There are many firms but none of them have a larger share of the market. 2. Products are differentiated. 3. Each firm has its own price policy; therefore prices are different in the market. 4. In order to maximize profits firm reduces its price therefore MR is below AR. 5. Firm continues business even in losses in short period of time. 6. Too much emphasis is given on advertisement. 7. Main difference between Perfect competition and Monopolistic competition is that in

perfect competition AR is equal to MR whereas in monopolistic competition MR is below AR. Products are identical in perfect competition whereas in monopolistic competition products are differentiated.

__________________________________________________________________

162

SUPER -NORMAL PROFIT

MC cuts MR at B, therefore output OA Total cost OAML Total Revenue OANK Position Super normal Profit LMNK

NORMAL PROFIT

MC cuts MR at K, therefore output OA Total cost OAMB Total Revenue OAMB Position Normal Profit LMNK

When firm is making normal profit it means that the minimum percentage of profits for businessman for his manageria l services are already included in cost of production. Thus when firm just covers its average total cost, it earns normal profits only.

M

R.

AR

. A

C

MC

.

0 MR

AC B

M MC

AR

A

K

Output

MC

AC

A 0

AR

MR

A

R,M

R, A

C, M

C

K

L

N

M

B

Out-put

__________________________________________________________________

163

LOSS

MC cuts MR at B, therefore output OA Total cost OANK Total Revenue OAML Position Loss LMNK

In the above case, firm, is meeting some part of its expenses i.e. Out of total cost of OANK, it is getting OAML only. If firm stops its production, in short run, it will loose much because the firm will have to bear all fixed expenses. In short run firm will continue to do business and shall bear some cost, with the hope of better prospects in future. In case it closes its business it will not only bear fixed expenses but will also loose clients and reputation of business.

EQUILIBRIUM OF A FIRM UNDER MONOPOLISTIC COMPETITION

(IN LONG RUN) (A)----Equilibrium is a situation where firm is interested neither to increase nor to decrease its output. In long run similarity between perfect competition and monopolistic competition becomes obvious. In long run since many firms produce close substitutes, any surplus profit disappears with competition; other firms imitate profitable products. Firms who suffer leave business in long run Therefore long run equilibrium of firm has only one possibility that is having normal profit, hence only one graph will be drawn.

(B)---- Long run is a time period in which 1-----Variable factors of production can be altered to change the production 2----- Fixed factors of production can also be changed. 3-----New firms can enter into the industry. 4-----Existing firms can leave the industry. (C)-----In Monopolistic Competition long run 1-----There are many firms but none of them have large share of the market. 2-----Commodity is not homogenous but differentiated. 3-----In order to maximize profits firm reduces its price ̀

AR

MR

AC

MC

0

MC

A AR

AC

MR

K

L

N

M

B

__________________________________________________________________

164

4-----Firm cannot continue business in losses in the long period of time. 5-----P = AR 6-----AR = is not equal to MR 7-----MR = MC (for determination of output this requirement is a must) 8-----Price is equal to AR and AR is equal to AC, therefore in long run profit

9-----The equilibrium of firm has only one possibility that is having normal profit.

NORMAL PROFIT MC cuts MR at K therefore Output OA Total Cost OAMB Total Revenue OAMB Position Normal Profit

DIFFERENCE BETWEEN PERFECT & MONOPOLISTIC COMPETITION 1. The demand curve (AR) is horizontal in perfect competition, which means that in

perfect competition price elasticity is infinite (perfectly ela stic)

2. The demand curve (AR) is not horizontal in monopolistic competition, it rather slopes downward, and here the demand is less than perfectly elastic.

3. This firm has some control over price, i.e., it has some market power. Price ela sticity of demand is not infinite.

3. In perfect competition AR is just tangent to minimum point of AC curve. In monopolistic competition AR is not tangent to the minimum point of AC, rather it is tangent to left of minimum point before reaching minimum point.

PR

ICE

,AR

, MR

C,M

C

0

MC

A

MR AR

Output

K

M AC

B

__________________________________________________________________

165

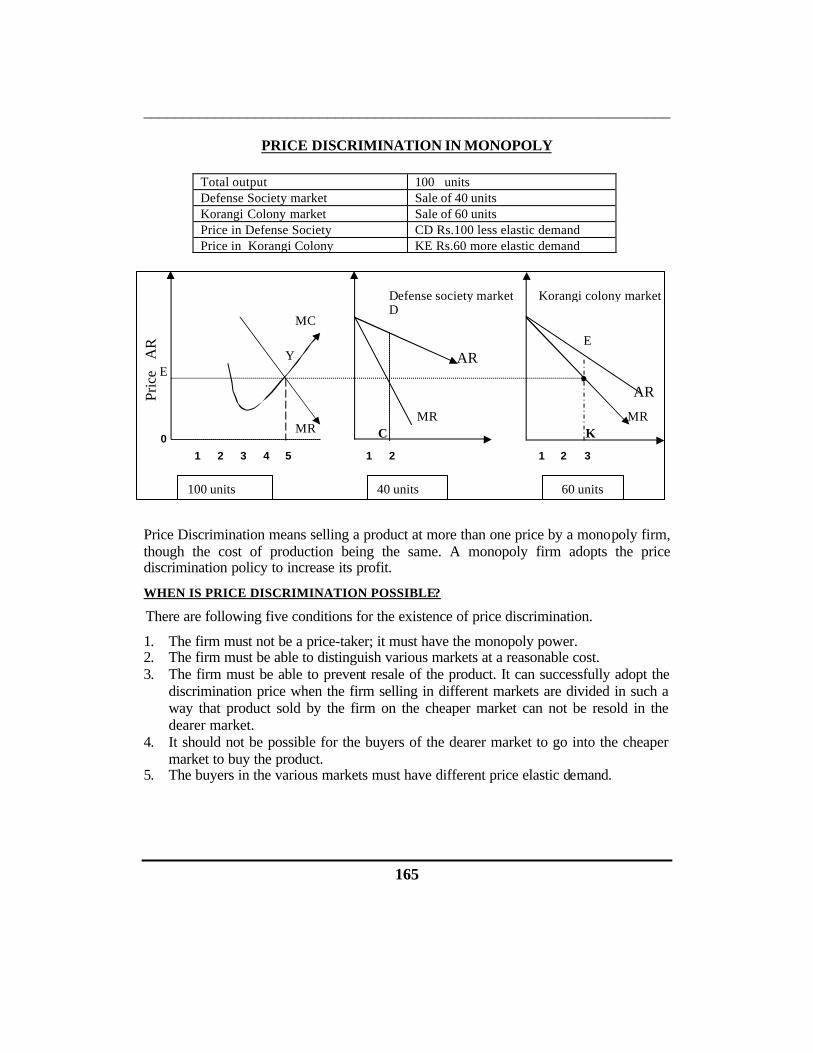

PRICE DISCRIMINATION IN MONOPOLY

Total output 100 units Defense Society market Sale of 40 units Korangi Colony market Sale of 60 units Price in Defense Society CD Rs.100 less elastic demand Price in Korangi Colony KE Rs.60 more elastic demand

Price Discrimination means selling a product at more than one price by a monopoly firm, though the cost of production being the same. A monopoly firm adopts the price discrimination policy to increase its profit.

WHEN IS PRICE DISCRIMINATION POSSIBLE?

There are following five conditions for the existence of price discrimination.

1. The firm must not be a price-taker; it must have the monopoly power. 2. The firm must be able to distinguish various markets at a reasonable cost. 3. The firm must be able to prevent resale of the product. It can successfully adopt the

discrimination price when the firm selling in different markets are divided in such a way that product sold by the firm on the cheaper market can not be resold in the dearer market.

4. It should not be possible for the buyers of the dearer market to go into the cheaper market to buy the product.

5. The buyers in the various markets must have different price elastic demand.

Pric

e A

R

100 units 40 units 60 units

0

5 2

Y

D

E

1 3 4 1 2 2 1 3

C K

E

MR MR

AR

AR

MC

MR

Defense society market Korangi colony market

__________________________________________________________________

166

1----- PERSON PRICE DISCRIMINATION. It means charging different prices from different customers for the same goods and services. Railways charge higher price for ticket from the father but less from his student son for the same seat and distance. Mr. Atta charges more tuition fee from rich students and less from poor students, though his teaching/instructions services for both of them are the same. 2-----LOCATION PRICE DISCRIMINATION A monopolist may charge different prices of his product from the customers of different regions and locations. Generally higher prices are charged from rich people living in posh areas, because their purchasing power is higher and demand is less elastic, whereas less prices are charged from the customers of poor localities because their purchasing power is less and demand is more elastic. 3----- USE PRICE DISCRIMINATION. It means to charge different prices as per the nature of the use of a good or service. KESC charges more for the supply of electricity from commercial users and less from the domestic users.

PRICE LEADERSHIP IN OLIGOPOLY When oligopolies enter into agreement to increase prices and share markets of their product it is called Cartel. The best example of cartel is OPEC, when few oil-producing countries have made an agreement for the sell of their oil. When oligopolies do not enter into a formal agreement and no formal meetings are held between them and there is only tacit collusion, then this situation is called Price Leadership. In this market situation a biggest dominating firm sets the price and allows other firms to sell all their products at that price. The dominating firm then sells the rest at the same price. Price Leadership requires one firm to be the leader but generally there is no agency to regulate the activities of all the firms of the same industry. Price leadership may not always work. If the price leader ends up much better off than the firms that follow, the followers firms may not accept the prices, which are set by the dominating firm. This results in Price War. If the dominating firm lowers its price a little whereas other firms may lower their prices even more. Super markets during holiday periods engage themselves in price wars. Price wars also happen in airline industry, particularly in Holiday Season. Hence price war is a pricing campaign designed to drive competing firms out of market by repeatedly cutting down the prices of their products and services.

__________________________________________________________________

167

Nature of Firm Firm A (Price Leader) Firm B (Price follower) Equilibrium point E F Output OM,it is more than Firm B ON, It is less than Firm A Marginal Cost ME, It is less than Firm B NF, It is more than Firm A Price MP, It is less than Firm B NK, It is more than Firm A Profit per unit EP, It is more than Firm B FK, It is less than Firm A Dominating firm will fix price equivalent to MP and follower will charge the same, which is equivalent to NW to him. Firm B will have to reduce Price otherwise it will have to go out of the market.

Generally price leader sets price in such a way that it allows some profits to the followers/firms. The price leader assesses the demand, cost, and competition and makes changes in such a way that all the firms of oligopoly market situation as a whole are benefited and whatever price is fixed by it, is accepted all the firms.

KINKY DEMAND CURVE IN OLIGOPOLY

MC

D, AR

MR-2

N

K

M

Demand

AR

MR

, M

C

P-2

p-1

O

L

A

MR-1

Elastic demand

Inelastic demand

0 N M

MC OF A

AR

MR

W

F

Output

MC of B P

K

E

__________________________________________________________________

168

Prof. Paul Sweezy gave the concept of Kinky demand curve in 1939. According to him in oligopoly the prices are usually rigid and sticky. Kink means a sharp twist in the curve otherwise the curve is straight. The competitive reaction pattern assumed by the kinky oligopoly demand curve theory is that:” Each oligopolist believes that if he lowers the price below the prevailing level, his competitors will follow him and will accordingly lower their prices, whereas if he raises the price above the prevailing level, his competitors will not follow to increase in prices of their products”. In the graph demand curve or AR is straight up to point M and then there is sudden twist and from M to D it is straight again. Prices are inflexible in this situation. The kink in the demand curve at M results in the discontinuity in the MR curve from N (MR-1) to K (MR-2). MC intersecting MR at any point between MR-1 and MR-2 and the resultant output is OA and price is OP-1 Cost of the firm may increase or decrease and the MC curve goes up or down in between the points N and K, yet output OA and Price P-1 remains unchanged. The kink in demand curve is always at the prevailing price because of the following. 1. A rise in the price by one firm may not invite retalia tion from the rival firms. Other

firms may not increase their prices rather they will allow the first firm to increase his prices so that it may lose the customers and the customers may come to them others have not increased their prices

2. A decrease in the price by one firm may immediately invite retaliation from the rival firms. Other firms may also decrease their prices, so that they may not lose their customers and the customers may continue to buy from them. In this situation the first firm reducing his prices will not be in a position to increase the sale of his products because others have also decreased their prices immediately.

3. The graph shows that LM part of demand curve is more elastic whereas MD part of

demand curve is less elastic and despite variations in cost and demand, the price under oligopoly remains unchanged, hence kinky demand curve shows sticky price in oligopoly.

DUOPOLY Duopoly is a subset of Oligopoly in which there are only two firms, which share the monopoly power. It may be of two types, duopoly with product differentiation and duopoly without product differentiation.

COLLUSIVE DUOPOLY OR CARTEL

In collusive duopoly, two firms attempt to maximize their joint profits by establishing agreed prices, which are above the competitive prices. The firms recognize that their

__________________________________________________________________

169

actions are interdependent and hence attempt to avoid mutually ruinous forms of rivalry. The total cost is sought to be minimized by producing such separate output as to make their costs of output equal. PRICE CONTROL IN DUOPOLY 1-----Since duopolies charge higher prices than the normal price therefore Government

should establish Monopoly Control Authority to control them and to break the monopoly power.

2-----There should be no restrictions and barriers in entering into the business, which are being undertaken by the duopolies.

3-----Anti cartel laws should be enforced. 4-----Heavy taxes should be imposed on them

VARIOUS MODELS OF DUOPOLIES

1 Game theory duopoly model 2 Cournot duopoly model 3 Edge-worth duopoly model

GAME THEORY

A 2 5

2 0

J

I H

G F

E D

C B

1 5

1 0

5 2 0 1 5 1 0

5

2 5

F I R M B

F I R M

A

Neumann and Oskar have developed this game theory. It is concerned with the general theory of conflict situations and help in decision-making and in selecting an optimum strategy. It is a way of describing the various possible outcomes in any situation involving two or more inter-acting individuals or firms when those individuals or firms are aware of the inter- active nature of their situation and plan accordingly. The plans

__________________________________________________________________

170

made by these individuals (firms) are known as game strategies. In duopoly there is PRICE WAR where these firms ruin each other by continuously reducing their prices.

In the above graph when Firm A reduces prices downward AB, (Vertical line) Firm B

also reacts and reduces prices by BC (Horizontal), again Firm A reduces prices by CD (vertical Line), firm B reacts and reduces its price by DE, (Horizontal). By looking the pattern of reaction and counter reaction we can see that this kind of rivalry ends in ruin of both the firms. Price cutting results in a big loss to both the firms, whereas, charging the normal price is a good strategy for both of them in the price war game.

Game Theory is a way of describing the various possible outcomes in any situation involving two or more interacting individuals/firms when these firms are aware of the interactive nature of their situation and plan accordingly. The plans made by these firms are known as game strategies

COURNOT DUOPOLY MODEL

In this model it is quantity of output, not the price, which is adjusted by the two firms. One firm changes its output on the assumption that his rival firms output will remain unchanged. Since both the firms think in the same way, output is expanded to the point where the two firms share the whole market demand equally and both of them get the normal profit. When Firm B produces ¼ of the total demand, the total output left for Firm A is ½(1-1/4= 3/8. Whatever is left over by Firm A and which now B produces is ½(1-3/8=5/16. Firm A will now react by producing ½(1-5/16) =11/32. This process will continue till output and price equilibrium is achieved.

W G

N

P

M

E

D C B A Out-put

Pric

e

__________________________________________________________________

171

Firm A Firm B

Output AB which is 50% (1/2) of total demand AD

--

Price AM -- Total demand of Market AD or (AB + BC +CD) -- Profit ABNM (Price AM into Output AB) --

Firm B now enters in the Market and produces

------- BC which is 25% (1/4) of total demand but 50% (1/2) as compared with Firm A’s output AB

Price

Due to entry and production of Firm B supplies has increased in market hence price has gone down from AM to AE

Profit Decreased from ABNM to ABWE BCGW

Loss of profit EWNM

EDGE-WORTH DUOPOLY MODEL

In this model it is price of output, not the quantity of output, which is adjusted by the two firms. The output of the rival firm is assumed to remain unchanged. One firm changes its price on the assumption that his rival’s price will remain unchanged. Since both the firms think in the same way, price keeps on changing.

Thus process of price-cutting continues till both the firms charge the same price and reach to an equilibrium position.

H

N

H

C

W

O Firm A Firm B

P

L

M

K

G

B

A

D

F

E

__________________________________________________________________

172

Firm A Firm B Demand PM PA Output ON OF Price PG -- Total sales EG

Price Enters in the market and charges price PD which is lower than PG of firm A

Total sales DH and takes away the market share of Firm A to the extent of WH

Price Reduces price to PK

Total sales CK and takes away the market share of Firm B to the extent of CH

Price Again reduces price to PB which is lower than Firm A

Total sales OF Price Further Reduces price to PL

Total sales ON Price of Firm A is L which is equal

to the Price of Firm B which is PB Output of Firm A is ON which is equal to the output of Firm B which is OF