peralta community college budget allocation model bam november 17, 2014

TRANSCRIPT

Peralta Community College Budget Allocation Model

BAMNovember 17, 2014

BAM

Modeled after SB 361◦Used for funding apportionment for all

California Community Colleges◦3 fundamental revenue drivers

Base allocation Credit Full Time Equivalent Students (FTES) Non-Credit FTES

◦Apportionment funding from this formula represents more than 70% of the District’s unrestricted revenue

Principles

Simple and easy to understandConsistent with State’s SB 361 modelProvides –

◦ Financial stability◦ A reserve in accordance with PCCD Board Policy◦ Clear Accountability◦ Periodic review and revision◦ Some services centralized at the District Office

Utilizes conservative revenue projectionsMaintains autonomous decision making at the college

levelIs responsive to the district’s and colleges’ planning

processes

Partnership

Between the Colleges and the District Office◦ To encourage and support collaboration

Colleges have broad oversight of institutional responsibilities◦ Primary authority over educational programs and student

services functions◦ Develops autonomous and individualized processes to meet

state and accreditation standardsDistrict office primarily ensures compliance with

applicable statue and regulatory compliance as well as essential support functions◦ Staff responsibility to fulfill fiduciary role of providing

appropriate oversight of District operations

Allocations

Similar allocation to four Colleges as SB 361 allocation to District

Allocates resources for Revenue, the District Office, District wide-services and regulatory costs based on percentage of 3 year rolling average of FTES

Components of Formula Used

Applicable Revenue = Revenue less Exclusions◦Amount of revenue to be distributed to

CollegesCentralized and District Office Expenses

◦Amount of expenditures to be distributed to Colleges

Three Year Rolling Averages◦3 year Average of the Total funded Full Time

Equivalent Students (FTES) for each College

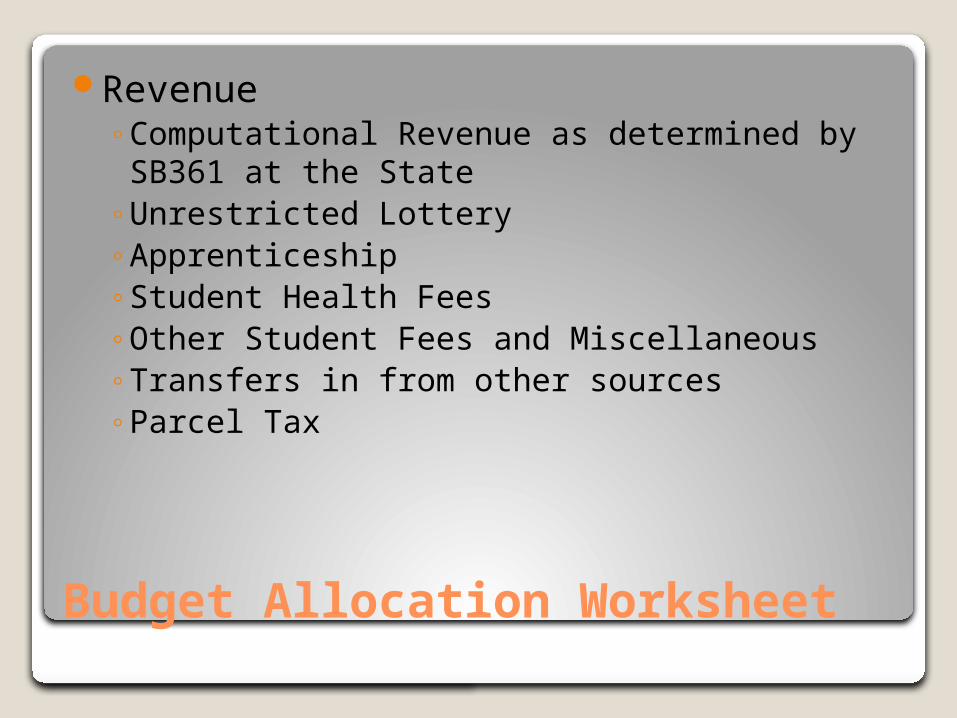

Budget Allocation Worksheet

Revenue◦Computational Revenue as determined by

SB361 at the State◦Unrestricted Lottery◦Apprenticeship◦Student Health Fees◦Other Student Fees and Miscellaneous◦Transfers in from other sources◦Parcel Tax

Exclusions

Other Post Employment Benefits (OPEB) paid for retirees

OPEB debt service payment

District Office Service Centers

Chancellors OfficeBoard of TrusteesGeneral CounselInformation TechnologyPublic InformationRisk ManagementEducation and Student ServicesInstitutional ResearchHuman ResourcesFinance and PurchasingGeneral Services

Centralized Services

DSPS ContributionAdmissions and RecordsFacilitiesFinancial AidInternational Education

Formula

Revenue Allocations to Colleges ◦Applicable revenue times the percentage

represented by the 3 year rolling FTES average of the district wide 3 year rolling average

District Office and Centralized Services◦Applicable cost of each service time the

percentage represented by the 3 year rolling FTES average of the district wide 3 year rolling averages

Total of these represent the revenue allocation to each College

Unrestricted Expenditure Budgets by College

Budget Cycle◦Tentative Budget to board by June 30◦Final Budget adopted by board by September

15Budget Calendar

◦Positions◦Discretionary ◦Categorical/Grants

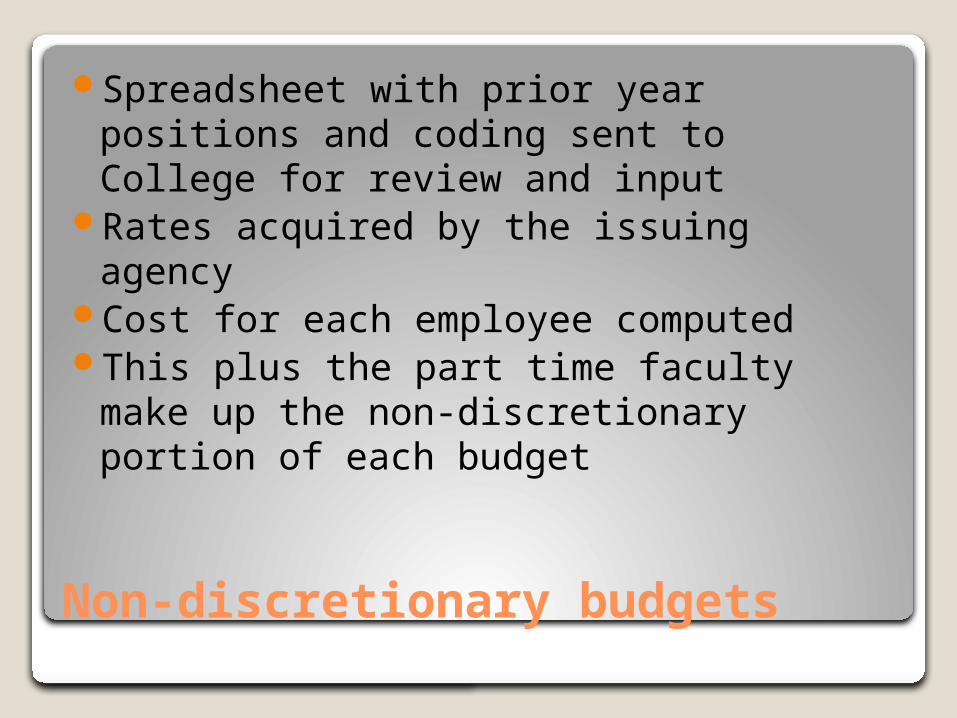

Non-discretionary budgets

Spreadsheet with prior year positions and coding sent to College for review and input

Rates acquired by the issuing agencyCost for each employee computedThis plus the part time faculty make up

the non-discretionary portion of each budget

FTEF calculation

FTES targets established for each College based on funded growth from the State

17.5 productivity used to determine number of Full Time Equivalent Faculty (FTEF) needed to meet the FTES targets

Full Time position for faculty subtracted from the number of FTEF needed to determine part time faculty budget

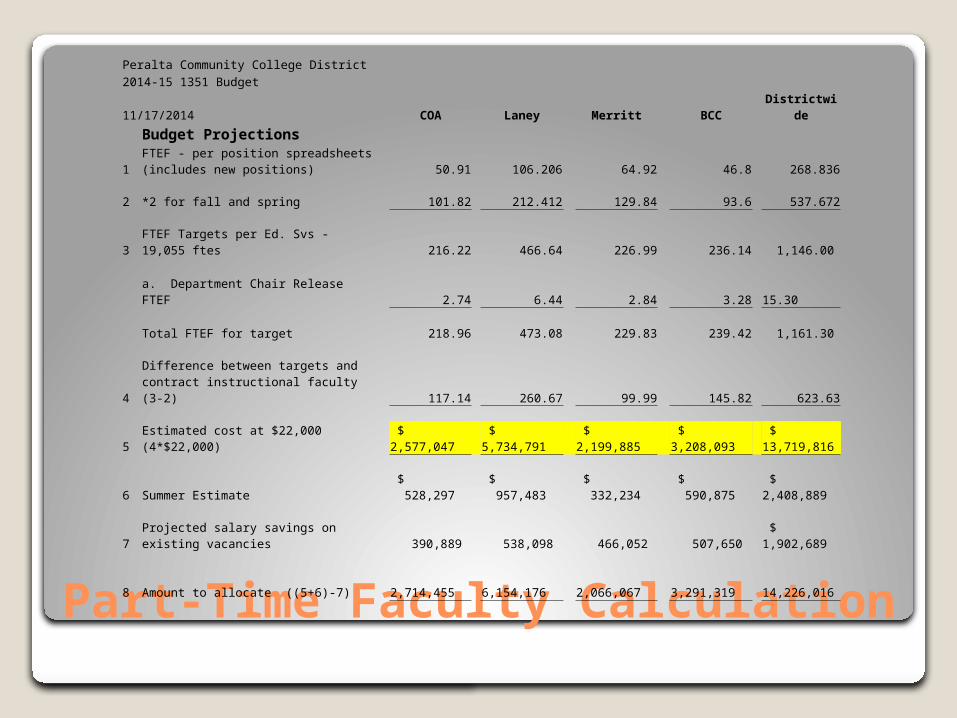

Part-Time Faculty Calculation

Peralta Community College District2014-15 1351 Budget11/17/2014 COA Laney Merritt BCC Districtwide

Budget Projections

1FTEF - per position spreadsheets (includes new positions) 50.91 106.206 64.92 46.8 268.836

2 *2 for fall and spring 101.82 212.412 129.84 93.6 537.672

3 FTEF Targets per Ed. Svs - 19,055 ftes 216.22 466.64 226.99 236.14 1,146.00

a. Department Chair Release FTEF 2.74 6.44 2.84 3.28 15.30

Total FTEF for target 218.96 473.08 229.83 239.42 1,161.30

4Difference between targets and contract instructional faculty (3-2) 117.14 260.67 99.99 145.82 623.63

5 Estimated cost at $22,000 (4*$22,000) $ 2,577,047 $ 5,734,791 $ 2,199,885 $ 3,208,093 $ 13,719,816

6 Summer Estimate $ 528,297 $ 957,483 $ 332,234 $ 590,875 $ 2,408,889

7 Projected salary savings on existing vacancies 390,889 538,098 466,052 507,650 $ 1,902,689

8 Amount to allocate ((5+6)-7) 2,714,455

6,154,176

2,066,067

3,291,319 14,226,016

Non-Discretionary Budgets

Full time positionsPart Time Faculty CalculationRelated payroll liabilitiesMedical and Dental premiums

On average, represents about 85% of College budget

Discretionary Budget

Prior Year Allocation used for: Hourly personnel Supplies Materials Services Capital Equipment

Include some fixed costs, such as utilities, rent, maintenance agreements, etc.

Represents on average 15% of College funding

Object codes ◦ 4xxx-7xxx ◦ 14xx and 13xx (except 1351)

Unrestricted Expenditure Budget by College

Total of the Discretionary and Non-Discretionary budgets as allocated based on the previous two slides

Differences

As anticipated, there are delta’s between the Revenue allocation by College and unrestricted expenditures by College

Identified in the BAM are strategies for Transition

Strategies for Transition

Will require multiple years to avoid negative and sudden operational impacts to programs and services

Options:◦Shifting FTES targets to provide additional

apportionment to some colleges◦Deficit reduction plans◦Shifting growth money from one college to another◦Reductions in centralized support functions and

services◦Utilization of international student tuition

Periodic Review

Still sorting out remaining issuesEvaluating the effectiveness of the

procedures outlinedSuggested review every 3 yearsKeeping the model up to date and

responsive to the changing community college landscape

Questions / Comments