pensions policy research online fieldwork: … household income london yorkshire (greater south east...

TRANSCRIPT

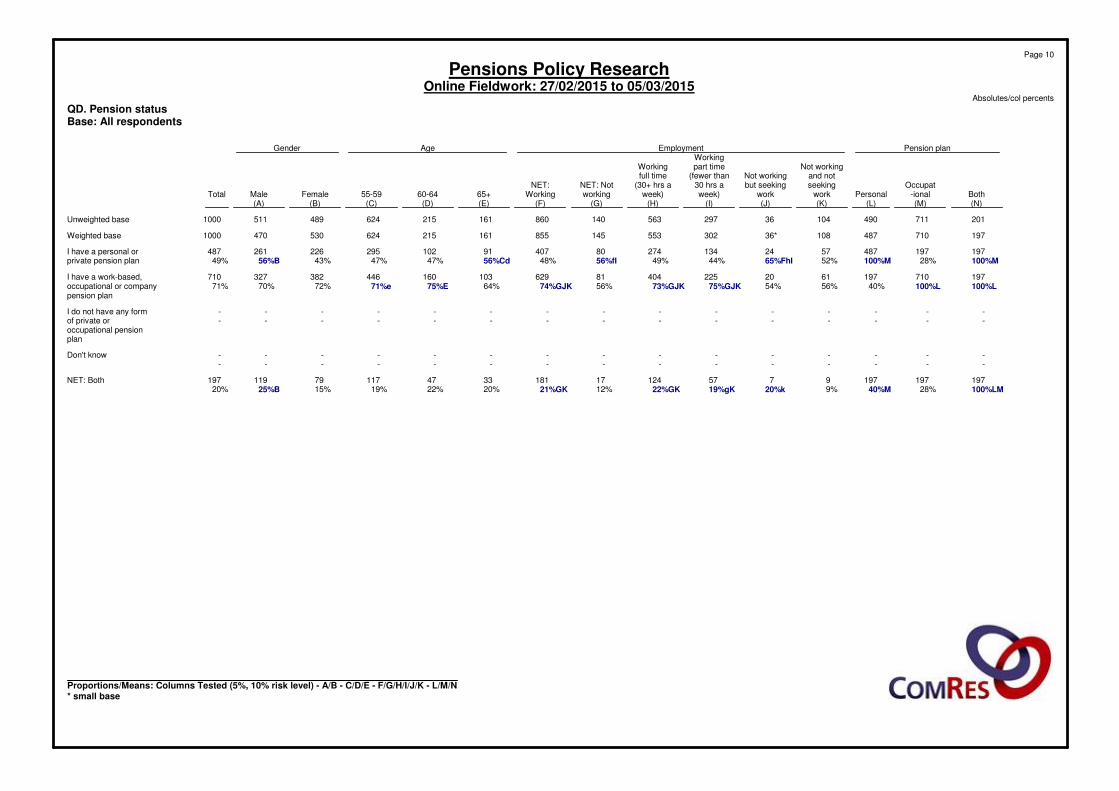

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

201711490104362975631408601612156244895111000Unweighted base

19771048710836*3025531458551612156245304701000Weighted base

1193272612719108317464248698286-470470Male60%M46%54%M25%51%GiK36%K57%FGIK32%50%GIK54%c45%46%-100%B47%

7938222681181942379943175117338530-530Female40%54%LN46%75%FHIJ49%64%FHj43%68%FHJ50%H46%55%54%e100%A-53%

Page 1

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QA. GenderBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

21337016538425919704599155107102847798110341000Unweighted base

21**33*68*16138626220**60*40*100*16011010080*90*110*11020*1000Weighted base

141847931849611342145715547334444597470Male67%53%m69%MN58%MN48%M37%54%56%ACe51%45%44%50%47%41%49%40%54%ACe34%47%

715216720216692619558955534746665113530Female33%47%31%42%52%OP63%NOPq46%44%49%55%56%50%53%59%bk51%60%BK46%66%BK53%

Page 2

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QA. GenderBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

28164734457759913713432164291686250164455391000Unweighted base

27864734557460013313131*16028868525117**4485351000Weighted base

145300153292294767319891563181282195273470Male52%46%44%51%m49%57%55%62%56%54%46%51%11%44%51%B47%

1323471932823055858127113336612315252263530Female48%54%56%l49%51%43%45%38%44%46%54%49%89%56%A49%53%

Page 3

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QA. GenderBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

201711490104362975631408601612156244895111000Unweighted base

19771048710836*3025531458551612156245304701000Weighted base

---------------Under 55---------------

1174462958731130377118506--62433828662455 - 59 years59%63%61%80%FHI86%FHI43%68%FI82%FHI59%I--100%DE64%61%62%

471601021737312220195-215-1179821560 - 64 years24%23%21%16%8%24%GJk22%GJ14%23%GJ-100%CE-22%21%21%

331039142100547154161--758616165 years or over17%15%19%m4%6%33%FGHJK10%gk5%18%GHjK100%CD--14%18%b16%

Page 4

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QB. AgeBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

21337016538425919704599155107102847798110341000Unweighted base

21**33*68*16138626220**60*40*100*16011010080*90*110*11020*1000Weighted base

-------------------Under 55-------------------

13224010423317215392461996460545972631462455 - 59 years63%68%58%65%60%66%75%65%59%61%62%59%60%67%66%66%57%71%62%

5718298851313112031212820192026421560 - 64 years23%20%26%18%23%20%16%21%27%20%19%19%28%25%21%18%24%18%21%

3411276538285183025126121821216165 years or over14%12%16%17%17%15%10%14%13%18%E19%E22%Ef12%8%14%16%19%E11%16%

Page 5

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QB. AgeBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

28164734457759913713432164291686250164455391000Unweighted base

27864734557460013313131*16028868525117**4485351000Weighted base

----------------Under 55----------------

153416225349356888218104151496991025935562455 - 59 years55%64%O65%61%59%66%63%F56%65%F52%72%D39%59%58%66%B62%

701326113012933274307812375311110121560 - 64 years25%n20%18%23%m21%25%21%12%19%27%gh18%30%E21%25%A19%21%

551005995115122110265966763778016165 years or over20%15%17%17%19%J9%16%32%Gi16%21%10%31%E20%17%15%16%

Page 6

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QB. AgeBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

201711490104362975631408601612156244895111000Unweighted base

19771048710836*3025531458551612156245304701000Weighted base

124404274---553-55354122377237317553Working full time (30+63%57%56%---100%FGIJK-65%GIJK34%57%E60%E45%67%B55%hrs a week)

57225134--302--30210073130194108302Working part time29%32%27%--100%FGHJK--35%GHJK62%CD34%C21%37%A23%30%(fewer than 30 hrs a

week)

72024-36--36-2331181936Not working but seeking4%3%5%m-100%FGHIK--25%FHIK-1%1%5%DE3%4%4%work

96157108---108-417878127108Not working and not5%9%n12%mN100%FGHIJ---75%FHIJ-3%8%E14%DE15%A6%11%seeking work

---------------Retired on a pension---------------

---------------Student---------------

---------------Prefer not to say---------------

181629407--302553-855154195506431424855NET: Working92%L89%L84%--100%GJK100%GJK-100%GJK96%Cd91%C81%81%90%B86%

17818010836--145-7201189946145NET: Not working8%11%16%MN100%FHI100%FHI--100%FHI-4%9%e19%DE19%A10%14%

Page 7

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QC. EmploymentBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

21337016538425919704599155107102847798110341000Unweighted base

21**33*68*16138626220**60*40*100*16011010080*90*110*11020*1000Weighted base

1826539923893183924419162544452615611553Working full time (30+86%78%Mno78%MNO62%M62%M35%88%66%bI59%I41%57%I57%I54%i55%i58%I56%I51%56%55%hrs a week)

3712491021021121143483330212534358302Working part time14%22%18%30%P27%39%NoPq6%21%28%43%cDEfg30%30%30%27%27%31%32%k38%k30%(fewer than 30 hrs a

HjKweek)

---5821-21365-3547136Not working but seeking---3%2%8%NOPq-3%f2%3%f4%F5%F-3%f5%F4%f6%F3%F4%work

--383745165131491612911121108Not working and not--5%5%10%oq17%NOPQ6%11%11%13%9%8%16%Agh15%a10%10%11%3%11%seeking work

-------------------Retired on a pension-------------------

-------------------Student-------------------

-------------------Prefer not to say-------------------

2133651483411951952358414096846577959119855NET: Working100%100%MNo95%Mn92%M88%M74%94%86%87%84%87%87%84%82%85%86%83%95%be86%

--313456718516201416151315191145NET: Not working--5%8%q12%pQ26%NOPQ6%14%13%16%13%13%16%18%a15%14%17%a5%14%

Page 8

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QC. EmploymentBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

28164734457759913713432164291686250164455391000Unweighted base

27864734557460013313131*16028868525117**4485351000Weighted base

14137019232232984758921674371037210336553Working full time (30+51%57%o56%56%55%63%k57%H25%58%H58%H64%D41%44%47%63%B55%hrs a week)

9518910317519831361646921731097159136302Working part time34%29%30%31%33%J23%28%51%FGI29%32%25%43%E42%35%A25%30%(fewer than 30 hrs a

week)

122112191773396268-162136Not working but seeking4%3%3%3%3%5%2%8%Fi6%F2%4%3%-4%4%4%work

2967385757121751324493126343108Not working and not11%10%11%10%9%9%13%15%8%8%7%12%E14%14%A8%11%seeking work

----------------Retired on a pension----------------

----------------Student----------------

----------------Prefer not to say----------------

2365602954985271141112413825961021215369472855NET: Working85%86%86%87%88%86%85%76%86%90%H89%d85%86%82%88%B86%

4288507673192082230753927963145NET: Not working15%14%14%13%12%14%15%24%F14%10%11%15%e14%18%A12%14%

Page 9

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QC. EmploymentBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

201711490104362975631408601612156244895111000Unweighted base

19771048710836*3025531458551612156245304701000Weighted base

19719748757241342748040791102295226261487I have a personal or100%M28%100%M52%65%FhI44%49%56%fI48%56%Cd47%47%43%56%B49%private pension plan

197710197612022540481629103160446382327710I have a work-based,100%L100%L40%56%54%75%GJK73%GJK56%74%GJK64%75%E71%e72%70%71%occupational or company

pension plan

---------------I do not have any form---------------of private or

occupational pensionplan

---------------Don't know---------------

197197197975712417181334711779119197NET: Both100%LM28%40%M9%20%k19%gK22%GK12%21%GK20%22%19%15%25%B20%

Page 10

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QD. Pension statusBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

21337016538425919704599155107102847798110341000Unweighted base

21**33*68*16138626220**60*40*100*16011010080*90*110*11020*1000Weighted base

131635731961257231660875748394454458487I have a personal or65%50%51%46%51%48%36%38%40%60%aBJK55%BjK52%bk48%48%49%49%40%41%49%private pension plan

1028531312711691745306211077716261788215710I have a work-based,49%85%Mn78%M81%MN70%65%84%75%i76%i62%69%70%71%78%I68%71%75%I76%71%occupational or company

pension plan

-------------------I do not have any form-------------------of private or

occupational pensionplan

-------------------Don't know-------------------

3112043813248621372419211522173197NET: Both14%35%Mn29%M27%M21%M12%20%14%16%21%23%22%19%26%bk17%20%15%17%20%

Page 11

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QD. Pension statusBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

28164734457759913713432164291686250164455391000Unweighted base

27864734557460013313131*16028868525117**4485351000Weighted base

136317152300266905923681593271259198281487I have a personal or49%49%44%52%M44%68%K45%72%fGI43%55%Gi48%50%52%44%52%B49%private pension plan

19746226438644082972511419549517811324374710I have a work-based,71%71%76%L67%73%J62%74%79%72%68%72%71%66%72%70%71%occupational or company

pension plan

----------------I do not have any form----------------of private or

occupational pensionplan

----------------Don't know----------------

5613271112106392616236613752374120197NET: Both20%20%21%19%18%29%K20%51%FGI14%23%G20%21%18%17%22%B20%

Page 12

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QD. Pension statusBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

201711490104362975631408601612156244895111000Unweighted base

19771048710836*3025531458551612156245304701000Weighted base

8452362123985281339263460Scotland4%6%5%6%5%4%7%i6%6%5%6%6%5%7%6%

315811811119241413720North East2%2%2%*1%3%2%1%2%1%2%2%2%1%2%

178245127355619912126635159110North West9%12%9%11%19%h12%10%13%11%13%12%10%10%13%11%

227854114346115951820726644110Yorkshire and the11%11%11%10%12%11%11%10%11%11%9%12%12%9%11%Humber

1561449525521377121959464490East Midlands8%9%9%8%13%8%9%9%9%8%9%9%9%9%9%

2162391232144156562054473380West Midlands10%9%8%11%8%7%8%10%8%4%9%E9%e9%7%8%

6301651112453551124192140Wales3%4%3%4%2%4%4%4%4%3%5%4%4%4%4%

19714816-305416841228605347100East of England10%10%10%15%fJ-10%j10%j11%J10%j8%13%10%10%10%10%

24775795336214962521645555110London12%11%12%8%14%11%11%10%11%15%c10%10%10%12%11%

37110871464891201403031998971160South East19%15%18%13%17%16%16%14%16%19%14%16%17%15%16%

216260133434116841820615545100South West11%9%12%M12%8%14%FH7%11%10%11%9%10%10%10%10%

41771-118119231591120Northern Ireland2%2%1%1%-*3%I1%2%I1%1%2%2%2%2%

Page 13

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QE. RegionBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

21337016538425919704599155107102847798110341000Unweighted base

21**33*68*16138626220**60*40*100*16011010080*90*110*11020*1000Weighted base

11392715-60----------60Scotland4%2%4%6%7%6%-100%ABCDEF----------6%

GHIJ

--1367-----------2020North East--1%2%2%3%-----------100%BCDEFG2%

HIJK

-44154633----------110-110North West-12%6%9%12%13%----------100%ACDEFGH-11%

IJK

-34165126---------110--110Yorkshire and the-10%6%10%13%10%---------100%ABDEFG--11%Humber

HIJK

1-8103727--------90---90East Midlands5%-11%q6%10%q10%q--------100%ABCEFG---9%

HIJK

135232023-------80----80West Midlands4%11%7%14%mN5%9%n-------100%ABCDFG----8%

HIJK

-2471214--40---------40Wales-6%6%4%3%5%--100%ABCDEF---------4%

GHIK

2412153723------100-----100East of England9%12%18%MNo9%9%9%------100%ABCDEG-----10%

HIJK

759233621-----110------110London34%16%13%14%Mn9%8%-----100%ABCDEFHI------11%

JK

6715216538----160-------160South East29%22%22%o13%17%14%----100%ABCDEF-------16%

GIJK

114124433---100--------100South West4%3%5%7%11%13%p---100%ABCDEF--------10%

GHJK

22166220-----------20Northern Ireland10%6%Mn1%4%M2%1%100%-----------2%

Page 14

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QE. RegionBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

28164734457759913713432164291686250164455391000Unweighted base

27864734557460013313131*16028868525117**4485351000Weighted base

1443282830718111144017-233760Scotland5%7%8%l5%5%6%14%FGh3%7%5%6%7%-5%7%6%

7136111031-64172111820North East2%2%2%2%2%2%*-4%i1%2%d1%4%3%2%2%

2875416558251262322673315653110North West10%12%12%11%10%18%K9%19%F15%F8%10%13%6%13%10%11%

2774336868101132221743415554110Yorkshire and the10%11%10%12%11%7%9%10%14%F7%11%14%7%12%10%11%Humber

255634455875-172665212474190East Midlands9%9%10%8%10%5%4%-11%hI9%hI10%8%14%10%8%9%

26482648421610313315519-384280West Midlands9%7%7%8%7%12%k8%8%8%11%8%8%-8%8%8%

122715212946-81125112142440Wales4%4%4%4%5%3%4%-5%4%4%5%11%3%5%4%

3160326467131371327711824949100East of England11%9%9%11%11%10%10%22%FGi8%9%10%7%13%11%9%10%

3170356767713418417425-4169110London11%11%10%12%11%J5%10%13%11%14%11%10%-9%13%b11%

461015591862625418541114036591160South East16%16%16%16%14%19%19%g13%11%19%G16%16%20%15%17%16%

2765325469141141034682643957100South West10%10%9%9%12%11%8%13%6%12%g10%11%26%9%11%10%

4169111625-12164-101020Northern Ireland1%2%2%2%3%2%4%FG-1%1%2%2%-2%2%2%

Page 15

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QE. RegionBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

201711490104362975631408601612156244895111000Unweighted base

19771048710836*3025531458551612156245304701000Weighted base

5373421122012333231151362965Up to £10,0003%5%7%N19%FHI34%FHIk7%FH2%23%FHI4%2%5%8%E7%6%7%

2713291259828034162354012113067196£10,001-£20,00014%19%19%23%H25%h27%FH15%23%H19%H22%19%19%24%A14%20%

461481121956212824189384113411697213£20,001-£30,00024%21%23%17%14%20%23%g16%22%24%19%21%22%21%21%

341238419341111211512747998687173£30,001-£40,00017%17%17%17%8%13%20%Ij15%18%i17%22%c16%16%19%17%

27904963366791031824714865113£40,001-£50,00014%13%10%6%8%12%gk12%gk6%12%gk11%11%11%9%14%B11%

1640242212324449534202848£50,001-£60,0008%l6%5%2%5%4%6%3%5%6%d2%5%d4%6%b5%

1330253-83233961423133043£60,001-£70,0007%4%5%3%-3%6%gI2%5%4%6%c4%2%6%B4%

7239--422-26541791726£70,001-£80,0003%3%2%--1%4%GIK-3%Gk3%2%3%2%4%b3%

6168--612-19231412719£80,001-£90,0003%2%2%--2%g2%g-2%g1%1%2%2%1%2%

6128--113-1424931114£90,001-£100,0003%2%2%--*2%gI-2%i1%2%1%1%2%B1%

136--17-8-17258£100,001-£110,000**1%--*1%-1%-*1%*1%1%

-22--13-42-2134£110,001-£120,000-**--*1%-*1%-**1%*

256--18-9144369More than £120,0001%1%1%--*1%-1%1%2%1%1%1%1%

7492914227271654131739521870Prefer not to answer4%7%6%13%FH6%9%H5%11%FH6%8%8%6%10%A4%7%

Page 16

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QF. Household incomeBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

21337016538425919704599155107102847798110341000Unweighted base

21**33*68*16138626220**60*40*100*16011010080*90*110*11020*1000Weighted base

-----65-43811758638265Up to £10,000-----25%NOPQ-7%7%8%7%7%5%9%c7%3%8%9%7%

-----1962111125271418162123255196£10,001-£20,000-----75%NOPQ12%18%27%G25%G17%12%18%20%23%g21%23%g27%G20%

----213-31952728251982228263213£20,001-£30,000----55%MOPQ-16%32%aEfHJ13%27%Ehj18%23%E19%e10%24%E25%E23%E15%21%

----173-38617361117111523203173£30,001-£40,000----45%MOPQ-16%14%16%17%23%G10%17%14%17%21%G18%g17%17%

---113--56461516917912102113£40,001-£50,000---70%MNPQ--25%10%11%6%9%15%I9%22%BcDFHI10%11%9%12%11%

K

---48--13366766135148£50,001-£60,000---30%MNPQ--5%5%7%6%4%7%d6%7%d1%3%4%5%5%

--43----323879353-143£60,001-£70,000--63%MNOQ----4%B4%B3%b5%B6%B9%Bci3%B6%B3%b-3%B4%

--26---1-217232214-26£70,001-£80,000--37%MNOQ---5%-6%ciK1%4%k2%3%2%2%1%4%-3%

-19----2-215221-21-19£80,001-£90,000-57%MNOP----11%-5%Dk1%3%2%2%1%-2%1%-2%

-14-----1--2323-13-14£90,001-£100,000-43%MNOP-----1%--1%3%i2%3%di-1%3%-1%

8------1-12121----8£100,001-£110,00036%------1%-1%1%1%2%1%----1%

4---------22------4£110,001-£120,00019%---------1%2%------*

9-----2---24--1---9More than £120,00044%-----11%---1%4%Bcefi--1%---1%

-------52698757108270Prefer not to answer-------8%4%6%5%8%7%6%8%9%8%12%7%

Page 17

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QF. Household incomeBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

28164734457759913713432164291686250164455391000Unweighted base

27864734557460013313131*16028868525117**4485351000Weighted base

2139233734913291148122125165Up to £10,0007%6%7%7%6%7%10%F6%6%4%7%5%12%3%10%B7%

45130849911427314354612752458134196£10,001-£20,00016%20%24%L17%19%20%24%F13%22%16%19%21%23%13%25%B20%

5414477114119283410354214950377133213£20,001-£30,00019%22%22%20%20%21%26%F32%F22%f15%22%20%20%17%25%B21%

52113611011052121530571214119577173£30,001-£40,00019%17%18%18%17%16%16%15%19%20%18%16%6%21%A14%17%

347132717016641644773116349113£40,001-£50,00012%11%9%12%12%12%5%12%10%i15%I11%12%5%14%A9%11%

192713333448112163115-311748£50,001-£60,0007%n4%4%6%6%3%6%3%8%6%4%6%-7%A3%5%

13281227298217232615-231943£60,001-£70,0005%4%3%5%5%6%1%3%4%8%I4%6%-5%4%4%

717121414631410215-161026£70,001-£80,0003%3%3%2%2%4%2%3%2%3%3%2%-4%a2%3%

510791433128144-13619£80,001-£90,0002%2%2%2%2%2%2%3%1%3%2%2%-3%A1%2%

3112111112138105-6814£90,001-£100,0001%2%*2%m2%1%2%3%2%3%1%2%-1%2%1%

34-8411122711348£100,001-£110,0001%1%-1%M1%1%1%3%1%1%1%*7%1%1%1%

13134-1--23--224£110,001-£120,000****1%-1%--1%*--***

1718522-1553-369More than £120,000*1%*1%m1%2%2%-1%2%1%1%-1%1%1%

204321374272141548184471970Prefer not to answer7%7%6%7%7%5%2%3%2%5%7%7%26%11%A3%7%

Page 18

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QF. Household incomeBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

201711490104362975631408601612156244895111000Unweighted base

19771048710836*3025531458551612156245304701000Weighted base

12037428143211363366347280101355263273535I am solely responsible61%M53%58%m40%57%k45%61%FGIK44%55%GIK50%47%57%D50%58%B54%for making household

financial decisions

7432419863161592107936977111259252195448I am jointly38%46%lN41%58%FH43%53%FH38%55%FH43%h48%52%C42%48%a42%45%responsible for making

household financialdecisions

31192-77215331015217I am not at all2%2%2%2%-2%1%2%2%2%2%2%3%A*2%responsible for making

household financialdecisions

Page 19

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QG. Responsibility for financial decisionsBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

21337016538425919704599155107102847798110341000Unweighted base

21**33*68*16138626220**60*40*100*16011010080*90*110*11020*1000Weighted base

1214296621018510372457916949424154538535I am solely responsible58%43%42%41%54%Op71%NOPQ52%61%abd60%a57%57%a63%ABCDF49%53%46%49%48%41%54%for making household

financial decisions

819399317170102314396541493847555611448I am jointly36%57%M58%MN58%MN44%M27%48%39%35%39%41%37%49%g47%52%Gj50%g51%Ghij56%gij45%responsible for making

household financialdecisions

1--156--243-2-211117I am not at all5%--1%1%2%--4%EGk4%eGk2%-2%-3%1%1%3%eGk2%responsible for making

household financialdecisions

Page 20

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QG. Responsibility for financial decisionsBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

28164734457759913713432164291686250164455391000Unweighted base

27864734557460013313131*16028868525117**4485351000Weighted base

14834617831433068811885155384117--535535I am solely responsible53%53%52%55%55%51%62%56%53%54%56%D46%--100%B54%for making household

financial decisions

12629016025526162471472132287132-448-448I am jointly45%45%46%44%43%47%36%44%45%46%i42%53%E-100%A-45%responsible for making

household financialdecisions

41275933-3214217--17I am not at all1%2%2%1%2%2%2%-2%1%2%1%100%--2%responsible for making

household financialdecisions

Page 21

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

QG. Responsibility for financial decisionsBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

201711490104362975631408601612156244895111000Unweighted base

19771048710836*3025531458551612156245304701000Weighted base

6619515924692167302595978151133156288Conservatives33%27%33%m22%15%30%Gj30%Gj21%30%Gjk37%C36%C24%25%33%B29%

231146813946922213826301047189160Labour12%16%14%12%25%k15%17%15%16%16%14%17%13%19%B16%

8403111115371252131238224163UKIP4%6%6%10%i3%5%7%8%6%8%6%6%4%9%B6%

1625235316882410418121931Liberal Democrats8%lM3%5%4%H7%H5%FH1%5%H3%h6%CD2%3%2%4%b3%

616103-412317131613720Green Party3%2%2%3%-1%2%2%2%1%1%3%3%1%2%

313911512217351161219Scottish National Party2%2%2%1%3%2%2%1%2%2%2%2%1%3%2%

51761187216351010818A coalition3%2%1%1%3%3%1%1%2%2%2%2%2%2%2%

31131-461102277511Other1%2%1%1%-1%1%1%1%1%1%1%1%1%1%

672781784916112212653244475270256133389I don't trust any34%39%37%46%45%37%38%45%f38%27%35%43%DE48%A28%39%political party to

deliver a fair pensionsystem

Page 22

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q1. Trust in political parties to deliver fair pension systemBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

21337016538425919704599155107102847798110341000Unweighted base

21**33*68*16138626220**60*40*100*16011010080*90*110*11020*1000Weighted base

916336099572141134544127312621224288Conservatives43%48%MN48%MN37%MN26%22%10%23%27%34%BC34%BC38%aBCK27%39%aBCfK29%19%20%20%29%

3511296444111810181813131722236160Labour14%14%16%18%17%17%5%18%21%hi10%11%16%13%16%19%i20%HI21%HI29%eFgHI16%

223430221-17194842710-63UKIP9%6%4%2%8%O8%O5%-2%7%K12%ADGjK4%8%dK6%k3%6%K9%adK-6%

1225156-1-44473-36-31Liberal Democrats4%6%3%3%4%2%-1%-4%d3%4%d7%Dj3%d-3%5%D-3%

211195112-3511212-20Green Party9%3%1%1%2%2%6%1%5%I-2%5%I1%1%3%1%2%-2%

---495-16-2-------119Scottish National Party---3%2%2%-27%ABCDEF-2%h-------3%BCDeFG2%

GHIJH

-1-56612111334-11-18A coalition-3%-3%2%2%5%3%2%1%1%3%3%5%bcDH-1%1%-2%

-111262-211111-2--11Other-4%N1%1%*2%N11%-5%BDHk1%1%1%1%1%-2%--1%

45185215210912161541593440234252469389I don't trust any20%17%27%33%q39%PQ42%oPQ59%27%38%41%ek37%31%40%k29%46%EGK47%EGK42%egK47%egK39%political party to

deliver a fair pensionsystem

Page 23

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q1. Trust in political parties to deliver fair pension systemBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

28164734457759913713432164291686250164455391000Unweighted base

27864734557460013313131*16028868525117**4485351000Weighted base

861918419218246---288183892132155288Conservatives31%29%24%34%M30%35%---100%GHI27%35%E10%29%29%29%

46105678410319--160-1143937285160Labour17%16%20%l15%17%14%--100%FHI-17%16%19%16%16%16%

1743223839963---38212243763UKIP6%7%6%7%7%7%49%FGH---6%9%12%5%7%6%

11181220206-31--1714-141831Liberal Democrats4%3%3%3%3%4%-100%FGI--2%5%E-3%3%3%

61281112320---145161320Green Party2%2%2%2%2%2%15%FGH---2%2%6%1%2%2%

512899319---127-81019Scottish National Party2%2%2%2%2%2%14%FGH---2%3%-2%2%2%

41231211318---142-81018A coalition1%2%1%2%2%2%14%FGH---2%1%-2%2%2%

28657-11---11--11011Other1%1%2%1%1%-9%FGh---2%D--*2%B1%

10024613620321644----283749183197389I don't trust any36%38%40%35%36%33%----41%D29%52%41%37%39%political party to

deliver a fair pensionsystem

Page 24

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q1. Trust in political parties to deliver fair pension systemBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

201711490104362975631408601612156244895111000Unweighted base

19771048710836*3025531458551612156245304701000Weighted base

299261252465227983138566164125(4) Very likely15%13%13%23%FHiJ5%15%fHj9%18%FHJ11%19%C18%C9%11%14%12%

238664666351121144637436264126(3) Fairly likely12%12%13%6%16%k21%FGHK9%8%13%HK28%CD17%C7%12%14%13%

5317211818578137232155064125128110238(2) Fairly unlikely27%24%24%16%13%26%Gjk25%Gk16%25%Gk31%C30%C20%24%23%24%

84323208312295299533941659371238209447(1) Very unlikely43%45%43%29%59%GIK31%54%FGIK36%46%GIK10%28%E59%DE45%44%45%

8363628220143134181630412464Don't know4%5%7%26%FHIJ7%7%fH2%21%FHIJ4%11%C8%5%8%a5%6%

5217812531810910339212767599123128251NET: Likely26%25%26%29%H21%36%FgHj19%27%H25%H48%CD35%C16%23%27%25%

13749532749261734377561066123496366318685NET: Unlikely69%70%67%45%73%GiK57%K79%FGIK52%71%GIK41%57%E79%DE69%68%68%

1.981.921.952.31FHJ1.642.21FHJ1.732.11fHJ1.90H2.64CD2.27C1.641.891.961.92Mean

1.091.071.071.280.951.080.981.231.040.951.090.971.051.091.07Standard deviation

0.080.040.050.150.160.070.040.120.040.080.080.040.050.050.03Standard error

Page 25

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q2. Likelihood of retirement in the next yearBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

21337016538425919704599155107102847798110341000Unweighted base

21**33*68*16138626220**60*40*100*16011010080*90*110*11020*1000Weighted base

2392447303571717118111113192125(4) Very likely11%9%13%15%12%11%16%8%18%17%f11%10%8%14%12%12%17%fk9%12%

26112144341124102314108102114-126(3) Fairly likely9%18%17%13%11%13%5%20%Aefi11%a10%a14%A12%A10%a9%a11%a19%Aefi13%A-13%

68234489504111020472631241417268238(2) Fairly unlikely29%24%34%Mn27%M23%19%20%19%25%20%29%CDik23%31%CDik30%CD15%16%24%41%BCDGI24%

K

915246418012512291549644840315256429447(1) Very unlikely42%46%35%40%47%p48%p58%49%38%49%40%44%40%39%57%BEFgH51%beh38%44%45%

J

21182623-335911106429164Don't know9%3%1%5%7%p9%P-5%9%c5%6%10%C10%C7%c4%2%8%C6%6%

49204591644171126402518192134332251NET: Likely20%27%30%28%24%24%21%28%A28%a26%A25%a23%18%24%a23%31%AF30%AF9%25%

1523471082701751640256811174715565746717685NET: Unlikely71%70%69%67%70%67%79%67%63%68%69%67%71%69%73%67%61%85%Bcegh68%

iJk

1.871.902.072.041.881.871.801.872.081.941.951.881.851.991.771.912.11aDf1.731.92Mean

1.041.031.031.091.071.071.151.031.161.151.011.040.961.071.091.101.150.921.07Standard deviation

0.240.180.120.090.060.070.260.130.180.120.080.110.100.120.130.110.110.160.03Standard error

Page 26

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q2. Likelihood of retirement in the next yearBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

28164734457759913713432164291686250164455391000Unweighted base

27864734557460013313131*16028868525117**4485351000Weighted base

3783358382211581845-125-6659125(4) Very likely13%13%10%15%m14%16%12%25%Gi11%16%-50%E-15%a11%12%

4279438165192062144-12626658126(3) Fairly likely15%12%12%14%11%14%15%19%13%15%-50%E14%15%a11%13%

7015773151139372793886238-4115119238(2) Fairly unlikely25%24%21%26%m23%28%21%29%24%30%i35%D-26%26%22%24%

109296178225280516187696447-10172265447(1) Very unlikely39%46%o52%L39%47%j38%47%FH24%47%FH33%65%D-57%38%50%B45%

2032163334571717--1293564Don't know7%5%5%6%6%4%5%3%4%6%--4%7%6%6%

79162781641474035143989-2512132117251NET: Likely28%25%23%29%M24%30%27%44%Gi24%31%-100%E14%29%A22%25%

179453251376419888917114183685-14287384685NET: Unlikely64%70%o73%L66%70%66%68%53%71%h63%100%D-83%64%72%B68%

2.031.921.802.04M1.912.09k1.912.46GI1.882.14Gi1.353.50E1.552.06A1.821.92Mean

1.081.071.031.091.091.101.071.141.051.080.480.500.751.091.041.07Standard deviation

0.070.040.060.050.050.100.100.210.080.070.020.030.190.050.050.03Standard error

Page 27

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q2. Likelihood of retirement in the next yearBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

201711490104362975631408601612156244895111000Unweighted base

19771048710836*3025531458551612156245304701000Weighted base

3982901273184191141233885876133Yes20%M12%18%M11%19%10%15%I13%13%8%15%E14%E11%16%B13%

106440266571719832973527115129356305294600No54%62%LN55%52%46%66%GhJK59%g51%62%Gjk72%CD60%57%58%63%60%

52187132401374141522153353181167100267Don't know26%26%27%37%FHI35%24%25%36%FHI25%21%25%29%E32%A21%27%

Page 28

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q3. Plan to use the new freedoms to withdraw cash from pension above the 25% tax-free allowanceBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

21337016538425919704599155107102847798110341000Unweighted base

21**33*68*16138626220**60*40*100*16011010080*90*110*11020*1000Weighted base

3414204936274142671316710253133Yes14%12%21%n13%13%14%11%12%10%14%g16%dG7%13%20%CDG8%9%22%CDfGjk14%13%

132543104224148163029698667674258685810600No62%76%MN64%65%58%57%80%50%71%aBEHK69%ABEHK54%61%67%aBeHK53%64%k62%52%50%60%

54113611377223717483621222532287267Don't know24%12%15%23%29%PQ30%PQ10%38%bFIJ18%17%30%I32%fIj21%27%i28%i29%I25%36%fIj27%

Page 29

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q3. Plan to use the new freedoms to withdraw cash from pension above the 25% tax-free allowanceBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

28164734457759913713432164291686250164455391000Unweighted base

27864734557460013313131*16028868525117**4485351000Weighted base

458225103-1331861946884036268133Yes16%13%7%18%M-100%K14%19%12%16%13%16%19%14%13%13%

179385233327600-78201031824191479261330600No65%59%67%L57%100%J-60%63%64%63%61%59%54%58%62%60%

5418088143--3463860178635125137267Don't know19%28%O25%25%--26%19%24%21%26%25%27%28%26%27%

Page 30

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q3. Plan to use the new freedoms to withdraw cash from pension above the 25% tax-free allowanceBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

4286931273088191181334905384137Unweighted base

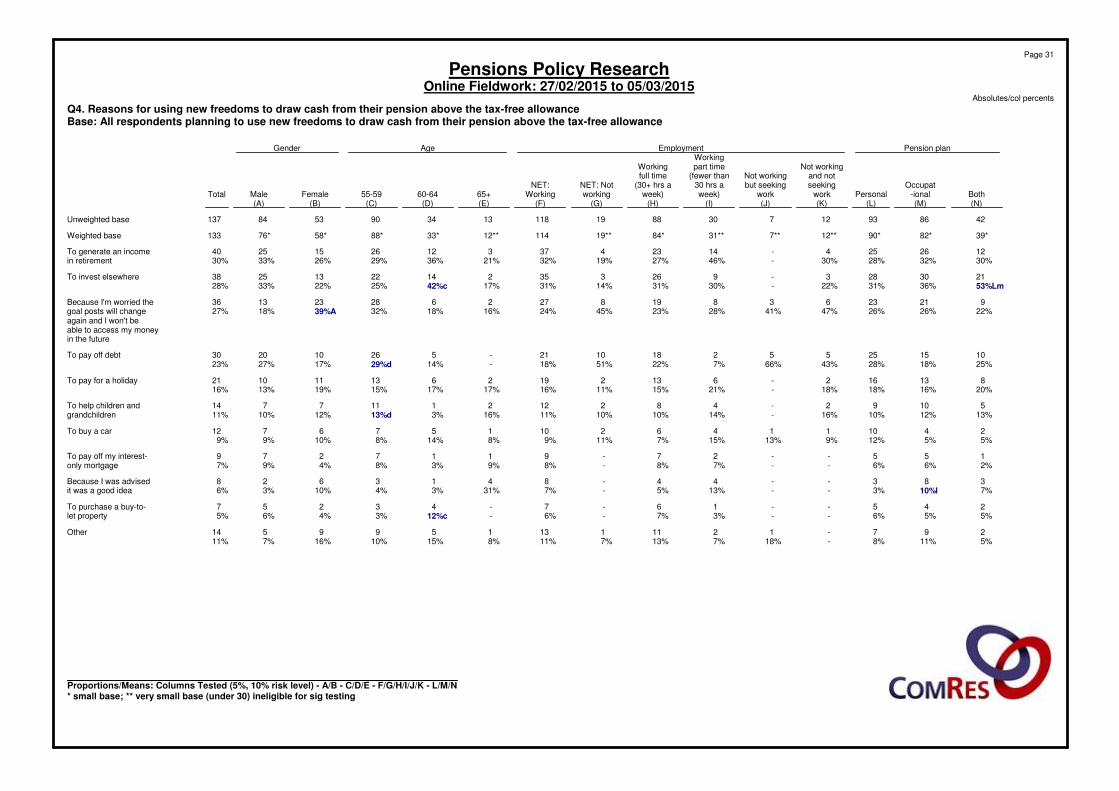

39*82*90*12**7**31**84*19**11412**33*88*58*76*133Weighted base

1226254-142343731226152540To generate an income30%32%28%30%-46%27%19%32%21%36%29%26%33%30%in retirement

2130283-92633521422132538To invest elsewhere53%Lm36%31%22%-30%31%14%31%17%42%c25%22%33%28%

92123638198272628231336Because I'm worried the22%26%26%47%41%28%23%45%24%16%18%32%39%A18%27%goal posts will change

again and I won't beable to access my moneyin the future

101525552181021-526102030To pay off debt25%18%28%43%66%7%22%51%18%-14%29%d17%27%23%

813162-6132192613111021To pay for a holiday20%16%18%18%-21%15%11%16%17%17%15%19%13%16%

51092-4821221117714To help children and13%12%10%16%-14%10%10%11%16%3%13%d12%10%11%grandchildren

241011462101576712To buy a car5%5%12%9%13%15%7%11%9%8%14%8%10%9%9%

155--27-9117279To pay off my interest-2%6%6%--7%8%-8%9%3%8%4%9%7%only mortgage

383--44-8413628Because I was advised7%10%l3%--13%5%-7%31%3%4%10%3%6%it was a good idea

245--16-7-43257To purchase a buy-to-5%5%6%--3%7%-6%-12%c3%4%6%5%let property

297-12111131599514Other5%11%8%-18%7%13%7%11%8%15%10%16%7%11%

Page 31

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q4. Reasons for using new freedoms to draw cash from their pension above the tax-free allowanceBase: All respondents planning to use new freedoms to draw cash from their pension above the tax-free allowance

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base; ** very small base (under 30) ineligible for sig testing

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

341522513529514257131769255137Unweighted base

3**4**14**20**49*36*2**7**4**14**26**7**13**16**7**10**25**3**133Weighted base

12461312-3247264129140To generate an income30%50%25%28%26%34%-35%60%29%28%29%45%24%15%23%35%19%30%in retirement

13581010-3278144116138To invest elsewhere31%74%38%38%20%28%-44%40%48%30%16%32%23%15%10%25%41%28%

-1191012-3266237--7-36Because I'm worried the-27%6%43%21%34%-35%40%44%25%31%25%42%--29%-27%goal posts will change

again and I won't beable to access my moneyin the future

1132131112-54216226-30To pay off debt39%26%21%8%26%30%54%22%-36%15%27%7%35%33%21%23%-23%

--4475-1-15143-24-21To pay for a holiday--29%19%14%14%-11%-7%21%16%31%18%-21%16%-16%

--253411113--4-12114To help children and--13%24%5%11%46%13%20%7%13%--24%-10%8%22%11%grandchildren

-1--55---132--114-12To buy a car-23%--10%15%---8%12%29%--18%10%15%-9%

1--1612----11--14-9To pay off my interest-39%--5%12%3%100%----13%8%--10%15%-7%only mortgage

---241-----1-1-1418Because I was advised---11%8%3%-----16%-5%-12%17%19%6%it was a good idea

2-11211---1--2-21-7To purchase a buy-to-70%-6%5%4%3%54%---4%--12%-21%4%-5%let property

--1184-2-311-3311-14Other--7%5%15%10%-22%-23%4%13%-17%36%12%4%-11%

Page 32

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q4. Reasons for using new freedoms to draw cash from their pension above the tax-free allowanceBase: All respondents planning to use new freedoms to draw cash from their pension above the tax-free allowance

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

458625107-1371962147914136470137Unweighted base

45*82*25**103-**13318**6**19**46*88*40*3**62*68*133Weighted base

1127436-40725172118-172340To generate an income24%32%16%35%-30%36%34%28%36%24%43%E-27%34%30%in retirement

1422632-38425142413-172138To invest elsewhere30%27%24%31%-28%24%37%24%30%27%32%-27%31%28%

1518531-36242102583102336Because I'm worried the32%22%20%30%-27%10%65%11%22%28%21%100%16%34%B27%goal posts will change

again and I won't beable to access my moneyin the future

1217622-304359245292030To pay off debt26%21%26%21%-23%23%47%26%20%28%D12%67%14%29%B23%

1011317-211-49154-111021To pay for a holiday23%13%13%16%-16%5%-20%19%17%10%-18%15%16%

41049-14122495-6814To help children and9%12%16%9%-11%5%32%13%8%10%11%-10%12%11%grandchildren

66-11-121-16102-5712To buy a car14%8%-11%-9%5%-5%14%12%5%-8%11%9%

2718-94-3263-549To pay off my interest-4%8%4%8%-7%22%-15%4%6%8%-8%6%7%only mortgage

3535-81--443-448Because I was advised7%6%14%4%-6%7%--9%4%8%-6%6%6%it was a good idea

25-7-72--252-527To purchase a buy-to-5%6%-7%-5%12%--4%6%5%-8%3%5%let property

31058-142-1610429314Other7%12%20%7%-11%9%-5%13%11%11%67%15%A4%11%

Page 33

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q4. Reasons for using new freedoms to draw cash from their pension above the tax-free allowanceBase: All respondents planning to use new freedoms to draw cash from their pension above the tax-free allowance

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

4286931273088191181334905384137Unweighted base

39*82*90*12**7**31**84*19**11412**33*88*58*76*133Weighted base

916214-519424252082028(4) Very well23%19%23%34%-17%22%22%21%20%16%23%13%27%b21%

22435044154986352343284371(3) Fairly well56%52%55%34%52%48%58%41%55%45%69%c49%49%57%53%

7161531812420451515924(2) Not very well19%20%17%23%14%28%14%19%18%35%15%17%26%A12%18%

174122537--107410(1) Not at all well2%9%5%9%34%7%6%18%6%--12%D12%5%8%

---------------Don't know---------------

315971842067128782863366399NET: Well79%71%79%68%52%65%80%62%76%65%85%71%62%83%B74%

824194311177274525221334NET: Not well21%29%21%32%48%35%20%38%24%35%15%29%38%A17%26%

3.002.822.982.932.192.752.972.652.912.853.012.822.643.05B2.87Mean

0.730.850.771.010.980.840.771.040.790.760.570.920.860.760.83Standard deviation

0.110.090.080.290.370.150.080.240.070.210.100.100.120.080.07Standard error

Page 34

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q5. Understanding of tax implicationsBase: All respondents planning to use new freedoms to draw cash from their pension above the tax-free allowance

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base; ** very small base (under 30) ineligible for sig testing

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

341522513529514257131769255137Unweighted base

3**4**14**20**49*36*2**7**4**14**26**7**13**16**7**10**25**3**133Weighted base

233410622235-42-34128(4) Very well69%73%19%19%21%17%100%33%40%22%20%-30%12%-31%15%37%21%

117122717-226154795713271(3) Fairly well31%27%52%59%54%48%-33%40%42%59%55%55%58%67%69%51%63%53%

--4496-21333251-4-24(2) Not very well--29%22%17%17%-24%20%22%12%45%15%30%15%-17%-18%

----47-1-22---1-4-10(1) Not at all well----8%18%-11%-14%9%---18%-16%-8%

-------------------Don't know-------------------

34101637232539204111151016399NET: Well100%100%71%78%75%65%100%65%80%64%79%55%85%70%67%100%66%100%74%

--441213-31553252-8-34NET: Not well--29%22%25%35%-35%20%36%21%45%15%30%33%-34%-26%

3.693.732.912.982.882.634.002.873.202.712.902.553.142.822.493.312.653.372.87Mean

0.570.510.710.650.830.980.001.070.861.000.830.540.680.640.840.490.950.600.83Standard deviation

0.330.260.180.140.120.170.000.360.380.270.170.200.190.160.340.160.190.270.07Standard error

Page 35

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q5. Understanding of tax implicationsBase: All respondents planning to use new freedoms to draw cash from their pension above the tax-free allowance

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

458625107-1371962147914136470137Unweighted base

45*82*25**103-**13318**6**19**46*88*40*3**62*68*133Weighted base

1213127-286-5916102121428(4) Very well26%16%4%26%-21%31%-28%20%18%25%67%19%21%21%

25431059-7111310264624-373471(3) Fairly well56%53%39%57%-53%59%49%51%55%52%60%-60%49%53%

8161013-2412411194-91524(2) Not very well18%20%41%13%-18%5%35%21%24%22%10%-14%23%18%

-945-1011--7214510(1) Not at all well-11%O16%4%-8%4%16%--8%5%33%7%7%8%

----------------Don't know----------------

37571186-99173153562342494899NET: Well82%69%43%83%-74%91%49%79%76%70%85%e67%79%70%74%

8251418-34234112661132034NET: Not well18%31%57%17%-26%9%51%21%24%30%d15%33%21%30%26%

3.08N2.742.313.05-2.873.182.333.082.962.803.053.002.902.842.87Mean

0.670.870.800.75-0.830.730.810.710.670.830.751.700.780.840.83Standard deviation

0.100.090.160.07-0.070.170.330.160.100.090.120.980.100.100.07Standard error

Page 36

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q5. Understanding of tax implicationsBase: All respondents planning to use new freedoms to draw cash from their pension above the tax-free allowance

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

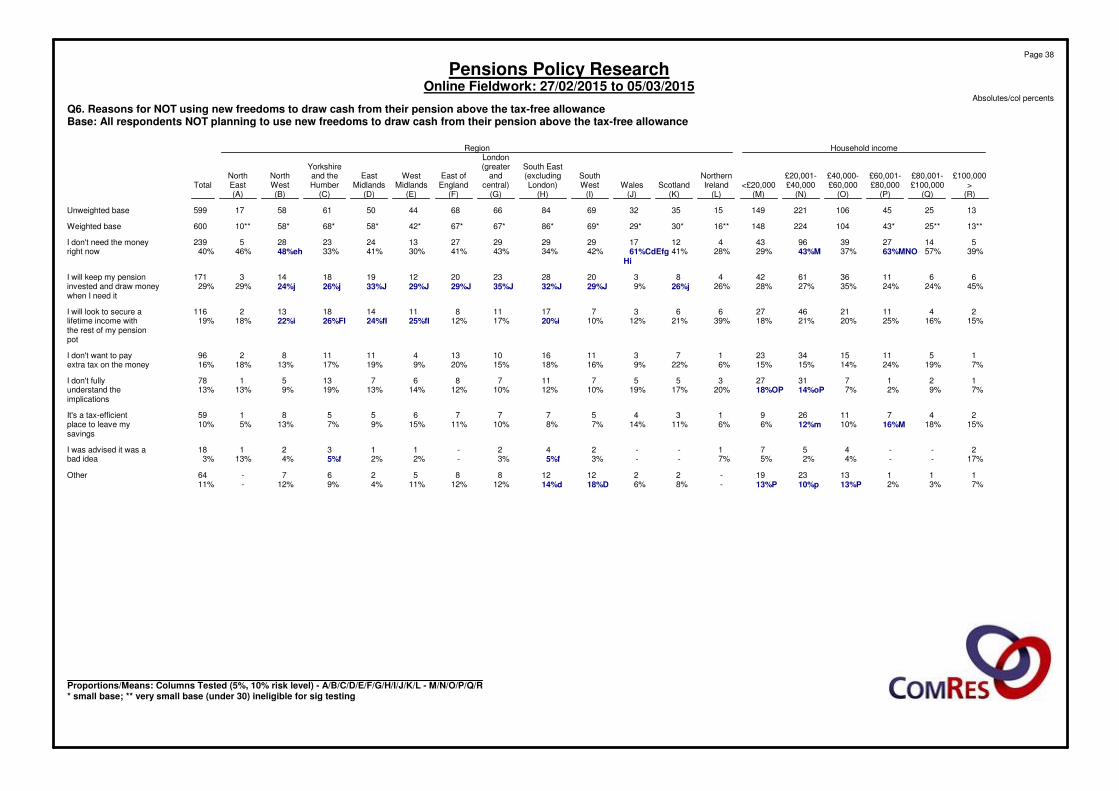

106440265551719433372527115129355281318599Unweighted base

10644026657*17**19832973*527115129356305294600Weighted base

391859415569151202203648156112127239I don't need the money37%42%l35%26%30%35%46%GIK27%42%GiK31%37%44%E37%43%40%right now

2811189135511031815422301198685171I will keep my pension27%25%33%M23%29%26%31%24%29%19%23%33%DE28%29%29%invested and draw money

when I need it

30895763386991073029575858116I will look to secure a28%m20%21%11%17%19%21%gk12%20%k26%C23%c16%19%20%19%lifetime income with

the rest of my pensionpot

2470508525581383142063375996I don't want to pay22%16%19%14%32%13%18%18%16%12%15%18%12%20%B16%extra tax on the money

1363281522140176182050483078I don't fully12%14%11%27%FHI12%11%12%24%FHI12%7%16%E14%e16%a10%13%understand the

implications

17433354133795010840194059It's a tax-efficient16%m10%12%9%22%7%11%i12%9%9%7%11%6%14%B10%place to leave my

savings

41392-610216331213618I was advised it was a4%3%3%4%-3%3%3%3%3%3%3%4%2%3%bad idea

947269135201055261721333164Other8%11%10%15%H6%18%FH6%13%H10%H23%Cd13%C6%11%11%11%

Page 37

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q6. Reasons for NOT using new freedoms to draw cash from their pension above the tax-free allowanceBase: All respondents NOT planning to use new freedoms to draw cash from their pension above the tax-free allowance

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base; ** very small base (under 30) ineligible for sig testing

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

132545106221149153532698466684450615817599Unweighted base

13**25**43*10422414816**30*29*69*86*67*67*42*58*68*58*10**600Weighted base

514273996434121729292927132423285239I don't need the money39%57%63%MNO37%43%M29%28%41%61%CdEfg42%34%43%41%30%41%33%48%eh46%40%right now

Hi

661136614248320282320121918143171I will keep my pension45%24%24%35%27%28%26%26%j9%29%J32%J35%J29%J29%J33%J26%j24%j29%29%invested and draw money

when I need it

2411214627663717118111418132116I will look to secure a15%16%25%20%21%18%39%21%12%10%20%i17%12%25%fI24%fI26%FI22%i18%19%lifetime income with

the rest of my pensionpot

151115342317311161013411118296I don't want to pay7%19%24%14%15%15%6%22%9%16%18%15%20%9%19%17%13%18%16%extra tax on the money

121731273557117867135178I don't fully7%9%2%7%14%oP18%OP20%17%19%10%12%10%12%14%13%19%9%13%13%understand the

implications

2471126913457776558159It's a tax-efficient15%18%16%M10%12%m6%6%11%14%7%8%10%11%15%9%7%13%5%10%place to leave my

savings

2--4571--242-1132118I was advised it was a17%--4%2%5%7%--3%5%f3%-2%2%5%f4%13%3%bad idea

111132319-221212885267-64Other7%3%2%13%P10%p13%P-8%6%18%D14%d12%12%11%4%9%12%-11%

Page 38

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q6. Reasons for NOT using new freedoms to draw cash from their pension above the tax-free allowanceBase: All respondents NOT planning to use new freedoms to draw cash from their pension above the tax-free allowance

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

182382232328599-80201051844181469257333599Unweighted base

179385233327600-**78*20**1031824191479**261330600Weighted base

7814886137239-3243979175554101135239I don't need the money43%38%37%42%40%-41%20%38%43%42%38%43%39%41%40%right now

4711658106171-17623631253618783171I will keep my pension26%30%25%32%m29%-21%29%23%34%GI30%25%7%34%A25%29%invested and draw money

when I need it

40725754116-1192634753824766116I will look to secure a22%19%25%L16%19%-14%45%25%i19%18%26%E25%18%20%19%lifetime income with

the rest of my pensionpot

3658345896-14511346825-336396I don't want to pay20%15%15%18%16%-18%24%11%19%g16%17%-13%19%B16%extra tax on the money

1856472378-16-141353174334178I don't fully10%14%20%L7%13%-21%F-14%f7%13%11%46%13%13%13%understand the

implications

1642213459-928214612-263359It's a tax-efficient9%11%9%10%10%-12%10%8%11%11%8%-10%10%10%place to leave my

savings

11610818-2153134-71118I was advised it was a1%4%O4%2%3%-3%5%5%f2%3%3%-3%3%3%bad idea

2335174264-8214244215-283764Other13%9%7%13%M11%-10%10%13%13%10%10%-11%11%11%

Page 39

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q6. Reasons for NOT using new freedoms to draw cash from their pension above the tax-free allowanceBase: All respondents NOT planning to use new freedoms to draw cash from their pension above the tax-free allowance

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

201711490104362975631408601612156244895111000Unweighted base

19771048710836*3025531458551612156245304701000Weighted base

173535519376473743242953(4) Very likely9%M5%7%5%3%3%7%I4%5%2%3%7%dE4%6%5%

378585962197151171737786172133(3) Fairly likely19%M12%17%M8%17%I7%17%fGIK11%14%I11%17%ce12%12%15%b13%

61173134181275140312163954153113134246(2) Fairly unlikely31%m24%28%17%33%K25%k25%k21%25%k24%25%24%21%28%B25%

45253143508137156582937381198199153352(1) Very unlikely23%36%LN29%n46%FHJ23%46%FHJ28%40%Hj34%H45%C38%32%37%33%35%

38164902695912334182283615313483217Don't know19%23%l19%24%24%20%22%24%21%17%17%25%De25%A18%22%

541201191473013421164214412085101185NET: Likely27%M17%24%M13%20%i10%24%FGIK15%19%I13%21%e19%e16%21%B19%

105426278692021329689509112135351311287598NET: Unlikely53%60%n57%63%h56%70%FgHj54%61%h60%H70%C63%c56%59%61%60%

2.16M1.822.03M1.632.001.602.04FGIK1.721.88IK1.631.83E1.93E1.771.94B1.85Mean

0.960.920.960.910.830.800.970.900.930.800.890.970.920.940.93Standard deviation

0.070.040.050.100.160.050.050.090.040.070.070.040.050.050.03Standard error

Page 40

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q7. Likelihood of saving more money into pensionBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

21337016538425919704599155107102847798110341000Unweighted base

21**33*68*16138626220**60*40*100*16011010080*90*110*11020*1000Weighted base

3361022923158466466253(4) Very likely14%8%8%m6%6%4%11%6%2%5%5%4%6%7%4%6%5%8%5%

510152356193105829171491110142133(3) Fairly likely24%30%MNO22%M14%M15%M7%15%17%i13%8%18%cI16%i14%12%13%9%12%9%13%

53204796584161318352425212627298246(2) Fairly unlikely23%9%30%Q29%Q25%Q22%q20%26%32%i18%22%22%25%26%29%i24%26%41%cfGHI25%

41119531161205151646552739312544434352(1) Very unlikely18%32%28%33%30%46%NOP27%25%40%agk46%ADGhK34%g25%39%aGk39%aGk28%40%adGk39%aGk21%35%

478289656516523323716122423194217Don't know21%20%12%17%25%OP21%p27%26%j11%23%j20%34%BCEFHJ16%15%26%ej21%17%20%22%

81321337828514613372119151517194185NET: Likely39%38%MNO31%Mn21%M20%M11%25%23%i16%13%23%I19%19%19%17%15%18%18%19%

81439100211178103129649051645351717212598NET: Unlikely40%42%57%62%Q55%68%NQ48%51%73%dGhK64%G57%47%64%Gk66%Gk57%64%Gk65%Gk62%60%

2.452.182.13M1.92M1.95M1.602.122.04I1.751.631.93I1.97I1.831.851.90i1.761.812.071.85Mean

1.061.100.980.930.950.841.110.950.820.910.960.920.940.970.880.930.920.920.93Standard deviation

0.260.210.120.080.060.060.300.130.130.100.090.110.100.110.120.110.100.180.03Standard error

Page 41

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q7. Likelihood of saving more money into pensionBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

28164734457759913713432164291686250164455391000Unweighted base

27864734557460013313131*16028868525117**4485351000Weighted base

1141143724209-14193714-173653(4) Very likely4%6%4%6%4%15%K7%-9%h7%5%5%-4%7%B5%

2510544876823196205910127-5775133(3) Fairly likely9%16%O13%15%11%17%k15%19%13%20%G15%11%-13%14%13%

7316299136161253294876168682118126246(2) Fairly unlikely26%25%29%24%27%J19%25%27%30%26%25%27%11%26%24%25%

11820111321722550451345922151127154191352(1) Very unlikely43%N31%33%38%38%38%35%42%28%32%31%45%E39%35%36%35%

501387697121152543344164308101107217Don't know18%21%22%l17%20%J12%19%12%21%15%24%D12%49%23%20%22%

36147571249343286347813841-74111185NET: Likely13%23%O17%22%m15%32%K22%19%21%27%20%16%-17%21%b19%

192363212353386757822931673831809273317598NET: Unlikely69%N56%61%62%64%j56%59%69%58%58%56%72%E51%61%59%60%

1.691.98O1.841.881.772.10K1.921.742.032.021.92D1.741.231.821.901.85Mean

0.860.960.880.970.871.140.970.800.980.960.940.900.450.880.970.93Standard deviation

0.060.040.050.040.040.100.090.150.090.060.040.060.160.050.050.03Standard error

Page 42

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q7. Likelihood of saving more money into pensionBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

201711490104362975631408601612156244895111000Unweighted base

19771048710836*3025531458551612156245304701000Weighted base

276678763470131042728615364117Yes - I am fully aware14%m9%16%M7%16%k11%13%9%12%17%C13%10%10%14%b12%of Pension Wise

1003012135011119233623526798249208205413Yes - I am aware of the51%lM42%44%46%31%39%42%43%41%42%46%40%39%44%41%guidance service but

not in detail

703431975019149251704006789314269201470No - I am not aware of36%48%LN40%47%53%49%45%48%47%41%41%50%DE51%A43%47%it

Page 43

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q8. Awareness of Pension WiseBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

21337016538425919704599155107102847798110341000Unweighted base

21**33*68*16138626220**60*40*100*16011010080*90*110*11020*1000Weighted base

5512165420473122315109812122117Yes - I am fully aware25%15%18%M10%14%M8%21%12%7%12%14%14%10%11%9%11%11%9%12%of Pension Wise

9202669159966241743654539313944547413Yes - I am aware of the42%60%MNoP38%43%41%37%29%39%42%43%41%41%39%39%43%40%49%35%41%guidance service but

not in detail

783076172145102920457250514043544411470No - I am not aware of33%24%44%q47%Q45%Q56%NoQ49%48%51%45%45%45%51%51%48%49%40%56%47%it

Page 44

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q8. Awareness of Pension WiseBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

28164734457759913713432164291686250164455391000Unweighted base

27864734557460013313131*16028868525117**4485351000Weighted base

3379219473271622144733734271117Yes - I am fully aware12%12%6%16%M12%20%K12%6%13%15%11%15%e19%9%13%b12%of Pension Wise

116277143248228535123571302751162204207413Yes - I am aware of the42%43%41%43%38%40%39%73%FGI36%45%g40%46%e14%46%A39%41%guidance service but

not in detail

12929218123229853646821153369711202257470No - I am not aware of47%45%53%L40%50%J40%49%fH20%51%FH40%H49%D39%67%45%48%47%it

Page 45

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q8. Awareness of Pension WiseBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

201711490104362975631408601612156244895111000Unweighted base

19771048710836*3025531458551612156245304701000Weighted base

22885012419811699920865857116(4) Very likely11%12%10%11%i11%6%15%I11%i12%I6%9%14%dE11%12%12%

64221148281584178442613561209157149305(3) Fairly likely32%31%30%26%42%ik28%32%30%31%22%28%33%E30%32%31%

40109781225181151323740697176147(2) Fairly unlikely20%15%16%11%6%17%g15%10%15%23%C19%C11%13%16%15%

34117931547583191585440837799177(1) Very unlikely17%17%19%14%11%25%FGHjK15%13%18%h34%CD18%c13%15%21%B18%

3817511940117413051204255417716788255Don't know19%25%24%37%FHI29%24%24%35%FHI24%15%25%E28%E31%A19%26%

853091984119102259603614581296215206421NET: Likely43%43%41%38%53%I34%47%fIk42%42%I28%38%E47%DE41%44%42%

74226171276126164332909180152148175324NET: Unlikely37%32%35%25%17%42%FGHJK30%23%34%GJk57%CD37%C24%28%37%B32%

2.462.522.422.57I2.752.202.61FI2.62I2.46I2.002.38E2.67DE2.542.432.48Mean

0.981.011.011.030.920.991.011.001.020.970.990.991.001.031.02Standard deviation

0.080.040.050.130.180.070.050.100.040.080.080.050.050.050.04Standard error

Page 46

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q9. Likelihood of using Pension Wise serviceBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

21337016538425919704599155107102847798110341000Unweighted base

21**33*68*16138626220**60*40*100*16011010080*90*110*11020*1000Weighted base

567164433657622119111313122116(4) Very likely25%18%10%10%11%12%31%8%18%I6%13%i10%9%14%i14%i11%11%12%12%

7132556120626201131474325282327387305(3) Fairly likely34%40%M36%M35%M31%M24%31%33%29%31%29%39%CdF25%35%26%25%34%35%31%

211130534031261330141871516103147(2) Fairly unlikely9%3%17%q18%Q14%q15%q16%20%BE14%13%18%BE13%18%be9%17%15%9%14%15%

4817326043-7529281622191317191177(1) Very unlikely17%23%25%n20%16%16%-11%13%29%ABCDG18%a15%22%Ak24%AK14%16%17%6%18%

HjK

35827108854171021332626152637327255Don't know15%16%12%17%28%OP32%OPq21%28%26%21%21%24%26%19%29%33%EHi29%33%e26%

121932721649412251937695334393640499421NET: Likely59%58%Mn46%45%m43%36%62%42%47%37%43%49%cFi34%49%cF40%36%45%47%42%

592862114823181142583040262834294324NET: Unlikely26%26%42%N39%N29%32%16%31%27%42%ABG36%ab28%40%ABg32%31%31%26%20%32%

2.792.632.362.422.532.483.192.54I2.69fI2.182.49I2.57fI2.282.48i2.56I2.47i2.54I2.792.48Mean

1.101.121.020.991.001.050.780.901.051.021.020.951.031.091.031.041.020.871.02Standard deviation

0.260.210.130.080.060.080.200.130.180.120.090.110.120.130.140.130.110.180.04Standard error

Page 47

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q9. Likelihood of using Pension Wise serviceBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C/D/E/F/G/H/I/J/K/L - M/N/O/P/Q/R* small base; ** very small base (under 30) ineligible for sig testing

Compulsory advice atComfort with managing ownPlan to use pensionResponsibility for financialretirementpensionfunds pre-retirementTrust in parties re. pensionsRetire in next yeardecisions

NET:NET:NET:NET:NET:NotDisagreeNET: AgreeUncomfortableComfortableNoYesOtherLDLabourConservativeUnlikelyLikelyat allJointSoleTotal

(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

28164734457759913713432164291686250164455391000Unweighted base

27864734557460013313131*16028868525117**4485351000Weighted base

1896446762261732832892424569116(4) Very likely7%15%O13%12%10%20%K13%9%18%f11%13%10%13%10%13%12%

58236105191162464794210022071-140166305(3) Fairly likely21%36%O30%33%27%35%k36%g28%26%35%g32%28%-31%31%31%

52905190104162662149895236777147(2) Fairly unlikely19%n14%15%16%17%12%20%19%13%17%13%21%E20%15%14%15%

8575581081332315629571045628887177(1) Very unlikely31%N12%17%19%22%18%12%20%18%20%I15%22%E13%20%16%18%

6414988119139222674050183479109138255Don't know23%23%25%21%23%j16%20%23%25%f17%27%D19%54%24%26%26%

7633214925722373641271133309952185234421NET: Likely27%51%O43%45%37%54%K49%38%44%46%45%d38%13%41%44%42%

137166109198237394113501061931086154164324NET: Unlikely49%N26%32%34%40%J29%32%40%31%37%28%43%E33%34%31%32%

2.052.71O2.522.472.332.68K2.622.342.582.452.59D2.312.282.422.542.48Mean

1.010.951.021.011.031.060.931.021.101.001.011.011.231.011.021.02Standard deviation

0.070.040.060.050.050.100.090.200.100.060.040.070.470.060.050.04Standard error

Page 48

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q9. Likelihood of using Pension Wise serviceBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B/C - D/E - F/G/H/I - J/K - L/M - N/O* small base; ** very small base (under 30) ineligible for sig testing

Pension planEmploymentAgeGenderWorking

Not workingpart timeWorkingand notNot working(fewer thanfull time

Occupatseekingbut seeking30 hrs a(30+ hrs aNET: NotNET:Both-ionalPersonalworkworkweek)week)workingWorking65+60-6455-59FemaleMaleTotal(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

201711490104362975631408601612156244895111000Unweighted base

19771048710836*3025531458551612156245304701000Weighted base

4916511314763145212083938152119110229(4) Strongly agree25%23%23%13%19%21%k26%GiK15%24%GK24%18%24%d22%23%23%

832972055214126225673526193264228191418(3) Tend to agree42%42%42%48%39%42%41%46%41%38%43%42%43%41%42%

421349820765972716234511059397190(2) Tend to disagree21%19%20%19%20%22%18%19%19%21%24%C17%18%21%19%

1364389529441474212048394988(1) Strongly disagree7%9%8%8%14%10%8%10%9%13%C9%8%7%10%9%

950341231842156061356512475Don't know5%7%7%11%i8%6%8%11%i7%4%6%9%E10%A5%8%

132462317672118937088560100132416347300647NET: Agree67%65%65%62%58%63%67%61%65%62%61%67%65%64%65%

56197136291295141422365570153132145278NET: Disagree28%28%28%27%34%31%h26%29%28%34%C33%C24%25%31%B28%

2.892.852.872.752.682.792.92GIk2.732.872.762.742.92De2.892.812.85Mean

0.880.910.880.830.980.910.900.870.910.980.880.880.870.930.90Standard deviation

0.060.040.040.090.170.050.040.080.030.080.060.040.040.040.03Standard error

Page 49

Pensions Policy ResearchOnline Fieldwork: 27/02/2015 to 05/03/2015

Absolutes/col percents

Q10. Agreement that receiving financial advice at retirement should be compulsoryBase: All respondents

Proportions/Means: Columns Tested (5%, 10% risk level) - A/B - C/D/E - F/G/H/I/J/K - L/M/N* small base

Household incomeRegionLondon

South East(greaterYorkshire£100,000£80,001-£60,001-£40,000-£20,001-NorthernSouth(excludingandEast ofWestEastand theNorthNorth

>£100,000£80,000£60,000£40,000<£20,000IrelandScotlandWalesWestLondon)central)EnglandMidlandsMidlandsHumberWestEastTotal(R)(Q)(P)(O)(N)(M)(L)(K)(J)(I)(H)(G)(F)(E)(D)(C)(B)(A)

21337016538425919704599155107102847798110341000Unweighted base