pension reforms in latin america - bbva

TRANSCRIPT

Pen

sion

ref

orm

s in

Lat

in A

mer

ica.

Bal

ance

an

d ch

alle

nge

s ah

ead

Pension reformsin Latin AmericaBalance and challenges ahead

This volume is a compilation of investigations that evaluates the accumulated experiences of the pension system reforms in Latin America during the past decades. As is known, the countries made valiant efforts to confront the collapse of many of their old pension systems and executed the reforms with attention to the social, economic and demo-graphic conditions of each country.

Many of the governments instituted structural changes based on the implementation of a defined contribution scheme. This scheme was based on individual administrative accounts through private specialized companies and was under strict supervision and regulation. More than two decades after the reforms had been implemented, they yielded impressive results in regards to their management and the growth of the private savings of the retired, as well as relevant results in terms of pensions granted and major social inclusion. Further-more, the pension systems had encountered in these years a global financial crisis of enor-mous magnitude, during which they had the opportunity to demonstrate their strength. However, the systems still encounter relevant challenges that need attention. One of the most important issues is the still low coverage of the pension systems, particularly in those countries with structural problems, characterized by their high levels of informality and poverty. In face of these challenges, BBVA with various years of investigation in the subject, and apart from their experience in the pension industry, has developed recommendations integrated into this book in hopes to construct a pension system that diligently addresses the great quantity of people approaching their retirement age.

Pensions reforms in Latin America.Balance and challenges ahead

Edited by:

Chap. 0 - Acknowledgments - Pensions Reforms in Latin America_Chap. 0 - Acknowledgments - Pensions Reforms in Latin America 07

Copyright© 2010 by BBVA

“Pensions reforms in Latin America.Balance and challenges ahead”

Carried out by: Pensions & Insurance and BBVA Research

The total or partial reproduction of this intellectual work is prohibited in all forms, includingthe typographical design and cover, without the written consent of the autor.

Page layout & Printing: Lateral Marketing y Comunicación, S.L. (Spain)Cover Adaptation: Bettina Ihle

Legal Deposit: M-43210-2010

Printed in Spain

Chap. 0 - Acknowledgments - Pensions Reforms in Latin America_Chap. 0 - Acknowledgments - Pensions Reforms in Latin America 07

Acknowledgments

This volume is the result of a series of studies contributed by different researcherswho have participated in the BBVA goal to spread knowledge in different areas ofstudy and thereby help create fundamental changes in the markets.

This study analyzes the progress made by Latin American countries in the reformof their pensions systems, to determine the challenges and steps to follow in thefuture. In general, the present work is the first phase of the in-depth reviews thatwe have undertaken of the pension systems in Chile, Colombia, Mexico, and Peru,which have been published in corresponding books over the last five years. Thesestudies are based on the development of macro-actuarial models that not onlyprovide us with an important methodological contribution, but have also been in-formed by statistics compiled at a level of detail that no other study of pensionplans in the region has benefited from.

The projections given in the various chapters of the study point to better prospectsfor the retirement of upcoming generations while the system gradually improves.However, it clearly indicates that these individual systems will need refining to getcloser to those segments of the population that will continue to be less protected.It will be necessary to create and implement proposals to sort out these difficul-ties, by improving economic policies, providing the countries with the productivitylevels they require to grow on the long term and maintain a necessary savingsbase. We believe that the most important contributions of this book are to befound in the model developed, the conclusions given, and the proposals for con-sideration.

This volume is the result of the joint efforts of several persons who have sup-ported the project in various phases. With this in mind, the editors reiterate theirsatisfaction with the relevant research alliance between BBVA Pensions and In-surance and BBVA Research for the development of these projects. Also, thiswork would not be the same without the industry knowledge gathered from theexperiences of José María Aragoné, Rafael Carranza, Francisco González Almaraz,Jorge Matuk, Carmen Pérez de Muniaín, Ricardo Rodríguez Marengo, EnriqueSummers, and Patricio Urrutia. The editors would also like to thank Ángel Melguizoand Juan Yermo, researchers at the OECD’s Development Centre and the Financialand Enterprise Affairs Department, respectively, for their collaboration in chapters2 and 7 of this volume.

3

Chap. 0 - Acknowledgments - Pensions Reforms in Latin America_Chap. 0 - Acknowledgments - Pensions Reforms in Latin America 07

We also want to highlight the key collaboration of BBVA chief economists in LatinAmerica, especially Adolfo Abo, Alejandro Puente, Hugo Perea, Juana Téllez, andJoaquín Vial. Finally, we would like to thank all who have contributed to publishthis book at the different specific stages of the project, in particular the importantcollaboration in analysis and coordination offered by Ivonne Ordoñez, as well asGonzalo Larrañaga, for his contribution to the design and realization of the book.

4

Chap. 0 - Acknowledgments - Pensions Reforms in Latin America_Chap. 0 - Acknowledgments - Pensions Reforms in Latin America 07

Contents

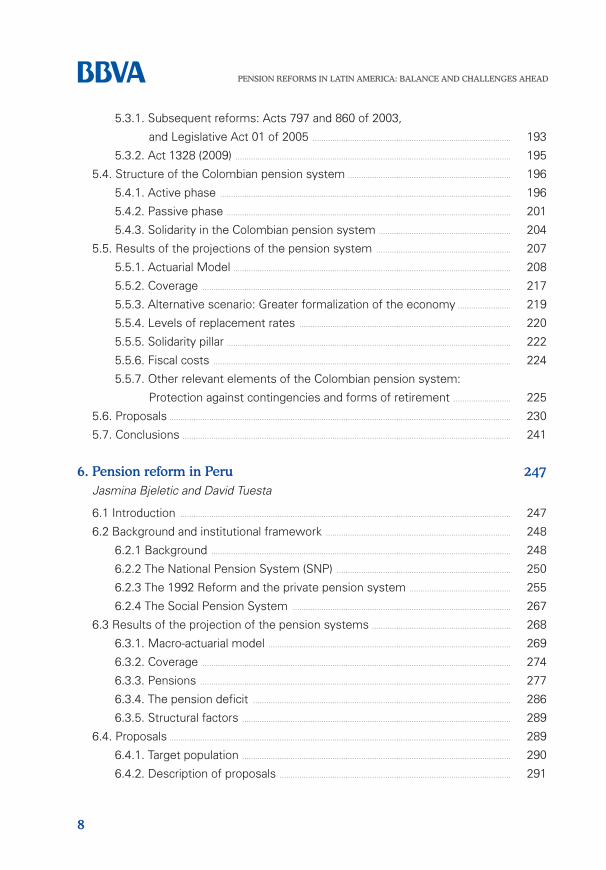

1. Assessment of Pension Reforms in Latin America 11

José Luis Escrivá, Eduardo Fuentes and Alicia García-Herrero

1.1. The Former Pension System............................................................................................................... 12

1.2. Pension system reforms ....................................................................................................................... 14

1.2.1. Structural reforms ....................................................................................................................... 14

1.2.2. Investment Reforms .................................................................................................................. 18

1.2.3. Demographic and Economic Factors ............................................................................. 22

1.3. Achievements and challenges of the reform ......................................................................... 28

1.3.1. The Capital Market ...................................................................................................................... 28

1.3.2. Fiscal Sustainability ..................................................................................................................... 29

1.3.3. Replacement Rates .................................................................................................................... 31

1.3.4. Coverage ............................................................................................................................................ 32

1.3.5. Labor markets and Informality ............................................................................................ 35

1.4. Conclusions ..................................................................................................................................................... 37

2. The unavoidable role of private pensions in retirement

income systems 39

Juan Yermo

2.1. Introduction ..................................................................................................................................................... 39

2.2. Driving forces behind pension reforms ...................................................................................... 40

2.2.1. Main types of reforms being implemented around the world .................... 42

2.3. Impact of reforms on the sustainability, adequacy and equity

of pension systems ................................................................................................................................... 46

2.4. Policy implications of the growing importance of prefunding and the

shift to defined contribution................................................................................................................. 48

2.5. Concluding remarks .................................................................................................................................. 51

3. Pension reform in Chile 53

Soledad Hormazábal

3.1. Background ...................................................................................................................................................... 53

3.1.1. The former pension system in Chile .............................................................................. 53

5

Chap. 0A - Contents - Pensions Reforms in Latin America_Chap. 0A - Contents - Pensions Reforms in Latin America 07/10/10 19:33 P

3.1.2. The need for a reform of the pension system ........................................................ 55

3.1.3. Transition to the new pension system ......................................................................... 56

3.2. The individual capitalization pension system .......................................................................... 59

3.2.1. Pillar Zero: welfare pensions and minimum pensions ...................................... 60

3.2.2. Pillar Two: obligatory saving ................................................................................................. 61

3.2.3. Pillar Three: voluntary saving ............................................................................................... 70

3.3. The 2008 pension reform ...................................................................................................................... 72

3.3.1. Assessment and proposals: 25 years on from the reform

of the Chilean pension system .......................................................................................... 73

3.3.2. The Presidential Advisory Council .................................................................................... 73

3.3.3. Coverage in the obligatory pillar of the Chilean pension system .............. 74

3.3.3.1. Measures in the 2008 reform to increase coverage

under the obligatory pillar of the Chilean

pension system .......................................................................................................... 80

3.3.4. Coverage in the solidarity pillar of the Chilean pension system ................ 81

3.3.4.1. Measures in the 2008 reform to perfect the solidarity

pillar of the Chilean pension system ........................................................... 84

3.3.5. Coverage in the voluntary pillar of the Chilean pension system ............... 86

3.3.5.1. Measures in the 2008 reform to extend the coverage

of the voluntary pillar of the Chilean pension system ....................................... 87

3.3.6. Gender elements .......................................................................................................................... 88

3.3.6.1. Measures contained in the 2008 reform to improve

gender equity ............................................................................................................... 91

3.3.7. Investment rules ........................................................................................................................... 92

3.3.7.1. Measures of the 2008 reform to perfect the

investment rules ........................................................................................................ 94

3.3.8. Benefits and contribution rates .......................................................................................... 95

3.3.8.1. Measures in the 2008 reform that resolve inequities in

the benefits of the contributory pillar of the

pension system .......................................................................................................... 96

3.3.9. Organization of the industry and competition ......................................................... 98

3.3.9.1. Measures in the 2008 reform that tackle aspects

of competition in the AFP industry ................................................................................. 103

3.4. Proposals ........................................................................................................................................................... 105

3.4.1. Proposals for perfecting the assessment of pension

fund investments ......................................................................................................................... 106

6

PENSION REFORMS IN LATIN AMERICA: BALANCE AND CHALLENGES AHEAD

Chap. 0A - Contents - Pensions Reforms in Latin America_Chap. 0A - Contents - Pensions Reforms in Latin America 07/10/10 19:33 P

3.4.2. Proposals to increase coverage in the second pillar

during the active life in the Chilean pension system ......................................... 107

3.4.3. Proposals to increase coverage in the passive stage

of the Chilean pension system .......................................................................................... 109

3.5. Conclusions ..................................................................................................................................................... 116

4. Towards stronger pension systems in Mexico:

vision and proposals for reform 121

Carlos Herrera

4.1. Introduction ..................................................................................................................................................... 121

4.2. Background ...................................................................................................................................................... 123

4.2.1. Social security and pensions in Mexico ....................................................................... 123

4.2.2. Coverage ............................................................................................................................................ 127

4.2.3. Mainly defined benedit schemes ..................................................................................... 131

4.3. Reform of the Pension System ........................................................................................................ 134

4.3.1. Reform of the IMSS pension system ........................................................................... 134

4.3.2. Reform of the ISSSTE pension system ....................................................................... 138

4.3.3. Pensions and the mechanisms for retirement savings .................................... 142

4.3.4. Regulation and competition in the Afore industry ............................................... 153

4.4. Results of the projection of the pension system ................................................................ 157

4.4.1. Macro-actuarial model .............................................................................................................. 158

4.4.2. Coverage ............................................................................................................................................ 166

4.4.3. Pension levels and replacement rates .......................................................................... 167

4.4.4. Fiscal Costs ...................................................................................................................................... 169

4.4.5. Other considerations ................................................................................................................. 171

4.5. Proposals ........................................................................................................................................................... 175

4.6. Conclusions ..................................................................................................................................................... 181

4.7. Appendix ............................................................................................................................................................ 184

5. Confidence in the future: Proposals for an improved

pension system in Colombia 189

María Claudia Llanes and Javier Alonso

5.1. Introduction ..................................................................................................................................................... 189

5.2. Background ...................................................................................................................................................... 190

5.3. The 1993 pension reform and subsequent reforms ......................................................... 192

CONTENTS

7

Chap. 0A - Contents - Pensions Reforms in Latin America_Chap. 0A - Contents - Pensions Reforms in Latin America 07/10/10 19:33 P

5.3.1. Subsequent reforms: Acts 797 and 860 of 2003,

and Legislative Act 01 of 2005 .......................................................................................... 193

5.3.2. Act 1328 (2009) ............................................................................................................................. 195

5.4. Structure of the Colombian pension system .......................................................................... 196

5.4.1. Active phase .................................................................................................................................... 196

5.4.2. Passive phase ................................................................................................................................. 201

5.4.3. Solidarity in the Colombian pension system ............................................................ 204

5.5. Results of the projections of the pension system ............................................................. 207

5.5.1. Actuarial Model .............................................................................................................................. 208

5.5.2. Coverage ............................................................................................................................................ 217

5.5.3. Alternative scenario: Greater formalization of the economy ........................ 219

5.5.4. Levels of replacement rates ................................................................................................ 220

5.5.5. Solidarity pillar ................................................................................................................................. 222

5.5.6. Fiscal costs ....................................................................................................................................... 224

5.5.7. Other relevant elements of the Colombian pension system:

Protection against contingencies and forms of retirement .......................... 225

5.6. Proposals ........................................................................................................................................................... 230

5.7. Conclusions ..................................................................................................................................................... 241

6. Pension reform in Peru 247

Jasmina Bjeletic and David Tuesta

6.1 Introduction ...................................................................................................................................................... 247

6.2 Background and institutional framework .................................................................................... 248

6.2.1 Background ........................................................................................................................................ 248

6.2.2 The National Pension System (SNP) ............................................................................... 250

6.2.3 The 1992 Reform and the private pension system .............................................. 255

6.2.4 The Social Pension System ................................................................................................... 267

6.3 Results of the projection of the pension systems ............................................................... 268

6.3.1. Macro-actuarial model .............................................................................................................. 269

6.3.2. Coverage ............................................................................................................................................ 274

6.3.3. Pensions ............................................................................................................................................. 277

6.3.4. The pension deficit ..................................................................................................................... 286

6.3.5. Structural factors .......................................................................................................................... 289

6.4. Proposals ........................................................................................................................................................... 289

6.4.1. Target population .......................................................................................................................... 290

6.4.2. Description of proposals ......................................................................................................... 291

8

PENSION REFORMS IN LATIN AMERICA: BALANCE AND CHALLENGES AHEAD

Chap. 0A - Contents - Pensions Reforms in Latin America_Chap. 0A - Contents - Pensions Reforms in Latin America 07/10/10 19:33 P

6.5 Impact evaluation ......................................................................................................................................... 296

6.5.1. Coverage ............................................................................................................................................ 296

6.5.2. Pensions ............................................................................................................................................. 296

6.5.3. Pension deficit ................................................................................................................................ 297

6.6. Conclusions ..................................................................................................................................................... 298

7. The challenge of developing the Solidarity Pillar 303

Angel Melguizo, Angel Muñoz, David Tuesta and Joaquín Vial

7.1. Motivation ......................................................................................................................................................... 303

7.2. The promise and outcome of pension reform: the fiscal impact ............................. 304

7.3. On-going reform: strengthening the redistributive system ......................................... 311

7.4. Reforms in Colombia, Peru and Mexico: work in progress ......................................... 318

7.5. To conclude: on the exportability of the Chilean model ................................................. 325

7.5.1. Market and public institutions ............................................................................................. 325

7.5.2. Gradual development of financial markets ................................................................ 325

7.5.3 Fiscal policy and transition design .................................................................................... 326

7.5.4. Informal labour market and solidarity pillar ................................................................ 327

7.6. Annex ................................................................................................................................................................... 329

8. Lessons for the Future 335

José Luis Escrivá, Eduardo Fuentes and Alicia García-Herrero

8.1. Summary of proposals ............................................................................................................................ 336

9. Bibliography 347

CONTENTS

9

Chap. 0A - Contents - Pensions Reforms in Latin America_Chap. 0A - Contents - Pensions Reforms in Latin America 07/10/10 19:33 P

Chap. 0A - Contents - Pensions Reforms in Latin America_Chap. 0A - Contents - Pensions Reforms in Latin America 07/10/10 19:33 P

1. Assessment of Pension Reforms in

Latin America

José Luis Escrivá, Eduardo Fuentes and Alicia García-Herrero

The major transformations affecting the world since the last century have led tothe urgent need for a reform of pension systems. These reforms may have variedfrom country to country, but their ultimate goals have been very similar, as JuanYermo explains well in Chapter 2. These common factors in developed and emerg-ing economies have paved the way towards improving the system, whether byway of supplementing it or introducing new plans for action.

The last two decades have seen major reforms in Latin America, especially in itspension systems. Twelve countries1 have modified their pension plans, in line withChile’s pioneering experience (1981). The changes have been parametric (such asincreasing contribution rates and raising the retirement age), but above all struc-tural. These structural reforms have been based on incorporating a system of in-dividual (obligatory or voluntary) capitalization2 with the private sector participatingfully or jointly in the administration of pension funds3. This new approach to dealingwith the retirement problem aimed to adapt to the new challenges and risks con-fronting countries due to the weakness of public finance, changes in birth rate,greater population longevity, public administration efficiency problems and greaterdevelopment potential for financial markets.

In Chile, Colombia, Mexico and Peru, particular financial, economic, social and po-litical conditions dictated the reforms, although with some common objectives.These included: achieving greater transparency; increasing returns; attracting con-tributors; increasing voluntary savings; guaranteeing payment of social securitycontributions; promoting competition among fund administrators and providingsavers with more choice; generating capital accumulation; controlling the fiscal

11

Chapter 1

1 Chile (1981), Peru (1992), Colombia (1993), Argentina (1994), Uruguay (1996), Mexico and El Salvador (1997),Bolivia (1998), Costa Rica and Nicaragua (2000), Ecuador (2001) and the Dominican Republic (2003).

2 The case of Brazil is worth noting, as it used a combined strategy (notional systems) in the obligatory pillar. Ac-cording to Bertranou (2004), Brazil introduced its reform for workers in the private sector in 1999 and in the publicsector in 2003-2004.

3 Bertranou, August 2004.

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 11

cost of switching between systems; developing new markets; diversifying port-folios; increasing gender equality; making gradual progress in non-contributorywelfare pension plans; and developing new regulations.

The results have been spectacular. Workers actively participating in the reformedsystems have gained much higher real returns than alternative saving plans. Pro-jected replacement rates (pension level compared to the average of last wagesreceived) are very reasonable for the future generations of retirees. However, asignificant percentage of workers still do not pay into pension systems becauseof the major problems still affecting Latin American economies. There are twomain factors that still hold back the potential of pension system reforms: the largeinformal economy and low income levels in large segments of the population, lim-iting the possibility of building up long-term savings.

Nevertheless, as these limiting factors are gradually solved, reformed pension sys-tems have a lot of potential. Now that the reforms have been underway for a num-ber of years, the current situation needs to be analyzed in detail. This analysis canserve as a basis for outlining new measures to strengthen these plans and extendcoverage in the countries concerned, ensuring decent pensions and improving thefinancial profile of pension systems. This detailed analysis has been carried out inthis book with a particular focus on the case studies of Chile, Colombia, Mexicoand Peru, and in this particular chapter we want to present an overview of thesestudies in terms of trends and comparisons. First, the former pension system isdescribed in general terms. Then we will look at the structural reforms in each ofthe four countries taken to create their new pension systems. That will be followedby an analysis of the structural economic factors that condition the results of thepension systems, which need to be reviewed in parallel, before ending with ananalysis of the achievements and challenges that are still pending.

1.1. The Former Pension System

At the start of the 20th century most Latin American countries introduced the de-fined-benefit pay-as-you-go plan into their pension systems. The pioneering coun-tries (1910-1930) to implement it were Uruguay, Argentina, Chile and Brazil; theintermediate countries (1940-1950) were Mexico, Peru, Colombia, Bolivia,Ecuador, Paraguay, Costa Rica and Venezuela; and the last ones (1960-1970) wereEl Salvador, Nicaragua, the Dominican Republic, Guatemala and Honduras.

The pension systems were organized and administered by public social securityinstitutions, and the state undertook to provide a broad range of guarantees and

12

PENSION REFORMS IN LATIN AMERICA: BALANCE AND CHALLENGES AHEAD

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 12

benefits. Initially, the income from worker contributions was much higher thanthe retirement obligations. As a result, there were political incentives for govern-ments to impose low contribution rates and generous pensions. Over the years,the number of retirees grew and a parallel demographic transition towards a so-ciety with a longer life expectancy began. It was no longer possible to continueto deliver the same pension levels under the existing rules. However, instead ofmaking the necessary adjustments (lower benefits and/or increased contribu-tions), governments tended to keep, and in some cases even increase, pensions.They were then forced to finance the pension system debt through greater fiscaldeficits.

This situation was made worse by a run of unfortunate economic policies that re-duced the growth potential of the countries involved. The lack of strict fiscal andmonetary discipline brought about a climate of high inflation and thus huge distor-tions for economic agents4. Other well-intending policies were undertaken simul-taneously, but were far removed from market realities. In fact, they increasedmarket inefficiencies, for example, excessive protection for workers was intro-duced which greatly limited the employer’s power to dismiss workers and in-creased minimum wages above the level of labor productivity5. There was nolonger much incentive to recruit, this unemployment rates rose and a significantpart of the population was forced into the informal economy.

Other problems included poor government administration at the time and lack oftransparency in running welfare systems. In almost every case, pension fund fi-nancial management was not efficient and, as a result, real returns on assetsunder management were negative. At the same time, more politically-biased orshort-sighted decisions were taken, leading in many cases to retirement fundsbeing used to finance public works or the central government’s revenue expen-diture.

This situation resulted in countries’ positions becoming unsustainable and gener-ated the need for a comprehensive reform in pension systems. Parametricchanges were required to ensure the financial viability of public systems (such asdelaying the retirement age, increasing contributions, limiting early retirement,and rationalizing benefits in accordance with the actuarial profile). Structuralchanges were also considered to be vital. These included the implementation ofpension plans based on individual obligatory saving accounts.

ASSESSMENT OF PENSION REFORMS IN LATIN AMERICA

13

4 This particularly affected workers who faced significant real losses in their pensions. For an analysis of the potentialrisks of inflation for pension funds, see Whitehouse (2009).

5 Pagés (2010) reviews the policies that could be the key to continuing to boost productivity in the region.

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 13

CHART 1.1: Real returns on some publicpension plans in the 1980s

1.2. Pension system reforms

Chile, Colombia, Mexico and Peru decided to make adjustments to their pay-as-you-go defined-benefit plan (in some cases eliminating the pay-as-you-go scheme) withindividual defined-contribution accounts. Each country adapted it to its own financial,economic, social, political and social security situation. The traditional, publicly-man-aged pay-as-you-go plan6 became more individual in character and involved privatepension saving managers7. The new plan focused on saving and insuring the indi-vidual, as well as the pension benefits, were dependent on individual savings.

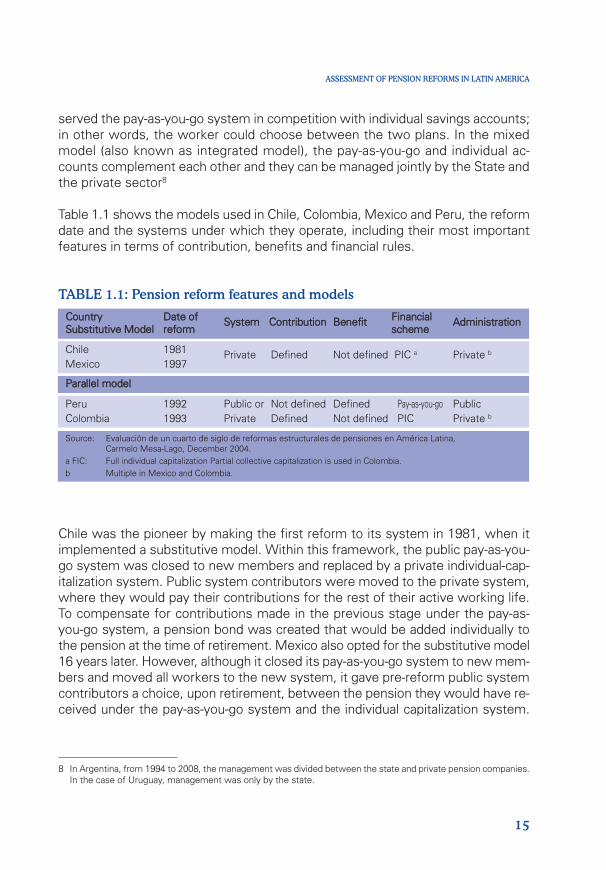

1.2.1. Structural reforms

The individual-account defined-contribution plan was implemented in differentforms, which authors have called substitutive, parallel and mixed models. Thesubstitutive model ended the pay-as-you-go scheme and replaced it with onebased on privately-managed individual savings accounts. The parallel model pre-

14

PENSION REFORMS IN LATIN AMERICA: BALANCE AND CHALLENGES AHEAD

-5%

-10%

-11%

-12%

-15%

-24%

-37%

-40% -30% -20% -10% 0%

Jamaica

Ecuador

Costa Rica

Egypt

Venezuela

Turkey

Peru

Source: Averting the Old-Age Crisis: Policies to Protect the Old and Promote Growth. New York. Oxford University. World Bank (1994)

6 The public system has a non-defined contribution, a defined benefit, a pay-as-you-go or collective partial capital-ization financial scheme and public administration (Mesa-Lago 2004).

7 The private system has defined contribution, non-defined benefit, full and individual capitalization financial schemeand a private administration, although it may be multiple (public, private and mixed) (Mesa-Lago 2004).

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 14

served the pay-as-you-go system in competition with individual savings accounts;in other words, the worker could choose between the two plans. In the mixedmodel (also known as integrated model), the pay-as-you-go and individual ac-counts complement each other and they can be managed jointly by the State andthe private sector8

Table 1.1 shows the models used in Chile, Colombia, Mexico and Peru, the reformdate and the systems under which they operate, including their most importantfeatures in terms of contribution, benefits and financial rules.

TABLE 1.1: Pension reform features and models

Chile was the pioneer by making the first reform to its system in 1981, when itimplemented a substitutive model. Within this framework, the public pay-as-you-go system was closed to new members and replaced by a private individual-cap-italization system. Public system contributors were moved to the private system,where they would pay their contributions for the rest of their active working life.To compensate for contributions made in the previous stage under the pay-as-you-go system, a pension bond was created that would be added individually tothe pension at the time of retirement. Mexico also opted for the substitutive model16 years later. However, although it closed its pay-as-you-go system to new mem-bers and moved all workers to the new system, it gave pre-reform public systemcontributors a choice, upon retirement, between the pension they would have re-ceived under the pay-as-you-go system and the individual capitalization system.

ASSESSMENT OF PENSION REFORMS IN LATIN AMERICA

15

8 In Argentina, from 1994 to 2008, the management was divided between the state and private pension companies.In the case of Uruguay, management was only by the state.

Country Date of System Contribution Benefit Financial AdministrationSubstitutive Model reform scheme

Source: Evaluación de un cuarto de siglo de reformas estructurales de pensiones en América Latina,Carmelo Mesa-Lago, December 2004.

a FIC: Full individual capitalization Partial collective capitalization is used in Colombia.b Multiple in Mexico and Colombia.

Chile 1981 Private Defined Not defined PIC a Private b

Mexico 1997

Peru 1992 Public or Not defined Defined Pay-as-you-go PublicColombia 1993 Private Defined Not defined PIC Private b

Parallel model

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 15

Meanwhile, Peru (1992) and Colombia (1993) opted for a parallel model with thechoice between a pay-as-you-go or a individual-capitalization system.

The private individual-capitalization system generally has two components: oneobligatory and the other voluntary. The obligatory part obliges workers to becomemembers and make contributions according to a legal contribution rate. The vol-untary component gives workers the option of increasing their retirement savingsby defining the amount that they want to add to their privately-managed assets.In both cases, contributions benefit from deferred taxation. In most cases, theamount accumulated in the individual account cannot be withdrawn until retire-ment, though there are exceptions in certain circumstances (Mesa-Lago 2004).

The finer details of these systems were adapted to each country’s particular situa-tion. In Chile, the new system was radically different from the previous one. It wasconceived as a system for saving in which worker contributions throughout theirworking life financed the pension. These contributions were part of an individual ac-count managed by the Pension Fund Administrators (AFPs). The state concentratedexclusively on operating the non-contributory pension plan. This subject will be dealtwith in more detail in Chapter 3 by Soledad Hormazabal and in the analysis in Chap-ter 7 by Ángel Melguizo, Ángel Muñoz, David Tuesta and Joaquín Vial.

In the case of Colombia, in Chapter 5 Maria Claudia Llanes and Javier Alonso de-scribe how at the start of the 1990s the pension system faced major finance andcoverage problems. The country choose a parallel system in which average pre-miums with defined benefits (RPM) coexisted with a system of individual savingswith a welfare element (RAIS). Members can only belong to one of the two, unlikein countries such as Uruguay and Costa Rica, where they can contribute to bothsystems. The reform objectives were three-fold: fiscal balance, increased cover-age and greater equity. The Colombian pension system conditions were set outin Law 100, 1993. Greater coverage, equity, efficiency and financial sustainabilityof the pension system have been the main aims of the various reforms undertakensince the first half of the 1990s.

As Carlos Herrera explains in Chapter 4, Mexico introduced a system that radicallytransformed the institutional design of pension plans. For the first time in the his-tory of the country’s social security system, people were guaranteed ownershipover their pension savings. The introduction of a defined-contribution plan underthe Mexican Social Security Institute (IMSS), backed by the public and private sec-tors, was also a step towards a better-equipped pension system. This was a startto solving the problems bogging down the old pension plan9, which was not fi-

16

PENSION REFORMS IN LATIN AMERICA: BALANCE AND CHALLENGES AHEAD

9 We refer to the Disability, Old-Age, Unemployment at Advanced Age and Death Insurance (IVDM).

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 16

nanced in the long term and was extremely vulnerable to demographic change,involving major guarantees on the government’s part.

In Peru, in Chapter 6 Jasmina Bjeletic and David Tuesta explain how, following the1992 pension reform, the system comprised two parallel models. The first is theNational Pension System (SNP), which the Office of Pension Standardization(ONP) manages, running under a pay-as-you-go system. The second is the PrivatePension System (SPP), which came into operation in July 1993. It is managed pri-vately by AFPs that is in charge of an individual-capitalization scheme under thesupervision of the Superintendency of Banking and Insurance. Given the large in-formal sector in the Peruvian economy and the need to extend pension coverageto low-income workers, the government has been taking steps to tackle this prob-lem. In June 2008, Legislative Decree No. 1086 was passed to give micro-enter-prise10 and SME11 employees more access to pension systems, either under theSNP or SPP. A welfare pension system was also established, targeted exclusivelyat micro-enterprise12 employees.

The individual-account defined-contribution plan was aimed at a more efficient man-agement of workers’ assets and the channeling of public resources towards moredisadvantaged groups, bearing in mind fiscal restrictions. The measures adopted were:

• Specialist management to improve contribution collection and the investmentof pension assets in financial holdings with a good risk-return balance.

• Supervision and regulation to balance the interests of the different parties in-volved in the pension industry, above all protecting the ownership of funds. Lawsstipulate clear trustee obligations for AFPs.

• Regulatory criteria to evaluate the risk-return trade-off, prudent holding manage-ment and capital market intervention, qualitative and quantitative limits on theassets in which AFPs can invest, among others.

ASSESSMENT OF PENSION REFORMS IN LATIN AMERICA

17

10 Within the scope of Decree No 1086, the micro-enterprise must satisfy the following characteristics: (i) one toten employees and annual sales up to a maximum of 150 applicable tax units (UIT, equivalent to S/. 3,600 in2010).

11 Under Decree No. 1086, the small enterprise must satisfy the following characteristics: (i) one to one hundredemployees and annual sales up to the maximum total of 1,700 applicable tax units (UIT, equivalent to S/. 3,600in 2010).

12 While this book was being prepared, the Presidential Message of July 28, 2010 announced the Government Pro-ject to develop a law aimed at providing a non-contributory pension for old people in a situation of extreme poverty.

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 17

• Insurance plans to allow pension funds to mitigate risks related to death andemployment incapacity.

• Where a public pay-as-you-go plan was kept, it was adjusted to the country’sdemographic and financial background.

A system was therefore consolidated where greater importance was attached tothe sense of ownership of retirement contributions by including individual accountsand a regulatory framework that ensured proper management. These regulationsapplied to the pay-as-you-go system, where contributions were collective yet in-tangible and guaranteed by proper finance management with more governmenttransparency. In the private case, strict regulations also ensured the individual prop-erty rights to each member’s savings. The pension reform also encouraged efficientuse of the state budget, had an impact on labor markets, improved productivity,gave a boost to economic institutions, fostered the development of financial mar-kets and in general had a global impact on long-term economic growth. Accordingto Schmidt-Hebbel (2003), in Chile the reform contributed 0.49 percentage pointsto an average GDP growth of 4.63% in the 1981-2001 period. The reform thereforeaccounted for 4.62% of the GDP in 2001. Since the reform was introduced 22 yearsago, it has had a substantial direct and indirect impact on the country’s outputthrough fiscal financing, accumulation and use of factors of production and the lev-els of efficiency with which these are used.

1.2.2. Investment Reforms

The management of pension fund holdings began to improve following the re-forms undertaken. Of particular note was the introduction of investment rulesthat allowed specialist institutions to invest in efficient holdings, in accordancewith the regulations in force. These regulations were gradually adapted to a morecompetitive system that allowed pension fund administrators to invest the sav-ings entrusted to them responsibly in different types of assets, and at the sametime gave an important boost to the capital market. The pension fund adminis-trators and capital markets formed a virtuous circle for countries which had apositive impact on the growth of managed pension assets, as can be seen inChart 1.2.

This new plan led to new regulatory changes, for example, individual accountscould not be treated equally because the system now included new youngmembers and older people on the verge of retirement. This gave rise to multi-fund plans.

18

PENSION REFORMS IN LATIN AMERICA: BALANCE AND CHALLENGES AHEAD

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 18

CHART 1.2: Funds as percentage of GDP (%)

i) The multi-fund scheme13

Investment rules in each country to a large extent depend on the assessment that pub-lic policymakers make of financial market development. These results in regulationsclearly focused on quantitative limits or more flexible plans to supervise fund managerbehavior through management indicators. Although rigid, strict plans aim to make con-tributor savings more secure, they could generate a poor risk-return balance.

Multi-fund plans help to balance investor and contributor risk profiles, and allowpension companies to manage investments in a defined number of portfolio dif-ferentiated by risk exposure. This greater or lesser return volatility tolerance ineach portfolio depends on the type of contributor, who in theory can choose whichfund they want to invest their savings in, with certain restrictions.

The financial documentation reviewed in Taguas and Vidal-Aragón (2005) hasshown that the right portfolio depends on the type of market, regulations and thetype of person (such as level of risk aversion, age, wealth and productivity). Multi-funds allow the contributors’ different characteristics and risk profile to be takeninto account in accordance with their employment status.

ASSESSMENT OF PENSION REFORMS IN LATIN AMERICA

19

0%

10%

20%

30%

40%

50%

60%

70%

1986

19

87

1988

19

89

1990

19

91

1992

19

93

1994

19

95

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

Chile (1982-2009) Colombia (1994-2009) Mexico (1997-2009) Peru (1993-2009)

Source: BBVA Research

13 Muñoz, A., Romero, C., Tellez, J., & Tuesta, D. (2009). Confianza en el Futuro: Propuestas para un Mejor Sistemade Pensiones BBVA Colombia, Publisher: Norma pp. 54-58.

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 19

In Chile, the system has been in operation since 200214. This new system gavecontributors the option of investing their pension savings in one of the five fundsestablished (they can choose up to two). Each worker, except those close to re-tirement age, is free to switch funds. If they do not choose an option, Chilean leg-islation established a default option that assigns members to three of the fivetypes of funds depending on their age: up to 35, Fund B (relatively volatile); from36 to 50 for women and 36 to 55 for men, Fund C (intermediate); and from 51 forwomen and 56 for men, Fund D (relatively safe). There are investment limits thatdepend on the type of instrument and on the fund, with maximum and minimumlimits for exposure to equity instruments. Throughout the 1990s, Chile also madeits financial regulations more flexible and allowed more equity instrument partici-pation in investment funds, hedging instruments, asset-backed securities and for-eign instruments, with a maximum limit on foreign instruments in 2008 of 45%.By March 2010, more than 3.8 million contributors (25% of the total) had chosenthe type of fund for themselves.

In Peru, multi-funds began operating in 200515. Three funds were created. If nofund was chosen, new contributors were assigned to Fund 2, except workers over60 years of age, who were assigned to Fund 1. There is no requirement on movingcontributions between funds. Pension companies can manage up to three typesof obligatory savings funds, and they can also offer more voluntary saving funds.Let us now look at the different types of funds. The purpose of Fund 1, also knownas the capital preservation fund, is to guarantee steady growth with low volatility.Fund 1 is obligatory for all contributors over the age of 60 and for those with aprogrammed retirement pension, unless the worker expresses an intention to joinFund 2. The minimum age for acquiring the right to a retirement pension is 65.Fund 2, or the mixed fund, aims to provide moderate growth with average volatil-ity. Finally, Fund 3, or the capital appreciation fund, aims to maximize growth andcan be subject to high volatility. The investment limits were defined in accordancewith the financial nature of the instruments (level of exposure to fixed-income orequity). Other limits on holdings were also defined, such as total investments ininstruments that the Peruvian government has issued or guaranteed, total invest-ments in instruments that the Central Reserve Bank of Peru has issued or guar-anteed, and investment abroad. In 2009, Fund 2, which came into force in 1993,recorded a real annualized return of 8.8% during its 16 years in operation. Funds1 and 3 have recorded real yields of 6.2% and 21.8% respectively over the lastfour years.

20

PENSION REFORMS IN LATIN AMERICA: BALANCE AND CHALLENGES AHEAD

14 See Chapter 3.15 See Chapter 6.

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 20

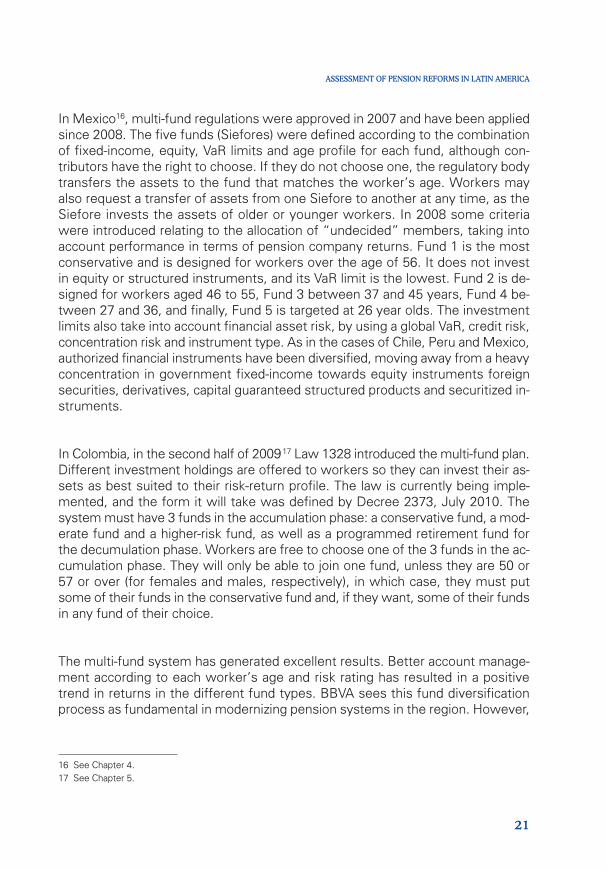

In Mexico16, multi-fund regulations were approved in 2007 and have been appliedsince 2008. The five funds (Siefores) were defined according to the combinationof fixed-income, equity, VaR limits and age profile for each fund, although con-tributors have the right to choose. If they do not choose one, the regulatory bodytransfers the assets to the fund that matches the worker’s age. Workers mayalso request a transfer of assets from one Siefore to another at any time, as theSiefore invests the assets of older or younger workers. In 2008 some criteriawere introduced relating to the allocation of “undecided” members, taking intoaccount performance in terms of pension company returns. Fund 1 is the mostconservative and is designed for workers over the age of 56. It does not investin equity or structured instruments, and its VaR limit is the lowest. Fund 2 is de-signed for workers aged 46 to 55, Fund 3 between 37 and 45 years, Fund 4 be-tween 27 and 36, and finally, Fund 5 is targeted at 26 year olds. The investmentlimits also take into account financial asset risk, by using a global VaR, credit risk,concentration risk and instrument type. As in the cases of Chile, Peru and Mexico,authorized financial instruments have been diversified, moving away from a heavyconcentration in government fixed-income towards equity instruments foreignsecurities, derivatives, capital guaranteed structured products and securitized in-struments.

In Colombia, in the second half of 200917 Law 1328 introduced the multi-fund plan.Different investment holdings are offered to workers so they can invest their as-sets as best suited to their risk-return profile. The law is currently being imple-mented, and the form it will take was defined by Decree 2373, July 2010. Thesystem must have 3 funds in the accumulation phase: a conservative fund, a mod-erate fund and a higher-risk fund, as well as a programmed retirement fund forthe decumulation phase. Workers are free to choose one of the 3 funds in the ac-cumulation phase. They will only be able to join one fund, unless they are 50 or57 or over (for females and males, respectively), in which case, they must putsome of their funds in the conservative fund and, if they want, some of their fundsin any fund of their choice.

The multi-fund system has generated excellent results. Better account manage-ment according to each worker’s age and risk rating has resulted in a positivetrend in returns in the different fund types. BBVA sees this fund diversificationprocess as fundamental in modernizing pension systems in the region. However,

ASSESSMENT OF PENSION REFORMS IN LATIN AMERICA

21

16 See Chapter 4.17 See Chapter 5.

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 21

this improvement needs to be combined with a more flexible risk regulation. Bymoving away from a highly-centralized investment policy-making system to onein which contributors are free to design part of their holding (fixed-income andequity ratio), the risk associated with concentration in the local market (domesticbond bias) could be aggravated18.

1.2.3. Demographic and Economic Factors

Although the new pension plan resulted in a more structured, organized and di-versified system, some flaws still need to be ironed out. The new plan interactswith other external factors, which partially or totally influences the final outcome.Demographic and economic variables have to be considered when making newstructural reforms: on a macroeconomic scale, labor market and capital market re-forms; and on a microeconomic scale, welfare programs and institutional reforms.This will improve coverage levels, replacement rates, fiscal sustainability, amongother direct parameters.

Population changes and the economic growth trend are two determining factorsfor pension funds. A growing life expectancy and higher birth rate place pressureon pay-as-you-go systems. Private systems will also be affected, as greaterlongevity will mean that future generations will gradually have to work longer andsave more of their income to get by when they are no longer part of the activelabor market. Economic stability and economic growth factors are also core vari-ables that will determine the level of savings needed for retirement.

I) Demographic Factors

a) Ageing

In the 1980s and 1990s, the population aged 65 years and over only representedan average 5.9% of the total population in Chile, 4.1% in Colombia, 4.0% in Mex-ico and 3.8% in Peru (Chart 1.3). In absolute terms, in accordance with CEPALpopulation statistics, in 1990 there were around 620,000 people of retirement agein Chile, 1,085,000 in Colombia, 2,599,000 in Mexico and 627,000 in Peru.

When the countries in the region were starting out on their demographic transitionduring these decades, in other words when the average workforce age was falling,

22

PENSION REFORMS IN LATIN AMERICA: BALANCE AND CHALLENGES AHEAD

18 See Chapter 8. See also Hinz et al (2010) about the evaluation of the financial performance of pension funds.

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 22

the system could have accumulated significant reserves. However, this did nothappen because the surpluses were used to finance the public deficit. The finan-cial situation in the systems worsened as the average workforce age increased.Benefits also increased and investment of balances brought low or zero real ratesof return.

CHART 1.3: Population aged 65 years or over (%)

From 2000 onwards, the increase in the population aged 65 years and over showsa steeper curve, and accounts for 7.2% in Chile, 4.7% in Colombia, 5.2% in Mex-ico and 4.8% in Peru. The sustained growth of the older population in these coun-tries is therefore a major challenge for their pension systems. This has led in theshort term to the search for pension plans that can cater for those who have notbeen able to save (and may find themselves in a position of helplessness), as wellas the inclusion of these workers in pension systems. Alternatives must also befound to tackle the financial problems that longevity risk brings with it for both thepay-as-you-go and individual capitalization plans.

According to CEPAL population estimates (see Chart 1.4) for 2050, the elderly pop-ulation will represent 20% in Chile and Mexico, 18% in Colombia and 16% in Peru.An adjustment of the systems is inevitable, given that the number of individuals ofworking age is falling, while the number of people at retirement age is increasing.

ASSESSMENT OF PENSION REFORMS IN LATIN AMERICA

23

0

5

10

15

20

25

1950

1960

1970

1980

1990

2000

2010

2020

2030

2040

2050

Source: CEPAL

Chile Colombia Mexico Peru

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 23

CHART 1.4: Population aged 65 yearsand over (%)

b) Life Expectancy

Another point to consider is life expectancy. In Chile, Colombia, Mexico and Peru,life expectancy for both men and women is increasing year by year, and with itthe number of months and/or years during which pensions have to be paid out. Inthe 1980s the average life expectancy for the four countries was around 67. Bythe 1990s this had increased to 70 and now, between 2010 and 2050, it is be-tween 76 and 80 respectively19 (see Chart 1.5).

c) Dependency Rate

According to the BBVA model, the dependency rate20 shows that the populationat retirement age will exceed the working age population in 2050. For example, inChile and Mexico the dependency rate will be at around 35%. In Colombia, at thebeginning of the 21st century, the dependency rate represents a ratio of 21 pen-sioners to 100 contributors, when in 1980 it was only 2 pensioners to 100 mem-bers. In Peru, the rate will be 24% (see Chart 1.6).

24

PENSION REFORMS IN LATIN AMERICA: BALANCE AND CHALLENGES AHEAD

5.6

3.8 3.8 3.6

7.2

4.7 5.2 4.8

9.0

5.66.5 6.0

22

18

21

16

0

5

10

15

20

25

Chile Colombia Mexico Peru

Source: CEPAL

1980 2000 2010 2050

19 CEPAL estimates.20 1) Albo, Adolfo, Fernando González, Ociel Hernández, Carlos A. Herrera and Ángel Muñoz (2007), “Hacia el Fort-

alecimiento de los Sistemas de Pensiones en México: Visión y Propuestas de Reforma”, 2) Favre, M., Melguizo,A., Muñoz, A., & Vial, J. (2006). A 25 años de la reforma del sistema de previsión chileno. Evaluación y propuestasde ajuste BBVA Chile, 3) Muñoz, A., Romero, C., Tellez, J., & Tuesta, D. (2009). Confianza en el Futuro: Propuestaspara un Mejor Sistema de Pensiones BBVA Colombia, Publisher: Norma, 4) Bernal, N., Muñoz, A., Perea, H., Tejada,J., & Tuesta, D. (2008). Una mirada al sistema de pensiones peruano: diagnóstico y propuestas BBVA Peru, Pub-lisher: Norma. http://serviciodeestudios.bbva.com/KETD/ketd/esp/nav/tematicas/pensiones/historico/libros/index.jsp

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 24

CHART 1.5: Life expectancy, both genders(average number of years)

CHART 1.6: Dependency Rate

Because the pension system clearly still faces major challenges due to demo-graphic changes, governments are analyzing new proposals to make improve-ments21.

ASSESSMENT OF PENSION REFORMS IN LATIN AMERICA

25

30

40

50

60

70

80

90

1950

_195

5

1955

_196

0

1960

_196

5

1965

_197

0

1970

_197

5

1975

_198

0

1980

_198

5

1985

_199

0

1990

_199

5

1995

_200

0

2000

_200

5

2005

_201

0

2010

_201

5

2015

_202

0

2020

_202

5

2025

_203

0

2030

_203

5

2035

_204

0

2040

_204

5

2045

_205

0

Source: CEPAL

ChileColombia

MexicoPeru

0%

5%

10%

15%

20%

25%

30%

35%

40%

2005

20

07

2009

20

11

2013

20

15

2017

20

19

2021

20

23

2025

20

27

2029

20

31

2033

20

35

2037

20

39

2041

20

43

2045

20

47

2049

Source: BBVA Research

Mexico ChilePeruColombia

21 See Chapter 8.

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 25

II) Macroeconomic Factors

During the 1980s and 1990s, most countries in the region experienced consider-able macroeconomic instability, due to the policies in place and poor public admin-istration management. Examples of this were a high level of bureaucracy andserious problems with corruption. Mexico and Peru faced hyperinflation periodswith low or zero growth. Peru, in particular, recorded average inflation of over7,000% in 1990, with a GDP decline of 5.4%. Pension systems inevitably becamea reflection of the economy’s performance.

The high inflation and low growth scenario in various Latin American economiesfor more than a decade prompted some governments to adopt structural re-forms. Chile had already embarked on this process of changes in the 1980s, butthe rest of Latin America only started on the same path in the 1990s. Drasticstabilization programs were the initial measure applied, with the aim of eliminat-ing distortion in the goods markets, factors of production and fiscal and monetarypolicy management. Governments then began to catch on to the core impor-tance of making these policies ironclad against intervention from politicians. Fis-cal rules were established to keep the public deficit balanced, and central bankswere given more independence to make decisions. Having established themacroeconomic framework for the policies, changes were gradually introducedto make the government’s role more productive. These changes include pensionsystem reform with the inclusion of privately-managed capitalization. The newprograms controlled inflation, and on average growth rates have tended to recordpositive trends. Latin American economies have not been unaffected by the re-cent global turbulence though, as happened in the mid-1990s with the Tequilacrisis in Mexico, the Asian and Russian crisis in the late 1990s and the recentglobal financial crisis. However, Latin America has steadily shown increasingstrength to reduce economic pounding and an ability to bounce back when facedwith the changes on the international scene.

Table 1.2 shows how economic consolidation has run parallel to the introductionof pension reforms. The second column shows how average economic growthhas remained at reasonable levels since the system was created. The third columngives growth rates in these countries during the last decade, which is in keepingwith the consolidation of pension system reforms and other reforms. The fourthcolumn shows the major changes in output during the recent financial crisis, whilethe last column shows the growth forecasts for 2010 and Latin America’s strongability to recover, in stark contrast to the developed world.

26

PENSION REFORMS IN LATIN AMERICA: BALANCE AND CHALLENGES AHEAD

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 26

CHART 1.7: Macroeconomic situationin the four countries

According to Corbo and Schmidt-Hebbel (2003), a 10% increase in the size of pen-sion funds has an impact of 0.1 pp in accumulated savings. These authors also re-veal that an increase of one percentage point in pension funds as a proportion ofGDP has an impact of between 1 and 5 points of GDP in savings, as can be seenin Chart 1.8.

ASSESSMENT OF PENSION REFORMS IN LATIN AMERICA

27

0

10

20

30

40

50

60

70

80 19

92

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Annual Average Inflation (%)

Source: BBVA Research with official data

Chile Colombia Mexico Peru

-10

-5

0

5

10

15

1990

19

91

1992

19

93

1994

19

95

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

Real GDP (%)

Source: BBVA Research with official data

Chile Colombia Mexico Peru

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 27

TABLE 1.2: Average GDP (%)

CHART 1.8: Impact of GDP on savings

1.3. Achievements and challenges of the reform

Pension system reforms in the four Latin American countries have brought aboutmajor changes and benefits, but there are still challenges that need to be ad-dressed.

1.3.1. The Capital Market

Capital markets have performed better since the introduction of multi-fundplans. Returns have been gained since the start of the system reforms in Chile,

28

PENSION REFORMS IN LATIN AMERICA: BALANCE AND CHALLENGES AHEAD

Country Growth from Growth over 2009 Projectionsthe start of the last for 2010*the system 10 yearsto 2010* (2001-2010*)

Source: BBVA Research* estimate by BBVA Research

Chile (1981) 4,7 3,7 -1,5 4,8Colombia (1994) 3,3 4,0 0,8 4,2Mexico (1997) 2,8 1,7 -6,6 4,5Peru (1993) 5,2 5,5 0,9 6,8

Source: Cobo & Schmidt-Hebbel 2003

* Ortogonal variables of demography rate and education level

Real and Forecast

Domestic Saving Rate(% of GDP)

PF Stock (% of GDP)

6,0

4,0

2,0

0,0

-2,0

-4,0

-6,0

-8,0

-10,0

-12,0

-30,0 -15,0 0,0 15,0 30,0 45,0 60,0

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 28

Colombia, Mexico and Peru, as mentioned above. The diversification of privatepension funds has evolved over the years. Currently in Chile there is greater ex-posure to foreign issues, with 45% of holdings in these instruments. However,in Mexico, Colombia and Peru there is still room to increase investment of hold-ings abroad. Mexico, for example, currently invests only 4.0% of its total abroad(see Table 1.3).

TABLE 1.3: Diversification of holdings by financialinstrument (%) (June 30, 2010)

BBVA’s actuarial model for Mexico cited in Chapter 4 shows that the new IMSSpension system has the capacity to continue strengthening financial saving in theMexican economy. This will help deepen and develop the country’s financial mar-kets and improve the allocation of resources. In addition, more flexible investmentrules will allow improved financing of viable productive activities with high eco-nomic returns. The market needs to therefore consider broadening its opportuni-ties, by developing more proposals for investment regulation22.

1.3.2. Fiscal Sustainability

By introducing new pension system reforms in terms of fiscal impacts, the fiscalcost of the pay-as-you-go system was reduced to different extents in the fourcountries. The public deficit has not disappeared though, and in some countries itcontinues to pose a problem. To calculate the deficits more accurately, an actuarialmodel was prepared for each of the countries (an explanation of them is given ineach of the chapters).

ASSESSMENT OF PENSION REFORMS IN LATIN AMERICA

29

Instruments Chile Colombia Mexico Peru

Source: BBVA Research* Fixed-income

Government securities 10,1 42,0 66,0 19,2Financial 17,3* 5,1 16,0 9,5Non-financial 11,2* 6,0 …. 11,1Stocks 14,6 33,5 13,0 30,3Mutual funds and others 2,4 0,0 …. 3,1Foreign issues 45,0 11,6 4,0 23,4Others -0,6 1,8 1,0 3,4

22 See Chapter 8.

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 29

In Mexico, it was clear that despite the major fiscal benefits that were implicitlyachieved by replacing the pay-as-you-go scheme with defined-contribution, thetransition between systems in the IMSS still represents a significant fiscal effort(54.6% of the GDP in 2004). Public sector pensions are still an important sourceof loss of internal savings and pressure on public finances. This is because pensionfunds that still operate in most public bodies (semi-state companies, universitiesand local governments) do so under pay-as-you-go plans and register serious fi-nancial imbalances.

In Peru, at the current value, the deficit represents 57.9% of the GDP in 2006. Al-though significant in comparison with macroeconomic ratios such as debt/GDP, itdoes not represent such a high cost compared to before the reform and comparedto what other countries in the region face. In Colombia, recent RPM-ISS recordsreveal that there is actually a financial imbalance in this system’s accounts whichcould have significant fiscal effects in the future. Since 2004, when the RPM-ISSreserves had been used up, the national government has undertaken to financethe pension deficits.

Chart 1.9, according to Zviniene & Packard 2004, shows the estimated pensiondeficit with or without reform as a percentage of the GDP for Colombia and Chile.This estimate shows that if the new reforms had not been introduced in Colombiaor Chile, the pension deficit could have been more than 300% and 150%, respec-tively. However, although this trend was avoided, there are still fiscal challengesahead.

CHART 1.9: Estimated pension deficit with and without reform(as percentage of GDP)

30

PENSION REFORMS IN LATIN AMERICA: BALANCE AND CHALLENGES AHEAD

Colombia

Source: Zviniene & Packard 2004

400%

201 203 205

No reform

Reform

300%

200%

100%

0%

Chile

Source: Zviniene & Packard 2004

200%

201 203 205

No reform

Reform

150%

100%

50%

0%

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 30

1.3.3. Replacement Rates

One of the main reasons behind pension system reforms is better access to aproper pension. The reformed systems generate better replacement rates as aresult of economic trends and private pension administrator management. How-ever, in the future, pensions will depend to a great extent on whether differentpopulation groups are able to save, and this in turn depends on access to the for-mal labor market. This may be closed off to broad sections of society in somecountries, where informality and unemployment rates are high.

In this situation, a divergence can be seen in replacement rates in different popu-lation segments. Groups who can remain in the labor market for longer obtainfairly high replacement rates, while those whose time on the market has been cutshort or who have not joined the market have lower pension levels. This can beseen in Chart 1.10.

CHART 1.10: Replacement rates (%)

Obviously, the solution to the problem of low-contribution-density groups is notdirectly related to pension systems, but rather to the country’s structural situa-tion. Problems such as informality, how labor markets operate and income in-equality require specific reforms, and their solution will have an effect on pensionsystems. Progress will be important in terms of replacement rates and systemcoverage.

ASSESSMENT OF PENSION REFORMS IN LATIN AMERICA

31

0%

20%

40%

60%

80%

100%

120%

140%

A2 B2 C2 A1 B C A2 B2 C2 A B C

Source: BBVA Research

Mexico Chile Peru Colombia

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 31

1.3.4. Coverage

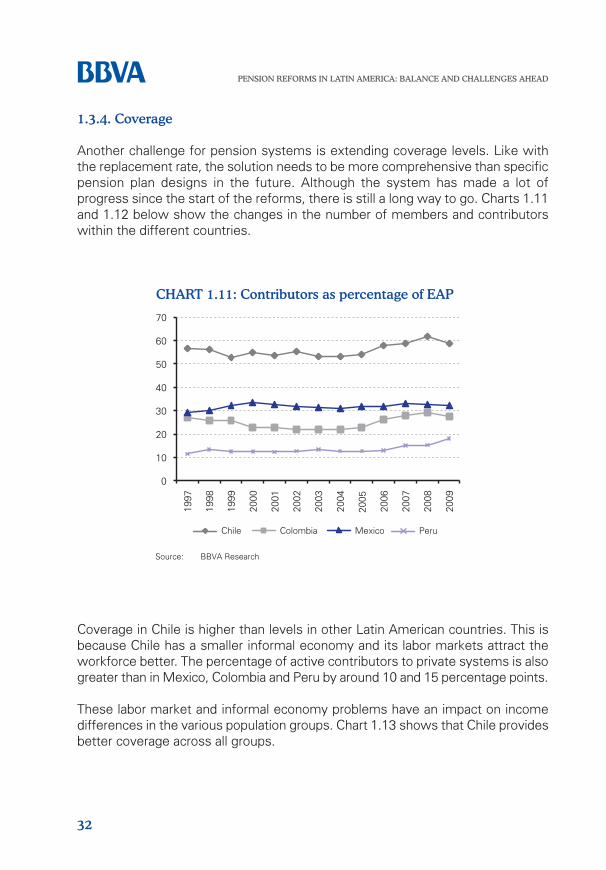

Another challenge for pension systems is extending coverage levels. Like withthe replacement rate, the solution needs to be more comprehensive than specificpension plan designs in the future. Although the system has made a lot ofprogress since the start of the reforms, there is still a long way to go. Charts 1.11and 1.12 below show the changes in the number of members and contributorswithin the different countries.

CHART 1.11: Contributors as percentage of EAP

Coverage in Chile is higher than levels in other Latin American countries. This isbecause Chile has a smaller informal economy and its labor markets attract theworkforce better. The percentage of active contributors to private systems is alsogreater than in Mexico, Colombia and Peru by around 10 and 15 percentage points.

These labor market and informal economy problems have an impact on incomedifferences in the various population groups. Chart 1.13 shows that Chile providesbetter coverage across all groups.

32

PENSION REFORMS IN LATIN AMERICA: BALANCE AND CHALLENGES AHEAD

0

10

20

30

40

50

60

70

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Source: BBVA Research

Chile Colombia Mexico Peru

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 32

CHART 1.12: Percentage of members whocontribute actively to private systems

CHART 1.13: EAP coverage by quintiles(Q1=poorest, Q5=richest)

ASSESSMENT OF PENSION REFORMS IN LATIN AMERICA

33

30

35

40

45

50

55

60

2004 2005 2006 2007 2008 2009

Source: BBVA Research

MexicoChile PeruColombia

0

20

40

60

80

100

Chile(2003)

Mexico(2004)

Argentina(2006)

Colombia(1999)

Peru(2003)

Source: Lucchetti and Rofman (2006)

Q3Q1 Q4 Q5Q2

Chap. 1 - Pensions Reforms in Latin America_Chap. 1 - Pensions Reforms in Latin America 13/10/10 12:21 Página 33

Although the solution to these problems requires resolute action outside the pen-sion system, governments have adopted new measures actions to mitigate cov-erage problems. For example, Colombia has introduced an integrated system ofsocial security contribution payments (starting June 30, 2005). This system allowspayment of monthly social security contributions and other parafiscal paymentsthrough electronic transfers using the PILA Integrated Contribution SettlementTemplate. This controls and monitors social security contributions more closely.Other regulations were later introduced to try to attract more independent workersand company employees23.

In Peru, competition, formalization and development of micro-enterprises andSMEs was established in June 2008. The aim behind the law is to include thelargest number of workers possible in the pension system and increase the lowcoverage level. In addition, the creation of the SPS (Sistema de Pensiones So-ciales-Welfare Pension System) included the approval of a voluntary monthly con-tribution above the minimum contribution24, thus extending pension coverage byup to two times. However, it has not been consolidated due to the implicit factorsmentioned above.

In Mexico, a reality that the defined-contribution scheme in the IMSS faces is thata large number of contributors do not have high contribution densities. These con-tributors include self-employed workers, temporary workers and those whose em-ployment status changes frequently, from employed to unemployed orindependent workers and vice-versa. Even though at some time in their lives theymight be members of an Afore, their life as active contributors is limited in mostcases to the time during which they were formal wage-earners. There is thereforeconcern that new proposals for reforms should be made25.