pension fund management and international investment … · 236 pensions vol. 10, 3, ... importers...

TRANSCRIPT

from diversification more thancompensates for the additional element ofvolatility arising from currencymovements.

Several ways may be envisagedwhereby a strategy of internationaldiversification should reduce risk.Crucially, to the extent that nationaltrade cycles are not correlated and shocksto equity markets tend to becountry-specific, the investment of partof the portfolio in other markets canreduce systematic risk for the samereturn. In the medium term, the profitshare in national economies may movedifferentially, which implies thatinternational investment hedges the riskof a decline in domestic profit share andhence in equity values.5 And in the verylong term, imperfect correlation of

Issues ininternational investment

Arguments favouring internationalinvestment

Modern portfolio theory3 suggests thatholding a diversified portfolio of assets ina domestic market can eliminateunsystematic risk resulting from thedifferent performance of individual firmsand industries, but not the systematic riskresulting from the performance of theeconomy as a whole. In an efficient andintegrated world capital market,systematic risk would be minimised byholding the global portfolio, whereinassets are held in proportion to theirdistribution by current value between thenational markets.4 In effect, theimprovement in the risk-return position

236 Pensions Vol. 10, 3, 236–261 � Henry Stewart Publications 1478-5315 (2005)

Pension fund management andinternational investment —A global perspectiveReceived: 14th January, 2005

E. Philip Davisis Professor of Economics and Finance at Brunel University, Visiting Fellow at the National Institute of Economic and SocialResearch, an associate member of the Financial Markets Group at LSE, Associate Fellow of the Royal Institute ofInternational Affairs and Research Fellow of the Pensions Institute at Birkbeck College, London.

Abstract This paper1 seeks to clarify the role of international investment in pensionfund investment strategies.2 It draws on experience of Organisation for EconomicCooperation and Development (OECD) countries and of selected emerging marketeconomies (EMEs) with established funded pension systems. It looks at aspects ofinternational investment, empirically, at domestic and international asset returns of thereturns and two policy issues — namely arguments for and against pension fundportfolio regulations limiting international investment and the implications for capitalflows and asset prices of ageing in the coming decades.

Keywords: pension fund investment strategies; emerging market economies (EMEs);international investment; pension fund portfolio regulations

E. Philip DavisDepartment of Economicsand Finance,Brunel University,Room SS251, Uxbridge,Middlesex UB8 3PH, UK.

Tel: �44 (0)1895 203 172;Fax: �44 (0)1895 203 384;e-mail:[email protected]

capital in lower-wage countries (egKorea) which may be attractive toinvestors.8 For investors in certainmarkets, international investment may bestimulated by the unavailability of certaininstruments in the home market such asindex-linked bonds. Equally, internationalinvestment avoids the risk of catastrophicfailure of domestic financial markets dueto war, revolution or other disasters, as hashappened to Germany and Japan in 1945and Russia in 1917. In the special case ofJapanese pension funds, investment inforeign assets provides a hedge against thepossibility of a catastrophic domesticearthquake.

Finance-theory arguments forinternational investment9 apply stronglyto emerging markets. In manydeveloping countries the financialmarkets may themselves be poorlydeveloped, offering only bank deposits.Even where they are active, securitiesmarkets may be highly vulnerable topolicy related or external macroeconomicshocks, leading to high and variableinflation that are damaging to the valueof domestic financial assets. If thedomestic currency tends to depreciateowing to inflation, real returns onforeign assets will be boosted, at leasttemporarily. Even more than for smallerOECD countries, the domestic stockmarket may itself be poorly diversified,being dominated by a small number ofcompanies, or unduly exposed to onetype of risk. There will be manyindustries offshore which are not presentin the domestic economy, investment inwhich will reduce risk. Small markets —particularly in developing countries —may be inherently volatile and illiquidboth due to their inherent characteristicsand the entry and exit of foreigninstitutional investors.2 If there are highermean returns in emerging markets thanin OECD countries then there would bea trade-off of return and risk in investing

demographic shifts should offerprotection against the effects on thedomestic economy of ageing of thepopulation.6 In effect, internationalinvestment in countries with a relativelyyoung population may be essential toprevent battles over resources betweenworkers and pensioners in countries withan ageing population, which could occureven with funding as pensioners consumepart of that country’s gross domesticproduct (GDP).7

Supporting arguments may be derivedfrom the special circumstances ofindividual countries or from inefficienciesin global capital markets. There may beindustries offshore (oil, gold mining etc)which are not present in the domesticeconomy, investment in which willreduce unsystematic risk even if tradecycles were correlated. If oil priceschange it is best to hold assets in bothoil exporters (who benefit from an oilprice rise and lose from a fall) andimporters (vice versa). A highdependency on oil would imply a higherweighting towards oil producers.

The domestic stock market may itselfbe poorly diversified, being dominated bya small number of large companies (eg theNetherlands), or unduly exposed to onetype of risk (eg Canada and rawmaterials). If the domestic currency tendsto depreciate (as in the past in the UK),real returns on foreign assets will beboosted correspondingly, and vice versafor appreciation (although in the long run,real returns will be equalised if purchasingpower parity holds). This implies anadditional inflation hedge. Othereconomies (eg the US in recent years)may be more successful in terms ofgrowth than the domestic economy andhence offer higher total returns, givenstock market returns ultimately depend ondividends, which in turn are a function ofprofits and GDP growth. Similarly, theremay be a higher marginal productivity of

� Henry Stewart Publications 1478-5315 (2005) Vol. 10, 3, 236–261 Pensions 237

International investment — A global perspective

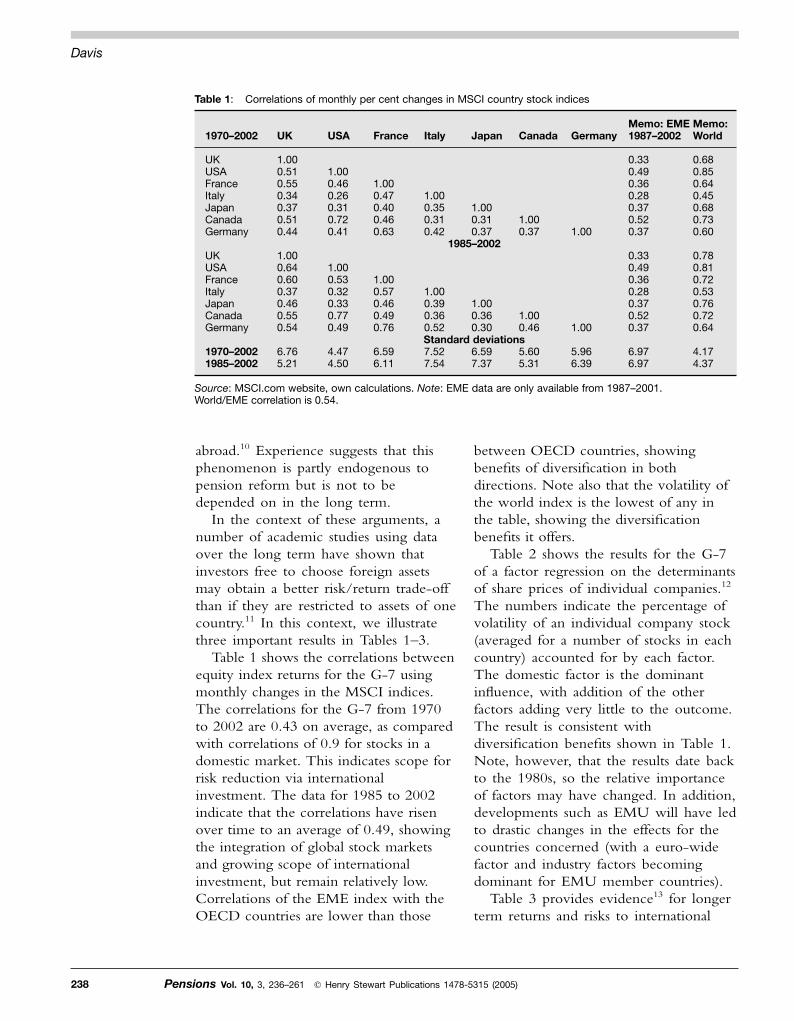

between OECD countries, showingbenefits of diversification in bothdirections. Note also that the volatility ofthe world index is the lowest of any inthe table, showing the diversificationbenefits it offers.

Table 2 shows the results for the G-7of a factor regression on the determinantsof share prices of individual companies.12

The numbers indicate the percentage ofvolatility of an individual company stock(averaged for a number of stocks in eachcountry) accounted for by each factor.The domestic factor is the dominantinfluence, with addition of the otherfactors adding very little to the outcome.The result is consistent withdiversification benefits shown in Table 1.Note, however, that the results date backto the 1980s, so the relative importanceof factors may have changed. In addition,developments such as EMU will have ledto drastic changes in the effects for thecountries concerned (with a euro-widefactor and industry factors becomingdominant for EMU member countries).

Table 3 provides evidence13 for longerterm returns and risks to international

abroad.10 Experience suggests that thisphenomenon is partly endogenous topension reform but is not to bedepended on in the long term.

In the context of these arguments, anumber of academic studies using dataover the long term have shown thatinvestors free to choose foreign assetsmay obtain a better risk/return trade-offthan if they are restricted to assets of onecountry.11 In this context, we illustratethree important results in Tables 1–3.

Table 1 shows the correlations betweenequity index returns for the G-7 usingmonthly changes in the MSCI indices.The correlations for the G-7 from 1970to 2002 are 0.43 on average, as comparedwith correlations of 0.9 for stocks in adomestic market. This indicates scope forrisk reduction via internationalinvestment. The data for 1985 to 2002indicate that the correlations have risenover time to an average of 0.49, showingthe integration of global stock marketsand growing scope of internationalinvestment, but remain relatively low.Correlations of the EME index with theOECD countries are lower than those

238 Pensions Vol. 10, 3, 236–261 � Henry Stewart Publications 1478-5315 (2005)

Davis

Table 1: Correlations of monthly per cent changes in MSCI country stock indices

Memo: EME Memo: 1970–2002 UK USA France Italy Japan Canada Germany 1987–2002 World

UK 1.00 0.33 0.68USA 0.51 1.00 0.49 0.85France 0.55 0.46 1.00 0.36 0.64Italy 0.34 0.26 0.47 1.00 0.28 0.45Japan 0.37 0.31 0.40 0.35 1.00 0.37 0.68Canada 0.51 0.72 0.46 0.31 0.31 1.00 0.52 0.73Germany 0.44 0.41 0.63 0.42 0.37 0.37 1.00 0.37 0.60

1985–2002UK 1.00 0.33 0.78USA 0.64 1.00 0.49 0.81France 0.60 0.53 1.00 0.36 0.72Italy 0.37 0.32 0.57 1.00 0.28 0.53Japan 0.46 0.33 0.46 0.39 1.00 0.37 0.76Canada 0.55 0.77 0.49 0.36 0.36 1.00 0.52 0.72Germany 0.54 0.49 0.76 0.52 0.30 0.46 1.00 0.37 0.64

Standard deviations1970–2002 6.76 4.47 6.59 7.52 6.59 5.60 5.96 6.97 4.171985–2002 5.21 4.50 6.11 7.54 7.37 5.31 6.39 6.97 4.37

Source: MSCI.com website, own calculations. Note: EME data are only available from 1987–2001. World/EME correlation is 0.54.

benefit (DB) funds, where there is aguarantee of returns by the sponsor. Hereoptimal investment may entail AssetLiability Management (ALM) whereinthe long-term balance between assets andliabilities is maintained by choice of aportfolio of assets with similar return, riskand duration characteristics to liabilities.There may also be shortfall riskconsiderations, where minimum-fundingregulations lead investors to maximise thereturn on the portfolio subject to aceiling on the probability of incurring aloss. Some funds may seek to avoid suchrisk via immunisation or matching ofassets and liabilities, but this may bedifficult or costly for funds whoseliabilities rise with wage inflation.

In this context, a significant number ofbenefits for pension funds arise frominternational investment. The mostimportant is the broadening of thefrontier of efficient portfolios as aconsequence of international investmentpossibilities. This means that for a mean-variance based investor such as a DCpension fund, a higher return is available

equity investment over the period 1921to 1996, using GDP to weight portfolioholdings. The results show that there is amajor reduction in risk; even theinclusion of markets that failed (ie ceasedto function entirely) does not greatlyreduce the global total return.

Benefits to pension funds

For all pension funds, a key aim ofinvestment is to match, or preferablyexceed, the growth of average labourearnings, given that this determines thereplacement rate at retirement, the keydeterminant of the liabilities of the fund.The traditional approach to investment isthe mean-variance approach based onrisk and return, first developed by Tobinand Markowitz. Optimal investmentinvolves the choice of a trade offbetween low risk and high return(chosen from the frontier of efficientportfolios), as appropriate for theinvestor’s preferences. This is relevant fordefined contribution (DC) pension funds.The case is more complex for defined

� Henry Stewart Publications 1478-5315 (2005) Vol. 10, 3, 236–261 Pensions 239

International investment — A global perspective

Table 2: Relative importance of factors in explaining return on a stock

Average R–squared of regression on factors

Single factor tests Joint test ofCountry World Industrial Currency Domestic all factors

UK 0.20 0.17 0.01 0.53 0.55USA 0.26 0.47 0.01 0.35 0.55France 0.13 0.08 0.01 0.45 0.60Italy 0.05 0.03 0.00 0.35 0.35Japan 0.09 0.16 0.01 0.26 0.33Canada 0.27 0.24 0.07 0.45 0.48Germany 0.08 0.10 0.00 0.41 0.42G-7 average 0.15 0.18 0.02 0.40 0.47

Source: Solnik and De Freitas cited in Bodie et al.12

Table 3: Returns on global stock indices, 1921–96

Index Real return (arithmetic) Standard deviation Real return (geometric)

USA 5.5 15.8 4.3Non-USA 3.8 10.0 3.4Global 5.0 12.1 4.3Survived markets 4.6 11.1 4.0

Source: Jorion and Goetzmann.13

In these cases a more precise match isprovided by domestic assets. To theextent that pensioners will seek to spendpart of their income on foreign goodsand services, the case for a degree ofinternational investment may remain, toan extent, dependent on the importshare in the consumption basket.

International investment benefitspension funds at a wider level. In smallcountries, such as the Netherlands andSingapore, the assets of pension fundsand other institutional investors mayexceed the entire domestic equitymarket, and hence simple liquidityconsiderations necessitate internationalinvestment, abstracting from risk/returnconsiderations, if regulations permit.Moreover, in emerging marketeconomies, pension funds may bevulnerable to banking crises as well asthe more general risks noted above,given that funded pension systems intheir early stages hold a certain amountof bank assets.15 International investmentavoids this and related ‘catastrophicrisks’.9

Reasons for ‘home asset preference’ ofpension funds

Given the force of these arguments, it isa puzzle that pension funds tend toinvest at least 60 per cent of their assetsin the home market, and in most, thefigure is over 90 per cent, see Table 4.Enormous differences in expected yieldswould be needed to account for suchportfolios in the context of the theory ofefficient markets.16 Reasons for this homeasset preference include the following.

Liabilities may play a role

The arguments above for sizeableexposure to international assets apply bestto a portfolio that is following amean-variance approach such as a DCpension fund, or an ongoing DB pension

for the same level of risk (when riskpreferences dictate high returns forimmature funds) or lower risk for thesame returns (when risk considerationsdictate low risk for mature funds). Givenrisk aversion falls with income andwealth, low income pensioners as inemerging market economies will beparticularly averse to avoidable risks toretirement income.

In terms of DB funds, similarconsiderations will for the most part beimportant. In an ALM approach, it canbe argued that international assets willtend to be part of a portfolio of assetswith similar return, risk and durationcharacteristics to pension liabilities, aslong as the fund is not winding down (iewith very short duration liabilities).Indeed, foreign assets may offer enhancedinflation protection, as the exchange ratedepreciates during periods of inflationwhen domestic asset returns are poor.

Where shortfall risk considerations areimportant for DB funds, it is anempirical question whether internationalassets offer greater downside risk thandomestic ones, but better diversificationand the exchange rate offset for inflationsuggests this would not be the case. Welldeveloped derivatives markets wouldallow protection. In this context, wenote that estimation14 of the frontier ofefficient portfolios based on historicalvariances and covariances of asset returnsshows minimum risk for a given returnto be at an exposure to foreign assets of20–30 per cent. Such calculations onlyshow average risks rather than extremevalues, however. Shortfall risk can arisefrom domestic as well as internationalinvestment, and such risk in the domesticeconomy may itself be relatively high inemerging market economies subject tohigh and volatile inflation.

Foreign assets may be avoided wherethe investment policy is merely toimmunise or match assets and liabilities.

240 Pensions Vol. 10, 3, 236–261 � Henry Stewart Publications 1478-5315 (2005)

Davis

are inefficient, for example showingbubbles, then global indexation bymarket capitalisation will not be anefficient strategy, as those who built upholdings of Japanese stocks in the late1980s and early 1990s discovered. Oratypically high returns on domesticbonds, as historically in Germany, mayencourage domestic investment.Consistent with the point made aboveabout the consumption basket,18 thereremains an optimal level of internationaldiversification in the presence ofinefficient global markets. This is basedon the ‘openness’ of the economy, andthus its exposure to output and inflationshocks. This suggests a higher level ofinternational investment than isappropriate for small open economies(both OECD and emerging markets)with high import/GDP ratios, than inrelatively closed economies such as theUSA, Japan and the Euro area.

Scepticism of purchasing power

A related point is that there is scepticismregarding purchasing power parity

fund with inflation-linked liabilitiesfollowing ALM considerations. For bothtypes of fund, maturity will make thefund less willing to accept the risk offoreign assets. Funds following shortfallrisk or immunisation strategies, or fundswith very short term liabilities (eg due towinding up), may wish to avoid foreignassets altogether.

A related point is that foreigninvestment will not overcome systemicrisks to world capital markets. Downsidemarket movements, notably in equitymarkets, occur much more in parallelthan do upside ones (as in the 1987crash).17 Pension funds that are adverse toshortfall risk (eg owing to minimumfunding requirements or low risktolerance of asset managers) will thereforebe cautious in assuming diversificationbenefits. Nevertheless, if such shocks aretruly systemic, they are not avoided bydomestic investment either.

Efficiency of global markets

The argument for the global portfolioassumes efficiency of markets. If markets

� Henry Stewart Publications 1478-5315 (2005) Vol. 10, 3, 236–261 Pensions 241

International investment — A global perspective

Table 4: Pension funds' portfolio composition 1998

Memo: Memo: Percent of Domestic Domestic Foreign pension assets/total Liquidity Loans bonds equities Property assets provision GDP

Australia 14 4 12 43 6 18 DC 42Canada 5 3 38 27 3 15 DB/DC 47Denmark 1 0 59 23 6 11 DC 22Germany 0 33 43 10 7 7 DB 15Japan 5 14 34 23 0 18 DB 17France 0 18 65 10 2 5 DB 7Italy 0 1 35 16 48 0 DC 2Netherlands 2 10 21 20 7 42 DB 116Sweden 0 0 64 20 8 8 DB/DC 49Finland 13 0 69 9 7 2 DB 8Switzerland 11 0 29 17 26 17 DC 111UK 4 0 14 52 3 18 DB/DC 87USA 4 1 21 53 0 11 DB/DC 72

Chile 15 17 44 21 3 4 DC 45Singapore 28 0 70 0 0 0 DC 60Malaysia 24 27 32 18 1 0 DC 51

Sources: National flow of funds balance sheets, Mercer, W. (1999) ‘European pension fund managers guide1999’, William M. Mercer, London. Chile: Palacios, R. and Pallares-Mirelles, M. (2000) ‘International patterns ofpension provision’, World Bank, Washington DC.; Singapore and Malaysia: Asher, M. (2000) ‘Socialsecurity reform imperatives; the South-East Asian case’, Working Paper, National University of Singapore.

Information

There are also issues of information andother costs. Better information on homemarkets may be a reason why investorschoose to concentrate their investmentsthere. Consistent with this, Table 5shows that UK pension funds obtainmuch lower returns in foreign markets,relative to passive benchmarks, than theydo in their home market (which begsthe question why do they not indexabroad?) Foreign investors in Japanconcentrate on larger stocks, which arebetter known.20 Prices of Mexican stocksdeclined more than closed-end fundstraded in the USA, suggesting thatinvestors in Mexico were betterinformed about fundamentals than thosein the USA.21 There will be sunk costsof setting up access to marketinformation, that institutions may choosenot to incur, as they cannot be recoveredwhen emerging from the market.Equally, higher transactions costs, linkedalso to clearance, settlement, and custody,may limit investment in foreign markets.UK pension funds also earned negativereturns from international market timing(ie switching between markets).22

Global corporate ownership

Home bias may to some extent bedriven by the structure of corporateownership around the world. Globalmarket portfolios based on outstanding

holding, even in the very long term.10

This can be justified by the existence oflong-term shifts in real exchange rates,which means currency mismatching caninvolve risk, especially for a mature fund.The issue will be of greater importance,the higher the share of non-traded goodsthat pensioners buy. Whereas short-termcurrency fluctuations can be hedgedagainst, the optimal degree of hedging ishighly uncertain.17

Equities, property an bonds

The arguments about globaldiversification may be considered toapply to different degrees in the casesof equities, property and bonds. Theyapply most precisely to equities,although one counter-argument is thatdiversification may be obtained byinvestment in the domestic market ifdomestic companies carry out foreigndirect investment. Bond markets aremore globally integrated, and hencethere is less benefit from diversificationout of domestic markets. Property is areal asset similar to equity, but is lessliquid and more reliant on imperfectlocal information. This makesinternational diversification moredifficult, although19 returns are for thatreason less internationally correlated,and hence, property company sharesoffer considerable diversificationbenefits.

242 Pensions Vol. 10, 3, 236–261 � Henry Stewart Publications 1478-5315 (2005)

Davis

Table 5: UK Pension Funds: Performance relative to benchmarks

1981–1998 1981–1989 1990–1998Standard Standard Standard

Percentage points Average deviation Average deviation Average deviation

USA –2.3 2.1 –3.7 2.0 –0.9 1.0Japan 0.3 7.5 –2.0 9.9 2.5 3.2Continental Europe –1.0 3.1 –1.8 4.0 –0.2 1.6World –1.6 6.0 –3.1 5.1 –0.2 6.7UK –0.4 0.7 –0.4 0.9 –0.3 0.6

Note: Before 1987, local indices for the USA and Japan, MSCI for Europe.After 1987, FT-A indices.Source: WM (1999) ‘WM UK pension fund annual review, 1998‘, The WM Company.

quantitative limit on holdings of a givenasset class. Typically, those instrumentswhose holdings are limited are thosewith high price volatility and/or lowliquidity, such as equities, real estate andforeign assets. Explicit allowance is bydefinition not made for potentiallyoffsetting correlations between types offinancial instrument. Such regulationsthereby override free choice ofinvestments. Meanwhile, a prudentperson rule stipulates that investmentsshould be made in such a way that theyare considered to be handled prudently(as someone would do in the conduct ofhis or her own affairs). The process ofmaking the investment is the key test ofprudence. The aim is to ensure adequatediversification, thus protecting thebeneficiaries against insolvency of thesponsor and investment risks.24 Theprudent person rule, in effect, allows thefree market to operate throughout theinvestment process.

For DB funds, solvency and minimumfunding rules and their interaction withassociated accounting arrangements mayalso play a crucial role in influencingportfolios, and may limit internationalinvestment independently of portfoliorestrictions. This is because theydetermine the size and volatility of thesurplus, as well as defining the rules fordealing with a corresponding deficit.They influence the likelihood and cost25

of any deficiency, and hence theimportance for pension funds ofmaintaining a stable valuation of assetsrelative to liabilities, independent ofportfolio limits. Minimum rates of returnset annually by regulation can constraindiversification even when quantitativelimits are not stringent (OECD 2000).They limit holdings of volatile assetswhich could reduce returns below thelimit in one year, even if they offer ahigh mean return. And application ofaccounting principles which insist on

shares may give a false impression ofthe proportion of shares that areactually tradeable, given that asignificant proportion may be firmlyheld in large stakes which control thecorporation in question. This isparticularly important outside the USAand the UK. This implies that anequilibrium degree of home bias maybe appropriate for US and UKinvestors (because foreign markets havelow free float) and elsewhere (becausecontrolling shareholders are usuallydomestic).23

A weaker justification for home assetpreference is that international investmentposes additional risk compared withdomestic investment— settlement,liquidity, transfer, and exchange rate risk.But settlement, liquidity, and transferrisks may be avoided by appropriatechoice of markets. Exchange rate risk canbe hedged,12 and, viewed in the contextof modern portfolio theory rather than inisolation, contributes to, rather thanoffsetting, the benefits of offshoreinvestment in terms of returns anddiversification of risk, notably forequities. In practice, foreign bonds areoften hedged while foreign equities arenot.

Foreign asset restrictions

Finally, home asset preference is widelyconsidered to be driven by foreign assetrestrictions in portfolio regulations. Giventhe importance of this issue the pros andcons of limiting international investmentare discussed separately below. Suffice tosay here that the main choice facing theauthorities is between so called prudentperson rules typically allowinginternational investment and quantitativeportfolio restrictions which usually limitit, although authorities may also vary thetightness of such portfolio restrictions. Tooffer brief definitions, a quantitativeportfolio regulation is simply a

� Henry Stewart Publications 1478-5315 (2005) Vol. 10, 3, 236–261 Pensions 243

International investment — A global perspective

risks. They are also total returns, withestimated capital gains and losses onbonds, equities and real estate beingadded to the yield. Foreign asset returnsare calculated by use of a simpleweighting scheme of nominal totalreturns to G-7 country equities andbonds, based on rough estimates ofworld capitalisation weights.28 Theseweighted returns are then derived indomestic currency in real terms bysubtracting the change in the nominaleffective exchange rate and the domesticinflation rate.

The line OECD average provides asummary for industrial countries. It isshown that the highest real returns aretypically from (domestic) equities,which also have the greatest volatility.Other high-return assets are propertyand foreign equities, followed by bondsand loans, and, finally, short-term assets.As regards standard deviations, Table 6verifies the proposition that the riskson foreign assets are generally lowerthan for domestic assets of the sametype because of the diversificationbenefits of foreign assets, which morethan offset exchange rate risk.Meanwhile, contrary to the expectationsof finance theory, the volatility patternis not entirely congruent with thepattern of real yields, with total returnson bonds showing a relatively highvolatility despite rather low real returns.This is partly linked to the fact that inthe 1970s, the real value of bonds fellsharply with high and volatile inflation,a pattern that was unique in historyand has been much less characteristicof the 1980s and 1990s.

Table 5 also shows inflation andgrowth in real average earnings. Thelatter, a key target of pension fundinvestment, has been an average of 2 percent for the countries shown. Inflationaveraged 6 per cent over the periodshown, although levels for individual

positive net worth of the fund at alltimes, carry equities on the balance sheetat the lower of book value and marketvalue26 and calculate returns net ofunrealised capital gains (as in Germanyuntil recently, and Switzerland) may alsorestrain international asset holdingsindependently of portfolio regulations.

International investment ofpension funds in practiceThis section, seeks to assess how theissues brought out above arise inpractice using data over 25 years forthe pension fund sectors of ten OECDcountries (Australia, Canada, Denmark,Germany, Japan, the Netherlands,Sweden, Switzerland, the UK and theUSA) and three emerging marketeconomies with long experience ofpension funds and pension fundinvestment (Chile, Singapore andMalaysia). These funded pensionsystems are mandatory in the cases ofAustralia, Denmark, Sweden,Switzerland and the three emergingmarket economies, and voluntaryelsewhere. These mandatory systems areall DC, while systems elsewhere areeither a mixture or purely DB. Inmost of the countries, pension fundsare sizeable, with assets amounting to50 per cent or more of GDP.Investment is by private managersexcept in Singapore, Malaysia and, untilrecently, Sweden.27

Asset return characteristics

Complementing the data alreadypresented, Table 6 illustrates the risk andreturn characteristics of internationalassets from 1970–1995, compared todomestic assets that are held by pensionfunds, to evaluate their potential role inpension fund investment. Note that theseare real returns and their corresponding

244 Pensions Vol. 10, 3, 236–261 � Henry Stewart Publications 1478-5315 (2005)

Davis

domestic assets between bonds andequities. The largest share of foreignassets is in the Netherlands (42 per cent),a small open economy with very largepension funds relative to the size of thedomestic financial markets. Note,however, that although many of thesecharacteristics are shared by theScandinavian countries, the holding offoreign assets is much lower (owing toportfolio restrictions on foreigninvestment). Shares of foreign assets areclose to 20 per cent in Australia, Canada,Japan, Switzerland and the UK, of whichJapan and the UK are medium-to largeeconomies while the others are againrelatively small. The USA, a large open

countries varied significantly. The limiteddata we have for the three emergingmarket economies shows that averageearnings growth considerably exceedsthat in OECD countries, in line witheconomic development, while Chileexperienced higher inflation over1980–1995.29 Returns on foreign assetsare comparable with those in OECDcountries.

Portfolios of pension funds

Patterns of portfolio shares in 1998 wereshown in Table 4. There are majorcontrasts in terms of the proportion offoreign assets, as well as the balance for

� Henry Stewart Publications 1478-5315 (2005) Vol. 10, 3, 236–261 Pensions 245

International investment — A global perspective

Table 6: Annual real asset returns and risks over 1967–1995

Average real Memo: Memo:return (and Short–term Domestic Domestic Real Foreign Foreign CPI Averagestandard deviation) assets Loans bonds shares estate equities bonds inflation earnings

Australia 1.8 4.8 –0.1 8.3 4.4 7.5 4.4 7.3 1.44.3 5.2 18.5 19.9 18.7 20.7 17.8 3.9 3.4

Canada 2.7 4.2 2.0 5.0 9.4 8.2 5.1 5.7 1.53.3 3.1 13.3 15.8 8.3 17.8 15.0 3.4 2.3

Denmark 2.3 6.6 4.4 5.9 5.2 2.1 7.1 2.62.8 3.5 19.1 25.6 21.4 17.7 3.5 3.4

France 2.9 3.3 2.5 7.7 4.3 6.9 3.8 6.3 2.93.4 3.3 15.8 18.4 14.5 17.2 14.5 4.2 2.4

Germany 3.1 6.8 3.9 10.8 10.9 5.5 2.4 3.5 3.02.1 2.0 15.7 23.8 11.5 21.4 17.4 1.9 2.8

Italy –0.3 4.3 –2.0 4.1 7.9 4.9 9.4 3.34.4 3.7 20.8 32.5 16.3 14.5 5.9 4.4

Japan –0.2 1.4 3.1 8.5 11.5 7.8 4.4 4.7 3.54.5 4.7 19.5 20.9 19.4 20.4 12.8 5.1 3.7

Netherlands 2.1 4.0 2.6 8.8 5.9 6.2 3.1 4.6 1.63.8 3.4 14.1 26.6 8.3 18.7 13.9 2.9 2.6

Sweden 2.1 4.4 1.4 14.1 10.3 7.7 4.6 7.7 1.53.9 3.8 16.3 31.4 27.1 17.6 15.4 3.0 3.5

Switzerland 1.3 2.8 0.0 7.8 1.7 5.3 2.2 3.9 1.72.0 2.0 18.7 22.8 9.1 19.9 15.9 2.4 2.0

UK 2.1 1.7 1.0 8.3 1.5 8.0 4.1 8.1 2.84.6 6.1 14.9 17.8 15.3 17.7 15.7 5.4 2.2

USA 2.0 3.8 1.2 2.0 5.6 8.5 5.5 5.5 –0.12.3 2.3 15.2 2.3 22.1 18.7 14.9 3.0 1.8

OECD 1.8 4.0 1.7 8.0 6.5 7.1 3.9 6.2 2.1Average 3.5 3.6 16.8 22.5 15.4 19.0 15.5 3.7 2.9

Chile 10.4 7.8 17.6 3.2(1980–95) 22.0 20.0 6.4 5.7Singapore 6.2 3.9 4.0 6.9

22.6 18.3 5.6 3.3Malaysia 7.9 5.6 4.5 4.4

21.5 17.0 3.6 2.9

Source: OECD, BIS.

(GSIC) and the Monetary Authority ofSingapore (MAS). The investment of theCPF is in non-tradable governmentbonds and liquid bank deposits with theMAS. The MAS then invests the assetsas foreign exchange reserves, and theGSIC in foreign equities. Moreover, inChile, bonds all tend to be indexed andthus offer inflation protection. Foreigninvestment in Chile rose sharply to 10per cent in 2000 following deregulation,to allow hedging of currency risk usingderivatives.

Portfolio regulations on pension funds

As background for interpreting theportfolio data, Table 7 illustrates thepattern of portfolio regulations in theOECD countries as well as in Chile,Singapore and Malaysia. Note that thisinformation is subject to change asregulations are amended and its accuracy

economy, has 11 per cent in foreignassets. Finally, there are a number ofcountries with very few foreign assets,including Denmark, Germany, France,Italy, Sweden and Finland.30 Thereappears to be no strong link from DB orDC to foreign investment, althoughthere is a slight tendency for moreinternational assets to be held in largelyDB-based systems.

In the emerging market economies,the stated level of foreign assets is verylow, despite the fact that they are smallopen economies where pension funds arevery large relative to the economy anddomestic financial markets. Note,however, that in Singapore, the fund isadministered by the governmentinvestment agency, the Central ProvidentFund (CPF), although the actualinvestment of the accumulated monies iscarried out by the Government ofSingapore Investment Corporation

246 Pensions Vol. 10, 3, 236–261 � Henry Stewart Publications 1478-5315 (2005)

Davis

Table 7: Foreign assets regulations for pension funds

General approach to Country investment regulation Foreign asset restrictions

Australia Prudent person rules (PPR) No currency matching limit but tax on income from foreign assets

Canada PPR No currency matching limit but foreign securities maximum of 30% of fund

Denmark Quantitative asset 80% currency matching limitrestrictions (QAR)

Finland PPR/QAR 80% currency matching limit, 5% in non-EEA countries, 20% in currencies other than the euros

Germany QAR 80% currency matching limit; 35% limit on EU equity, 10% on non-EU equity, 10% non-EU bonds

Italy PPR/QAR 67% currency matching limit. Non-OECD securities limit to 5%

Japan PPR None (Since 1998 only)Netherlands PPR NoneSweden QAR Currency matching required. Foreign assets limited to

5–10% of the fundSwitzerland QAR 30% limit on foreign assetsUnited Kingdom PPR NoneUnited States PPR None

Chile QAR 80% currency matching limitSingapore [PPR] Government invests assets at its discretion but holders

are ‘credited’ with returns equivalent to bank depositsMalaysia QAR 70% of assets in domestic government bonds

Note: PPR: prudent person rules, QAR: quantitative asset restrictions. Source: OECD (2004) ‘Survey of investment regulations of pension funds’, Financial Affairs Department,Organisation for Economic Co-operation and Development, Paris.

to 30 per cent and 33 per centrespectively.

In the emerging market economies,the limit in Chile is 20 per cent foreignassets, while in Malaysia, 70 per cent ofassets must be in domestic governmentbonds. As noted, Singapore is a hybrid inthat investments are carried out by thegovernment independently of the fundand its returns (the government ‘saves’the excess return over that on bankdeposits as a contingency reserve for the‘future of the country’).

Table 8 shows that there isconsiderable headroom relative to theforeign asset restrictions imposed bycountries on their pension funds. Themain exception is Sweden. Note that theinterpretation of headroom could be onthe one hand that there is no effect ofthe restrictions on normal business — oron the other that the existence of suchrestrictions may lead to very cautiousportfolio management to avoid everbreaching them even if markets soar.The distinction is hard to test; as notedabove, some home bias seems to occureven in the absence of regulation, dueinter alia to accounting and solvencylimits.

Potential and actual returns oninternational investment

This section seeks to address the degreeto which pension funds’ actual returns orpotential domestic returns could beimproved by more internationalinvestment. It uses a dataset for pensionfund portfolios and asset returns coveringthe period 1970–1995. This is asufficiently long and turbulent period tooffer some reasonably robust conclusions.First, the calculations provide, anestimate of actual real returns on pensionfunds, calculated by weighting eachportfolio share in each year by itsexpected return (as illustrated for a

cannot be guaranteed. In Japan, theNetherlands, UK and the USA, pensionfunds are subject to a ‘prudent personrule’. This is a relatively recentphenomenon in Japan, where regulationslimited international investment until1998. Australian funds are not subject toprudent person rules but taxationprovisions, which enable domesticdividend tax credits to be offset againstother tax liabilities, and are reportedly amajor disincentive to internationalinvestment.31 Canadian funds, despitehaving a prudent person rule, face limitson the share of external assets (but nottheir composition) as tax regulations limitforeign investment to 30 per cent of theportfolio. A tax of 1 per cent of excessforeign holdings was imposed for everymonth the limit is exceeded.

The other countries have quantitativerestrictions on foreign investment. Thishelps to explain the low levels of foreigninvestment there. For example, Germanfunds are subject to the 20 per centlimits on foreign investment imposed onlife insurers under the relevant EUDirectives, despite the different liabilitycomposition of pension funds to lifeinsurance. In Finland, this EU limit issupplemented by tighter limits oninvestment outside the Europeaneconomic area. Swedish funds are limitedto five to ten per cent foreigninvestment, and Swiss and Italian funds

� Henry Stewart Publications 1478-5315 (2005) Vol. 10, 3, 236–261 Pensions 247

International investment — A global perspective

Table 8: Headroom relative to portfolio restrictionson foreign assets

Per cent of portfolio

Canada 15Germany 13Finland 18Italy 33Sweden 2Switzerland 13

Chile 16Malaysia 30

Source for OECD countries: See Table 4.

smaller countries. Unfortunately,consistent data for domestic securityreturns back to 1970 were not availablefor the EMEs, so the focus is on thecomparison of the actual portfolio withthe global portfolio.

Following the discussion above, theresults are divided into those relevant tothe traditional mean-variance approach,to shortfall risk and to ALM. Beginningwith mean-variance, Table 9 shows thatfor the ten OECD countries, actualportfolios had a lower return than a50–50 domestic portfolio, and alsomarkedly lower risk. As noted, thiscautious asset allocation may link to riskpreferences but also to portfolio andother regulations. As regards internationaldiversification, this is shown to have littleeffect on return short of the full global

slightly longer period in Table 4) andsubtracting the inflation rate. Secondly, abenchmark is provided based on thereturns on a dummy portfolio of 50 percent domestic bonds and 50 per centdomestic equities (referred to as 50–50domestic). Compared to the actualreturns, this illustrates the influence ofregulations limiting domestic investmentin equities as well as risk preferences.Successive estimates of the effects ofdiversifying this portfolio (while retainingthe balance between equities and bonds),up to 20 per cent international and then40 per cent international, and finally afull global portfolio are provided. Notethat in the last case, there will only bedomestic assets for the G-7 countriesaccording to their global capitalisationweights and no domestic assets for the

248 Pensions Vol. 10, 3, 236–261 � Henry Stewart Publications 1478-5315 (2005)

Davis

Table 9: Mean variance 1: Estimated real returns and risks on pension funds' portfolios and on foreign assets (1970–95)

50–50 domestic Actual bonds andportfolios equities 20% foreign 40% foreign Global portfolio

Australia 1.8 3.5 4.0 4.6 6.111.4 17.5 16.5 16.1 18.2

Canada 4.8 4.0 4.6 5.3 7.110.0 12.1 11.7 11.8 14.7

Denmark 4.9 6.1 5.6 5.1 3.711.0 19.0 17.6 16.7 18.5

Germany 6.0 6.4 5.9 5.4 3.95.9 17.7 16.1 15.3 18.4

Japan 4.4 6.1 6.2 6.4 6.910.2 16.9 15.5 14.6 16.0

Netherlands 4.6 5.5 5.4 5.2 4.86.0 18.3 17.2 16.2 14.7

Sweden 2.1 8.0 7.6 7.3 6.313.2 20.1 17.7 15.8 14.8

Switzerland 1.8 2.4 2.6 2.9 3.77.7 18.1 16.9 16.2 17.0

UK 5.9 4.7 4.9 5.2 5.912.8 15.4 14.8 14.4 15.0

USA 4.5 4.4 5.0 5.6 7.511.8 13.3 12.8 12.8 15.2

OECD 4.4 6.3 6.3 6.3 6.6Average 9.6 15.7 14.7 14.1 15.3

Chile 13.0 9.1(1980–95) 9.5 19.1Singapore 1.3 5.1

5.4 18.4Malaysia 3.0 6.7

3.9 17.2

Source: Davis and Steil30, own calculations.

portfolios relative to actual portfolios andthe 50–50 domestic benchmark. The‘cleaner’ comparison is the latter,reflecting as it does the location of theassets and not differences in portfolios interms of instruments also. That said, it isclear than on average, OECD sectorscould gain a markedly higher return byholding a 50–50 portfolio, and the costin terms of risk is lowest for the 40 percent foreign portfolio. For all theportfolios based on a 50–50 bond-equitysplit, the internationally diversifiedportfolios on average dominate thepurely domestic one, with lower risk inall cases and (for the global portfolio)higher return. The corollary is that thesame risk could have generated a higherreturn (via a higher share of equities).

Table 11 gives a third approach to themean variance paradigm, by showing theSharpe ratios on the differing portfolios.The measure is defined as the real returnas a proportion of the standard deviation.It shows the reward to total volatilitytrade-off; mean variance preferences leadto a desire to maximise this measure.12

The actual portfolios have higher Sharperatios than those based on 50–50 bondsand equities. This is not solely theconsequence of more conservativeallocations, since it is also true for themore aggressive UK pension funds, aswell as those in Chile — but is not forAustralia and Sweden. It may reflectwider diversification into assets such asreal estate, liquidity and loans. There isstill a benefit from internationalinvestment, with Sharpe ratios beingmarkedly lower for the domestic 50–50portfolio. In Australia, Sweden and theUSA, the global portfolio has a higherShape ratio than the actual portfolio, butin Canada, Japan and Switzerland it isvirtually the same. For Chile andSingapore, Sharpe ratios are higher inactual than global portfolios, while this isnot the case for Malaysia.

portfolio, which offers 30 basis pointsmore than the rest. There are shown tobe benefits in terms of risk reduction upto 40 per cent foreign assets, while onaverage the global portfolio has a higherrisk than the less internationallydiversified ones. This is consistent withthe result14 quoted above. Thesesummary results do not apply to allcountries. The UK sector had a higheractual return than a 50–50 portfolio,reflecting high levels of equityinvestment, while the USA and Canadahad comparable returns, given pensionfund portfolios are typically close to thisportfolio benchmark. Elsewhere, due tohigher bond shares than 50 per cent,returns and risks have typically beenlower. Looking at comparable portfoliosin terms of instruments (50–50 bondsand equities), the differing returnsavailable in domestic financial marketsare apparent. In Switzerland such aportfolio would return only 2.4 per cent,while in Sweden it would offer 8 percent. Global portfolios minimise theseextremes. Benefits of internationalinvestment are low in Germany,reflecting the appreciation of thecurrency, but are correspondingly high inthe UK.

As regards the EMEs, the globalportfolio would return much more thanactual returns in Singapore and Malaysiaover the 1970–1995 period, at a cost ofhigher risk. In Chile, data for returns areonly available from 1980, reflecting thedate of introduction of the personalpension system. Returns there werehigher than the global portfolio over thesame period, and risks lower. Thisperiod, however, may have beenexceptional and indeed over 1996–1999,average returns of Chilean funds wereonly 5.8 per cent.32

Table 10 uses the data from Table 9 tooffer a comparison of the returns andrisks for internationally diversified

� Henry Stewart Publications 1478-5315 (2005) Vol. 10, 3, 236–261 Pensions 249

International investment — A global perspective

250 Pensions Vol. 10, 3, 236–261 � Henry Stewart Publications 1478-5315 (2005)

Davis

Table 10: Mean variance 2: Comparing pension fund real returns and risks with foreign asset benchmarks(1970–95)

Actual risk/return less: Domestic 50–50 less:20% 40% Global 20% 40% Global

50–50 foreign foreign portfolio foreign foreign portfolio

Australia –1.7 –2.2 –2.8 –4.3 –0.5 –1.0 –2.6–6.1 –5.1 –4.7 –6.8 1.0 1.4 –0.7

Canada 0.8 0.2 –0.5 –2.3 –0.6 –1.2 –3.1–2.1 –1.7 –1.8 –4.7 0.4 0.3 –2.6

Denmark –1.2 –0.7 –0.2 1.2 0.5 1.0 2.4–8.0 –6.6 –5.7 –7.5 1.5 2.3 0.5

Germany –0.4 0.1 0.6 2.1 0.5 1.0 2.5–11.8 –10.2 –9.4 –12.5 1.6 2.4 –0.7

Japan –1.6 –1.8 –2.0 –2.5 –0.2 –0.3 –0.9–6.7 –5.2 –4.4 –5.7 1.4 2.3 0.9

Netherlands –0.9 –0.8 –0.6 –0.2 0.2 0.3 0.8–12.3 –11.2 –10.2 –8.7 1.1 2.1 3.6

Sweden –5.8 –5.5 –5.2 –4.2 0.3 0.7 1.6–6.9 –4.5 –2.6 –1.6 2.4 4.3 5.3

Switzerland –0.6 –0.8 –1.1 –1.9 –0.3 –0.5 –1.3–10.4 –9.2 –8.5 –9.3 1.2 1.9 1.1

UK 1.2 1.0 0.7 0.0 –0.2 –0.5 –1.2–2.6 –2.0 –1.6 –2.1 0.6 1.0 0.5

USA 0.1 –0.5 –1.1 –3.0 –0.6 –1.3 –3.1–1.5 –1.0 –1.0 –3.5 0.5 0.5 –1.9

OECD –1.9 –1.8 –1.9 –2.2 0.0 0.0 –0.3Average –6.1 –5.1 –4.5 –5.7 1.0 1.6 0.4

Chile 3.9(1980–95) –9.5Singapore –3.7

–13.2Malaysia –3.8

–13.0

Source: Davis and Steil30, own calculations.

Table 11: Mean variance 3: Sharpe ratios (real return/standard deviation) (1970–95)

Actual Global portfolios 50–50 20% foreign 40% foreign portfolio

Australia 0.16 0.20 0.24 0.28 0.33Canada 0.48 0.33 0.40 0.45 0.48Denmark 0.44 0.32 0.32 0.31 0.20Germany 1.01 0.36 0.36 0.35 0.21Japan 0.43 0.36 0.40 0.44 0.43Netherlands 0.78 0.30 0.31 0.32 0.33Sweden 0.16 0.40 0.43 0.46 0.43Switzerland 0.23 0.13 0.15 0.18 0.22UK 0.46 0.30 0.33 0.36 0.39USA 0.38 0.33 0.39 0.44 0.49OECD average 0.45 0.30 0.34 0.36 0.35

Chile (1980–95) 1.37 0.5Singapore 0.78 0.39Malaysia 0.23 0.27

Source: Own calculations.

tends to increase in bear markets,reducing the seeming diversificationbenefits of international investment. Thispattern reflects common behaviour ofinstitutional investors (often repatriatingtheir holdings) as well as commonfundamentals across the world. Table14,33 illustrates these patterns in the bearmarkets of 1972 and 2001. For example,in 1972 the average correlation ofmonthly share price changes with thosein the world market was 0.53 while in1975 it was 0.69. This is not preciselymirrored in the country data, but ageneral tendency is apparent (the UScorrelation is high because it represents alarge share of the world market).Meanwhile in the recent period, whenglobal financial integration had in anycase ensured a much higher level ofcorrelations, the highest correlation isagain apparent late in the bear market in2001 and 2002, with all countries exceptJapan having correlations of 0.88 ormore. These are much higher than theaverage correlations shown in Table 1.

Table 15 shows a comparison ofpension fund returns with averageearnings growth, relevant for ALM.The figures in the table show the

Table 12 gives an indication of theshortfall risks to which sectors would beexposed in adopting the differentinvestment approaches. This is shownsimply by the lowest real return achievedduring the period 1970–1995. (In mostcases this was in 1973–1974, when theoil crisis led to high inflation andcollapses in securities prices.) Actualportfolios tended to be better protectedagainst such contingencies than thedummy 50–50 ones. Average worst-caseswithin the sample are �21 per cent forthe actual portfolios as opposed to �30per cent for the benchmark ones. Similarresults obtain for the EMEs. Of course,hedging could reduce the potential costsfrom such market falls. In Australia,Sweden and the UK, the worst case forthe actual portfolio is more adverse thanfor the constructed global portfolio. Notealso that in the Asian crisis, domesticstock markets in the affected countriesfell by 50 per cent or more, while theexchange rates also fell 50 per cent(Table 13). Ceteris paribus, foreign assetswould thus have risen in value, offsettinglosses on domestic stocks.

It was noted that the correlation ofdomestic share prices with world indices

� Henry Stewart Publications 1478-5315 (2005) Vol. 10, 3, 236–261 Pensions 251

International investment — A global perspective

Table 12: Shortfall risk: Comparing pension fund minimum real returns with those on diversified and global portfolios (1970–95)

Actual Global portfolios 50–50 20% foreign 40% foreign portfolio

Australia –33 –42 –40 –38 –31Canada –17 –21 –22 –23 –26Denmark –15 –29 –29 –28 –33Germany –9 –20 –19 –23 –34Japan –22 –31 –34 –37 –45Netherlands –10 –27 –26 –25 –29Sweden –36 –25 –22 –20 –23Switzerland –11 –28 –29 –30 –31UK –36 –46 –42 –38 –26USA –21 –22 –23 –24 –26OECD average –21 –29 –29 –29 –30

Chile (1980–95) –3 –22Singapore –11 –34Malaysia –16 –43

Source: Own calculations.

correlation with average earnings (toensure asset growth is in line withliabilities). In fact, portfolios arenegatively correlated with both. Forinflation, this means that high inflationleads to a low return on assets. It isnotable, however, that the globalportfolio suffers least from this problem,and the actual portfolios are much morevulnerable. As regards earnings, thecorrelation is close to zero, and is highestfor the actual portfolio. Interestingly, thedomestic 50–50 portfolio is lessnegatively correlated with earnings thanis the global portfolio.

We suggest that results presented inthis section are consistent with a nuancedview of the benefits of internationalinvestment. We find indeed that thereare higher risk adjusted returns whenportfolios are diversified internationally.On the other hand, shortfall risks arecomparable and although the headroomover average earnings is higher for aninternationally diversified portfolio, it is

headroom over average earningsavailable from the different investmentportfolios. On average, the headroom ismuch greater for the 50–50 portfoliosthan for the actual returns obtained.Indeed, in Australia, Sweden andSwitzerland, the returns are less than1 per cent above average earnings, aquantity which is easily absorbed bytransactions costs. Comparing theportfolios with different levels ofinternational investment, headroom ishigher for the global portfolio. In theEMEs, actual returns fall far short ofaverage earnings in Singapore andMalaysia — international investment ina global portfolio would have improvedthe situation considerably. This is notthe case in Chile, however.

Table 16 shows the correlationsbetween the real asset returns andaverage earnings and inflation. It isdesirable to have a zero correlation withinflation (so inflation does not affect realasset returns), and a strong positive

252 Pensions Vol. 10, 3, 236–261 � Henry Stewart Publications 1478-5315 (2005)

Davis

Table 13: Asset price changes in Asian markets, 1 July 1997 to 18 February 1998 (per cent)

Equity market US$ exchange rate

Indonesia –81.2 –73.5S Korea –32.3 –48.1Thailand –47.9 –43.2Malaysia –59.0 –33.2Singapore –45.0 –13.2Hong Kong –36.6 0

Table 14: Correlation of share prices with world indices in bear markets

Country UK USA Germany Japan Canada France Italy averages

1972 0.74 0.83 0.47 0.63 0.66 0.17 0.22 0.531973 0.64 0.96 0.51 0.65 0.88 0.45 0.03 0.591974 0.59 0.95 0.39 0.09 0.78 0.80 0.50 0.591975 0.72 0.96 0.51 0.72 0.72 0.50 0.69 0.69

1998 0.92 0.94 0.87 0.75 0.93 0.81 0.72 0.851999 0.71 0.97 0.88 0.61 0.85 0.86 0.54 0.772000 0.78 0.96 0.44 0.54 0.81 0.66 0.22 0.632001 0.96 0.98 0.95 0.72 0.89 0.95 0.90 0.912002 0.98 0.99 0.95 0.40 0.88 0.97 0.95 0.88

Source: MSCI

appropriate.34 First, there is the questionwhether such limits reduce risks, taking abroad view of the investment needs ofpension funds. Secondly, there is theissue whether, abstracting from risk, thereis a benefit to restricting internationalinvestment to stabilise themacroeconomy or develop the capitalmarket. The general case against portfolioregulations on international investmentare parallel to those against restrictionson portfolios more generally. Assummarised by European Commission,35

they are ‘in the way of optimisation ofthe asset allocation and security selectionprocess, and therefore may have led tosub-optimal return and risk taking’.Focusing on pension funds, foreign assetrestrictions have a number of adverseconsequences:

not the case that the correlation withaverage earnings is more favourable.

Policy issuesThis final section assesses some of thepolicy issues arising from internationalinvestment of pension funds. The focusis on two aspects: whether regulationsshould be set to limit internationalinvestment and; whether internationalinvestment can help protect againstfuture capital market turbulence as thepopulation ages in OECD countries.

Portfolio regulations bearing oninternational investment

Two main issues arise when deciding iflimits on international investment are

� Henry Stewart Publications 1478-5315 (2005) Vol. 10, 3, 236–261 Pensions 253

International investment — A global perspective

Table 15: Asset-Liability Management 1: Comparing pension fund real returns and global portfolio with realaverage earnings (1970–95)

Real average Actual Global earnings portfolios 50–50 20% foreign 40% foreign portfolio

Australia 1.0 0.8 2.5 3.0 3.5 5.13.4 8.0 14.1 13.1 12.7 14.8

Canada 1.3 3.5 2.7 3.3 3.9 5.82.4 7.6 9.7 9.3 9.4 12.3

Denmark 2.4 2.5 3.6 3.2 2.7 1.23.5 7.5 15.6 14.1 13.3 15.1

Germany 2.7 3.3 3.7 3.2 2.7 1.22.7 3.2 15.0 13.4 12.6 15.7

Japan 2.4 2.1 3.7 3.9 4.0 4.53.0 7.2 13.9 12.5 11.6 13.0

Netherlands 1.4 3.2 4.2 4.0 3.9 3.42.6 3.4 15.7 14.6 13.6 12.1

Sweden 1.4 0.8 6.6 6.3 5.9 5.03.5 9.7 16.6 14.2 12.3 11.3

Switzerland 1.5 0.2 0.8 1.1 1.3 2.12.1 5.6 16.0 14.8 14.1 14.9

UK 2.8 3.0 1.8 2.1 2.3 3.12.3 10.5 13.1 12.5 12.1 12.6

USA –0.2 4.8 4.6 5.3 5.9 7.81.9 9.9 11.4 10.9 10.9 13.4

OECD 1.7 2.7 4.6 4.5 4.6 4.9Average 2.7 6.9 13.0 12.0 11.4 12.6

Chile 3.2 9.8 5.9(1980–95) 5.7 3.8 13.4Singapore 6.9 –5.6 –1.8

3.3 2.1 15.1Malaysia 4.4 –1.4 2.3

2.9 1.0 14.3

Source: Davis and Steil30, own calculations.

For DC funds, it is hard to argue asound case for such rules, given thesuperior alternative of prudent personrules. They can even be said to exposebeneficiaries to currency risk, given thatbeneficiaries will want to spend some oftheir income on foreign goods andservices, and the domestic currency maydepreciate. There seems little evidencethat DC investors need ‘protecting fromthemselves’ ie prevent from taking highrisks by quantitative restrictions. Indeed,in practice, experience suggests that USinvestors in individual DC funds at leasthistorically tended to be too cautious todevelop adequate funds at retirement,while companies running DC funds mayinvest excessively cautiously to avoidlawsuits. A case could be made (as inChile37) that a danger with unrestrictedinvestments would be that firmsproviding pension contracts would seekto boost yield to attract clients, at a cost

In terms of risk and returnoptimisation, they are likely to enforceholdings of a portfolio below theefficient frontier, because they typicallyinsist on high proportions of bonds anddomestic assets. They focus unduly onthe risk and liquidity of individual assetsand fail to take into account the factthat, at the level of the portfolio, defaultrisk and price volatility can be reducedby diversification. They hence increaserisk for a given return by reducing theextent to which the diversificationbenefits of international investment maybe attained. For pension funds, thedegree to which such regulations actuallycontribute to benefit security is open todoubt. This relates to the link ofliabilities to average earnings growth (aswell as the vulnerability of liabilities toregulatory changes)36 besides the fact thatappropriate global diversification of assetscan eliminate idiosyncratic risk.

254 Pensions Vol. 10, 3, 236–261 � Henry Stewart Publications 1478-5315 (2005)

Davis

Table 16: Asset-Liability Management 2: Correlations of returns with inflation and average earnings

Actual Global portfolios 50–50 20% foreign 40% foreign portfolio

Australia Inflation –0.49 –0.44 –0.41 –0.37 –0.17Earnings –0.45 –0.40 –0.43 –0.46 –0.45

Canada Inflation –0.42 –0.39 –0.40 –0.38 –0.38Earnings –0.24 –0.27 –0.24 –0.19 –0.06

Denmark Inflation –0.29 –0.11 –0.13 –0.14 –0.14Earnings –0.37 –0.12 –0.19 –0.27 –0.43

Germany Inflation –0.17 –0.25 –0.21 –0.15 –0.15Earnings –0.16 –0.38 –0.45 –0.51 –0.51

Japan Inflation –0.62 –0.50 –0.54 –0.58 –0.58Earnings 0.04 0.05 0.04 0.02 –0.03

Netherlands Inflation –0.53 –0.40 –0.40 –0.40 –0.40Earnings 0.04 –0.07 –0.11 –0.16 –0.32

Sweden Inflation –0.33 0.02 –0.01 –0.06 –0.06Earnings –0.03 –0.17 –0.16 –0.15 –0.06

Switzerland Inflation –0.40 –0.29 –0.31 –0.32 –0.32Earnings –0.10 –0.24 –0.25 –0.25 –0.20

UK Inflation –0.49 –0.42 –0.44 –0.45 –0.45Earnings 0.14 0.07 0.09 0.10 0.14

USA Inflation –0.66 –0.64 –0.66 –0.65 –0.65Earnings 0.29 0.27 0.29 0.30 0.27

OECD Inflation –0.41 –0.33 –0.34 –0.34 –0.32Average Earnings –0.12 –0.15 –0.17 –0.18 –0.19

Chile Inflation 0.11 0.16Singapore Inflation –0.97 –0.20Malaysia Inflation –0.96 –0.55

Source: Own calculations.

restrictions which explicitly orimplicitly38 oblige pension funds to investin government bonds, which mustthemselves be repaid from taxation, theremay be no benefit to capital formationand the ‘funded’ plans may at amacroeconomic level be virtuallyequivalent to pay-as-you-go.

As previously noted, internationalinvestment will forestall the point atwhich pension fund investment becomesso large as to face diminishing returnsdomestically, so restrictions bring thispoint closer. Also there may be a benefitat a national level if national income issubject to frequent terms-of-trade shocksowing to the position of being largelydependent on commodities for exportearnings, while export earnings accountfor a large proportion of GDP, as iscommon in developing countries. Hence,holdings of assets offshore can actuallyhelp to contribute to greater stability ofnational income.39

Some additional points apply. Forexample, asset restrictions such as thoseon foreign assets are inflexible andtypically cannot be changed rapidly inresponse to changing conjuncturaleconomic circumstances and movementsin domestic or international securities,currency and real estate markets; theyalso may find it difficult to adapt tostructural changes in financial assetmarkets, such as EMU. If enforcedstrictly, they may give incentives to assetmanagers to hold proportions of riskyassets which fall well short of the limits,to avoid breaching them when marketsperform well and prices rise. Thiscompounds the loss of potential riskreduction for a given return. They maylimit tactical asset allocation — there isno incentive for the institutional investorto nominate investment managers withskills to achieve higher return and lowerrisk, by equity and internationalinvestment. Competition among asset

of excessive risk which could ultimatelybe borne by the government. But thesetendencies could also be dealt with by aprudent person rule.

Portfolio limits would also appear tobe inappropriate for DB pensions, giventhe ‘buffer’ of the company guarantee forthe beneficiaries and risk sharing betweenolder and younger workers, and ifbenefits must be indexed. Clearly, insuch cases, portfolio regulations mayaffect the cost to companies of providingpensions, if it constrains managers intheir choice of risk and return, forcingthem to hold low yielding assets, andpossibly increasing their risks and costsby limiting their possibilities ofdiversification. Indeed, restrictions onforeign assets may prevent appropriateaccount being taken of the duration ofthe liabilities (which may differ sharplybetween funds, as well as over time), andrelated changes in risk aversion. Theyalso render difficult or impossible theapplication of appropriate ALMtechniques for maturity matching,because such techniques may requiresharp variations in the portfolio betweendomestic and foreign equities to bonds,and use of derivatives. If portfolioregulations limit use of derivatives,abstracting from other operative limits,they will force the institution either tohold low-yielding assets or expose itselfto unnecessary risks, notably ininternational markets.

For all systems, restrictions encouragenational governments to treat pensionfunds as means to finance budgetaryrequirements (by enforcing high portfolioshares of government debt), in a waythat could not occur under a prudentperson rule where internationaldiversification is permitted. Holdings ofgovernment debt are vulnerable tomonetisation as government createsinflation to reduce its debt burden.Taking a broader view, in the case of

� Henry Stewart Publications 1478-5315 (2005) Vol. 10, 3, 236–261 Pensions 255

International investment — A global perspective

restrict international investment. This is acomplex, threefold issue: Do capitalmarkets contribute to economic growth?Do pensions contribute to capitalmarkets? And is this the case only ifforeign investment is restricted? Theevidence on the first point is fairly clear,both for capital markets and banks.41

There is some support for the link topension funds to capital marketdevelopment; most is based on Chileanexperience,42 although some work alsosuggests benefits for a range of EMEs43 aspension funds are seen to increase thesupply of long-term finance, financialinnovation, infrastructure modernisationand possibly increase household saving.On the other hand, besides requiringfixed costs of set-up, development ofpension and insurance industries, or evendomestic capital markets, may becontrary to the comparative advantage ofEMEs.9

Even if pension funds can aid growthof capital markets, openness to foreigninvestment may also achieve thisobjective. Assuming sound andtransparent economic policy, competitionand financial regulation, this would itselfbe encouraged by allowing internationalinvestment by domestic institutions,because it would give foreign investorsconfidence that the repatriation of theirportfolios will not itself be restricted infuture. Meanwhile, home bias even inthe absence of such restrictions wouldlead to ample inflows to domesticinstruments.44

There could be a rationale forportfolio regulations (albeit not minima)if fund managers as well as regulators arehighly inexperienced and the marketsvolatile and open to manipulation byinsiders. In a sense, they ensure portfoliodiversification in a rough and ready way,and avoid risk becoming excessive insuch cases. A corollary is that restrictionsmay justifiably be eased as expertise

managers is discouraged if their mainfunction is to meet quantitative assetrestrictions.

As was noted previously, the case forinternational diversification appliesparticularly strongly to emerging marketeconomies. Nevertheless, some possibleexceptions are often suggested to theargument for liberalisation, which alsoapply notably in emerging marketeconomies.

Some issues arise in the context ofcapital outflow controls in developingcountries. Exchange controls have in thepast been — justifiably — imposedduring foreign exchange crises to dealwith capital flight, to avoid a sharp andcostly overshooting of the currency, butoften kept in looser form once normalconditions were re-established.39 It wouldbe feasible40 to gain the diversificationbenefits of international investmentwithout risk of capital flight by use ofappropriate swap contracts. Foreign assetrestriction can ease the fiscal cost ofmoving from a pay-as-you-go to afunded scheme. For example in Chile,pension fund development facilitatedinternal resource transfers, enabling theChilean government to service itsinternational debts without extreme fiscaladjustment which was damagingelsewhere to the real economy, byproviding a domestic source ofborrowing without requiring excessivelyhigh interest rates (in fact, the debt wasgenerally CPI-indexed).39 Later, thedemand of pension funds enabled debtconversion — by both private and publicinstitutions — to occur smoothly. Heargues that the process would have beenless smooth if international investmenthad been permitted.

Some would also argue thatrestrictions are needed to boostdevelopment of domestic capital marketsand hence growth. Most Latin Americancountries with recent pension reforms

256 Pensions Vol. 10, 3, 236–261 � Henry Stewart Publications 1478-5315 (2005)

Davis

be a shift within demand for securitiesfrom equity to bond-related instrumentsbecause of the growing maturity ofpension schemes, and the increaseddemand for annuities per se wouldnecessitate holding of shorter durationassets.

Such flows arising from funding willnot be purely domestic, to the extentthat ageing occurs at different rates indifferent countries. Net flows will arisefrom balance of payments surpluses incountries which are ageing mostrapidly, offset by deficits in slowerageing countries,48 although such flowscould arise via banking flows orforeign direct investment (FDI) as wellas pension portfolio flows. Reflectingdesire for diversification, and subject toportfolio regulations, it seems likelythat there will be much greater grosscapital flows between OECD countriesand from OECD to EME countriesduring this phase, in the form of bondand equity finance. These are likely toexceed considerably the amplitude ofnet flows (ie arising fromsaving-investment imbalances andconsequent balance of paymentsdisequilibria).49

Experience suggests that a large shareof OECD pension saving directed toEMEs can lead to bubbles and financialstability risks in the latter owing toinstitutional behaviour. This supports theneed for pension funds in EMEs toinvest globally rather than solelyconcentrating on the home market.Owing, for example, to autonomousshocks affecting profitability andcreditworthiness, there may be periodicflights of investable funds back to theOECD or to other EMEs. Securities arein principle much easier to repatriatethan bank loans. Indeed, behaviour ofOECD institutional investors is alreadywidely considered to destabilise EMEs,not least owing to their tendency to

develops, and such arguments do notsupport international investmentrestrictions. This point applies moregenerally where regulators have initialdoubts about internal controls ininstitutions, as well as about theindustry’s capacity for self-regulation andrelated governance structures. Moreover,compliance with portfolio limits is morereadily verified and monitored bysupervisors than for prudent person rules.The latter requires a high degree oftransparency of institutions, and strictsupervisory controls on investormalpractice (such as occurred in theMaxwell case45) as well as onself-regulatory bodies. But even if thisargument is accepted, rules should beeased or switched to prudent persononce experience is gained. On balance,we consider the liberal approach to bebest both for OECD countries andEMEs.

Some longer term risks

Before concluding, it is important toassess what will happen to asset returnswhen global ageing takes place incoming decades.46 Will internationalinvestment help? Various predictions canbe made.

During the transition phase as theworking population ages whileaccumulating for retirement, there willbe considerable demand for securities,notably in the form of equities (whereregulations permit) and bonds. This willbe enhanced as more countries currentlydependent on pay-as-you-go switchrelatively to funding (as witness recentsteps by Germany and Italy). Given thecontrasting portfolios of institutionalinvestors and households, and theevidence of a lack of offsetting shifts inportfolios when institutional investmentincreases,47 relative demand for deposits islikely to decline. Over time, there will

� Henry Stewart Publications 1478-5315 (2005) Vol. 10, 3, 236–261 Pensions 257

International investment — A global perspective

rate could rise to historic peaks onlypreviously seen in the early 1980s. Thesetentative results suggest a severe downturnis possible, thus underlining the potentialmarket risks associated with sole relianceon fully funded pension schemes.

There could nevertheless be offsettingfactors. Even if there were to be netdecumulation of securities by OECDinvestors, global demand will also dependon the degree to which rapidlydeveloping countries, eg in the Far Eastor Latin America, experience slowerdemographic ageing and thus provide acountervailing factor in the context ofglobalised financial markets. Note,however, that maintaining global demandfor securities would require them not onlyto substitute for capital inflows fromOECD countries, but also to generatesubstantial surpluses to cover declines indemand for securities in OECD countriesthemselves. The more EMEs that fundpensions, and the more rapid theireconomic development, the more likelythis is. The increase and subsequentdecrease in savings flows will be balancedby rises and falls in equity issues, withlittle effect on prices and returns.55 Alsothe increase in the ratio of pensioners toworkers is already underway, and willcontinue steadily rather than abruptly,again casting doubt on the idea of a cycle.Or at least, the market will take on boardsuch gradual future shifts without majorand abrupt adjustments in prices.Furthermore, OECD countries are ageingat different rates and there may beoffsetting demands for securities fromEMEs.

Despite these counter arguments to the‘baby bust’, we suggest that there aregrounds for caution as a consequence ofthese projected patterns, whichinternational investment alone cannotresolve, as it is a systematic risk to theglobal portfolio. They clearly justify aretention of some element of

invest in EMEs as a bloc rather thanfocusing closely on individual countries’fundamentals.50

Looking further ahead, when anincreasing proportion of the populationretires in the rapidly ageing OECDcountries and begins to live on theaccumulated assets, domestic demand forsecurities in OECD countries could fallsharply, which could entail withdrawal offinancing from EMEs. Decumulation isan ineluctable process for DB pensionfunds,51 and suggest that they will ceaseto contribute to US net saving around2024. They note, however, that thiseffect is unlikely to occur for DC fundsin the foreseeable future. Given the needto finance annuities, demand for equitieswould fall more than demand forbonds.52 Poterba53 focuses on extantinformation on age-specific asset holdings(excluding DB pension funds), correctedfor cohort effects to evaluate this issue.He concludes that asset demands mayindeed rise as households age, and notesthat surveys suggest that there is adecline in risk tolerance at ages over 65,but suggests that there is less evidence ofa downturn in asset holdings at the endof the life cycle. He thus considers that asharp fall in demand for securities isunlikely to arise in coming decades.54

Econometric evidence46 shows thatdemographics have had a significantimpact on US, panel and aggregatedOECD stock prices and bond yields from1950–1999, even in the presence ofstandard additional independent variables.The results show that the size of the40–64 age cohort has a strong importantpositive influence on asset prices, asupport that would be removed as itsshare of the population declines, whilemore tentatively the 65� cohort has anegative effect. Projections suggest thatthe equity price is set to come underdownward pressure, other things equal,from 2015 onwards, while the real interest

258 Pensions Vol. 10, 3, 236–261 � Henry Stewart Publications 1478-5315 (2005)

Davis

author thanks Mukul Asher and Dennison Noel fortheir assistance.

2 See Davis, E. P. and Steil, B. (2001) ‘InstitutionalInvestors’, MIT Press, Cambridge, MA. This paperdraws on this work throughout.

3 See Solnik, B. (1988) ‘International Investments’,Addison Wesley, Reading, MA, and Solnik, B. (1998)‘Global asset management’, Journal of PortfolioManagement, Summer 1998, pp. 43–51.

4 Baxter, M. and Jermann, U. J. (1997) ‘Theinternational diversification puzzle is worse than youthink’, American Economic Review, Vol. 87, pp.170–180, go further and suggest that since humancapital is non-diversifiable and labour income growthand domestic capital market returns are stronglycorrelated, it is optimal to sell short domesticsecurities and hold wealth in a portfolio of foreignassets.

5 This will be of particular importance to DB pensionfunds in which liabilities are tied to wages and hencerise as the profit share falls. Similarly, at an individualfirm level, investment in competitors’ shares hedgesagainst a loss of profits due to partial loss of thedomestic market.

6 As discussed, there remains an issue whether commonageing of OECD countries will render thisdiversification benefit ineffective.

7 Blake, D. (1997) ‘Pension funds and capital markets’,Discussion Paper No PI-9706, The Pensions Institute,Birkbeck College, London.

8 Technically, these results imply inefficiency and/orslow adjustment of global capital markets.

9 Kotlikoff, L. J. (1998) ‘The right approach to pensionreform’, Paper presented at the Asian DevelopmentBank conference on Pension Reform, Manila,December 1998.

10 Reisen, H. (1997) ‘Liberalizing foreign investmentsby pension funds: Positive and normative aspects’World Development, Vol. 25, No. 1, pp. 1173–82.

11 See, for example Meric, I. and Meric, G. (1989)‘Potential gains from international portfoliodiversification and intertemporal stability andseasonally in international stock market relationships’,Journal of Banking and Finance, Vol. 13, Nos. 4–5, pp.627–40.

12 Drawn from Solnik, B. and De Freitas, A. (1988)‘International factors of stock price behaviour’, inKhoury, S. and Ghosh, S. (eds) ‘RecentDevelopments in International Finance and Banking’,Lexington Books, Lexington. Cited in Bodie, Z.,Kane, A. and Marcus, A. J. (1999) ‘Investments’, 4thed, McGraw Hill, Boston, MA.

13 Jorion, P. and Goetzmann, W. N. (1999) ‘Globalstock markets in the twentieth century’, Journal ofFinance, Vol. 54, pp. 953– 980.

14 Greenwood, J. G. (1993) ‘Portfolio investment inAsian and Pacific economies: Trends and prospects’,Asian Development Review, Vol. 11, No. 1, pp.120–150.

15 Mitchell, O. S. (1997) ‘Building an environment forpension reform in developing countries’, in Bodie, Z.and Davis, E. P. (eds), ‘Foundations of Pension

pay-as-you-go as a form of insuranceagainst a future crisis in global capitalmarkets. It is evident that internationalinvestment will still be beneficial inreducing the risks from ageing ascompared to purely domestic investment,given that countries will age at differentrates in the coming decades. And indeed,in many countries balance of paymentssurpluses due to ageing will makeliberalisation of international investmentessential. EMEs should develop domesticpension fund sectors also as a bulwarkagainst eventual withdrawal of OECDfunds.

ConclusionsData confirm the theory that internationalinvestment allows superior investmentperformance in terms of risk and return.Pension funds are well placed to takeadvantage of the benefits of internationalinvestment — to an extent that dependson the maturity of the fund and theinvestment approach. There are sizeabledifferences in international investment bythe pension fund sectors in the countriesstudied. Whereas some degree of homebias is likely to occur naturally, it isundesirable for regulations to enforcetighter limits on foreign assets than thesemarket forces would suggest. Thearguments favouring such restrictions areweak. The future of funding itself seemslikely to be turbulent given the growingscope of asset flows and the futuredecumulation when ageing accelerates inOECD countries. These developments donot negate the case for internationalinvestment, but they do suggest a need toretain elements of a pay-as-you-gosystem, as a form of insurance.

References1 An earlier version of this paper was presented at the

Senior Level Policy Seminar, Caribbean Centre forMonetary Studies, Trinidad, 3rd May, 2002. The

� Henry Stewart Publications 1478-5315 (2005) Vol. 10, 3, 236–261 Pensions 259

International investment — A global perspective

of pension fund assets’, in Blommestein, H. andFunke, N. (eds) ‘Institutional Investors in the NewFinancial Landscape’, OECD, Paris.

28 A cross-check with the MSCI world equity indexrevealed similar risks and returns.

29 In the 1970s there was a hyperinflation, whichcontributed to the demise of the pay-as-you-gosystem.

30 It may be added that earlier data (in Davis and Steil2001) shows that even for some of the sectorsshown to have substantial assets, this is a relativelyrecent phenomenon. In 1970, the data suggest thatonly the Netherlands (7 per cent) and the UK (2per cent) had substantial foreign assets at all, due inmost cases to exchange controls as well as specificregulations on pension funds.

31 Bateman, H. and Piggott, J. (1993) ‘Australia’smandated retirement income scheme: An economicperspective’, Retirement Income Perspectives. Twopapers prepared for the office of EPAC, July.

32 Palacios, R. and Pallares-Mirelles, M. (2000)‘International Patterns of Pension Provision’, WorldBank, Washington DC.

33 Davis, E. P. (2003) ‘Comparing bear markets, 1973and 2000’, National Institute Economic Review, Vol.183, pp. 78–89.

34 Davis, E. P. (1998) ‘Policy and implementation issuesin reforming pension systems’, Working Paper No.31, European Bank for Reconstruction andDevelopment, London.