pennsylvania tax amnesty program by: r. nicholas nanovic

TRANSCRIPT

Pennsylvania Tax Pennsylvania Tax Amnesty ProgramAmnesty Program

By: R. Nicholas NanovicBy: R. Nicholas Nanovic

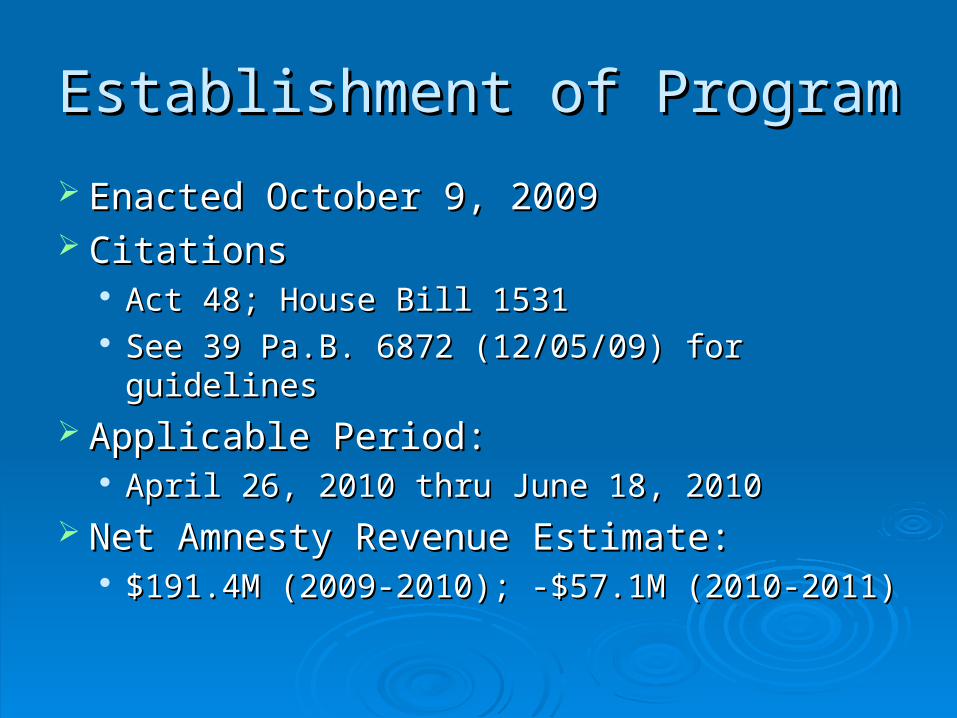

Establishment of ProgramEstablishment of Program

Enacted October 9, 2009Enacted October 9, 2009 CitationsCitations

Act 48; House Bill 1531Act 48; House Bill 1531 See 39 Pa.B. 6872 (12/05/09) for guidelinesSee 39 Pa.B. 6872 (12/05/09) for guidelines

Applicable Period:Applicable Period: April 26, 2010 thru June 18, 2010April 26, 2010 thru June 18, 2010

Net Amnesty Revenue Estimate:Net Amnesty Revenue Estimate: $191.4M (2009-2010); -$57.1M (2010-2011)$191.4M (2009-2010); -$57.1M (2010-2011)

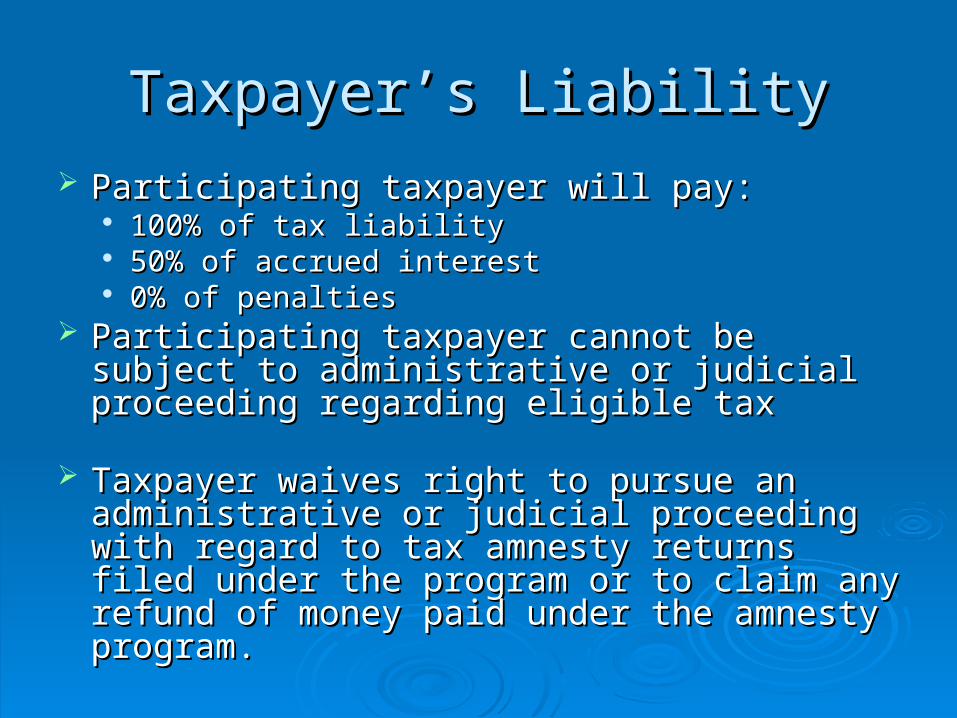

Taxpayer’s LiabilityTaxpayer’s Liability Participating taxpayer will pay:Participating taxpayer will pay:

100% of tax liability100% of tax liability 50% of accrued interest50% of accrued interest 0% of penalties0% of penalties

Participating taxpayer cannot be subject to Participating taxpayer cannot be subject to administrative or judicial proceeding regarding administrative or judicial proceeding regarding eligible taxeligible tax

Taxpayer waives right to pursue an Taxpayer waives right to pursue an administrative or judicial proceeding with regard administrative or judicial proceeding with regard to tax amnesty returns filed under the program to tax amnesty returns filed under the program or to claim any refund of money paid under the or to claim any refund of money paid under the amnesty program.amnesty program.

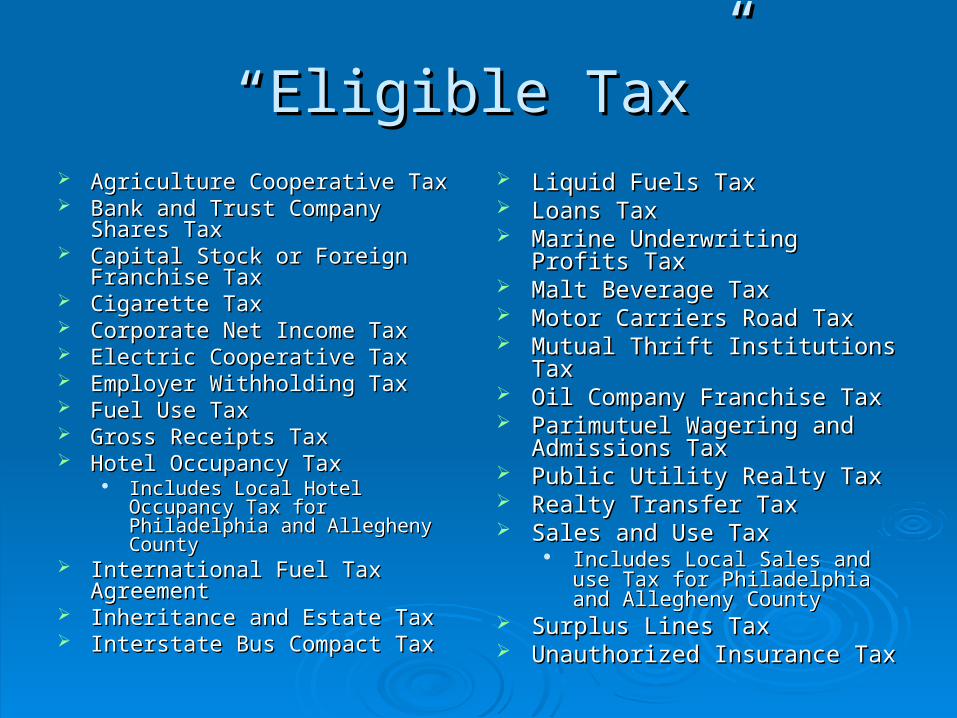

““Eligible Tax”Eligible Tax” Agriculture Cooperative TaxAgriculture Cooperative Tax Bank and Trust Company Shares Bank and Trust Company Shares

TaxTax Capital Stock or Foreign Franchise Capital Stock or Foreign Franchise

TaxTax Cigarette TaxCigarette Tax Corporate Net Income TaxCorporate Net Income Tax Electric Cooperative TaxElectric Cooperative Tax Employer Withholding TaxEmployer Withholding Tax Fuel Use TaxFuel Use Tax Gross Receipts TaxGross Receipts Tax Hotel Occupancy TaxHotel Occupancy Tax

Includes Local Hotel Occupancy Includes Local Hotel Occupancy Tax for Philadelphia and Tax for Philadelphia and Allegheny CountyAllegheny County

International Fuel Tax AgreementInternational Fuel Tax Agreement Inheritance and Estate TaxInheritance and Estate Tax Interstate Bus Compact TaxInterstate Bus Compact Tax

Liquid Fuels TaxLiquid Fuels Tax Loans TaxLoans Tax Marine Underwriting Profits TaxMarine Underwriting Profits Tax Malt Beverage TaxMalt Beverage Tax Motor Carriers Road TaxMotor Carriers Road Tax Mutual Thrift Institutions TaxMutual Thrift Institutions Tax Oil Company Franchise TaxOil Company Franchise Tax Parimutuel Wagering and Parimutuel Wagering and

Admissions TaxAdmissions Tax Public Utility Realty TaxPublic Utility Realty Tax Realty Transfer TaxRealty Transfer Tax Sales and Use TaxSales and Use Tax

Includes Local Sales and use Tax Includes Local Sales and use Tax for Philadelphia and Allegheny for Philadelphia and Allegheny CountyCounty

Surplus Lines TaxSurplus Lines Tax Unauthorized Insurance TaxUnauthorized Insurance Tax

““Eligible Tax”Eligible Tax”

Tax liability must be due as of June 30, Tax liability must be due as of June 30, 20092009

Exception:Exception: Unknown liabilities due prior to July 1, 2004Unknown liabilities due prior to July 1, 2004

““Unknown Liability”Unknown Liability”

An unknown liability is a liability for an An unknown liability is a liability for an eligible tax for which either:eligible tax for which either: No return or report has been filed, no No return or report has been filed, no

payment has been made, and the taxpayer payment has been made, and the taxpayer has not been contacted by the Department has not been contacted by the Department concerning the unfiled returns or reports or concerning the unfiled returns or reports or unpaid tax, orunpaid tax, or

A return or report has been filed, the tax was A return or report has been filed, the tax was underreported, and the taxpayer has not been underreported, and the taxpayer has not been contacted by the Department concerning the contacted by the Department concerning the underreported taxunderreported tax

Eligible TaxpayersEligible Taxpayers

PersonPerson AssociationAssociation FiduciaryFiduciary PartnershipPartnership CorporationCorporation Other entity required to pay or collect any Other entity required to pay or collect any

eligible taxeligible tax

Ineligible TaxpayerIneligible Taxpayer

Taxpayer that has received notice prior to April Taxpayer that has received notice prior to April 26, 2010 that taxpayer is under criminal 26, 2010 that taxpayer is under criminal investigation for an alleged violation of any law investigation for an alleged violation of any law imposing an eligible tax;imposing an eligible tax;

Taxpayer named as defendant in a criminal Taxpayer named as defendant in a criminal complaint prior to April 26, 2010, alleging a complaint prior to April 26, 2010, alleging a violation of any law imposing an eligible tax; orviolation of any law imposing an eligible tax; or

Taxpayer currently a defendant in a criminal Taxpayer currently a defendant in a criminal action for an alleged violation of any law action for an alleged violation of any law imposing an eligible taximposing an eligible tax

Taxpayer RequirementsTaxpayer Requirements

File an online Amnesty Return with the File an online Amnesty Return with the DepartmentDepartment

Make payment of all taxes and one-half the Make payment of all taxes and one-half the interest due to the Commonwealthinterest due to the Commonwealth

File complete tax returns for all required tax File complete tax returns for all required tax periods for which the taxpayer previously has periods for which the taxpayer previously has not filed a returnnot filed a return

File complete amended returns for all required File complete amended returns for all required periods for which the taxpayer underreported tax periods for which the taxpayer underreported tax liabilityliability

Example 1Example 1

Martha does not file a tax return for 2006. Martha does not file a tax return for 2006. Martha’s tax return would have shown a liability Martha’s tax return would have shown a liability of $5,000. Martha has never been contacted by of $5,000. Martha has never been contacted by the Department regarding the liability.the Department regarding the liability.

Martha may participate in the amnesty program Martha may participate in the amnesty program by filing an amnesty return and her 2006 income by filing an amnesty return and her 2006 income tax return. Martha will pay $5,000 plus one-half tax return. Martha will pay $5,000 plus one-half of the accrued interest.of the accrued interest.

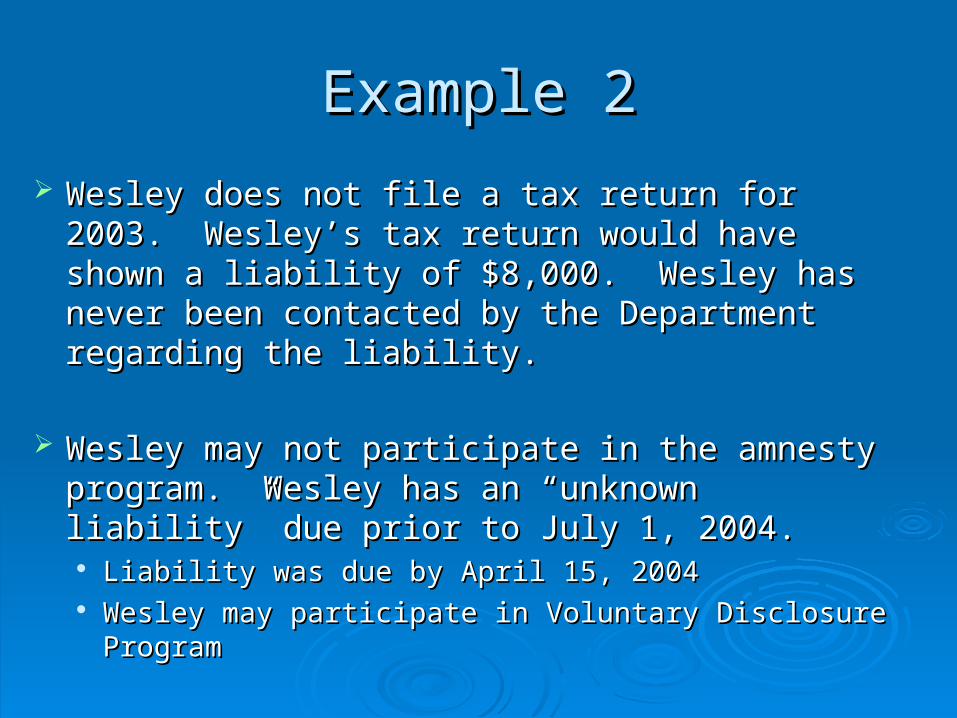

Example 2Example 2

Wesley does not file a tax return for 2003. Wesley does not file a tax return for 2003. Wesley’s tax return would have shown a liability of Wesley’s tax return would have shown a liability of $8,000. Wesley has never been contacted by the $8,000. Wesley has never been contacted by the Department regarding the liability.Department regarding the liability.

Wesley may not participate in the amnesty Wesley may not participate in the amnesty program. Wesley has an “unknown liability” due program. Wesley has an “unknown liability” due prior to July 1, 2004.prior to July 1, 2004. Liability was due by April 15, 2004Liability was due by April 15, 2004 Wesley may participate in Voluntary Disclosure ProgramWesley may participate in Voluntary Disclosure Program

Forgiveness of unknown liabilitiesForgiveness of unknown liabilities

Taxpayer that, pursuant to amnesty Taxpayer that, pursuant to amnesty program, reports and pays unknown program, reports and pays unknown liabilities due as of July 1, 2004 or later is liabilities due as of July 1, 2004 or later is not liable for taxes of the same type due not liable for taxes of the same type due prior to July 1, 2004prior to July 1, 2004 Taxpayer must comply with all other Taxpayer must comply with all other

requirements of amnesty programrequirements of amnesty program

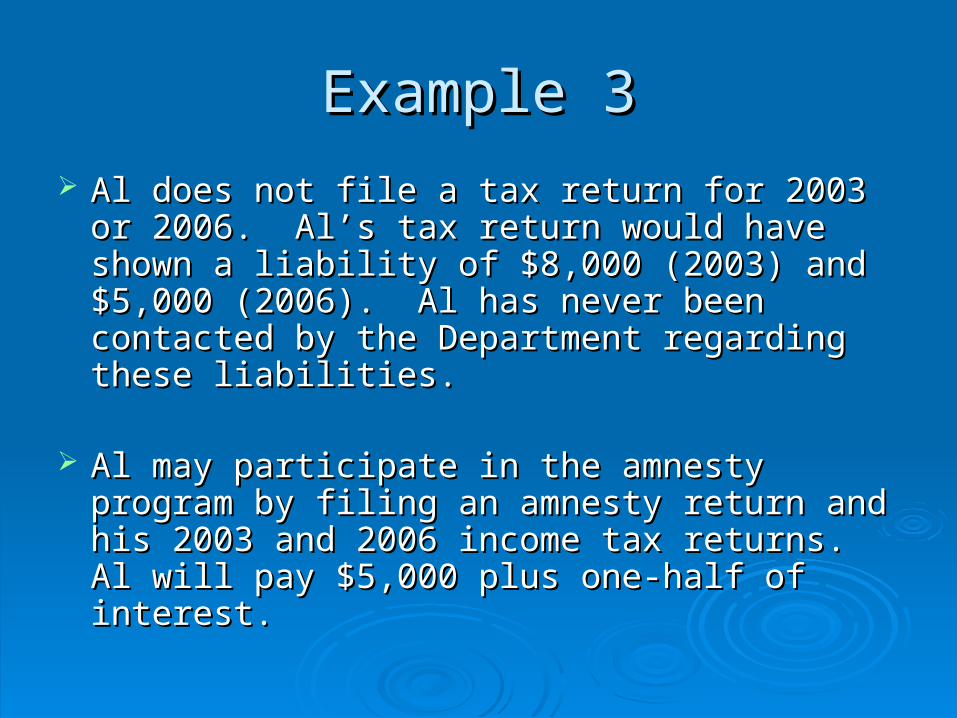

Example 3Example 3

Al does not file a tax return for 2003 or 2006. Al does not file a tax return for 2003 or 2006. Al’s tax return would have shown a liability of Al’s tax return would have shown a liability of $8,000 (2003) and $5,000 (2006). Al has never $8,000 (2003) and $5,000 (2006). Al has never been contacted by the Department regarding been contacted by the Department regarding these liabilities.these liabilities.

Al may participate in the amnesty program by Al may participate in the amnesty program by filing an amnesty return and his 2003 and 2006 filing an amnesty return and his 2003 and 2006 income tax returns. Al will pay $5,000 plus one-income tax returns. Al will pay $5,000 plus one-half of interest.half of interest.

NoticeNotice

Department will send written notice to last Department will send written notice to last known address of each tax delinquent.known address of each tax delinquent. Delinquencies for multiple tax types = multiple Delinquencies for multiple tax types = multiple

noticesnotices

No notification for unknown liabilitiesNo notification for unknown liabilities

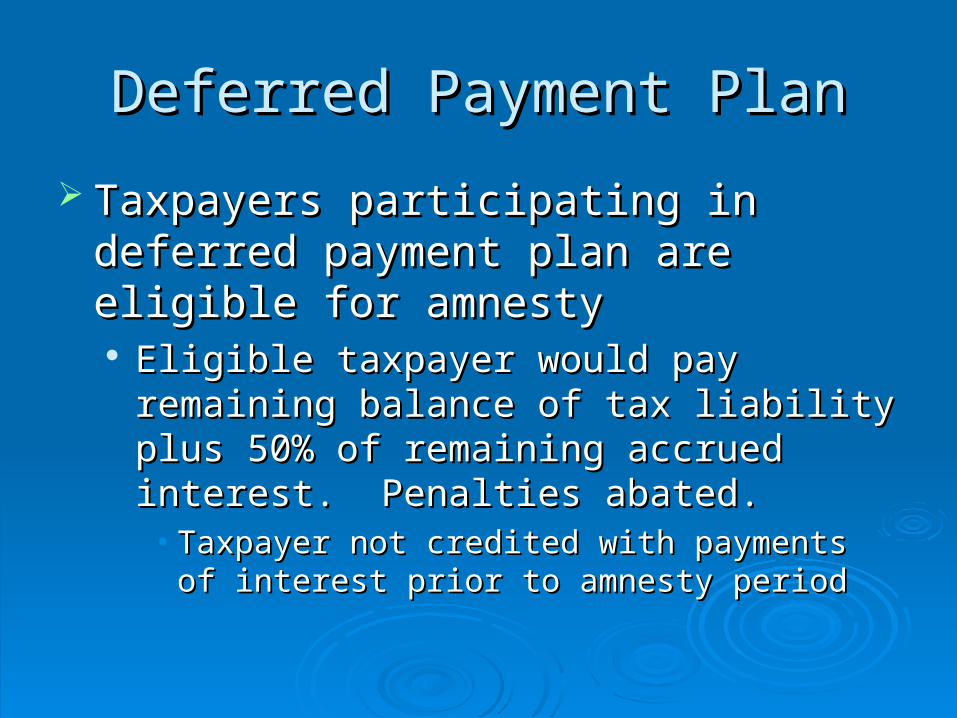

Deferred Payment PlanDeferred Payment Plan

Taxpayers participating in deferred Taxpayers participating in deferred payment plan are eligible for amnestypayment plan are eligible for amnesty Eligible taxpayer would pay remaining Eligible taxpayer would pay remaining

balance of tax liability plus 50% of remaining balance of tax liability plus 50% of remaining accrued interest. Penalties abated.accrued interest. Penalties abated.• Taxpayer not credited with payments of interest Taxpayer not credited with payments of interest

prior to amnesty periodprior to amnesty period

Example 4Example 4

Richard owes $22,000 for tax liability for Richard owes $22,000 for tax liability for 2004, 2005, and 2006. On January 1, 2009, 2004, 2005, and 2006. On January 1, 2009, Richard agreed to pay monthly installments. Richard agreed to pay monthly installments. On April 26, 2010, Richard liable for $7,000 On April 26, 2010, Richard liable for $7,000 of taxes plus penalties and interest.of taxes plus penalties and interest.

Richard is eligible for tax amnesty program. Richard is eligible for tax amnesty program. Richard would pay $7,000 plus one-half of Richard would pay $7,000 plus one-half of unpaid accrued interest. No credit for unpaid accrued interest. No credit for interest and penalties paid on $15,000.interest and penalties paid on $15,000.

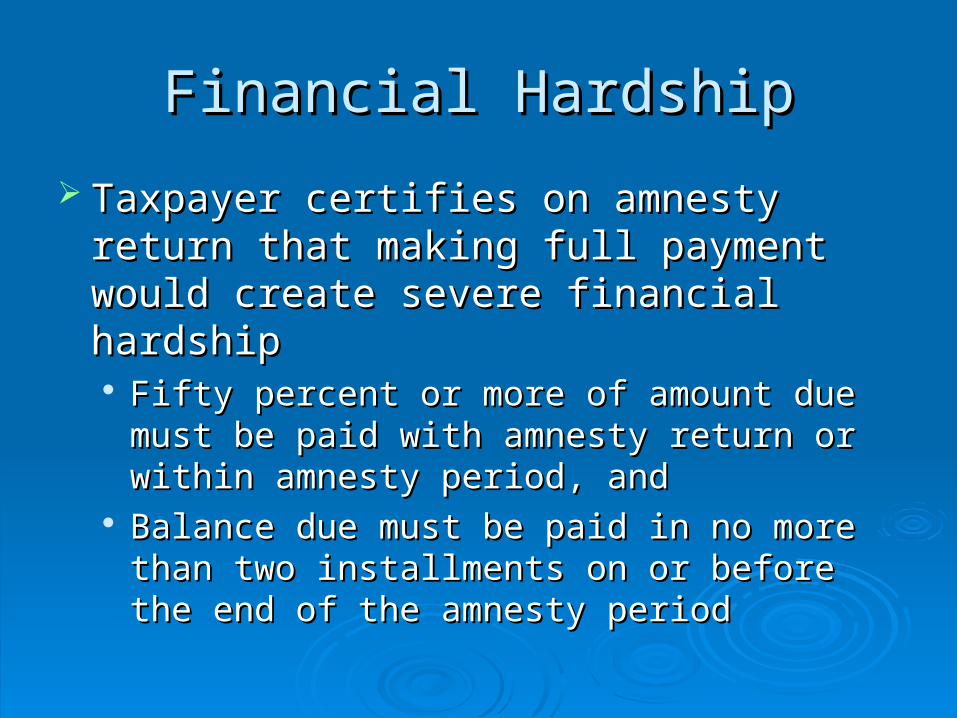

Financial HardshipFinancial Hardship

Taxpayer certifies on amnesty return that Taxpayer certifies on amnesty return that making full payment would create severe making full payment would create severe financial hardshipfinancial hardship Fifty percent or more of amount due must be Fifty percent or more of amount due must be

paid with amnesty return or within amnesty paid with amnesty return or within amnesty period, andperiod, and

Balance due must be paid in no more than Balance due must be paid in no more than two installments on or before the end of the two installments on or before the end of the amnesty periodamnesty period

Future AmnestyFuture Amnesty

Taxpayer waives eligibility for any future Taxpayer waives eligibility for any future amnesty program.amnesty program.

Continued ComplianceContinued Compliance

Department may assess and collect waived Department may assess and collect waived penalties and interest if, within two years penalties and interest if, within two years after the end of the program, either event after the end of the program, either event occurs:occurs: Taxpayer becomes delinquent for 3+ Taxpayer becomes delinquent for 3+

consecutive periods in payment of taxes or consecutive periods in payment of taxes or filing of returns on semi-monthly, monthly, filing of returns on semi-monthly, monthly, quarterly, or other basisquarterly, or other basis

Taxpayer becomes delinquent and is 8+ Taxpayer becomes delinquent and is 8+ months late in payment of taxes due or filing of months late in payment of taxes due or filing of returns on an annual basisreturns on an annual basis

Deficiency AssessmentDeficiency Assessment

If Department issues deficiency If Department issues deficiency assessment with respect to a tax amnesty assessment with respect to a tax amnesty return, the Department has authority to return, the Department has authority to impose penalties and pursue criminal impose penalties and pursue criminal action with respect to difference between action with respect to difference between amount reported on amnesty return and amount reported on amnesty return and current amount of tax.current amount of tax.

Undisclosed LiabilitiesUndisclosed Liabilities

Department is allowed to pursue civil or Department is allowed to pursue civil or criminal proceedings against any taxpayer criminal proceedings against any taxpayer for:for: Any tax not disclosed on tax amnesty returnAny tax not disclosed on tax amnesty return Any amount disclosed on tax amnesty return Any amount disclosed on tax amnesty return

but not paidbut not paid

Penalty for Non-paymentPenalty for Non-payment

Taxpayer penalized 5% of amount of Taxpayer penalized 5% of amount of unpaid tax liability and penalties and unpaid tax liability and penalties and interest if:interest if: Taxpayer had failed to remit eligible tax dueTaxpayer had failed to remit eligible tax due Taxpayer had an unreported or underreported Taxpayer had an unreported or underreported

liability for an eligible tax on or after the day liability for an eligible tax on or after the day after the end of the amnesty program.after the end of the amnesty program.

Voluntary Disclosure ProgramVoluntary Disclosure Program ApplicationApplication

Contact Voluntary Disclosure Office to obtain a Contact Voluntary Disclosure Office to obtain a case numbercase number

Provide information to Department regarding:Provide information to Department regarding:• Types of tax dueTypes of tax due• Dates that tax liabilities beganDates that tax liabilities began• Detailed description of Pennsylvania activitiesDetailed description of Pennsylvania activities• Explanation of failure to file and pay taxesExplanation of failure to file and pay taxes• Verify that taxpayer not previously contacted by Verify that taxpayer not previously contacted by

DepartmentDepartment• Complete Business Activities Questionnaire (DAS-77)Complete Business Activities Questionnaire (DAS-77)

Voluntary Disclosure ProgramVoluntary Disclosure Program

Taxpayers owing non-corporate taxTaxpayers owing non-corporate tax Pay tax liability and interest for current year plus three Pay tax liability and interest for current year plus three

previous years; all penalties waivedprevious years; all penalties waived Additional years’ liabilities will be forgivenAdditional years’ liabilities will be forgiven

Taxpayers owing corporate taxTaxpayers owing corporate tax Pay tax liability and interest for current year plus five Pay tax liability and interest for current year plus five

previous years; all penalties waivedprevious years; all penalties waived Additional years’ liabilities will be forgivenAdditional years’ liabilities will be forgiven Registered taxpayers ineligibleRegistered taxpayers ineligible

Amnesty > Voluntary DisclosureAmnesty > Voluntary Disclosure

Formal procedureFormal procedure Waive 50% of interestWaive 50% of interest Unknown and known liabilitiesUnknown and known liabilities

Any Questions?Any Questions?