pearson chaaron - legislative news, studies and analysis

TRANSCRIPT

pewtrusts.org/taxincentives

Tax Incentive Evaluation

NCSL Legislative Fiscal Directors Post-Conference 2017

Chaaron PearsonSenior Manager, The Pew Charitable Trusts

pewtrusts.org/taxincentives

pewtrusts.org/taxincentives

Why evaluate tax incentives

Tax incentives are one of states’ primary economic development tools

Tax incentives collectively cost states billions of dollars per year

Evaluation is a proven way to improve the effectiveness of incentives

Evaluations can lead to a more constructive conversation about incentives

pewtrusts.org/taxincentives

Year evaluation laws were adopted in states that are “leading” or “making progress”

Pre-2014

2014

2015

2016

WA

OR

IA

MO

LA

FL

AK

TX

OK

NE

NDMN

MS

TN

IN

ME

NH

RI

CT

MD

DC

WI

AL

VACO

OHHI

UT

pewtrusts.org/taxincentives

Three steps to effective evaluation

Step 1: Make a plan

Step 2: Measure the impact

Step 3: Inform policy choices

pewtrusts.org/taxincentives

State tax incentive evaluation ratings

pewtrusts.org/taxincentives

Make a plan: Who evaluates in states that are “leading” or “making progress”

CO

WA

OR

IA

MO

LA

FL

AK

TX

OK

NE

NDMN

MS

TN

IN

ME

NH

RI

CT

MD

DC

WI

AL

VA

Executive branch agency

Independent agency

Legislative staff

Legislators themselves

Outside experts

OHHI

UT

pewtrusts.org/taxincentives

Make a plan: Developing a strategic schedule

Include all major incentives

Use a rotating multi-year cycle

Study incentives with similar goals in the same year

Coordinate evaluations with sunset dates

pewtrusts.org/taxincentives

Measure the impact: High-quality evaluations include…

A description of the incentive, its history, and goals

An assessment of the incentive’s design and administration

An estimate of the incentive’s economic and fiscal impact

Policy recommendations

pewtrusts.org/taxincentives

Evaluation example: Indiana

pewtrusts.org/taxincentives

Evaluation example: Alabama

pewtrusts.org/taxincentives

Evaluation example: Minnesota

pewtrusts.org/taxincentives

Options to inform policy choices

Create new legislative committees

Utilize existing committee structure

Require the governor to make recommendations after evaluations

Establish expiration dates on incentives to encourage review

pewtrusts.org/taxincentives

With evaluations, states can…

Make subtle changes to incentives to increase their return on investment

Identify programs that are working well, so that the state can invest in them with confidence

Repeal or replace ineffective or obsolete incentives

Maine Legislature’s On-going Review of Tax Expenditures

Beth Ashcroft, DirectorOffice of Program Evaluation and Government Accountability

Purpose of Formal, On-going Review Process

To ensure that:

tax expenditures are reviewed regularly according to a

strategic schedule organized so that tax expenditures

with similar goals are reviewed at the same time;

reviews are rigorous in collecting and assessing relevant

data, determining benefits and costs, and drawing clear

conclusions based on measurable goals; and

reviews inform policy choices and the policymaking

process.

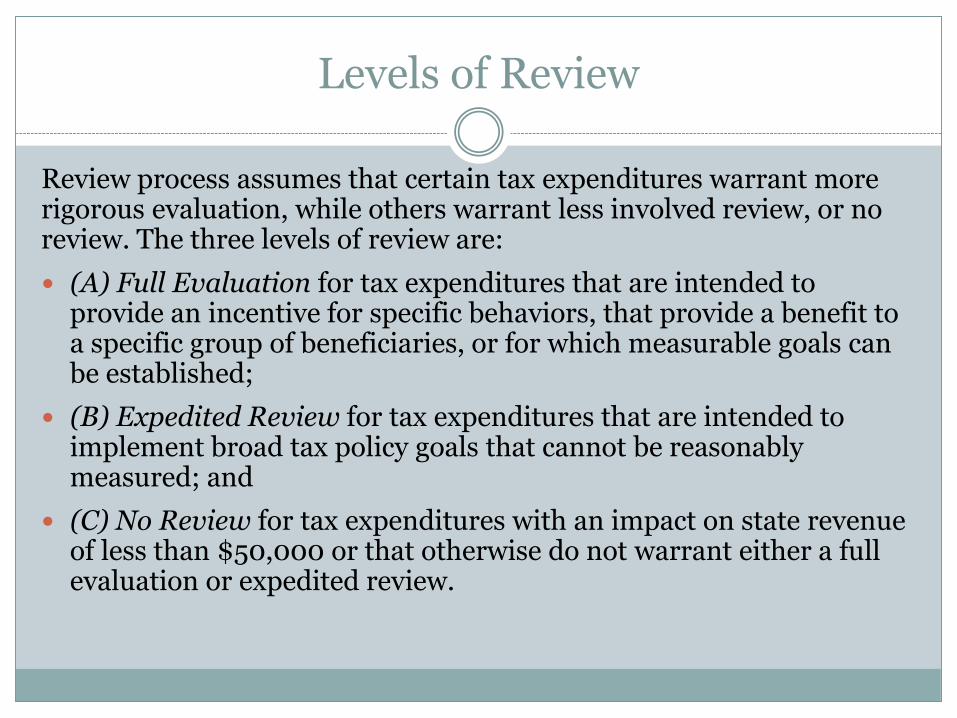

Levels of Review

Review process assumes that certain tax expenditures warrant more rigorous evaluation, while others warrant less involved review, or no review. The three levels of review are:

(A) Full Evaluation for tax expenditures that are intended to provide an incentive for specific behaviors, that provide a benefit to a specific group of beneficiaries, or for which measurable goals can be established;

(B) Expedited Review for tax expenditures that are intended to implement broad tax policy goals that cannot be reasonably measured; and

(C) No Review for tax expenditures with an impact on state revenue of less than $50,000 or that otherwise do not warrant either a full evaluation or expedited review.

Full Evaluation Objectives

The extent to which those actually benefiting from the tax expenditure are the intended beneficiaries;

The fiscal impact of the tax expenditure, including past and estimated future impacts;

The extent to which the design of the tax expenditure is effective in accomplishing its purposes, intent or goals and is consistent with best practices;

The extent to which the tax expenditure is achieving its purposes, intent or goals;

The extent to which the desired behavior might have occurred without the tax expenditure;

The extent to which there are other tax expenditures, state spending or other government programs that have the same purposes, intent or goals as the tax expenditure and whether those additional programs are appropriately coordinated with the tax expenditure and are complementary or duplicative;

Any opportunities to improve the effectiveness of the tax expenditure in meeting its purposes, intent or goals; and

The extent to which the tax expenditure is a cost-effective use of resources compared to other options for using the same resources or addressing the same purposes, intent or goals.

Expenditures by Review Level and Rationale

Rationale

Review Category*

A B C Total

Business Incentive 13 5 18

Non-Business Incentive 7 11 18

Tax Relief 8 2 10

Charitable 33 43 76

Conformity with IRC 2 2

Tax Fairness 14 7 21

Necessity of Life 13 13

Interstate or Foreign Commerce 13 2 15

Inputs to Tangible Products 7 3 10

Specific Policy Goal/Mandate 2 5 7

Non-Taxable Services 2 2

Administrative Burden 1 3 4

Total 31 84 81 196

*Review Category – (A) Full Evaluation, (B) Expedited Review, (C) No Review

Initial Review Schedule – 6 Year Cycle

FULL EVALUATIONS EXPEDITED REVIEWS

Year Count Rationale Count Rationale

2016 4 ➢ Business Incentive• Job Creation

13 ➢ Necessity of Life

2017 5 ➢ Business Incentive• Equipment Investment• Research Investment

14 ➢ Tax Fairness

2018 4 ➢ Business Incentive• Financial Investment• Targeted Industry Support

14 ➢ Charitable• Elderly• Government• Veterans• Other

2019 5 ➢ Business Incentive• Targeted Industry Support

➢ Specific Policy Goal/Mandate ➢ Administrative Burden

19 ➢ Charitable• Education• Health & Safety• Low Income• Youth• Other

2020 6 ➢ Non-Business Incentive• Education• Financial Investment• Health and Safety

13 ➢ Interstate/Foreign Commerce

2021 7 ➢ Targeted Tax Relief• Individuals• Industry

11 ➢ Inputs to Tangible Products➢ Conformity with IRC➢ Non-Taxable Services

Schedule Challenges and Changes

Statutory deadlines for Committee approvals on evaluation parameters and for issuing evaluation reports did not provide enough flexibility in scheduling, completion and reporting and did not fit well with legislative schedules.

A six year cycle with a certain number of evaluations to be completed each year was not realistic for what comprehensive evaluations require and OPEGA’s capacity for conducting multiple evaluations in any given time period.

Schedule Challenges and Changes

Tax expenditure programs still grouped by Rationale but scheduled for full evaluation by group rather than by year. Committee sets the schedule according to the priority for each group and adjusts priorities annually as needed.

OPEGA commits to having at least two evaluations “in progress” at any given time, with one of the evaluations being given priority until it is complete. Once the priority project is complete, the other “in progress” project becomes the top priority and OPEGA begins evaluation of the next program in the current group – or moves to a program in the next group as appropriate.

GOC continues to approve Evaluation Parameters prior to OPEGA beginning an evaluation of any program. However, these would be presented to the GOC for consideration as a new evaluation is beginning rather than by a particular date each year.

OPEGA presents each report to the Committee at the time the evaluation is completed. By July 1st of each year, the Committee transmits the reports on evaluations completed in the past year to the Taxation Committee for consideration of recommendations.

Georgia:

Administrative Data

Challenges

NCSL/Pew Tax Incentive Evaluation, Boston 2017

Laura Wheeler, Senior Research Associate

Center for State and Local Finance/

Fiscal Research Center

Georgia State University

Administrative Data Challenges

▪ Gaining access

• It’s about relationship and trust.

• Do your administrative and technical systems play

well with others?

▪ Using administrative data is

• Messy

• Typically too large for Excel or Access

• Usually not well documented

• May not be easily linked to other data sources

• May require geocoding

• Not designed for evaluation purposes

NCSL/Pew Tax Incentive Evaluation, Boston 2017

Administrative Data Challenges

▪ Reporting results

• Nondisclosure concerns

• Can the data be made available to others?

• Allow the data’s home department to join the

review process

▪ Protecting administrative data

• Who can see the data?

• Where can it be used? If offsite, how is it

transferred to another location?

• Once offsite, how is it protected and accessed?

• After project ends, how is the data treated?

NCSL/Pew Tax Incentive Evaluation, Fall 2017

pewtrusts.org/taxincentives

Chaaron PearsonSenior Manager, The Pew

Charitable Trusts

Questions?

Beth AshcroftDirector, Maine Office of Program

Evaluation and Government Accountability

Laura WheelerSenior Research Associate,

Georgia State University

Fiscal Research Center